ACCT20074 Contemporary Accounting Theory: Framework & Analysis

VerifiedAdded on 2023/04/04

|28

|5583

|402

Report

AI Summary

This report, divided into two parts, examines contemporary accounting theory. Part A provides a literature review of the history and development of the conceptual framework in financial accounting across Australia, the USA, and the UK, highlighting its evolution from a disorganized system prone to scandals to a more standardized approach following the introduction of the framework in 1989 and its subsequent revisions. It also addresses concerns raised by academics and accounting professionals regarding the framework's applicability. Part B discusses sustainability and integrated reporting, comparing Discovery Limited's integrated report with AUB Group Limited's interactive annual report, noting similarities in financial position presentation but differing approaches to reporting. The report emphasizes the importance of the conceptual framework in providing a foundation for understanding and evaluating accounting information.

Running Head: CONTEMPORARY ACCOUNTING THEORY 1

Contemporary Accounting Theory

Name

Date

Affiliation

Contemporary Accounting Theory

Name

Date

Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 2

Contemporary Accounting Theory

Executive Summary

This paper comprises of two parts, A and B. Part A provides a literature review about the

history of the conceptual framework in financial accounting and its development in Australia,

USA and UK. According to researchers, accounting standards settles were operating without a

conceptual framework. There were therefore several scandals in financial accounting and the

entire system was disorganized. However, the introduction of the conceptual framework in 1989

resulted into establishment of a one set of accounting standards that govern the operations of the

accounting sector. The financial accounting field even further improved as the conceptual

framework was revised in 2001. As a result, there have been several concerns raised by both

academics and accounting professionals about the applicability of the framework. Part B of the

report discusses sustainability and integrated reporting and the strengths as well as limitations of

conventional accounting. According to the integrated report presented by Discovery Limited, the

company disclosed all the information of the elements of an integrated report. Both companies

have several things in common including the way they present their financial positions.

However, AUB Group Limited comprises of an interactive annual report whereas Discovery

Limited comprises of an integrated report.

Introduction

Conceptual framework is one of the most important systems in accounting which

comprises of fundamentals and inter-related objectives that facilitate issuing of consistent

standards which describe nature and control preparation and presentation of financial statements

as well financial accounting as a whole (IFRS Foundation,2017). The framework plays a vital

Contemporary Accounting Theory

Executive Summary

This paper comprises of two parts, A and B. Part A provides a literature review about the

history of the conceptual framework in financial accounting and its development in Australia,

USA and UK. According to researchers, accounting standards settles were operating without a

conceptual framework. There were therefore several scandals in financial accounting and the

entire system was disorganized. However, the introduction of the conceptual framework in 1989

resulted into establishment of a one set of accounting standards that govern the operations of the

accounting sector. The financial accounting field even further improved as the conceptual

framework was revised in 2001. As a result, there have been several concerns raised by both

academics and accounting professionals about the applicability of the framework. Part B of the

report discusses sustainability and integrated reporting and the strengths as well as limitations of

conventional accounting. According to the integrated report presented by Discovery Limited, the

company disclosed all the information of the elements of an integrated report. Both companies

have several things in common including the way they present their financial positions.

However, AUB Group Limited comprises of an interactive annual report whereas Discovery

Limited comprises of an integrated report.

Introduction

Conceptual framework is one of the most important systems in accounting which

comprises of fundamentals and inter-related objectives that facilitate issuing of consistent

standards which describe nature and control preparation and presentation of financial statements

as well financial accounting as a whole (IFRS Foundation,2017). The framework plays a vital

CONTEMPORARY ACCOUNTING THEORY 3

role in financial accounting as it lays foundation for better understanding and evaluation of

accounting information. Following the important role played by this system, it is currently

adopted by multiple countries in the world. This paper provides research about the numerous

corporate external reporting aspects. It reviews the available literature about the history and

advancement of the conceptual framework, the concerns raised by the accounting professionals,

as well as the concerns of academics about its application. The report is to be presented in two

parts, A and B. Part A provides literature about the conceptual framework and its applicability in

AUB Group Limited, an Australian company. Part B discusses sustainability and integrated

reporting and its applicability in Discovery Limited, a South African company (IFRS

Foundation,2017).

Part A: Conceptual Framework

A ) Literature review of the history and development of the Conceptual Framework for

Financial Reporting

Conceptual framework is a system of objectives and ideas that facilitates the creation of

standards and rules. In Financial accounting, a conceptual framework is mainly developed to

provide a framework for setting the foundation of solving accounting disputes, accounting

standards and fundamental principles (Dennis, 2018). Conceptual framework is a very important

system in accounting as it helps in providing a better understanding of financial reports. Very

many years back, setters of accounting standards were operating without a conceptual

framework. As a result, scandals were the order of the day and accounting standards were

disorganized (Sori, 2017).

role in financial accounting as it lays foundation for better understanding and evaluation of

accounting information. Following the important role played by this system, it is currently

adopted by multiple countries in the world. This paper provides research about the numerous

corporate external reporting aspects. It reviews the available literature about the history and

advancement of the conceptual framework, the concerns raised by the accounting professionals,

as well as the concerns of academics about its application. The report is to be presented in two

parts, A and B. Part A provides literature about the conceptual framework and its applicability in

AUB Group Limited, an Australian company. Part B discusses sustainability and integrated

reporting and its applicability in Discovery Limited, a South African company (IFRS

Foundation,2017).

Part A: Conceptual Framework

A ) Literature review of the history and development of the Conceptual Framework for

Financial Reporting

Conceptual framework is a system of objectives and ideas that facilitates the creation of

standards and rules. In Financial accounting, a conceptual framework is mainly developed to

provide a framework for setting the foundation of solving accounting disputes, accounting

standards and fundamental principles (Dennis, 2018). Conceptual framework is a very important

system in accounting as it helps in providing a better understanding of financial reports. Very

many years back, setters of accounting standards were operating without a conceptual

framework. As a result, scandals were the order of the day and accounting standards were

disorganized (Sori, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 4

Additionally, the absence of the conceptual framework increased inconsistence in the

accounting standards and the overall purpose of preparing and presenting financial statements.

The International Accounting Standards Committee (IASC) in 1989 (Silva, 2018), issued

conceptual framework. Since then, it had been left unchanged until the International Accounting

Standards Board in 2001, an organization that replaced IASC, adopted it. IASB is an

independent organization whose main goal is to establish a single set of accounting standards

that govern all international companies across the globe. The organization deals in capital and

capital maintenance concepts, the objectives of preparing and presenting financial statements,

qualitative traits which determine how important the information in financial statements is, and

defining as well as measuring the elements which provide a basis for constructing financial

statements (Sori, 2017).

In U.K, conceptual framework was developed by the nation in 1999. It was referred to as

the Statement of Principles and was approved by the Accounting Standards Board. Following the

several gains such as globalization, which were realized by U.S after adoption of its conceptual

framework, United Kingdom also aimed at decreasing any form of prospects of staying behind as

far as accounting is concerned through developing its own conceptual framework, (Becker,

2010). Considering the above, there exists consistence between the Statement of Principles and

the statements of the conceptual framework, which were issued by several nations including

United States and New Zealand (Carrahera and Auken, 2013). The Financial statements elements

were the foundation for the development of the Statement of principles in U.K. These included

ownership interest, losses and gains, assets and liabilities. These principles are applied to the

financial statements which are included in the constitution of the interim reports and initial

announcements of the listed companies in U.K (Becker, 2010).

Additionally, the absence of the conceptual framework increased inconsistence in the

accounting standards and the overall purpose of preparing and presenting financial statements.

The International Accounting Standards Committee (IASC) in 1989 (Silva, 2018), issued

conceptual framework. Since then, it had been left unchanged until the International Accounting

Standards Board in 2001, an organization that replaced IASC, adopted it. IASB is an

independent organization whose main goal is to establish a single set of accounting standards

that govern all international companies across the globe. The organization deals in capital and

capital maintenance concepts, the objectives of preparing and presenting financial statements,

qualitative traits which determine how important the information in financial statements is, and

defining as well as measuring the elements which provide a basis for constructing financial

statements (Sori, 2017).

In U.K, conceptual framework was developed by the nation in 1999. It was referred to as

the Statement of Principles and was approved by the Accounting Standards Board. Following the

several gains such as globalization, which were realized by U.S after adoption of its conceptual

framework, United Kingdom also aimed at decreasing any form of prospects of staying behind as

far as accounting is concerned through developing its own conceptual framework, (Becker,

2010). Considering the above, there exists consistence between the Statement of Principles and

the statements of the conceptual framework, which were issued by several nations including

United States and New Zealand (Carrahera and Auken, 2013). The Financial statements elements

were the foundation for the development of the Statement of principles in U.K. These included

ownership interest, losses and gains, assets and liabilities. These principles are applied to the

financial statements which are included in the constitution of the interim reports and initial

announcements of the listed companies in U.K (Becker, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 5

In Australia, the conceptual framework was initially observed as a package that consisted

of several concepts of accounting statements. These statements provided the definition of

subject, purpose and nature of the significance of financial reporting in both private and public

companies (Carrahera and Auken, 2013). In 2004, the Australian Accounting Standards

Board(AASB) developed the conceptual framework for financial reporting. The framework was

then implemented in 2005 and it served the purpose of improving and regulating accounting

practices and financial reporting of all public companies in the country. The main aim of the

framework was to assists financial statement users and auditors to interpret and form opinions on

the financial information contained in the financial statements as per the AASB (Carrahera and

Auken, 2013).

Globally, the conceptual framework was first introduced in 1989. It was authorized by

Inter-Agency Standing Committee (IASC) and was initially adopted by IASB in 2005.The

accounting standards that were established by IASC are currently still in use and are referred to

as the International Accounting Standards(IAS) (Daske et al, 2013). On the other side standards

developed by IASB are referred to as International Financial Reporting standards. In 2004, the

conceptual framework was reviewed and revised by the Financial Accounting Standards Board

(FASB) and IASB. However, slow progress and change in the priorities resulted into abandoning

of the project after 6 years when only the first phase (Phase A) of the project was finalized

(Flower, 2015). Phase D was not finalized even after viewing the exposure draft and discussion

paper publication. Phases B and C were extensively discussed by the board without issuing any

consultation document. Other phases were never touched. In March 2018, the revised version of

the conceptual framework was issued which effective for companies which apply the conceptual

framework to establish accounting policies especially when there is no IFRS standard that

In Australia, the conceptual framework was initially observed as a package that consisted

of several concepts of accounting statements. These statements provided the definition of

subject, purpose and nature of the significance of financial reporting in both private and public

companies (Carrahera and Auken, 2013). In 2004, the Australian Accounting Standards

Board(AASB) developed the conceptual framework for financial reporting. The framework was

then implemented in 2005 and it served the purpose of improving and regulating accounting

practices and financial reporting of all public companies in the country. The main aim of the

framework was to assists financial statement users and auditors to interpret and form opinions on

the financial information contained in the financial statements as per the AASB (Carrahera and

Auken, 2013).

Globally, the conceptual framework was first introduced in 1989. It was authorized by

Inter-Agency Standing Committee (IASC) and was initially adopted by IASB in 2005.The

accounting standards that were established by IASC are currently still in use and are referred to

as the International Accounting Standards(IAS) (Daske et al, 2013). On the other side standards

developed by IASB are referred to as International Financial Reporting standards. In 2004, the

conceptual framework was reviewed and revised by the Financial Accounting Standards Board

(FASB) and IASB. However, slow progress and change in the priorities resulted into abandoning

of the project after 6 years when only the first phase (Phase A) of the project was finalized

(Flower, 2015). Phase D was not finalized even after viewing the exposure draft and discussion

paper publication. Phases B and C were extensively discussed by the board without issuing any

consultation document. Other phases were never touched. In March 2018, the revised version of

the conceptual framework was issued which effective for companies which apply the conceptual

framework to establish accounting policies especially when there is no IFRS standard that

CONTEMPORARY ACCOUNTING THEORY 6

applies to a given transaction. The new version of the conceptual framework will only be applied

for annual reporting periods starting from 1st January 2020. The revised version of the conceptual

framework comprises of significant concepts of financial reporting that provide guidance to

IASB while establishing IFRS standards (Armstrong, 2013). It plays a vital role in ensuring that

all similar transactions are handled in the same way and consistence in the set standards. This

helps to give important information to lenders, investors and other creditors. Additionally, the

new version of the conceptual framework also helps companies in formulating accounting

policies when there exists no IFRS standard relevant to a particular transaction and more

importantly, it assists stakeholders to interpret standards. IASB issued an accompanying

document " Amendments to References" to help companies to clearly understand the transition

(Daske et al, 2013).

B) Discussion of the Australian accounting profession`s concerns on the application of the

Conceptual Framework

The Australian accounting profession is specifically concerned with the multiple political

interferences which have been expressed about the implementation of the conceptual framework

of financial reporting. A significant number of professions are taking part in debates about the

generation and implementation of the elements of the financial statements since conceptual

framework entails formulation of ideas and objectives (Armstrong, 2013). On several occasions,

the stage of decision making is the one most interfered by politics especially among members of

the board. Some great ideas are sometimes ignored because of the selfish interests of the IASB

members. This is evident specifically when the frame work is applied to resolve issues associated

with several disagreements among board members (Humayun and Asheq, 2018). Due to the

rapidly changing economic conditions in different parts of the world, IFRS members may also

applies to a given transaction. The new version of the conceptual framework will only be applied

for annual reporting periods starting from 1st January 2020. The revised version of the conceptual

framework comprises of significant concepts of financial reporting that provide guidance to

IASB while establishing IFRS standards (Armstrong, 2013). It plays a vital role in ensuring that

all similar transactions are handled in the same way and consistence in the set standards. This

helps to give important information to lenders, investors and other creditors. Additionally, the

new version of the conceptual framework also helps companies in formulating accounting

policies when there exists no IFRS standard relevant to a particular transaction and more

importantly, it assists stakeholders to interpret standards. IASB issued an accompanying

document " Amendments to References" to help companies to clearly understand the transition

(Daske et al, 2013).

B) Discussion of the Australian accounting profession`s concerns on the application of the

Conceptual Framework

The Australian accounting profession is specifically concerned with the multiple political

interferences which have been expressed about the implementation of the conceptual framework

of financial reporting. A significant number of professions are taking part in debates about the

generation and implementation of the elements of the financial statements since conceptual

framework entails formulation of ideas and objectives (Armstrong, 2013). On several occasions,

the stage of decision making is the one most interfered by politics especially among members of

the board. Some great ideas are sometimes ignored because of the selfish interests of the IASB

members. This is evident specifically when the frame work is applied to resolve issues associated

with several disagreements among board members (Humayun and Asheq, 2018). Due to the

rapidly changing economic conditions in different parts of the world, IFRS members may also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 7

fail to develop a similar solution towards the measurement of assets. More so, members may

raise different views on both the present and historical costs of assets due to their political

interests (Flower, 2015).

Over the past years, there have been several concerns that have been raised by the

accounting professionals in Australia about the application of the conceptual framework.

According to Wayne Lonergan, a professor of Business and Economics in the University of

Sydney, adoption of international accounting standards by Australia has significant outcomes for

the Australian economy as whole (Humayun and Asheq, 2018). Primarily, the process of setting

accounting standards in Australia was weakened by the policy of adopting the international

accounting standards. The introduction of this system did not only emasculate the setting process

of accounting standards in Australia but also weakened Australia`s setting capacity of accounting

standards and its position as the foundation for accounting excellence. Professionals explain that

less quality financial reports are produced by Australian companies as a result of the adoption of

IAS (Gordon et al, 2015). According to some of the accounting professionals in Australia, the

adoption of IAS created financial stability in corporate government. Currently, most of the

efforts employed by the corporate government are focused on ensuring increase in independence,

disclosure and practice of best guidelines which entail disclosure of failure to comply with the

required standards of annual reports. The major objective of the corporate government is to

develop a culture of trust and integrity between stakeholders and relevant parties such as fund

managers, company directors, auditors and other shareholders. The current reforms are mainly

focusing on making right the symptoms instead of finding solutions for the root causes of the

problems. The back bone of financial reporting are the accounting standards. In Australia, the

regime of financial reporting still has significant deficiencies and limitations. Recently, it was

fail to develop a similar solution towards the measurement of assets. More so, members may

raise different views on both the present and historical costs of assets due to their political

interests (Flower, 2015).

Over the past years, there have been several concerns that have been raised by the

accounting professionals in Australia about the application of the conceptual framework.

According to Wayne Lonergan, a professor of Business and Economics in the University of

Sydney, adoption of international accounting standards by Australia has significant outcomes for

the Australian economy as whole (Humayun and Asheq, 2018). Primarily, the process of setting

accounting standards in Australia was weakened by the policy of adopting the international

accounting standards. The introduction of this system did not only emasculate the setting process

of accounting standards in Australia but also weakened Australia`s setting capacity of accounting

standards and its position as the foundation for accounting excellence. Professionals explain that

less quality financial reports are produced by Australian companies as a result of the adoption of

IAS (Gordon et al, 2015). According to some of the accounting professionals in Australia, the

adoption of IAS created financial stability in corporate government. Currently, most of the

efforts employed by the corporate government are focused on ensuring increase in independence,

disclosure and practice of best guidelines which entail disclosure of failure to comply with the

required standards of annual reports. The major objective of the corporate government is to

develop a culture of trust and integrity between stakeholders and relevant parties such as fund

managers, company directors, auditors and other shareholders. The current reforms are mainly

focusing on making right the symptoms instead of finding solutions for the root causes of the

problems. The back bone of financial reporting are the accounting standards. In Australia, the

regime of financial reporting still has significant deficiencies and limitations. Recently, it was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

recognized as one of the most powerful financial reporting regimes in the entire world. It is one

of the remarkable achievements Australia has ever got despite the fact that the country comprises

of a small economy size and capital markets as compared to the economies of UK, US, Asia and

Europe. The Australian Accounting Standards Board (AASB) was initially responsible for

issuing and preparing of accounting standards to both the public and private sector (Humayun

and Asheq, 2018). However, complying with the accounting standards set by AASB was

mandatory according to the Corporations act. Although, there were few financial resources

provided by the Federal government and the accounting bodies, the setting process of accounting

standards was operating independently. The main objective of the former system was to improve

quality of auditing and financial reporting in Australia for both the end users and the preparing

organizations. The former system managed to develop a globally recognized core of excellence

in financial reporting. Adopting of International accounting standards overshadowed the policies

of AASB despite the fact that the organization also had its own priorities. AASB was made

irrelevant especially for the private sector since accounting standards were no longer issued by

the AASB but instead issued by IASB hence eliminating the need for AASB (Gordon et al,

2015).

C) Explanation of the academics` concerns regarding the benefits and limitations of the

Conceptual Framework

The conceptual framework provides concepts, which are developed in an orderly manner

that make reporting and financial accounting logical and consistent. Through the created

consistency, the framework increases compatibility of the standards both nationally and

internationally (Al-Dmour, 2018). Conceptual framework also facilitates development of the

accounting department as a whole and enhances communication. Development of accounting

recognized as one of the most powerful financial reporting regimes in the entire world. It is one

of the remarkable achievements Australia has ever got despite the fact that the country comprises

of a small economy size and capital markets as compared to the economies of UK, US, Asia and

Europe. The Australian Accounting Standards Board (AASB) was initially responsible for

issuing and preparing of accounting standards to both the public and private sector (Humayun

and Asheq, 2018). However, complying with the accounting standards set by AASB was

mandatory according to the Corporations act. Although, there were few financial resources

provided by the Federal government and the accounting bodies, the setting process of accounting

standards was operating independently. The main objective of the former system was to improve

quality of auditing and financial reporting in Australia for both the end users and the preparing

organizations. The former system managed to develop a globally recognized core of excellence

in financial reporting. Adopting of International accounting standards overshadowed the policies

of AASB despite the fact that the organization also had its own priorities. AASB was made

irrelevant especially for the private sector since accounting standards were no longer issued by

the AASB but instead issued by IASB hence eliminating the need for AASB (Gordon et al,

2015).

C) Explanation of the academics` concerns regarding the benefits and limitations of the

Conceptual Framework

The conceptual framework provides concepts, which are developed in an orderly manner

that make reporting and financial accounting logical and consistent. Through the created

consistency, the framework increases compatibility of the standards both nationally and

internationally (Al-Dmour, 2018). Conceptual framework also facilitates development of the

accounting department as a whole and enhances communication. Development of accounting

CONTEMPORARY ACCOUNTING THEORY 9

standards with the help of the conceptual framework is more economical and is made easier. This

is because the basic principles have already been established (Adams, 2015). The already

debated principles can even be applied in situations, which do not have any accounting standards

relevant to them and where there are conflicts of interests on the principles and policies to apply

in particular situations. Additionally, the already established policies, which are obtained from

the conceptual framework, are less criticized. Without development of the conceptual

framework, the organizations setting the standards were most likely to make decisions basing on

the demand of the companies, which would result into issuing of ambiguous and haphazard rules.

However, with the presence of a conceptual framework, the reason behind the establishment of

specific standards is clarified and the standard setters are made accountable to financial

statement users. Generally, the conceptual framework has significantly contributed to public

confidence and credibility of financial reporting with relevance, consistence and reliability

through the use of distinctly defined principles (Adams, 2017). However, the conceptual

framework greatly relies on assumptions, which makes it of less help while preparing financial

statements. As a result, the accounting standards developed are very theoretical, academic and

can easily be exposed to fraud. Practically, these standards make financial information more

complex for users and preparers of the financial reports. Although concepts may be refined and

pure, the difficulty and complexity in understanding the importance of the financial statements

may render the conceptual framework irrelevant. In addition, the framework does not cater for

the interest on information, which facilitates stewardship management assessment. More

criticisms are raised about the emphasis of accounting principles on only economic transactions

and phenomena. There are also diverse user requirements and there may as well be need for

other standards which the conceptual framework cannot cover (Al-Dmour,2018).

standards with the help of the conceptual framework is more economical and is made easier. This

is because the basic principles have already been established (Adams, 2015). The already

debated principles can even be applied in situations, which do not have any accounting standards

relevant to them and where there are conflicts of interests on the principles and policies to apply

in particular situations. Additionally, the already established policies, which are obtained from

the conceptual framework, are less criticized. Without development of the conceptual

framework, the organizations setting the standards were most likely to make decisions basing on

the demand of the companies, which would result into issuing of ambiguous and haphazard rules.

However, with the presence of a conceptual framework, the reason behind the establishment of

specific standards is clarified and the standard setters are made accountable to financial

statement users. Generally, the conceptual framework has significantly contributed to public

confidence and credibility of financial reporting with relevance, consistence and reliability

through the use of distinctly defined principles (Adams, 2017). However, the conceptual

framework greatly relies on assumptions, which makes it of less help while preparing financial

statements. As a result, the accounting standards developed are very theoretical, academic and

can easily be exposed to fraud. Practically, these standards make financial information more

complex for users and preparers of the financial reports. Although concepts may be refined and

pure, the difficulty and complexity in understanding the importance of the financial statements

may render the conceptual framework irrelevant. In addition, the framework does not cater for

the interest on information, which facilitates stewardship management assessment. More

criticisms are raised about the emphasis of accounting principles on only economic transactions

and phenomena. There are also diverse user requirements and there may as well be need for

other standards which the conceptual framework cannot cover (Al-Dmour,2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 10

D) Explanation of the applicability of the conceptual framework by AUB Group Limited

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components?

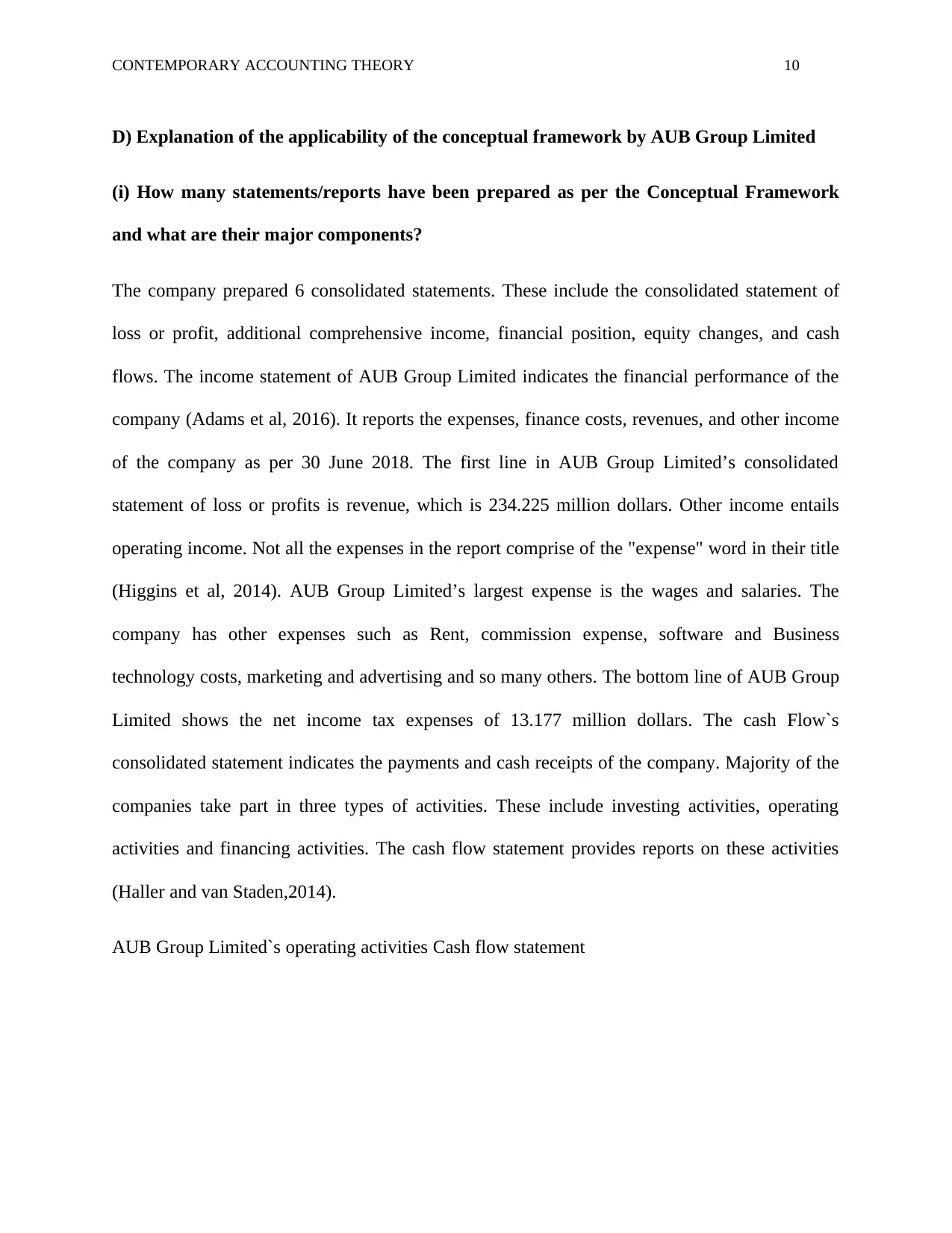

The company prepared 6 consolidated statements. These include the consolidated statement of

loss or profit, additional comprehensive income, financial position, equity changes, and cash

flows. The income statement of AUB Group Limited indicates the financial performance of the

company (Adams et al, 2016). It reports the expenses, finance costs, revenues, and other income

of the company as per 30 June 2018. The first line in AUB Group Limited’s consolidated

statement of loss or profits is revenue, which is 234.225 million dollars. Other income entails

operating income. Not all the expenses in the report comprise of the "expense" word in their title

(Higgins et al, 2014). AUB Group Limited’s largest expense is the wages and salaries. The

company has other expenses such as Rent, commission expense, software and Business

technology costs, marketing and advertising and so many others. The bottom line of AUB Group

Limited shows the net income tax expenses of 13.177 million dollars. The cash Flow`s

consolidated statement indicates the payments and cash receipts of the company. Majority of the

companies take part in three types of activities. These include investing activities, operating

activities and financing activities. The cash flow statement provides reports on these activities

(Haller and van Staden,2014).

AUB Group Limited`s operating activities Cash flow statement

D) Explanation of the applicability of the conceptual framework by AUB Group Limited

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components?

The company prepared 6 consolidated statements. These include the consolidated statement of

loss or profit, additional comprehensive income, financial position, equity changes, and cash

flows. The income statement of AUB Group Limited indicates the financial performance of the

company (Adams et al, 2016). It reports the expenses, finance costs, revenues, and other income

of the company as per 30 June 2018. The first line in AUB Group Limited’s consolidated

statement of loss or profits is revenue, which is 234.225 million dollars. Other income entails

operating income. Not all the expenses in the report comprise of the "expense" word in their title

(Higgins et al, 2014). AUB Group Limited’s largest expense is the wages and salaries. The

company has other expenses such as Rent, commission expense, software and Business

technology costs, marketing and advertising and so many others. The bottom line of AUB Group

Limited shows the net income tax expenses of 13.177 million dollars. The cash Flow`s

consolidated statement indicates the payments and cash receipts of the company. Majority of the

companies take part in three types of activities. These include investing activities, operating

activities and financing activities. The cash flow statement provides reports on these activities

(Haller and van Staden,2014).

AUB Group Limited`s operating activities Cash flow statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 11

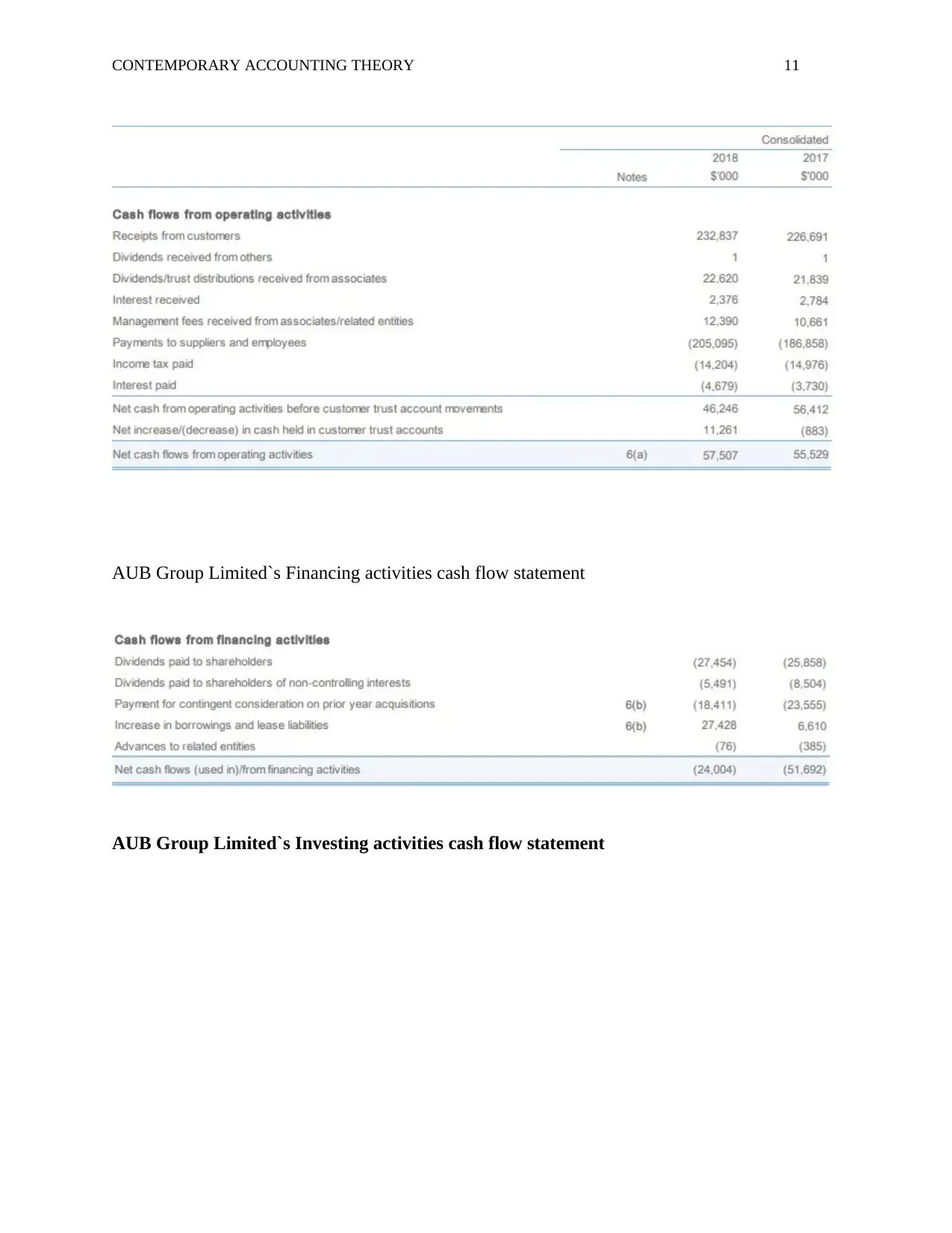

AUB Group Limited`s Financing activities cash flow statement

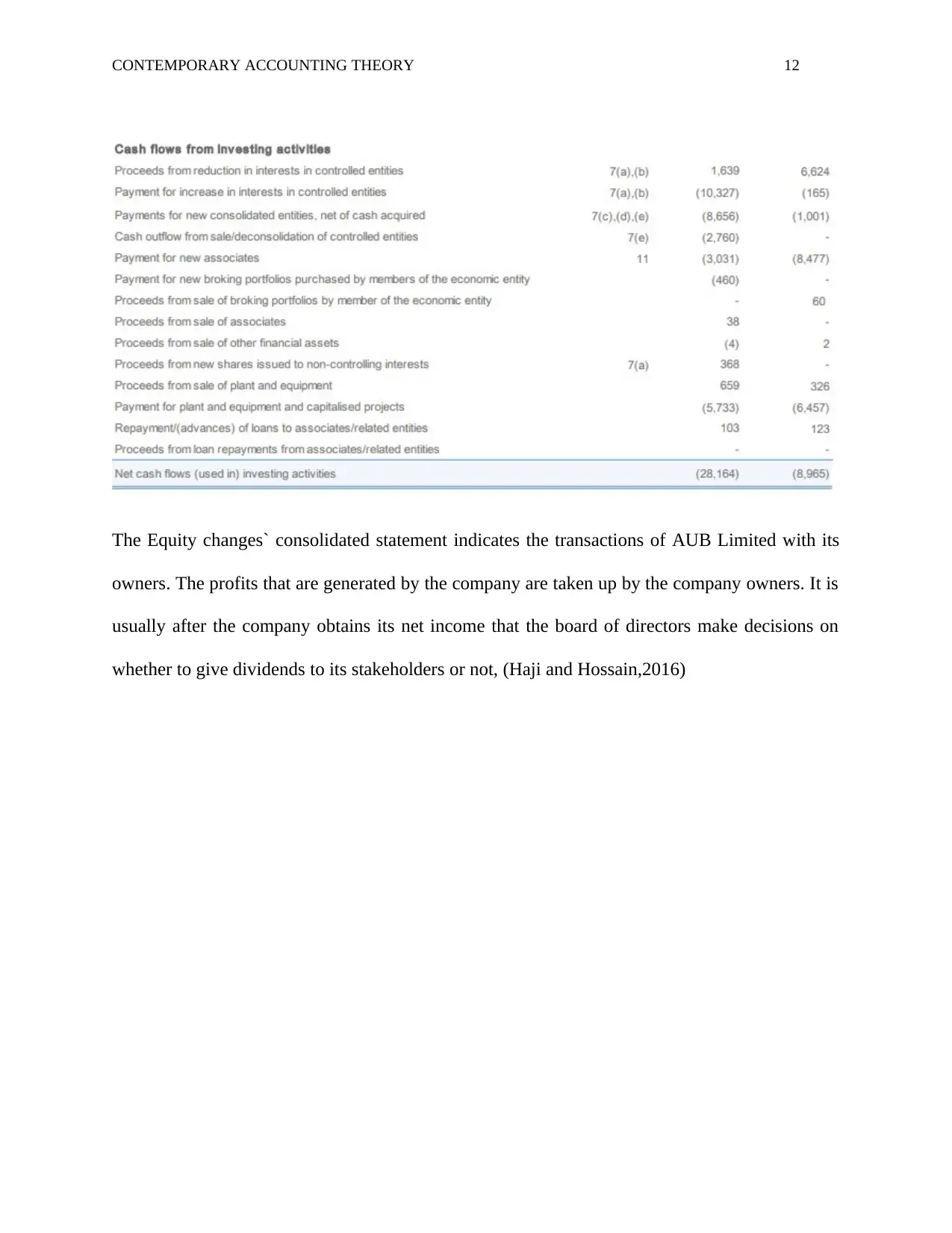

AUB Group Limited`s Investing activities cash flow statement

AUB Group Limited`s Financing activities cash flow statement

AUB Group Limited`s Investing activities cash flow statement

CONTEMPORARY ACCOUNTING THEORY 12

The Equity changes` consolidated statement indicates the transactions of AUB Limited with its

owners. The profits that are generated by the company are taken up by the company owners. It is

usually after the company obtains its net income that the board of directors make decisions on

whether to give dividends to its stakeholders or not, (Haji and Hossain,2016)

The Equity changes` consolidated statement indicates the transactions of AUB Limited with its

owners. The profits that are generated by the company are taken up by the company owners. It is

usually after the company obtains its net income that the board of directors make decisions on

whether to give dividends to its stakeholders or not, (Haji and Hossain,2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.