Comprehensive Analysis of Costs and Revenues in Business Operations

VerifiedAdded on 2020/10/22

|15

|2609

|170

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues within a business context. It begins with an introduction to internal reporting, emphasizing its purpose in providing accurate information to management, and explores the relationships between various costing systems, including job and process costing. The report delves into responsibility centers, cost centers, and investment centers, along with cost classifications, including marginal and absorption costing. It examines cost details for labor, materials, and expenses, analyzing cost information and inventory valuation methods like FIFO. The report covers overhead costs, allocation, apportionment, and absorption methods, as well as the treatment of under- or over-recovered overhead costs. Additionally, it addresses budget variance analysis, management reporting, and the use of future income and costs for decision-making, including break-even analysis and discounted cash flow. The impact of changing activity levels on unit costs and factors affecting short-term and long-term decision-making are also evaluated, culminating in a conclusion that summarizes the key concepts discussed. References are provided to support the analysis.

COSTS AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and providing accurate information to management.......1

1.2 Relationship between the various costing systems with in business.....................................1

1.3 the responsibility centres, cost centres and investment centres with in organisation............2

1.4 The characteristics of various kind of cost classifications and its use in costing..................2

1.5 The difference between marginal and absorption costing.....................................................2

TASK 2............................................................................................................................................3

2.1 Cost details for labour, material and expenses as per the organisation's costing procedure..3

2.2 Analysis of cost information as labour, material and expenses as per the organisation's

costing procedure.........................................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Valuation of inventories by using inventory valuation methods...........................................4

2.5 Behaviour of cost...................................................................................................................5

2.6 Cost information by using costing system.............................................................................5

TASK 3............................................................................................................................................6

3.1 Overhead costs to production and service cost centres as per allocation and apportionment

......................................................................................................................................................6

3.2 Analysis of rates in accordance with adequate bases of absorption......................................6

3.3 Treatment of under or over recovered overhead costs in accordance with established

procedures....................................................................................................................................6

Over and under absorption: -.......................................................................................................7

3.4 Methods of allocation, apportionment and absorption at regular intervals...........................7

3.5 Execution with staff to resolve the questions in overhead cost data......................................7

TASK 4............................................................................................................................................8

4.1 Comparison of budget with actual budget cost and variances...............................................8

4.2 Analysis of variances for management reports......................................................................8

4.3 Information for budget holders of significant variances making suggestions remedial

actions..........................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and providing accurate information to management.......1

1.2 Relationship between the various costing systems with in business.....................................1

1.3 the responsibility centres, cost centres and investment centres with in organisation............2

1.4 The characteristics of various kind of cost classifications and its use in costing..................2

1.5 The difference between marginal and absorption costing.....................................................2

TASK 2............................................................................................................................................3

2.1 Cost details for labour, material and expenses as per the organisation's costing procedure..3

2.2 Analysis of cost information as labour, material and expenses as per the organisation's

costing procedure.........................................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Valuation of inventories by using inventory valuation methods...........................................4

2.5 Behaviour of cost...................................................................................................................5

2.6 Cost information by using costing system.............................................................................5

TASK 3............................................................................................................................................6

3.1 Overhead costs to production and service cost centres as per allocation and apportionment

......................................................................................................................................................6

3.2 Analysis of rates in accordance with adequate bases of absorption......................................6

3.3 Treatment of under or over recovered overhead costs in accordance with established

procedures....................................................................................................................................6

Over and under absorption: -.......................................................................................................7

3.4 Methods of allocation, apportionment and absorption at regular intervals...........................7

3.5 Execution with staff to resolve the questions in overhead cost data......................................7

TASK 4............................................................................................................................................8

4.1 Comparison of budget with actual budget cost and variances...............................................8

4.2 Analysis of variances for management reports......................................................................8

4.3 Information for budget holders of significant variances making suggestions remedial

actions..........................................................................................................................................8

4.4 Formation of management report in a proper format, presenting timescales........................9

TASK 5............................................................................................................................................9

5.1 Future income and costs for decision making using..............................................................9

5.2 Effect of changing activity levels on unit cost.....................................................................10

5.3 Evaluation of factors affecting short term and long-term decision making.........................10

5.4 Factors affecting short-term and long-term decision making..............................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

TASK 5............................................................................................................................................9

5.1 Future income and costs for decision making using..............................................................9

5.2 Effect of changing activity levels on unit cost.....................................................................10

5.3 Evaluation of factors affecting short term and long-term decision making.........................10

5.4 Factors affecting short-term and long-term decision making..............................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost indicates towards expensed incurred for a particular event, transaction in

organisational context. Revenue is recognised as a consideration of levied expenses in operations

(Amico, Chilingerian and Van Hasselt, 2014). Nature and role of costing system with in

organisational context are defined in this report. Cost records and applications are also analysed

with in organisational context. It contains the appropriation of cost according to organisational

requirements. Cost and revenues with proper organisational requirements are also considered in

this report. Allocation and appropriation cost by applying accounting concepts and observations

are also analysed with practical based examples. Use of information generated form costing

system for decision making also defined in this report.

TASK 1

1.1 The purpose of internal reporting and providing accurate information to management

Motivation behind inner detailing: Internal revealing is directed in all the business

elements to dissect that association is performing great or not. In the event that it isn't great, key

choices can be taken by the supervisors so as to enhance it.

Reason for giving exact data to the board: It is essential to give precise, solid and fitting

data to the administration. Fundamental motivation behind this, is to encourage administrators in

settling on right choices for business and its improvement.

1.2 Relationship between the various costing systems with in business

All the business elements utilize two noteworthy sort of costing framework these are

employment and process costing frameworks. Them two are interrelated with one another. In

employment costing material, work and overheads are recorded for each errand which is

performed by the organization. In second strategy every one of these components are deciphered

for whole creation methodology (Elliott and Santos, 2012).

At the point when chiefs have any issue seeing generation process as brief data is

recorded in it, at that point work costing can be utilized to get proper data for each cost

consequently both are identified with one another.

1

Cost indicates towards expensed incurred for a particular event, transaction in

organisational context. Revenue is recognised as a consideration of levied expenses in operations

(Amico, Chilingerian and Van Hasselt, 2014). Nature and role of costing system with in

organisational context are defined in this report. Cost records and applications are also analysed

with in organisational context. It contains the appropriation of cost according to organisational

requirements. Cost and revenues with proper organisational requirements are also considered in

this report. Allocation and appropriation cost by applying accounting concepts and observations

are also analysed with practical based examples. Use of information generated form costing

system for decision making also defined in this report.

TASK 1

1.1 The purpose of internal reporting and providing accurate information to management

Motivation behind inner detailing: Internal revealing is directed in all the business

elements to dissect that association is performing great or not. In the event that it isn't great, key

choices can be taken by the supervisors so as to enhance it.

Reason for giving exact data to the board: It is essential to give precise, solid and fitting

data to the administration. Fundamental motivation behind this, is to encourage administrators in

settling on right choices for business and its improvement.

1.2 Relationship between the various costing systems with in business

All the business elements utilize two noteworthy sort of costing framework these are

employment and process costing frameworks. Them two are interrelated with one another. In

employment costing material, work and overheads are recorded for each errand which is

performed by the organization. In second strategy every one of these components are deciphered

for whole creation methodology (Elliott and Santos, 2012).

At the point when chiefs have any issue seeing generation process as brief data is

recorded in it, at that point work costing can be utilized to get proper data for each cost

consequently both are identified with one another.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 the responsibility centres, cost centres and investment centres with in organisation

Responsibility centre: It is subunit of an organization for which a director has duty and

expert. These are the diverse useful offices inside an association, for example, back, advertising,

human asset, IT and so on.

Cost centre: It is a cost division of a business element in which all the staff individuals

and chiefs are in charge of costs related choices not incomes. It incorporates creation, support

and quality control divisions.

Benefit centre: It is a focal piece of an undertaking which is mindful to make higher

commitment in hierarchical benefits. It incorporates moving division of the organization.

Venture centre: It is an interior division of an association which uses capital and assets

suitably so as to improve generally speaking productivity of the organization. sales and

assembling offices are considered as the piece of this middle (Gillen and Mantin, 2014).

1.4 The characteristics of various kind of cost classifications and its use in costing

There are five kinds of cost characterizations essentially, in connection to cost focus, by

time, for basic leadership and ordinarily of generation process. Attributes of every one of them

are as per the following:

It settles on best choices for the association by isolating expenses in different parts.

All the arranged costs measures costs that may happen in future and afterwards

supervisors can design ahead of time to tolerate them.

Budgeted expenses are utilized to decide each cost which has been happened in

assembling process.

Employments of arrangement of expenses:

These are additionally used to designate suitable assets to various practical divisions of

the organization as indicated by their necessities by dissecting their expenses.

1.5 The difference between marginal and absorption costing

Marginal costing Absorption costing

This method helps to categorise the cost in

fixed and variable streams in different ways.

This costing method helps in determining the

profit by absorbing fixed manufacturing

expenses in production process.

This costing method is also used in decision This costing method is not considered viable

2

Responsibility centre: It is subunit of an organization for which a director has duty and

expert. These are the diverse useful offices inside an association, for example, back, advertising,

human asset, IT and so on.

Cost centre: It is a cost division of a business element in which all the staff individuals

and chiefs are in charge of costs related choices not incomes. It incorporates creation, support

and quality control divisions.

Benefit centre: It is a focal piece of an undertaking which is mindful to make higher

commitment in hierarchical benefits. It incorporates moving division of the organization.

Venture centre: It is an interior division of an association which uses capital and assets

suitably so as to improve generally speaking productivity of the organization. sales and

assembling offices are considered as the piece of this middle (Gillen and Mantin, 2014).

1.4 The characteristics of various kind of cost classifications and its use in costing

There are five kinds of cost characterizations essentially, in connection to cost focus, by

time, for basic leadership and ordinarily of generation process. Attributes of every one of them

are as per the following:

It settles on best choices for the association by isolating expenses in different parts.

All the arranged costs measures costs that may happen in future and afterwards

supervisors can design ahead of time to tolerate them.

Budgeted expenses are utilized to decide each cost which has been happened in

assembling process.

Employments of arrangement of expenses:

These are additionally used to designate suitable assets to various practical divisions of

the organization as indicated by their necessities by dissecting their expenses.

1.5 The difference between marginal and absorption costing

Marginal costing Absorption costing

This method helps to categorise the cost in

fixed and variable streams in different ways.

This costing method helps in determining the

profit by absorbing fixed manufacturing

expenses in production process.

This costing method is also used in decision This costing method is not considered viable

2

making and strategic planning. and formal in order to managing the decisions

and strategic plannig.

TASK 2

2.1 Cost details for labour, material and expenses as per the organisation's costing procedure

Costing technique executed in any association characterizes as a movement of chronicle

costs in fitting records with the goal that real expense can be determined for assembling process

as an individual premise and for entire assembling process (Kimball, 2014). In any association,

there are different sort of costs that are brought about because of business activities. These are

material, work and costs.

Material expense:

Material expense shift as indicated by the yield level yet it stays same per unit of yield. It

incorporates cost of crude materials that are obtained by the association from the market to

deliver yield.

Labour Cost:

Works are the labourers of an element that is occupied with delivering the yield and

substance offers wages to them. These wages are called work cost, this expense is same per unit

of yield yet it changes whenever yield level increments all in all.

Direct Costs:

There are two sorts of costs which is immediate costs and circuitous costs, coordinate

costs caused specifically on a specific item. Then again, roundabout costs are caused on all in all

for the association and it is additionally called as overhead. It tends to be settled overhead and

can be variable overhead.

2.2 Analysis of cost information as labour, material and expenses as per the organisation's

costing procedure

This would rely on total item that are made within the company if it would reduce or

increase then wages paid to work forces that will changes as per the units of production (Kong,

Bayram and Devetsikiotis, 2015). There are certain types of expense that are faced by every

business organization while manufacturing items. Few of them are fixed as well as variables cost

such as rent, depreciation and insurance premium etc.

3

and strategic plannig.

TASK 2

2.1 Cost details for labour, material and expenses as per the organisation's costing procedure

Costing technique executed in any association characterizes as a movement of chronicle

costs in fitting records with the goal that real expense can be determined for assembling process

as an individual premise and for entire assembling process (Kimball, 2014). In any association,

there are different sort of costs that are brought about because of business activities. These are

material, work and costs.

Material expense:

Material expense shift as indicated by the yield level yet it stays same per unit of yield. It

incorporates cost of crude materials that are obtained by the association from the market to

deliver yield.

Labour Cost:

Works are the labourers of an element that is occupied with delivering the yield and

substance offers wages to them. These wages are called work cost, this expense is same per unit

of yield yet it changes whenever yield level increments all in all.

Direct Costs:

There are two sorts of costs which is immediate costs and circuitous costs, coordinate

costs caused specifically on a specific item. Then again, roundabout costs are caused on all in all

for the association and it is additionally called as overhead. It tends to be settled overhead and

can be variable overhead.

2.2 Analysis of cost information as labour, material and expenses as per the organisation's

costing procedure

This would rely on total item that are made within the company if it would reduce or

increase then wages paid to work forces that will changes as per the units of production (Kong,

Bayram and Devetsikiotis, 2015). There are certain types of expense that are faced by every

business organization while manufacturing items. Few of them are fixed as well as variables cost

such as rent, depreciation and insurance premium etc.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

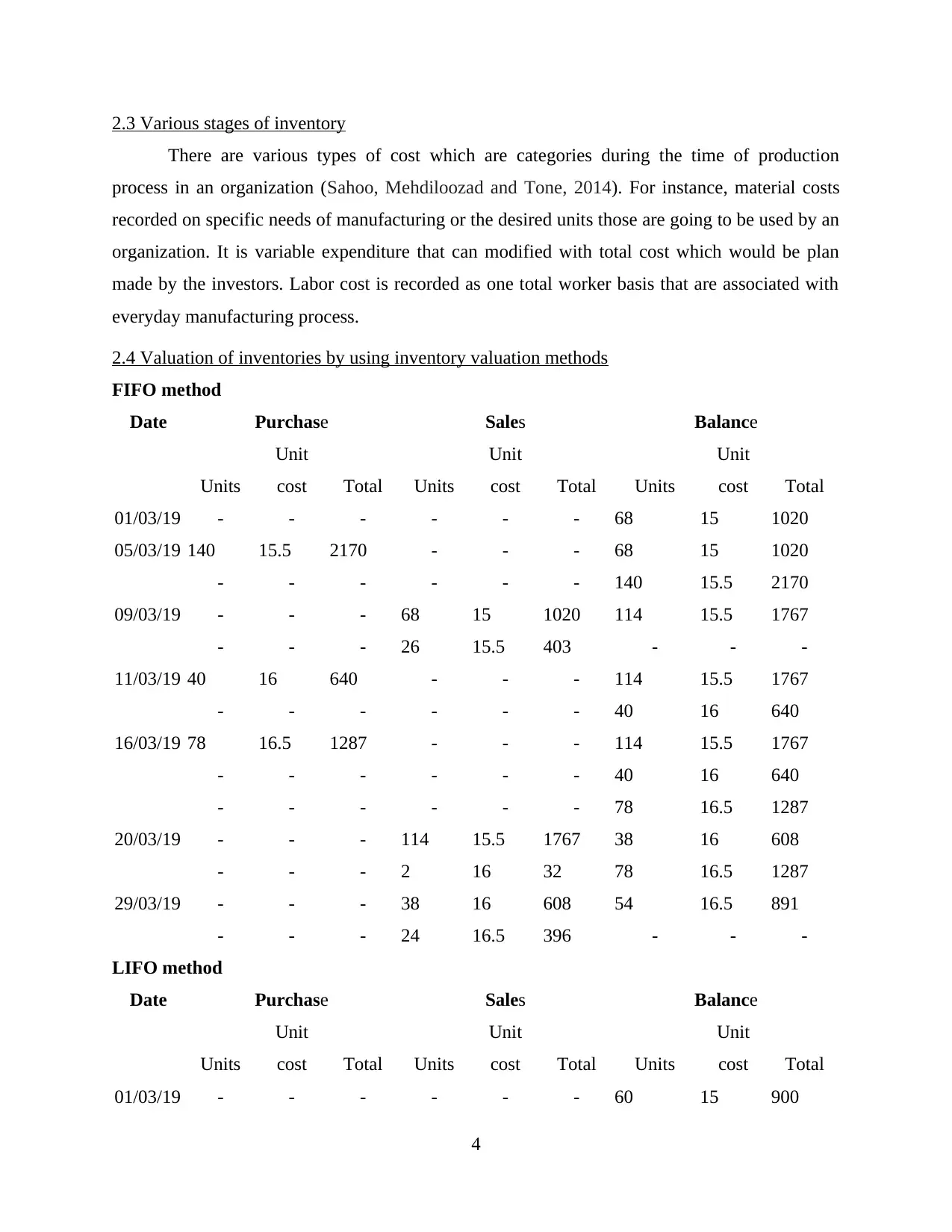

2.3 Various stages of inventory

There are various types of cost which are categories during the time of production

process in an organization (Sahoo, Mehdiloozad and Tone, 2014). For instance, material costs

recorded on specific needs of manufacturing or the desired units those are going to be used by an

organization. It is variable expenditure that can modified with total cost which would be plan

made by the investors. Labor cost is recorded as one total worker basis that are associated with

everyday manufacturing process.

2.4 Valuation of inventories by using inventory valuation methods

FIFO method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 68 15 1020

05/03/19 140 15.5 2170 - - - 68 15 1020

- - - - - - 140 15.5 2170

09/03/19 - - - 68 15 1020 114 15.5 1767

- - - 26 15.5 403 - - -

11/03/19 40 16 640 - - - 114 15.5 1767

- - - - - - 40 16 640

16/03/19 78 16.5 1287 - - - 114 15.5 1767

- - - - - - 40 16 640

- - - - - - 78 16.5 1287

20/03/19 - - - 114 15.5 1767 38 16 608

- - - 2 16 32 78 16.5 1287

29/03/19 - - - 38 16 608 54 16.5 891

- - - 24 16.5 396 - - -

LIFO method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 60 15 900

4

There are various types of cost which are categories during the time of production

process in an organization (Sahoo, Mehdiloozad and Tone, 2014). For instance, material costs

recorded on specific needs of manufacturing or the desired units those are going to be used by an

organization. It is variable expenditure that can modified with total cost which would be plan

made by the investors. Labor cost is recorded as one total worker basis that are associated with

everyday manufacturing process.

2.4 Valuation of inventories by using inventory valuation methods

FIFO method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 68 15 1020

05/03/19 140 15.5 2170 - - - 68 15 1020

- - - - - - 140 15.5 2170

09/03/19 - - - 68 15 1020 114 15.5 1767

- - - 26 15.5 403 - - -

11/03/19 40 16 640 - - - 114 15.5 1767

- - - - - - 40 16 640

16/03/19 78 16.5 1287 - - - 114 15.5 1767

- - - - - - 40 16 640

- - - - - - 78 16.5 1287

20/03/19 - - - 114 15.5 1767 38 16 608

- - - 2 16 32 78 16.5 1287

29/03/19 - - - 38 16 608 54 16.5 891

- - - 24 16.5 396 - - -

LIFO method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 60 15 900

4

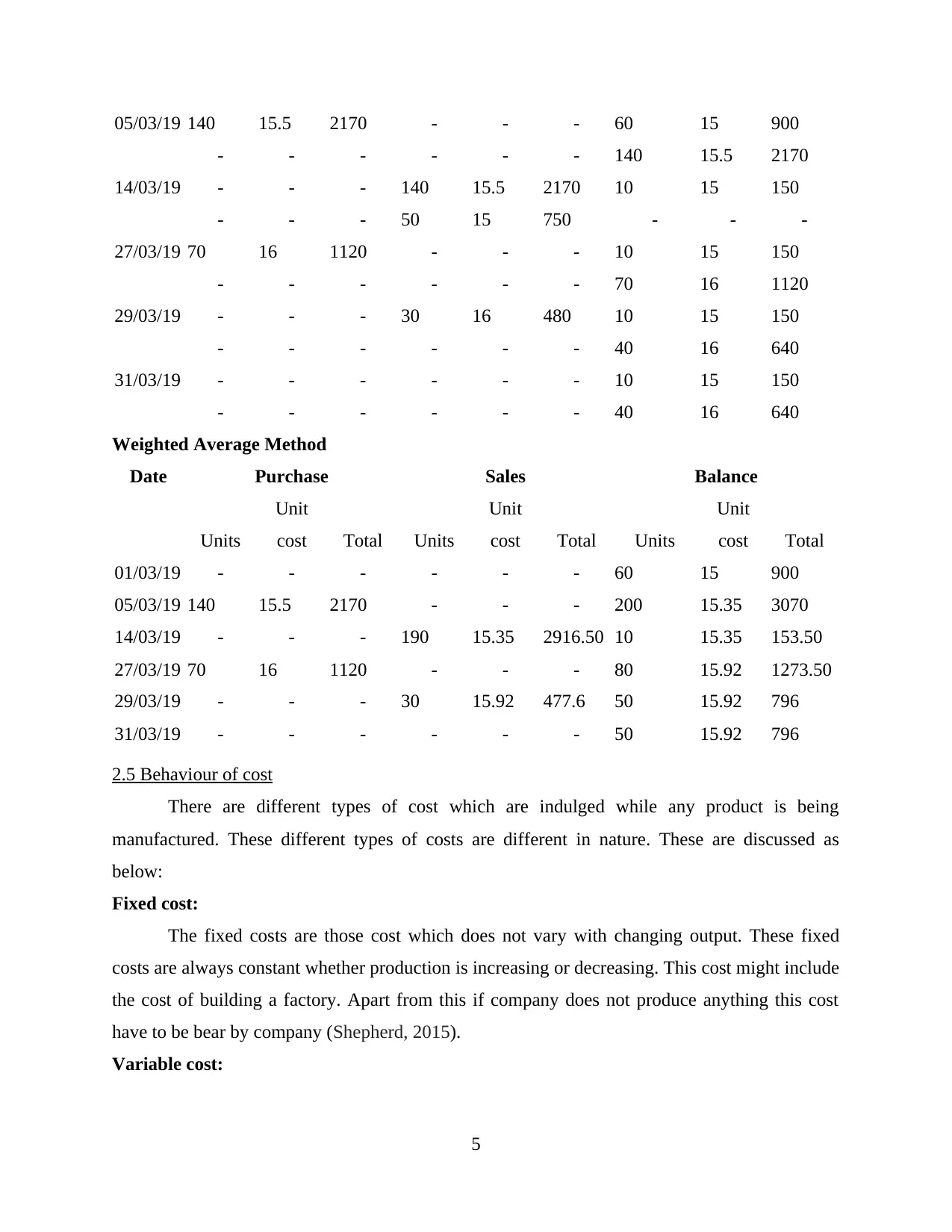

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

05/03/19 140 15.5 2170 - - - 60 15 900

- - - - - - 140 15.5 2170

14/03/19 - - - 140 15.5 2170 10 15 150

- - - 50 15 750 - - -

27/03/19 70 16 1120 - - - 10 15 150

- - - - - - 70 16 1120

29/03/19 - - - 30 16 480 10 15 150

- - - - - - 40 16 640

31/03/19 - - - - - - 10 15 150

- - - - - - 40 16 640

Weighted Average Method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 60 15 900

05/03/19 140 15.5 2170 - - - 200 15.35 3070

14/03/19 - - - 190 15.35 2916.50 10 15.35 153.50

27/03/19 70 16 1120 - - - 80 15.92 1273.50

29/03/19 - - - 30 15.92 477.6 50 15.92 796

31/03/19 - - - - - - 50 15.92 796

2.5 Behaviour of cost

There are different types of cost which are indulged while any product is being

manufactured. These different types of costs are different in nature. These are discussed as

below:

Fixed cost:

The fixed costs are those cost which does not vary with changing output. These fixed

costs are always constant whether production is increasing or decreasing. This cost might include

the cost of building a factory. Apart from this if company does not produce anything this cost

have to be bear by company (Shepherd, 2015).

Variable cost:

5

- - - - - - 140 15.5 2170

14/03/19 - - - 140 15.5 2170 10 15 150

- - - 50 15 750 - - -

27/03/19 70 16 1120 - - - 10 15 150

- - - - - - 70 16 1120

29/03/19 - - - 30 16 480 10 15 150

- - - - - - 40 16 640

31/03/19 - - - - - - 10 15 150

- - - - - - 40 16 640

Weighted Average Method

Date Purchase Sales Balance

Units

Unit

cost Total Units

Unit

cost Total Units

Unit

cost Total

01/03/19 - - - - - - 60 15 900

05/03/19 140 15.5 2170 - - - 200 15.35 3070

14/03/19 - - - 190 15.35 2916.50 10 15.35 153.50

27/03/19 70 16 1120 - - - 80 15.92 1273.50

29/03/19 - - - 30 15.92 477.6 50 15.92 796

31/03/19 - - - - - - 50 15.92 796

2.5 Behaviour of cost

There are different types of cost which are indulged while any product is being

manufactured. These different types of costs are different in nature. These are discussed as

below:

Fixed cost:

The fixed costs are those cost which does not vary with changing output. These fixed

costs are always constant whether production is increasing or decreasing. This cost might include

the cost of building a factory. Apart from this if company does not produce anything this cost

have to be bear by company (Shepherd, 2015).

Variable cost:

5

Variable costs are those which always keep changing and it totally depend on the output

produced. If company produced more than they have to pay more and similarly if they pay less

than company needs to pay less.

Semi variable cost:

A labour might be a semi variable cost. For example if a company produces car than they

need more workers and that is variable cost (Shoup, 2017). Therefore, even if company does not

produce any car than also they have to need some worker to look after empty factory.

2.6 Cost information by using costing system

Administration: In this costing method costs identified with each administration

rendered by an organization is recorded. It is basically utilized in cordiality industry.

Batch: This strategy is utilized to accept homogeneous items as cost unit for association.

In this costing system a bunch incorporates a specific number of things or articles (Stiglitz and

Rosengard, 2015).

Job: In employment costing strategy expenses of each errand which is performed by the

association is recorded. Administrators may get nitty gritty data of costs that have occurred for

that are looked by the organization.

Process: Costs identified with generation process is recorded in this strategy. It is

fundamentally utilized in those organizations which makes items in substantial amounts.

Unit: In this framework cost that has occurred for assembling a particular unit of item is

recorded. All settled and variable costs identified with one thing is considered in this strategy.

TASK 3

3.1 Overhead costs to production and service cost centres as per allocation and apportionment

Material expenses are recorded based on absolute prerequisite of generation or the ideal

units that will be produced by the organization. It is a variable cost that changes with all out

generation units. Work cost is recorded based on complete labourers who are associated with

assembling process.

3.2 Analysis of rates in accordance with adequate bases of absorption

Machine Hours : -

Overhead absorption rate = Estimated Factory Overheads / Estimated machine hours * 100

= $150000 / 25000 * 100

6

produced. If company produced more than they have to pay more and similarly if they pay less

than company needs to pay less.

Semi variable cost:

A labour might be a semi variable cost. For example if a company produces car than they

need more workers and that is variable cost (Shoup, 2017). Therefore, even if company does not

produce any car than also they have to need some worker to look after empty factory.

2.6 Cost information by using costing system

Administration: In this costing method costs identified with each administration

rendered by an organization is recorded. It is basically utilized in cordiality industry.

Batch: This strategy is utilized to accept homogeneous items as cost unit for association.

In this costing system a bunch incorporates a specific number of things or articles (Stiglitz and

Rosengard, 2015).

Job: In employment costing strategy expenses of each errand which is performed by the

association is recorded. Administrators may get nitty gritty data of costs that have occurred for

that are looked by the organization.

Process: Costs identified with generation process is recorded in this strategy. It is

fundamentally utilized in those organizations which makes items in substantial amounts.

Unit: In this framework cost that has occurred for assembling a particular unit of item is

recorded. All settled and variable costs identified with one thing is considered in this strategy.

TASK 3

3.1 Overhead costs to production and service cost centres as per allocation and apportionment

Material expenses are recorded based on absolute prerequisite of generation or the ideal

units that will be produced by the organization. It is a variable cost that changes with all out

generation units. Work cost is recorded based on complete labourers who are associated with

assembling process.

3.2 Analysis of rates in accordance with adequate bases of absorption

Machine Hours : -

Overhead absorption rate = Estimated Factory Overheads / Estimated machine hours * 100

= $150000 / 25000 * 100

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= $600

Labour Hours : -

Overhead absorption rate = Estimated Factory Overheads / Estimated labour hours * 100

= $150000 / 30000 * 100

= $500

3.3 Treatment of under or over recovered overhead costs in accordance with established

procedures

Normal working hours = No of machines*No of working hour per week*No of work per week

= 28*42*48

= 56448

Loss of hours on maintenance = No of machines*No of hour loss on maintenance per week*No

of work per week

= 28*5*48

= 6720

Annual effective working hours = Normal working hours - Loss of hours on maintenance

= 56448 - 6720

= 49728

Machine hours = Estimated annual overhead / Estimated working hours

= 124320/49728

= £2.5 per hours.

Over and under absorption: -

Over absorption = Machine hours produce – Overhead incurred

= (4200*2.5) – £10200

= £10500-£10200

= £300

Under absorption = Wages absorption – Wages incurred

= (28*42*4 @ £1.50) - £7400

= £7056 – £7400

= £344

7

Labour Hours : -

Overhead absorption rate = Estimated Factory Overheads / Estimated labour hours * 100

= $150000 / 30000 * 100

= $500

3.3 Treatment of under or over recovered overhead costs in accordance with established

procedures

Normal working hours = No of machines*No of working hour per week*No of work per week

= 28*42*48

= 56448

Loss of hours on maintenance = No of machines*No of hour loss on maintenance per week*No

of work per week

= 28*5*48

= 6720

Annual effective working hours = Normal working hours - Loss of hours on maintenance

= 56448 - 6720

= 49728

Machine hours = Estimated annual overhead / Estimated working hours

= 124320/49728

= £2.5 per hours.

Over and under absorption: -

Over absorption = Machine hours produce – Overhead incurred

= (4200*2.5) – £10200

= £10500-£10200

= £300

Under absorption = Wages absorption – Wages incurred

= (28*42*4 @ £1.50) - £7400

= £7056 – £7400

= £344

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.4 Methods of allocation, apportionment and absorption at regular intervals

Square footage: This helps in managing the rent and other expense's allocation.

Machine time: This method helps to determine the cost by evaluating the machine hours.

Direct labour: This method helps to analyse the cost by bifurcating the direct labour and

cost (Sufian and Kamarudin, 2015).

3.5 Execution with staff to resolve the questions in overhead cost data

Communication regarding the budgeted overheads and expenses for staff member for

making strategies and policies. For each director it is vital to determine every one of the inquiries

that are identified with overhead cost information so it tends to be investigated that every one of

them are significant to generation or not. The data can be assembled by directing a formal

gathering or assessing reports that are created by the labourers.

TASK 4

4.1 Comparison of budget with actual budget cost and variances

Budget costing is a money related arrangement which incorporates budgetary and non-

monetary information. The primary component of Budget costing is to pre-decide income and

costs. It is important to plan Budget plan so we can make a decision in which division what

measure of cash ought to be spend as abundance Budget lead towards negative effect on

association (Wang and et. al., 2015). Where as genuine costing can be characterized as cost

bookkeeping framework which utilizes exact information, real characteristics utilized in

assembling procedure to discover the expense of explicit items. In real cost, costs are sure and

determined by required material.

4.2 Analysis of variances for management reports

Material cost variance= Total budgeted cost- total actual cost

=21750-20720

=1030(F)

Material price variance= SP-AP*(AQ)

For A: 60-60*180= 0

For B: 65-62*160= 480(F)

MPV= 480(F)

Material usage variance= SQ-AQ*(SP)

8

Square footage: This helps in managing the rent and other expense's allocation.

Machine time: This method helps to determine the cost by evaluating the machine hours.

Direct labour: This method helps to analyse the cost by bifurcating the direct labour and

cost (Sufian and Kamarudin, 2015).

3.5 Execution with staff to resolve the questions in overhead cost data

Communication regarding the budgeted overheads and expenses for staff member for

making strategies and policies. For each director it is vital to determine every one of the inquiries

that are identified with overhead cost information so it tends to be investigated that every one of

them are significant to generation or not. The data can be assembled by directing a formal

gathering or assessing reports that are created by the labourers.

TASK 4

4.1 Comparison of budget with actual budget cost and variances

Budget costing is a money related arrangement which incorporates budgetary and non-

monetary information. The primary component of Budget costing is to pre-decide income and

costs. It is important to plan Budget plan so we can make a decision in which division what

measure of cash ought to be spend as abundance Budget lead towards negative effect on

association (Wang and et. al., 2015). Where as genuine costing can be characterized as cost

bookkeeping framework which utilizes exact information, real characteristics utilized in

assembling procedure to discover the expense of explicit items. In real cost, costs are sure and

determined by required material.

4.2 Analysis of variances for management reports

Material cost variance= Total budgeted cost- total actual cost

=21750-20720

=1030(F)

Material price variance= SP-AP*(AQ)

For A: 60-60*180= 0

For B: 65-62*160= 480(F)

MPV= 480(F)

Material usage variance= SQ-AQ*(SP)

8

For A: 200-180*60= 1200(F)

For B: 150-160*65= 650(A)

MPV= 550(F)

4.3 Information for budget holders of significant variances making suggestions remedial actions

There are three primary sorts of differences these are material cost, cost and utilization

fluctuations. Every one of them are vital for spending holders since it might control them to

dissect that their estimations have met the genuine outcomes (Yang and Chen, 2018). On the off

chance that there is any fluctuations, they can influence changes in their methodologies with the

goal that suitable anticipating to can be made for future period. It will be extremely advantageous

for them as it can assist them with allotting right assets to useful branches of the organization

4.4 Formation of management report in a proper format, presenting timescales

A time scale for acquiring elements of variances is as follows:

Activity Time

Budgeted

Material 6 Days

Labour 10 Days

Actual

Material 5 Days

Labour 10 Days

TASK 5

5.1 Future income and costs for decision making using

Break even analysis: It refers to the methodology which can be utilising for estimating

the stages where all relevant costs may be recovering and business entity may reach to the level

where no earned are purchased and no losses are incurred.

Discounted cash flow: It is an approximation method which is required to assume

possible returns on a particular investment.

Limiting factors: Shortfall of labour, machine hours and materials etc. are constrictive

factors of organization.

9

For B: 150-160*65= 650(A)

MPV= 550(F)

4.3 Information for budget holders of significant variances making suggestions remedial actions

There are three primary sorts of differences these are material cost, cost and utilization

fluctuations. Every one of them are vital for spending holders since it might control them to

dissect that their estimations have met the genuine outcomes (Yang and Chen, 2018). On the off

chance that there is any fluctuations, they can influence changes in their methodologies with the

goal that suitable anticipating to can be made for future period. It will be extremely advantageous

for them as it can assist them with allotting right assets to useful branches of the organization

4.4 Formation of management report in a proper format, presenting timescales

A time scale for acquiring elements of variances is as follows:

Activity Time

Budgeted

Material 6 Days

Labour 10 Days

Actual

Material 5 Days

Labour 10 Days

TASK 5

5.1 Future income and costs for decision making using

Break even analysis: It refers to the methodology which can be utilising for estimating

the stages where all relevant costs may be recovering and business entity may reach to the level

where no earned are purchased and no losses are incurred.

Discounted cash flow: It is an approximation method which is required to assume

possible returns on a particular investment.

Limiting factors: Shortfall of labour, machine hours and materials etc. are constrictive

factors of organization.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.