Comprehensive Examination of Stock Return Data and Analysis

VerifiedAdded on 2023/06/07

|9

|725

|324

Homework Assignment

AI Summary

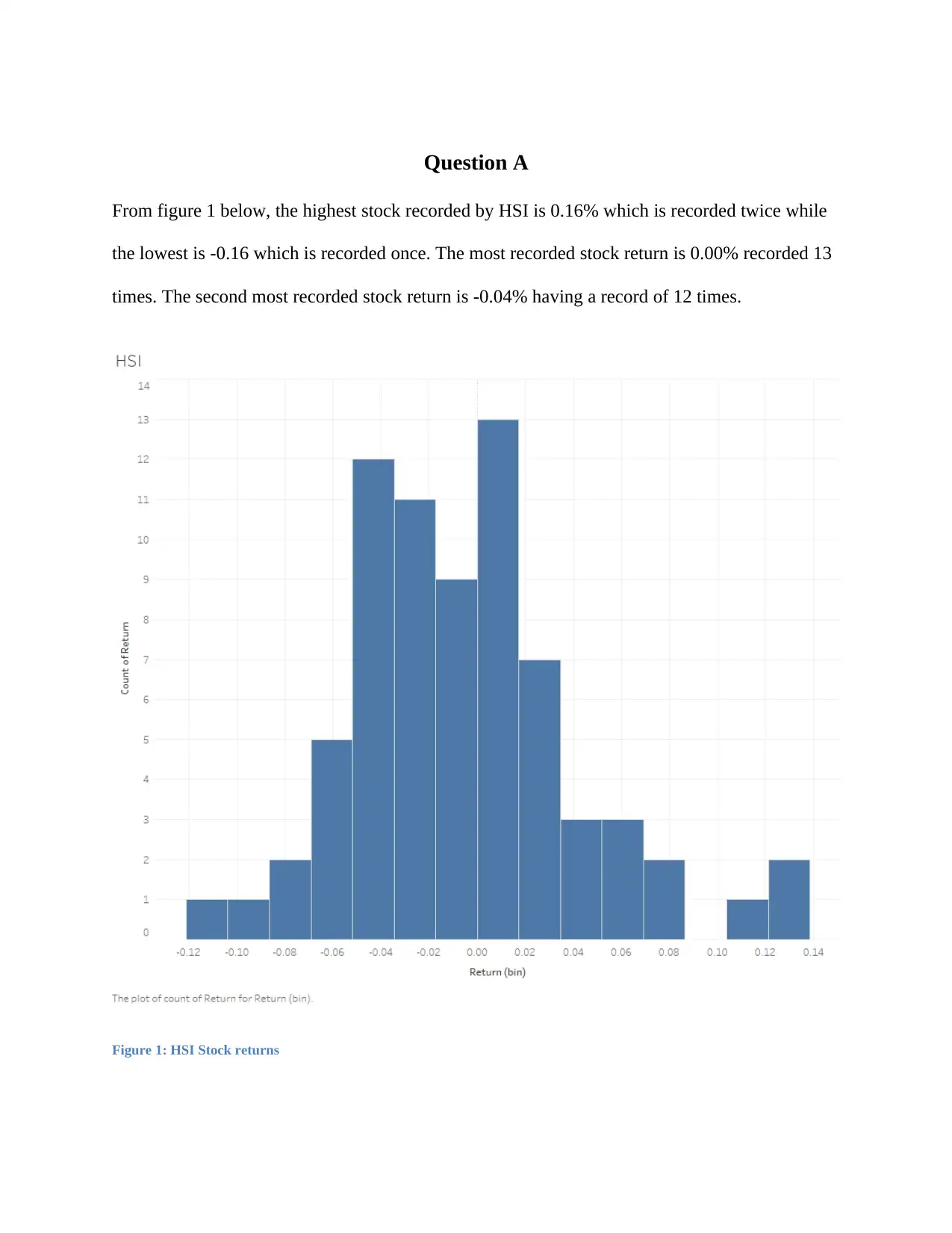

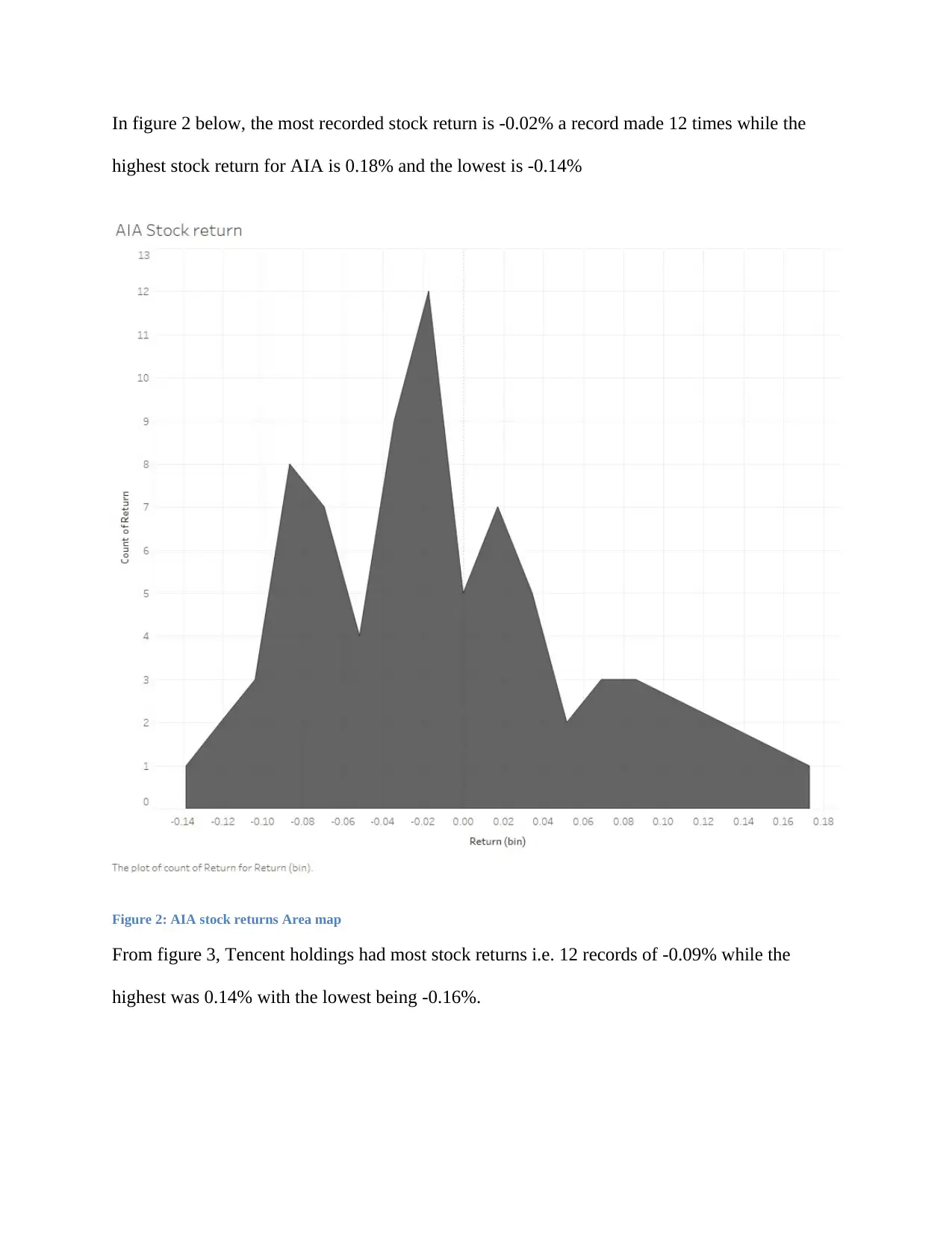

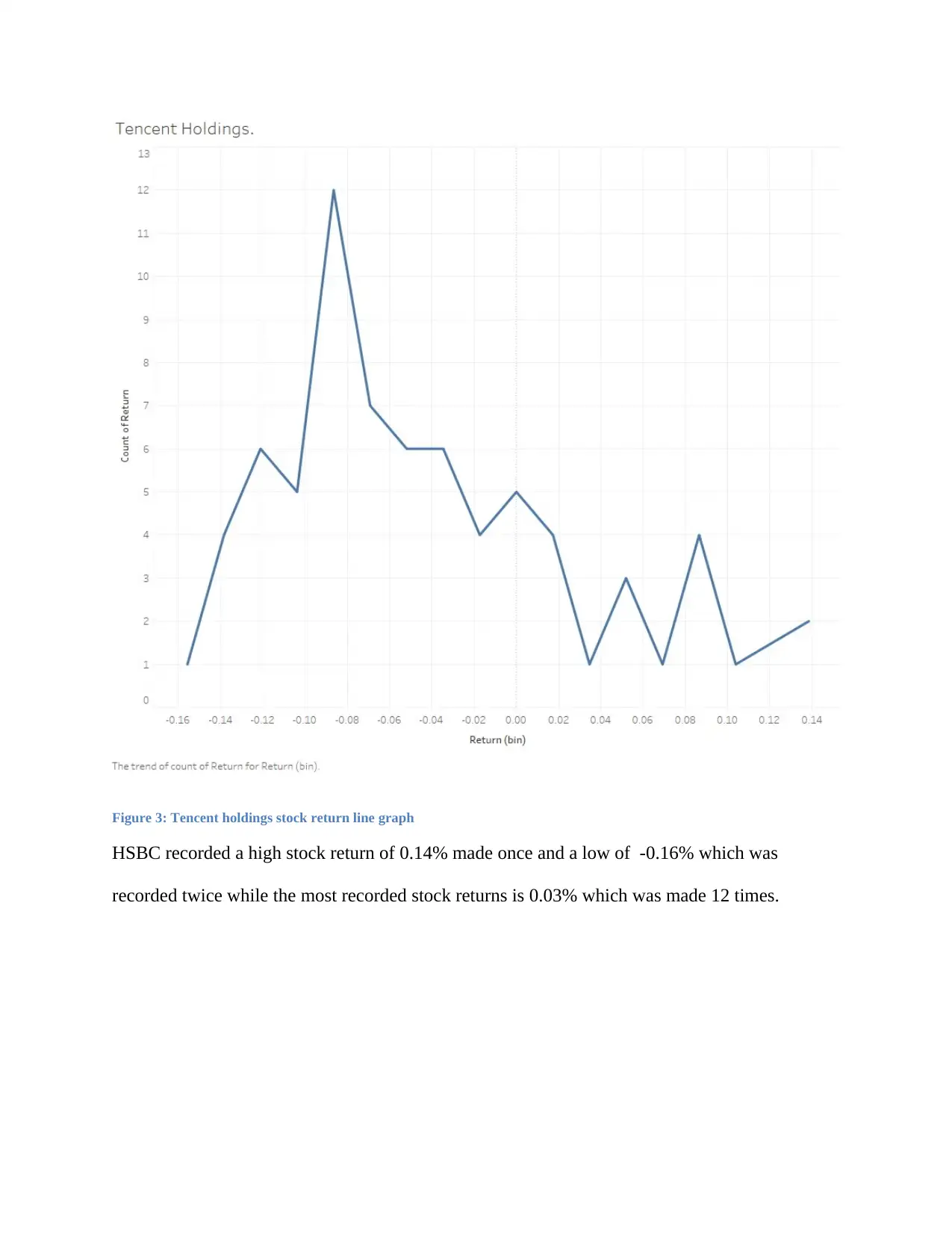

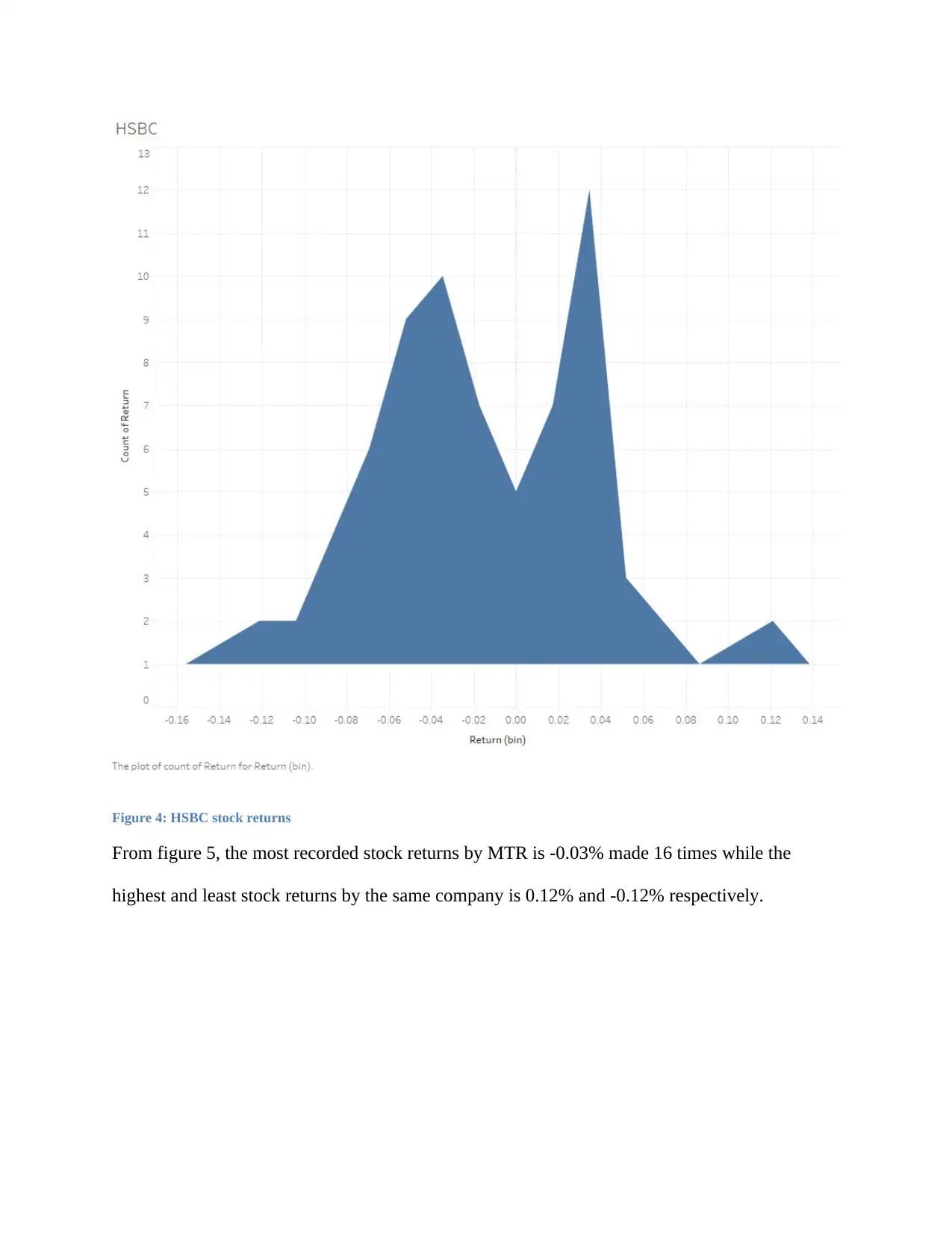

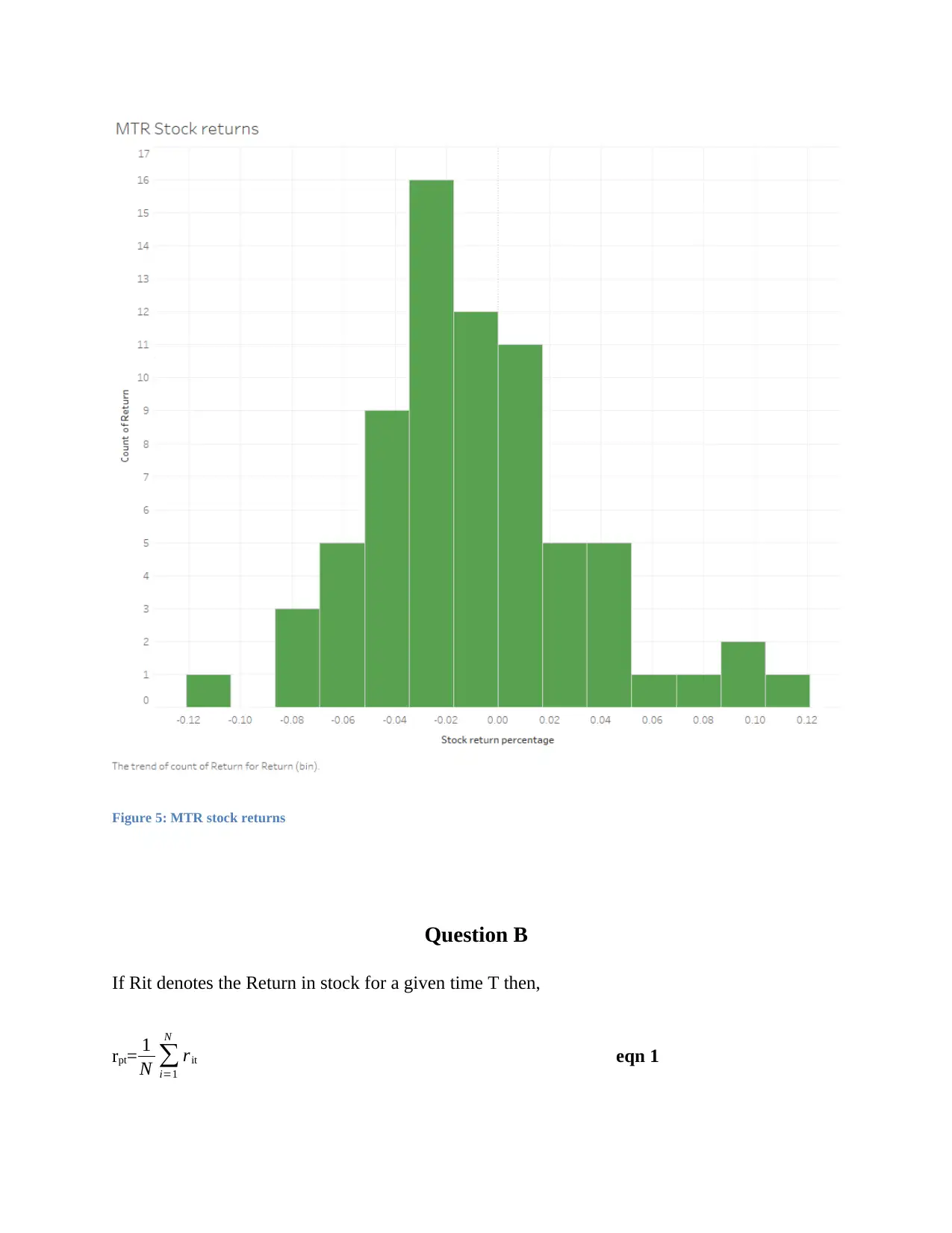

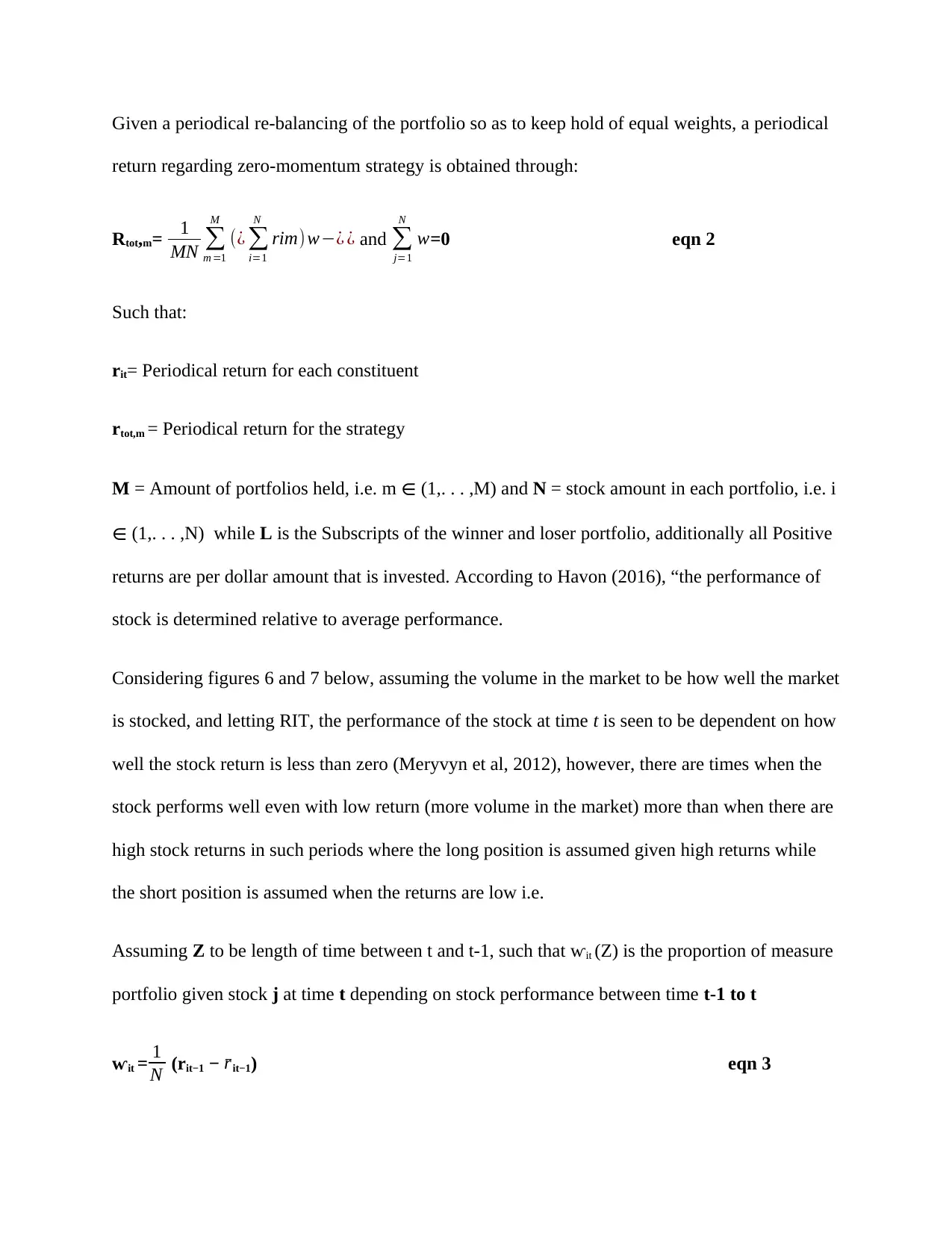

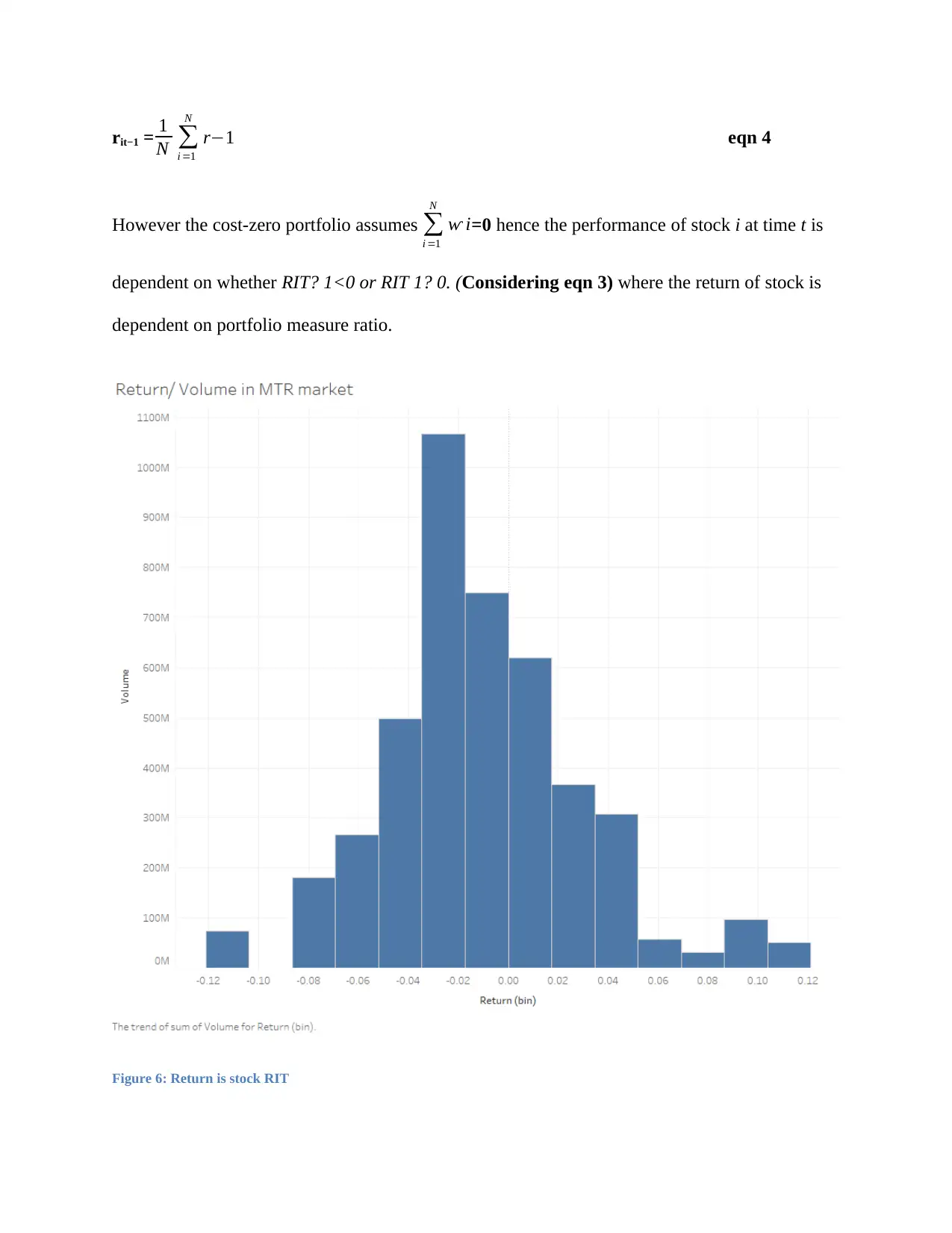

This assignment analyzes stock return data from various companies, including HSI, AIA, Tencent, HSBC, and MTR. It presents a breakdown of stock returns, identifying the highest, lowest, and most frequently recorded returns for each company using figures and charts. The analysis extends to the calculation of portfolio returns using the provided equations (1 and 2) and explores the concept of zero-momentum strategy. The document also delves into how stock performance is determined relative to average performance, considering market volume and the relationship between stock returns and portfolio measure ratios. The assignment references Havon (2016) and Meryvyn et al. (2012) to support its arguments and calculations, providing a comprehensive overview of stock return analysis and financial modeling.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.