Conceptual Framework Analysis of Financial Statements: A Report

VerifiedAdded on 2020/03/04

|14

|2759

|245

Report

AI Summary

This report provides an in-depth analysis of the conceptual framework in accounting, examining the financial statements of Australian Agricultural Company Limited and Australian Vintage Limited. It explores key elements, accounting concepts, and standards, including IASB, AASB, and IFRS guidelines, to assess their application in practice. The report covers concepts like prudence, disclosure of differences, segment reporting, and the treatment of fixed and current assets. It highlights the companies' adherence to and deviations from the framework, considering aspects such as historical cost versus fair value accounting, and the use of various accounting assumptions. The analysis aims to help stakeholders make informed decisions by understanding the reliability, consistency, and comparability of financial information, ultimately offering recommendations and conclusions based on the findings. The report also considers the impact of different corporation acts and segment reporting on financial data presentation.

RUNNING HEAD: Advance Accounting

1

ADVANCE ACCOUNTING

1

ADVANCE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Accounting

2

Executive Summary

This report depicts the users about the conceptual framework concept. This report has

been prepared to make them understand about the key elements and accounting concept

which could assist organization’s external and internal stakeholders to make decision about

the company. In this report Australia virgin company and Australia Agriculture Company

limited’s annual report have been analyzed to recognize the concepts used by the company.

This corporation’s financial statement has been purposeful according to understandability of

conceptual framework which has been analyzed. IFSR, IASB, AASB and accounting

standards have been analyzed to perform this study.

2

Executive Summary

This report depicts the users about the conceptual framework concept. This report has

been prepared to make them understand about the key elements and accounting concept

which could assist organization’s external and internal stakeholders to make decision about

the company. In this report Australia virgin company and Australia Agriculture Company

limited’s annual report have been analyzed to recognize the concepts used by the company.

This corporation’s financial statement has been purposeful according to understandability of

conceptual framework which has been analyzed. IFSR, IASB, AASB and accounting

standards have been analyzed to perform this study.

Advance Accounting

3

Contents

Introduction.......................................................................................................................4

Australian Agriculture Company limited.........................................................................4

Final Financial Statement.............................................................................................4

Extract of annual reports...............................................................................................5

Snap shot of annual reports...........................................................................................5

Australian Vintage limited................................................................................................7

Income Statement.........................................................................................................7

Extract of annual reports...............................................................................................8

Snap shot of annual reports...........................................................................................8

Concept of prudence.......................................................................................................10

Disclosure of differences................................................................................................10

Segment reporting...........................................................................................................11

Fixed assets.....................................................................................................................11

Current assets..................................................................................................................11

Recommendation and conclusion...................................................................................11

References.......................................................................................................................13

3

Contents

Introduction.......................................................................................................................4

Australian Agriculture Company limited.........................................................................4

Final Financial Statement.............................................................................................4

Extract of annual reports...............................................................................................5

Snap shot of annual reports...........................................................................................5

Australian Vintage limited................................................................................................7

Income Statement.........................................................................................................7

Extract of annual reports...............................................................................................8

Snap shot of annual reports...........................................................................................8

Concept of prudence.......................................................................................................10

Disclosure of differences................................................................................................10

Segment reporting...........................................................................................................11

Fixed assets.....................................................................................................................11

Current assets..................................................................................................................11

Recommendation and conclusion...................................................................................11

References.......................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advance Accounting

4

Introduction:

Conceptual framework is just a guideline offered by the IASB and AASB to the

professionals and the companies to maintain, present and prepare the final statements of the

company. It is not evaluated as a regulation or a guideline about preparation and presentation

of final statement of a company. These conceptual framework rules help the company to

manage the aspects related to final financial statement and assist them to prepare the bets

final statements and present them in a well manner. These frameworks have been set by the

IASB/AASB to make it quite easy for the stakeholders to make decision about the

performance and position of the company. It ensures the internal and external stakeholder of

the company about their reliability, consistency, compliance, relevancy, comparability etc. It

has removed the complexity from the earlier set regulations to make it easy for the

professionals to prepare the final statements and present them in a good manner.

Basically, conceptual framework has been set to offer huge knowledge about the

regulations, norms, rules of IASB and AASB standards so that the professionals find it easy

to understand and apply it while preparing the final statements. With the help of Conceptual

framework, it becomes quite easy for the stakeholders to make decision about the

performance and position of the company.

Australian Agriculture Company limited:

Australian Agricultural Company Limited manufactures and sells beef in Australian

market. This company is engaging in possessing, functioning, and developing countrified

properties; dealing in beef, including reproduction, feedlot ting, back grounding and

processing the cattle and the grass fed beef production, grain fed beef production, and Wagyu

beef production. This company functions under many brands such as Wylarah, 1824,

Westholme, Welltree and Brunette Downs Grass-fed Beef brands. It functions an

incorporated cattle creation system across around 18 owned cattle stations, 7 agisted

properties, 2 leased stations, and a beef processing facility, 2 owned feedlots and 2 owned

farms which are covering an area of around 7 million hectares of Queensland and around the

Northern Territory (Bloomberg, 2017). The Australian agriculture company limited also

exports its beef items to around 20 countries. It has been founded in 1824 and currently it is

in Newstead, Australia.

Final Financial Statement:

4

Introduction:

Conceptual framework is just a guideline offered by the IASB and AASB to the

professionals and the companies to maintain, present and prepare the final statements of the

company. It is not evaluated as a regulation or a guideline about preparation and presentation

of final statement of a company. These conceptual framework rules help the company to

manage the aspects related to final financial statement and assist them to prepare the bets

final statements and present them in a well manner. These frameworks have been set by the

IASB/AASB to make it quite easy for the stakeholders to make decision about the

performance and position of the company. It ensures the internal and external stakeholder of

the company about their reliability, consistency, compliance, relevancy, comparability etc. It

has removed the complexity from the earlier set regulations to make it easy for the

professionals to prepare the final statements and present them in a good manner.

Basically, conceptual framework has been set to offer huge knowledge about the

regulations, norms, rules of IASB and AASB standards so that the professionals find it easy

to understand and apply it while preparing the final statements. With the help of Conceptual

framework, it becomes quite easy for the stakeholders to make decision about the

performance and position of the company.

Australian Agriculture Company limited:

Australian Agricultural Company Limited manufactures and sells beef in Australian

market. This company is engaging in possessing, functioning, and developing countrified

properties; dealing in beef, including reproduction, feedlot ting, back grounding and

processing the cattle and the grass fed beef production, grain fed beef production, and Wagyu

beef production. This company functions under many brands such as Wylarah, 1824,

Westholme, Welltree and Brunette Downs Grass-fed Beef brands. It functions an

incorporated cattle creation system across around 18 owned cattle stations, 7 agisted

properties, 2 leased stations, and a beef processing facility, 2 owned feedlots and 2 owned

farms which are covering an area of around 7 million hectares of Queensland and around the

Northern Territory (Bloomberg, 2017). The Australian agriculture company limited also

exports its beef items to around 20 countries. It has been founded in 1824 and currently it is

in Newstead, Australia.

Final Financial Statement:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Accounting

5

Australian agriculture limited is an organization that has a main goal of earning the

profits and enhances the growth of the company. A registration has been done by this

company in the Australian stock exchange so that it could trade into the Australian stock

market. Annual report of the company has been analyzed and found that entire aspects of the

company which has been shown into the annual report of the company are not according to

the IASB and AASB framework. Company has used many aspects which are not ethical such

as it somewhere company has used the traditional method and somewhere modern approach

has been used by the company according to its benefits (ACCA Global, 2017). It has been

analyzed that the final statements of the company has not been prepared according to the

IASB and AASB compliances.

Extract of annual reports:

Annual report of the company has been analyzed to conduct a study over the

Australian agriculture company limited. The following extracts have been evaluated further

for this study:

The final financial statement of the Australian agriculture company limited:

Has not been incorporated with entire IASB and AASB guidelines

Corporation act has not been considered by the accountant while preparing the statements

Historical cost concept as well s fair value accounting, both approaches have been considered

AUD currency sign has been used for the data in the annual reports

Some data has been misstated in the annual report of the company

International regulations of accounting have not been followed (Annual report, 2017)

Materiality, going concern and accrued accounting assumptions have been used.

Snap shot of annual reports:

The annual report evaluation of the company depict that there are huge mistakes

which has taken place while preparing and presenting this data. Still, it has been analyzed that

the mistakes are of a little level which could not make a huge impact over the reports and

opinion of stakeholder of the company about the operations, performance and profitability of

the firm (IASB, 2006). It has been analyzed that company have tried to use the entire

5

Australian agriculture limited is an organization that has a main goal of earning the

profits and enhances the growth of the company. A registration has been done by this

company in the Australian stock exchange so that it could trade into the Australian stock

market. Annual report of the company has been analyzed and found that entire aspects of the

company which has been shown into the annual report of the company are not according to

the IASB and AASB framework. Company has used many aspects which are not ethical such

as it somewhere company has used the traditional method and somewhere modern approach

has been used by the company according to its benefits (ACCA Global, 2017). It has been

analyzed that the final statements of the company has not been prepared according to the

IASB and AASB compliances.

Extract of annual reports:

Annual report of the company has been analyzed to conduct a study over the

Australian agriculture company limited. The following extracts have been evaluated further

for this study:

The final financial statement of the Australian agriculture company limited:

Has not been incorporated with entire IASB and AASB guidelines

Corporation act has not been considered by the accountant while preparing the statements

Historical cost concept as well s fair value accounting, both approaches have been considered

AUD currency sign has been used for the data in the annual reports

Some data has been misstated in the annual report of the company

International regulations of accounting have not been followed (Annual report, 2017)

Materiality, going concern and accrued accounting assumptions have been used.

Snap shot of annual reports:

The annual report evaluation of the company depict that there are huge mistakes

which has taken place while preparing and presenting this data. Still, it has been analyzed that

the mistakes are of a little level which could not make a huge impact over the reports and

opinion of stakeholder of the company about the operations, performance and profitability of

the firm (IASB, 2006). It has been analyzed that company have tried to use the entire

Advance Accounting

6

guideline of conceptual framework while preparing and presenting the final financial

statements of the company.

6

guideline of conceptual framework while preparing and presenting the final financial

statements of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advance Accounting

7

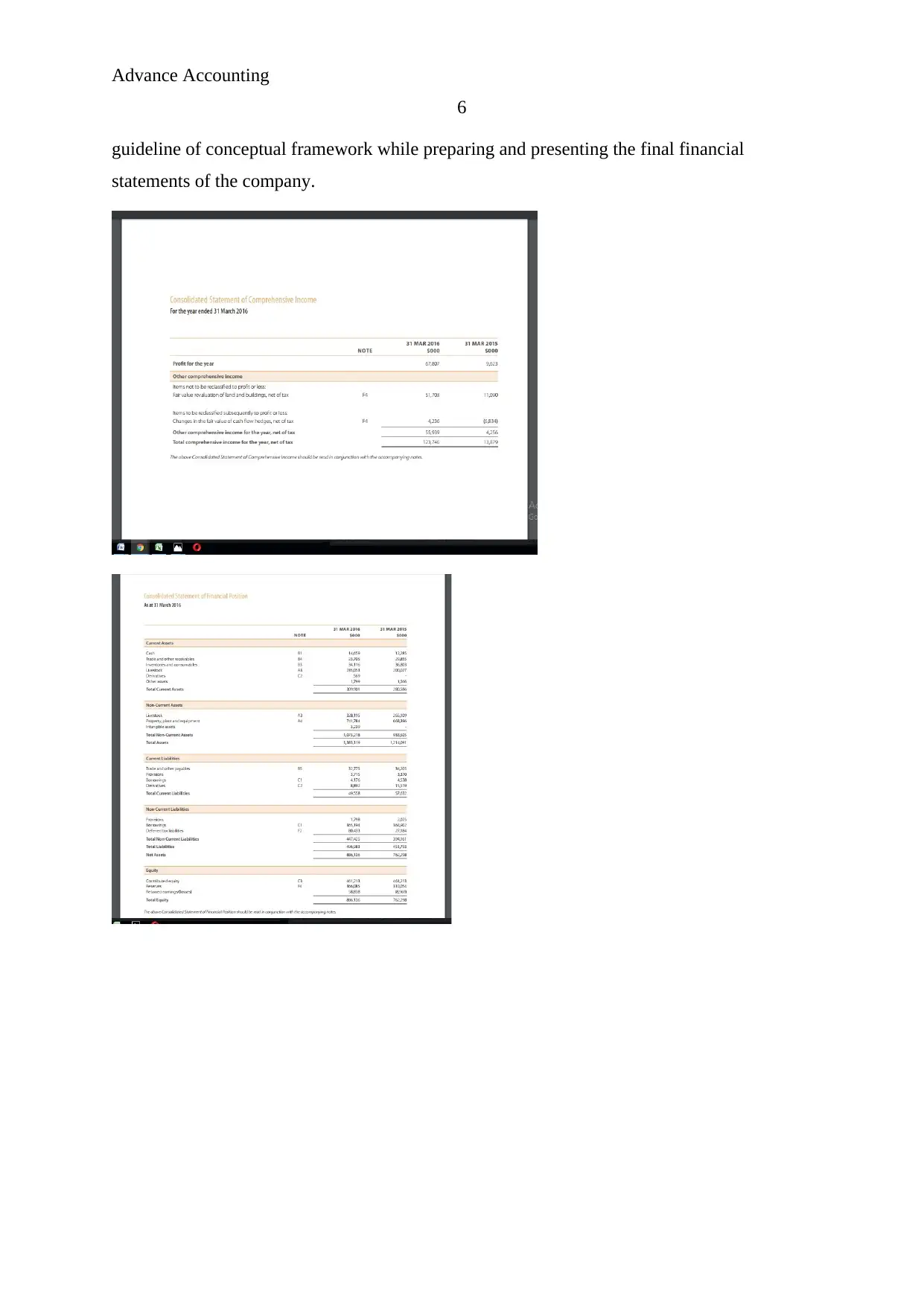

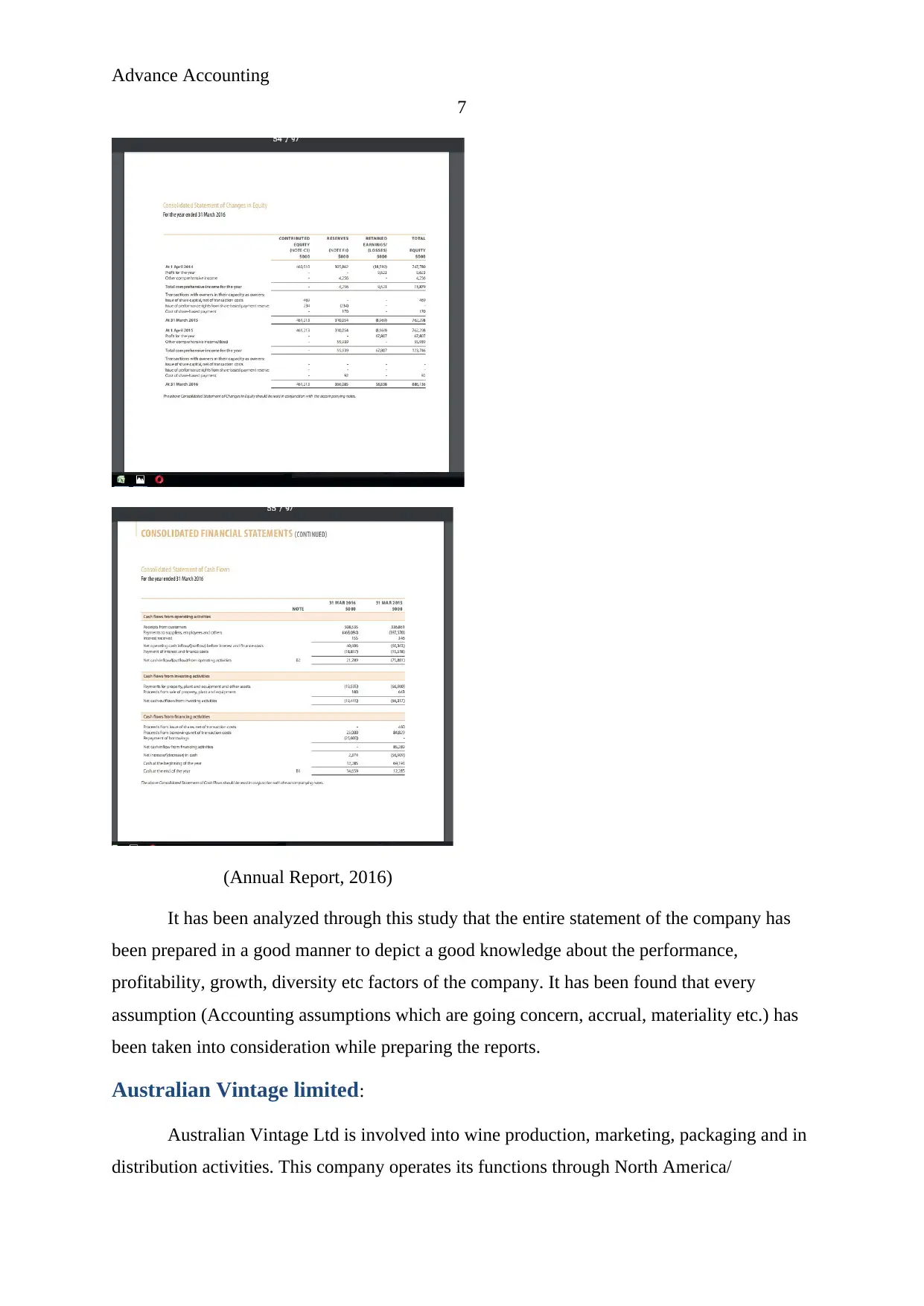

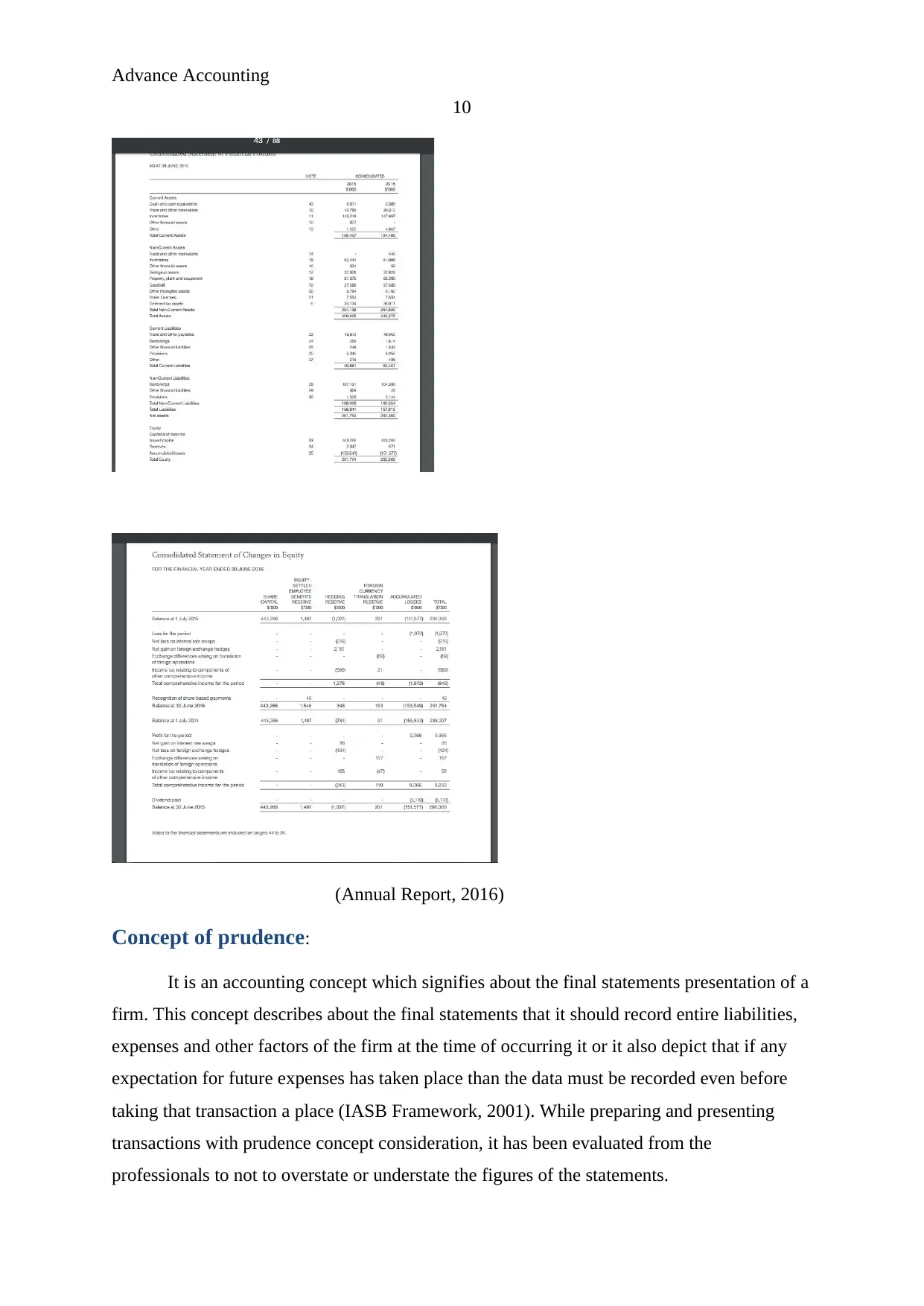

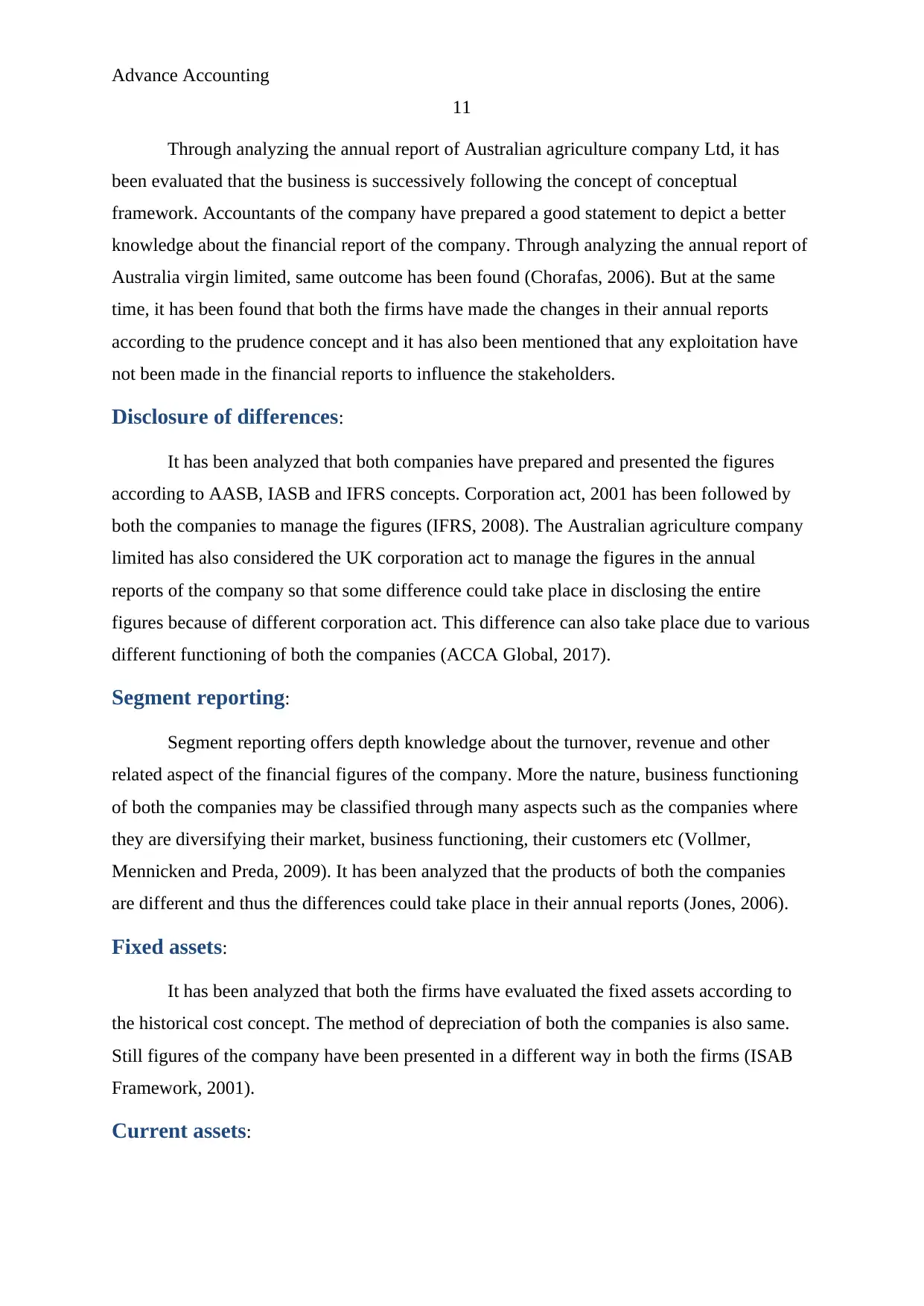

(Annual Report, 2016)

It has been analyzed through this study that the entire statement of the company has

been prepared in a good manner to depict a good knowledge about the performance,

profitability, growth, diversity etc factors of the company. It has been found that every

assumption (Accounting assumptions which are going concern, accrual, materiality etc.) has

been taken into consideration while preparing the reports.

Australian Vintage limited:

Australian Vintage Ltd is involved into wine production, marketing, packaging and in

distribution activities. This company operates its functions through North America/

7

(Annual Report, 2016)

It has been analyzed through this study that the entire statement of the company has

been prepared in a good manner to depict a good knowledge about the performance,

profitability, growth, diversity etc factors of the company. It has been found that every

assumption (Accounting assumptions which are going concern, accrual, materiality etc.) has

been taken into consideration while preparing the reports.

Australian Vintage limited:

Australian Vintage Ltd is involved into wine production, marketing, packaging and in

distribution activities. This company operates its functions through North America/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Accounting

8

Australasia Packaged, Cellar Door, UK/Europe, North America/ Australia Bulk & Processing

segments and wine grower segments. It provides wine under many brands such as Miranda,

McGuigan, Nepenthe, Passion Pop brands and Tempus Two. This company also possesses,

administers, and maintains wine grower and offers packaged and mass wines, at the same

time, it also offers concentrate over the winery processing services. This company sells its

manufacturing items through distributer, wholesaler and retailer channels, as well as it also

uses the regional outlets to sell its products (Bloomberg, 2017). This company is situated in

Balmain, Australia.

Income Statement:

Australian vintage limited is an organization that has a main goal of earning the

profits and enhances the growth of the company. Annual report of the company has been

analyzed and found that entire aspects of the company which has been shown into the annual

report of the company are not according to the IASB and AASB framework. Company has

used many aspects which are not ethical such as it somewhere company has used the

traditional method and somewhere modern approach has been used by the company

according to its benefits (Bezemer, 2010). A registration has been done by this company in

the Australian stock exchange so that it could trade into the Australian stock market. It has

been analyzed that the final statements of the company has not been prepared according to

the IASB and AASB compliances.

Extract of annual reports:

Annual report of the company has been analyzed to conduct a study over the financial

data presentation of Australian virgin limited. The following extracts have been evaluated

further for this study:

The final financial statement of the Australian vintage limited:

Has not been incorporated with entire IASB and AASB guidelines

Corporation act has not been considered by the accountant while preparing the statements

Historical cost concept as well s fair value accounting, both approaches have been considered

AUD currency sign has been used for the data in the annual reports

Some data has been misstated in the annual report of the company (Annual report, 2017)

8

Australasia Packaged, Cellar Door, UK/Europe, North America/ Australia Bulk & Processing

segments and wine grower segments. It provides wine under many brands such as Miranda,

McGuigan, Nepenthe, Passion Pop brands and Tempus Two. This company also possesses,

administers, and maintains wine grower and offers packaged and mass wines, at the same

time, it also offers concentrate over the winery processing services. This company sells its

manufacturing items through distributer, wholesaler and retailer channels, as well as it also

uses the regional outlets to sell its products (Bloomberg, 2017). This company is situated in

Balmain, Australia.

Income Statement:

Australian vintage limited is an organization that has a main goal of earning the

profits and enhances the growth of the company. Annual report of the company has been

analyzed and found that entire aspects of the company which has been shown into the annual

report of the company are not according to the IASB and AASB framework. Company has

used many aspects which are not ethical such as it somewhere company has used the

traditional method and somewhere modern approach has been used by the company

according to its benefits (Bezemer, 2010). A registration has been done by this company in

the Australian stock exchange so that it could trade into the Australian stock market. It has

been analyzed that the final statements of the company has not been prepared according to

the IASB and AASB compliances.

Extract of annual reports:

Annual report of the company has been analyzed to conduct a study over the financial

data presentation of Australian virgin limited. The following extracts have been evaluated

further for this study:

The final financial statement of the Australian vintage limited:

Has not been incorporated with entire IASB and AASB guidelines

Corporation act has not been considered by the accountant while preparing the statements

Historical cost concept as well s fair value accounting, both approaches have been considered

AUD currency sign has been used for the data in the annual reports

Some data has been misstated in the annual report of the company (Annual report, 2017)

Advance Accounting

9

International regulations of accounting have not been followed

Materiality, going concern and accrued accounting assumptions have been used.

Snap shot of annual reports:

The annual report evaluation of the company depict that there accountant of the

company has prepared and presented the financial data with a good understanding and

knowledge. Still, it has been analyzed that the mistakes which are of a little level that could

not make a huge impact over the reports and opinion of stakeholder of the company about the

operations, performance and profitability of the firm. It has been analyzed that company have

tried to use the entire guideline of conceptual framework while preparing and presenting the

final financial statements of the company (IASB, 2007).

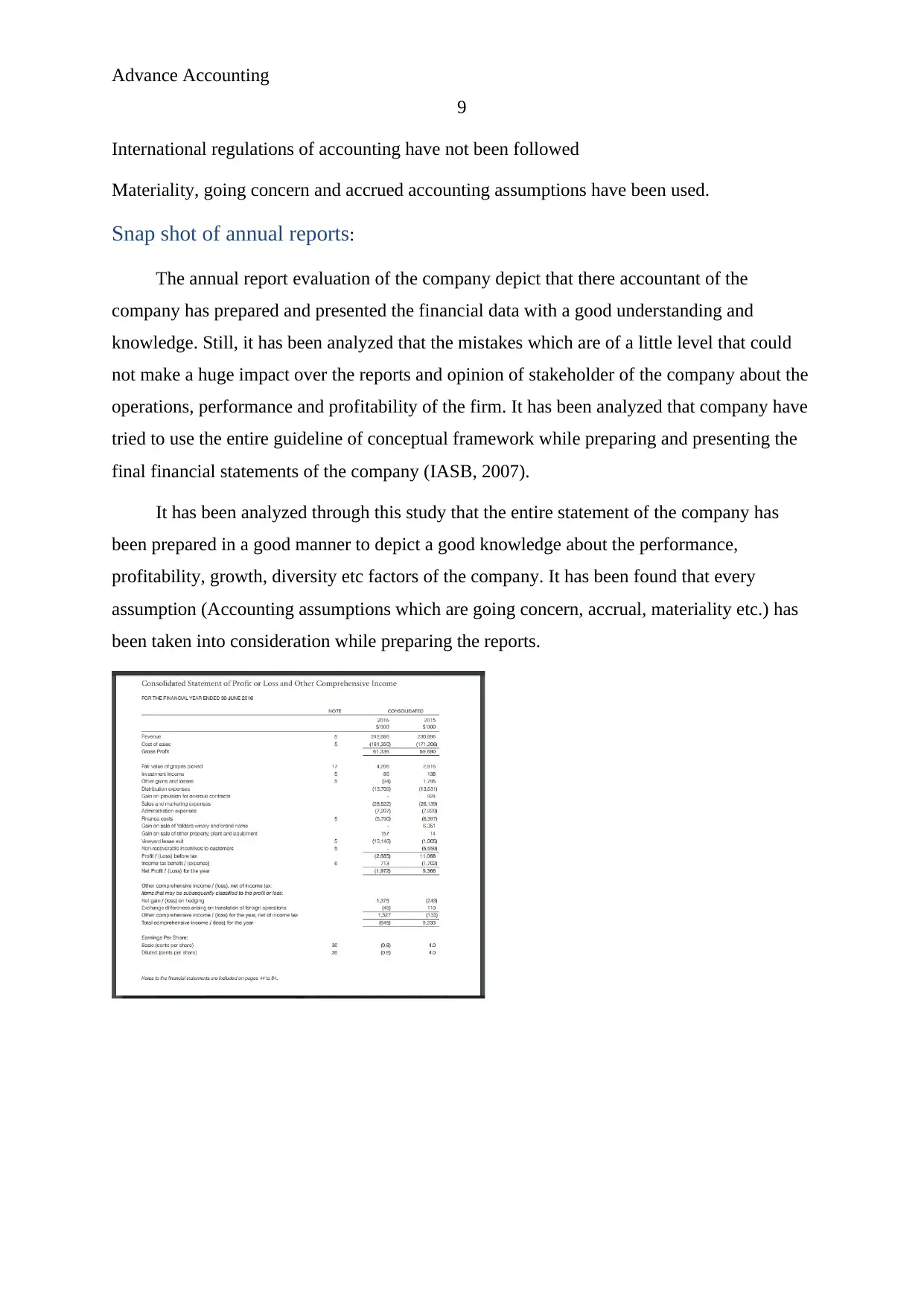

It has been analyzed through this study that the entire statement of the company has

been prepared in a good manner to depict a good knowledge about the performance,

profitability, growth, diversity etc factors of the company. It has been found that every

assumption (Accounting assumptions which are going concern, accrual, materiality etc.) has

been taken into consideration while preparing the reports.

9

International regulations of accounting have not been followed

Materiality, going concern and accrued accounting assumptions have been used.

Snap shot of annual reports:

The annual report evaluation of the company depict that there accountant of the

company has prepared and presented the financial data with a good understanding and

knowledge. Still, it has been analyzed that the mistakes which are of a little level that could

not make a huge impact over the reports and opinion of stakeholder of the company about the

operations, performance and profitability of the firm. It has been analyzed that company have

tried to use the entire guideline of conceptual framework while preparing and presenting the

final financial statements of the company (IASB, 2007).

It has been analyzed through this study that the entire statement of the company has

been prepared in a good manner to depict a good knowledge about the performance,

profitability, growth, diversity etc factors of the company. It has been found that every

assumption (Accounting assumptions which are going concern, accrual, materiality etc.) has

been taken into consideration while preparing the reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advance Accounting

10

(Annual Report, 2016)

Concept of prudence:

It is an accounting concept which signifies about the final statements presentation of a

firm. This concept describes about the final statements that it should record entire liabilities,

expenses and other factors of the firm at the time of occurring it or it also depict that if any

expectation for future expenses has taken place than the data must be recorded even before

taking that transaction a place (IASB Framework, 2001). While preparing and presenting

transactions with prudence concept consideration, it has been evaluated from the

professionals to not to overstate or understate the figures of the statements.

10

(Annual Report, 2016)

Concept of prudence:

It is an accounting concept which signifies about the final statements presentation of a

firm. This concept describes about the final statements that it should record entire liabilities,

expenses and other factors of the firm at the time of occurring it or it also depict that if any

expectation for future expenses has taken place than the data must be recorded even before

taking that transaction a place (IASB Framework, 2001). While preparing and presenting

transactions with prudence concept consideration, it has been evaluated from the

professionals to not to overstate or understate the figures of the statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advance Accounting

11

Through analyzing the annual report of Australian agriculture company Ltd, it has

been evaluated that the business is successively following the concept of conceptual

framework. Accountants of the company have prepared a good statement to depict a better

knowledge about the financial report of the company. Through analyzing the annual report of

Australia virgin limited, same outcome has been found (Chorafas, 2006). But at the same

time, it has been found that both the firms have made the changes in their annual reports

according to the prudence concept and it has also been mentioned that any exploitation have

not been made in the financial reports to influence the stakeholders.

Disclosure of differences:

It has been analyzed that both companies have prepared and presented the figures

according to AASB, IASB and IFRS concepts. Corporation act, 2001 has been followed by

both the companies to manage the figures (IFRS, 2008). The Australian agriculture company

limited has also considered the UK corporation act to manage the figures in the annual

reports of the company so that some difference could take place in disclosing the entire

figures because of different corporation act. This difference can also take place due to various

different functioning of both the companies (ACCA Global, 2017).

Segment reporting:

Segment reporting offers depth knowledge about the turnover, revenue and other

related aspect of the financial figures of the company. More the nature, business functioning

of both the companies may be classified through many aspects such as the companies where

they are diversifying their market, business functioning, their customers etc (Vollmer,

Mennicken and Preda, 2009). It has been analyzed that the products of both the companies

are different and thus the differences could take place in their annual reports (Jones, 2006).

Fixed assets:

It has been analyzed that both the firms have evaluated the fixed assets according to

the historical cost concept. The method of depreciation of both the companies is also same.

Still figures of the company have been presented in a different way in both the firms (ISAB

Framework, 2001).

Current assets:

11

Through analyzing the annual report of Australian agriculture company Ltd, it has

been evaluated that the business is successively following the concept of conceptual

framework. Accountants of the company have prepared a good statement to depict a better

knowledge about the financial report of the company. Through analyzing the annual report of

Australia virgin limited, same outcome has been found (Chorafas, 2006). But at the same

time, it has been found that both the firms have made the changes in their annual reports

according to the prudence concept and it has also been mentioned that any exploitation have

not been made in the financial reports to influence the stakeholders.

Disclosure of differences:

It has been analyzed that both companies have prepared and presented the figures

according to AASB, IASB and IFRS concepts. Corporation act, 2001 has been followed by

both the companies to manage the figures (IFRS, 2008). The Australian agriculture company

limited has also considered the UK corporation act to manage the figures in the annual

reports of the company so that some difference could take place in disclosing the entire

figures because of different corporation act. This difference can also take place due to various

different functioning of both the companies (ACCA Global, 2017).

Segment reporting:

Segment reporting offers depth knowledge about the turnover, revenue and other

related aspect of the financial figures of the company. More the nature, business functioning

of both the companies may be classified through many aspects such as the companies where

they are diversifying their market, business functioning, their customers etc (Vollmer,

Mennicken and Preda, 2009). It has been analyzed that the products of both the companies

are different and thus the differences could take place in their annual reports (Jones, 2006).

Fixed assets:

It has been analyzed that both the firms have evaluated the fixed assets according to

the historical cost concept. The method of depreciation of both the companies is also same.

Still figures of the company have been presented in a different way in both the firms (ISAB

Framework, 2001).

Current assets:

Advance Accounting

12

It has been analyzed that both the firms have evaluated the current assets according to

the going concern concept. The method of inventory management technique of both the

companies is also same.

Recommendation and conclusion:

Through this report, it has been analyzed that conceptual framework rules help the

company to manage the aspects related to final financial statement and assist them to prepare

the bets final statements and present them in a well manner. These frameworks have been set

by the IASB/AASB to make it quite easy for the stakeholders to make decision about the

performance and position of the company. Thus it is recommended to both the companies to

manage the framework and present the data accordingly. It is also suggested to the internal

and external stakeholder of the company to make some changes into the accounting policy to

make their final reports better.

Thus it could be concluded that both companies have prepared and presented the

figures according to AASB, IASB and IFRS concepts. Corporation act, 2001 has been

followed by both the companies to manage the figures. Some changes have taken place due to

different nature, business functioning, products, different diversified countries etc. It has also

been concluded that reliability, consistency, compliance, relevancy, comparability etc

enhances due to conceptual framework.

12

It has been analyzed that both the firms have evaluated the current assets according to

the going concern concept. The method of inventory management technique of both the

companies is also same.

Recommendation and conclusion:

Through this report, it has been analyzed that conceptual framework rules help the

company to manage the aspects related to final financial statement and assist them to prepare

the bets final statements and present them in a well manner. These frameworks have been set

by the IASB/AASB to make it quite easy for the stakeholders to make decision about the

performance and position of the company. Thus it is recommended to both the companies to

manage the framework and present the data accordingly. It is also suggested to the internal

and external stakeholder of the company to make some changes into the accounting policy to

make their final reports better.

Thus it could be concluded that both companies have prepared and presented the

figures according to AASB, IASB and IFRS concepts. Corporation act, 2001 has been

followed by both the companies to manage the figures. Some changes have taken place due to

different nature, business functioning, products, different diversified countries etc. It has also

been concluded that reliability, consistency, compliance, relevancy, comparability etc

enhances due to conceptual framework.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.