Financial Analysis of Finance in Hospitality Industry Report

VerifiedAdded on 2020/07/23

|18

|4323

|22

Report

AI Summary

This report provides a comprehensive analysis of financial aspects within the hospitality industry. It begins by exploring various internal and external sources of funding available for businesses, particularly focusing on a steel spoon manufacturer named Ciprian. The report then delves into revenue generation strategies for restaurants, including increasing customer base, transaction size, and frequency, as well as pricing and quantity adjustments. It includes detailed financial statements, including a profit and loss account and balance sheet for R Rigs, alongside ratio analysis to evaluate the financial performance. Furthermore, the report addresses cost control methods, budgetary control processes, and variance analysis with suggestions for improvement. It also covers different cost categories and the cost-volume-profit relationship, culminating in a justification of management decisions based on profit and loss calculations and break-even analysis. The report utilizes PPTs to explain certain elements. Finally, the report provides a detailed financial overview of the hospitality industry, covering funding sources, revenue generation, cost management, and financial analysis.

Finance In Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Available sources of funding for Business and service industries........................................1

1.2 Various methods of generating income by a restaurant........................................................3

TASK 2............................................................................................................................................4

2.1 Elements related to Cost, Gross profit and selling price.......................................................4

2.2 Various methods of controlling cash and stock in business environment............................4

TASK 3............................................................................................................................................4

3.3 Budgetary control and its process.........................................................................................4

3.4 Analysing variances between actual results and budgeted results along with suggestions. .4

TASK 4............................................................................................................................................4

3.1 Different structure and sources of trial balance....................................................................4

3.2 analysing of business accounts, notes and adjustments........................................................6

4.1 Calculation and analysis of ratios.........................................................................................8

4.2 Recommending appropriate management strategies for future............................................9

TASK 5..........................................................................................................................................10

5.1 Different categories of cost.................................................................................................10

5.2 Calculation of contribution and explanation of cost volume profit relationship................11

5.3 Justification of management decision on the basis of calculation of profit and loss and

break-even.................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Available sources of funding for Business and service industries........................................1

1.2 Various methods of generating income by a restaurant........................................................3

TASK 2............................................................................................................................................4

2.1 Elements related to Cost, Gross profit and selling price.......................................................4

2.2 Various methods of controlling cash and stock in business environment............................4

TASK 3............................................................................................................................................4

3.3 Budgetary control and its process.........................................................................................4

3.4 Analysing variances between actual results and budgeted results along with suggestions. .4

TASK 4............................................................................................................................................4

3.1 Different structure and sources of trial balance....................................................................4

3.2 analysing of business accounts, notes and adjustments........................................................6

4.1 Calculation and analysis of ratios.........................................................................................8

4.2 Recommending appropriate management strategies for future............................................9

TASK 5..........................................................................................................................................10

5.1 Different categories of cost.................................................................................................10

5.2 Calculation of contribution and explanation of cost volume profit relationship................11

5.3 Justification of management decision on the basis of calculation of profit and loss and

break-even.................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Finance is the life line of any business. A business cannot be operated in the best manner

until and unless, there is the availability of adequate finance. Thus, in this report necessity of

finance in Hospitality industry has been evaluated by discussing various factors. The report

focuses on various internal and external sources of funds that can be raised for further investment

in the business. Further, various methods from where a restaurant can gather its revenue are

identified along with some strategies that can help in increasing in revenue. It also talks about

budgeted results and actual results along with providing reasons and suggestions for mitigating

variances among them for Ciprian who is steel spoon manufacturer. Under this report financial

statements has been prepared for r Rigs along with their analysis using ratio analysis tool.

TASK 1

1.1 Available sources of funding for Business and service industries

In order to start any business, funds are required for the operation of business activities

and for the purpose of capital expansion (Jang and Park, 2011). A sole trader find it difficult to

expand his business or to allocate funds for capital expansion. However, capital expenditure may

be financed through various external as well as internal sources. Increased ways of financing,

also increases difficulty in making decisions regarding investment appraisal technique, etc.

Therefore, being a sole trader of a small business, funds can be raised from various sources for

the purpose of purchasing a new building, costing to £450,000. According to given scenario,

Ciprian can use some effective source of funds which can be very useful for the organisation. In

order to expand their business, they are use following sources of the funds:

Internal sources of Funds

Personal savings: Initial source of fund is use of personal savings. Sole trader can use

his personal savings for the purchase of new building, this will increase its capital

investment in the business. According to given scenario Ciprian should start their saving

from the business.

1

Finance is the life line of any business. A business cannot be operated in the best manner

until and unless, there is the availability of adequate finance. Thus, in this report necessity of

finance in Hospitality industry has been evaluated by discussing various factors. The report

focuses on various internal and external sources of funds that can be raised for further investment

in the business. Further, various methods from where a restaurant can gather its revenue are

identified along with some strategies that can help in increasing in revenue. It also talks about

budgeted results and actual results along with providing reasons and suggestions for mitigating

variances among them for Ciprian who is steel spoon manufacturer. Under this report financial

statements has been prepared for r Rigs along with their analysis using ratio analysis tool.

TASK 1

1.1 Available sources of funding for Business and service industries

In order to start any business, funds are required for the operation of business activities

and for the purpose of capital expansion (Jang and Park, 2011). A sole trader find it difficult to

expand his business or to allocate funds for capital expansion. However, capital expenditure may

be financed through various external as well as internal sources. Increased ways of financing,

also increases difficulty in making decisions regarding investment appraisal technique, etc.

Therefore, being a sole trader of a small business, funds can be raised from various sources for

the purpose of purchasing a new building, costing to £450,000. According to given scenario,

Ciprian can use some effective source of funds which can be very useful for the organisation. In

order to expand their business, they are use following sources of the funds:

Internal sources of Funds

Personal savings: Initial source of fund is use of personal savings. Sole trader can use

his personal savings for the purchase of new building, this will increase its capital

investment in the business. According to given scenario Ciprian should start their saving

from the business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained Profits: For the purchasing of new building funds can be taken form the

retained earnings of past profits by not distributing these profits among the shareholders

or in case of small business not withdrawing this profit amount. If company want to gain

more profit then they should follow the given scenario and they will be able to gain more

profit from the business. Increasing internal cash flow: Business can increase its internal cash flow by increasing

profit percentage on services and cutting of cost, selling of old assets which are least

required, by managing working capital, etc. Increased in cash flow then can be used for

the purchasing of new building (Walker, 2016).

External sources of Funds

Issuing share capital: Business can raise further capital by issuing shares in the market

or to the relatives. Issue can be made of ordinary shares, preference shares, rights issue,

etc. Ciprian company can issue their share for arrange the fund, and it is very useful

source of the fund.

Bank Overdraft: More funds can be raised by maintaining a negative balance at the

business bank account. This can become a long term source of finance and further

advantages of bank overdraft is flexibility and competitive interest rates. They can

borrow the fund from the bank overdraft and it is very secure source of the fund.

Term loan: Business can also take loan form financial institutions like banks and other

finance proving organisations at a fixed interest rate (Park and Jang, 2014). This option is

an easy source of finance. According to given scenario, company can borrow the term

loan from the banks or any other finance company.

Finance Lease: Under this option of funds raising, business can approach to financial

institution for the purchase of an asset by them, and then the asset is taken on lease by the

business by paying rents or instalments. According to given scenario they can use the

lease system of finance for borrow the fund, it is very useful source of the fund.

2

retained earnings of past profits by not distributing these profits among the shareholders

or in case of small business not withdrawing this profit amount. If company want to gain

more profit then they should follow the given scenario and they will be able to gain more

profit from the business. Increasing internal cash flow: Business can increase its internal cash flow by increasing

profit percentage on services and cutting of cost, selling of old assets which are least

required, by managing working capital, etc. Increased in cash flow then can be used for

the purchasing of new building (Walker, 2016).

External sources of Funds

Issuing share capital: Business can raise further capital by issuing shares in the market

or to the relatives. Issue can be made of ordinary shares, preference shares, rights issue,

etc. Ciprian company can issue their share for arrange the fund, and it is very useful

source of the fund.

Bank Overdraft: More funds can be raised by maintaining a negative balance at the

business bank account. This can become a long term source of finance and further

advantages of bank overdraft is flexibility and competitive interest rates. They can

borrow the fund from the bank overdraft and it is very secure source of the fund.

Term loan: Business can also take loan form financial institutions like banks and other

finance proving organisations at a fixed interest rate (Park and Jang, 2014). This option is

an easy source of finance. According to given scenario, company can borrow the term

loan from the banks or any other finance company.

Finance Lease: Under this option of funds raising, business can approach to financial

institution for the purchase of an asset by them, and then the asset is taken on lease by the

business by paying rents or instalments. According to given scenario they can use the

lease system of finance for borrow the fund, it is very useful source of the fund.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debt Factoring: Debts of business can be recovered by outsourcing to other agency.

This can increase cash assets by providing savings in credit management and certainty in

cash flows. An organisation provides a credit service to their customers, so they can take

action for the customers who are not paying their outstanding amount on time. So they

can arrange the fund from this types of sources.

However, being a small business, the best source of funding will be Bank Loan, which

would be easily available.

1.2 Various methods of generating income by a restaurant

Restaurant is a service providing organisation. The main service through which restaurant

generate its revenue is through providing meals to its customers. Therefore, to increase its

revenue, restaurant must focus on its customers (Arif, Noor-E-Jannat and Anwar, 2016). From

below mentioned four ways, restaurant can increase its revenue:

Increasing number of customers: Restaurant need to follow a strategy to attract more

and more customers to come atleast once at its place, them providing better quality service it can

retain customers. In order to attract more customers, various marketing strategies can be used

like, offering discounts, providing happy hours, advertising more and more, etc.

Increasing transaction size: This can be done through a process of upselling. This

mainly refers to making customers to purchase more. This can be done by offering more like

appetizers, drinks and desserts. More the variety in menu, more will be purchasing of customers.

Increasing the frequency of transaction: this includes encouraging customers to visit

the restaurant more often. For example, if averagely, customer comes once in a month,

encourage them to visit atleast twice in a month (Sargeant and Jay, 2014). More the transactions,

more will be revenue generation.

Raising prices or reducing Quantity: two cheap tricks of increasing revenue is by

raising the prices in the menu card or by reducing the quantity to be served. Increase in prices

3

This can increase cash assets by providing savings in credit management and certainty in

cash flows. An organisation provides a credit service to their customers, so they can take

action for the customers who are not paying their outstanding amount on time. So they

can arrange the fund from this types of sources.

However, being a small business, the best source of funding will be Bank Loan, which

would be easily available.

1.2 Various methods of generating income by a restaurant

Restaurant is a service providing organisation. The main service through which restaurant

generate its revenue is through providing meals to its customers. Therefore, to increase its

revenue, restaurant must focus on its customers (Arif, Noor-E-Jannat and Anwar, 2016). From

below mentioned four ways, restaurant can increase its revenue:

Increasing number of customers: Restaurant need to follow a strategy to attract more

and more customers to come atleast once at its place, them providing better quality service it can

retain customers. In order to attract more customers, various marketing strategies can be used

like, offering discounts, providing happy hours, advertising more and more, etc.

Increasing transaction size: This can be done through a process of upselling. This

mainly refers to making customers to purchase more. This can be done by offering more like

appetizers, drinks and desserts. More the variety in menu, more will be purchasing of customers.

Increasing the frequency of transaction: this includes encouraging customers to visit

the restaurant more often. For example, if averagely, customer comes once in a month,

encourage them to visit atleast twice in a month (Sargeant and Jay, 2014). More the transactions,

more will be revenue generation.

Raising prices or reducing Quantity: two cheap tricks of increasing revenue is by

raising the prices in the menu card or by reducing the quantity to be served. Increase in prices

3

will directly increase revenue and reduce in quantity will make customer to order more and

hence increase in revenue.

However, by using various strategic tactics also, restaurant business can increase their

sales. Following tactics are:

Food services

Food Quality and safety

Marketing

Creativity

Embracing technology

TASK 2

2.1 Elements related to Cost, Gross profit and selling price

Enclosed in PPT.

2.2 Various methods of controlling cash and stock in business environment

Enclosed in PPT.

TASK 3

3.3 Budgetary control and its process

Enclosed in PPT.

3.4 Analysing variances between actual results and budgeted results along with suggestions

Enclosed in PPT.

4

hence increase in revenue.

However, by using various strategic tactics also, restaurant business can increase their

sales. Following tactics are:

Food services

Food Quality and safety

Marketing

Creativity

Embracing technology

TASK 2

2.1 Elements related to Cost, Gross profit and selling price

Enclosed in PPT.

2.2 Various methods of controlling cash and stock in business environment

Enclosed in PPT.

TASK 3

3.3 Budgetary control and its process

Enclosed in PPT.

3.4 Analysing variances between actual results and budgeted results along with suggestions

Enclosed in PPT.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 4

3.1 Different structure and sources of trial balance

Structure of trial balance :-

A trial balance is a list and total of all the debit and credit accounts for an entity for a

given period usually a month. The format of the trial balance is a two column schedule with all

the debit balances listed in one column and all the credit balances listed in the other. The trial

balance is prepared after all the transactions for the period have been journalized and posted to

the general ledger. Key to preparing a trial balance is making sure that all the account balances

are listed under the correct column. The appropriate columns are as follows:

Equity = Credit balance

Assets = Debit balance

Liabilities = Credit balance

Revenue = Credit balance

Trial balance is a summary of the balances of all the ledger accounts. All the balancing

figures of different ledger accounts are then posted to the trail balance as per the nature of

accounts. Trial balance includes name of all the accounts along with their balancing figures on

debit side or credit side (Mason and Harrison, 2015). Debit balances show values of either assets

or expenses and credit balance show values of either incomes and liabilities. Mainly there are

two sources of Trial Balance that are as follows:

Journal entries: These are the recording of transactions that occur in a financial year in the books

of accounts.

Ledger accounts: Journal entries recorded are then posted to their respective ledger accounts and

then these ledger Accounts are balanced. Balancing figure i.e. the closing balance of each

account is then transferred to trial balance.

Below is the preparation of trail balance of adjustment entries:

5

3.1 Different structure and sources of trial balance

Structure of trial balance :-

A trial balance is a list and total of all the debit and credit accounts for an entity for a

given period usually a month. The format of the trial balance is a two column schedule with all

the debit balances listed in one column and all the credit balances listed in the other. The trial

balance is prepared after all the transactions for the period have been journalized and posted to

the general ledger. Key to preparing a trial balance is making sure that all the account balances

are listed under the correct column. The appropriate columns are as follows:

Equity = Credit balance

Assets = Debit balance

Liabilities = Credit balance

Revenue = Credit balance

Trial balance is a summary of the balances of all the ledger accounts. All the balancing

figures of different ledger accounts are then posted to the trail balance as per the nature of

accounts. Trial balance includes name of all the accounts along with their balancing figures on

debit side or credit side (Mason and Harrison, 2015). Debit balances show values of either assets

or expenses and credit balance show values of either incomes and liabilities. Mainly there are

two sources of Trial Balance that are as follows:

Journal entries: These are the recording of transactions that occur in a financial year in the books

of accounts.

Ledger accounts: Journal entries recorded are then posted to their respective ledger accounts and

then these ledger Accounts are balanced. Balancing figure i.e. the closing balance of each

account is then transferred to trial balance.

Below is the preparation of trail balance of adjustment entries:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

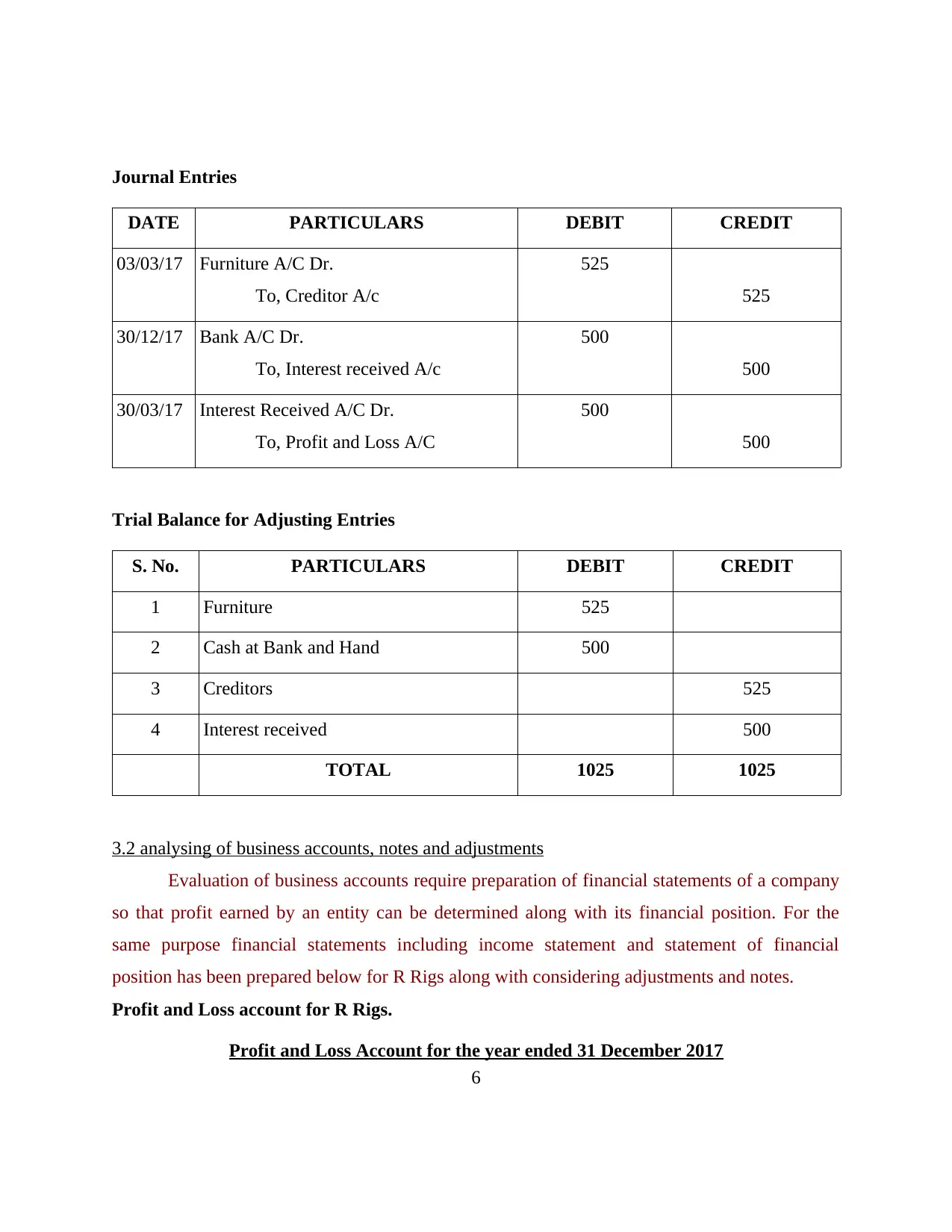

Journal Entries

DATE PARTICULARS DEBIT CREDIT

03/03/17 Furniture A/C Dr.

To, Creditor A/c

525

525

30/12/17 Bank A/C Dr.

To, Interest received A/c

500

500

30/03/17 Interest Received A/C Dr.

To, Profit and Loss A/C

500

500

Trial Balance for Adjusting Entries

S. No. PARTICULARS DEBIT CREDIT

1 Furniture 525

2 Cash at Bank and Hand 500

3 Creditors 525

4 Interest received 500

TOTAL 1025 1025

3.2 analysing of business accounts, notes and adjustments

Evaluation of business accounts require preparation of financial statements of a company

so that profit earned by an entity can be determined along with its financial position. For the

same purpose financial statements including income statement and statement of financial

position has been prepared below for R Rigs along with considering adjustments and notes.

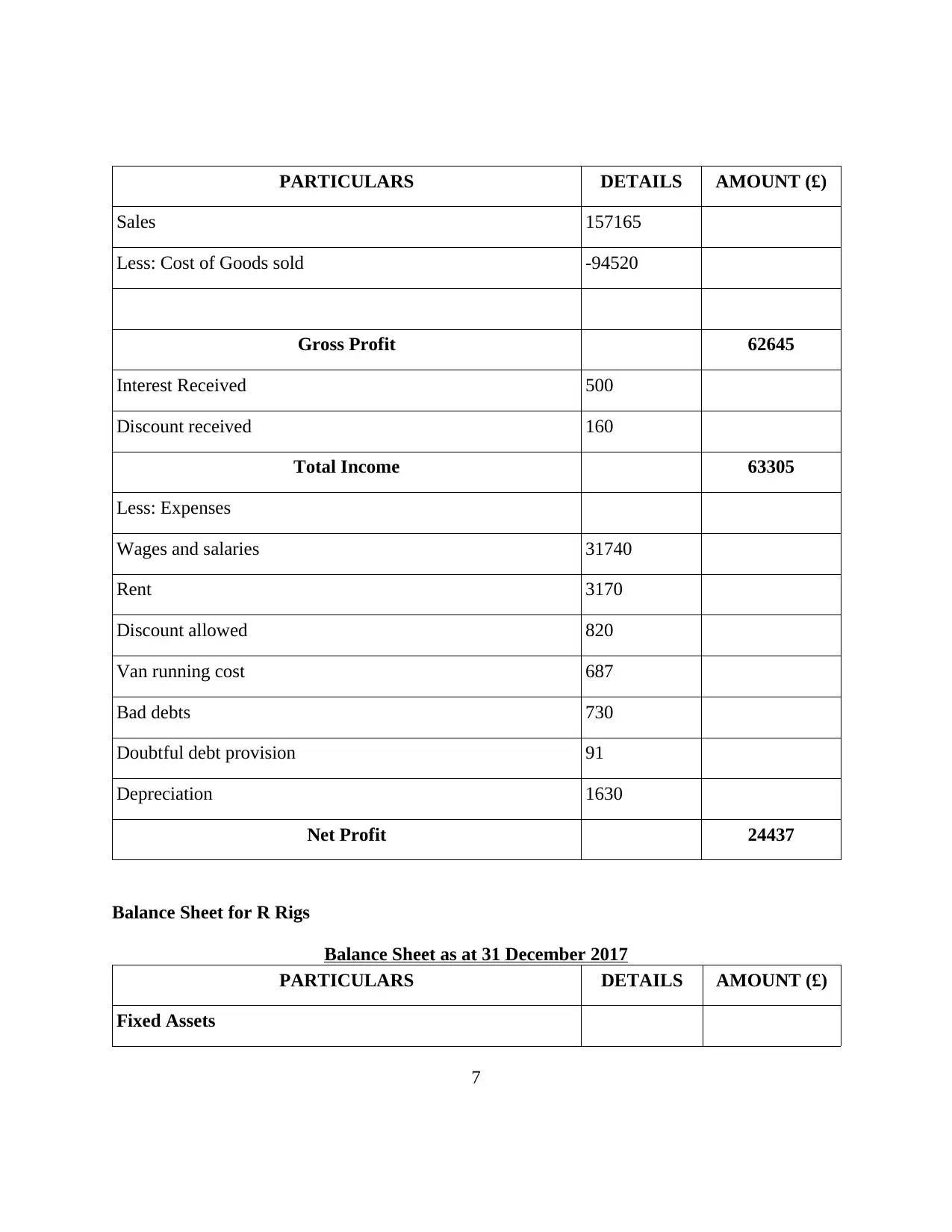

Profit and Loss account for R Rigs.

Profit and Loss Account for the year ended 31 December 2017

6

DATE PARTICULARS DEBIT CREDIT

03/03/17 Furniture A/C Dr.

To, Creditor A/c

525

525

30/12/17 Bank A/C Dr.

To, Interest received A/c

500

500

30/03/17 Interest Received A/C Dr.

To, Profit and Loss A/C

500

500

Trial Balance for Adjusting Entries

S. No. PARTICULARS DEBIT CREDIT

1 Furniture 525

2 Cash at Bank and Hand 500

3 Creditors 525

4 Interest received 500

TOTAL 1025 1025

3.2 analysing of business accounts, notes and adjustments

Evaluation of business accounts require preparation of financial statements of a company

so that profit earned by an entity can be determined along with its financial position. For the

same purpose financial statements including income statement and statement of financial

position has been prepared below for R Rigs along with considering adjustments and notes.

Profit and Loss account for R Rigs.

Profit and Loss Account for the year ended 31 December 2017

6

PARTICULARS DETAILS AMOUNT (£)

Sales 157165

Less: Cost of Goods sold -94520

Gross Profit 62645

Interest Received 500

Discount received 160

Total Income 63305

Less: Expenses

Wages and salaries 31740

Rent 3170

Discount allowed 820

Van running cost 687

Bad debts 730

Doubtful debt provision 91

Depreciation 1630

Net Profit 24437

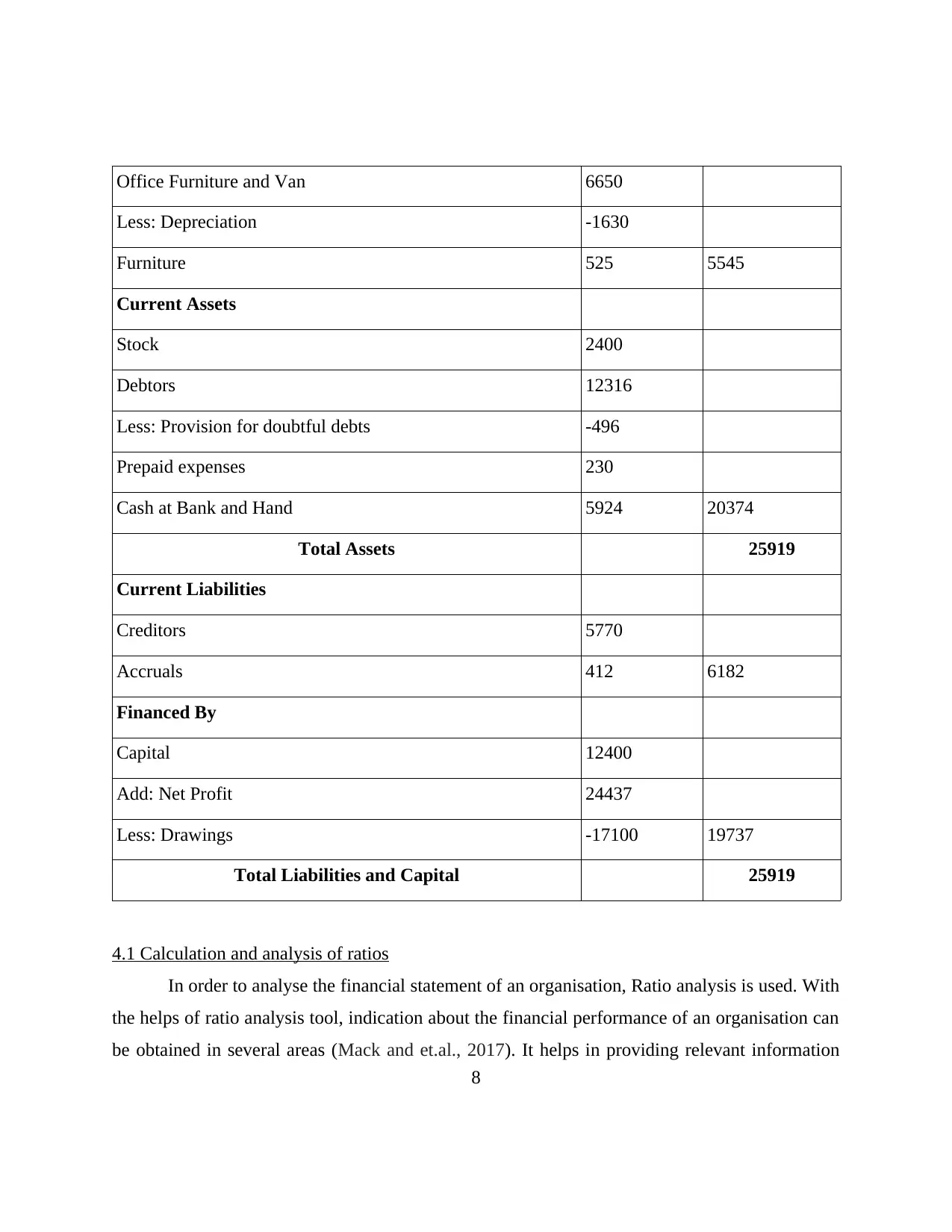

Balance Sheet for R Rigs

Balance Sheet as at 31 December 2017

PARTICULARS DETAILS AMOUNT (£)

Fixed Assets

7

Sales 157165

Less: Cost of Goods sold -94520

Gross Profit 62645

Interest Received 500

Discount received 160

Total Income 63305

Less: Expenses

Wages and salaries 31740

Rent 3170

Discount allowed 820

Van running cost 687

Bad debts 730

Doubtful debt provision 91

Depreciation 1630

Net Profit 24437

Balance Sheet for R Rigs

Balance Sheet as at 31 December 2017

PARTICULARS DETAILS AMOUNT (£)

Fixed Assets

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Office Furniture and Van 6650

Less: Depreciation -1630

Furniture 525 5545

Current Assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts -496

Prepaid expenses 230

Cash at Bank and Hand 5924 20374

Total Assets 25919

Current Liabilities

Creditors 5770

Accruals 412 6182

Financed By

Capital 12400

Add: Net Profit 24437

Less: Drawings -17100 19737

Total Liabilities and Capital 25919

4.1 Calculation and analysis of ratios

In order to analyse the financial statement of an organisation, Ratio analysis is used. With

the helps of ratio analysis tool, indication about the financial performance of an organisation can

be obtained in several areas (Mack and et.al., 2017). It helps in providing relevant information

8

Less: Depreciation -1630

Furniture 525 5545

Current Assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts -496

Prepaid expenses 230

Cash at Bank and Hand 5924 20374

Total Assets 25919

Current Liabilities

Creditors 5770

Accruals 412 6182

Financed By

Capital 12400

Add: Net Profit 24437

Less: Drawings -17100 19737

Total Liabilities and Capital 25919

4.1 Calculation and analysis of ratios

In order to analyse the financial statement of an organisation, Ratio analysis is used. With

the helps of ratio analysis tool, indication about the financial performance of an organisation can

be obtained in several areas (Mack and et.al., 2017). It helps in providing relevant information

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

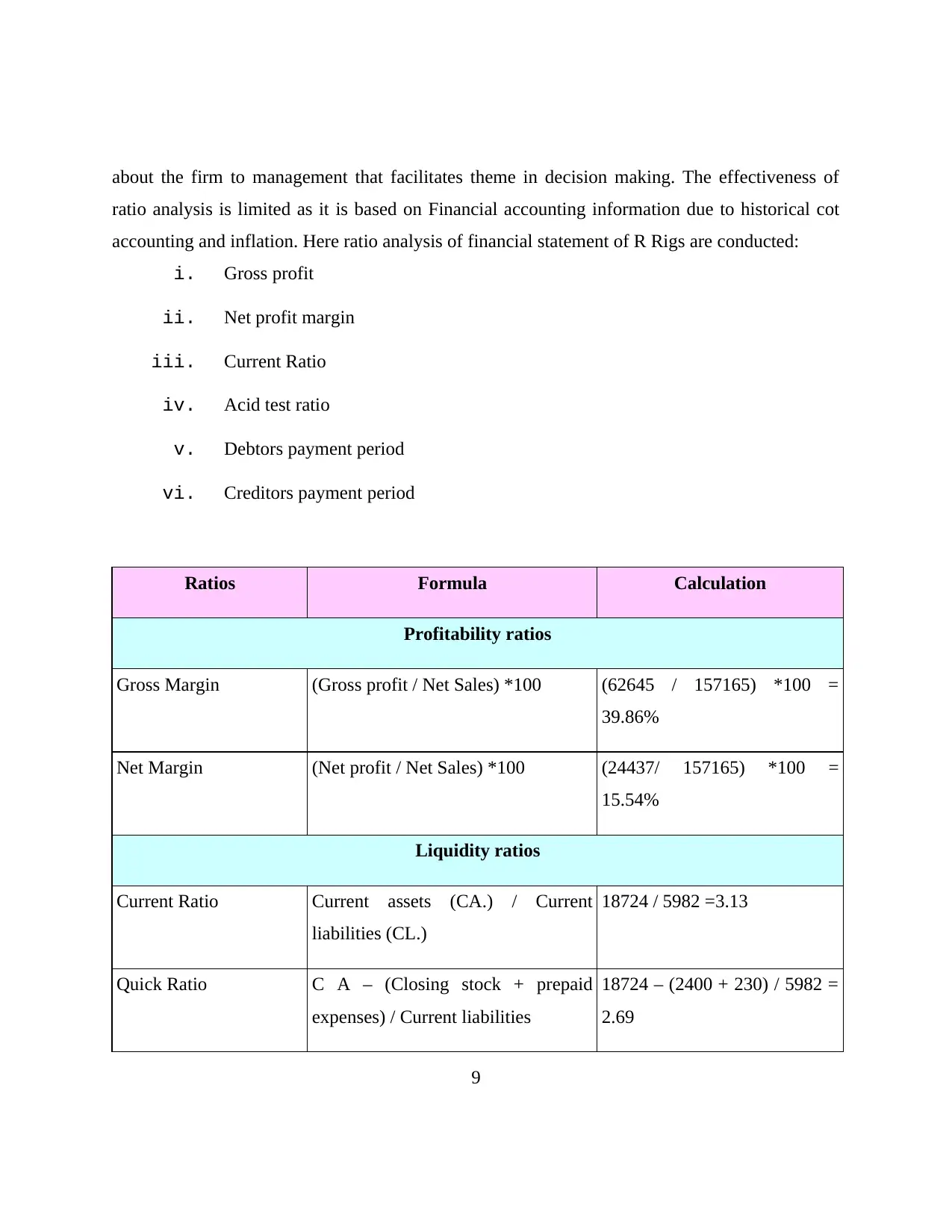

about the firm to management that facilitates theme in decision making. The effectiveness of

ratio analysis is limited as it is based on Financial accounting information due to historical cot

accounting and inflation. Here ratio analysis of financial statement of R Rigs are conducted:

i. Gross profit

ii. Net profit margin

iii. Current Ratio

iv. Acid test ratio

v. Debtors payment period

vi. Creditors payment period

Ratios Formula Calculation

Profitability ratios

Gross Margin (Gross profit / Net Sales) *100 (62645 / 157165) *100 =

39.86%

Net Margin (Net profit / Net Sales) *100 (24437/ 157165) *100 =

15.54%

Liquidity ratios

Current Ratio Current assets (CA.) / Current

liabilities (CL.)

18724 / 5982 =3.13

Quick Ratio C A – (Closing stock + prepaid

expenses) / Current liabilities

18724 – (2400 + 230) / 5982 =

2.69

9

ratio analysis is limited as it is based on Financial accounting information due to historical cot

accounting and inflation. Here ratio analysis of financial statement of R Rigs are conducted:

i. Gross profit

ii. Net profit margin

iii. Current Ratio

iv. Acid test ratio

v. Debtors payment period

vi. Creditors payment period

Ratios Formula Calculation

Profitability ratios

Gross Margin (Gross profit / Net Sales) *100 (62645 / 157165) *100 =

39.86%

Net Margin (Net profit / Net Sales) *100 (24437/ 157165) *100 =

15.54%

Liquidity ratios

Current Ratio Current assets (CA.) / Current

liabilities (CL.)

18724 / 5982 =3.13

Quick Ratio C A – (Closing stock + prepaid

expenses) / Current liabilities

18724 – (2400 + 230) / 5982 =

2.69

9

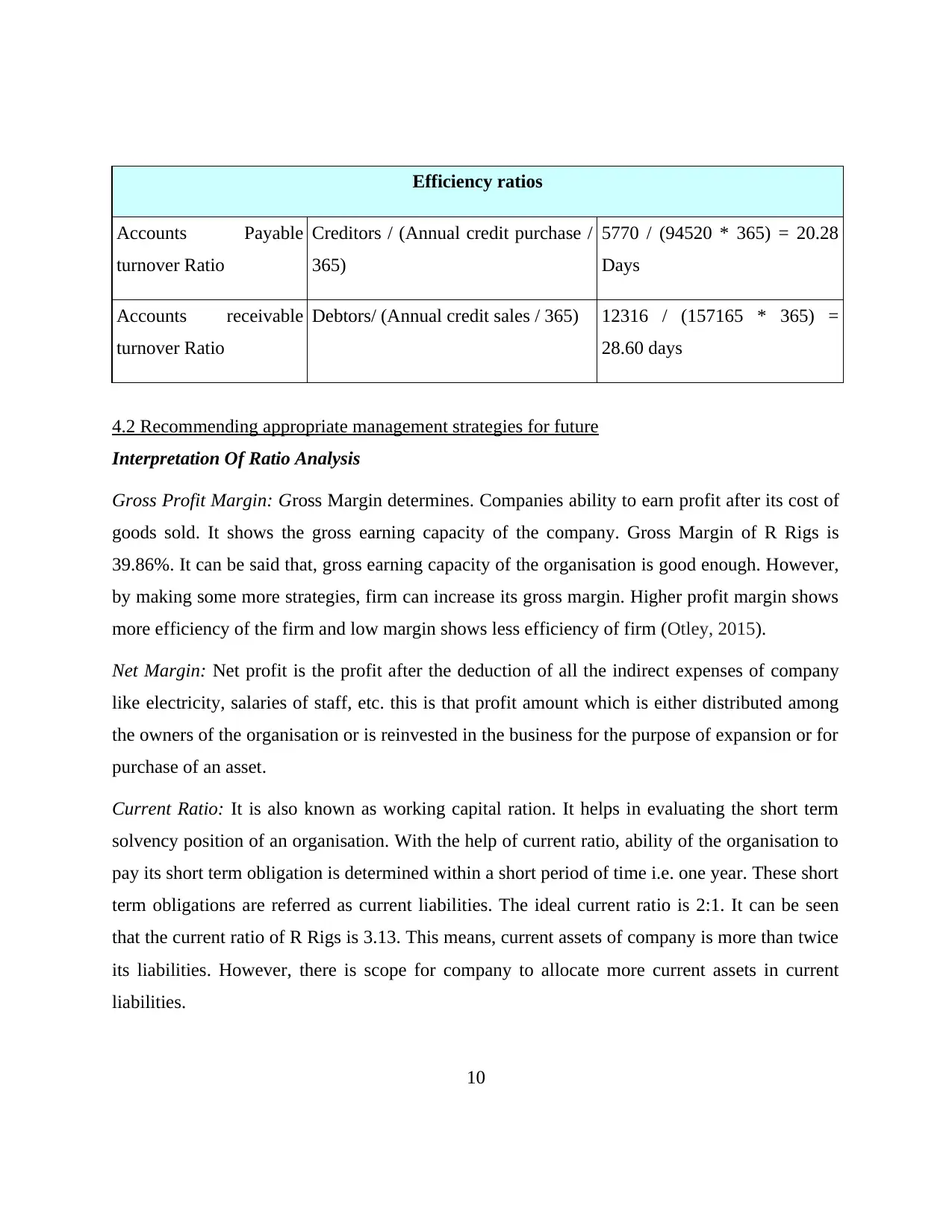

Efficiency ratios

Accounts Payable

turnover Ratio

Creditors / (Annual credit purchase /

365)

5770 / (94520 * 365) = 20.28

Days

Accounts receivable

turnover Ratio

Debtors/ (Annual credit sales / 365) 12316 / (157165 * 365) =

28.60 days

4.2 Recommending appropriate management strategies for future

Interpretation Of Ratio Analysis

Gross Profit Margin: Gross Margin determines. Companies ability to earn profit after its cost of

goods sold. It shows the gross earning capacity of the company. Gross Margin of R Rigs is

39.86%. It can be said that, gross earning capacity of the organisation is good enough. However,

by making some more strategies, firm can increase its gross margin. Higher profit margin shows

more efficiency of the firm and low margin shows less efficiency of firm (Otley, 2015).

Net Margin: Net profit is the profit after the deduction of all the indirect expenses of company

like electricity, salaries of staff, etc. this is that profit amount which is either distributed among

the owners of the organisation or is reinvested in the business for the purpose of expansion or for

purchase of an asset.

Current Ratio: It is also known as working capital ration. It helps in evaluating the short term

solvency position of an organisation. With the help of current ratio, ability of the organisation to

pay its short term obligation is determined within a short period of time i.e. one year. These short

term obligations are referred as current liabilities. The ideal current ratio is 2:1. It can be seen

that the current ratio of R Rigs is 3.13. This means, current assets of company is more than twice

its liabilities. However, there is scope for company to allocate more current assets in current

liabilities.

10

Accounts Payable

turnover Ratio

Creditors / (Annual credit purchase /

365)

5770 / (94520 * 365) = 20.28

Days

Accounts receivable

turnover Ratio

Debtors/ (Annual credit sales / 365) 12316 / (157165 * 365) =

28.60 days

4.2 Recommending appropriate management strategies for future

Interpretation Of Ratio Analysis

Gross Profit Margin: Gross Margin determines. Companies ability to earn profit after its cost of

goods sold. It shows the gross earning capacity of the company. Gross Margin of R Rigs is

39.86%. It can be said that, gross earning capacity of the organisation is good enough. However,

by making some more strategies, firm can increase its gross margin. Higher profit margin shows

more efficiency of the firm and low margin shows less efficiency of firm (Otley, 2015).

Net Margin: Net profit is the profit after the deduction of all the indirect expenses of company

like electricity, salaries of staff, etc. this is that profit amount which is either distributed among

the owners of the organisation or is reinvested in the business for the purpose of expansion or for

purchase of an asset.

Current Ratio: It is also known as working capital ration. It helps in evaluating the short term

solvency position of an organisation. With the help of current ratio, ability of the organisation to

pay its short term obligation is determined within a short period of time i.e. one year. These short

term obligations are referred as current liabilities. The ideal current ratio is 2:1. It can be seen

that the current ratio of R Rigs is 3.13. This means, current assets of company is more than twice

its liabilities. However, there is scope for company to allocate more current assets in current

liabilities.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.