Comprehensive Financial Analysis of a Geodes Business Plan: Report

VerifiedAdded on 2022/12/27

|23

|6652

|88

Report

AI Summary

This report presents a comprehensive financial analysis of a proposed Geodes business venture. It begins with an introduction outlining the importance of financial planning for new businesses and the methodologies used in the analysis. The report details key assumptions, including funding sources and pricing strategies. It then delves into the financial statements, including a profit and loss statement, balance sheet, and a detailed monthly cash flow statement, along with forecasted annual cash flows for three years. The analysis incorporates a break-even analysis for different business models (internet sales and cabinet sales), sensitivity analysis, and discounted cash flow calculations to assess the venture's viability. Furthermore, financial ratio analysis is conducted to interpret the business's financial performance. The report concludes with recommendations and a critical reflection on the business plan, providing a comprehensive overview of the financial aspects of the Geodes business.

FINANCE MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Summary of assumptions and estimates for analysis including the justifications for the same. .1

OTHER FINANCIAL DETAILS....................................................................................................5

MONTHLY CASH FLOW STATEMENT.....................................................................................7

FORECASTED ANNUAL CASH FLOW FOR THREE YEARS.................................................8

REQUIRED CAPITAL TO START THE VENTURE.................................................................10

SENSITIVITY ANALYSIS..........................................................................................................11

DISCOUNTED CASH FLOW......................................................................................................12

FINANCIAL RATIO ANALYSIS................................................................................................13

Interpretation of financial result on the basis of ratio calculation- ...........................................14

CONCLUSION..............................................................................................................................17

RECOMMENDATION.................................................................................................................17

CRITICAL REFLECTION............................................................................................................19

REFERENCES..............................................................................................................................21

INTRODUCTION...........................................................................................................................1

Summary of assumptions and estimates for analysis including the justifications for the same. .1

OTHER FINANCIAL DETAILS....................................................................................................5

MONTHLY CASH FLOW STATEMENT.....................................................................................7

FORECASTED ANNUAL CASH FLOW FOR THREE YEARS.................................................8

REQUIRED CAPITAL TO START THE VENTURE.................................................................10

SENSITIVITY ANALYSIS..........................................................................................................11

DISCOUNTED CASH FLOW......................................................................................................12

FINANCIAL RATIO ANALYSIS................................................................................................13

Interpretation of financial result on the basis of ratio calculation- ...........................................14

CONCLUSION..............................................................................................................................17

RECOMMENDATION.................................................................................................................17

CRITICAL REFLECTION............................................................................................................19

REFERENCES..............................................................................................................................21

INTRODUCTION

Starting a new business is not an easy task as it involves extensive planning. It is

accompanied by the plan which provides a direction and guidelines in regard to the operations to

be carried out. This is therefore, very essential to conduct a proper analysis of the plan which has

been set up mainly for the purpose of the initiating a new business. Thus, financial analysis of

the business plan pertaining to the new venture should be properly analysed, which assist in

determining the viability of the overall business plan in respect to the future earnings. In this

context, this business report is being prepared which analysis the business plan being proposed

pertaining to the Geodes business.

In order to make the analysis effective various tools and approaches are being utilized. It

involves the break-even point analysis, preparation of the cash flow statement along with the

other financial statement which is considered to be important for the new business venture plan.

This will result in better and effective analysis of the plan developed along with understanding

the viability of the business for the long run is also measured and monitored. Along with this,

certain estimations and assumptions have been made in regard to preparation of the financial

statement of the business. It will also assist in framing certain recommendations in respect to the

business plan based upon the information provided. At last, the critical reflection of the report is

presented which will be provided to Hattie in order to make the project a success.

Summary of assumptions and estimates for analysis including the justifications for the same

Sources of Funding

It is being clear from the case study, that Hattie has already received a lump sum amount

of 450,000 pounds after leaving the company. Therefore, this amount can be utilized by

the Hattie pertaining to the business operation of the Geodes.

In terms of requirement of additional funds, Hattie is willing to take 40,000 pounds as

loan at the rate of 7% interest.

In addition to this, it is also assumed that the company can also borrow funds from the

capital market pertaining to the business operation of Geodes.

The last option which is available to to Hattie is to add partners to the venture who will

bring in their share of capital to the business and will also have a share in the profits of

the company. This will help in decreasing the financial burden of Hattie to a great extend.

Profit and Loss Items

1

Starting a new business is not an easy task as it involves extensive planning. It is

accompanied by the plan which provides a direction and guidelines in regard to the operations to

be carried out. This is therefore, very essential to conduct a proper analysis of the plan which has

been set up mainly for the purpose of the initiating a new business. Thus, financial analysis of

the business plan pertaining to the new venture should be properly analysed, which assist in

determining the viability of the overall business plan in respect to the future earnings. In this

context, this business report is being prepared which analysis the business plan being proposed

pertaining to the Geodes business.

In order to make the analysis effective various tools and approaches are being utilized. It

involves the break-even point analysis, preparation of the cash flow statement along with the

other financial statement which is considered to be important for the new business venture plan.

This will result in better and effective analysis of the plan developed along with understanding

the viability of the business for the long run is also measured and monitored. Along with this,

certain estimations and assumptions have been made in regard to preparation of the financial

statement of the business. It will also assist in framing certain recommendations in respect to the

business plan based upon the information provided. At last, the critical reflection of the report is

presented which will be provided to Hattie in order to make the project a success.

Summary of assumptions and estimates for analysis including the justifications for the same

Sources of Funding

It is being clear from the case study, that Hattie has already received a lump sum amount

of 450,000 pounds after leaving the company. Therefore, this amount can be utilized by

the Hattie pertaining to the business operation of the Geodes.

In terms of requirement of additional funds, Hattie is willing to take 40,000 pounds as

loan at the rate of 7% interest.

In addition to this, it is also assumed that the company can also borrow funds from the

capital market pertaining to the business operation of Geodes.

The last option which is available to to Hattie is to add partners to the venture who will

bring in their share of capital to the business and will also have a share in the profits of

the company. This will help in decreasing the financial burden of Hattie to a great extend.

Profit and Loss Items

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase of Geodes

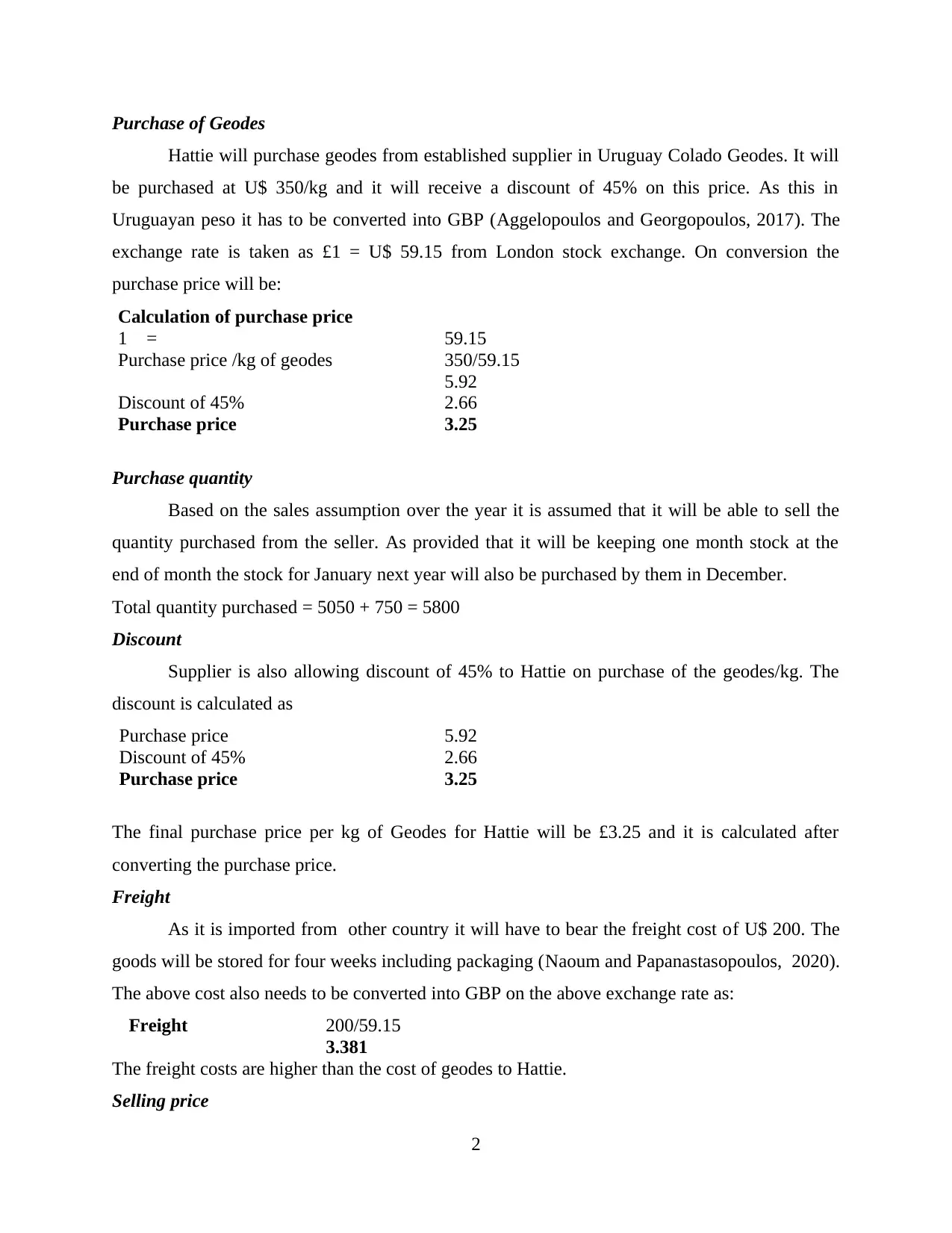

Hattie will purchase geodes from established supplier in Uruguay Colado Geodes. It will

be purchased at U$ 350/kg and it will receive a discount of 45% on this price. As this in

Uruguayan peso it has to be converted into GBP (Aggelopoulos and Georgopoulos, 2017). The

exchange rate is taken as £1 = U$ 59.15 from London stock exchange. On conversion the

purchase price will be:

Calculation of purchase price

1 £= 59.15

Purchase price /kg of geodes 350/59.15

5.92

Discount of 45% 2.66

Purchase price 3.25

Purchase quantity

Based on the sales assumption over the year it is assumed that it will be able to sell the

quantity purchased from the seller. As provided that it will be keeping one month stock at the

end of month the stock for January next year will also be purchased by them in December.

Total quantity purchased = 5050 + 750 = 5800

Discount

Supplier is also allowing discount of 45% to Hattie on purchase of the geodes/kg. The

discount is calculated as

Purchase price 5.92

Discount of 45% 2.66

Purchase price 3.25

The final purchase price per kg of Geodes for Hattie will be £3.25 and it is calculated after

converting the purchase price.

Freight

As it is imported from other country it will have to bear the freight cost of U$ 200. The

goods will be stored for four weeks including packaging (Naoum and Papanastasopoulos, 2020).

The above cost also needs to be converted into GBP on the above exchange rate as:

Freight 200/59.15

3.381

The freight costs are higher than the cost of geodes to Hattie.

Selling price

2

Hattie will purchase geodes from established supplier in Uruguay Colado Geodes. It will

be purchased at U$ 350/kg and it will receive a discount of 45% on this price. As this in

Uruguayan peso it has to be converted into GBP (Aggelopoulos and Georgopoulos, 2017). The

exchange rate is taken as £1 = U$ 59.15 from London stock exchange. On conversion the

purchase price will be:

Calculation of purchase price

1 £= 59.15

Purchase price /kg of geodes 350/59.15

5.92

Discount of 45% 2.66

Purchase price 3.25

Purchase quantity

Based on the sales assumption over the year it is assumed that it will be able to sell the

quantity purchased from the seller. As provided that it will be keeping one month stock at the

end of month the stock for January next year will also be purchased by them in December.

Total quantity purchased = 5050 + 750 = 5800

Discount

Supplier is also allowing discount of 45% to Hattie on purchase of the geodes/kg. The

discount is calculated as

Purchase price 5.92

Discount of 45% 2.66

Purchase price 3.25

The final purchase price per kg of Geodes for Hattie will be £3.25 and it is calculated after

converting the purchase price.

Freight

As it is imported from other country it will have to bear the freight cost of U$ 200. The

goods will be stored for four weeks including packaging (Naoum and Papanastasopoulos, 2020).

The above cost also needs to be converted into GBP on the above exchange rate as:

Freight 200/59.15

3.381

The freight costs are higher than the cost of geodes to Hattie.

Selling price

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

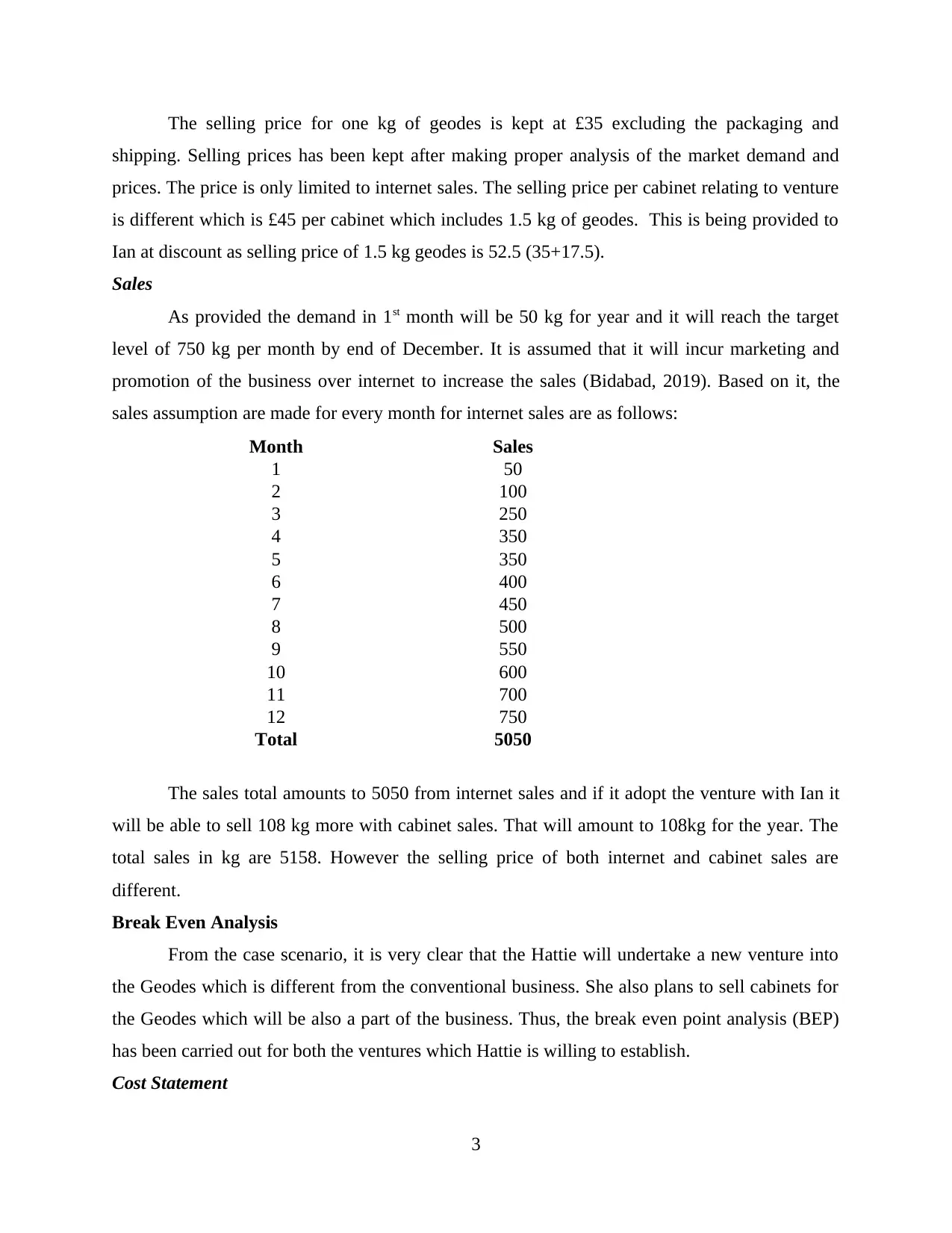

The selling price for one kg of geodes is kept at £35 excluding the packaging and

shipping. Selling prices has been kept after making proper analysis of the market demand and

prices. The price is only limited to internet sales. The selling price per cabinet relating to venture

is different which is £45 per cabinet which includes 1.5 kg of geodes. This is being provided to

Ian at discount as selling price of 1.5 kg geodes is 52.5 (35+17.5).

Sales

As provided the demand in 1st month will be 50 kg for year and it will reach the target

level of 750 kg per month by end of December. It is assumed that it will incur marketing and

promotion of the business over internet to increase the sales (Bidabad, 2019). Based on it, the

sales assumption are made for every month for internet sales are as follows:

Month Sales

1 50

2 100

3 250

4 350

5 350

6 400

7 450

8 500

9 550

10 600

11 700

12 750

Total 5050

The sales total amounts to 5050 from internet sales and if it adopt the venture with Ian it

will be able to sell 108 kg more with cabinet sales. That will amount to 108kg for the year. The

total sales in kg are 5158. However the selling price of both internet and cabinet sales are

different.

Break Even Analysis

From the case scenario, it is very clear that the Hattie will undertake a new venture into

the Geodes which is different from the conventional business. She also plans to sell cabinets for

the Geodes which will be also a part of the business. Thus, the break even point analysis (BEP)

has been carried out for both the ventures which Hattie is willing to establish.

Cost Statement

3

shipping. Selling prices has been kept after making proper analysis of the market demand and

prices. The price is only limited to internet sales. The selling price per cabinet relating to venture

is different which is £45 per cabinet which includes 1.5 kg of geodes. This is being provided to

Ian at discount as selling price of 1.5 kg geodes is 52.5 (35+17.5).

Sales

As provided the demand in 1st month will be 50 kg for year and it will reach the target

level of 750 kg per month by end of December. It is assumed that it will incur marketing and

promotion of the business over internet to increase the sales (Bidabad, 2019). Based on it, the

sales assumption are made for every month for internet sales are as follows:

Month Sales

1 50

2 100

3 250

4 350

5 350

6 400

7 450

8 500

9 550

10 600

11 700

12 750

Total 5050

The sales total amounts to 5050 from internet sales and if it adopt the venture with Ian it

will be able to sell 108 kg more with cabinet sales. That will amount to 108kg for the year. The

total sales in kg are 5158. However the selling price of both internet and cabinet sales are

different.

Break Even Analysis

From the case scenario, it is very clear that the Hattie will undertake a new venture into

the Geodes which is different from the conventional business. She also plans to sell cabinets for

the Geodes which will be also a part of the business. Thus, the break even point analysis (BEP)

has been carried out for both the ventures which Hattie is willing to establish.

Cost Statement

3

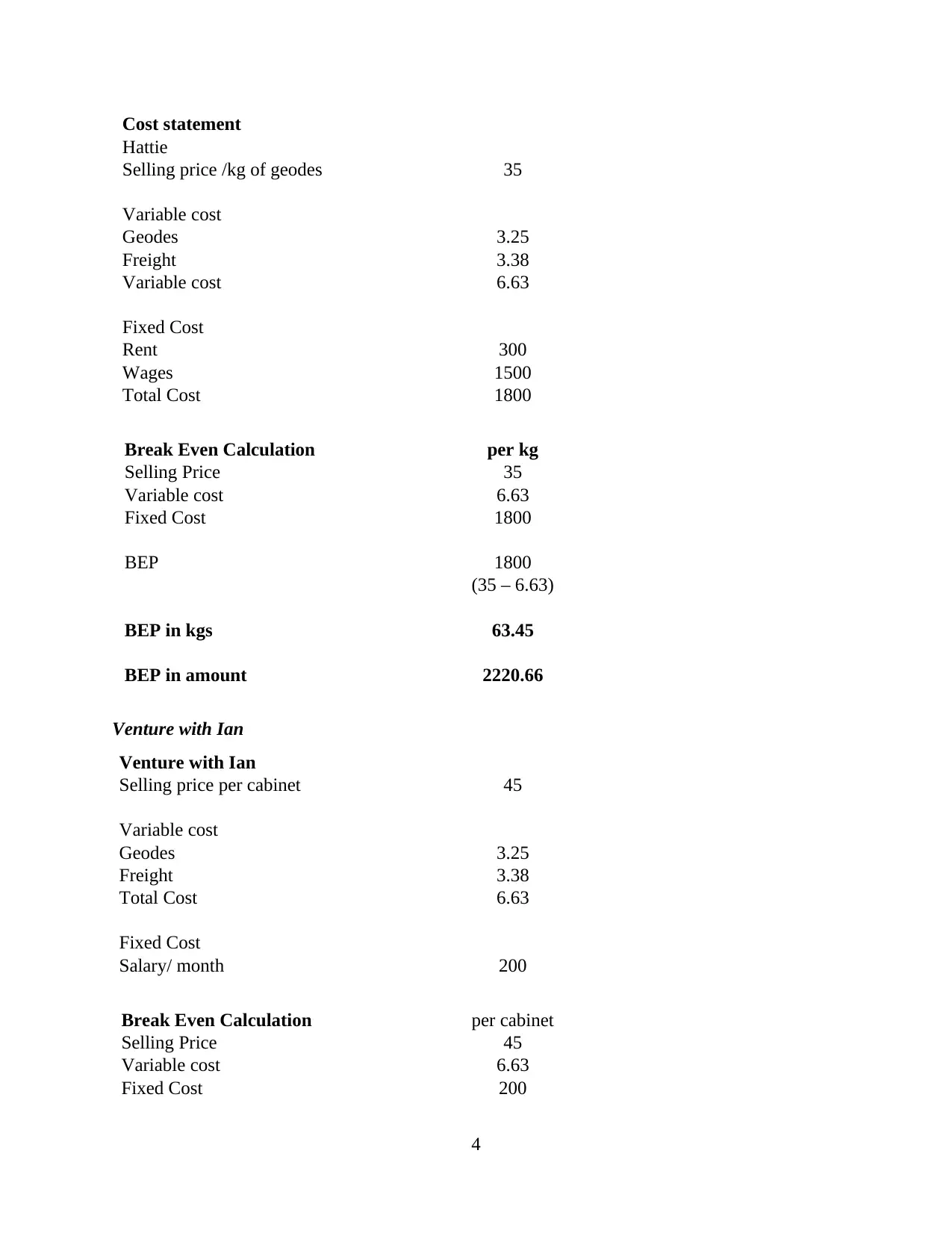

Cost statement

Hattie

Selling price /kg of geodes 35

Variable cost

Geodes 3.25

Freight 3.38

Variable cost 6.63

Fixed Cost

Rent 300

Wages 1500

Total Cost 1800

Break Even Calculation per kg

Selling Price 35

Variable cost 6.63

Fixed Cost 1800

BEP 1800

(35 – 6.63)

BEP in kgs 63.45

BEP in amount 2220.66

Venture with Ian

Venture with Ian

Selling price per cabinet 45

Variable cost

Geodes 3.25

Freight 3.38

Total Cost 6.63

Fixed Cost

Salary/ month 200

Break Even Calculation per cabinet

Selling Price 45

Variable cost 6.63

Fixed Cost 200

4

Hattie

Selling price /kg of geodes 35

Variable cost

Geodes 3.25

Freight 3.38

Variable cost 6.63

Fixed Cost

Rent 300

Wages 1500

Total Cost 1800

Break Even Calculation per kg

Selling Price 35

Variable cost 6.63

Fixed Cost 1800

BEP 1800

(35 – 6.63)

BEP in kgs 63.45

BEP in amount 2220.66

Venture with Ian

Venture with Ian

Selling price per cabinet 45

Variable cost

Geodes 3.25

Freight 3.38

Total Cost 6.63

Fixed Cost

Salary/ month 200

Break Even Calculation per cabinet

Selling Price 45

Variable cost 6.63

Fixed Cost 200

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEP 200

(35 – 6.04)

BEP in cabinet 5.21

BEP in amount 234.56

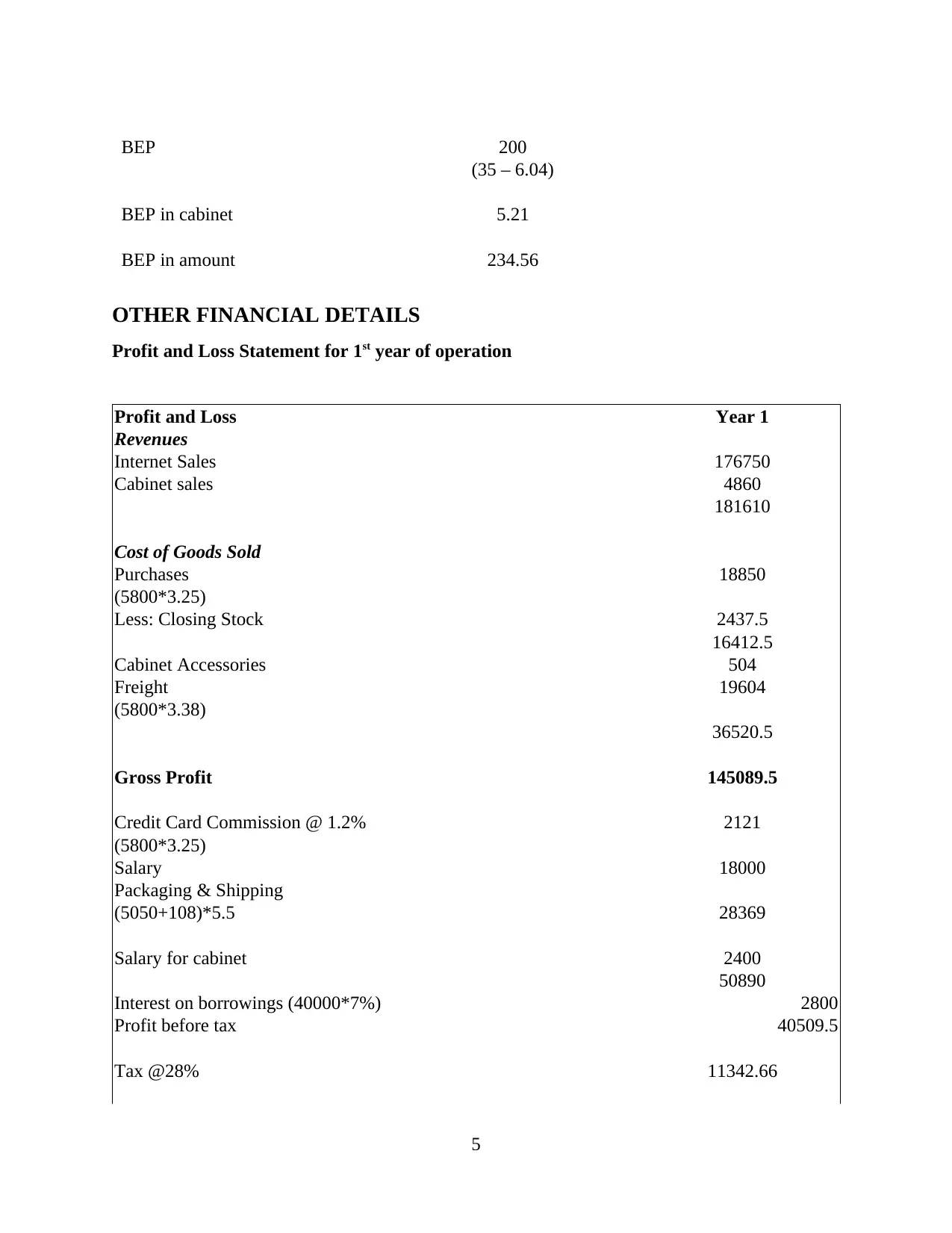

OTHER FINANCIAL DETAILS

Profit and Loss Statement for 1st year of operation

Profit and Loss Year 1

Revenues

Internet Sales 176750

Cabinet sales 4860

181610

Cost of Goods Sold

Purchases 18850

(5800*3.25)

Less: Closing Stock 2437.5

16412.5

Cabinet Accessories 504

Freight 19604

(5800*3.38)

36520.5

Gross Profit 145089.5

Credit Card Commission @ 1.2% 2121

(5800*3.25)

Salary 18000

Packaging & Shipping

(5050+108)*5.5 28369

Salary for cabinet 2400

50890

Interest on borrowings (40000*7%) 2800

Profit before tax 40509.5

Tax @28% 11342.66

5

(35 – 6.04)

BEP in cabinet 5.21

BEP in amount 234.56

OTHER FINANCIAL DETAILS

Profit and Loss Statement for 1st year of operation

Profit and Loss Year 1

Revenues

Internet Sales 176750

Cabinet sales 4860

181610

Cost of Goods Sold

Purchases 18850

(5800*3.25)

Less: Closing Stock 2437.5

16412.5

Cabinet Accessories 504

Freight 19604

(5800*3.38)

36520.5

Gross Profit 145089.5

Credit Card Commission @ 1.2% 2121

(5800*3.25)

Salary 18000

Packaging & Shipping

(5050+108)*5.5 28369

Salary for cabinet 2400

50890

Interest on borrowings (40000*7%) 2800

Profit before tax 40509.5

Tax @28% 11342.66

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

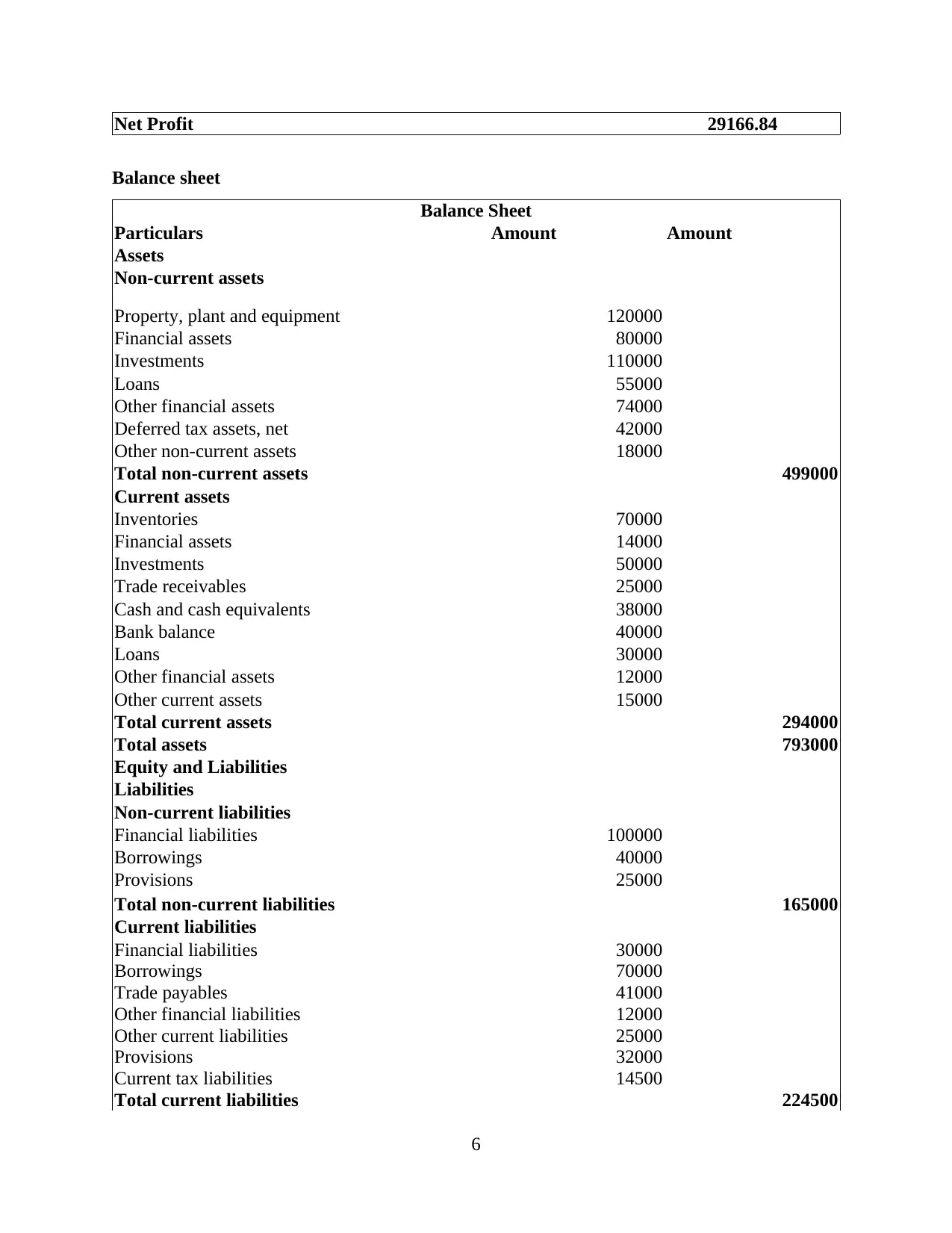

Net Profit 29166.84

Balance sheet

Balance Sheet

Particulars Amount Amount

Assets

Non-current assets

Property, plant and equipment 120000

Financial assets 80000

Investments 110000

Loans 55000

Other financial assets 74000

Deferred tax assets, net 42000

Other non-current assets 18000

Total non-current assets 499000

Current assets

Inventories 70000

Financial assets 14000

Investments 50000

Trade receivables 25000

Cash and cash equivalents 38000

Bank balance 40000

Loans 30000

Other financial assets 12000

Other current assets 15000

Total current assets 294000

Total assets 793000

Equity and Liabilities

Liabilities

Non-current liabilities

Financial liabilities 100000

Borrowings 40000

Provisions 25000

Total non-current liabilities 165000

Current liabilities

Financial liabilities 30000

Borrowings 70000

Trade payables 41000

Other financial liabilities 12000

Other current liabilities 25000

Provisions 32000

Current tax liabilities 14500

Total current liabilities 224500

6

Balance sheet

Balance Sheet

Particulars Amount Amount

Assets

Non-current assets

Property, plant and equipment 120000

Financial assets 80000

Investments 110000

Loans 55000

Other financial assets 74000

Deferred tax assets, net 42000

Other non-current assets 18000

Total non-current assets 499000

Current assets

Inventories 70000

Financial assets 14000

Investments 50000

Trade receivables 25000

Cash and cash equivalents 38000

Bank balance 40000

Loans 30000

Other financial assets 12000

Other current assets 15000

Total current assets 294000

Total assets 793000

Equity and Liabilities

Liabilities

Non-current liabilities

Financial liabilities 100000

Borrowings 40000

Provisions 25000

Total non-current liabilities 165000

Current liabilities

Financial liabilities 30000

Borrowings 70000

Trade payables 41000

Other financial liabilities 12000

Other current liabilities 25000

Provisions 32000

Current tax liabilities 14500

Total current liabilities 224500

6

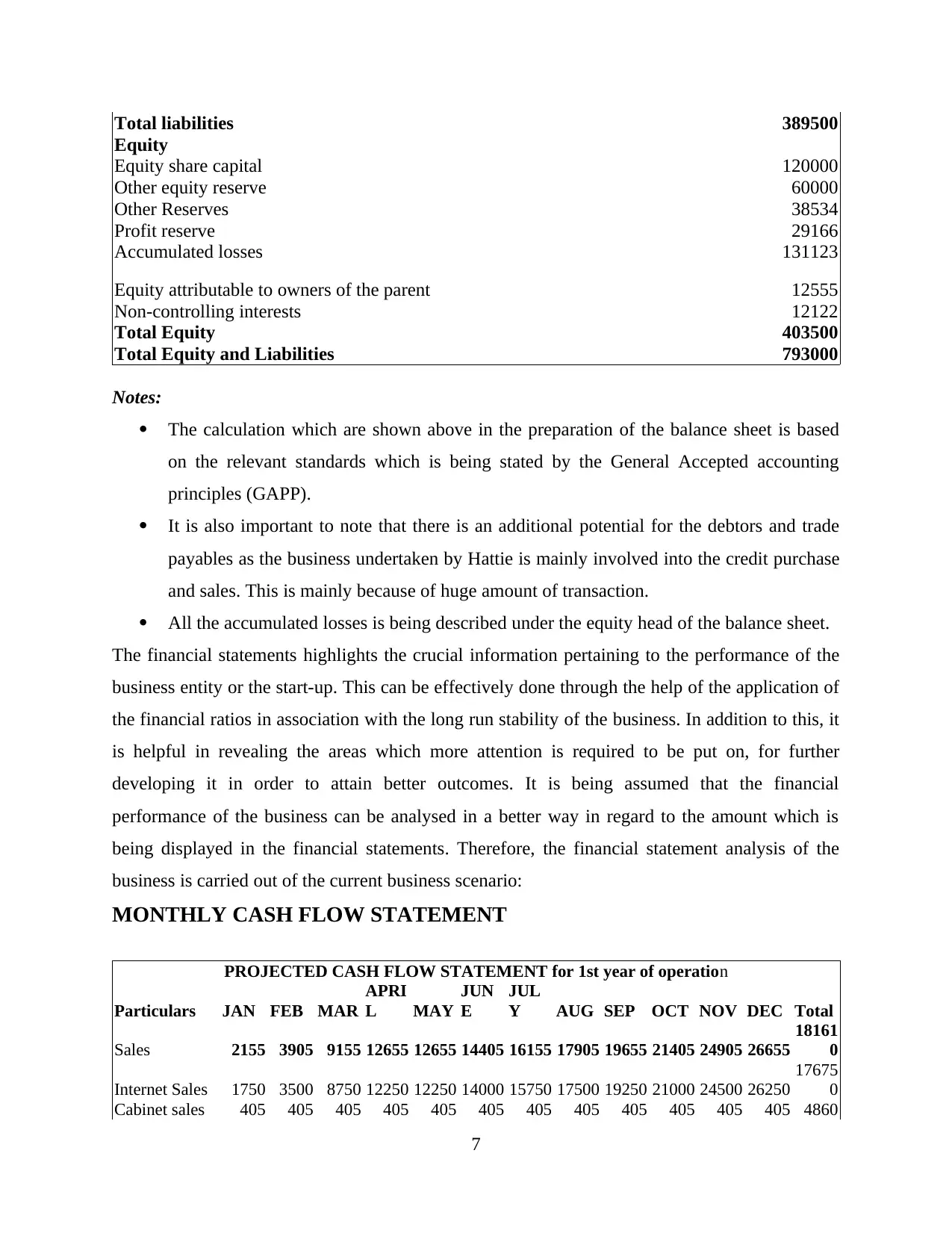

Total liabilities 389500

Equity

Equity share capital 120000

Other equity reserve 60000

Other Reserves 38534

Profit reserve 29166

Accumulated losses 131123

Equity attributable to owners of the parent 12555

Non-controlling interests 12122

Total Equity 403500

Total Equity and Liabilities 793000

Notes:

The calculation which are shown above in the preparation of the balance sheet is based

on the relevant standards which is being stated by the General Accepted accounting

principles (GAPP).

It is also important to note that there is an additional potential for the debtors and trade

payables as the business undertaken by Hattie is mainly involved into the credit purchase

and sales. This is mainly because of huge amount of transaction.

All the accumulated losses is being described under the equity head of the balance sheet.

The financial statements highlights the crucial information pertaining to the performance of the

business entity or the start-up. This can be effectively done through the help of the application of

the financial ratios in association with the long run stability of the business. In addition to this, it

is helpful in revealing the areas which more attention is required to be put on, for further

developing it in order to attain better outcomes. It is being assumed that the financial

performance of the business can be analysed in a better way in regard to the amount which is

being displayed in the financial statements. Therefore, the financial statement analysis of the

business is carried out of the current business scenario:

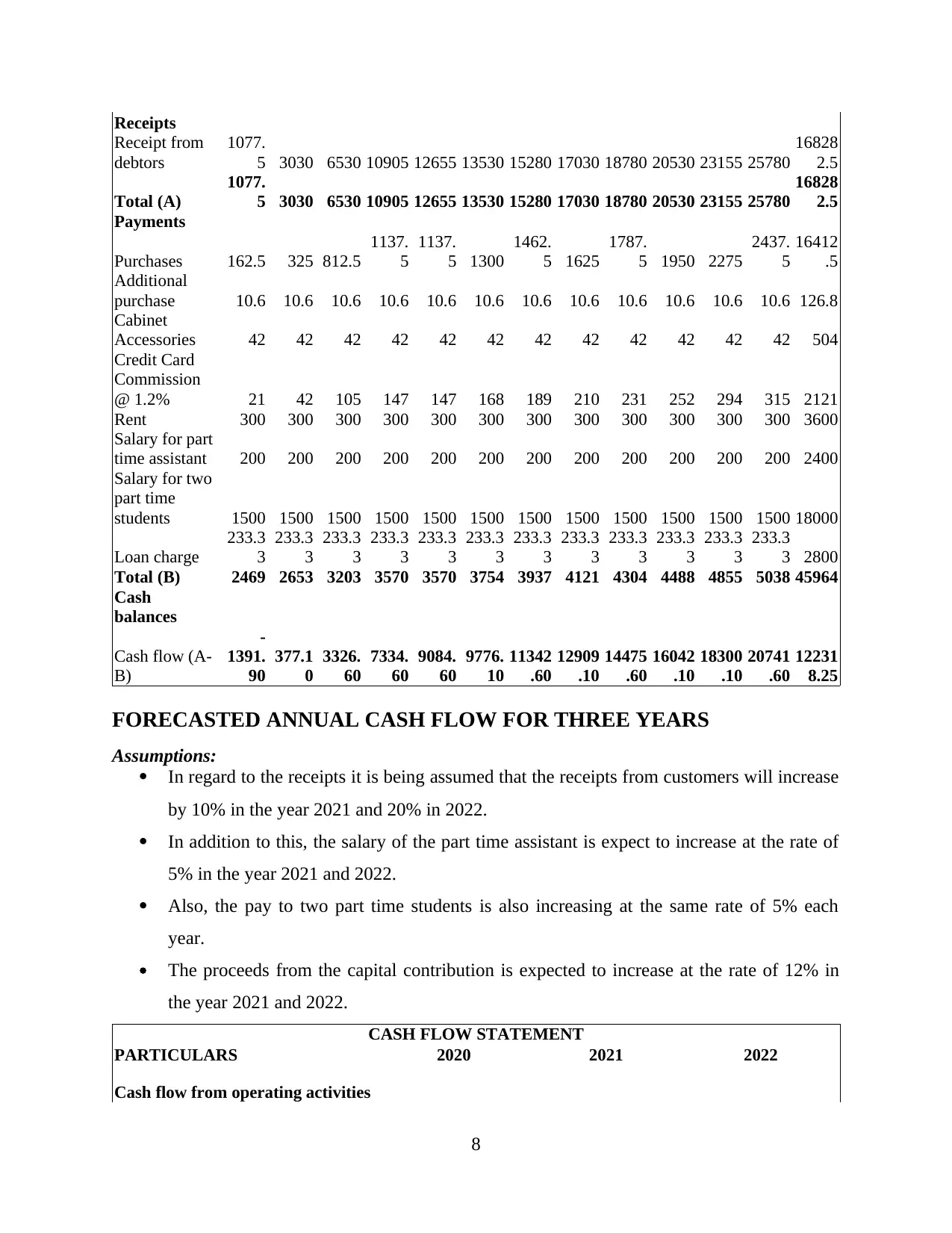

MONTHLY CASH FLOW STATEMENT

PROJECTED CASH FLOW STATEMENT for 1st year of operation

Particulars JAN FEB MAR

APRI

L MAY

JUN

E

JUL

Y AUG SEP OCT NOV DEC Total

Sales 2155 3905 9155 12655 12655 14405 16155 17905 19655 21405 24905 26655

18161

0

Internet Sales 1750 3500 8750 12250 12250 14000 15750 17500 19250 21000 24500 26250

17675

0

Cabinet sales 405 405 405 405 405 405 405 405 405 405 405 405 4860

7

Equity

Equity share capital 120000

Other equity reserve 60000

Other Reserves 38534

Profit reserve 29166

Accumulated losses 131123

Equity attributable to owners of the parent 12555

Non-controlling interests 12122

Total Equity 403500

Total Equity and Liabilities 793000

Notes:

The calculation which are shown above in the preparation of the balance sheet is based

on the relevant standards which is being stated by the General Accepted accounting

principles (GAPP).

It is also important to note that there is an additional potential for the debtors and trade

payables as the business undertaken by Hattie is mainly involved into the credit purchase

and sales. This is mainly because of huge amount of transaction.

All the accumulated losses is being described under the equity head of the balance sheet.

The financial statements highlights the crucial information pertaining to the performance of the

business entity or the start-up. This can be effectively done through the help of the application of

the financial ratios in association with the long run stability of the business. In addition to this, it

is helpful in revealing the areas which more attention is required to be put on, for further

developing it in order to attain better outcomes. It is being assumed that the financial

performance of the business can be analysed in a better way in regard to the amount which is

being displayed in the financial statements. Therefore, the financial statement analysis of the

business is carried out of the current business scenario:

MONTHLY CASH FLOW STATEMENT

PROJECTED CASH FLOW STATEMENT for 1st year of operation

Particulars JAN FEB MAR

APRI

L MAY

JUN

E

JUL

Y AUG SEP OCT NOV DEC Total

Sales 2155 3905 9155 12655 12655 14405 16155 17905 19655 21405 24905 26655

18161

0

Internet Sales 1750 3500 8750 12250 12250 14000 15750 17500 19250 21000 24500 26250

17675

0

Cabinet sales 405 405 405 405 405 405 405 405 405 405 405 405 4860

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Receipts

Receipt from

debtors

1077.

5 3030 6530 10905 12655 13530 15280 17030 18780 20530 23155 25780

16828

2.5

Total (A)

1077.

5 3030 6530 10905 12655 13530 15280 17030 18780 20530 23155 25780

16828

2.5

Payments

Purchases 162.5 325 812.5

1137.

5

1137.

5 1300

1462.

5 1625

1787.

5 1950 2275

2437.

5

16412

.5

Additional

purchase 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 126.8

Cabinet

Accessories 42 42 42 42 42 42 42 42 42 42 42 42 504

Credit Card

Commission

@ 1.2% 21 42 105 147 147 168 189 210 231 252 294 315 2121

Rent 300 300 300 300 300 300 300 300 300 300 300 300 3600

Salary for part

time assistant 200 200 200 200 200 200 200 200 200 200 200 200 2400

Salary for two

part time

students 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 18000

Loan charge

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3 2800

Total (B) 2469 2653 3203 3570 3570 3754 3937 4121 4304 4488 4855 5038 45964

Cash

balances

Cash flow (A-

B)

-

1391.

90

377.1

0

3326.

60

7334.

60

9084.

60

9776.

10

11342

.60

12909

.10

14475

.60

16042

.10

18300

.10

20741

.60

12231

8.25

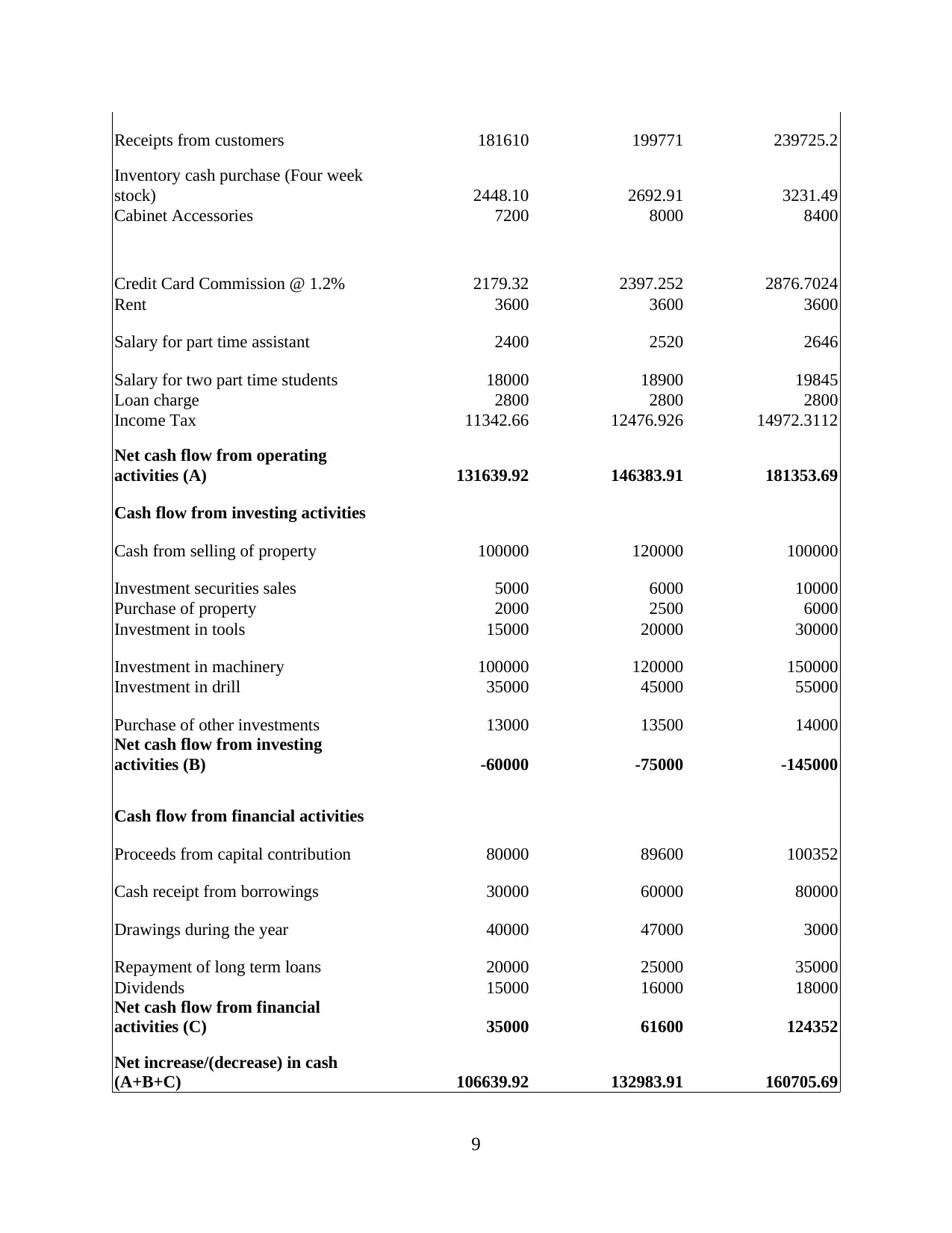

FORECASTED ANNUAL CASH FLOW FOR THREE YEARS

Assumptions:

In regard to the receipts it is being assumed that the receipts from customers will increase

by 10% in the year 2021 and 20% in 2022.

In addition to this, the salary of the part time assistant is expect to increase at the rate of

5% in the year 2021 and 2022.

Also, the pay to two part time students is also increasing at the same rate of 5% each

year.

The proceeds from the capital contribution is expected to increase at the rate of 12% in

the year 2021 and 2022.

CASH FLOW STATEMENT

PARTICULARS 2020 2021 2022

Cash flow from operating activities

8

Receipt from

debtors

1077.

5 3030 6530 10905 12655 13530 15280 17030 18780 20530 23155 25780

16828

2.5

Total (A)

1077.

5 3030 6530 10905 12655 13530 15280 17030 18780 20530 23155 25780

16828

2.5

Payments

Purchases 162.5 325 812.5

1137.

5

1137.

5 1300

1462.

5 1625

1787.

5 1950 2275

2437.

5

16412

.5

Additional

purchase 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 10.6 126.8

Cabinet

Accessories 42 42 42 42 42 42 42 42 42 42 42 42 504

Credit Card

Commission

@ 1.2% 21 42 105 147 147 168 189 210 231 252 294 315 2121

Rent 300 300 300 300 300 300 300 300 300 300 300 300 3600

Salary for part

time assistant 200 200 200 200 200 200 200 200 200 200 200 200 2400

Salary for two

part time

students 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 18000

Loan charge

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3

233.3

3 2800

Total (B) 2469 2653 3203 3570 3570 3754 3937 4121 4304 4488 4855 5038 45964

Cash

balances

Cash flow (A-

B)

-

1391.

90

377.1

0

3326.

60

7334.

60

9084.

60

9776.

10

11342

.60

12909

.10

14475

.60

16042

.10

18300

.10

20741

.60

12231

8.25

FORECASTED ANNUAL CASH FLOW FOR THREE YEARS

Assumptions:

In regard to the receipts it is being assumed that the receipts from customers will increase

by 10% in the year 2021 and 20% in 2022.

In addition to this, the salary of the part time assistant is expect to increase at the rate of

5% in the year 2021 and 2022.

Also, the pay to two part time students is also increasing at the same rate of 5% each

year.

The proceeds from the capital contribution is expected to increase at the rate of 12% in

the year 2021 and 2022.

CASH FLOW STATEMENT

PARTICULARS 2020 2021 2022

Cash flow from operating activities

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receipts from customers 181610 199771 239725.2

Inventory cash purchase (Four week

stock) 2448.10 2692.91 3231.49

Cabinet Accessories 7200 8000 8400

Credit Card Commission @ 1.2% 2179.32 2397.252 2876.7024

Rent 3600 3600 3600

Salary for part time assistant 2400 2520 2646

Salary for two part time students 18000 18900 19845

Loan charge 2800 2800 2800

Income Tax 11342.66 12476.926 14972.3112

Net cash flow from operating

activities (A) 131639.92 146383.91 181353.69

Cash flow from investing activities

Cash from selling of property 100000 120000 100000

Investment securities sales 5000 6000 10000

Purchase of property 2000 2500 6000

Investment in tools 15000 20000 30000

Investment in machinery 100000 120000 150000

Investment in drill 35000 45000 55000

Purchase of other investments 13000 13500 14000

Net cash flow from investing

activities (B) -60000 -75000 -145000

Cash flow from financial activities

Proceeds from capital contribution 80000 89600 100352

Cash receipt from borrowings 30000 60000 80000

Drawings during the year 40000 47000 3000

Repayment of long term loans 20000 25000 35000

Dividends 15000 16000 18000

Net cash flow from financial

activities (C) 35000 61600 124352

Net increase/(decrease) in cash

(A+B+C) 106639.92 132983.91 160705.69

9

Inventory cash purchase (Four week

stock) 2448.10 2692.91 3231.49

Cabinet Accessories 7200 8000 8400

Credit Card Commission @ 1.2% 2179.32 2397.252 2876.7024

Rent 3600 3600 3600

Salary for part time assistant 2400 2520 2646

Salary for two part time students 18000 18900 19845

Loan charge 2800 2800 2800

Income Tax 11342.66 12476.926 14972.3112

Net cash flow from operating

activities (A) 131639.92 146383.91 181353.69

Cash flow from investing activities

Cash from selling of property 100000 120000 100000

Investment securities sales 5000 6000 10000

Purchase of property 2000 2500 6000

Investment in tools 15000 20000 30000

Investment in machinery 100000 120000 150000

Investment in drill 35000 45000 55000

Purchase of other investments 13000 13500 14000

Net cash flow from investing

activities (B) -60000 -75000 -145000

Cash flow from financial activities

Proceeds from capital contribution 80000 89600 100352

Cash receipt from borrowings 30000 60000 80000

Drawings during the year 40000 47000 3000

Repayment of long term loans 20000 25000 35000

Dividends 15000 16000 18000

Net cash flow from financial

activities (C) 35000 61600 124352

Net increase/(decrease) in cash

(A+B+C) 106639.92 132983.91 160705.69

9

Overall cash flow analysis:

From the monthly cash flow statement, it can be summarized that the option is seemed to

be fairly profitable but at the initial stage of the start-up, the cost would exceed the cash inflows

which will result into making of the negative balance for the new venture business. On the other

hand, the operation of the following month will assist in covering up the loss which is being

incurred during the first month (Chen and et.al., 2021). From the actual cash flow, it has been

estimated that the operation will be profitable in the long run starting from 2020 to 2021. This

will result into increase in the cost and the revenue pertaining to the business which will

consequently lead to making the company profitable. Apart from this, it has been assumed that

the receipt from the customers will rise by 10% and 20% in the year 2021 and 2022 respectively

(Dhole and et.al., 2021). This rate is expected to continue for the next 5 years of the business

operation as the supplier will expand gradually after which the revenue will be stick at a certain

point. For the first month sale, only 50 units of Geodes will be sold.

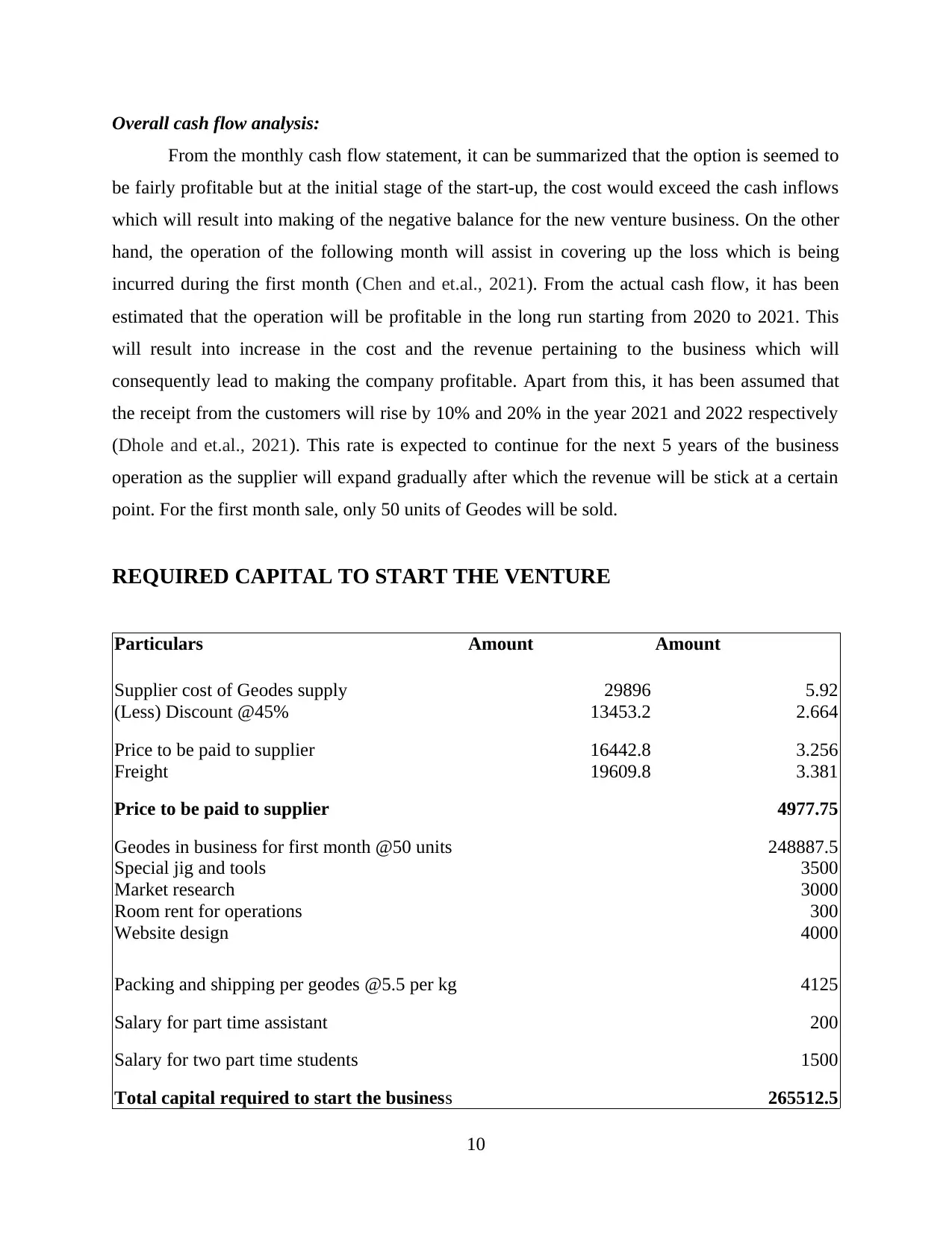

REQUIRED CAPITAL TO START THE VENTURE

Particulars Amount Amount

Supplier cost of Geodes supply 29896 5.92

(Less) Discount @45% 13453.2 2.664

Price to be paid to supplier 16442.8 3.256

Freight 19609.8 3.381

Price to be paid to supplier 4977.75

Geodes in business for first month @50 units 248887.5

Special jig and tools 3500

Market research 3000

Room rent for operations 300

Website design 4000

Packing and shipping per geodes @5.5 per kg 4125

Salary for part time assistant 200

Salary for two part time students 1500

Total capital required to start the business 265512.5

10

From the monthly cash flow statement, it can be summarized that the option is seemed to

be fairly profitable but at the initial stage of the start-up, the cost would exceed the cash inflows

which will result into making of the negative balance for the new venture business. On the other

hand, the operation of the following month will assist in covering up the loss which is being

incurred during the first month (Chen and et.al., 2021). From the actual cash flow, it has been

estimated that the operation will be profitable in the long run starting from 2020 to 2021. This

will result into increase in the cost and the revenue pertaining to the business which will

consequently lead to making the company profitable. Apart from this, it has been assumed that

the receipt from the customers will rise by 10% and 20% in the year 2021 and 2022 respectively

(Dhole and et.al., 2021). This rate is expected to continue for the next 5 years of the business

operation as the supplier will expand gradually after which the revenue will be stick at a certain

point. For the first month sale, only 50 units of Geodes will be sold.

REQUIRED CAPITAL TO START THE VENTURE

Particulars Amount Amount

Supplier cost of Geodes supply 29896 5.92

(Less) Discount @45% 13453.2 2.664

Price to be paid to supplier 16442.8 3.256

Freight 19609.8 3.381

Price to be paid to supplier 4977.75

Geodes in business for first month @50 units 248887.5

Special jig and tools 3500

Market research 3000

Room rent for operations 300

Website design 4000

Packing and shipping per geodes @5.5 per kg 4125

Salary for part time assistant 200

Salary for two part time students 1500

Total capital required to start the business 265512.5

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.