Accounting Theory & Contemporary Issues: A Report for ACC301

VerifiedAdded on 2022/11/13

|8

|1609

|138

Report

AI Summary

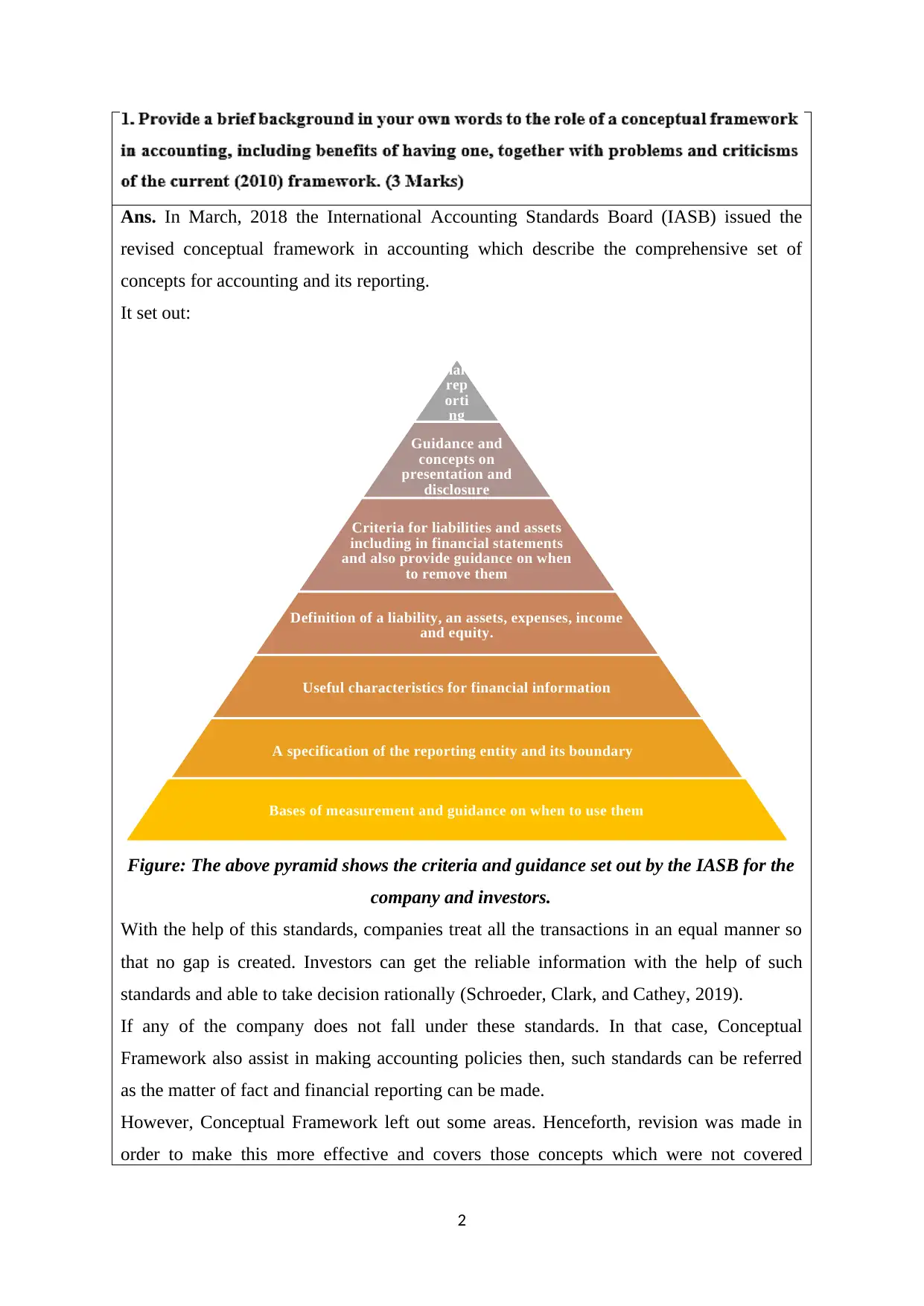

This report analyzes the International Accounting Standards Board's (IASB) revised conceptual framework for financial reporting, issued in March 2018. The report addresses the framework's objectives, including providing relevant information for stakeholders, and discusses the definitions of assets, liabilities, expenses, income, and equity. It also examines the concept of prudence, also known as the principle of conservatism, and asymmetrical prudence, highlighting how these concepts impact financial statements. Additionally, the report explores the concept of substance over form, emphasizing the importance of representing the true economic value of transactions. The report incorporates a video transcript that summarizes the key points of the written analysis and provides a comprehensive overview of the contemporary accounting issues.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.