ACC301: Analysis of the IASB's Revised Conceptual Framework Report

VerifiedAdded on 2022/11/13

|7

|512

|438

Report

AI Summary

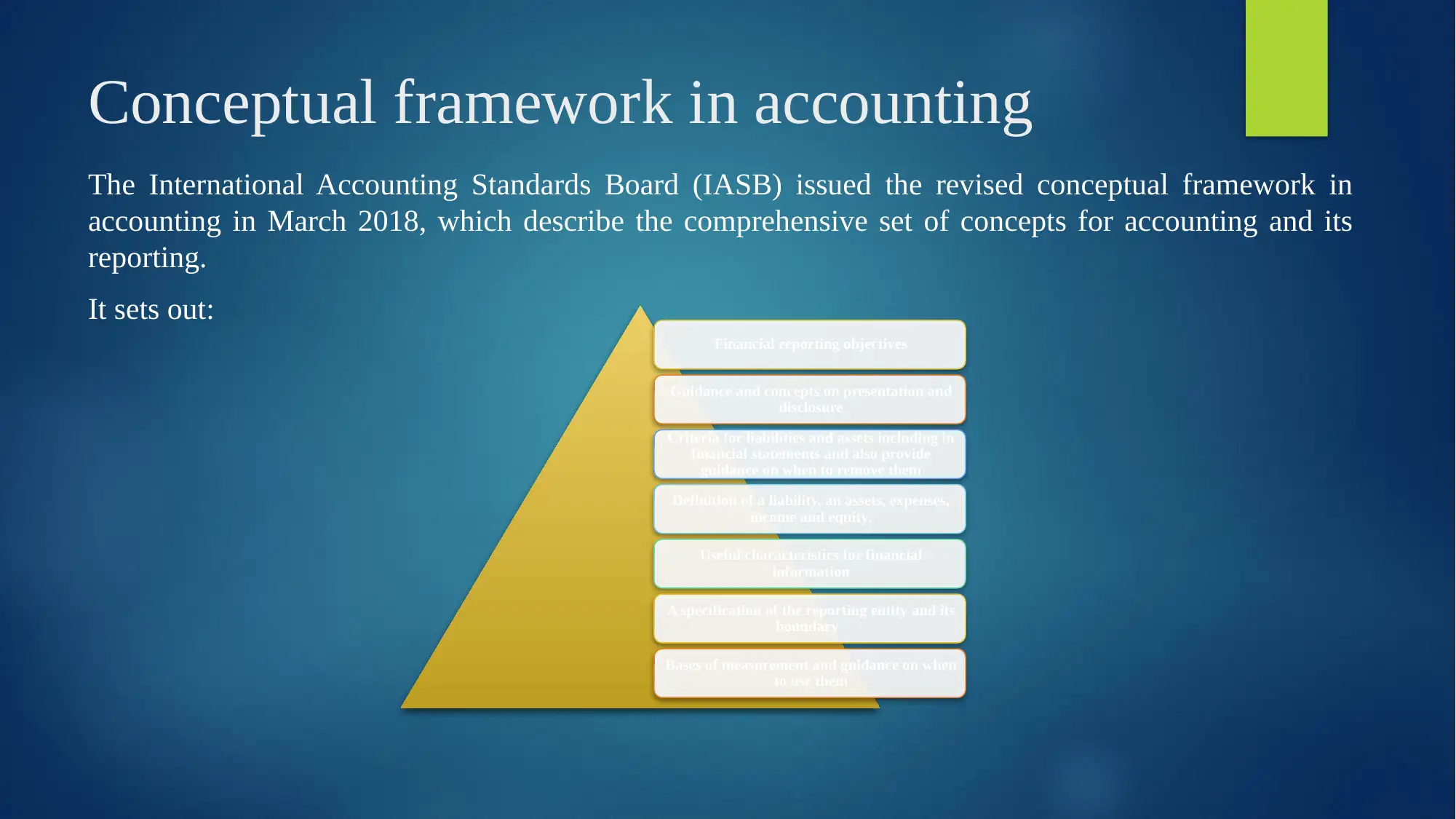

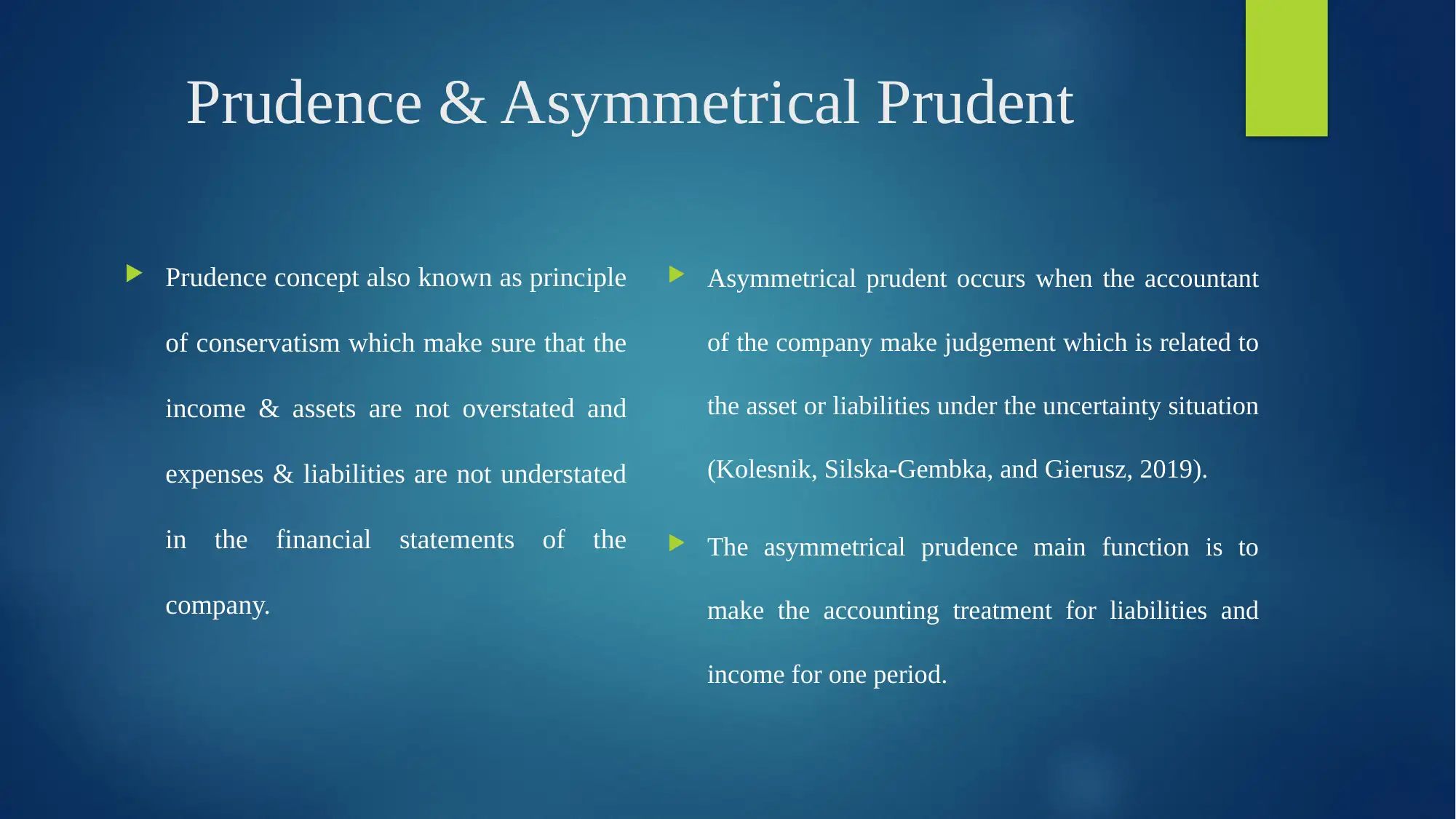

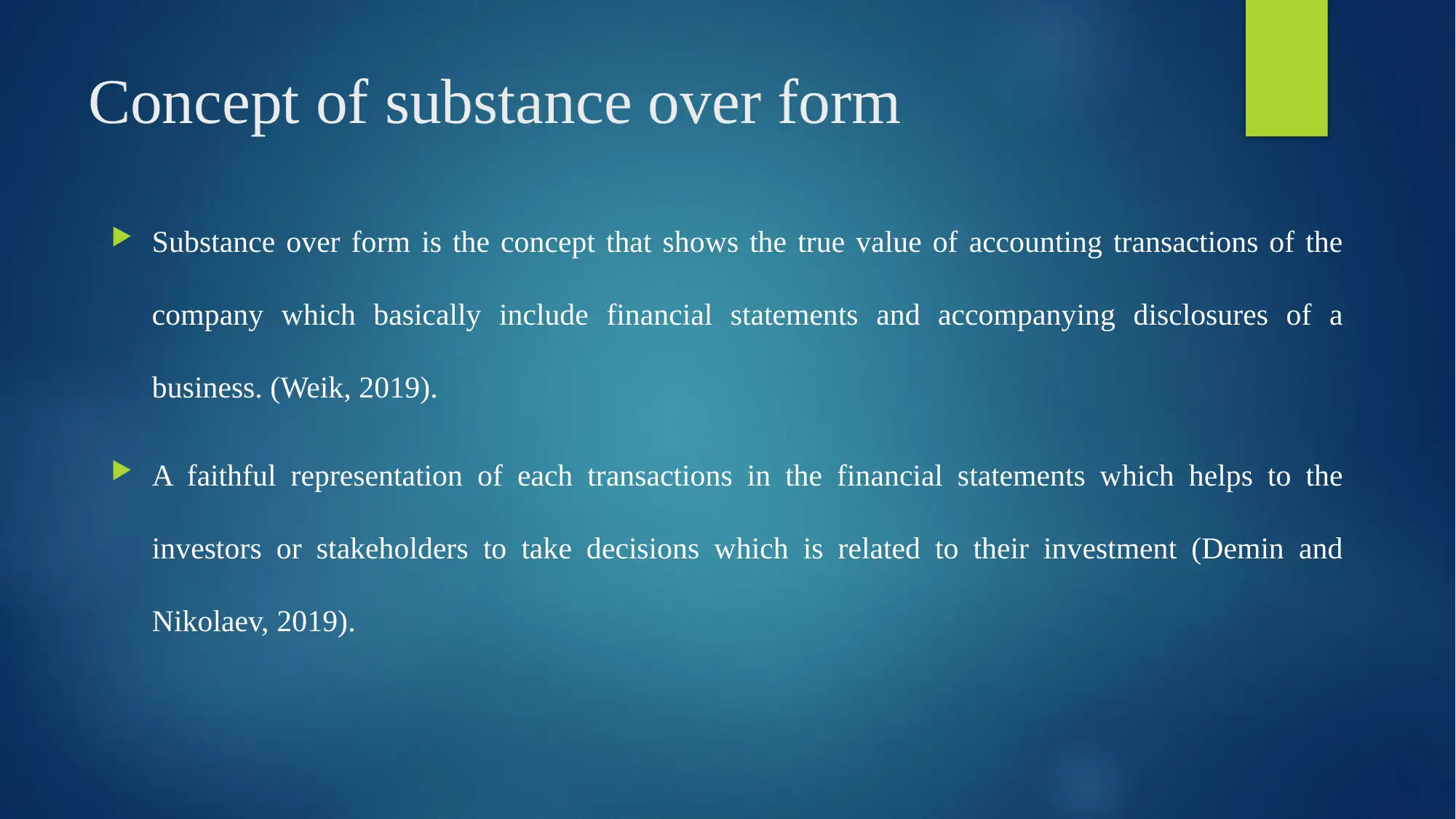

This report analyzes the revised conceptual framework for financial reporting, focusing on the key concepts introduced by the International Accounting Standards Board (IASB). The report begins with an overview of the conceptual framework, followed by an examination of the objective of general-purpose financial reporting, emphasizing its importance to stakeholders. It then explores the concepts of prudence and asymmetrical prudence, highlighting their role in ensuring that financial statements are not misleading. Finally, the report discusses the concept of substance over form and its significance in accurately representing accounting transactions. The report is supported by relevant references to academic literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.