Financial Analysis and Performance Report for Compsoft Limited

VerifiedAdded on 2021/05/27

|10

|1722

|54

Report

AI Summary

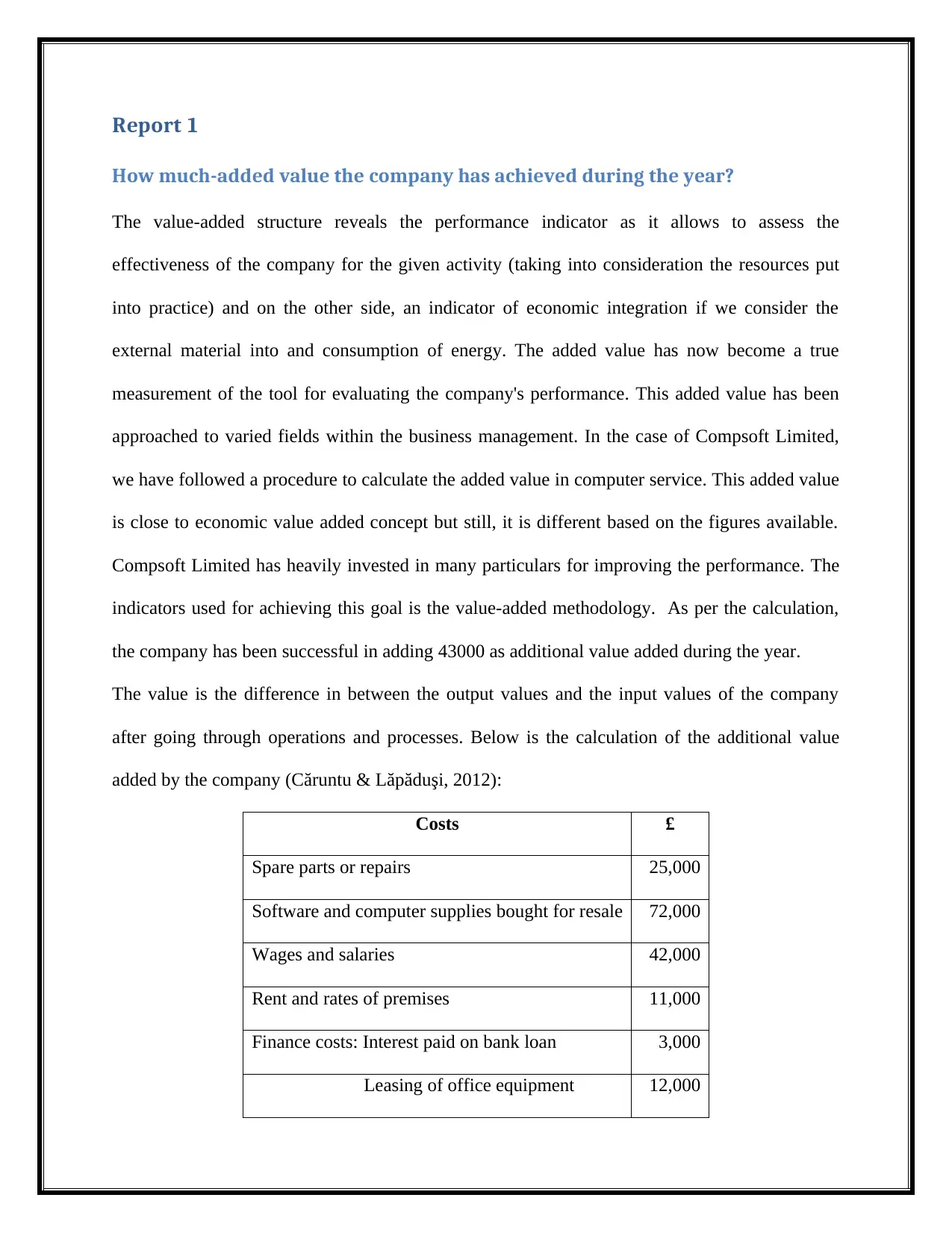

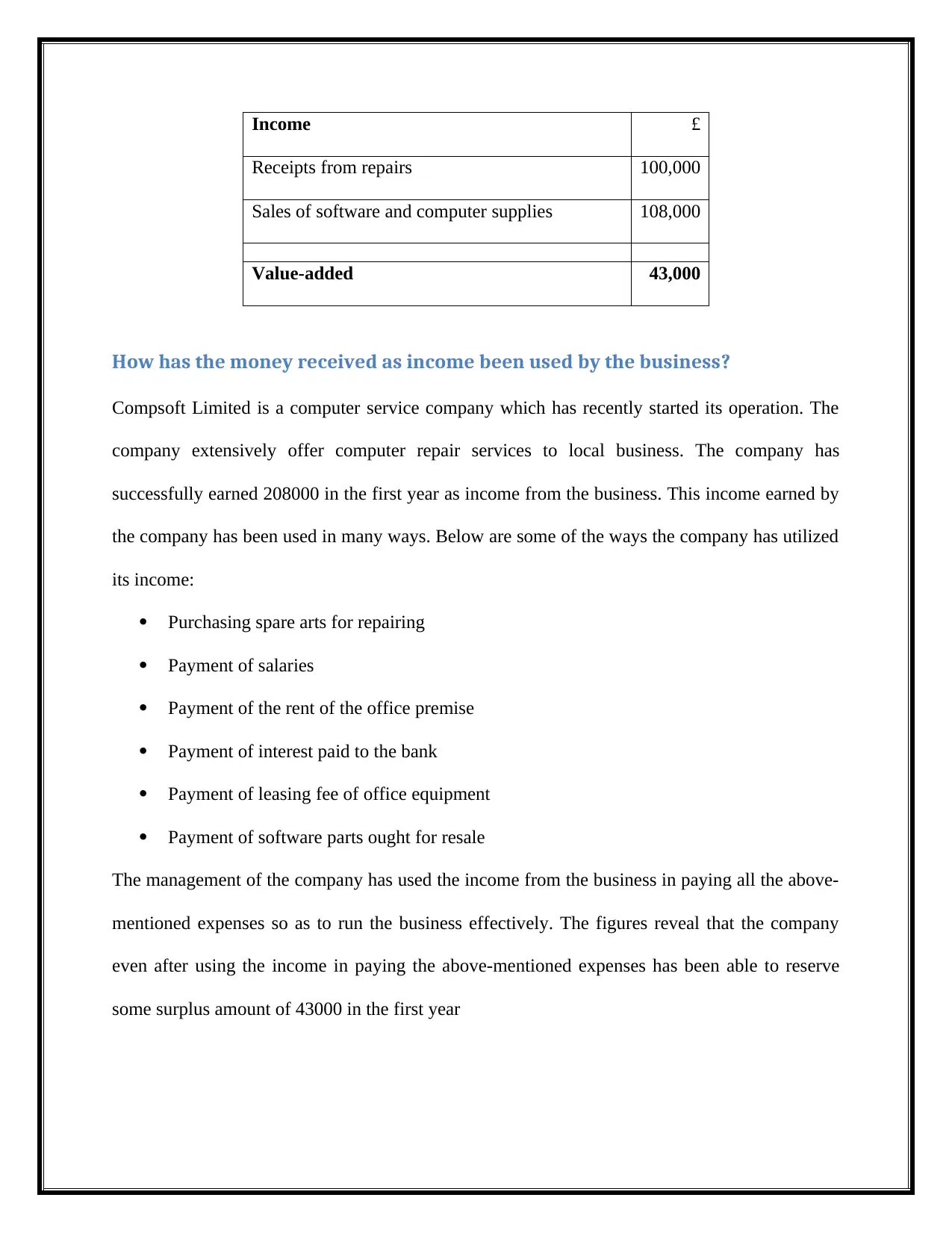

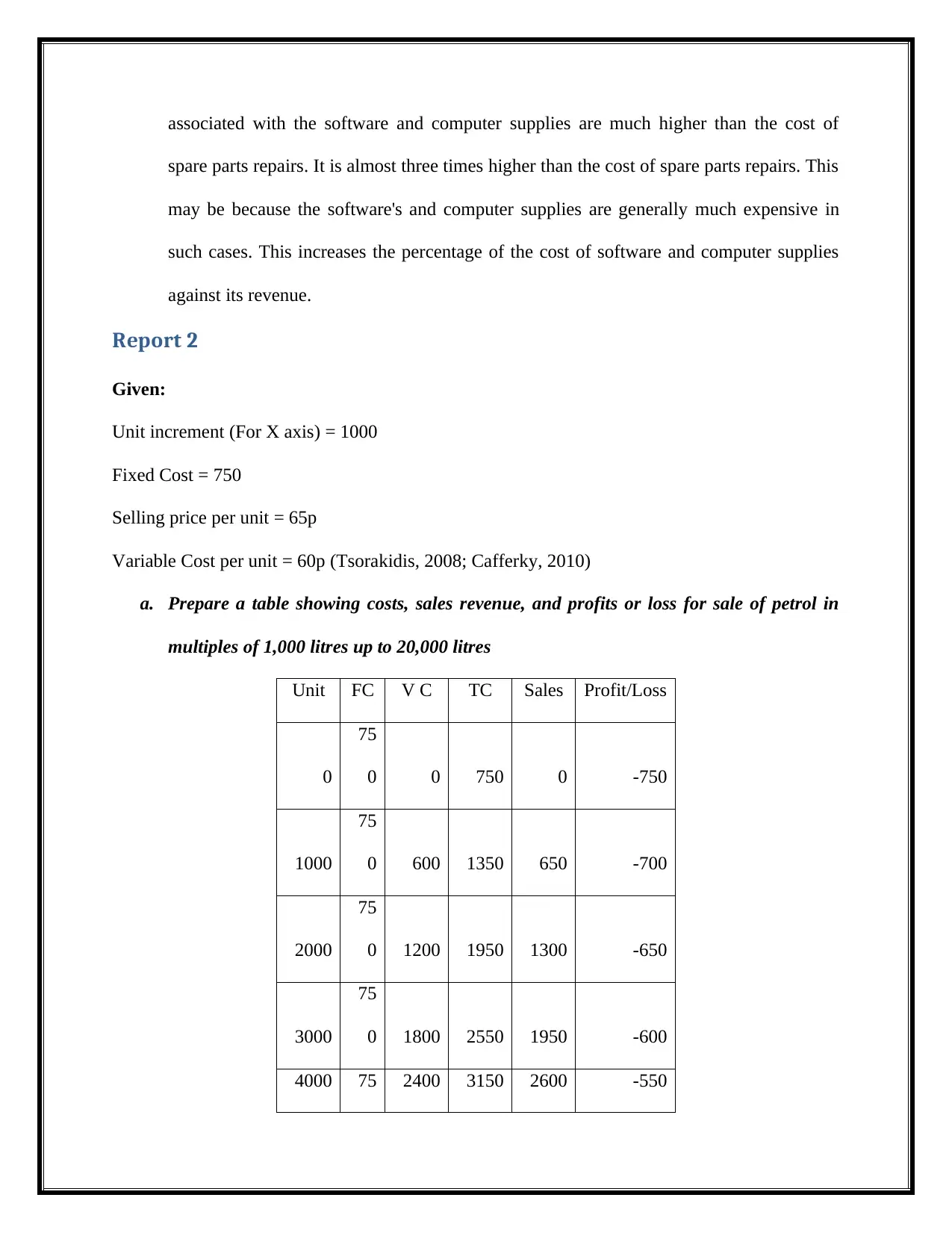

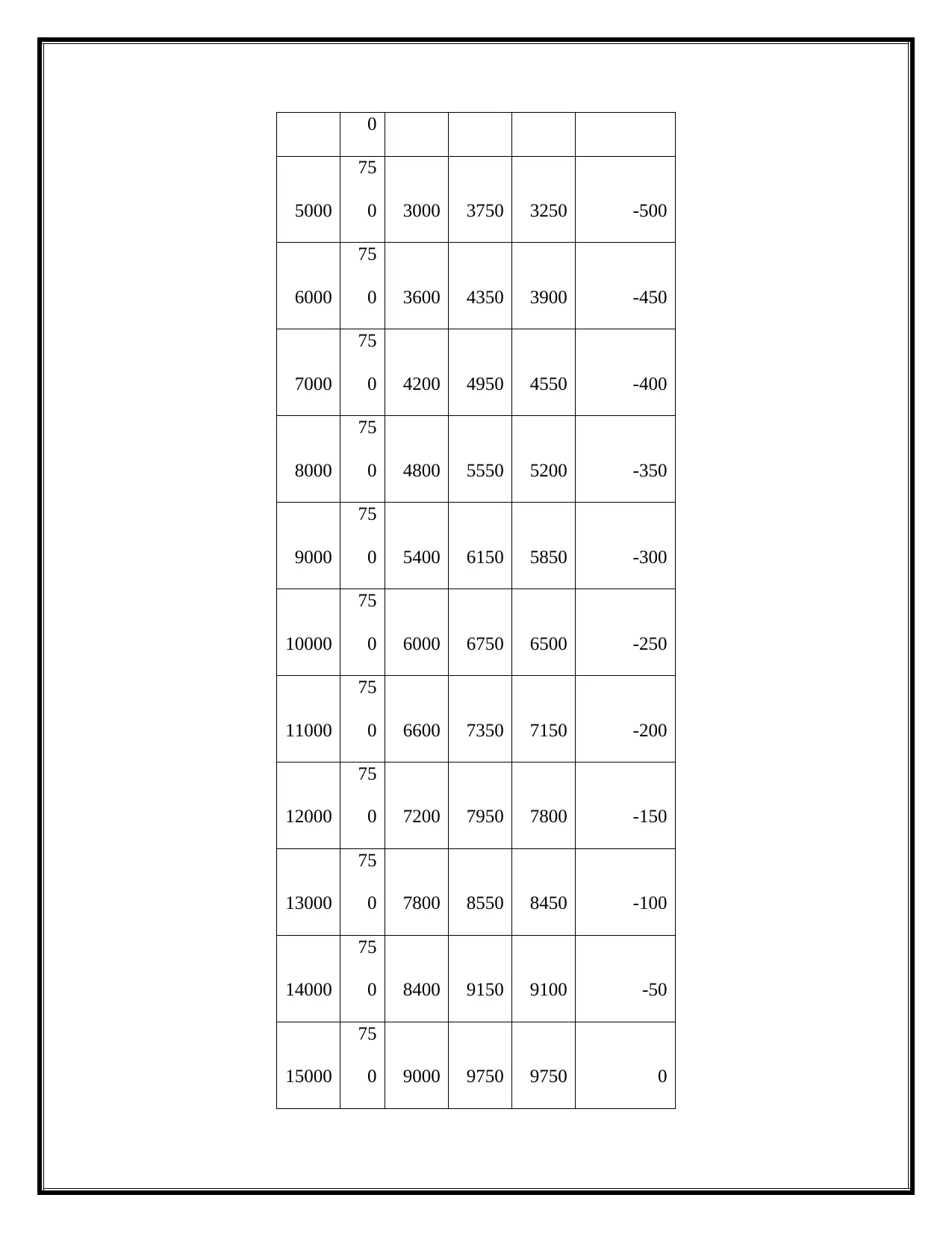

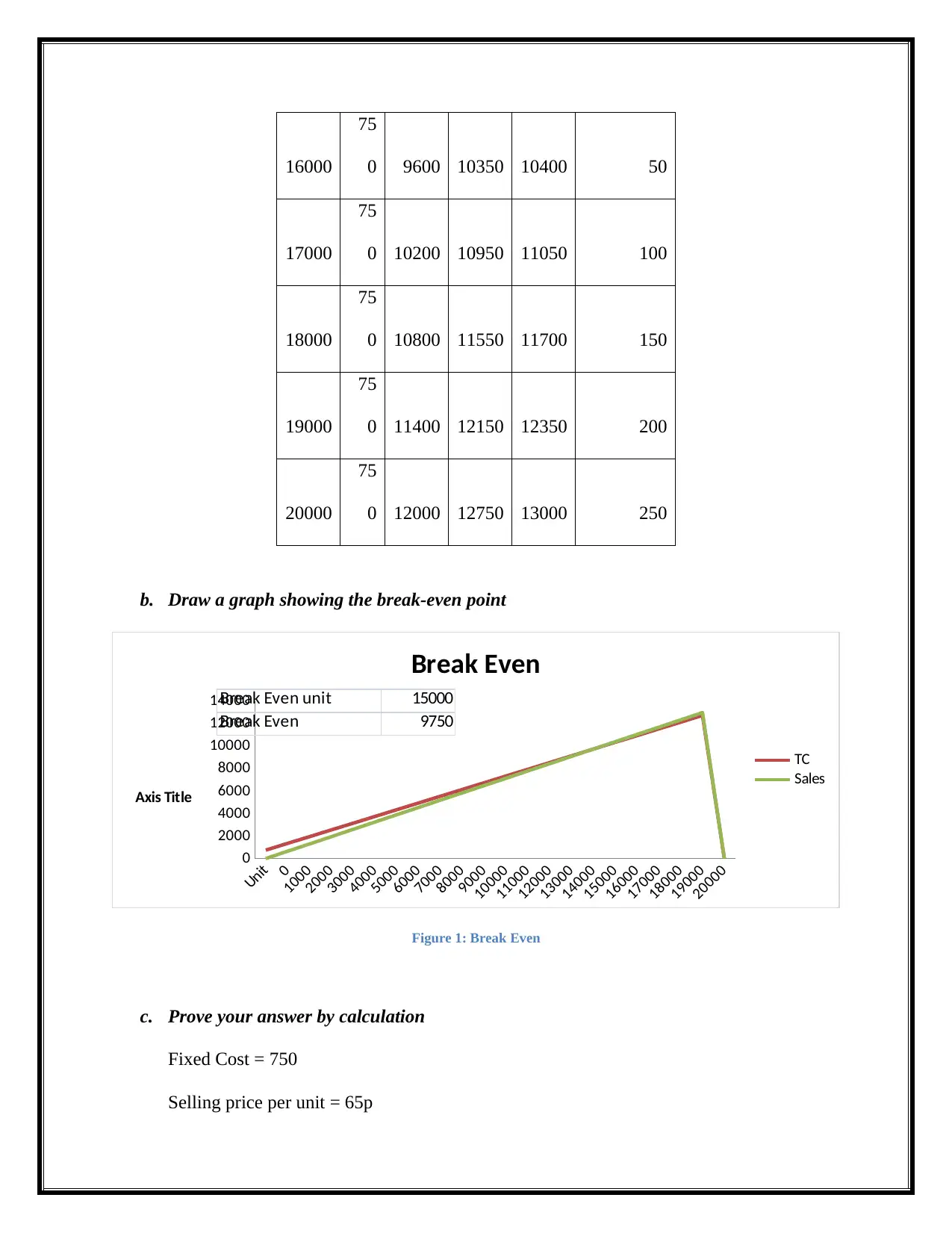

This report presents a comprehensive financial analysis of Compsoft Limited, a computer service company. The first part of the report calculates the value added by the company, which amounted to £43,000, and details how the company utilized its income, including expenses such as spare parts, salaries, rent, and leasing fees. It further provides advice on utilizing surplus cash, suggesting options like paying down debts or investing, considering factors such as interest rates and investment opportunities. The second part of the report delves into cost and revenue analysis, calculating percentages for various costs and analyzing the break-even point for petrol sales, including a table showing costs, sales revenue, and profits or losses. It includes a break-even graph, calculations for profit/loss at different sales volumes, and the margin of safety. The report concludes with a list of references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.