Operational Budgets: Analysis, Types, and Financial Statements

VerifiedAdded on 2020/12/18

|16

|4737

|131

Report

AI Summary

This report provides a comprehensive overview of operational budgets, encompassing various aspects of financial planning and analysis. It begins with an introduction to budgets, their significance, and the different types, including master, static, and sales budgets, along with budgetary control principles. The report emphasizes the importance of discussing budgets with colleagues and peers for effective planning and covers the preparation of budgeted profit and loss statements. It delves into practical examples, such as sales, purchase, and cash budgets, providing detailed calculations and working notes. Furthermore, the report includes variance analysis, forecasting techniques, and a discussion on double-entry accounting, offering a holistic understanding of financial management. The report also features a presentation on the same topics, enhancing the learning experience.

Prepare Operational

Budgets

Budgets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

ASSESSMENT ACTIVITY 1.........................................................................................................3

Task 1.1........................................................................................................................................3

Task 1.2........................................................................................................................................4

Task 1.3........................................................................................................................................4

Task 1.4........................................................................................................................................5

Task 1.5........................................................................................................................................5

Task 1.6........................................................................................................................................6

Task 1.7........................................................................................................................................7

Task 1.8........................................................................................................................................8

Task 1.9........................................................................................................................................8

ASSESSMENT ACTIVITY 2.......................................................................................................10

Task 2.1......................................................................................................................................10

Task 2.2......................................................................................................................................10

Task 2.3......................................................................................................................................10

Task 2.4......................................................................................................................................11

Task 2.5......................................................................................................................................11

Task 2.6......................................................................................................................................12

Task 2.7......................................................................................................................................13

Task 2.8......................................................................................................................................14

Task 2.9......................................................................................................................................15

CONCLUSION..............................................................................................................................16

ASSESSMENT ACTIVITY 3 – PRESENTATION.....................................................................17

INTRODUCTION ........................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

ASSESSMENT ACTIVITY 1.........................................................................................................3

Task 1.1........................................................................................................................................3

Task 1.2........................................................................................................................................4

Task 1.3........................................................................................................................................4

Task 1.4........................................................................................................................................5

Task 1.5........................................................................................................................................5

Task 1.6........................................................................................................................................6

Task 1.7........................................................................................................................................7

Task 1.8........................................................................................................................................8

Task 1.9........................................................................................................................................8

ASSESSMENT ACTIVITY 2.......................................................................................................10

Task 2.1......................................................................................................................................10

Task 2.2......................................................................................................................................10

Task 2.3......................................................................................................................................10

Task 2.4......................................................................................................................................11

Task 2.5......................................................................................................................................11

Task 2.6......................................................................................................................................12

Task 2.7......................................................................................................................................13

Task 2.8......................................................................................................................................14

Task 2.9......................................................................................................................................15

CONCLUSION..............................................................................................................................16

ASSESSMENT ACTIVITY 3 – PRESENTATION.....................................................................17

INTRODUCTION ........................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Budgets are significant aspects of business organisation and essential to assess actual

performance of organisation during a particular period. Budgets are not only provide a

framework for assessment of performance bust also gives a detailed comparison of financial data

to make vital decisions. Operational budget is kind of budget of that gives a detailed estimation

of cost and expenditures associated with different functions and operations. It is generally

prepared on annual basis or for short term period (McDonald and Wilson, 2016). This type of

budget includes items such as labour, marketing, administration and other production related

costs. This report exhibits a complete discussion about budget, various types of budgets and

importance of budget of different budgets in business organisation along with practical sums

related to preparation of budgets like cash budgets, purchase budgets, sales budgets based on

different criteria, income statement and statement of financial position.

ASSESSMENT ACTIVITY 1

Task 1.1

Budget: Budget is the estimation of the expense which will be incurred and the incomes

which can be generated in a specific period of time. Budget is used as a internal tool in an

organisation by the management to know the estimation of profit or loss and to redevelop their

strategies to convert the loss in profit. Budget can be prepared before acquiring a new assets to

estimate the cost and the to check whether the assets purchased is in the budget of the company

or not.

Types of budget: Following are the types of budget use by the organisation to see the

estimation:

Master Budget: Master budget is defined as a overall budget to carry out an operation or

to know the estimation of the profit or loss of the company. It is known as a summary of

all the other types of budget (Raudla, 2012).

Static Budget: A budget that is left unaltered even if there is a change in the factor

related to sales volume or income is called the static budget. This type of budget remains

fixed during the whole accounting period.

Budgets are significant aspects of business organisation and essential to assess actual

performance of organisation during a particular period. Budgets are not only provide a

framework for assessment of performance bust also gives a detailed comparison of financial data

to make vital decisions. Operational budget is kind of budget of that gives a detailed estimation

of cost and expenditures associated with different functions and operations. It is generally

prepared on annual basis or for short term period (McDonald and Wilson, 2016). This type of

budget includes items such as labour, marketing, administration and other production related

costs. This report exhibits a complete discussion about budget, various types of budgets and

importance of budget of different budgets in business organisation along with practical sums

related to preparation of budgets like cash budgets, purchase budgets, sales budgets based on

different criteria, income statement and statement of financial position.

ASSESSMENT ACTIVITY 1

Task 1.1

Budget: Budget is the estimation of the expense which will be incurred and the incomes

which can be generated in a specific period of time. Budget is used as a internal tool in an

organisation by the management to know the estimation of profit or loss and to redevelop their

strategies to convert the loss in profit. Budget can be prepared before acquiring a new assets to

estimate the cost and the to check whether the assets purchased is in the budget of the company

or not.

Types of budget: Following are the types of budget use by the organisation to see the

estimation:

Master Budget: Master budget is defined as a overall budget to carry out an operation or

to know the estimation of the profit or loss of the company. It is known as a summary of

all the other types of budget (Raudla, 2012).

Static Budget: A budget that is left unaltered even if there is a change in the factor

related to sales volume or income is called the static budget. This type of budget remains

fixed during the whole accounting period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales Budget: A sale budget is a budget which is prepared to to see the estimated total

sales revenue and all the selling expense including the cost of goods sold during the year

to know the estimated operating profit (Engel, 2015).

Budgetary control principles: Budgetary control is a system that helps the organisation

to control its cost including the cost of preparation of the budget and than comparing it with the

actual performance to maximize the profit. The basic principles of budgetary control is to

compare the budgeted performance with the actual performance and calculate the variance and

also to find out the reason for the differences.

Task 1.2

Yes, it is very important to discuss the budget with colleagues and peers to determine the

scope and nature of budget planning. As budgeting is the most important part of any financial

planning. Discussing it with peers and colleagues will help to understand the parts of budget as

in an organisation there are many people working under different department. Budgeting will

help the organisation to keep the track of expense. It is considered as an essential tool to convert

the general plan into a specific plan to achieve the greater result for the organisation. In the

budget sufficient details are given to anticipate the cost and all the expenses and the income

which will be generated through the operation for which the budget is prepared (Singer, 2012). It

helps the line managers to work with caution and care and also guides the mangers in

formulating policies which can help the organisation to achieve the organisational goal. By

discussing the budget with peers and colleagues helps to decentralize the obligations. Profit

mindedness environment is created in the organisation which motivates the employees to work

more efficiently. Budget also helps the top level of management to measure its performance of

different departments in an organisation. Through budget sales department can see the product

which are no giving profit and can also stop the sales of these products and services.

Task 1.3

Expected fees 350000.00

Marketing expense:

Fixed Advertising (6,800 per annum) 81600.00

Advertising (4 % of Expected fees) 14000.00

Financial expense

Interest paid (1,400 per month) 16800.00

sales revenue and all the selling expense including the cost of goods sold during the year

to know the estimated operating profit (Engel, 2015).

Budgetary control principles: Budgetary control is a system that helps the organisation

to control its cost including the cost of preparation of the budget and than comparing it with the

actual performance to maximize the profit. The basic principles of budgetary control is to

compare the budgeted performance with the actual performance and calculate the variance and

also to find out the reason for the differences.

Task 1.2

Yes, it is very important to discuss the budget with colleagues and peers to determine the

scope and nature of budget planning. As budgeting is the most important part of any financial

planning. Discussing it with peers and colleagues will help to understand the parts of budget as

in an organisation there are many people working under different department. Budgeting will

help the organisation to keep the track of expense. It is considered as an essential tool to convert

the general plan into a specific plan to achieve the greater result for the organisation. In the

budget sufficient details are given to anticipate the cost and all the expenses and the income

which will be generated through the operation for which the budget is prepared (Singer, 2012). It

helps the line managers to work with caution and care and also guides the mangers in

formulating policies which can help the organisation to achieve the organisational goal. By

discussing the budget with peers and colleagues helps to decentralize the obligations. Profit

mindedness environment is created in the organisation which motivates the employees to work

more efficiently. Budget also helps the top level of management to measure its performance of

different departments in an organisation. Through budget sales department can see the product

which are no giving profit and can also stop the sales of these products and services.

Task 1.3

Expected fees 350000.00

Marketing expense:

Fixed Advertising (6,800 per annum) 81600.00

Advertising (4 % of Expected fees) 14000.00

Financial expense

Interest paid (1,400 per month) 16800.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

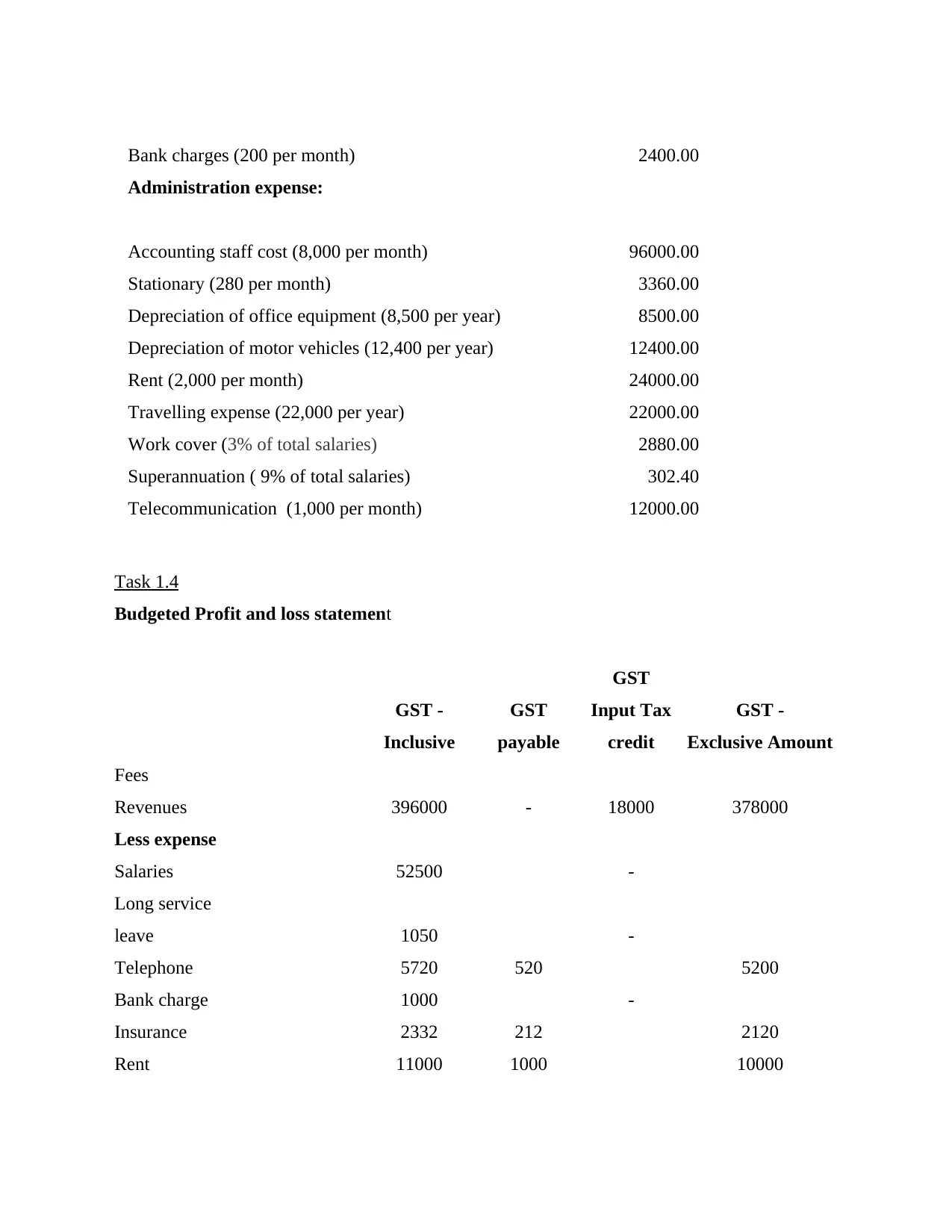

Bank charges (200 per month) 2400.00

Administration expense:

Accounting staff cost (8,000 per month) 96000.00

Stationary (280 per month) 3360.00

Depreciation of office equipment (8,500 per year) 8500.00

Depreciation of motor vehicles (12,400 per year) 12400.00

Rent (2,000 per month) 24000.00

Travelling expense (22,000 per year) 22000.00

Work cover (3% of total salaries) 2880.00

Superannuation ( 9% of total salaries) 302.40

Telecommunication (1,000 per month) 12000.00

Task 1.4

Budgeted Profit and loss statement

GST -

Inclusive

GST

payable

GST

Input Tax

credit

GST -

Exclusive Amount

Fees

Revenues 396000 - 18000 378000

Less expense

Salaries 52500 -

Long service

leave 1050 -

Telephone 5720 520 5200

Bank charge 1000 -

Insurance 2332 212 2120

Rent 11000 1000 10000

Administration expense:

Accounting staff cost (8,000 per month) 96000.00

Stationary (280 per month) 3360.00

Depreciation of office equipment (8,500 per year) 8500.00

Depreciation of motor vehicles (12,400 per year) 12400.00

Rent (2,000 per month) 24000.00

Travelling expense (22,000 per year) 22000.00

Work cover (3% of total salaries) 2880.00

Superannuation ( 9% of total salaries) 302.40

Telecommunication (1,000 per month) 12000.00

Task 1.4

Budgeted Profit and loss statement

GST -

Inclusive

GST

payable

GST

Input Tax

credit

GST -

Exclusive Amount

Fees

Revenues 396000 - 18000 378000

Less expense

Salaries 52500 -

Long service

leave 1050 -

Telephone 5720 520 5200

Bank charge 1000 -

Insurance 2332 212 2120

Rent 11000 1000 10000

Profit 322398 1732 18000 360680

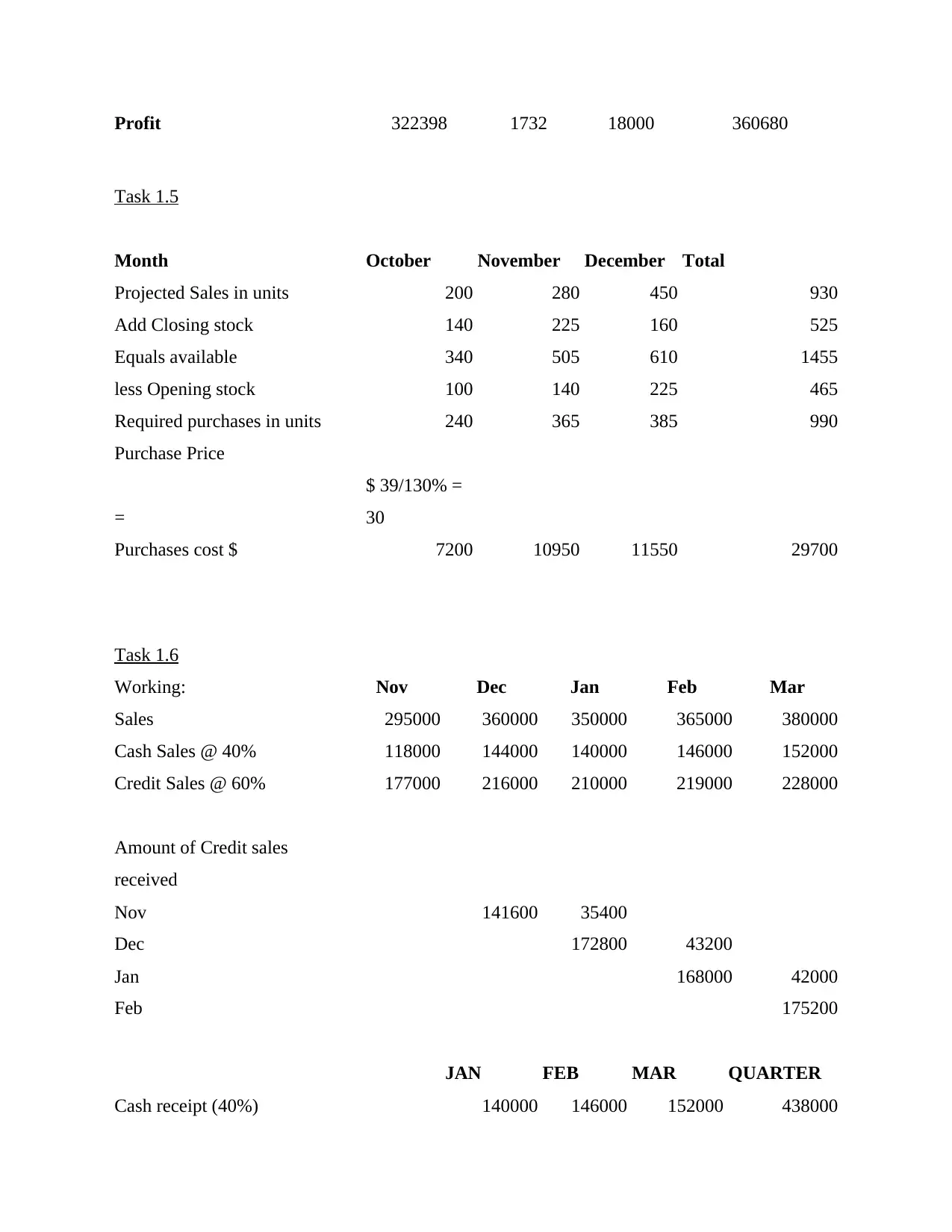

Task 1.5

Month October November December Total

Projected Sales in units 200 280 450 930

Add Closing stock 140 225 160 525

Equals available 340 505 610 1455

less Opening stock 100 140 225 465

Required purchases in units 240 365 385 990

Purchase Price

=

$ 39/130% =

30

Purchases cost $ 7200 10950 11550 29700

Task 1.6

Working: Nov Dec Jan Feb Mar

Sales 295000 360000 350000 365000 380000

Cash Sales @ 40% 118000 144000 140000 146000 152000

Credit Sales @ 60% 177000 216000 210000 219000 228000

Amount of Credit sales

received

Nov 141600 35400

Dec 172800 43200

Jan 168000 42000

Feb 175200

JAN FEB MAR QUARTER

Cash receipt (40%) 140000 146000 152000 438000

Task 1.5

Month October November December Total

Projected Sales in units 200 280 450 930

Add Closing stock 140 225 160 525

Equals available 340 505 610 1455

less Opening stock 100 140 225 465

Required purchases in units 240 365 385 990

Purchase Price

=

$ 39/130% =

30

Purchases cost $ 7200 10950 11550 29700

Task 1.6

Working: Nov Dec Jan Feb Mar

Sales 295000 360000 350000 365000 380000

Cash Sales @ 40% 118000 144000 140000 146000 152000

Credit Sales @ 60% 177000 216000 210000 219000 228000

Amount of Credit sales

received

Nov 141600 35400

Dec 172800 43200

Jan 168000 42000

Feb 175200

JAN FEB MAR QUARTER

Cash receipt (40%) 140000 146000 152000 438000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

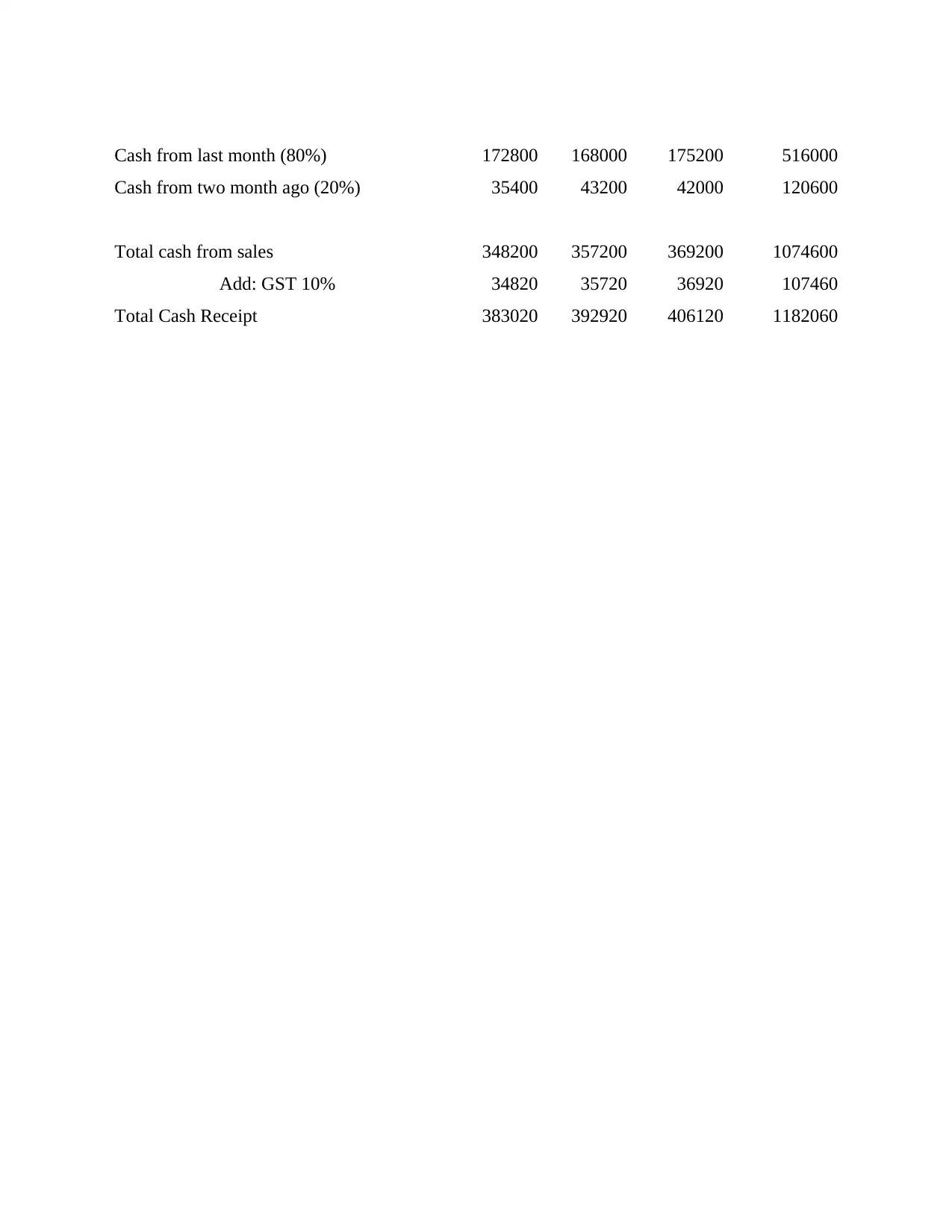

Cash from last month (80%) 172800 168000 175200 516000

Cash from two month ago (20%) 35400 43200 42000 120600

Total cash from sales 348200 357200 369200 1074600

Add: GST 10% 34820 35720 36920 107460

Total Cash Receipt 383020 392920 406120 1182060

Cash from two month ago (20%) 35400 43200 42000 120600

Total cash from sales 348200 357200 369200 1074600

Add: GST 10% 34820 35720 36920 107460

Total Cash Receipt 383020 392920 406120 1182060

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nov Dec Jan Feb Mar

Purchase (60% of sales) 177000 216000 210000 219000 228000

Credit Purchase 177000 216000 210000 219000 228000

Amount of Credit purchase

paid 177000 216000 210000 219000

Cash payments

JAN FEB MAR QUARTER

Cash purchase last month 216000 210000 219000 645000

Add: GST 10% 21600 21000 21900 64500

Total cash Payments 237600 231000 240900 709500

The summary statement

JAN FEB MAR QUARTER

Total actual receipt 383020 392920 406120 1182060

Total cash Payments 237600 231000 240900 709500

Surplus 145420 161920 165220 472560

Opening balance -35400 110020 271940 346560

Closing cash balance 110020 271940 437160 819120

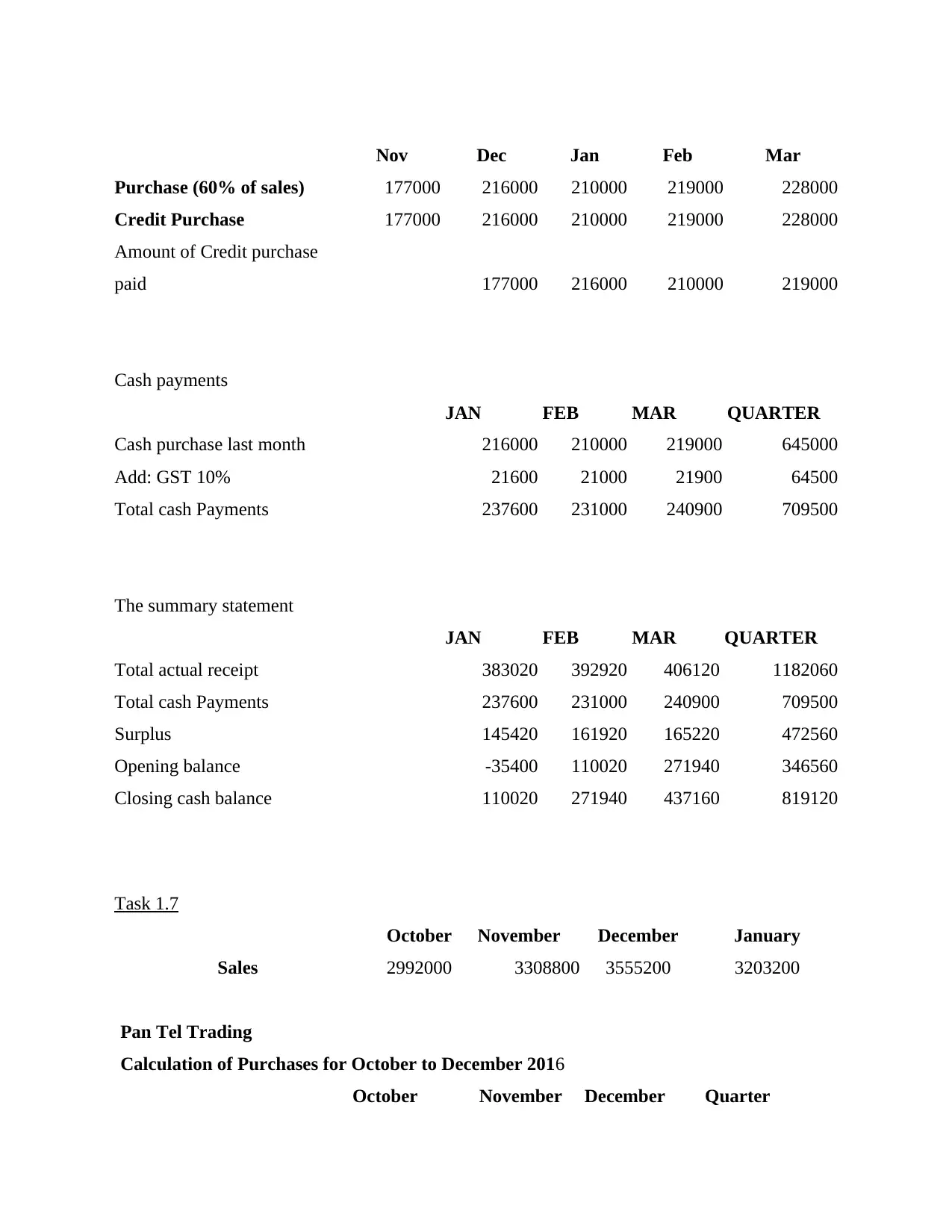

Task 1.7

October November December January

Sales 2992000 3308800 3555200 3203200

Pan Tel Trading

Calculation of Purchases for October to December 2016

October November December Quarter

Purchase (60% of sales) 177000 216000 210000 219000 228000

Credit Purchase 177000 216000 210000 219000 228000

Amount of Credit purchase

paid 177000 216000 210000 219000

Cash payments

JAN FEB MAR QUARTER

Cash purchase last month 216000 210000 219000 645000

Add: GST 10% 21600 21000 21900 64500

Total cash Payments 237600 231000 240900 709500

The summary statement

JAN FEB MAR QUARTER

Total actual receipt 383020 392920 406120 1182060

Total cash Payments 237600 231000 240900 709500

Surplus 145420 161920 165220 472560

Opening balance -35400 110020 271940 346560

Closing cash balance 110020 271940 437160 819120

Task 1.7

October November December January

Sales 2992000 3308800 3555200 3203200

Pan Tel Trading

Calculation of Purchases for October to December 2016

October November December Quarter

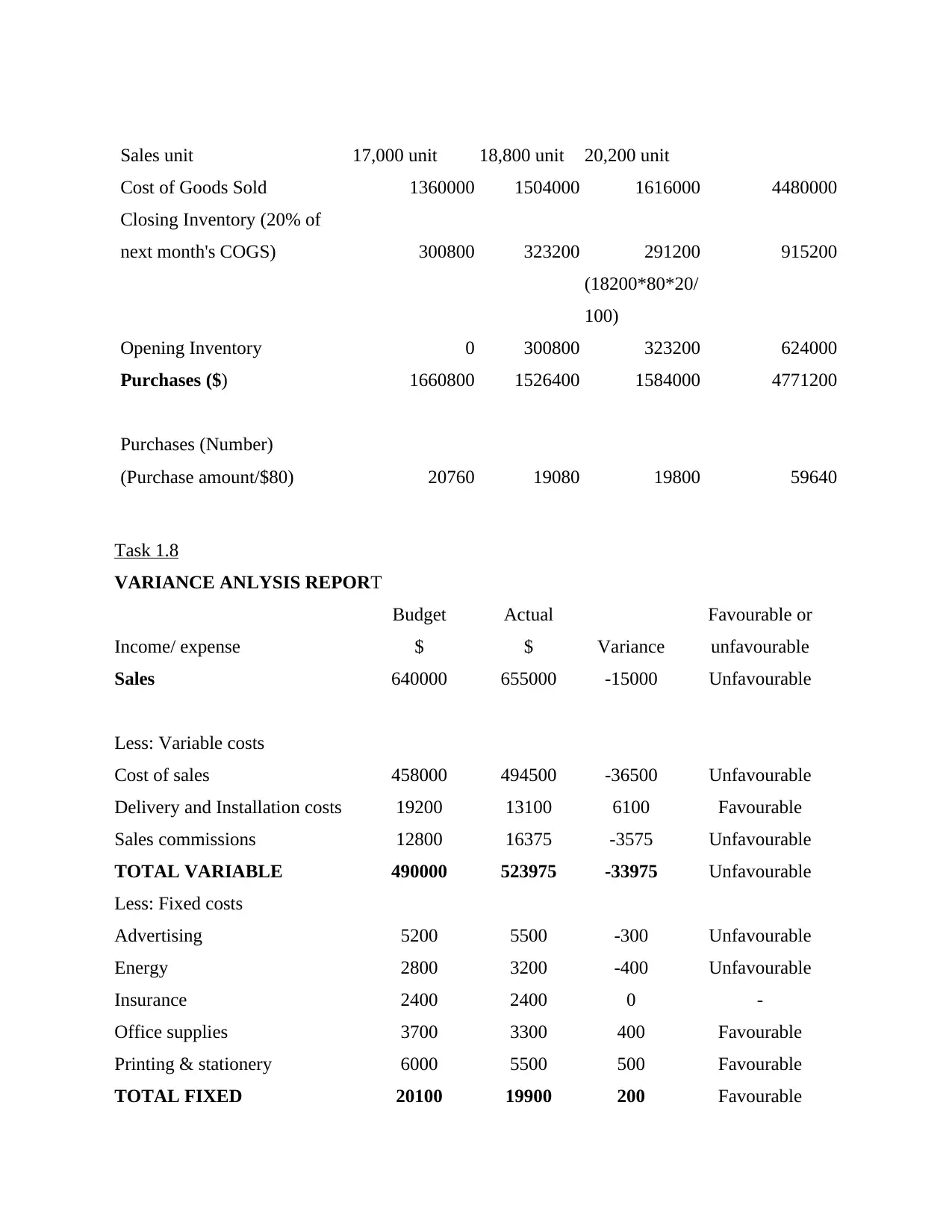

Sales unit 17,000 unit 18,800 unit 20,200 unit

Cost of Goods Sold 1360000 1504000 1616000 4480000

Closing Inventory (20% of

next month's COGS) 300800 323200 291200 915200

(18200*80*20/

100)

Opening Inventory 0 300800 323200 624000

Purchases ($) 1660800 1526400 1584000 4771200

Purchases (Number)

(Purchase amount/$80) 20760 19080 19800 59640

Task 1.8

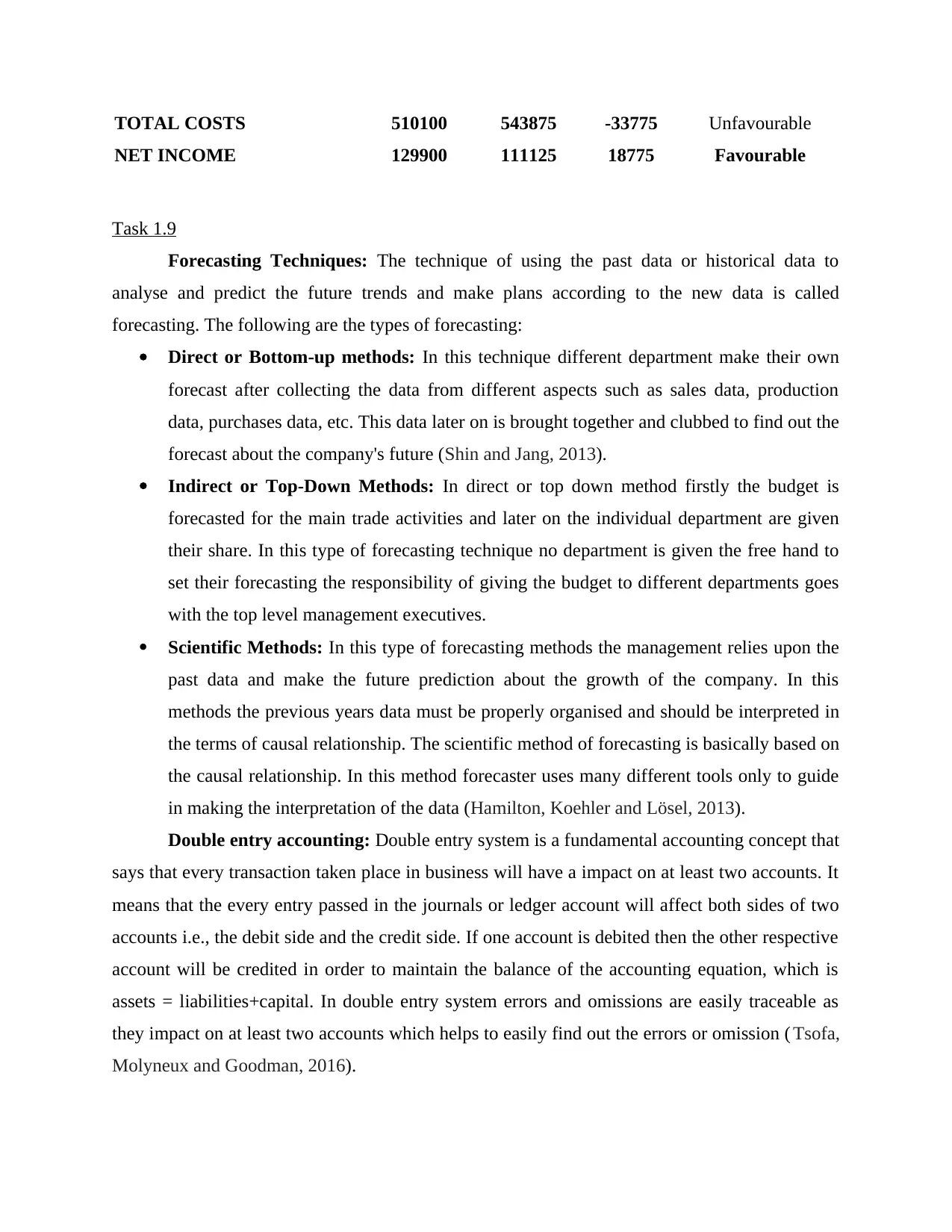

VARIANCE ANLYSIS REPORT

Income/ expense

Budget

$

Actual

$ Variance

Favourable or

unfavourable

Sales 640000 655000 -15000 Unfavourable

Less: Variable costs

Cost of sales 458000 494500 -36500 Unfavourable

Delivery and Installation costs 19200 13100 6100 Favourable

Sales commissions 12800 16375 -3575 Unfavourable

TOTAL VARIABLE 490000 523975 -33975 Unfavourable

Less: Fixed costs

Advertising 5200 5500 -300 Unfavourable

Energy 2800 3200 -400 Unfavourable

Insurance 2400 2400 0 -

Office supplies 3700 3300 400 Favourable

Printing & stationery 6000 5500 500 Favourable

TOTAL FIXED 20100 19900 200 Favourable

Cost of Goods Sold 1360000 1504000 1616000 4480000

Closing Inventory (20% of

next month's COGS) 300800 323200 291200 915200

(18200*80*20/

100)

Opening Inventory 0 300800 323200 624000

Purchases ($) 1660800 1526400 1584000 4771200

Purchases (Number)

(Purchase amount/$80) 20760 19080 19800 59640

Task 1.8

VARIANCE ANLYSIS REPORT

Income/ expense

Budget

$

Actual

$ Variance

Favourable or

unfavourable

Sales 640000 655000 -15000 Unfavourable

Less: Variable costs

Cost of sales 458000 494500 -36500 Unfavourable

Delivery and Installation costs 19200 13100 6100 Favourable

Sales commissions 12800 16375 -3575 Unfavourable

TOTAL VARIABLE 490000 523975 -33975 Unfavourable

Less: Fixed costs

Advertising 5200 5500 -300 Unfavourable

Energy 2800 3200 -400 Unfavourable

Insurance 2400 2400 0 -

Office supplies 3700 3300 400 Favourable

Printing & stationery 6000 5500 500 Favourable

TOTAL FIXED 20100 19900 200 Favourable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TOTAL COSTS 510100 543875 -33775 Unfavourable

NET INCOME 129900 111125 18775 Favourable

Task 1.9

Forecasting Techniques: The technique of using the past data or historical data to

analyse and predict the future trends and make plans according to the new data is called

forecasting. The following are the types of forecasting:

Direct or Bottom-up methods: In this technique different department make their own

forecast after collecting the data from different aspects such as sales data, production

data, purchases data, etc. This data later on is brought together and clubbed to find out the

forecast about the company's future (Shin and Jang, 2013).

Indirect or Top-Down Methods: In direct or top down method firstly the budget is

forecasted for the main trade activities and later on the individual department are given

their share. In this type of forecasting technique no department is given the free hand to

set their forecasting the responsibility of giving the budget to different departments goes

with the top level management executives.

Scientific Methods: In this type of forecasting methods the management relies upon the

past data and make the future prediction about the growth of the company. In this

methods the previous years data must be properly organised and should be interpreted in

the terms of causal relationship. The scientific method of forecasting is basically based on

the causal relationship. In this method forecaster uses many different tools only to guide

in making the interpretation of the data (Hamilton, Koehler and Lösel, 2013).

Double entry accounting: Double entry system is a fundamental accounting concept that

says that every transaction taken place in business will have a impact on at least two accounts. It

means that the every entry passed in the journals or ledger account will affect both sides of two

accounts i.e., the debit side and the credit side. If one account is debited then the other respective

account will be credited in order to maintain the balance of the accounting equation, which is

assets = liabilities+capital. In double entry system errors and omissions are easily traceable as

they impact on at least two accounts which helps to easily find out the errors or omission ( Tsofa,

Molyneux and Goodman, 2016).

NET INCOME 129900 111125 18775 Favourable

Task 1.9

Forecasting Techniques: The technique of using the past data or historical data to

analyse and predict the future trends and make plans according to the new data is called

forecasting. The following are the types of forecasting:

Direct or Bottom-up methods: In this technique different department make their own

forecast after collecting the data from different aspects such as sales data, production

data, purchases data, etc. This data later on is brought together and clubbed to find out the

forecast about the company's future (Shin and Jang, 2013).

Indirect or Top-Down Methods: In direct or top down method firstly the budget is

forecasted for the main trade activities and later on the individual department are given

their share. In this type of forecasting technique no department is given the free hand to

set their forecasting the responsibility of giving the budget to different departments goes

with the top level management executives.

Scientific Methods: In this type of forecasting methods the management relies upon the

past data and make the future prediction about the growth of the company. In this

methods the previous years data must be properly organised and should be interpreted in

the terms of causal relationship. The scientific method of forecasting is basically based on

the causal relationship. In this method forecaster uses many different tools only to guide

in making the interpretation of the data (Hamilton, Koehler and Lösel, 2013).

Double entry accounting: Double entry system is a fundamental accounting concept that

says that every transaction taken place in business will have a impact on at least two accounts. It

means that the every entry passed in the journals or ledger account will affect both sides of two

accounts i.e., the debit side and the credit side. If one account is debited then the other respective

account will be credited in order to maintain the balance of the accounting equation, which is

assets = liabilities+capital. In double entry system errors and omissions are easily traceable as

they impact on at least two accounts which helps to easily find out the errors or omission ( Tsofa,

Molyneux and Goodman, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variance analysis: Variance is the difference between the actual performance and

budgeted performance. The critical analysis of this difference to find out the reason and

formulating new strategies to overcome the difference. When the variance is analysed by the

management on the basis of trend this analysis becomes the effective tool. This tool also helps

the management to answer the questions like why there is a change in budgeted and actual

performance. Variance analysis is also used for forecasting as it uses the patterns from the past

data in order to develop the new theory about the business performance in future (McCord, Liu

and Singh, 2013).

budgeted performance. The critical analysis of this difference to find out the reason and

formulating new strategies to overcome the difference. When the variance is analysed by the

management on the basis of trend this analysis becomes the effective tool. This tool also helps

the management to answer the questions like why there is a change in budgeted and actual

performance. Variance analysis is also used for forecasting as it uses the patterns from the past

data in order to develop the new theory about the business performance in future (McCord, Liu

and Singh, 2013).

ASSESSMENT ACTIVITY 2

Task 2.1

Budget objectives:

Primary objective of budget is to provide a systematic structure. Structure is very

important before starting a task. Structure gives us a framework to work and gives the

company a basis to plan that what should the company do to maximize its profit. As in

Johnson trading, a predefined structure will help the organisation grow and keep track of

the employees performance.

It provide organisation to predict the inflows and outflows of the cash from the company.

It is very helpful for the organisations which are growing rapidly or have an uneven sales

patterns. These types of firms faces the problem related to cash crises. Through budgeting

these company can predict the inflow or the outflow of the cash in the near future and can

save the company for facing these types of problems. As Johnson trading is a trading

company and these type of companies usually have the uneven sales or some time

seasonal sales and can face the problems of cash crises but with the help of budget this

problem is not faced.

Budget provide assistance to organisation to allocate the uses of resources efficiently.

With the help of the budget many organisation try to allocate their resources for the

purchase of assets or getting into new business.

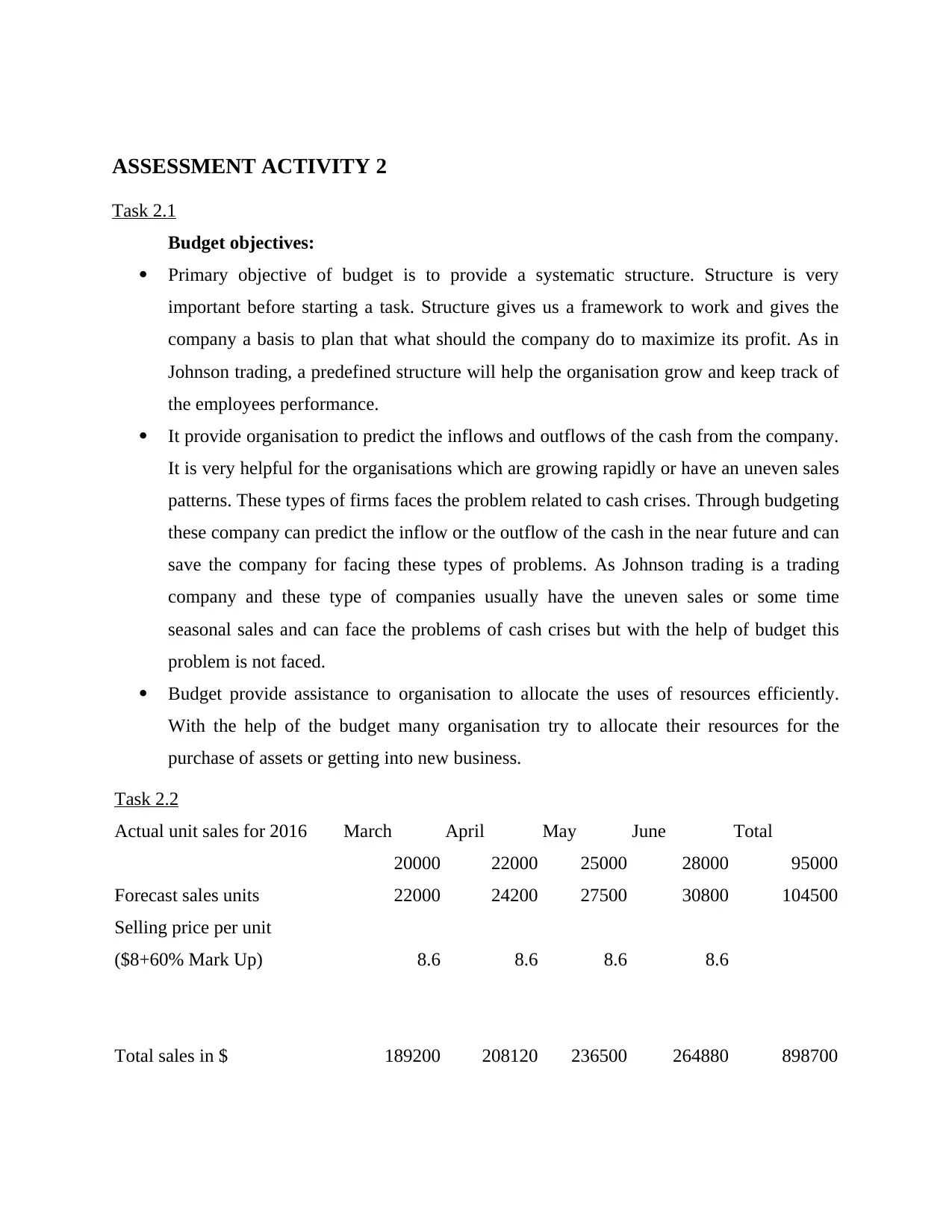

Task 2.2

Actual unit sales for 2016 March April May June Total

20000 22000 25000 28000 95000

Forecast sales units 22000 24200 27500 30800 104500

Selling price per unit

($8+60% Mark Up) 8.6 8.6 8.6 8.6

Total sales in $ 189200 208120 236500 264880 898700

Task 2.1

Budget objectives:

Primary objective of budget is to provide a systematic structure. Structure is very

important before starting a task. Structure gives us a framework to work and gives the

company a basis to plan that what should the company do to maximize its profit. As in

Johnson trading, a predefined structure will help the organisation grow and keep track of

the employees performance.

It provide organisation to predict the inflows and outflows of the cash from the company.

It is very helpful for the organisations which are growing rapidly or have an uneven sales

patterns. These types of firms faces the problem related to cash crises. Through budgeting

these company can predict the inflow or the outflow of the cash in the near future and can

save the company for facing these types of problems. As Johnson trading is a trading

company and these type of companies usually have the uneven sales or some time

seasonal sales and can face the problems of cash crises but with the help of budget this

problem is not faced.

Budget provide assistance to organisation to allocate the uses of resources efficiently.

With the help of the budget many organisation try to allocate their resources for the

purchase of assets or getting into new business.

Task 2.2

Actual unit sales for 2016 March April May June Total

20000 22000 25000 28000 95000

Forecast sales units 22000 24200 27500 30800 104500

Selling price per unit

($8+60% Mark Up) 8.6 8.6 8.6 8.6

Total sales in $ 189200 208120 236500 264880 898700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.