ACCT20074: Conceptual Framework and Integrated Reporting

VerifiedAdded on 2023/01/10

|19

|5298

|97

Report

AI Summary

This report provides a comprehensive analysis of the conceptual framework and integrated reporting, crucial components of contemporary accounting theory. The report begins by exploring the history, benefits, and limitations of the conceptual framework, with a specific focus on its adoption in the USA, UK, and Australia. It then delves into the concerns of the Australian accounting profession regarding the application of the IASB/IFRS framework. The report evaluates the annual report of Wesfarmers, assessing its compliance with the conceptual framework's qualitative principles, including financial statement components, recognition and measurement principles, and qualitative characteristics. Furthermore, the report examines the differences between the Global Reporting Initiative (GRI) and integrated reporting frameworks, including the theories used in developing sustainability reports. It compares the reporting practices of RCL Foods Limited (South Africa) and Wesfarmers Limited (Australia), evaluating their application of integrated reporting components. The report concludes by summarizing the key findings and implications of the analysis, offering valuable insights into the evolving landscape of corporate external reporting practices.

ACCT20074

Contemporary Accounting Theory

Term 1 Assessment 3

1

Contemporary Accounting Theory

Term 1 Assessment 3

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has been developed into two separate sections. The first section has explained

the usefulness, history, benefits and limitations of conceptual accounting framework. This

applicability of CF in developing the financial reports has been explained in reference to the

ASX listed entity of Wesfarmers. It has been identified through analysis of the annual report of

Wesfarmers that it has complied with all the qualitative principle provided by the conceptual

accounting framework in development of its annual reports. The next section has discussed the

difference between GRI and integrated reporting systems and the different theories used in

developing the contents of sustainable reports. The different criterion of integrated reporting

system and its difference with the sustainability reports has been explained by presenting the

comparison between a selected South African, that is, RCL Foods Limited and ASX listed entity,

that is Wesfarmers limited. It has been identified that RCL Food Limited has applied integrated

reporting framework to disclose both financial and non-financial data. On the other hand,

Wesfarmers has also complied with the essential criterion of integrated reporting framework in

providing information about its financial as well as sustainability matters.

2

This report has been developed into two separate sections. The first section has explained

the usefulness, history, benefits and limitations of conceptual accounting framework. This

applicability of CF in developing the financial reports has been explained in reference to the

ASX listed entity of Wesfarmers. It has been identified through analysis of the annual report of

Wesfarmers that it has complied with all the qualitative principle provided by the conceptual

accounting framework in development of its annual reports. The next section has discussed the

difference between GRI and integrated reporting systems and the different theories used in

developing the contents of sustainable reports. The different criterion of integrated reporting

system and its difference with the sustainability reports has been explained by presenting the

comparison between a selected South African, that is, RCL Foods Limited and ASX listed entity,

that is Wesfarmers limited. It has been identified that RCL Food Limited has applied integrated

reporting framework to disclose both financial and non-financial data. On the other hand,

Wesfarmers has also complied with the essential criterion of integrated reporting framework in

providing information about its financial as well as sustainability matters.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A: Conceptual Framework.......................................................................................................4

(a): History of Conceptual Framework (CF) Adoption in the USA, UK and Australia..............4

(b): Australian Accounting Profession Concerns Regarding the Application of the IASB/IFRS

CF for Financial Reporting..........................................................................................................5

(c): Potential Benefits and Limitations of conceptual framework for financial reporting...........5

(d): Evaluation of Annual report of Wesfarmers using Conceptual Framework.........................6

Subpart (i): Number of financial statements and their components............................................6

Subpart (ii): Principles of recognition and measurement basis used for asset, revenue and

liabilities.......................................................................................................................................7

Subpart (iii): Qualitative characteristics of Wesfarmers’s financial information presented in

financial information:...................................................................................................................7

Part B: Integrated Reporting..........................................................................................................11

(a): Comparison of Global Reporting Initiative (GRI) and International Integrated Reporting

Framework for Social Responsibility Reporting.......................................................................11

(b): Rigor of Conventional Accounting Approaches for Explaining the Contents of

Sustainability..............................................................................................................................11

(c): Usefulness and Limitations of Theories for Explaining the Contents of Sustainability

Reports.......................................................................................................................................12

(d): Evaluation of application of integrated reporting components by selected South African

Company (RCL Foods Limited)................................................................................................12

(e): Comparison table showing the difference in reporting practice of the selected Australian

Company with the index of components of IIRC as used by South African Company............15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A: Conceptual Framework.......................................................................................................4

(a): History of Conceptual Framework (CF) Adoption in the USA, UK and Australia..............4

(b): Australian Accounting Profession Concerns Regarding the Application of the IASB/IFRS

CF for Financial Reporting..........................................................................................................5

(c): Potential Benefits and Limitations of conceptual framework for financial reporting...........5

(d): Evaluation of Annual report of Wesfarmers using Conceptual Framework.........................6

Subpart (i): Number of financial statements and their components............................................6

Subpart (ii): Principles of recognition and measurement basis used for asset, revenue and

liabilities.......................................................................................................................................7

Subpart (iii): Qualitative characteristics of Wesfarmers’s financial information presented in

financial information:...................................................................................................................7

Part B: Integrated Reporting..........................................................................................................11

(a): Comparison of Global Reporting Initiative (GRI) and International Integrated Reporting

Framework for Social Responsibility Reporting.......................................................................11

(b): Rigor of Conventional Accounting Approaches for Explaining the Contents of

Sustainability..............................................................................................................................11

(c): Usefulness and Limitations of Theories for Explaining the Contents of Sustainability

Reports.......................................................................................................................................12

(d): Evaluation of application of integrated reporting components by selected South African

Company (RCL Foods Limited)................................................................................................12

(e): Comparison table showing the difference in reporting practice of the selected Australian

Company with the index of components of IIRC as used by South African Company............15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report has been developed for providing an analysis of the framework and policies

that are used by businesses all over the world to develop and present their financial as well as

non-financial information. In this context, there has been discussion in relation to the

applicability of the conceptual framework provided by the IASB to develop the financial reports.

This is carried out by stating the history, strengths, limitations and its application in developing

the financial statements in reference to an ASX listed entity. The next section of the report

relates to explaining the manner in which businesses are disclosing their sustainability reports.

This has been conducted by explaining the sustainability frameworks such as Global Reporting

Initiative (GRI) and integrated reporting systems. The limitations of conventional accounting

approaches, relevant theories for developing the content of sustainability reports and criteria used

in developing integrated reports are discussed in this section with comparing it to the

sustainability reports criterion used by ASX listed entity.

Part A: Conceptual Framework

(a): History of Conceptual Framework (CF) Adoption in the USA, UK and Australia

The conceptual framework (CF) is regarded as a theory of accounting that provides a

reference frame to be used for developing the financial reports on the basis of certain qualified

qualitative principles. The IASB (International Accounting Standards Board) has provided the

CF for improving quality in the financial reporting process. It has been followed and

implemented by different countries to enhance the quality of financial reports and attaining the

goal of converging accounting standards of IASB (Dean and Clarke, 2003). The developed

countries such as the UK, Australia and the US are adopting and implementing the CF to

improve the international comparability of their financial reports. The Accounting Principles

Board (APB) in the US has been developed in the year 1965 for stating the accounting principles

and policies to be followed for developing and producing the financial reports (Macías and

Muiño, 2011). This has lead to the development of a Trueblood Committee in the year 1971 that

has provided the objectives and principles to be used for disclosing the financial information to

the users. These objectives and principles were criticized on the basis of providing limited

information to the users. As such, there has been replacement of APB by FASB and this lead to

the adoption of the CF project. The FASB is working in co-ordination with IASB for developing

a revised CF (Seng, 2014). The development of the CF in the UK can be linked with the presence

of issues related with inconsistencies in the financial reporting system related with recognition

and measurement of different financial items (Barth, 2008). The ASB has adopted the IASC

framework in the year 1991 for improving consistency within the financial reporting system. The

issues related with measurement inconsistencies in Australia has lead to the adoption of the CF

after the decisions taken by the Financial Reporting Council in the year 2005 (Chua, Chee and

Cheong, 2012).

4

This report has been developed for providing an analysis of the framework and policies

that are used by businesses all over the world to develop and present their financial as well as

non-financial information. In this context, there has been discussion in relation to the

applicability of the conceptual framework provided by the IASB to develop the financial reports.

This is carried out by stating the history, strengths, limitations and its application in developing

the financial statements in reference to an ASX listed entity. The next section of the report

relates to explaining the manner in which businesses are disclosing their sustainability reports.

This has been conducted by explaining the sustainability frameworks such as Global Reporting

Initiative (GRI) and integrated reporting systems. The limitations of conventional accounting

approaches, relevant theories for developing the content of sustainability reports and criteria used

in developing integrated reports are discussed in this section with comparing it to the

sustainability reports criterion used by ASX listed entity.

Part A: Conceptual Framework

(a): History of Conceptual Framework (CF) Adoption in the USA, UK and Australia

The conceptual framework (CF) is regarded as a theory of accounting that provides a

reference frame to be used for developing the financial reports on the basis of certain qualified

qualitative principles. The IASB (International Accounting Standards Board) has provided the

CF for improving quality in the financial reporting process. It has been followed and

implemented by different countries to enhance the quality of financial reports and attaining the

goal of converging accounting standards of IASB (Dean and Clarke, 2003). The developed

countries such as the UK, Australia and the US are adopting and implementing the CF to

improve the international comparability of their financial reports. The Accounting Principles

Board (APB) in the US has been developed in the year 1965 for stating the accounting principles

and policies to be followed for developing and producing the financial reports (Macías and

Muiño, 2011). This has lead to the development of a Trueblood Committee in the year 1971 that

has provided the objectives and principles to be used for disclosing the financial information to

the users. These objectives and principles were criticized on the basis of providing limited

information to the users. As such, there has been replacement of APB by FASB and this lead to

the adoption of the CF project. The FASB is working in co-ordination with IASB for developing

a revised CF (Seng, 2014). The development of the CF in the UK can be linked with the presence

of issues related with inconsistencies in the financial reporting system related with recognition

and measurement of different financial items (Barth, 2008). The ASB has adopted the IASC

framework in the year 1991 for improving consistency within the financial reporting system. The

issues related with measurement inconsistencies in Australia has lead to the adoption of the CF

after the decisions taken by the Financial Reporting Council in the year 2005 (Chua, Chee and

Cheong, 2012).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b): Australian Accounting Profession Concerns Regarding the Application of the

IASB/IFRS CF for Financial Reporting

The major issues that the Australian accounting professional bodies such as Certified

Public Accountants (CPAs) have identified relates to the complexity in the financial statements

that have been incurred with the IFRS adoption. The financial reporting system of Australia has

become too complex with the adoption of IFRS reporting standards. This issue was also

highlighted by the Australian Financial Reporting Council which has stated that the compliance

with the different IFRS standards have resulted in causing complexities in the regulatory

framework (Financial Reporting Council, 2019). This has increased the time required in

developing the financial reports and also caused complications before the financial managers in

developing and recording the financial transactions as per the new standards. It has been stated

by CPA accounting body in this context that the adoption of IFRS is not useful for small and

medium sized business entities in Australia (Wong, 2004). This is because it would incur higher

costs and complexities for them in comparison to the benefits obtained and therefore it is quite

challenging for them to comply with different IFRS requirements. It has been recommended by

the CPA that it is necessary for AASB (Australian Accounting Standards Board) to undertake the

cost-benefits analysis before making final decision for the IFRS adoption. The CPA’s has also

presented the challenge of complying with the Corporations Act 2001 in addition with

complying with IFRS requirements (Gregor, 2012).

(c): Potential Benefits and Limitations of conceptual framework for financial reporting

Financial reporting following conceptual framework has some defined benefits which are

as follows:

Financial reporting using conceptual framework seems to be a standard framework

which enhances stakeholders trust on the financial information provided in the report

by the company. Conceptual framework allows discussion on accounting problems. It

supports better regulation by guiding standard makers (Silvia, 2016).

Basic accounting practices can be tested by following conceptual framework for

financial reporting.

Increase reliability on financial statements.

Strong communication is possible between the finance team and standard makers.

Conceptual framework offers all reasonable and objective aspect to be presented in

financial reporting (Pacter, 2013).

It helps in choosing the best accounting practices and methods to comply with

accounting standards.

Despite of so many benefits in following conceptual framework for financial reporting

some limitation are also exist.

5

IASB/IFRS CF for Financial Reporting

The major issues that the Australian accounting professional bodies such as Certified

Public Accountants (CPAs) have identified relates to the complexity in the financial statements

that have been incurred with the IFRS adoption. The financial reporting system of Australia has

become too complex with the adoption of IFRS reporting standards. This issue was also

highlighted by the Australian Financial Reporting Council which has stated that the compliance

with the different IFRS standards have resulted in causing complexities in the regulatory

framework (Financial Reporting Council, 2019). This has increased the time required in

developing the financial reports and also caused complications before the financial managers in

developing and recording the financial transactions as per the new standards. It has been stated

by CPA accounting body in this context that the adoption of IFRS is not useful for small and

medium sized business entities in Australia (Wong, 2004). This is because it would incur higher

costs and complexities for them in comparison to the benefits obtained and therefore it is quite

challenging for them to comply with different IFRS requirements. It has been recommended by

the CPA that it is necessary for AASB (Australian Accounting Standards Board) to undertake the

cost-benefits analysis before making final decision for the IFRS adoption. The CPA’s has also

presented the challenge of complying with the Corporations Act 2001 in addition with

complying with IFRS requirements (Gregor, 2012).

(c): Potential Benefits and Limitations of conceptual framework for financial reporting

Financial reporting following conceptual framework has some defined benefits which are

as follows:

Financial reporting using conceptual framework seems to be a standard framework

which enhances stakeholders trust on the financial information provided in the report

by the company. Conceptual framework allows discussion on accounting problems. It

supports better regulation by guiding standard makers (Silvia, 2016).

Basic accounting practices can be tested by following conceptual framework for

financial reporting.

Increase reliability on financial statements.

Strong communication is possible between the finance team and standard makers.

Conceptual framework offers all reasonable and objective aspect to be presented in

financial reporting (Pacter, 2013).

It helps in choosing the best accounting practices and methods to comply with

accounting standards.

Despite of so many benefits in following conceptual framework for financial reporting

some limitation are also exist.

5

Developed countries set their own conceptual framework and use it in financial

reporting. Developing countries find it very time consuming and costly to set up the

conceptual framework

Conceptual framework is very inflexible and it does not appreciate any new ideas in

it. Because of this limitation conceptual framework does not give that much direction

in accounting as needed (Tschopp and Nastanski, 2014).

Following conceptual framework for financial report creates conflict with accounting

standard. The reason of conflict is many companies are following accounting standard

in reporting

It makes it hard to compare entities financial information presented in report

following conceptual framework with other company following accounting standard

(Fajard, 2016).

(d): Evaluation of Annual report of Wesfarmers using Conceptual Framework

Subpart (i): Number of financial statements and their components

Every company should comply with the principles and guidelines provided in compliance

framework. Annual report of Wesfarmer has been evaluated in this part to check whether

company has complied with it successfully or not. There are four types of reports or financial

statements that a company must prepare according to compliance framework. Wesfarmers has

prepared these following statements (Conceptual Framework, 2018).

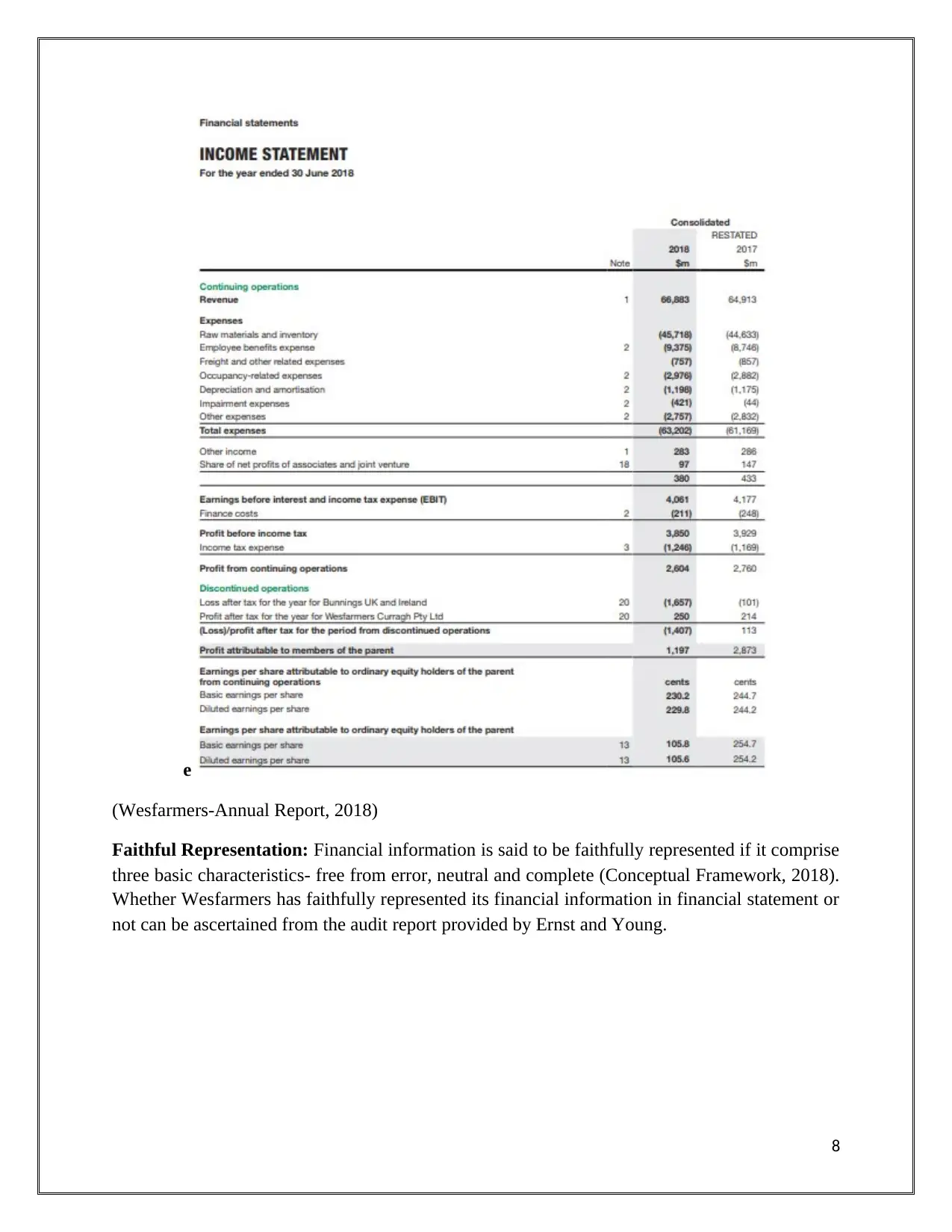

Income Statement: Income statement is a vital part to report on company’s financial

performance. It mainly focuses on four key financial items- revenue, expenses, profits

and losses. Annual report of Wesfarmer reveals that it has prepared consolidated

income statement with the restated figures for the year 2017 to show company’s

financial performance.

Balance sheet: Balance sheet of a company can be said a snapshot of the company

that discloses what a company own and what it owes as well as investments of

shareholders at a specified point of time. Wesfarmers has prepared consolidated

balance sheet reporting on company’s assets, liabilities and equity to calculate rate of

return and reflect capital structure.

Statement of changes in Equity: Statement of changes in equity reflects changes in

company’s equity between the beginning and end of the reporting period. The

changes arise from the transactions by and with the owners in the capacity of owner.

Wesfarmers has prepared consolidated statement of changes in equity (Wesfarmers-

Annual Report, 2018).

Cash flow statement: This financial statement shows the cash position of the

company. It reflects the changes occur in balance sheet and income statement due to

cash and cash equivalent received and paid during the year. Wesfarmers has prepared

consolidated cash flow statement to show its cash position. This statement has been

6

reporting. Developing countries find it very time consuming and costly to set up the

conceptual framework

Conceptual framework is very inflexible and it does not appreciate any new ideas in

it. Because of this limitation conceptual framework does not give that much direction

in accounting as needed (Tschopp and Nastanski, 2014).

Following conceptual framework for financial report creates conflict with accounting

standard. The reason of conflict is many companies are following accounting standard

in reporting

It makes it hard to compare entities financial information presented in report

following conceptual framework with other company following accounting standard

(Fajard, 2016).

(d): Evaluation of Annual report of Wesfarmers using Conceptual Framework

Subpart (i): Number of financial statements and their components

Every company should comply with the principles and guidelines provided in compliance

framework. Annual report of Wesfarmer has been evaluated in this part to check whether

company has complied with it successfully or not. There are four types of reports or financial

statements that a company must prepare according to compliance framework. Wesfarmers has

prepared these following statements (Conceptual Framework, 2018).

Income Statement: Income statement is a vital part to report on company’s financial

performance. It mainly focuses on four key financial items- revenue, expenses, profits

and losses. Annual report of Wesfarmer reveals that it has prepared consolidated

income statement with the restated figures for the year 2017 to show company’s

financial performance.

Balance sheet: Balance sheet of a company can be said a snapshot of the company

that discloses what a company own and what it owes as well as investments of

shareholders at a specified point of time. Wesfarmers has prepared consolidated

balance sheet reporting on company’s assets, liabilities and equity to calculate rate of

return and reflect capital structure.

Statement of changes in Equity: Statement of changes in equity reflects changes in

company’s equity between the beginning and end of the reporting period. The

changes arise from the transactions by and with the owners in the capacity of owner.

Wesfarmers has prepared consolidated statement of changes in equity (Wesfarmers-

Annual Report, 2018).

Cash flow statement: This financial statement shows the cash position of the

company. It reflects the changes occur in balance sheet and income statement due to

cash and cash equivalent received and paid during the year. Wesfarmers has prepared

consolidated cash flow statement to show its cash position. This statement has been

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

categorized in three parts- Operating activities, financing activities and investing

activities.

Wesfarmers has provided supporting information notes to accounts with its financial

statement to comply with the regulatory requirement for better understanding of financial items

in financial statements for the stakeholders. Notes to accounts reflect company’s assumption,

accounting methods used in preparation of financial statements (Wesfarmers-Annual Report,

2018).

Subpart (ii): Principles of recognition and measurement basis used for asset, revenue and

liabilities

Revenue: Wesfarmers generates majority of its revenue from the supermarkets and

grocery stores in Australia. Company has measured it revenue at the fair value of the

consideration received or receivable. Wesfarmers has followed IFRS 15 for

accounting for recognition its revenue.

Assets: Wesfarmers has classified its assets into current assets and non-current assets.

Cash and short term deposit comprise cash in hand and at bank and short term

deposits. Trade receivable, loans and advances, debtors and short term deposit with

the maturity of three months or less recognized at amortized cost. Inventories are

valued at cost or net realizable value whichever is less. Property, plant and equipment

have carried at asset’s cost less accumulated depreciation and impairment. Goodwill

and intangible assets have been initially measured at cost (Conceptual Framework,

2018).

Liabilities: Wesfarmers has made provision for employee benefits that represents

accrued annual leaves, long service leave entitlements and incentives. Liabilities for

wages and salaries are recognized at the amounts that should be paid at the time of

settlement. Lease provision has been made to cover stepped lease to recognize the

lease expenses on straight line basis over lease term (Conceptual Framework, 2018).

Subpart (iii): Qualitative characteristics of Wesfarmers’s financial information presented

in financial information:

Relevance: Financial information can be said relevant if it can change the decision of users on

financial statements (Conceptual Framework, 2018). This can be happen only when the financial

information has predictive value and confirmatory value. Investors should be able to predict and

confirm the value of financial information to analyze present and future performance of the

company. Earnings per share can be taken to assess whether this information has relevance

characteristic to evaluate the performance of Wesfarmers (Wesfarmers-Annual Report, 2018).

7

activities.

Wesfarmers has provided supporting information notes to accounts with its financial

statement to comply with the regulatory requirement for better understanding of financial items

in financial statements for the stakeholders. Notes to accounts reflect company’s assumption,

accounting methods used in preparation of financial statements (Wesfarmers-Annual Report,

2018).

Subpart (ii): Principles of recognition and measurement basis used for asset, revenue and

liabilities

Revenue: Wesfarmers generates majority of its revenue from the supermarkets and

grocery stores in Australia. Company has measured it revenue at the fair value of the

consideration received or receivable. Wesfarmers has followed IFRS 15 for

accounting for recognition its revenue.

Assets: Wesfarmers has classified its assets into current assets and non-current assets.

Cash and short term deposit comprise cash in hand and at bank and short term

deposits. Trade receivable, loans and advances, debtors and short term deposit with

the maturity of three months or less recognized at amortized cost. Inventories are

valued at cost or net realizable value whichever is less. Property, plant and equipment

have carried at asset’s cost less accumulated depreciation and impairment. Goodwill

and intangible assets have been initially measured at cost (Conceptual Framework,

2018).

Liabilities: Wesfarmers has made provision for employee benefits that represents

accrued annual leaves, long service leave entitlements and incentives. Liabilities for

wages and salaries are recognized at the amounts that should be paid at the time of

settlement. Lease provision has been made to cover stepped lease to recognize the

lease expenses on straight line basis over lease term (Conceptual Framework, 2018).

Subpart (iii): Qualitative characteristics of Wesfarmers’s financial information presented

in financial information:

Relevance: Financial information can be said relevant if it can change the decision of users on

financial statements (Conceptual Framework, 2018). This can be happen only when the financial

information has predictive value and confirmatory value. Investors should be able to predict and

confirm the value of financial information to analyze present and future performance of the

company. Earnings per share can be taken to assess whether this information has relevance

characteristic to evaluate the performance of Wesfarmers (Wesfarmers-Annual Report, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e

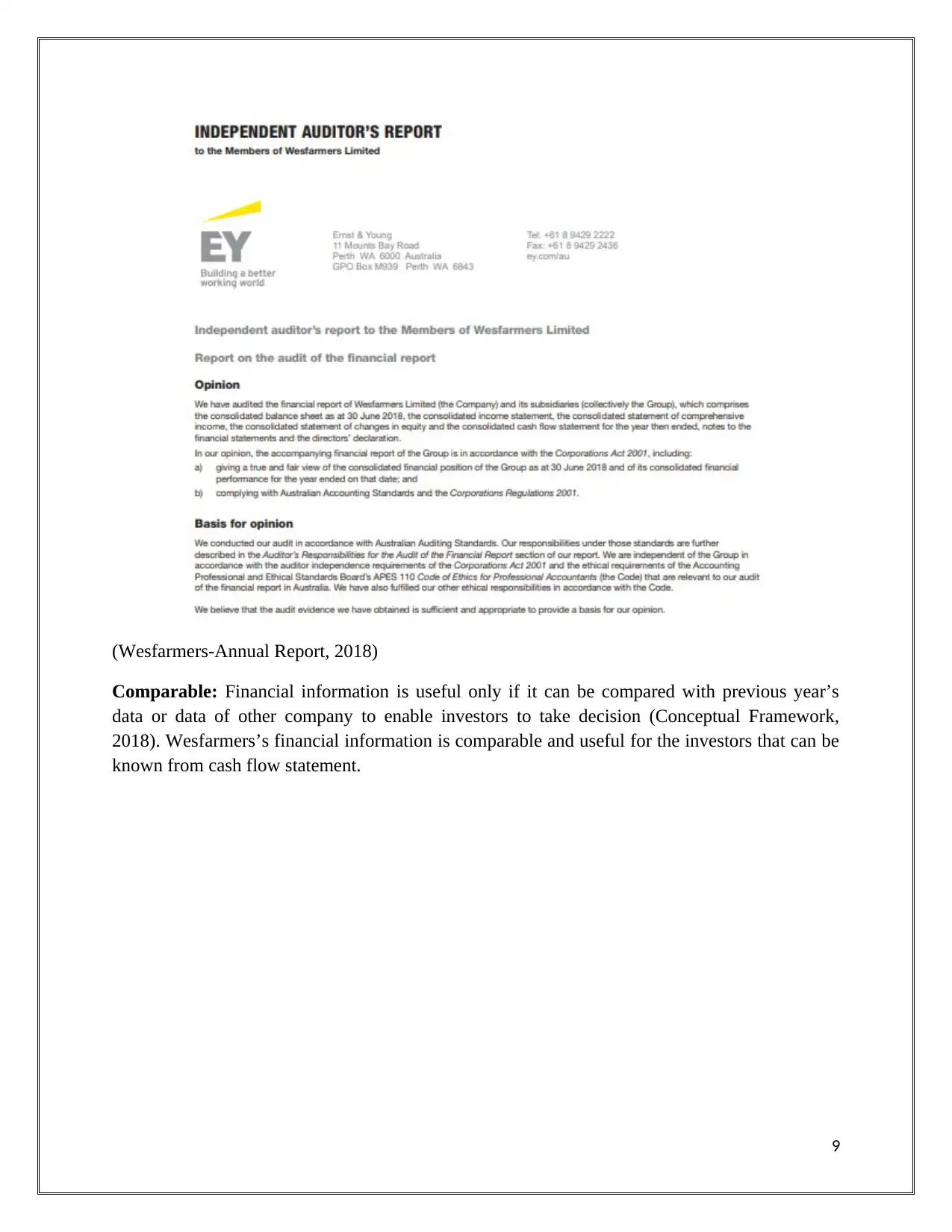

(Wesfarmers-Annual Report, 2018)

Faithful Representation: Financial information is said to be faithfully represented if it comprise

three basic characteristics- free from error, neutral and complete (Conceptual Framework, 2018).

Whether Wesfarmers has faithfully represented its financial information in financial statement or

not can be ascertained from the audit report provided by Ernst and Young.

8

(Wesfarmers-Annual Report, 2018)

Faithful Representation: Financial information is said to be faithfully represented if it comprise

three basic characteristics- free from error, neutral and complete (Conceptual Framework, 2018).

Whether Wesfarmers has faithfully represented its financial information in financial statement or

not can be ascertained from the audit report provided by Ernst and Young.

8

(Wesfarmers-Annual Report, 2018)

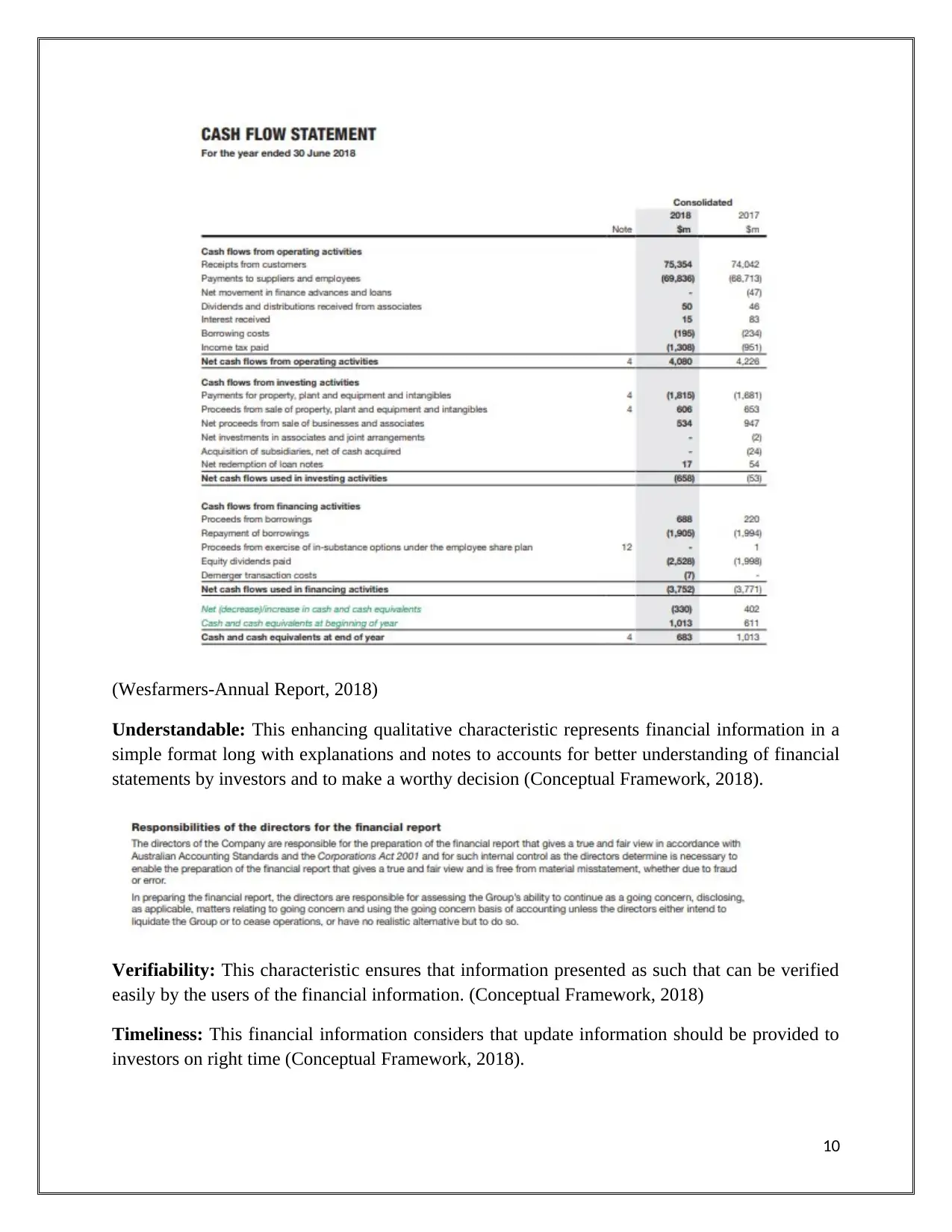

Comparable: Financial information is useful only if it can be compared with previous year’s

data or data of other company to enable investors to take decision (Conceptual Framework,

2018). Wesfarmers’s financial information is comparable and useful for the investors that can be

known from cash flow statement.

9

Comparable: Financial information is useful only if it can be compared with previous year’s

data or data of other company to enable investors to take decision (Conceptual Framework,

2018). Wesfarmers’s financial information is comparable and useful for the investors that can be

known from cash flow statement.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Wesfarmers-Annual Report, 2018)

Understandable: This enhancing qualitative characteristic represents financial information in a

simple format long with explanations and notes to accounts for better understanding of financial

statements by investors and to make a worthy decision (Conceptual Framework, 2018).

Verifiability: This characteristic ensures that information presented as such that can be verified

easily by the users of the financial information. (Conceptual Framework, 2018)

Timeliness: This financial information considers that update information should be provided to

investors on right time (Conceptual Framework, 2018).

10

Understandable: This enhancing qualitative characteristic represents financial information in a

simple format long with explanations and notes to accounts for better understanding of financial

statements by investors and to make a worthy decision (Conceptual Framework, 2018).

Verifiability: This characteristic ensures that information presented as such that can be verified

easily by the users of the financial information. (Conceptual Framework, 2018)

Timeliness: This financial information considers that update information should be provided to

investors on right time (Conceptual Framework, 2018).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B: Integrated Reporting

(a): Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting

The Global Reporting Imitative supports the sustainability report for organizations to

make them sustainable and contribute to create a sustainable global economy. GRI’s aim is to

make it a standard practice. In current scenario Investors are eager to know financial as well as

non-financial information of company such as social, economic, environmental and governance

performance. GRI makes it understand and communicate to business and government effect of

their activities on climate change, society, economy on a large scale. Global Reporting Initiative

sustainability reporting has been developed by the contribution of multi-stakeholders. GRI aims

to make it globally acceptable as standard format for sustainability reporting. The practice of

disclosing sustainability information take a step forward to grasp new opportunities for entities,

manage risk and help an organization in becoming accountable. Reporting sustainability

information along with financial statement helps the companies to protect environment, create a

better standard for society, improved governance (GRI, 2017).

Reporting non-financial information with financial information is known as integrated

reporting to help investors to make worthy decision. Stakeholders consider companies activities

towards welfare of society, protection of environment and many non-financial information

before investing in any entity (The IIRC, 2017). This type of sustainability reporting format is

provided by the International Integrated Reporting Council (IIRC). GRI framework supports

integrate reporting as it put attention to take integrated approach rather than following only

traditional approach. Integrated reporting mandates entity to give demo of application of its long

term strategy by keeping in mind all the integrated risk and opportunities (The IIRC, 2017).

(b): Rigor of Conventional Accounting Approaches for Explaining the Contents of

Sustainability

The conventional accounting approaches that is Conceptual Framework (CF) for financial

reporting though is able to provide effective guidance for development and presentation of

financial statements has not proved to be of any usefulness in reporting of environmental and

social performance. The major limitations that are associated with the use of approach in

presentation of non-financial data related to social and environmental performance can be stated

as follows:

Limitation of Conceptual Framework (CF) Objective: The CF has provided that

objective of financial reporting is to facilitate the investment decisions of users mainly

investors, creditors and lenders. However, it has not placed any emphasis on meeting the

requirements of its wider stakeholder groups such as environment and community

members. It only intends to provide financial information and not included any

consideration related to presentation of non-financial information (Ivan, 2009).

11

(a): Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting

The Global Reporting Imitative supports the sustainability report for organizations to

make them sustainable and contribute to create a sustainable global economy. GRI’s aim is to

make it a standard practice. In current scenario Investors are eager to know financial as well as

non-financial information of company such as social, economic, environmental and governance

performance. GRI makes it understand and communicate to business and government effect of

their activities on climate change, society, economy on a large scale. Global Reporting Initiative

sustainability reporting has been developed by the contribution of multi-stakeholders. GRI aims

to make it globally acceptable as standard format for sustainability reporting. The practice of

disclosing sustainability information take a step forward to grasp new opportunities for entities,

manage risk and help an organization in becoming accountable. Reporting sustainability

information along with financial statement helps the companies to protect environment, create a

better standard for society, improved governance (GRI, 2017).

Reporting non-financial information with financial information is known as integrated

reporting to help investors to make worthy decision. Stakeholders consider companies activities

towards welfare of society, protection of environment and many non-financial information

before investing in any entity (The IIRC, 2017). This type of sustainability reporting format is

provided by the International Integrated Reporting Council (IIRC). GRI framework supports

integrate reporting as it put attention to take integrated approach rather than following only

traditional approach. Integrated reporting mandates entity to give demo of application of its long

term strategy by keeping in mind all the integrated risk and opportunities (The IIRC, 2017).

(b): Rigor of Conventional Accounting Approaches for Explaining the Contents of

Sustainability

The conventional accounting approaches that is Conceptual Framework (CF) for financial

reporting though is able to provide effective guidance for development and presentation of

financial statements has not proved to be of any usefulness in reporting of environmental and

social performance. The major limitations that are associated with the use of approach in

presentation of non-financial data related to social and environmental performance can be stated

as follows:

Limitation of Conceptual Framework (CF) Objective: The CF has provided that

objective of financial reporting is to facilitate the investment decisions of users mainly

investors, creditors and lenders. However, it has not placed any emphasis on meeting the

requirements of its wider stakeholder groups such as environment and community

members. It only intends to provide financial information and not included any

consideration related to presentation of non-financial information (Ivan, 2009).

11

Materiality Considerations: It has also been provided by the CF that materiality aspect

relates to disclose data that can be verified with the use of practical methods and is

generally objective in nature. This concept is not effective for providing social and

environmental data as it cannot be quantified in monetary terms and thus is not able to be

disclosed as per the materiality concept (Dragomir, 2011)

Elements of Financial Reporting: The CF provided by the IASB has recognized the

different elements of financial reports such as revenue, expenses, assets and others in

monetary terms. As such, the elements provided by the CF are not appropriate for

providing social and environmental data as it cannot be disclosed in monetary terms

(Bazley, Hancock and Robinson, 2014).

(c): Usefulness and Limitations of Theories for Explaining the Contents of Sustainability

Reports

Usefulness

The theories such as stakeholder or legitimacy theories are highly useful to explain the

contents of sustainable reports as they have identified the needs for companies to meet

the varying needs of its different stakeholders. The meeting of different needs of

stakeholders such as suppliers, customers, employees, community and other environment

provides a comprehensive framework for the businesses to develop the sustainable

reports (Manetti, 2011). The disclosure of significant risks and consequent measures

undertaken to overcome them helps the businesses in developing a framework in

disclosure of their sustainable reports (Faisal, Tower and Rusmin, 2012)

Limitations

The limitation of these theoretical frameworks is that they are not able to develop and

provide a coherent system for disclosing the sustainable information. They have only

provided voluntary basis to develop the suitable reports but not able to develop a

mandatory system to report such non-financial information (Villiers and Maroun, 2017)

(d): Evaluation of application of integrated reporting components by selected South

African Company (RCL Foods Limited)

RCL Foods Limited follows IIRC framework to produce the integrated report for year

2018. According to IIRC framework there are 7 major components that need to be included in

the integrated report and all these 7 components have been evaluated in the below table. The

purpose of this section is to evaluate the integrated report of RCL Foods Limited for year 2018

and to provide whether company has disclosed information according to each of these

components.

Components as per

IIRC Framework

Whether

component has

been included in

How each component has been

disclosed by RCL Foods Limited in its

12

relates to disclose data that can be verified with the use of practical methods and is

generally objective in nature. This concept is not effective for providing social and

environmental data as it cannot be quantified in monetary terms and thus is not able to be

disclosed as per the materiality concept (Dragomir, 2011)

Elements of Financial Reporting: The CF provided by the IASB has recognized the

different elements of financial reports such as revenue, expenses, assets and others in

monetary terms. As such, the elements provided by the CF are not appropriate for

providing social and environmental data as it cannot be disclosed in monetary terms

(Bazley, Hancock and Robinson, 2014).

(c): Usefulness and Limitations of Theories for Explaining the Contents of Sustainability

Reports

Usefulness

The theories such as stakeholder or legitimacy theories are highly useful to explain the

contents of sustainable reports as they have identified the needs for companies to meet

the varying needs of its different stakeholders. The meeting of different needs of

stakeholders such as suppliers, customers, employees, community and other environment

provides a comprehensive framework for the businesses to develop the sustainable

reports (Manetti, 2011). The disclosure of significant risks and consequent measures

undertaken to overcome them helps the businesses in developing a framework in

disclosure of their sustainable reports (Faisal, Tower and Rusmin, 2012)

Limitations

The limitation of these theoretical frameworks is that they are not able to develop and

provide a coherent system for disclosing the sustainable information. They have only

provided voluntary basis to develop the suitable reports but not able to develop a

mandatory system to report such non-financial information (Villiers and Maroun, 2017)

(d): Evaluation of application of integrated reporting components by selected South

African Company (RCL Foods Limited)

RCL Foods Limited follows IIRC framework to produce the integrated report for year

2018. According to IIRC framework there are 7 major components that need to be included in

the integrated report and all these 7 components have been evaluated in the below table. The

purpose of this section is to evaluate the integrated report of RCL Foods Limited for year 2018

and to provide whether company has disclosed information according to each of these

components.

Components as per

IIRC Framework

Whether

component has

been included in

How each component has been

disclosed by RCL Foods Limited in its

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.