Comprehensive Analysis of Business Transactions and Accounting

VerifiedAdded on 2021/10/06

|21

|3846

|295

Homework Assignment

AI Summary

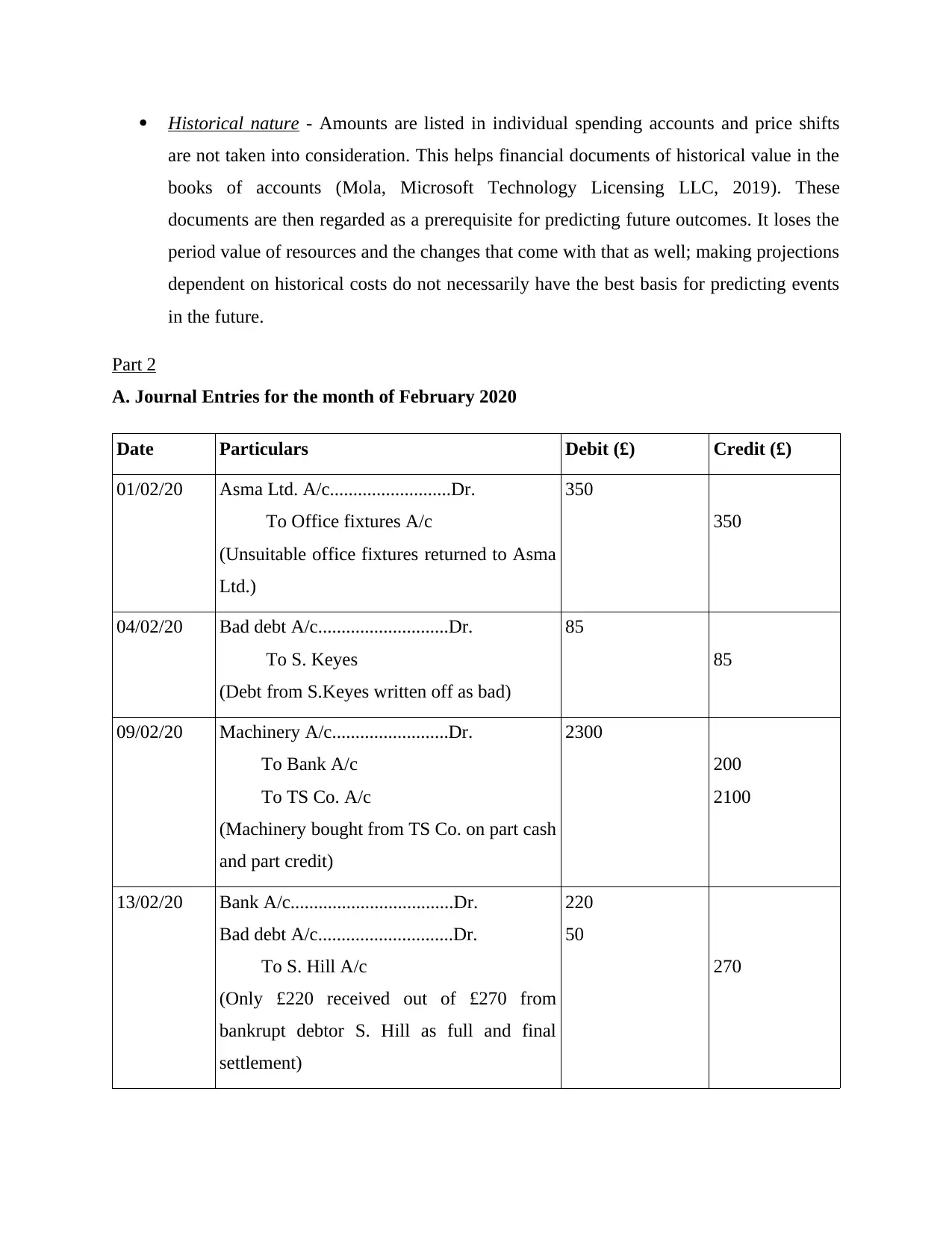

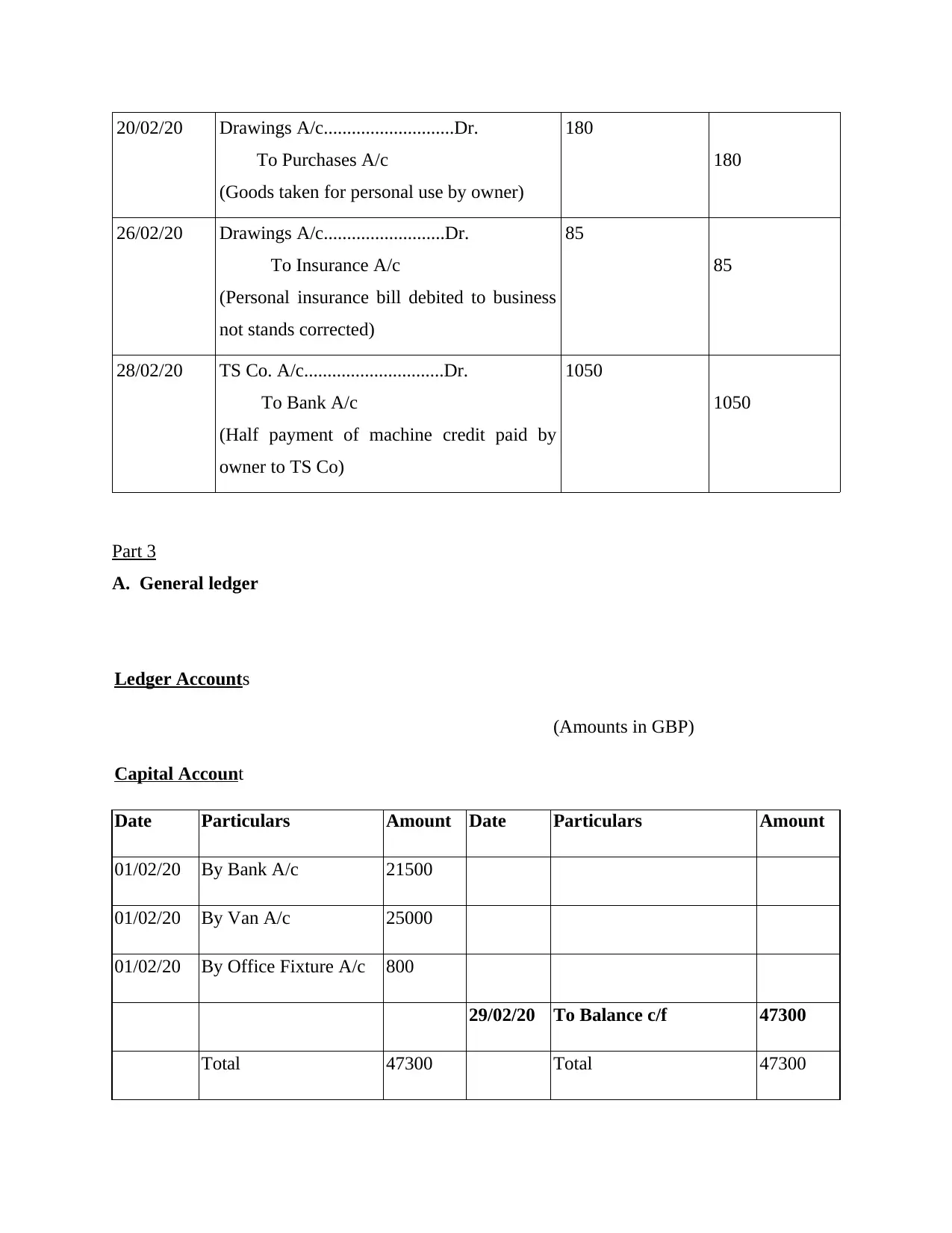

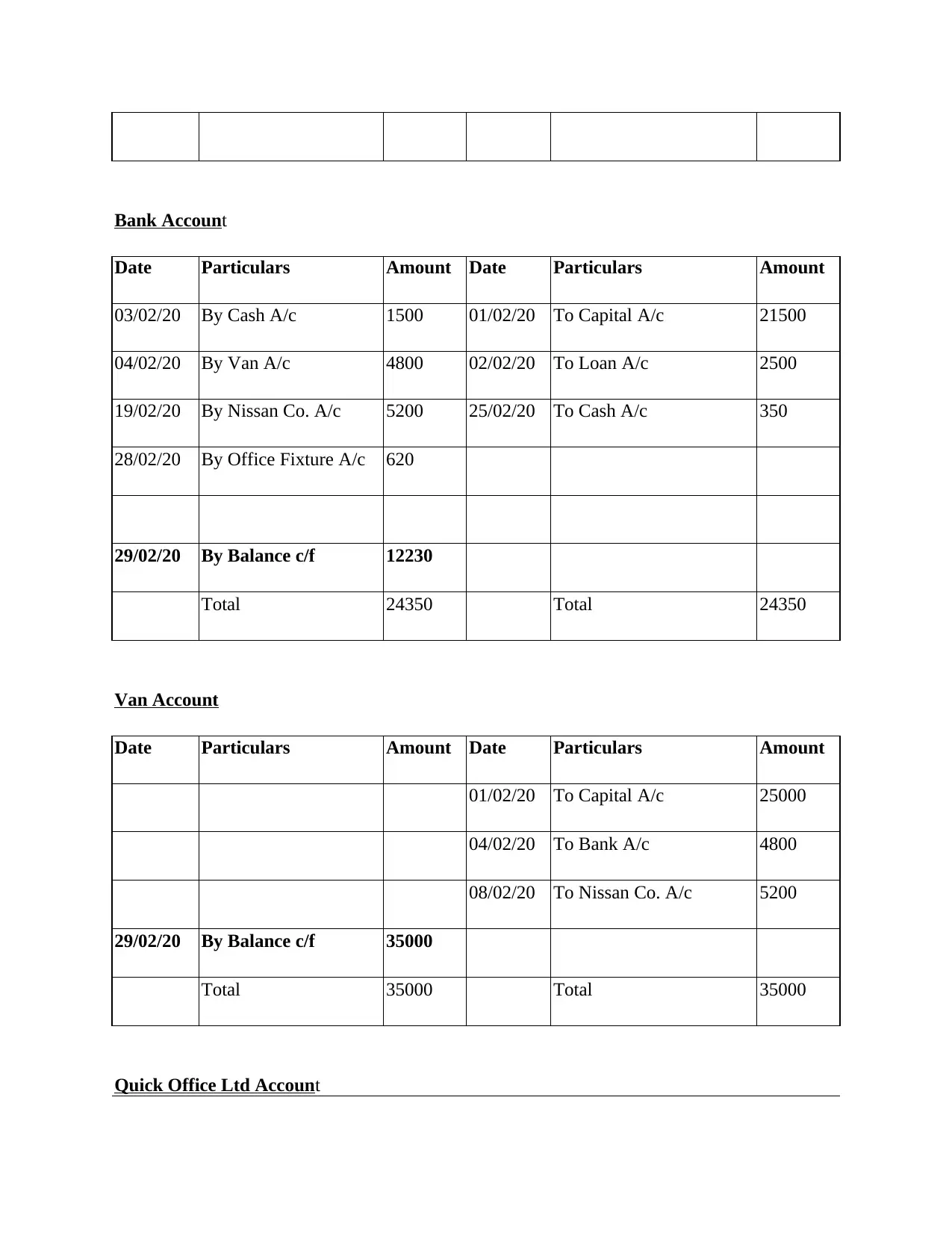

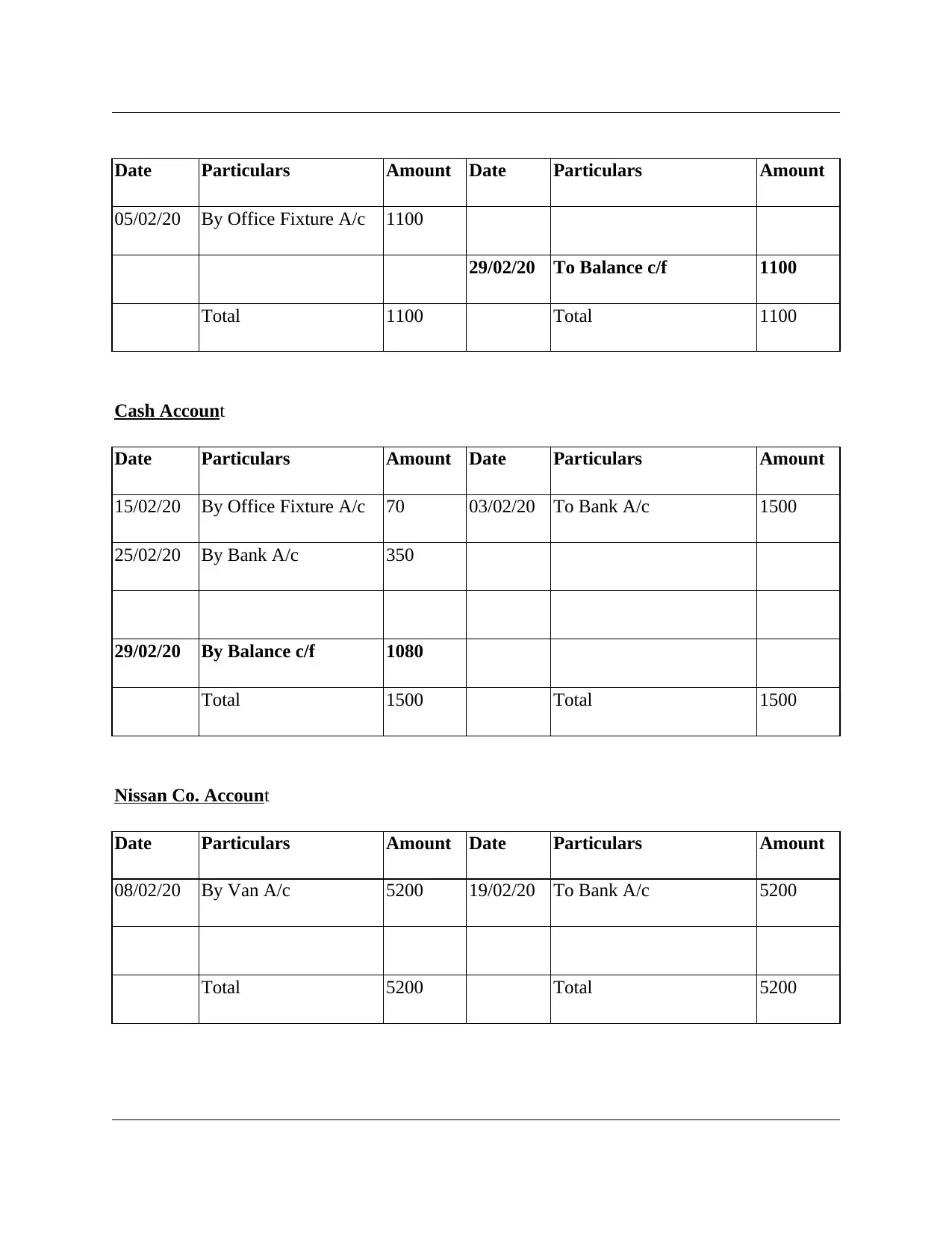

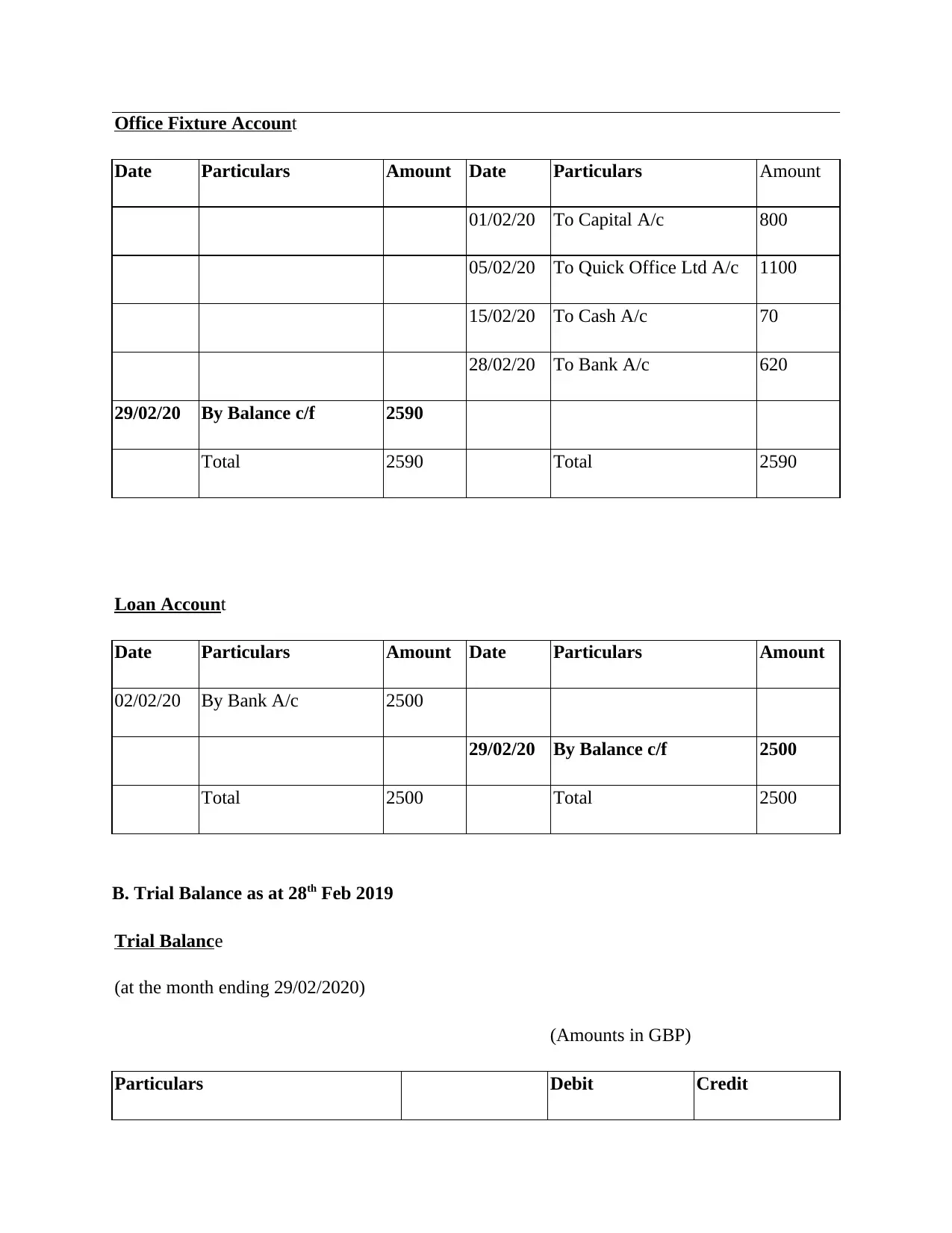

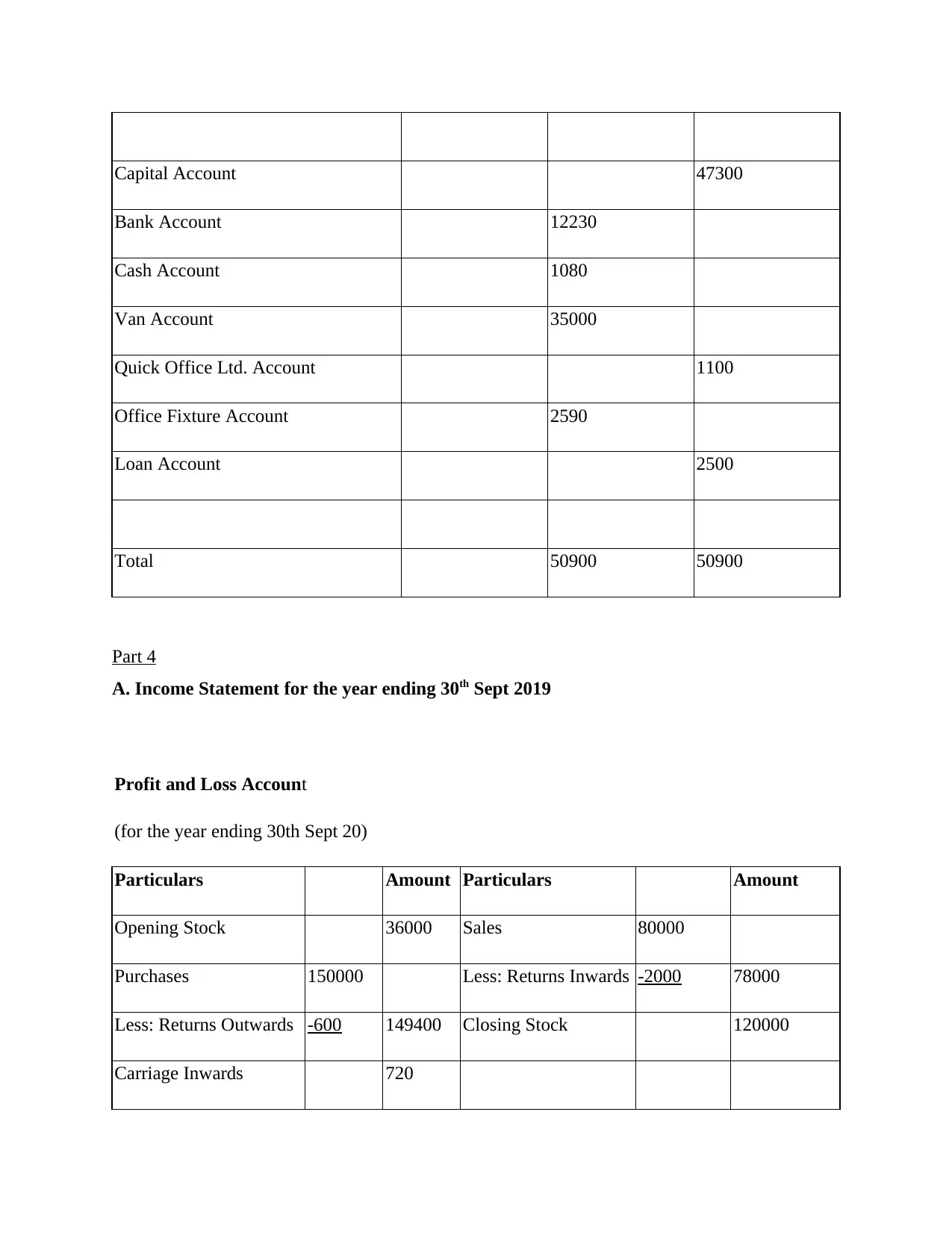

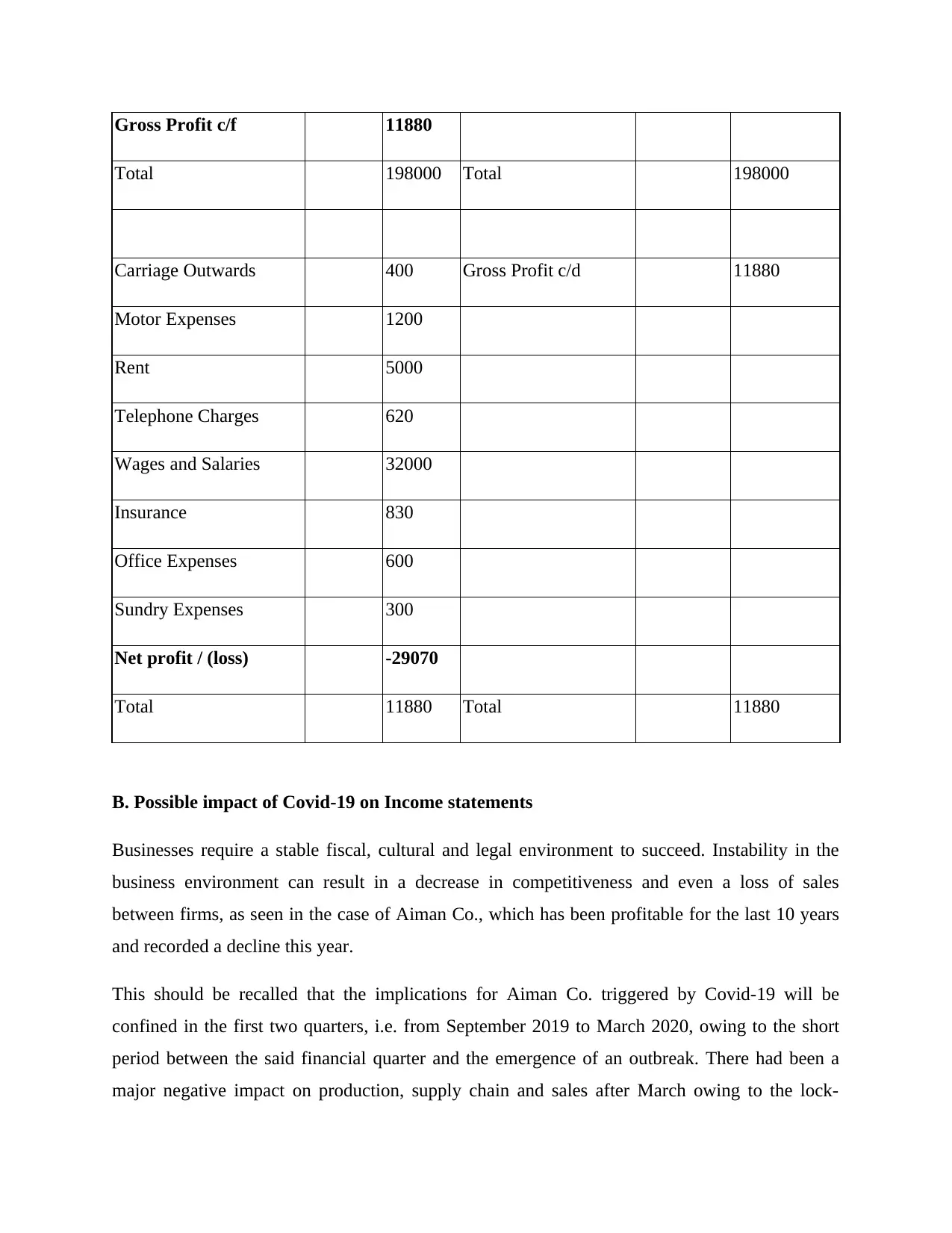

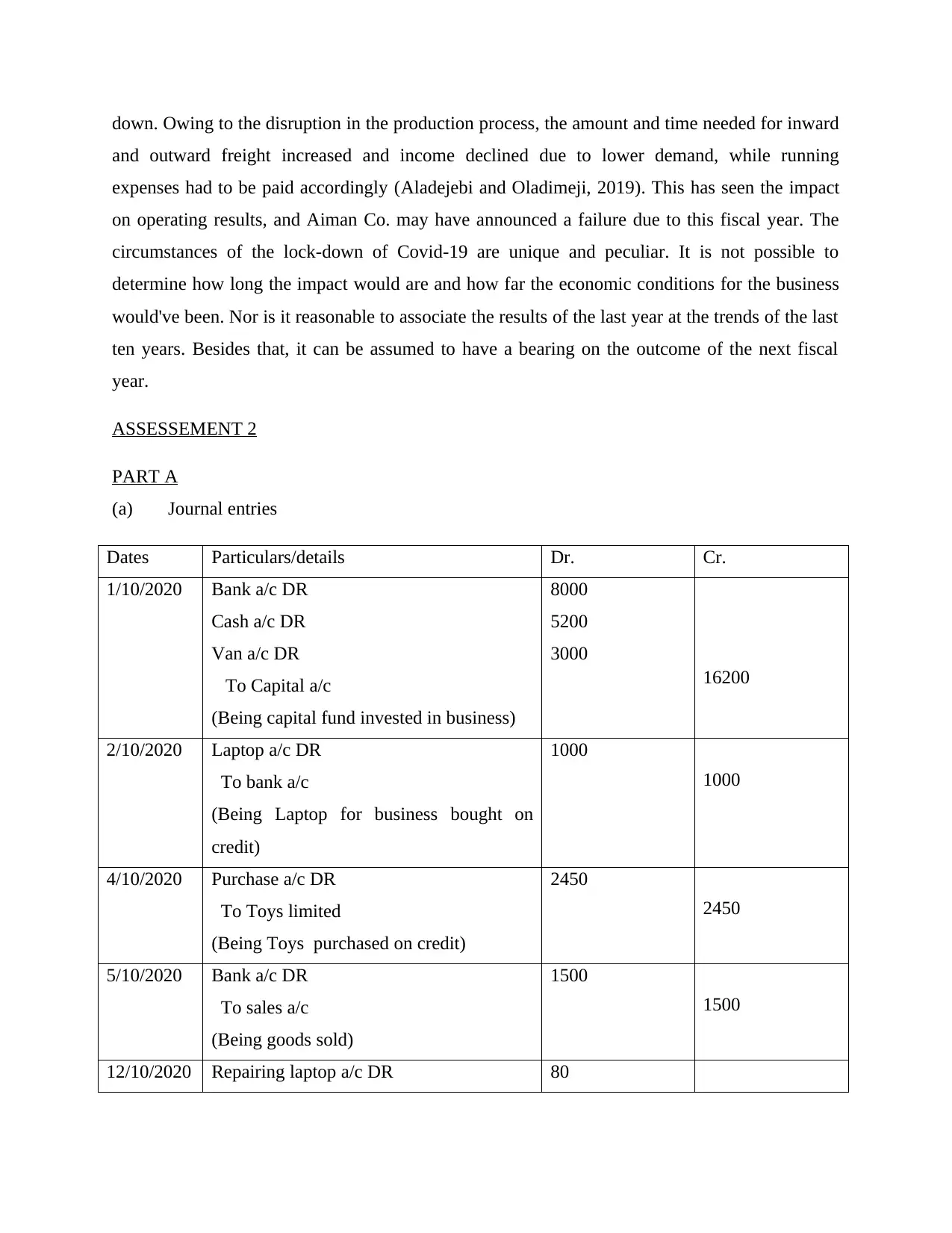

This assignment delves into the core principles of accounting by analyzing and recording various business transactions. It begins with an introduction to accounting, emphasizing its role in financial reporting and decision-making, and then explores the advantages and disadvantages of accounting for a business. The assignment provides detailed journal entries, general ledger accounts, and a trial balance. Furthermore, it includes the preparation of an income statement and discusses the potential impacts of Covid-19 on income statements. The solution covers different aspects of accounting, from recording transactions to preparing financial statements and analyzing the impact of external factors, offering a comprehensive understanding of accounting practices. The assignment also includes a practical component with journal entries, ledgers, and financial statements, providing a hands-on learning experience. Finally, it balances and brings down an opening balance for the accounts.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.