Comprehensive Analysis of Management Accounting Systems and Methods

VerifiedAdded on 2022/01/20

|44

|12222

|84

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its definition, origin, roles, principles, and systems. It explains the core functions of management accounting, including formulating financial strategies, explaining the financial consequences of decisions, monitoring expenses, and maintaining profitability. The report also explores different management accounting systems such as inventory management, cost accounting, job costing, and price optimization systems. Furthermore, it contrasts financial and management accounting, highlighting their key differences. Finally, the report discusses the importance of relevant, reliable, accurate, and timely information, as well as the need for understandable presentation in management accounting reporting. The report emphasizes the critical role of management accounting in providing internal financial reports and aiding managers' decision-making processes to achieve business goals.

Management Accounting

LO1. Demonstrate an understanding of management accounting

systems.

rAHMEE 1

LO1. Demonstrate an understanding of management accounting

systems.

rAHMEE 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

P1. Explain management accounting and give the essential requirement of

different types of management accounting systems.

Management Accounting

Management accounting, also called managerial accounting or cost accounting, is the process

of analyzing business costs and operations to prepare internal financial report, records, and

account to aid managers’ decision-making process in achieving business goals. In other words,

it is the act of making sense of financial and costing data and translating that data into useful

information for management and officers within an organization.

Origin

Managerial accounting has its roots in the industrial revolution of the 19th century. During this

early period, most firms were tightly controlled by a few owner-managers who borrowed based

on personal relationships and their personal assets.

Since there were no external shareholders and little unsecured debt, there was little need for

elaborate financial reports. In contrast, managerial accounting was relatively sophisticated and

provided the essential information needed to manage the early large-scale production of textile,

steel, and other products. After the turn of the century, financial accounting requirements

burgeoned because of new pressures placed on companies by capital markets, creditors,

regulatory bodies, and federal taxation of income. Johnson and Kaplan state that “many firms

needed to raise funds from increasingly widespread and detached suppliers of capital. To tap

these vast reservoirs of outside capital, firms’ managers had to supply audited financial reports.

And because outside suppliers of capital relied on audited financial statements, independent

accountants had a keen interest in establishing well defined procedures for corporate financial

reporting. The inventory costing procedure adopted by public accountants after the turn of the

century had a profound effect on management accounting. As a consequence, for many

decades, management accountants increasingly focused their efforts on ensuring that financial

accounting requirements were met and financial reports were released on time.

Roles

Formulate Financial Strategies

Management accountants can formulate financial strategies using sales forecasts, budgets and

job-costing techniques, among other managerial accounting tools. They also can incorporate

data from a company’s financial statements to develop strategies that enhance gross income,

net profit and earnings per share. Whether it’s formulating a plan to purchase capital equipment

or reduce operating costs to ensure the continued viability of a business, management

accountants serve a vital role in formulating effective financial strategies.

Explain Financial Consequences of Decisions

If senior leaders adjust their company’s capital structure, management accountants can explain

the ramifications of adding additional debt or equity financing. This is true of other decisions,

rAHMEE 2

P1. Explain management accounting and give the essential requirement of

different types of management accounting systems.

Management Accounting

Management accounting, also called managerial accounting or cost accounting, is the process

of analyzing business costs and operations to prepare internal financial report, records, and

account to aid managers’ decision-making process in achieving business goals. In other words,

it is the act of making sense of financial and costing data and translating that data into useful

information for management and officers within an organization.

Origin

Managerial accounting has its roots in the industrial revolution of the 19th century. During this

early period, most firms were tightly controlled by a few owner-managers who borrowed based

on personal relationships and their personal assets.

Since there were no external shareholders and little unsecured debt, there was little need for

elaborate financial reports. In contrast, managerial accounting was relatively sophisticated and

provided the essential information needed to manage the early large-scale production of textile,

steel, and other products. After the turn of the century, financial accounting requirements

burgeoned because of new pressures placed on companies by capital markets, creditors,

regulatory bodies, and federal taxation of income. Johnson and Kaplan state that “many firms

needed to raise funds from increasingly widespread and detached suppliers of capital. To tap

these vast reservoirs of outside capital, firms’ managers had to supply audited financial reports.

And because outside suppliers of capital relied on audited financial statements, independent

accountants had a keen interest in establishing well defined procedures for corporate financial

reporting. The inventory costing procedure adopted by public accountants after the turn of the

century had a profound effect on management accounting. As a consequence, for many

decades, management accountants increasingly focused their efforts on ensuring that financial

accounting requirements were met and financial reports were released on time.

Roles

Formulate Financial Strategies

Management accountants can formulate financial strategies using sales forecasts, budgets and

job-costing techniques, among other managerial accounting tools. They also can incorporate

data from a company’s financial statements to develop strategies that enhance gross income,

net profit and earnings per share. Whether it’s formulating a plan to purchase capital equipment

or reduce operating costs to ensure the continued viability of a business, management

accountants serve a vital role in formulating effective financial strategies.

Explain Financial Consequences of Decisions

If senior leaders adjust their company’s capital structure, management accountants can explain

the ramifications of adding additional debt or equity financing. This is true of other decisions,

rAHMEE 2

Management Accounting

such as merging with other companies, opening new operating facilities or laying off large

numbers of employees. They can explain how decisions impact budgets and financial

statements, illustrating how decisions change a company’s profit or loss for a given period of

time. While some business decisions may sound good, it's only when digging into the numbers

that a company finds whether they truly add up or not.

Monitor Expenses

Management accountants can create static, flexible or rolling budgets, along with other types of

reports that allow senior leaders and department heads to monitor expenses. This is important,

because operating expenses have a direct impact on bottom-line profit. Management

accountants can select the optimal budgeting technique, given the specific needs of their

stakeholders, and help their company run as cost-effectively as possible. They also can create

ad-hoc reports that make it easier for their stakeholders to understand the nature of the

expenses their department or organization incur.

Maintain Profitability

There are many tools management accountants can use to keep their businesses profitable,

including performing a break-even analysis. With this type of analysis, the accountants weigh

sales against variable and fixed costs to determine the point at which a company breaks even.

Knowing this point will help management determine production levels, sales objectives and

overhead costs, among other points impacting profitability. Also, management accountants can

examine direct and indirect manufacturing costs, helping to optimize a company’s cost structure.

Principles

Designing and Compiling

Accounting information, records, reports, statements and other evidence of past, present or

future results should be designed and compiled to meet the needs of the particular business

and/or specific problem.

It means that management accounting system is designed in such a way presenting the

relevant data. If so, a particular problem is to be solved. Moreover, accounting information can

be modified and adopted to meet the requirements of management.

Management by Exception

The principle of management by exception is followed when presenting information to

management. It means that budgetary control system and standard costing techniques are

followed in the management accounting system.

rAHMEE 3

such as merging with other companies, opening new operating facilities or laying off large

numbers of employees. They can explain how decisions impact budgets and financial

statements, illustrating how decisions change a company’s profit or loss for a given period of

time. While some business decisions may sound good, it's only when digging into the numbers

that a company finds whether they truly add up or not.

Monitor Expenses

Management accountants can create static, flexible or rolling budgets, along with other types of

reports that allow senior leaders and department heads to monitor expenses. This is important,

because operating expenses have a direct impact on bottom-line profit. Management

accountants can select the optimal budgeting technique, given the specific needs of their

stakeholders, and help their company run as cost-effectively as possible. They also can create

ad-hoc reports that make it easier for their stakeholders to understand the nature of the

expenses their department or organization incur.

Maintain Profitability

There are many tools management accountants can use to keep their businesses profitable,

including performing a break-even analysis. With this type of analysis, the accountants weigh

sales against variable and fixed costs to determine the point at which a company breaks even.

Knowing this point will help management determine production levels, sales objectives and

overhead costs, among other points impacting profitability. Also, management accountants can

examine direct and indirect manufacturing costs, helping to optimize a company’s cost structure.

Principles

Designing and Compiling

Accounting information, records, reports, statements and other evidence of past, present or

future results should be designed and compiled to meet the needs of the particular business

and/or specific problem.

It means that management accounting system is designed in such a way presenting the

relevant data. If so, a particular problem is to be solved. Moreover, accounting information can

be modified and adopted to meet the requirements of management.

Management by Exception

The principle of management by exception is followed when presenting information to

management. It means that budgetary control system and standard costing techniques are

followed in the management accounting system.

rAHMEE 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

In this way, the actual performance is compared with pre-determined one for finding the

deviations. The unfavorable deviations alone are informed precisely to management as what is

going wrong. If so, the management has spent less time to read and study the information and

more time to take action.

Absorption of Overhead Costs

Overhead costs are absorbed on anyone of the predetermined basis. The overhead costs are

the combination of indirect materials, indirect labour and indirect expenses. Hence, the selected

method or methods for the absorption of overheads should bring about the desired results in the

most equitable manner.

Control at Source Accounting

Costs are best controlled at the points at which they are incurred – control at source accounting.

The performance of individual workers, details of materials issues and utilization and usage of

services such as machine, power, repairs and maintenance, vehicles etc. are prepared in the

form of quantitative and qualitative information. In this way, control can be exercised over

employees, materials and service providing devices.

Accounting for Inflation

A profit cannot be said to be earned unless capital is maintained intact in real terms. It means

that money value is not stable. Hence, it is necessary to assess the value of capital contributed

by the owners of the business concern in terms of real value of money through revaluation

accounting. In this way, rate of inflation is taken into account to judge the real success of the

business concern.

Management Accounting System

Financial accounting focuses on preparing information for external parties, such as

stockholders, public regulators and lenders, in accordance with generally accepted accounting

principles. Managerial accounting, on the other hand, takes a company's financial information

and develops reports for internal and confidential use by managers for decision-making and

rAHMEE 4

In this way, the actual performance is compared with pre-determined one for finding the

deviations. The unfavorable deviations alone are informed precisely to management as what is

going wrong. If so, the management has spent less time to read and study the information and

more time to take action.

Absorption of Overhead Costs

Overhead costs are absorbed on anyone of the predetermined basis. The overhead costs are

the combination of indirect materials, indirect labour and indirect expenses. Hence, the selected

method or methods for the absorption of overheads should bring about the desired results in the

most equitable manner.

Control at Source Accounting

Costs are best controlled at the points at which they are incurred – control at source accounting.

The performance of individual workers, details of materials issues and utilization and usage of

services such as machine, power, repairs and maintenance, vehicles etc. are prepared in the

form of quantitative and qualitative information. In this way, control can be exercised over

employees, materials and service providing devices.

Accounting for Inflation

A profit cannot be said to be earned unless capital is maintained intact in real terms. It means

that money value is not stable. Hence, it is necessary to assess the value of capital contributed

by the owners of the business concern in terms of real value of money through revaluation

accounting. In this way, rate of inflation is taken into account to judge the real success of the

business concern.

Management Accounting System

Financial accounting focuses on preparing information for external parties, such as

stockholders, public regulators and lenders, in accordance with generally accepted accounting

principles. Managerial accounting, on the other hand, takes a company's financial information

and develops reports for internal and confidential use by managers for decision-making and

rAHMEE 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

identifying ways to run the company more efficiently. These reports are based on

management's informational needs and include budgeting, breakeven charts, product cost

analysis, trend charts and forecasting.

Inventory management System

Inventory management is a discipline primarily about specifying the shape and

placement of stocked goods. It is required at different locations within a facility or within

many locations of a supply network to precede the regular and planned course of

production and stock of materials.

Cost Accounting System

A cost accounting system is used by manufacturers to record production activities using

a perpetual inventory system. In other words, it’s an accounting system designed for

manufacturers that tracks the flow of inventory continually through the various stages of

production.

Job Costing System

Job cost accounting is the process of assigning the costs you incur to a specific job you

or your business is involved with. This term is widely used in the construction industry

and it refers to allocating costs to individual construction projects at a company.

Price optimization System

Price optimization is the process of finding that pricing sweet spot, or maximizing price

against the customers willingness to pay. Companies up and down the supply chain,

both in B2B and B2C settings, rightly dedicate a massive amount of time towards price

optimization to ensure that their products will sell quickly at the right price while still

making a decent profit.

The different between Financial Accounting and Management Accounting

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

rAHMEE 5

identifying ways to run the company more efficiently. These reports are based on

management's informational needs and include budgeting, breakeven charts, product cost

analysis, trend charts and forecasting.

Inventory management System

Inventory management is a discipline primarily about specifying the shape and

placement of stocked goods. It is required at different locations within a facility or within

many locations of a supply network to precede the regular and planned course of

production and stock of materials.

Cost Accounting System

A cost accounting system is used by manufacturers to record production activities using

a perpetual inventory system. In other words, it’s an accounting system designed for

manufacturers that tracks the flow of inventory continually through the various stages of

production.

Job Costing System

Job cost accounting is the process of assigning the costs you incur to a specific job you

or your business is involved with. This term is widely used in the construction industry

and it refers to allocating costs to individual construction projects at a company.

Price optimization System

Price optimization is the process of finding that pricing sweet spot, or maximizing price

against the customers willingness to pay. Companies up and down the supply chain,

both in B2B and B2C settings, rightly dedicate a massive amount of time towards price

optimization to ensure that their products will sell quickly at the right price while still

making a decent profit.

The different between Financial Accounting and Management Accounting

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

rAHMEE 5

Management Accounting

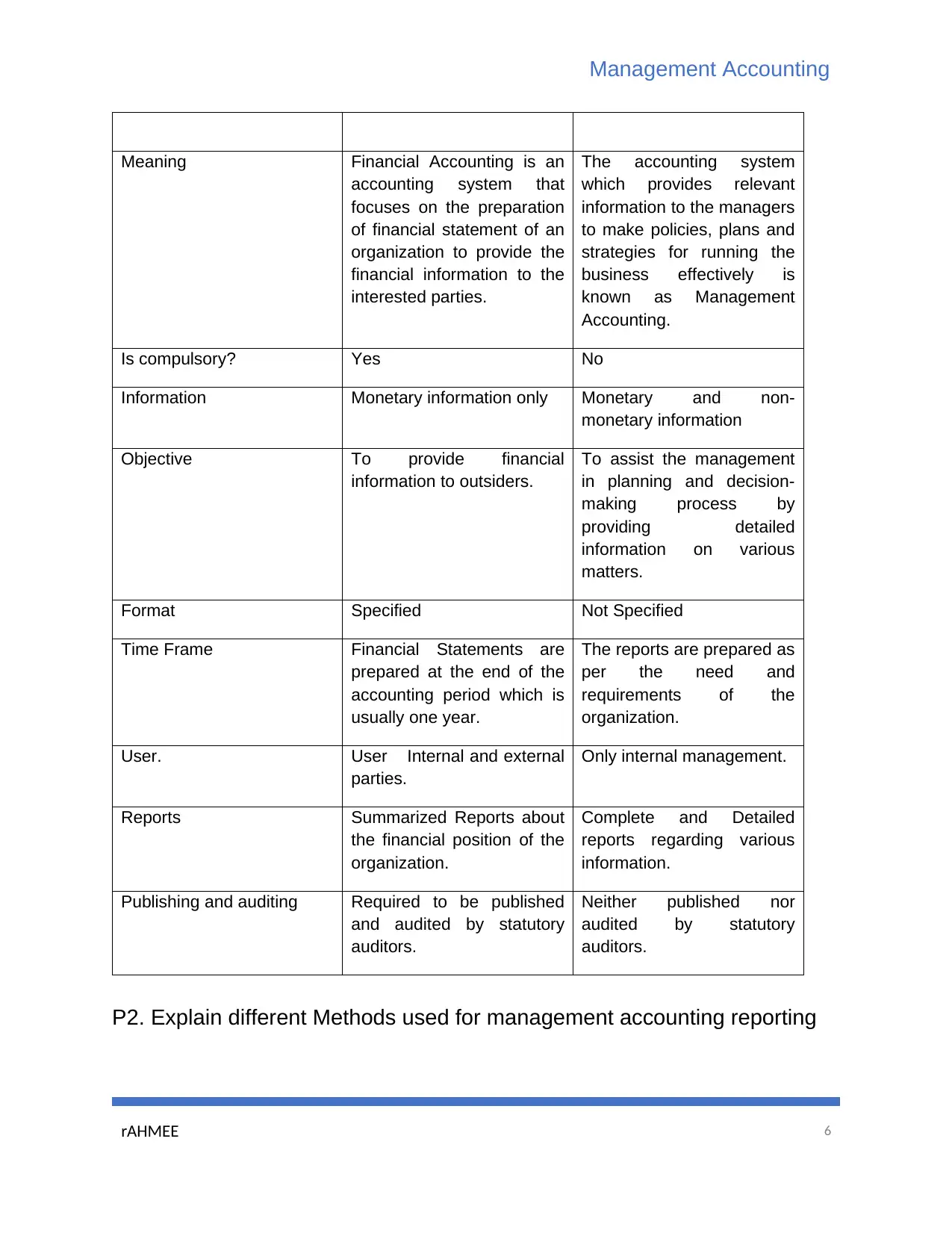

Meaning Financial Accounting is an

accounting system that

focuses on the preparation

of financial statement of an

organization to provide the

financial information to the

interested parties.

The accounting system

which provides relevant

information to the managers

to make policies, plans and

strategies for running the

business effectively is

known as Management

Accounting.

Is compulsory? Yes No

Information Monetary information only Monetary and non-

monetary information

Objective To provide financial

information to outsiders.

To assist the management

in planning and decision-

making process by

providing detailed

information on various

matters.

Format Specified Not Specified

Time Frame Financial Statements are

prepared at the end of the

accounting period which is

usually one year.

The reports are prepared as

per the need and

requirements of the

organization.

User. User Internal and external

parties.

Only internal management.

Reports Summarized Reports about

the financial position of the

organization.

Complete and Detailed

reports regarding various

information.

Publishing and auditing Required to be published

and audited by statutory

auditors.

Neither published nor

audited by statutory

auditors.

P2. Explain different Methods used for management accounting reporting

rAHMEE 6

Meaning Financial Accounting is an

accounting system that

focuses on the preparation

of financial statement of an

organization to provide the

financial information to the

interested parties.

The accounting system

which provides relevant

information to the managers

to make policies, plans and

strategies for running the

business effectively is

known as Management

Accounting.

Is compulsory? Yes No

Information Monetary information only Monetary and non-

monetary information

Objective To provide financial

information to outsiders.

To assist the management

in planning and decision-

making process by

providing detailed

information on various

matters.

Format Specified Not Specified

Time Frame Financial Statements are

prepared at the end of the

accounting period which is

usually one year.

The reports are prepared as

per the need and

requirements of the

organization.

User. User Internal and external

parties.

Only internal management.

Reports Summarized Reports about

the financial position of the

organization.

Complete and Detailed

reports regarding various

information.

Publishing and auditing Required to be published

and audited by statutory

auditors.

Neither published nor

audited by statutory

auditors.

P2. Explain different Methods used for management accounting reporting

rAHMEE 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

Why information should be relevant to the user, reliable, up to date

and accurate.

What is Information?

Data that is accurate and timely, specific and organized for a purpose, presented within a

context that gives it meaning and relevance, and can lead to an increase in understanding and

decrease in uncertainty. Information is valuable because it can affect behavior, a decision, or an

outcome.

Relevance

Data captured should be relevant to the purposes for which it is to be used. This will require

a periodic review of requirements to reflect changing needs.

We have a duty to collect and report performance information against a wide range

of statutory indicators. These are set out in the context of the Government’s White

Paper – Strong and Prosperous Communities. Where appropriate each service will

identify reliable local performance indicators to manage performance and drive

improvement. These are reviewed on an annual basis to ensure relevance.

Reliable

Data should reflect stable and consistent data collection processes across collection points

and over time. Progress toward performance targets should reflect real changes rather than

variations in data collection approaches or methods.

Source data is clearly identified and readily available from manual, automated or other

systems and records. Protocols exist where data is provided from a third party, such as

Hertfordshire Constabulary and Hertfordshire County Council.

Accuracy

Data should be sufficiently accurate for the intended use and should be captured only once,

although it may have multiple uses. Data should be captured at the point of activity.

Data is always captured at the point of activity. Performance data is directly input into

Performance Plus by the service manager or nominated data entry staff.

Access to P+ for the purpose of data entry is restricted through secure password

controls and limited access to appropriate data entry pages. Individual passwords can

be changed by the user and which under no circumstances should be used by anyone

other than that user.

Where appropriate, base data, i.e. denominators and numerators, will be input into the

system which will then calculate the result. These have been determined in accordance

rAHMEE 7

Why information should be relevant to the user, reliable, up to date

and accurate.

What is Information?

Data that is accurate and timely, specific and organized for a purpose, presented within a

context that gives it meaning and relevance, and can lead to an increase in understanding and

decrease in uncertainty. Information is valuable because it can affect behavior, a decision, or an

outcome.

Relevance

Data captured should be relevant to the purposes for which it is to be used. This will require

a periodic review of requirements to reflect changing needs.

We have a duty to collect and report performance information against a wide range

of statutory indicators. These are set out in the context of the Government’s White

Paper – Strong and Prosperous Communities. Where appropriate each service will

identify reliable local performance indicators to manage performance and drive

improvement. These are reviewed on an annual basis to ensure relevance.

Reliable

Data should reflect stable and consistent data collection processes across collection points

and over time. Progress toward performance targets should reflect real changes rather than

variations in data collection approaches or methods.

Source data is clearly identified and readily available from manual, automated or other

systems and records. Protocols exist where data is provided from a third party, such as

Hertfordshire Constabulary and Hertfordshire County Council.

Accuracy

Data should be sufficiently accurate for the intended use and should be captured only once,

although it may have multiple uses. Data should be captured at the point of activity.

Data is always captured at the point of activity. Performance data is directly input into

Performance Plus by the service manager or nominated data entry staff.

Access to P+ for the purpose of data entry is restricted through secure password

controls and limited access to appropriate data entry pages. Individual passwords can

be changed by the user and which under no circumstances should be used by anyone

other than that user.

Where appropriate, base data, i.e. denominators and numerators, will be input into the

system which will then calculate the result. These have been determined in accordance

rAHMEE 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

with published guidance or agreed locally. This will eliminate calculation errors at this

stage of the process, as well as provide contextual information for the reader.

Timeliness

Data should be captured as quickly as possible after the event or activity and must be

available for the intended use within a reasonable time period. Data must be available

quickly and frequently enough to support information needs and to influence service or

management decisions.

Performance data is requested to be available within one calendar month from the end

of the previous quarter and is subsequently reported to the respective Policy and

Scrutiny Panel on a quarterly basis. As a part of the ongoing development of

Performance Plus it is intended that performance information will be exported through

custom reporting and made available via the Three Rivers DC website. This will improve

access to information and eliminate delays in publishing information through traditional

methods.

Why the way in which the information is presented must be

understandable

The Understandable information must be easily to get ideas when users can be read. And this

information gives how to planning, how to control and also how to organize for the decision

making. Understanding is a brief, complete and clear explanation for the information provided in

the report. The Information relating to the relationship is essential to users in understanding

financial statements. The legitimate background of business activities represents the

understanding of the data the financial quality that can be understood from they people with

knowledge.

The main things are we consider the understandable presented information, there are:

Information must be understandable by its users.

Main two external users are Investors and Creditors.

Users are assumed to have reasonable comprehension of, and ability to study, the

accounting, business, and economic concepts needed to the underattended information.

However, by understanding its fundamental problems, each of them will not fully understand the

complex information. Instead of providing a system, the information must be published correctly.

Different types of managerial accounting reports

rAHMEE 8

with published guidance or agreed locally. This will eliminate calculation errors at this

stage of the process, as well as provide contextual information for the reader.

Timeliness

Data should be captured as quickly as possible after the event or activity and must be

available for the intended use within a reasonable time period. Data must be available

quickly and frequently enough to support information needs and to influence service or

management decisions.

Performance data is requested to be available within one calendar month from the end

of the previous quarter and is subsequently reported to the respective Policy and

Scrutiny Panel on a quarterly basis. As a part of the ongoing development of

Performance Plus it is intended that performance information will be exported through

custom reporting and made available via the Three Rivers DC website. This will improve

access to information and eliminate delays in publishing information through traditional

methods.

Why the way in which the information is presented must be

understandable

The Understandable information must be easily to get ideas when users can be read. And this

information gives how to planning, how to control and also how to organize for the decision

making. Understanding is a brief, complete and clear explanation for the information provided in

the report. The Information relating to the relationship is essential to users in understanding

financial statements. The legitimate background of business activities represents the

understanding of the data the financial quality that can be understood from they people with

knowledge.

The main things are we consider the understandable presented information, there are:

Information must be understandable by its users.

Main two external users are Investors and Creditors.

Users are assumed to have reasonable comprehension of, and ability to study, the

accounting, business, and economic concepts needed to the underattended information.

However, by understanding its fundamental problems, each of them will not fully understand the

complex information. Instead of providing a system, the information must be published correctly.

Different types of managerial accounting reports

rAHMEE 8

Management Accounting

Managerial accounting reports help small business owners and managers monitor the

company's performance and are prepared frequently throughout accounting periods as needed.

Depending on the type of project and the time-sensitivity of the information, an owner or

manager may request reports quarterly, monthly, weekly or even daily.

Budget Report

Budget reports help small business owners analyze their company's performance and, if the

business is big enough, managers analyze their department's performance and control costs.

The estimated budget for the period is usually based on the actual expenses from prior years. If

the small business as a whole or a specific department was substantially over budget in a

previous year and cannot find feasible ways to trim costs, the budget for future years may need

to be increased to a more accurate level. Owners and managers can also use budget reports to

provide incentives to employees. In this case, some of the funds budgeted may be given out up

as bonuses to employees for meeting specific financial goals.

Accounts Receivable Aging Reports

The accounts receivable aging report is a critical tool for managing cash flow for companies that

extend credit to their customers. This report breaks down the customer balances by how long

they have been owed. Most aging reports include separate columns for invoices that are 30

days late, 60 days late and 90 days late or more. A manager can use the aging report to find

problems with the company's collections process. If a significant number of customers are

unable to pay their balances, the company may need to tighten its credit policies. Periodically

analyzing the accounts receivable aging also keeps the collections department from overlooking

old debts.

Job Cost Reports

Job cost reports show expenses for a specific project. They are usually matched with an

estimate of revenue so the company can evaluate the job's profitability. This helps identify

higher-earning areas of the business so the company can focus its efforts there instead of

wasting time and money on jobs with low profit margins. Job cost reports are also used to

analyze expenses while the project is in progress so managers can correct areas of waste

before the costs escalate.

Inventory and Manufacturing

Companies with physical inventory can use managerial accounting reports to make their

manufacturing processes more efficient. These reports generally include items such as

inventory waste, hourly labor costs or per-unit overhead costs. The manager can then compare

different assembly lines within the company to see where one can improve or to offer bonuses

to the best-performing departments.

rAHMEE 9

Managerial accounting reports help small business owners and managers monitor the

company's performance and are prepared frequently throughout accounting periods as needed.

Depending on the type of project and the time-sensitivity of the information, an owner or

manager may request reports quarterly, monthly, weekly or even daily.

Budget Report

Budget reports help small business owners analyze their company's performance and, if the

business is big enough, managers analyze their department's performance and control costs.

The estimated budget for the period is usually based on the actual expenses from prior years. If

the small business as a whole or a specific department was substantially over budget in a

previous year and cannot find feasible ways to trim costs, the budget for future years may need

to be increased to a more accurate level. Owners and managers can also use budget reports to

provide incentives to employees. In this case, some of the funds budgeted may be given out up

as bonuses to employees for meeting specific financial goals.

Accounts Receivable Aging Reports

The accounts receivable aging report is a critical tool for managing cash flow for companies that

extend credit to their customers. This report breaks down the customer balances by how long

they have been owed. Most aging reports include separate columns for invoices that are 30

days late, 60 days late and 90 days late or more. A manager can use the aging report to find

problems with the company's collections process. If a significant number of customers are

unable to pay their balances, the company may need to tighten its credit policies. Periodically

analyzing the accounts receivable aging also keeps the collections department from overlooking

old debts.

Job Cost Reports

Job cost reports show expenses for a specific project. They are usually matched with an

estimate of revenue so the company can evaluate the job's profitability. This helps identify

higher-earning areas of the business so the company can focus its efforts there instead of

wasting time and money on jobs with low profit margins. Job cost reports are also used to

analyze expenses while the project is in progress so managers can correct areas of waste

before the costs escalate.

Inventory and Manufacturing

Companies with physical inventory can use managerial accounting reports to make their

manufacturing processes more efficient. These reports generally include items such as

inventory waste, hourly labor costs or per-unit overhead costs. The manager can then compare

different assembly lines within the company to see where one can improve or to offer bonuses

to the best-performing departments.

rAHMEE 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

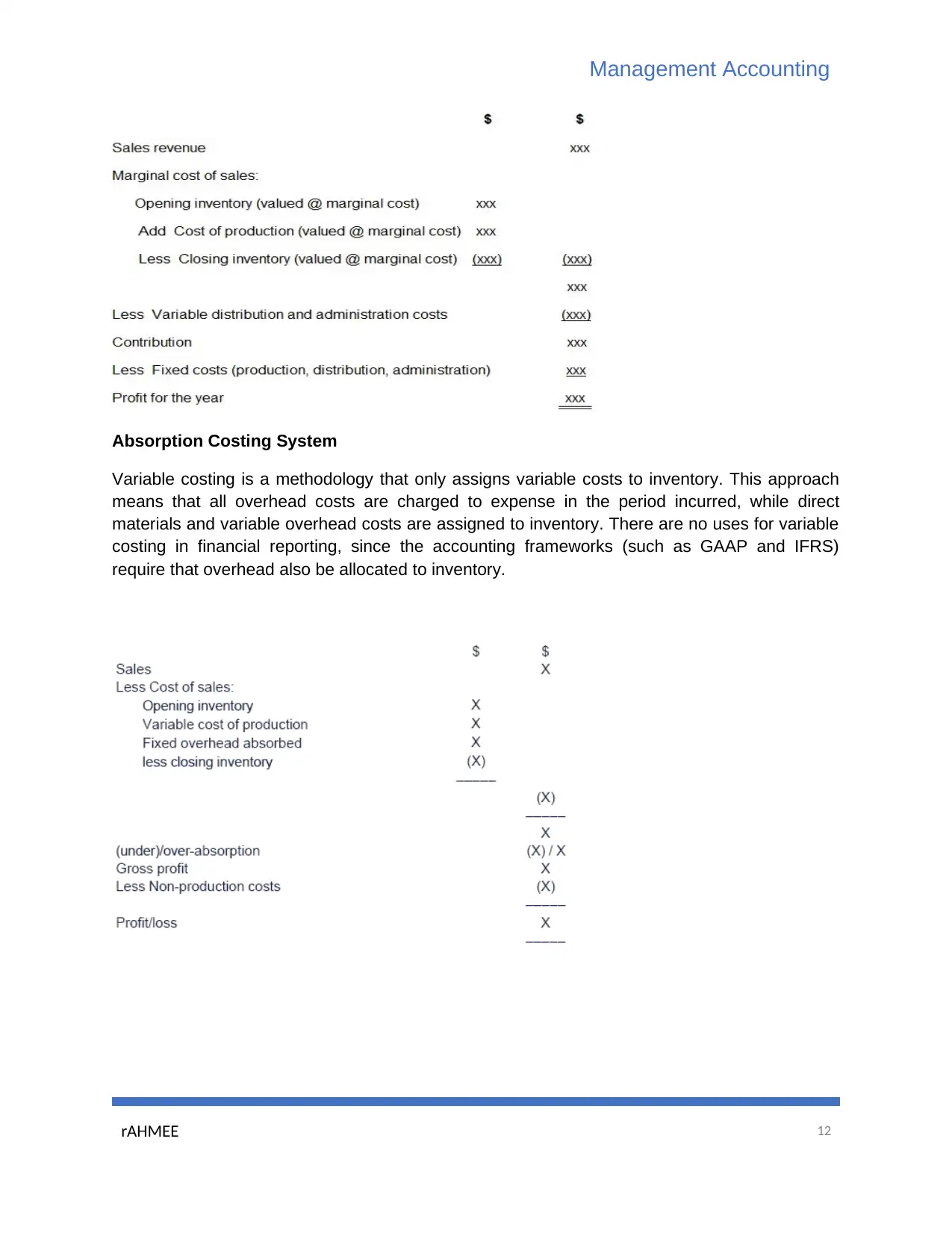

LO2. Apply a range of management accounting techniques

P3. Calculate costs using appropriates techniques of cost analysis to

prepare an income statement using marginal and absorption costs.

A.Cost

In business and accounting, cost is the monetary value that a company has spent in order to

produce something. Cost denotes the amount of money that a company spends on the creation

or production of goods or services. It does not include the markup for profit. From a seller’s point

of view, cost is the amount of money that is spent to produce a good or product. If a producer

were to sell his products at the production price, his costs and income would break even,

meaning that he would not lose money on the sales. However, he would not make a profit. From

a buyer’s point of view the cost of a product is also known as the price. This is the amount that

the seller charges for a product, and it includes both the production cost and the mark-up, which

is added by the seller in order to make a profit.

B. Different Classification cost such as,

Fixed Cost

A periodic cost that remains more or less unchanged irrespective of the output level or sales

revenue, While in practice, all costs vary over time and no cost is a purely fixed cost, the

concept of fixed costs is necessary in short term cost accounting. Organizations with high fixed

costs are significantly different from those with high variable costs. This difference affects the

financial structure of the organization as well as its pricing and profits. The breakeven point in

such organizations (in comparison with high variable cost organizations) is typically at a much

higher level of output, and their marginal profit (rate of contribution) is also much higher.

EX- insurance, interest, rent, salaries

Variable Cost

A variable cost is a cost that varies in relation to either production volume or services provided.

If there is no production or no services are provided, then there should be no variable costs.

EX- Bonus, wage cost

Direct Cost

A direct cost is a price that can be completely attributed to the production of specific goods or

services. Some costs, such as depreciation or administrative expenses, are more difficult to

assign to a specific product and therefore are considered to be indirect costs.

EX-Direct material, Direct labour

rAHMEE 10

LO2. Apply a range of management accounting techniques

P3. Calculate costs using appropriates techniques of cost analysis to

prepare an income statement using marginal and absorption costs.

A.Cost

In business and accounting, cost is the monetary value that a company has spent in order to

produce something. Cost denotes the amount of money that a company spends on the creation

or production of goods or services. It does not include the markup for profit. From a seller’s point

of view, cost is the amount of money that is spent to produce a good or product. If a producer

were to sell his products at the production price, his costs and income would break even,

meaning that he would not lose money on the sales. However, he would not make a profit. From

a buyer’s point of view the cost of a product is also known as the price. This is the amount that

the seller charges for a product, and it includes both the production cost and the mark-up, which

is added by the seller in order to make a profit.

B. Different Classification cost such as,

Fixed Cost

A periodic cost that remains more or less unchanged irrespective of the output level or sales

revenue, While in practice, all costs vary over time and no cost is a purely fixed cost, the

concept of fixed costs is necessary in short term cost accounting. Organizations with high fixed

costs are significantly different from those with high variable costs. This difference affects the

financial structure of the organization as well as its pricing and profits. The breakeven point in

such organizations (in comparison with high variable cost organizations) is typically at a much

higher level of output, and their marginal profit (rate of contribution) is also much higher.

EX- insurance, interest, rent, salaries

Variable Cost

A variable cost is a cost that varies in relation to either production volume or services provided.

If there is no production or no services are provided, then there should be no variable costs.

EX- Bonus, wage cost

Direct Cost

A direct cost is a price that can be completely attributed to the production of specific goods or

services. Some costs, such as depreciation or administrative expenses, are more difficult to

assign to a specific product and therefore are considered to be indirect costs.

EX-Direct material, Direct labour

rAHMEE 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

Indirect Cost

Indirect costs are costs that are not directly accountable to a cost object (such as a particular

project, facility, function or product). Indirect costs may be either fixed or variable, But some

overhead costs can be directly attributed to a project and are direct costs.

EX--Indirect material, Indirect labour

Material Cost

Direct materials cost the cost of direct materials which can be easily identified with the unit of

production. For example, the cost of glass is a direct materials cost in light bulb manufacturing.

The manufacture of products or goods required material as the prime element.

Labor Cost

Labor cost is wages that are incurred in order to produce specific goods or provide specific

services to customers. The total amount of labor cost is much more than wages paid. It also

includes the payroll taxes associated with those wages, plus the cost of company-paid medical

insurance, life insurance, workers' compensation insurance, any company-matched pension

contributions, and other company benefits.

Inventory Cost

Inventory cost includes the costs to order and hold inventory, as well as to administer the

related paperwork. This cost is examined by management as part of its evaluation of how much

inventory to keep on hand. This can result in changes in the order fulfillment rate for customers,

as well as variations in the production process flow.

C. Different Costing system such as,

Marginal Costing System

Marginal cost is the cost of one additional unit of output. The concept is used to determine the

optimum production quantity for a company, where it costs the least amount to produce

additional units. If a company operates within this "sweet spot," it can maximize its profits. The

concept is also used to determine product pricing when customers request the lowest possible

price for certain orders.

rAHMEE 11

Indirect Cost

Indirect costs are costs that are not directly accountable to a cost object (such as a particular

project, facility, function or product). Indirect costs may be either fixed or variable, But some

overhead costs can be directly attributed to a project and are direct costs.

EX--Indirect material, Indirect labour

Material Cost

Direct materials cost the cost of direct materials which can be easily identified with the unit of

production. For example, the cost of glass is a direct materials cost in light bulb manufacturing.

The manufacture of products or goods required material as the prime element.

Labor Cost

Labor cost is wages that are incurred in order to produce specific goods or provide specific

services to customers. The total amount of labor cost is much more than wages paid. It also

includes the payroll taxes associated with those wages, plus the cost of company-paid medical

insurance, life insurance, workers' compensation insurance, any company-matched pension

contributions, and other company benefits.

Inventory Cost

Inventory cost includes the costs to order and hold inventory, as well as to administer the

related paperwork. This cost is examined by management as part of its evaluation of how much

inventory to keep on hand. This can result in changes in the order fulfillment rate for customers,

as well as variations in the production process flow.

C. Different Costing system such as,

Marginal Costing System

Marginal cost is the cost of one additional unit of output. The concept is used to determine the

optimum production quantity for a company, where it costs the least amount to produce

additional units. If a company operates within this "sweet spot," it can maximize its profits. The

concept is also used to determine product pricing when customers request the lowest possible

price for certain orders.

rAHMEE 11

Management Accounting

Absorption Costing System

Variable costing is a methodology that only assigns variable costs to inventory. This approach

means that all overhead costs are charged to expense in the period incurred, while direct

materials and variable overhead costs are assigned to inventory. There are no uses for variable

costing in financial reporting, since the accounting frameworks (such as GAAP and IFRS)

require that overhead also be allocated to inventory.

rAHMEE 12

Absorption Costing System

Variable costing is a methodology that only assigns variable costs to inventory. This approach

means that all overhead costs are charged to expense in the period incurred, while direct

materials and variable overhead costs are assigned to inventory. There are no uses for variable

costing in financial reporting, since the accounting frameworks (such as GAAP and IFRS)

require that overhead also be allocated to inventory.

rAHMEE 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.