Comprehensive Management Accounting Report - Unit 5 Analysis

VerifiedAdded on 2022/11/28

|15

|4593

|294

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its significance in organizational decision-making. It analyzes various aspects, including different types of management accounting systems like traditional, lean, throughput, and transfer pricing. The report delves into methods of management accounting reporting, such as budget reports, accounting receivable aging reports, cost managerial accounting reports, and performance reports, highlighting their roles in financial planning, control, and performance evaluation. Furthermore, it explores cost analysis techniques, specifically absorption and marginal costing, along with the preparation of income statements. The report also examines the advantages and disadvantages of different planning tools used for budgetary control. The report uses a case study of Hichrom, a manufacturing company, to illustrate these concepts and provide practical insights into their application in a real-world business context.

Unit 5 Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................1

P1 Management Accounting and its various types......................................................................2

P2 Methods of Management accounting reporting......................................................................4

P3 Cost analysis...........................................................................................................................6

P4 Advantages and disadvantages of different planning tools of budgetary control..................7

P5 Different Management accounting system...........................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................13

1

Introduction......................................................................................................................................1

P1 Management Accounting and its various types......................................................................2

P2 Methods of Management accounting reporting......................................................................4

P3 Cost analysis...........................................................................................................................6

P4 Advantages and disadvantages of different planning tools of budgetary control..................7

P5 Different Management accounting system...........................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................13

1

Introduction

The following report is based on management accounting. Management accounting is the

continuous process of recognising, measuring analysing and coordinating all the financial

information to the management of the organisation which pursuit to the goal of company. In this

report a company called Hichrom has been taken (Hiebl and et.al 2019). It is a manufacturing

company which produces the products of medicine and forensic. Is company is continuously

increasing their expansion and working in more than 20 countries and they have good network of

supply therefore they are manufacturing this medicine easily supplying to the retailers. This

report provides explanation of Management Accounting and also different types of Management

Accounting system for the company. This report also provides in-depth information about the

management accounting reporting. Calculation of various cost by using appropriate technique

and also the preparation of income statement using marginal and absorption costing is mentioned

in this report. Various pros and cons of different planning tool which is used for budgetary

control is also defined in this report.

P1 Management Accounting and its various types

Management accounting is one of the essential tools for the organisation. As accounting system

keeps track on various income and expenses of the company and also provides significant

information about various financial and non financial factors to the management so that they can

further make favourable decisions for the company. Management Accounting provides its

services to public company private company and also the government agencies because all these

companies need day to day information about their expenses and level of income. The main role

of management accounting is to help the management to know about the various investment

budgeting planning and create risk management so that in future, Hichrom do not have to run

short of money. Management Accounting also provides detailed information about the lower

level of accounting in the organisation as well so that management can know the various

expenses of each department. Apart from this Management Accounting helps in forecasting

budgets and also it measures the performance of various strategies which has been made by the

management in past. One of the biggest advantages of management accounting is that it provides

timely information to the management so that they can improvise all the strategies and prepared

new strategies which will provide benefits to the organisation.

Types

2

The following report is based on management accounting. Management accounting is the

continuous process of recognising, measuring analysing and coordinating all the financial

information to the management of the organisation which pursuit to the goal of company. In this

report a company called Hichrom has been taken (Hiebl and et.al 2019). It is a manufacturing

company which produces the products of medicine and forensic. Is company is continuously

increasing their expansion and working in more than 20 countries and they have good network of

supply therefore they are manufacturing this medicine easily supplying to the retailers. This

report provides explanation of Management Accounting and also different types of Management

Accounting system for the company. This report also provides in-depth information about the

management accounting reporting. Calculation of various cost by using appropriate technique

and also the preparation of income statement using marginal and absorption costing is mentioned

in this report. Various pros and cons of different planning tool which is used for budgetary

control is also defined in this report.

P1 Management Accounting and its various types

Management accounting is one of the essential tools for the organisation. As accounting system

keeps track on various income and expenses of the company and also provides significant

information about various financial and non financial factors to the management so that they can

further make favourable decisions for the company. Management Accounting provides its

services to public company private company and also the government agencies because all these

companies need day to day information about their expenses and level of income. The main role

of management accounting is to help the management to know about the various investment

budgeting planning and create risk management so that in future, Hichrom do not have to run

short of money. Management Accounting also provides detailed information about the lower

level of accounting in the organisation as well so that management can know the various

expenses of each department. Apart from this Management Accounting helps in forecasting

budgets and also it measures the performance of various strategies which has been made by the

management in past. One of the biggest advantages of management accounting is that it provides

timely information to the management so that they can improvise all the strategies and prepared

new strategies which will provide benefits to the organisation.

Types

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are most common Management Accounting system which present in the organisation such

as traditional cost accounting them in accounting throughput accounting and various Transfer

pricing with the organisation to track down the financial and non-financial information. So that

by focusing on that information company can make further changes in the Strategies and policies

so that their mission can be obtained.

Traditional Management accounting system

This management accounting system is one of the old process and method of Management

Accounting (Zakirova and et.al 2020). This process and technique used for border and process

costing method. The major objective of traditional Management Accounting system is to

determine and analyse how this company distribute various cost on direct materials labour and

different overheads. The main purpose of using this traditional management costing is to analyse

the overall expenses of the company so that they can recover them by earning good income. This

management accounting system is useful for big projects and also the individual projects so that

in big project company has to spend a lot of money on buying material paying wages and salary

to the labour and also they have to work for manufacturing overheads. If the name suggest

process costing distributes the overall cost pictures typically rely on various processes which is

used for producing different goods for the company as a manufacturing of this goods have to go

through a continuous procedure and therefore it becomes difficult for the company to recognise

the cost in each and every process.

Lean accounting system

This is one of the most used Management Accounting systems by each and every organisation

because it does not focus on the individual cost of the production (Sidik 2019). This accounting

system provides a proper strategy to the management so that they can minimise the cost of

production by reducing waste. Therefore this accounting system is very popular. Along with this

clean accounting system also provides financial information for making and creating decisions

by looking at value stream. This helps the management to make accurate decisions so that the

profitability of the organisation can be increased in long run. The main motive of using this

accounting system is to cut down the cost of waste and improvise the profitability.

Throughput accounting

This is not used under traditional Management Accounting system but many manufacturing

companies use this accounting method (Drury, 2018). As this method focuses on recognising the

3

as traditional cost accounting them in accounting throughput accounting and various Transfer

pricing with the organisation to track down the financial and non-financial information. So that

by focusing on that information company can make further changes in the Strategies and policies

so that their mission can be obtained.

Traditional Management accounting system

This management accounting system is one of the old process and method of Management

Accounting (Zakirova and et.al 2020). This process and technique used for border and process

costing method. The major objective of traditional Management Accounting system is to

determine and analyse how this company distribute various cost on direct materials labour and

different overheads. The main purpose of using this traditional management costing is to analyse

the overall expenses of the company so that they can recover them by earning good income. This

management accounting system is useful for big projects and also the individual projects so that

in big project company has to spend a lot of money on buying material paying wages and salary

to the labour and also they have to work for manufacturing overheads. If the name suggest

process costing distributes the overall cost pictures typically rely on various processes which is

used for producing different goods for the company as a manufacturing of this goods have to go

through a continuous procedure and therefore it becomes difficult for the company to recognise

the cost in each and every process.

Lean accounting system

This is one of the most used Management Accounting systems by each and every organisation

because it does not focus on the individual cost of the production (Sidik 2019). This accounting

system provides a proper strategy to the management so that they can minimise the cost of

production by reducing waste. Therefore this accounting system is very popular. Along with this

clean accounting system also provides financial information for making and creating decisions

by looking at value stream. This helps the management to make accurate decisions so that the

profitability of the organisation can be increased in long run. The main motive of using this

accounting system is to cut down the cost of waste and improvise the profitability.

Throughput accounting

This is not used under traditional Management Accounting system but many manufacturing

companies use this accounting method (Drury, 2018). As this method focuses on recognising the

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

constants within the production department of the organisation. Constants speak about

insufficient level of labour material and overheads if the labour and material is insufficient then

company can produce more goods and products. This method is used by manufacturing

companies to reduce the constraints and also increase the volume of production by minimising

the cost.

Transfer pricing management system

This is one of the Common Management Accounting systems which is being used by the

companies and manufacturers to decide the cost of goods as they go through to different

departments. Each product of the company has to go through from various channels and

departments for processing and therefore each product has different cost. Transfer pricing

management system provides different cost for different product as per their life cycle.

P2 Methods of Management accounting reporting

Management accounting which is popularly known as managerial accounting or cost accounting.

As it provides all the inside information about the financial and non financial accounting to the

organisation. Show the management accounting system generates different reports which

produces various financial and non financial information such as planning Regulation and

decision making so that management can overall measures the performance of the organisation.

Therefore various management reports are generated for bookkeeping. These reports are

mentioned below.

Budget report

Budget report plays a very vital and Critical role in the organisation because it helps the

punishment to measure the overall performance of the company. Budget report has been

prepared on the basis of size of the organisation such as small business, medium term business

and for large organisation as well. Budget report can be prepared on department wise as well

however it is important for every company to create budget so that they can know the ground

level information about their business and especially for the cost and expenses. Budget is being

created for unforeseen circumstances if uncertain situation arises in front of the organisation then

how this organisation can be stabilized and the situations do not impact the overall profitability

in production of the organisation (Chaudhry and et.al 2020). This is the main reason of preparing

budget by the companies. As management accounting report will also help the management to

provide better career opportunities to the Employees so that they do not think to switch their

4

insufficient level of labour material and overheads if the labour and material is insufficient then

company can produce more goods and products. This method is used by manufacturing

companies to reduce the constraints and also increase the volume of production by minimising

the cost.

Transfer pricing management system

This is one of the Common Management Accounting systems which is being used by the

companies and manufacturers to decide the cost of goods as they go through to different

departments. Each product of the company has to go through from various channels and

departments for processing and therefore each product has different cost. Transfer pricing

management system provides different cost for different product as per their life cycle.

P2 Methods of Management accounting reporting

Management accounting which is popularly known as managerial accounting or cost accounting.

As it provides all the inside information about the financial and non financial accounting to the

organisation. Show the management accounting system generates different reports which

produces various financial and non financial information such as planning Regulation and

decision making so that management can overall measures the performance of the organisation.

Therefore various management reports are generated for bookkeeping. These reports are

mentioned below.

Budget report

Budget report plays a very vital and Critical role in the organisation because it helps the

punishment to measure the overall performance of the company. Budget report has been

prepared on the basis of size of the organisation such as small business, medium term business

and for large organisation as well. Budget report can be prepared on department wise as well

however it is important for every company to create budget so that they can know the ground

level information about their business and especially for the cost and expenses. Budget is being

created for unforeseen circumstances if uncertain situation arises in front of the organisation then

how this organisation can be stabilized and the situations do not impact the overall profitability

in production of the organisation (Chaudhry and et.al 2020). This is the main reason of preparing

budget by the companies. As management accounting report will also help the management to

provide better career opportunities to the Employees so that they do not think to switch their

4

organisation apart from this by making proper budgets company can produce incentive and

various perks for the employees.

Accounting receivable ageing reports

This accounting report is beneficial for doors business and organisations who fully depend on the

credit extension in such case account receivable ageing report helpful for them (Darvishi and

et.al 2020). It cut down the remaining balance of all the clients for specific period and also helps

the management to recognise the defaulters and find out the problems the process of collection.

With this report management can know how many people are defaulters and to reduce the

number of defaulter management can prepare various policies and Strategies for bad debts.

Cost managerial accounting reports

The entire manufacturer from has to repair cost of article and cost managerial accounting reports

help the organisation prepare various cost of articles. This report provides detailed information

about the raw material which is used for the production apart from this how many overheads are

there in the organisation along with this various wages and salaries of labour is also being added

in this report (Taschner and et.al 2020). Therefore this report provides all the cost which is being

levied on the organisation. By analysing this entire coast company can produce various profit

margins for the product. This report provides a snapshot of all the ghost of production in the cost

of article so that when mint is can make for their policies to cut down the labour cost and

specially the waste of inventory so that the overall profit margin can be increased.

Performance report

The main motive of creating performance report is to review the entire performance of the

company for the accounting period. This report also prepared for analysing the performance of

employee for the accounting period. This report can be prepared on the basis of department as in

the large Corporation there are many departments work in the organisation it is very necessary

to recognise the overall performance of each and every department. Management uses this

performance report to analyse the key strategic performance and decisions for the upcoming

future of the company. With the help of performance report employee forget various promotional

opportunities and they remain committed towards the organisation. The main objective of

creating performance report is to measure the accurate performance of the organisation that is the

strategies helpful for the organisation to achieve their goals and objectives or not?

Other cultural accounting reports

5

various perks for the employees.

Accounting receivable ageing reports

This accounting report is beneficial for doors business and organisations who fully depend on the

credit extension in such case account receivable ageing report helpful for them (Darvishi and

et.al 2020). It cut down the remaining balance of all the clients for specific period and also helps

the management to recognise the defaulters and find out the problems the process of collection.

With this report management can know how many people are defaulters and to reduce the

number of defaulter management can prepare various policies and Strategies for bad debts.

Cost managerial accounting reports

The entire manufacturer from has to repair cost of article and cost managerial accounting reports

help the organisation prepare various cost of articles. This report provides detailed information

about the raw material which is used for the production apart from this how many overheads are

there in the organisation along with this various wages and salaries of labour is also being added

in this report (Taschner and et.al 2020). Therefore this report provides all the cost which is being

levied on the organisation. By analysing this entire coast company can produce various profit

margins for the product. This report provides a snapshot of all the ghost of production in the cost

of article so that when mint is can make for their policies to cut down the labour cost and

specially the waste of inventory so that the overall profit margin can be increased.

Performance report

The main motive of creating performance report is to review the entire performance of the

company for the accounting period. This report also prepared for analysing the performance of

employee for the accounting period. This report can be prepared on the basis of department as in

the large Corporation there are many departments work in the organisation it is very necessary

to recognise the overall performance of each and every department. Management uses this

performance report to analyse the key strategic performance and decisions for the upcoming

future of the company. With the help of performance report employee forget various promotional

opportunities and they remain committed towards the organisation. The main objective of

creating performance report is to measure the accurate performance of the organisation that is the

strategies helpful for the organisation to achieve their goals and objectives or not?

Other cultural accounting reports

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Apart from above records organisation needs to maintain various reports suggest Information

Report project report analysis of competitors report and various other small reports (Leotta, and

et.al 2017). These reports are necessary for the organisation to you know the situation of market

and how their competitors are operating in the market so that as per the competitors and market

situation management can create new strategies. This report helps the management to make

search Strategies for the organisation can produce more quality products and fulfil the demand of

the market.

P3 Cost analysis

Absorption costing

Absorption costing States about the method of costing which states about all the cost of

manufacturing (Le, and et.al 2019). This costing method is being used by the manufacturers so

that they can absorb the overall cost incurred on each and every product. Absorption costing

includes direct and indirect cost so that they can provide better outcome and result to the

organisation. Direct cost includes various materials labours and other which is used for

production. Absorption costing also calculates the appropriate profitability for the organisation

by each and every cost which is being levied on the organisation. This costing helps the company

to obtain a desired profitability.

Marginal costing

Marginal costing works on certain principles and which the variable cost get changed to different

cost units and the fixed cost remain attributable for the relevant period. Marginal cost which

added one additional unit to the output shaft is used by the organisation to determine the

optimum production of the company. This cost helps the organisation to cut down the

unnecessary cost of production and Manufacturing and help them to attain the higher return and

profitability.

Particulars Amount

Direct material £30

Direct Labour £40

Total variable cost per pizza £70

Fixed costs:

6

Report project report analysis of competitors report and various other small reports (Leotta, and

et.al 2017). These reports are necessary for the organisation to you know the situation of market

and how their competitors are operating in the market so that as per the competitors and market

situation management can create new strategies. This report helps the management to make

search Strategies for the organisation can produce more quality products and fulfil the demand of

the market.

P3 Cost analysis

Absorption costing

Absorption costing States about the method of costing which states about all the cost of

manufacturing (Le, and et.al 2019). This costing method is being used by the manufacturers so

that they can absorb the overall cost incurred on each and every product. Absorption costing

includes direct and indirect cost so that they can provide better outcome and result to the

organisation. Direct cost includes various materials labours and other which is used for

production. Absorption costing also calculates the appropriate profitability for the organisation

by each and every cost which is being levied on the organisation. This costing helps the company

to obtain a desired profitability.

Marginal costing

Marginal costing works on certain principles and which the variable cost get changed to different

cost units and the fixed cost remain attributable for the relevant period. Marginal cost which

added one additional unit to the output shaft is used by the organisation to determine the

optimum production of the company. This cost helps the organisation to cut down the

unnecessary cost of production and Manufacturing and help them to attain the higher return and

profitability.

Particulars Amount

Direct material £30

Direct Labour £40

Total variable cost per pizza £70

Fixed costs:

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

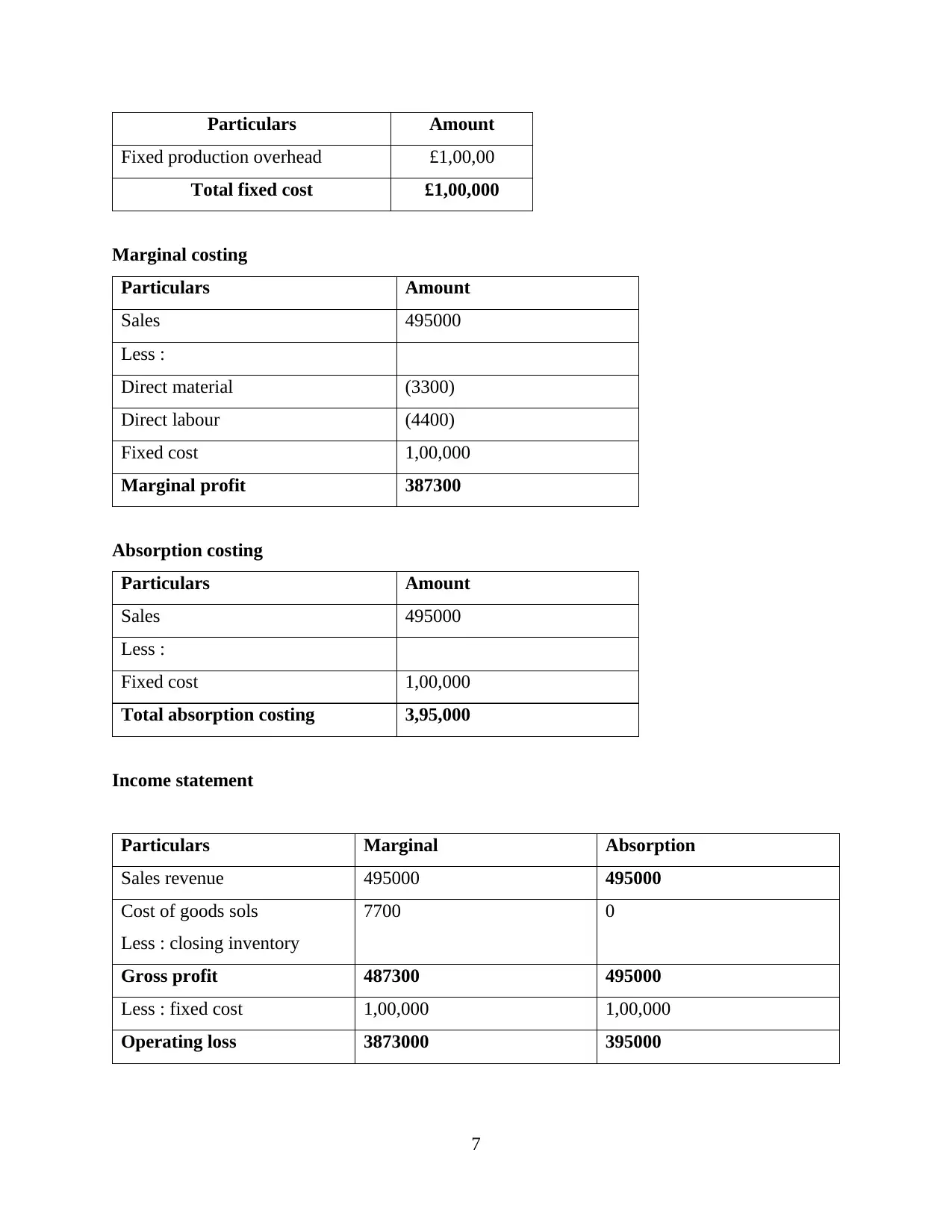

Particulars Amount

Fixed production overhead £1,00,00

Total fixed cost £1,00,000

Marginal costing

Particulars Amount

Sales 495000

Less :

Direct material (3300)

Direct labour (4400)

Fixed cost 1,00,000

Marginal profit 387300

Absorption costing

Particulars Amount

Sales 495000

Less :

Fixed cost 1,00,000

Total absorption costing 3,95,000

Income statement

Particulars Marginal Absorption

Sales revenue 495000 495000

Cost of goods sols

Less : closing inventory

7700 0

Gross profit 487300 495000

Less : fixed cost 1,00,000 1,00,000

Operating loss 3873000 395000

7

Fixed production overhead £1,00,00

Total fixed cost £1,00,000

Marginal costing

Particulars Amount

Sales 495000

Less :

Direct material (3300)

Direct labour (4400)

Fixed cost 1,00,000

Marginal profit 387300

Absorption costing

Particulars Amount

Sales 495000

Less :

Fixed cost 1,00,000

Total absorption costing 3,95,000

Income statement

Particulars Marginal Absorption

Sales revenue 495000 495000

Cost of goods sols

Less : closing inventory

7700 0

Gross profit 487300 495000

Less : fixed cost 1,00,000 1,00,000

Operating loss 3873000 395000

7

P4 Advantages and disadvantages of different planning tools of budgetary control

For the purpose of budgetary control organisation and its management has decreased different

planning tools so that they can help the organisation to achieve all the predetermined goals.

There are various planning tools have been used by the organisation such as budget to volume

profit analysis and various pricing strategies of the organisation so that it helps them to improve

the overall sales and revenue in the market.

Budget

As budget is a detail statement of various expected financial and non financial expenses of the

organisation. The main objective of creating budget is to analyse the overall expenses and

revenue for a defined period of time organisation. So that if the expenses are higher than the

revenue then management can improvise them within the given time period of future. Budgetary

control is a planning tool which is prepared to plant and control the overall production and sales

of product and services (Laela and et.al 2018). It also promotes the communication and

coordination of different departments and it also bring encouragement to managers so that they

can evaluate the performance of the organisation and achieve the predetermined goal.

Advantages

Budgetary report is necessary for creating healthy coordination and communication between all

the departments of the organisation. To help the management to translate the strategic plans and

in force them into action and specify the various resources and revenue different activities which

is used for strategic plan and their enforceability. It also produces and excellent record about the

different activities of the organisation. It helps in improving the coordination and communication

between the employees as well so that the match wills all the relevant information with each

other. It also improves the overall uses of resources and their location so that all the needs of

different departments can be clarified and justified.

Disadvantage

There are many disadvantages of budgetary report as well because it takes a lot of time in

research then only it can provide suitable and beneficial results to the organisation. Apart from

this sometimes projected budget to not meet with the actual result so the organisation has to face

loss as well (Mogues, and et.al 2020). It also decreases the fairness of the organisation if that do

not meet the Expectations of different departments then conflict take place among various

departments. Budget make it field when any inverse situation arises in front of the organisation

8

For the purpose of budgetary control organisation and its management has decreased different

planning tools so that they can help the organisation to achieve all the predetermined goals.

There are various planning tools have been used by the organisation such as budget to volume

profit analysis and various pricing strategies of the organisation so that it helps them to improve

the overall sales and revenue in the market.

Budget

As budget is a detail statement of various expected financial and non financial expenses of the

organisation. The main objective of creating budget is to analyse the overall expenses and

revenue for a defined period of time organisation. So that if the expenses are higher than the

revenue then management can improvise them within the given time period of future. Budgetary

control is a planning tool which is prepared to plant and control the overall production and sales

of product and services (Laela and et.al 2018). It also promotes the communication and

coordination of different departments and it also bring encouragement to managers so that they

can evaluate the performance of the organisation and achieve the predetermined goal.

Advantages

Budgetary report is necessary for creating healthy coordination and communication between all

the departments of the organisation. To help the management to translate the strategic plans and

in force them into action and specify the various resources and revenue different activities which

is used for strategic plan and their enforceability. It also produces and excellent record about the

different activities of the organisation. It helps in improving the coordination and communication

between the employees as well so that the match wills all the relevant information with each

other. It also improves the overall uses of resources and their location so that all the needs of

different departments can be clarified and justified.

Disadvantage

There are many disadvantages of budgetary report as well because it takes a lot of time in

research then only it can provide suitable and beneficial results to the organisation. Apart from

this sometimes projected budget to not meet with the actual result so the organisation has to face

loss as well (Mogues, and et.al 2020). It also decreases the fairness of the organisation if that do

not meet the Expectations of different departments then conflict take place among various

departments. Budget make it field when any inverse situation arises in front of the organisation

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

so that in such situation it can demotivate the employees and increases the absenteeism in the

organisation.

Cost volume profit analysis

Cost volume profit analysis is also being used by various organisations to know the level of sales

and the overall cost of production so your organisation can generate better and Hike operating

profit. As the name suggests this method why do all the detailed information about the cost of the

goods which is implemented on in the process of manufacturing (Abernethy and et.al 2019). So

with the help of cost volume profit analysis management can easily know how much cost will be

implemented on each and every product so that they can generate high profit margin by selling

such products in the market. Along with this cost volume profit analysis also analyse about fixed

cost and variable cost so that management can deduct variable cost and improve the overall

profitability for the organisation.

Advantages

The key advantage of Cost volume profit analysis is that it is very easy to calculate and

management can easily use this method to know the overall profitability of the product. Apart

from this Cost volume profit analysis do not consider more rules regulations and Standards

therefore most of the organisation uses this method because it is very easy to implement within

the organisation as management do not have to follow many rules and regulations. This method

also assists management to create various strategies policies and plans for the organisation and

also to enhance the profitability of the company. This method helps the management to cut down

the unnecessary cost of production of the product so that the overall profitability can be

increased.

Disadvantage

This method is very time consuming and takes a lot of time to provide productively result to the

management (Osim and et.al 2020). So that sometimes by using this method organisation can use

various good opportunities to increase the sales and revenue. It also sometimes brings

miscommunication within the organisation and employees so that the entire process of

production can become lengthy and when the production gets lengthy then it is unable for the

company to fulfil the market demand. It is very necessary for the organisation to maintain the

overall supply in the market so that their loyal customers do not get switch to other companies

and especially to the competitors. Therefore this method can become little expensive for the

9

organisation.

Cost volume profit analysis

Cost volume profit analysis is also being used by various organisations to know the level of sales

and the overall cost of production so your organisation can generate better and Hike operating

profit. As the name suggests this method why do all the detailed information about the cost of the

goods which is implemented on in the process of manufacturing (Abernethy and et.al 2019). So

with the help of cost volume profit analysis management can easily know how much cost will be

implemented on each and every product so that they can generate high profit margin by selling

such products in the market. Along with this cost volume profit analysis also analyse about fixed

cost and variable cost so that management can deduct variable cost and improve the overall

profitability for the organisation.

Advantages

The key advantage of Cost volume profit analysis is that it is very easy to calculate and

management can easily use this method to know the overall profitability of the product. Apart

from this Cost volume profit analysis do not consider more rules regulations and Standards

therefore most of the organisation uses this method because it is very easy to implement within

the organisation as management do not have to follow many rules and regulations. This method

also assists management to create various strategies policies and plans for the organisation and

also to enhance the profitability of the company. This method helps the management to cut down

the unnecessary cost of production of the product so that the overall profitability can be

increased.

Disadvantage

This method is very time consuming and takes a lot of time to provide productively result to the

management (Osim and et.al 2020). So that sometimes by using this method organisation can use

various good opportunities to increase the sales and revenue. It also sometimes brings

miscommunication within the organisation and employees so that the entire process of

production can become lengthy and when the production gets lengthy then it is unable for the

company to fulfil the market demand. It is very necessary for the organisation to maintain the

overall supply in the market so that their loyal customers do not get switch to other companies

and especially to the competitors. Therefore this method can become little expensive for the

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company because it takes a lot of time to produce quality results which will put negative impact

on the profitability of the organisation.

Pricing strategies

Strategy for pricing is one of the important tool for the organisation because the overall

profitability totally depends on the pricing strategy of the company. Company can’t charge

higher prices from the consumers if the company charge higher prices compared to their

competitors then the survival of the company will become very difficult. As no one consumer

wants to spend a lot of money on goods and services if they get same products at cheaper prices

so if the company has adopted high pricing strategy then they may face loss in the future. On the

other hand if the company set very low prices as compared to their competitors then it becomes

very difficult for the company to attain predetermined objective and profit.

Advantages

The management of the organisation has set a great pricing strategy for the company then

company will get in men’s growth and also increase the profitability for accounting period (Hung

and et.al 2019). But on the other hand if the pricing strategy of the company is not fruitful and it

is not working in the favour of the company then and it becomes very difficult to survive and

give the competition to the competitors because no one consumer will buy similar products at

Higher or cheaper prices. With the help of pricing strategy company can the price of each and

every product.

Disadvantages

Pricing strategy has a lot of disadvantages as well because consumer wants every product at

cheap prices and therefore to attract new consumers sometimes company provide cheap products

which will hamper the profitability and overall goal of the company.

P5 Different Management accounting system

Each and every organisation uses different accounting system so that they can predict the profit

and also recognise all the issues which are concerned with the financial and non financial factors.

Financial factors are those which greatly impact the financial aspects, profitability and financial

decisions of the company. And non financial factors are related with the human resources and

other resources of the company.

Solvency ratio

10

on the profitability of the organisation.

Pricing strategies

Strategy for pricing is one of the important tool for the organisation because the overall

profitability totally depends on the pricing strategy of the company. Company can’t charge

higher prices from the consumers if the company charge higher prices compared to their

competitors then the survival of the company will become very difficult. As no one consumer

wants to spend a lot of money on goods and services if they get same products at cheaper prices

so if the company has adopted high pricing strategy then they may face loss in the future. On the

other hand if the company set very low prices as compared to their competitors then it becomes

very difficult for the company to attain predetermined objective and profit.

Advantages

The management of the organisation has set a great pricing strategy for the company then

company will get in men’s growth and also increase the profitability for accounting period (Hung

and et.al 2019). But on the other hand if the pricing strategy of the company is not fruitful and it

is not working in the favour of the company then and it becomes very difficult to survive and

give the competition to the competitors because no one consumer will buy similar products at

Higher or cheaper prices. With the help of pricing strategy company can the price of each and

every product.

Disadvantages

Pricing strategy has a lot of disadvantages as well because consumer wants every product at

cheap prices and therefore to attract new consumers sometimes company provide cheap products

which will hamper the profitability and overall goal of the company.

P5 Different Management accounting system

Each and every organisation uses different accounting system so that they can predict the profit

and also recognise all the issues which are concerned with the financial and non financial factors.

Financial factors are those which greatly impact the financial aspects, profitability and financial

decisions of the company. And non financial factors are related with the human resources and

other resources of the company.

Solvency ratio

10

Solvency ratio is a valuable tool which used to determine the overall quality and capacity of the

organisation to meet all long term obligations of the company (Emrich, 2020). The main

objective of using solvency ratio is that management want to determine do the company has

proper cash flow or not so that with help of proper cash flow company can meet all its long-term

liabilities and obligations. Solvency ratio States about the overall financial health of the

organisation and it also mitigate the chances of default.

Profitability ratio

Profitability ratio is measures the financial sector in the organisation and it also measures the

ability of the company to generate earnings. Profitability ratio also considers operating cost

various revenues equity of shareholders and all the data which is related to the revenue of the

company for specific time duration. It can be compared with the efficiency ratio of the company

because profitability is also measured how a company is able to generate revenue and income by

using their assets properly.

Liquidity ratio

Liquidity ratio refers to the current ratio of the company. This ratio talks about the current assets

of the company these ratio current assets of the company should be properly managed so that

organisation can repay short term liabilities with the help of current assets. Apart from this if the

current ratio of any company is a strong then they can manage working capital effectively (Laela

and et.al 2018). Every organisation needs sufficient working capital so that they can’t prepare to

their apart from this working capital is necessary to make payments of labour and also their

wages. If the working capital is in good position then the organisation can easily get fund from

different sources because if the organisation has trumpeting capital then they can easily repay

their short-term as well as long-term obligations.

Non financial factors

Managing human resources

The overall management of human resources is very necessary for the Welfare and development

of the. As human resources are the one who work effectively in the organisation therefore the

company can attain its predetermined goals and objectives. So organisation must abide that

human resources are the valuable asset for the company. It is the duty of organisation that they

must provide all the training and learning opportunity to the Employees so that they can enhance

their knowledge and skills and produce more quality products and work within the organisation.

11

organisation to meet all long term obligations of the company (Emrich, 2020). The main

objective of using solvency ratio is that management want to determine do the company has

proper cash flow or not so that with help of proper cash flow company can meet all its long-term

liabilities and obligations. Solvency ratio States about the overall financial health of the

organisation and it also mitigate the chances of default.

Profitability ratio

Profitability ratio is measures the financial sector in the organisation and it also measures the

ability of the company to generate earnings. Profitability ratio also considers operating cost

various revenues equity of shareholders and all the data which is related to the revenue of the

company for specific time duration. It can be compared with the efficiency ratio of the company

because profitability is also measured how a company is able to generate revenue and income by

using their assets properly.

Liquidity ratio

Liquidity ratio refers to the current ratio of the company. This ratio talks about the current assets

of the company these ratio current assets of the company should be properly managed so that

organisation can repay short term liabilities with the help of current assets. Apart from this if the

current ratio of any company is a strong then they can manage working capital effectively (Laela

and et.al 2018). Every organisation needs sufficient working capital so that they can’t prepare to

their apart from this working capital is necessary to make payments of labour and also their

wages. If the working capital is in good position then the organisation can easily get fund from

different sources because if the organisation has trumpeting capital then they can easily repay

their short-term as well as long-term obligations.

Non financial factors

Managing human resources

The overall management of human resources is very necessary for the Welfare and development

of the. As human resources are the one who work effectively in the organisation therefore the

company can attain its predetermined goals and objectives. So organisation must abide that

human resources are the valuable asset for the company. It is the duty of organisation that they

must provide all the training and learning opportunity to the Employees so that they can enhance

their knowledge and skills and produce more quality products and work within the organisation.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.