Analysis of Concetta Ltd.'s Costing System and Inventory Management

VerifiedAdded on 2022/11/24

|6

|1825

|245

Homework Assignment

AI Summary

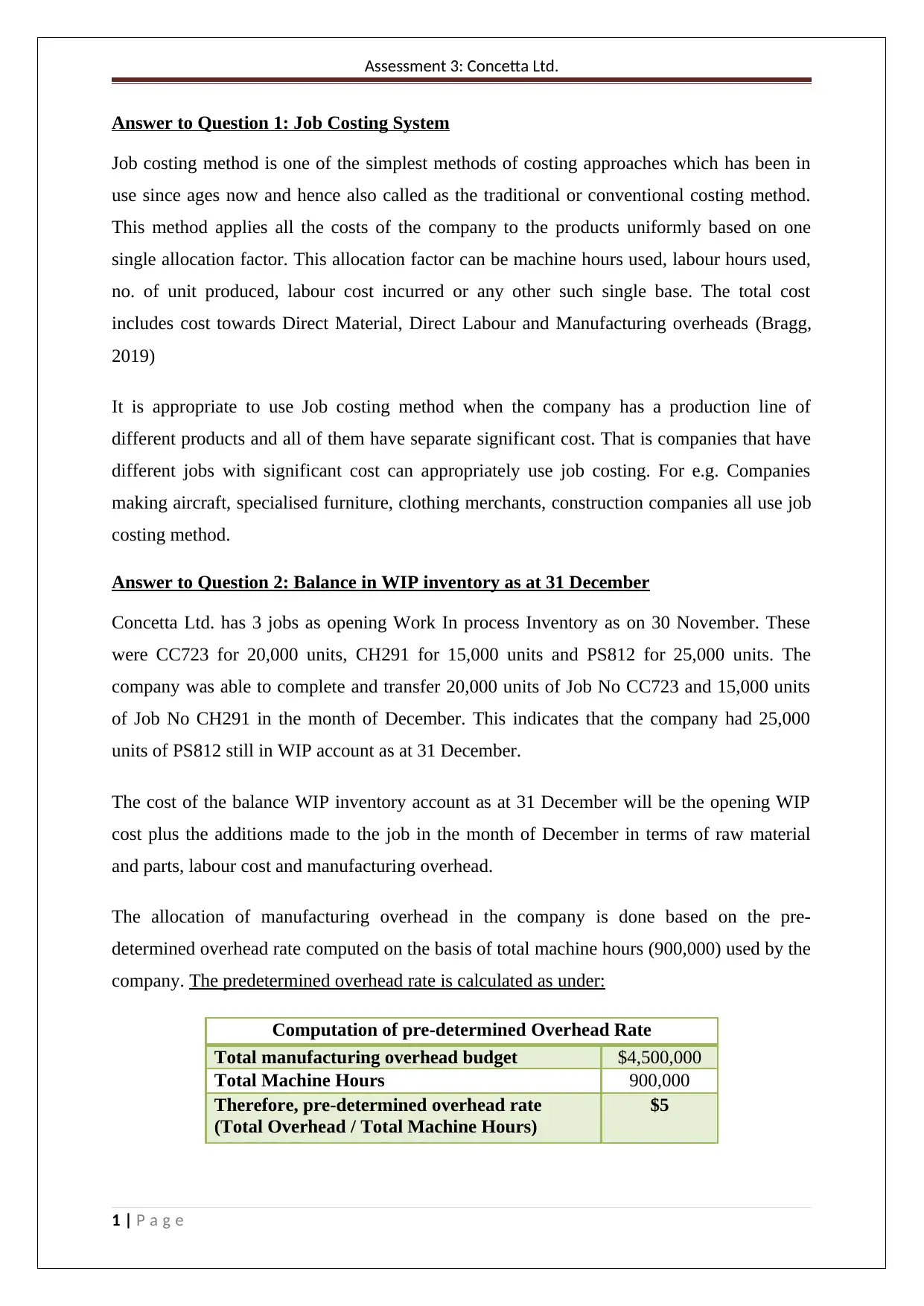

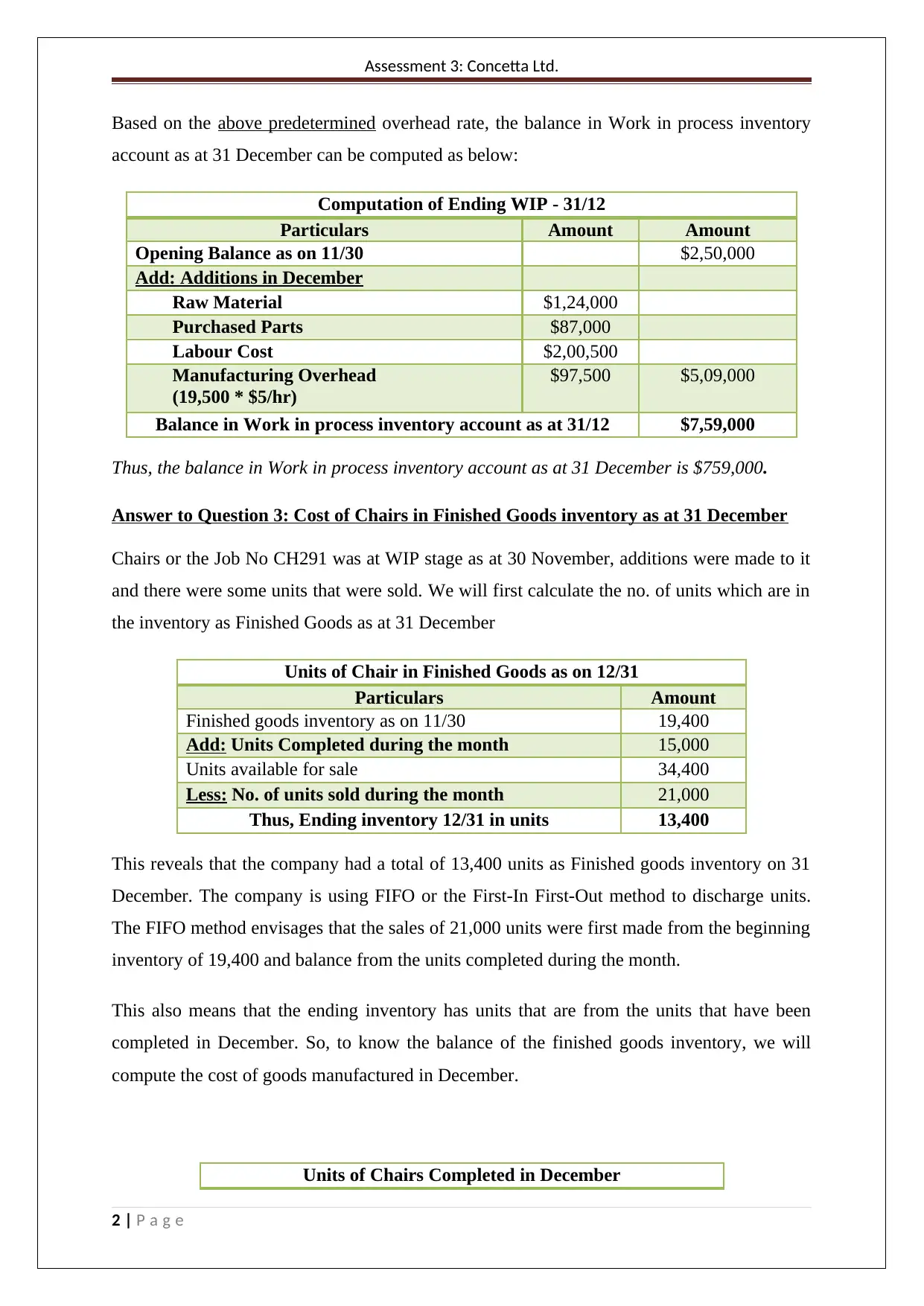

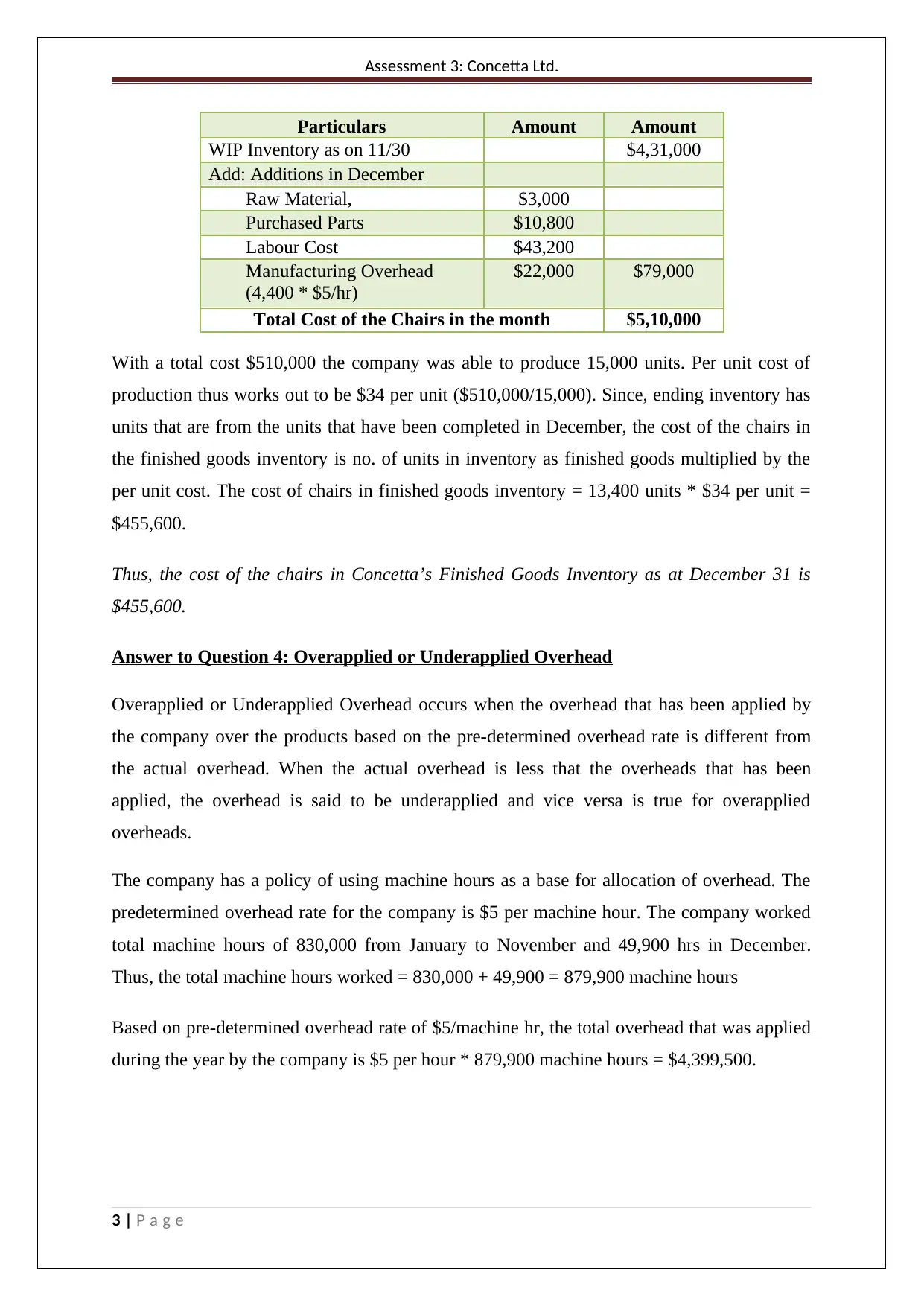

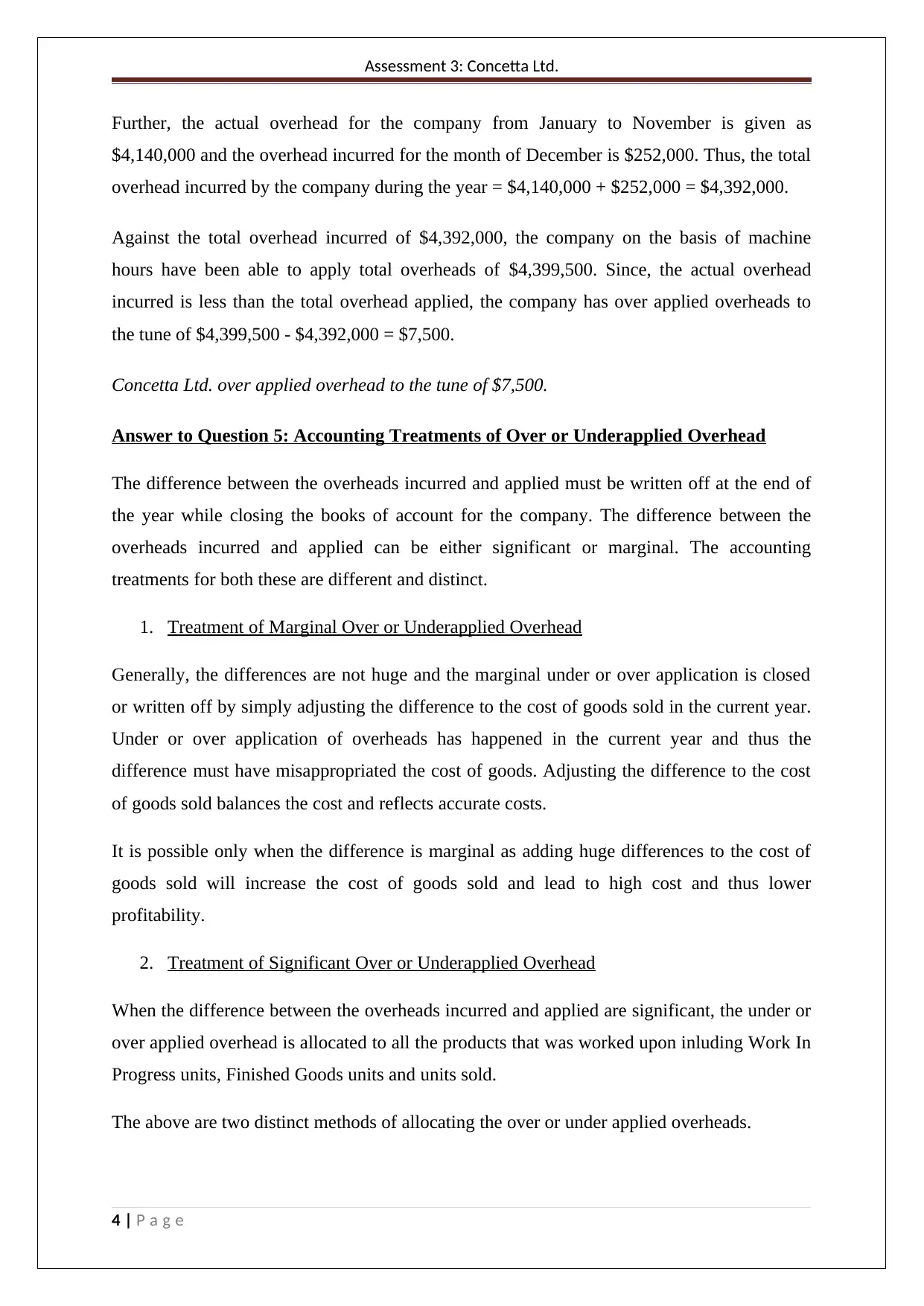

This homework assignment analyzes the costing system of Concetta Ltd., a company utilizing a job costing method. The analysis begins with an overview of job costing, followed by the calculation of the balance in Work-In-Process (WIP) inventory as of December 31st, considering raw materials, purchased parts, labor costs, and manufacturing overhead based on a predetermined overhead rate. The assignment then calculates the cost of chairs in finished goods inventory, applying the FIFO method. Further analysis involves determining overapplied or underapplied overhead, comparing applied overhead with actual overhead, and discussing accounting treatments for both marginal and significant differences. Finally, the assignment compares and contrasts the existing costing system with Activity-Based Costing (ABC), highlighting the limitations of the current approach and the advantages of ABC in allocating costs more accurately based on activity usage.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.