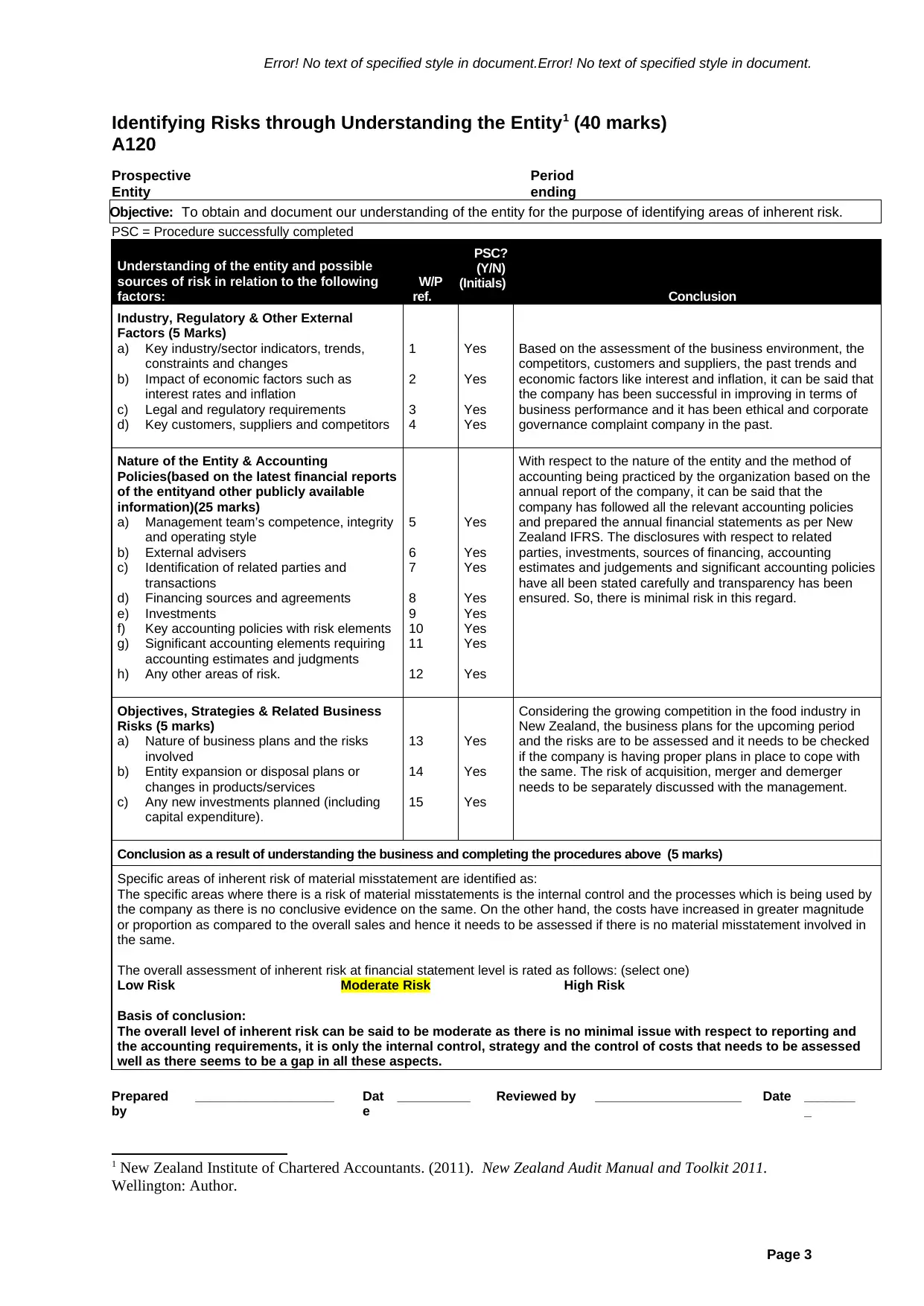

A120 Audit Programme: Identifying Risks in Comvita Limited Audit 2018

VerifiedAdded on 2023/06/03

|4

|1414

|165

Practical Assignment

AI Summary

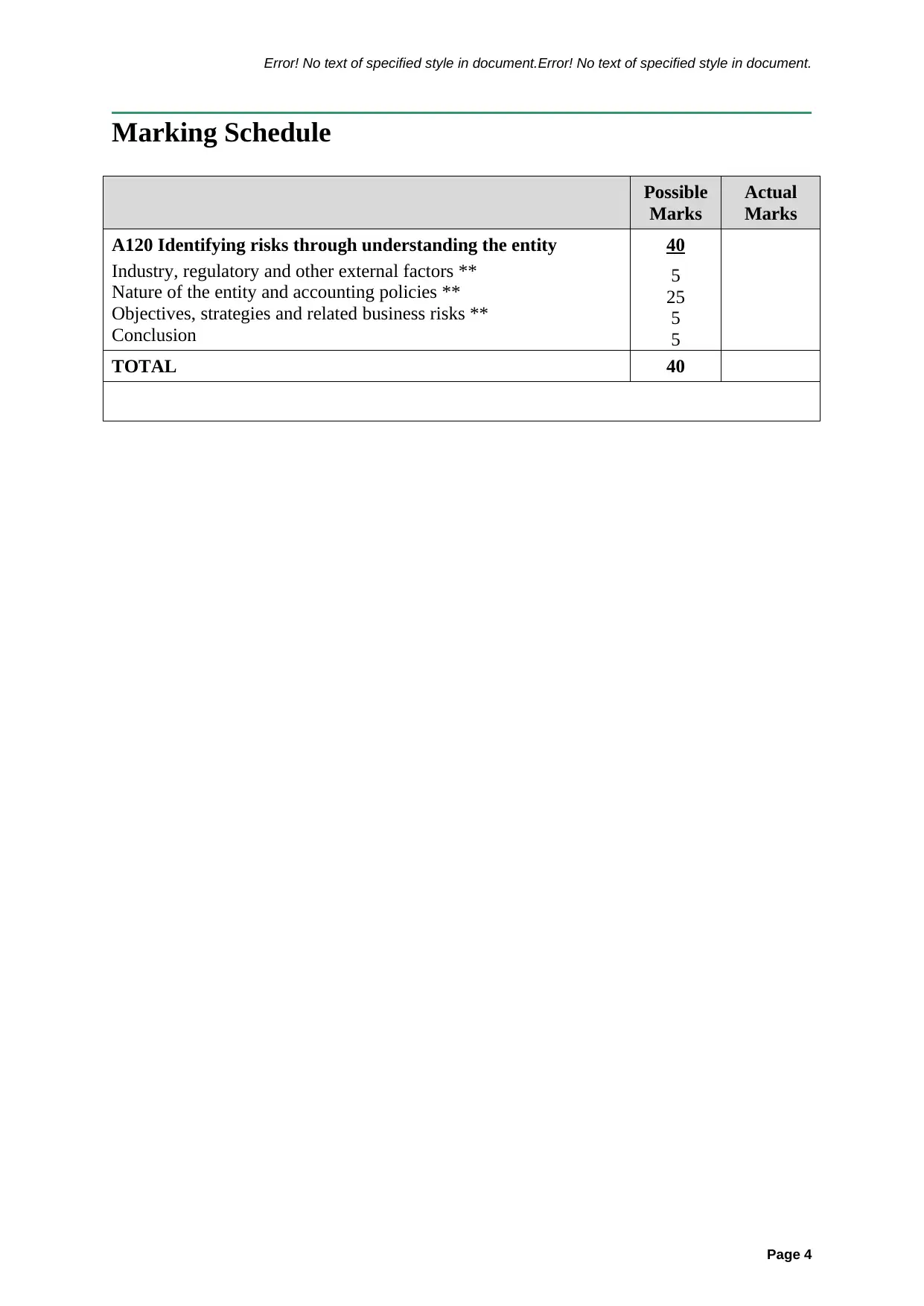

This assignment solution focuses on identifying risks through understanding the entity, Comvita Limited, as part of an audit program (A120). The audit team evaluates industry factors, regulatory requirements, the nature of the entity, accounting policies, objectives, strategies, and related business risks. The conclusion assesses inherent risks, identifying areas of potential material misstatement related to internal controls and cost management. The overall inherent risk is rated as moderate, emphasizing the need for further assessment of internal controls, strategy, and cost control measures. This solution, contributed by a student and available on Desklib, provides valuable insights into practical audit risk assessment.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.