Financial Reporting's Conceptual Framework: An In-Depth Analysis

VerifiedAdded on 2020/10/22

|12

|3336

|100

Report

AI Summary

This report provides a comprehensive analysis of the conceptual framework for financial reporting. It begins with an introduction to the framework and outlines the research methodology, including quantitative research with a sample of 20 managerial personnel. The report discusses key concepts such as the objectives of financial statements, qualitative characteristics (understandability, relevance, reliability, comparability), and basic elements of financial statements. It explores the impact of these concepts on stakeholders' decision-making processes, highlighting the importance of IFRS, IASB, and FASB standards. The report also examines the limitations of the research, presents the results of a survey, and concludes with a discussion of the benefits of the conceptual framework for both companies and stakeholders. The survey results, presented through descriptive statistics and frequency tables, provide insights into stakeholders' perceptions of the framework's effectiveness, including the impact of comparability, reliability, and understandability on their analysis of financial statements.

Conceptual Framework for

financial reporting

financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Abstract............................................................................................................................................1

Introduction......................................................................................................................................1

Research Methodology ...................................................................................................................1

Research Approach..........................................................................................................................1

Limitation of research......................................................................................................................1

Discussion of concepts.....................................................................................................................2

Hypothesis........................................................................................................................................5

Survey..............................................................................................................................................5

Result...............................................................................................................................................6

References......................................................................................................................................10

Abstract............................................................................................................................................1

Introduction......................................................................................................................................1

Research Methodology ...................................................................................................................1

Research Approach..........................................................................................................................1

Limitation of research......................................................................................................................1

Discussion of concepts.....................................................................................................................2

Hypothesis........................................................................................................................................5

Survey..............................................................................................................................................5

Result...............................................................................................................................................6

References......................................................................................................................................10

Abstract

The present research is based on conceptual framework and various principles are applied

which are relevant to stakeholders. Sample of 20 managerial personnels are taken to analyse

effect of financial reporting taking decisions by external users.

Introduction

Aim: The Aim of this research project is to describe conceptual framework for financial

reporting and underline objective of financial statements

Objectives: The objectives can be categorised as follows-

To describe the effectiveness of conceptual framework

To clearly understand the objective of financial reporting

To assess the qualitative characteristics of financial information

To identify the basic elements of financial statements

To analyse the impact of constraints have on reporting accounting information

Research Methodology

Research type: In carrying out conceptual framework, quantitative research type is taken for

analysing research on the topic.

Sampling: Simple random sampling is used by taking sample of 20 personnels. This is helpful as

taking data from entire population is practically not possible.

Data collection: In this aspect, primary and secondary data is gathered for effectively extracting

results. Moreover, survey is also conducted to assess results.

Data Analysis: This is done by implementing descriptive analysis in order to take out research on

conceptual framework for financial reporting.

Research Approach

The research approach used in this scenario is deductive approach for carrying out

objectives of the research topic in effective manner.

Limitation of research

There are certain limitation of research such as sampling size might be small by which

results obtained may not be reliable. Another limitation is implementation of data collection

1

The present research is based on conceptual framework and various principles are applied

which are relevant to stakeholders. Sample of 20 managerial personnels are taken to analyse

effect of financial reporting taking decisions by external users.

Introduction

Aim: The Aim of this research project is to describe conceptual framework for financial

reporting and underline objective of financial statements

Objectives: The objectives can be categorised as follows-

To describe the effectiveness of conceptual framework

To clearly understand the objective of financial reporting

To assess the qualitative characteristics of financial information

To identify the basic elements of financial statements

To analyse the impact of constraints have on reporting accounting information

Research Methodology

Research type: In carrying out conceptual framework, quantitative research type is taken for

analysing research on the topic.

Sampling: Simple random sampling is used by taking sample of 20 personnels. This is helpful as

taking data from entire population is practically not possible.

Data collection: In this aspect, primary and secondary data is gathered for effectively extracting

results. Moreover, survey is also conducted to assess results.

Data Analysis: This is done by implementing descriptive analysis in order to take out research on

conceptual framework for financial reporting.

Research Approach

The research approach used in this scenario is deductive approach for carrying out

objectives of the research topic in effective manner.

Limitation of research

There are certain limitation of research such as sampling size might be small by which

results obtained may not be reliable. Another limitation is implementation of data collection

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique such as lack of having experience in collecting primary data. Moreover, literature

review findings may not be properly extracted from the scope of works attained by previous

scholars.

Discussion of concepts

As per the views of Warren and Jones (2018), conceptual framework for financial

reporting is required so that information may be disclosed in financial statements of company

and as such, stakeholders may be benefited by such information. This is essentially required to

effectively maintain and classify data of financials in the respective heads. It means that expense

and revenue must be disclosed in income statement whereas, liabilities and assets shall be

classified in balance sheet of entity. This provides clarity to shareholders in assessing financial

condition of the firm in effective way. It helps stakeholders to make better and enhanced

decisions by seeking statements in the best possible manner. In relation to this, Hermann,

DiStasio and Tkatchenko (2017) says that these statements such as balance sheet, income

statement and cash flow statement and statement of changes in equity should be made in

accordance to the framework provided by professional bodies. These are IFRS (International

Financial Reporting Standards), IASB (International Accounting Standards Board), FASB

(Financial Accounting Standards Board) to name a few. The above mentioned professional

bodies provides legal and conceptual framework to effectively prepare financial statements with

information disclosed in that manner which imparts clarity to the stakeholders in taking better

decisions.

However, on contrary to this as per the views of Larkin, DiTommaso and Ruppel (2017),

basic objective of financial reporting should be identified so that reliability can be addressed in a

better way. The main objective is to impart necessary information to potential investors, lenders

and creditor and other various stakeholders in order to give clarity about financial health of the

business in the best possible manner. This is required so that they may be able to take effective

decisions. The general purpose of preparation of financial statements is to provide stakeholders

adequate and true information which enhances them to make decisions in effectual way.

Furthermore, management of the firm is required to protect shareholders who invests in shares of

firm. This is required so that integrity and reliability may be given to them for making enhanced

decisions in the best possible manner.

2

review findings may not be properly extracted from the scope of works attained by previous

scholars.

Discussion of concepts

As per the views of Warren and Jones (2018), conceptual framework for financial

reporting is required so that information may be disclosed in financial statements of company

and as such, stakeholders may be benefited by such information. This is essentially required to

effectively maintain and classify data of financials in the respective heads. It means that expense

and revenue must be disclosed in income statement whereas, liabilities and assets shall be

classified in balance sheet of entity. This provides clarity to shareholders in assessing financial

condition of the firm in effective way. It helps stakeholders to make better and enhanced

decisions by seeking statements in the best possible manner. In relation to this, Hermann,

DiStasio and Tkatchenko (2017) says that these statements such as balance sheet, income

statement and cash flow statement and statement of changes in equity should be made in

accordance to the framework provided by professional bodies. These are IFRS (International

Financial Reporting Standards), IASB (International Accounting Standards Board), FASB

(Financial Accounting Standards Board) to name a few. The above mentioned professional

bodies provides legal and conceptual framework to effectively prepare financial statements with

information disclosed in that manner which imparts clarity to the stakeholders in taking better

decisions.

However, on contrary to this as per the views of Larkin, DiTommaso and Ruppel (2017),

basic objective of financial reporting should be identified so that reliability can be addressed in a

better way. The main objective is to impart necessary information to potential investors, lenders

and creditor and other various stakeholders in order to give clarity about financial health of the

business in the best possible manner. This is required so that they may be able to take effective

decisions. The general purpose of preparation of financial statements is to provide stakeholders

adequate and true information which enhances them to make decisions in effectual way.

Furthermore, management of the firm is required to protect shareholders who invests in shares of

firm. This is required so that integrity and reliability may be given to them for making enhanced

decisions in the best possible manner.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per the views of Jollands and Quinn (2017), IASB standards are provided to guide

organisation to prepare its financials in accordance to the framework. The concepts imparted by

IASB are more conceptual in nature and less rule based. On the other hand, Van Minh (2017)

says that FASB standards issued are in detail and more comprehensive as well. Moreover, there

are other organisations which provides standards to be followed by company. It includes IOSCO

(International Organisation of Securities Commissions) which ensures that international markets

may effectively operate on consistent basis. The conceptual framework help to ensure that

organisation provides clarity to stakeholders regarding the financial statements prepared. As per

the views of Maynard (2017), accounting information presented to stakeholders of business

should be understandable. This qualitative characteristic of accounting is quite important as firm

must disclose financial statements to them and as such, it may be easily understandable by them.

This implies that such information should be understood to even a layman. Thus, it is required

that firm should prepare financials which could be ascertained by stakeholders with much ease.

As per the views of Mazzanti and et.al (2017), it is advantageous to both company and its

stakeholders as information is disclosed in a better way. Furthermore, organisation enhances its

image in front of shareholders as it is easily understandable to them and effective decisions can

be taken by assessing such statements in the best possible manner. On the other hand, relevance

concept of accounting states that firm should provide information which is related to current

accounting period. This clearly implies that information must be relevant to take decision by the

external users of company and as such, it impacts their decision-making as well. This

information should be useful to investors and creditors, if this is not relevant, then it adversely

impacts them while taking decisions. GAAP (Generally Accepted Accounting Principles)

provides that financial statements should be prepared as per the prescribed format. This

accounting principle states that useful information must be imparted to them listed in financials.

Thus, external users are benefited by seeking such data that is relevant to take better decisions

for their own purposes in the best possible manner. Furthermore, they will be benefited by

relying on such information.

As per the views of Libby (2017), accounting information should be reliable to seek the

same by external users. Here comes the concept of reliability which is much beneficial to

stakeholders. Reliability principle states that accurate and true picture must get reflected of

3

organisation to prepare its financials in accordance to the framework. The concepts imparted by

IASB are more conceptual in nature and less rule based. On the other hand, Van Minh (2017)

says that FASB standards issued are in detail and more comprehensive as well. Moreover, there

are other organisations which provides standards to be followed by company. It includes IOSCO

(International Organisation of Securities Commissions) which ensures that international markets

may effectively operate on consistent basis. The conceptual framework help to ensure that

organisation provides clarity to stakeholders regarding the financial statements prepared. As per

the views of Maynard (2017), accounting information presented to stakeholders of business

should be understandable. This qualitative characteristic of accounting is quite important as firm

must disclose financial statements to them and as such, it may be easily understandable by them.

This implies that such information should be understood to even a layman. Thus, it is required

that firm should prepare financials which could be ascertained by stakeholders with much ease.

As per the views of Mazzanti and et.al (2017), it is advantageous to both company and its

stakeholders as information is disclosed in a better way. Furthermore, organisation enhances its

image in front of shareholders as it is easily understandable to them and effective decisions can

be taken by assessing such statements in the best possible manner. On the other hand, relevance

concept of accounting states that firm should provide information which is related to current

accounting period. This clearly implies that information must be relevant to take decision by the

external users of company and as such, it impacts their decision-making as well. This

information should be useful to investors and creditors, if this is not relevant, then it adversely

impacts them while taking decisions. GAAP (Generally Accepted Accounting Principles)

provides that financial statements should be prepared as per the prescribed format. This

accounting principle states that useful information must be imparted to them listed in financials.

Thus, external users are benefited by seeking such data that is relevant to take better decisions

for their own purposes in the best possible manner. Furthermore, they will be benefited by

relying on such information.

As per the views of Libby (2017), accounting information should be reliable to seek the

same by external users. Here comes the concept of reliability which is much beneficial to

stakeholders. Reliability principle states that accurate and true picture must get reflected of

3

financial condition to the stakeholders. This concept is much useful to investors and creditors as

it provides them with reliable information which meets their needs and as such, effective

decisions can be made by them in the best possible manner. Furthermore, if information

disclosed in various financial statements lacks accuracy then, stakeholders cannot take enhanced

decision with much ease. The reliable concept means that only those transactions should be

recorded which could be effectively verified as an evidence which implies that such transactions

must have occurred and recorded and displayed in the financial statements. It includes evidence

of receipts of purchases or even checks which are cancelled. This means that information should

be verified and can be used by external users.

The author McCann (2017) says that materiality concept of accounting states that only

material information should be recorded which is useful for stakeholders to assess financials in

the best possible manner. The principle also states that any information should be disregarded

and ignored which may not impact decision-making of stakeholders. This means that such

information can be ignored which does not affect taking decisions by them. Furthermore, non-

materials items which is not useful for external users may be disregarded but it should not

mislead them and affect in making decisions. Thus, this will affect financial statements of

company if any information which is regarded as material is ignored by the firm. Hence, material

items shall be determined by company before excluding the same from financials. On the

contrary Kvaal (2017), says that company should account for material elements and as such, any

exclusion should be made in the financials. Another concept is that accounting information must

be comparable. This means that business should consistently follow same accounting policies

year after year. It is done in a manner so that it may be easily compared with previous period to

current one in the best possible way.

As per the views of Alver and Alver (2017), comparison is beneficial for stakeholders so

that they may be able to compare previous financial statements with other in effective manner.

Moreover, external users can compare financials of one entity with another so that they can get

desired results regarding financial health of the firm in effective manner. This will provide

effective results to them with much ease. Furthermore, comparability principle is quite useful for

stakeholders by which they can easily compare performance of company in the best possible

manner. As per the views of Tucker (2017), conceptual framework is quite effective as it helps

4

it provides them with reliable information which meets their needs and as such, effective

decisions can be made by them in the best possible manner. Furthermore, if information

disclosed in various financial statements lacks accuracy then, stakeholders cannot take enhanced

decision with much ease. The reliable concept means that only those transactions should be

recorded which could be effectively verified as an evidence which implies that such transactions

must have occurred and recorded and displayed in the financial statements. It includes evidence

of receipts of purchases or even checks which are cancelled. This means that information should

be verified and can be used by external users.

The author McCann (2017) says that materiality concept of accounting states that only

material information should be recorded which is useful for stakeholders to assess financials in

the best possible manner. The principle also states that any information should be disregarded

and ignored which may not impact decision-making of stakeholders. This means that such

information can be ignored which does not affect taking decisions by them. Furthermore, non-

materials items which is not useful for external users may be disregarded but it should not

mislead them and affect in making decisions. Thus, this will affect financial statements of

company if any information which is regarded as material is ignored by the firm. Hence, material

items shall be determined by company before excluding the same from financials. On the

contrary Kvaal (2017), says that company should account for material elements and as such, any

exclusion should be made in the financials. Another concept is that accounting information must

be comparable. This means that business should consistently follow same accounting policies

year after year. It is done in a manner so that it may be easily compared with previous period to

current one in the best possible way.

As per the views of Alver and Alver (2017), comparison is beneficial for stakeholders so

that they may be able to compare previous financial statements with other in effective manner.

Moreover, external users can compare financials of one entity with another so that they can get

desired results regarding financial health of the firm in effective manner. This will provide

effective results to them with much ease. Furthermore, comparability principle is quite useful for

stakeholders by which they can easily compare performance of company in the best possible

manner. As per the views of Tucker (2017), conceptual framework is quite effective as it helps

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company may be able to disclose financials statements which are based on the accounting

principles of materiality, understandability, reliability, relevance and comparability. These

concepts or principles are much relevant to stakeholders so that they may take enhanced

decisions and furthermore, organisation is also benefited by imparting such information to the

external users which eventually enhances their faith and as such, overall reliability is obtained.

Thus, it can be said that conceptual framework for financial reporting is quite beneficial for

company and stakeholders.

Hypothesis

Research Questions

1. Do comparability concept help stakeholders to compare information?

2. Do reliability principle influences investing decisions of shareholders?

3. Do understandability concept help external users to analyse financials?

4. Do exclusion of immaterial items affect output of financial statements?

5. Do all relevant items are included in financials of company?

6. Is financial reporting beneficial for stakeholders to analyse financial health?

Survey

Questionnaire

Demographic Information

Name

1. Do you think comparability concept help stakeholders to compare information?

Strongly Agree 1

Agree 2

Strongly Disagree 3

Neutral 4

2. Do you think reliability principle influences shareholders' investing decisions ?

Yes 1

No 2

Sometimes 3

3. Do you think understandability concept help external users to analyse financial statements?

Yes 1

5

principles of materiality, understandability, reliability, relevance and comparability. These

concepts or principles are much relevant to stakeholders so that they may take enhanced

decisions and furthermore, organisation is also benefited by imparting such information to the

external users which eventually enhances their faith and as such, overall reliability is obtained.

Thus, it can be said that conceptual framework for financial reporting is quite beneficial for

company and stakeholders.

Hypothesis

Research Questions

1. Do comparability concept help stakeholders to compare information?

2. Do reliability principle influences investing decisions of shareholders?

3. Do understandability concept help external users to analyse financials?

4. Do exclusion of immaterial items affect output of financial statements?

5. Do all relevant items are included in financials of company?

6. Is financial reporting beneficial for stakeholders to analyse financial health?

Survey

Questionnaire

Demographic Information

Name

1. Do you think comparability concept help stakeholders to compare information?

Strongly Agree 1

Agree 2

Strongly Disagree 3

Neutral 4

2. Do you think reliability principle influences shareholders' investing decisions ?

Yes 1

No 2

Sometimes 3

3. Do you think understandability concept help external users to analyse financial statements?

Yes 1

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

No 2

Sometimes 3

4. Do you think excluding immaterial items affects overall output of financial statements?

Strongly Agree 1

Agree 2

Strongly Disagree 3

Neutral 4

5. Do you include all relevant items in the financial statements of the business units?

Yes 1

No 2

Sometimes 3

6. Is financial reporting beneficial to stakeholders for attaining desired information regarding

financial health of company?

Yes 1

No 2

Sometimes 3

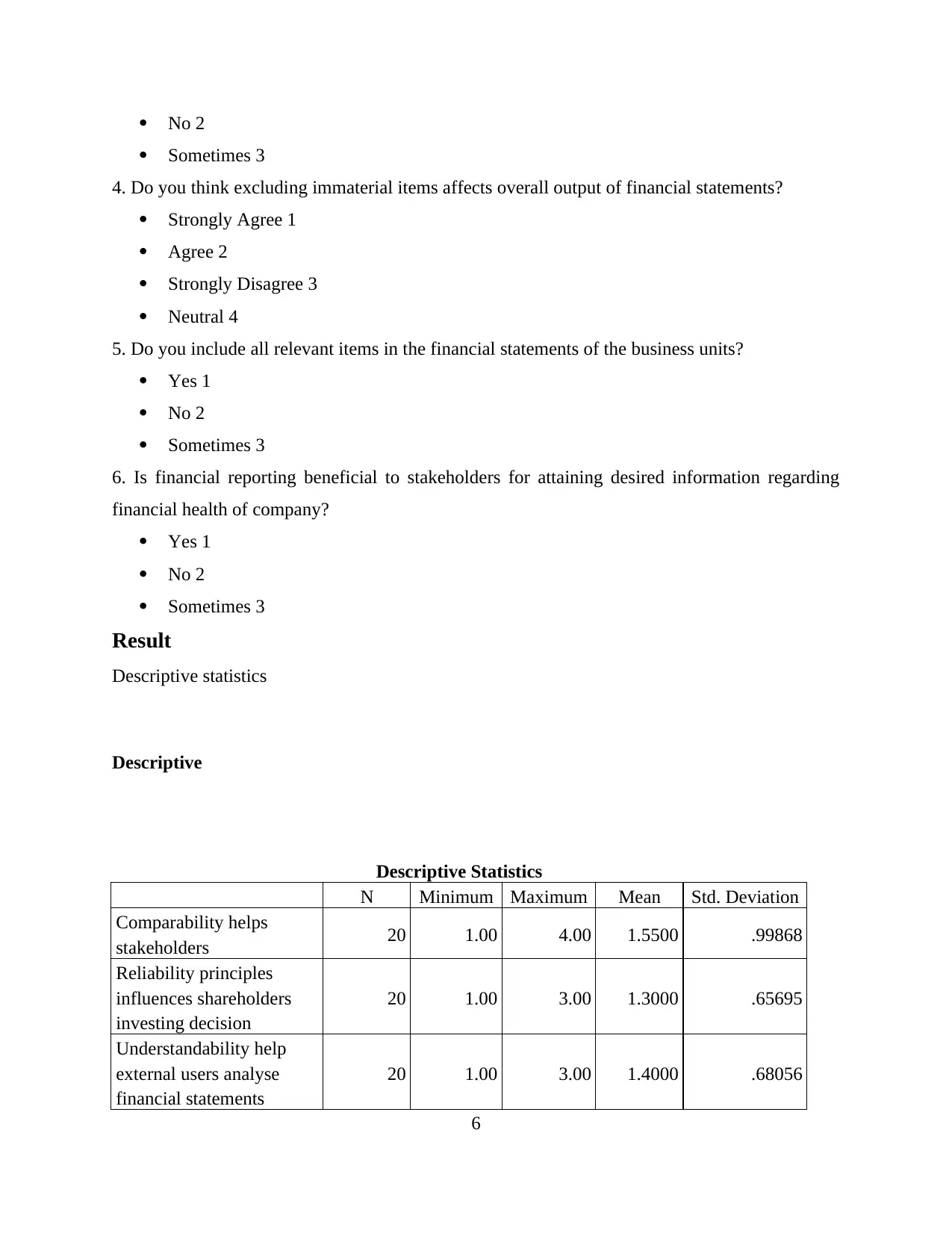

Result

Descriptive statistics

Descriptive

Descriptive Statistics

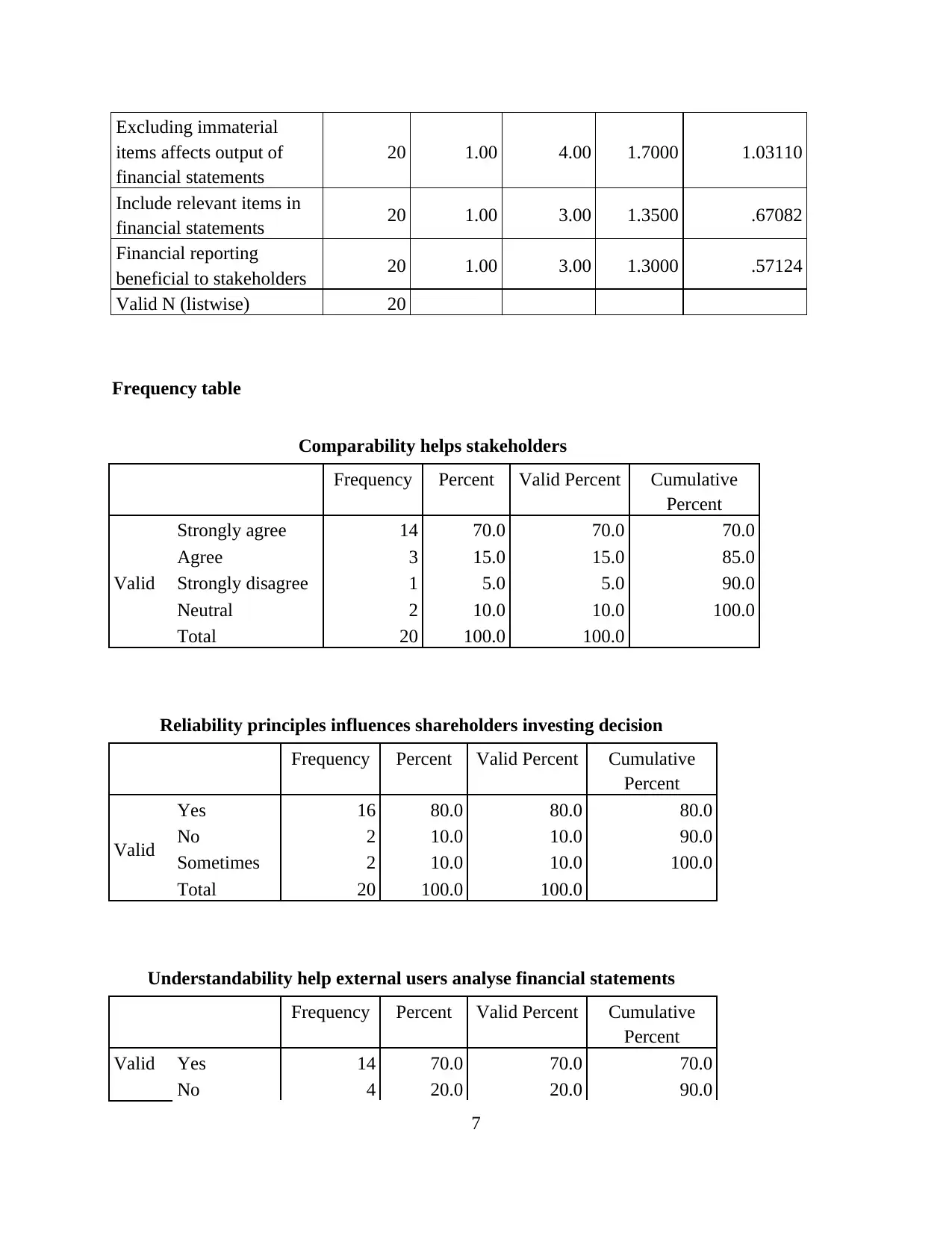

N Minimum Maximum Mean Std. Deviation

Comparability helps

stakeholders 20 1.00 4.00 1.5500 .99868

Reliability principles

influences shareholders

investing decision

20 1.00 3.00 1.3000 .65695

Understandability help

external users analyse

financial statements

20 1.00 3.00 1.4000 .68056

6

Sometimes 3

4. Do you think excluding immaterial items affects overall output of financial statements?

Strongly Agree 1

Agree 2

Strongly Disagree 3

Neutral 4

5. Do you include all relevant items in the financial statements of the business units?

Yes 1

No 2

Sometimes 3

6. Is financial reporting beneficial to stakeholders for attaining desired information regarding

financial health of company?

Yes 1

No 2

Sometimes 3

Result

Descriptive statistics

Descriptive

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Comparability helps

stakeholders 20 1.00 4.00 1.5500 .99868

Reliability principles

influences shareholders

investing decision

20 1.00 3.00 1.3000 .65695

Understandability help

external users analyse

financial statements

20 1.00 3.00 1.4000 .68056

6

Excluding immaterial

items affects output of

financial statements

20 1.00 4.00 1.7000 1.03110

Include relevant items in

financial statements 20 1.00 3.00 1.3500 .67082

Financial reporting

beneficial to stakeholders 20 1.00 3.00 1.3000 .57124

Valid N (listwise) 20

Frequency table

Comparability helps stakeholders

Frequency Percent Valid Percent Cumulative

Percent

Valid

Strongly agree 14 70.0 70.0 70.0

Agree 3 15.0 15.0 85.0

Strongly disagree 1 5.0 5.0 90.0

Neutral 2 10.0 10.0 100.0

Total 20 100.0 100.0

Reliability principles influences shareholders investing decision

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 16 80.0 80.0 80.0

No 2 10.0 10.0 90.0

Sometimes 2 10.0 10.0 100.0

Total 20 100.0 100.0

Understandability help external users analyse financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid Yes 14 70.0 70.0 70.0

No 4 20.0 20.0 90.0

7

items affects output of

financial statements

20 1.00 4.00 1.7000 1.03110

Include relevant items in

financial statements 20 1.00 3.00 1.3500 .67082

Financial reporting

beneficial to stakeholders 20 1.00 3.00 1.3000 .57124

Valid N (listwise) 20

Frequency table

Comparability helps stakeholders

Frequency Percent Valid Percent Cumulative

Percent

Valid

Strongly agree 14 70.0 70.0 70.0

Agree 3 15.0 15.0 85.0

Strongly disagree 1 5.0 5.0 90.0

Neutral 2 10.0 10.0 100.0

Total 20 100.0 100.0

Reliability principles influences shareholders investing decision

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 16 80.0 80.0 80.0

No 2 10.0 10.0 90.0

Sometimes 2 10.0 10.0 100.0

Total 20 100.0 100.0

Understandability help external users analyse financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid Yes 14 70.0 70.0 70.0

No 4 20.0 20.0 90.0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

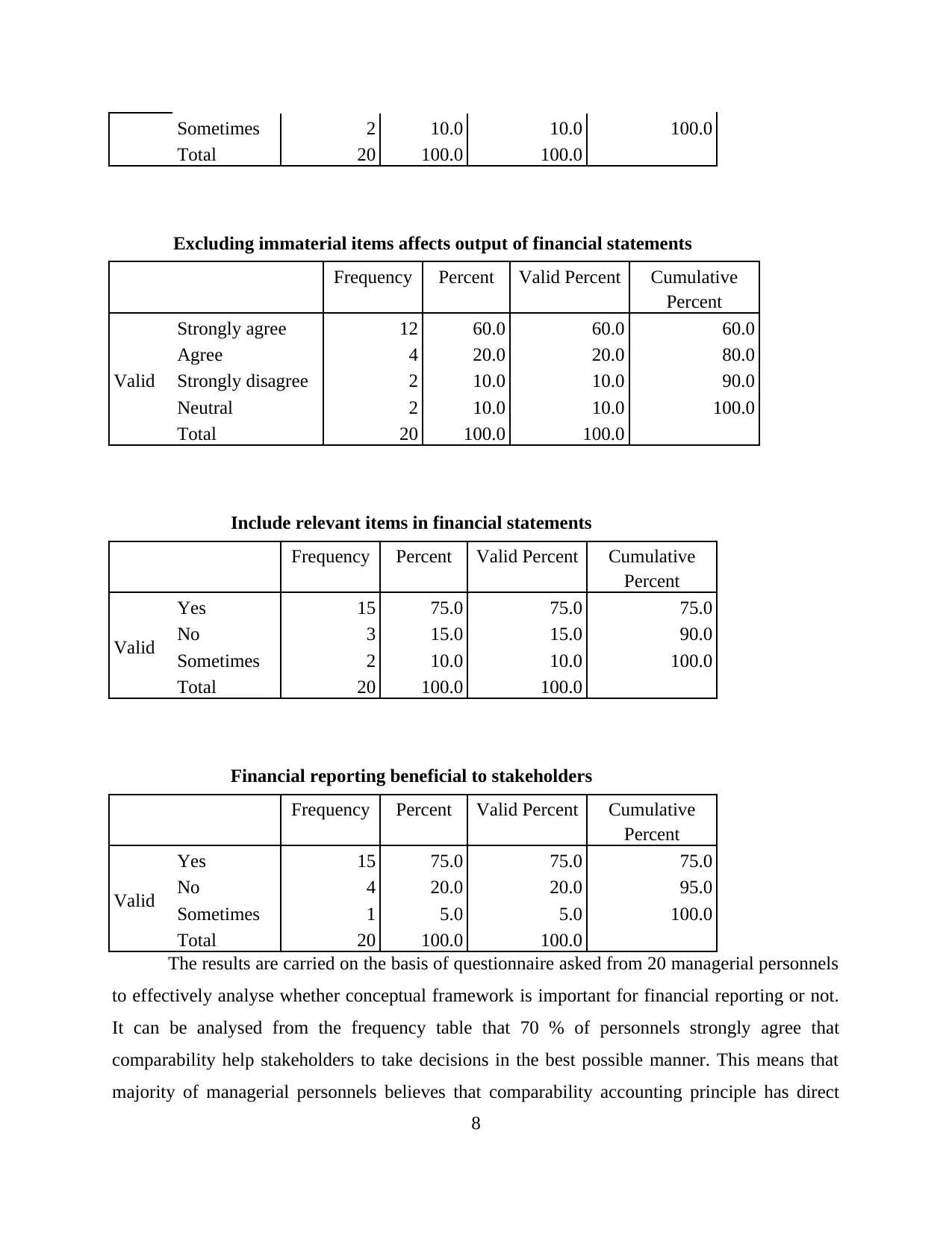

Sometimes 2 10.0 10.0 100.0

Total 20 100.0 100.0

Excluding immaterial items affects output of financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid

Strongly agree 12 60.0 60.0 60.0

Agree 4 20.0 20.0 80.0

Strongly disagree 2 10.0 10.0 90.0

Neutral 2 10.0 10.0 100.0

Total 20 100.0 100.0

Include relevant items in financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 15 75.0 75.0 75.0

No 3 15.0 15.0 90.0

Sometimes 2 10.0 10.0 100.0

Total 20 100.0 100.0

Financial reporting beneficial to stakeholders

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 15 75.0 75.0 75.0

No 4 20.0 20.0 95.0

Sometimes 1 5.0 5.0 100.0

Total 20 100.0 100.0

The results are carried on the basis of questionnaire asked from 20 managerial personnels

to effectively analyse whether conceptual framework is important for financial reporting or not.

It can be analysed from the frequency table that 70 % of personnels strongly agree that

comparability help stakeholders to take decisions in the best possible manner. This means that

majority of managerial personnels believes that comparability accounting principle has direct

8

Total 20 100.0 100.0

Excluding immaterial items affects output of financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid

Strongly agree 12 60.0 60.0 60.0

Agree 4 20.0 20.0 80.0

Strongly disagree 2 10.0 10.0 90.0

Neutral 2 10.0 10.0 100.0

Total 20 100.0 100.0

Include relevant items in financial statements

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 15 75.0 75.0 75.0

No 3 15.0 15.0 90.0

Sometimes 2 10.0 10.0 100.0

Total 20 100.0 100.0

Financial reporting beneficial to stakeholders

Frequency Percent Valid Percent Cumulative

Percent

Valid

Yes 15 75.0 75.0 75.0

No 4 20.0 20.0 95.0

Sometimes 1 5.0 5.0 100.0

Total 20 100.0 100.0

The results are carried on the basis of questionnaire asked from 20 managerial personnels

to effectively analyse whether conceptual framework is important for financial reporting or not.

It can be analysed from the frequency table that 70 % of personnels strongly agree that

comparability help stakeholders to take decisions in the best possible manner. This means that

majority of managerial personnels believes that comparability accounting principle has direct

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

impact to take decision by the external users of company. In relation to this, mean value arrived

is 1.55 which means that maximum personnels are of view that comparability principle has much

significance and also standard deviation is 0.99.

On the other hand, second questions asked to respondents was related to whether

reliability principle affects shareholders' investing decision or not. In such analysis, it is found

that majority of respondents are in favour of this principle as investing decision is influenced by

reliability observed in the financials statements prepared by company. It can be analysed that

there are almost 80 % managerial personnels who said yes and are in favour of the question

asked to them. Furthermore, mean value calculated comes to 1.30 which means that respondents

believe reliability concept has importance in shareholders taking decision whether to invest or

not. The standard deviation is 0.65 which means that this much amount of population differs

from mean value. While, understandability principle regarding question was asked which 70 %

of personnels believes that this principle affects external users when assessing financials. The

value of mean calculated is 1.40 and standard deviation is 0.68 which implies that

understandability principle influences stakeholders when they assess financial statements.

On the other hand, materiality concept also plays important role in financial reporting. It

can be interpreted that excluding immaterial items affects output of statements prepared by

company. This is evident from the fact that these items influences the output quite effectively.

Mean value is 1.70 and standard deviation is 1.03. While, another question was asked to

respondents regarding inclusion of relevant items influences financials. It can be interpreted that

mean arrived is 1.35 and standard deviation calculated is 0.67. It can be seen that 75 % of

respondents believe that relevance concept enhances value of financial statements. On the other

hand, response received in question related to whether financial reporting is beneficial to

stakeholders or not. In this case, 75 % of respondents believes that reporting is quite useful to

external users to effectively assess financial health of firm. Thus, it can be analysed that

conceptual framework related to financial reporting is useful for stakeholders in order to evaluate

financial condition of company and it enhances external users to take decisions.

9

is 1.55 which means that maximum personnels are of view that comparability principle has much

significance and also standard deviation is 0.99.

On the other hand, second questions asked to respondents was related to whether

reliability principle affects shareholders' investing decision or not. In such analysis, it is found

that majority of respondents are in favour of this principle as investing decision is influenced by

reliability observed in the financials statements prepared by company. It can be analysed that

there are almost 80 % managerial personnels who said yes and are in favour of the question

asked to them. Furthermore, mean value calculated comes to 1.30 which means that respondents

believe reliability concept has importance in shareholders taking decision whether to invest or

not. The standard deviation is 0.65 which means that this much amount of population differs

from mean value. While, understandability principle regarding question was asked which 70 %

of personnels believes that this principle affects external users when assessing financials. The

value of mean calculated is 1.40 and standard deviation is 0.68 which implies that

understandability principle influences stakeholders when they assess financial statements.

On the other hand, materiality concept also plays important role in financial reporting. It

can be interpreted that excluding immaterial items affects output of statements prepared by

company. This is evident from the fact that these items influences the output quite effectively.

Mean value is 1.70 and standard deviation is 1.03. While, another question was asked to

respondents regarding inclusion of relevant items influences financials. It can be interpreted that

mean arrived is 1.35 and standard deviation calculated is 0.67. It can be seen that 75 % of

respondents believe that relevance concept enhances value of financial statements. On the other

hand, response received in question related to whether financial reporting is beneficial to

stakeholders or not. In this case, 75 % of respondents believes that reporting is quite useful to

external users to effectively assess financial health of firm. Thus, it can be analysed that

conceptual framework related to financial reporting is useful for stakeholders in order to evaluate

financial condition of company and it enhances external users to take decisions.

9

References

Alver, L. and Alver, J., 2017. The Role and Current Status of IFRS in the Completion of the

National Accounting Rules–Evidence from Estonia. Accounting in Europe. 14(1-2). pp.80-

87.

Hermann, J., DiStasio Jr, R. A. and Tkatchenko, A., 2017. First-principles models for van der

Waals interactions in molecules and materials: concepts, theory, and applications.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts.Accounting, Auditing & Accountability Journal. 30(1). pp.164-190.

Kvaal, E., 2017. The role and current status of IFRS in the completion of national accounting

rules–Evidence from Norway. Accounting in Europe. 14(1-2). pp.150-157.

Larkin, R. F., DiTommaso, M. and Ruppel, W., 2017. Wiley Not-for-Profit GAAP 2017:

Interpretation and Application of Generally Accepted Accounting Principles. John Wiley

& Sons.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Maynard, J., 2017. Financial Accounting, Reporting, and Analysis. Oxford University Press.

Mazzanti, P. and et.al, 2017, March. Geotechnical asset management for Italian transport

agencies: Implementation principles and concepts. In Transport Infrastructure and

Systems: Proceedings of the AIIT International Congress on Transport Infrastructure and

Systems (Rome, Italy, 10-12 April 2017) (p. 325). CRC Press.

McCann, L. M., 2017. Thinking outside the ledger: a visual representation project for accounting

students. The Accounting Educators' Journal. 26.

Tucker, B. P., 2017. Figuratively speaking: analogies in the accounting classroom. Accounting

Education. 26(2). pp.166-190.

Van Minh, N., 2017. Quantum gauss-Jordan elimination and simulation of accounting principles

on quantum computers.International Journal of Theoretical Physics. 56(6). pp.1948-1960.

Ward, D. M. and Calabrese, T., 2018. Accounting fundamentals for health care management.

Jones & Bartlett Learning.

10

Alver, L. and Alver, J., 2017. The Role and Current Status of IFRS in the Completion of the

National Accounting Rules–Evidence from Estonia. Accounting in Europe. 14(1-2). pp.80-

87.

Hermann, J., DiStasio Jr, R. A. and Tkatchenko, A., 2017. First-principles models for van der

Waals interactions in molecules and materials: concepts, theory, and applications.

Jollands, S. and Quinn, M., 2017. Politicising the sustaining of water supply in Ireland–the role

of accounting concepts.Accounting, Auditing & Accountability Journal. 30(1). pp.164-190.

Kvaal, E., 2017. The role and current status of IFRS in the completion of national accounting

rules–Evidence from Norway. Accounting in Europe. 14(1-2). pp.150-157.

Larkin, R. F., DiTommaso, M. and Ruppel, W., 2017. Wiley Not-for-Profit GAAP 2017:

Interpretation and Application of Generally Accepted Accounting Principles. John Wiley

& Sons.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Maynard, J., 2017. Financial Accounting, Reporting, and Analysis. Oxford University Press.

Mazzanti, P. and et.al, 2017, March. Geotechnical asset management for Italian transport

agencies: Implementation principles and concepts. In Transport Infrastructure and

Systems: Proceedings of the AIIT International Congress on Transport Infrastructure and

Systems (Rome, Italy, 10-12 April 2017) (p. 325). CRC Press.

McCann, L. M., 2017. Thinking outside the ledger: a visual representation project for accounting

students. The Accounting Educators' Journal. 26.

Tucker, B. P., 2017. Figuratively speaking: analogies in the accounting classroom. Accounting

Education. 26(2). pp.166-190.

Van Minh, N., 2017. Quantum gauss-Jordan elimination and simulation of accounting principles

on quantum computers.International Journal of Theoretical Physics. 56(6). pp.1948-1960.

Ward, D. M. and Calabrese, T., 2018. Accounting fundamentals for health care management.

Jones & Bartlett Learning.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.