Comprehensive Financial Accounting Report: Conga Toy Retailer (2018)

VerifiedAdded on 2020/12/09

|14

|3603

|479

Homework Assignment

AI Summary

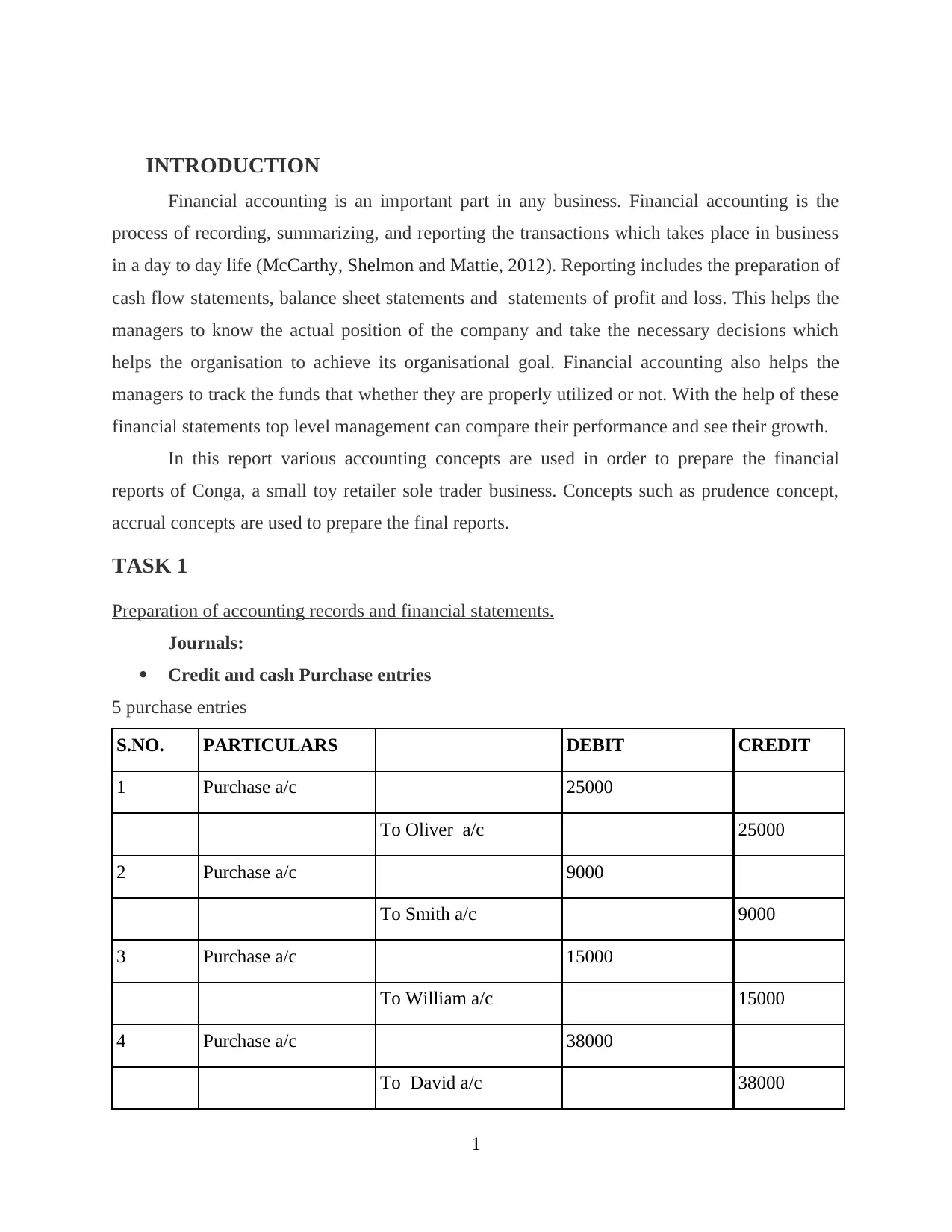

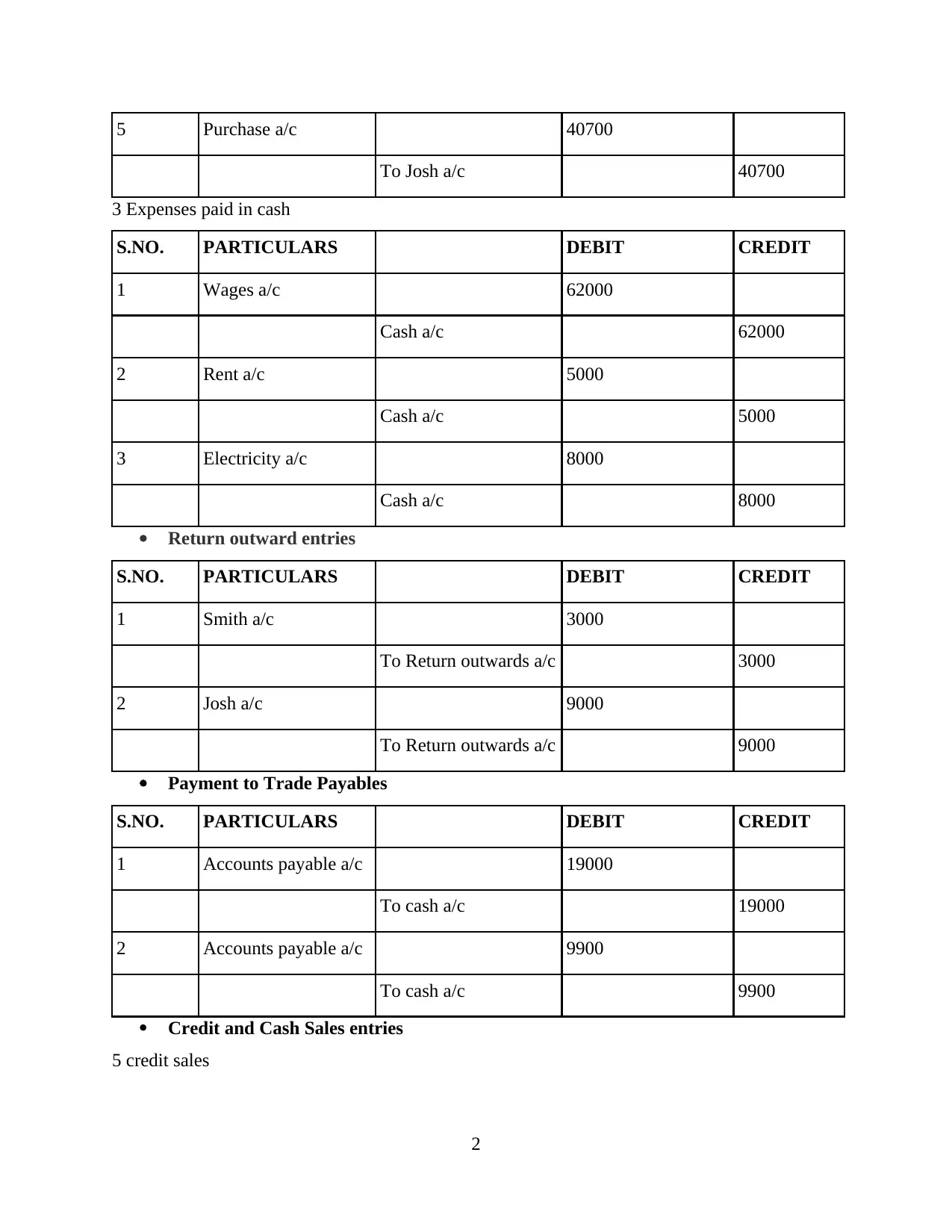

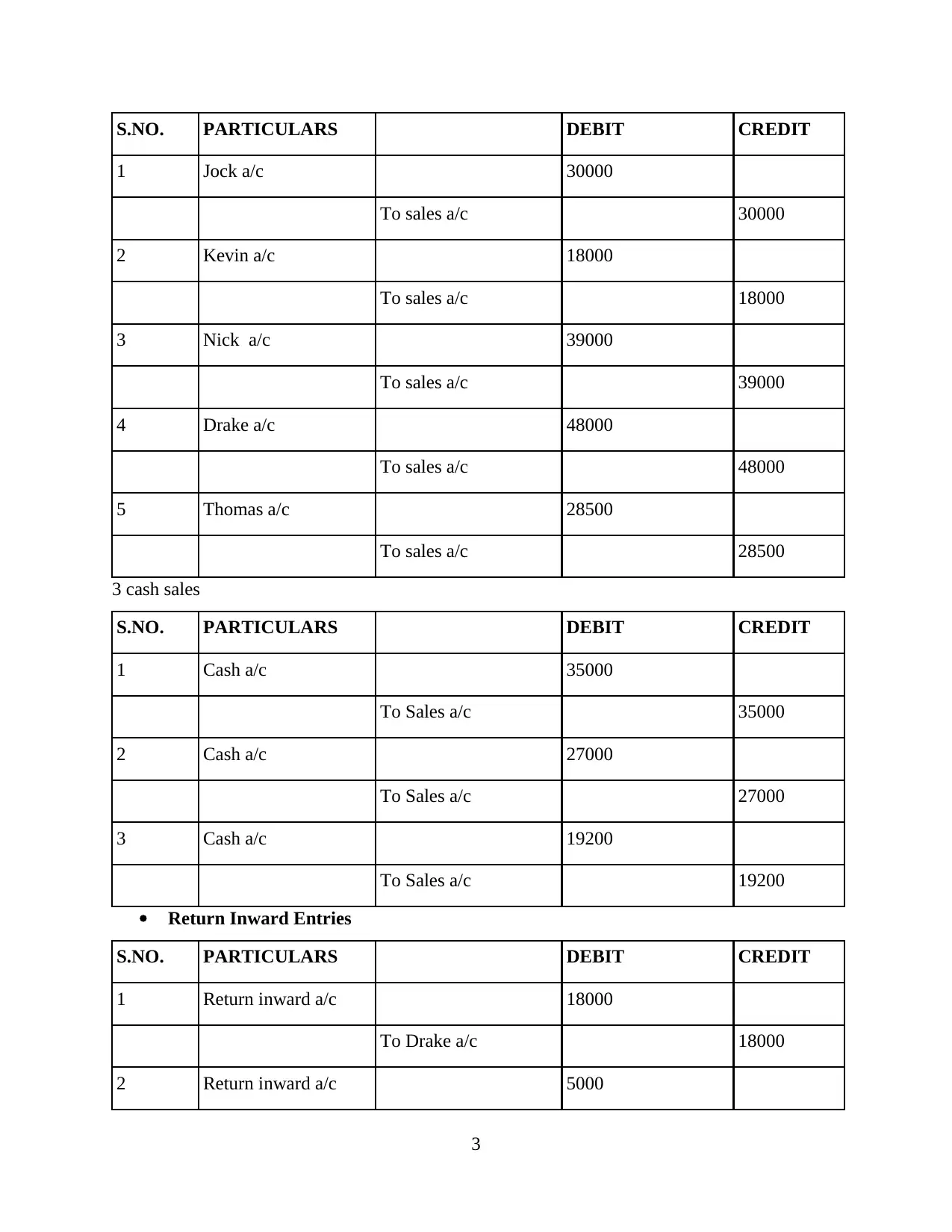

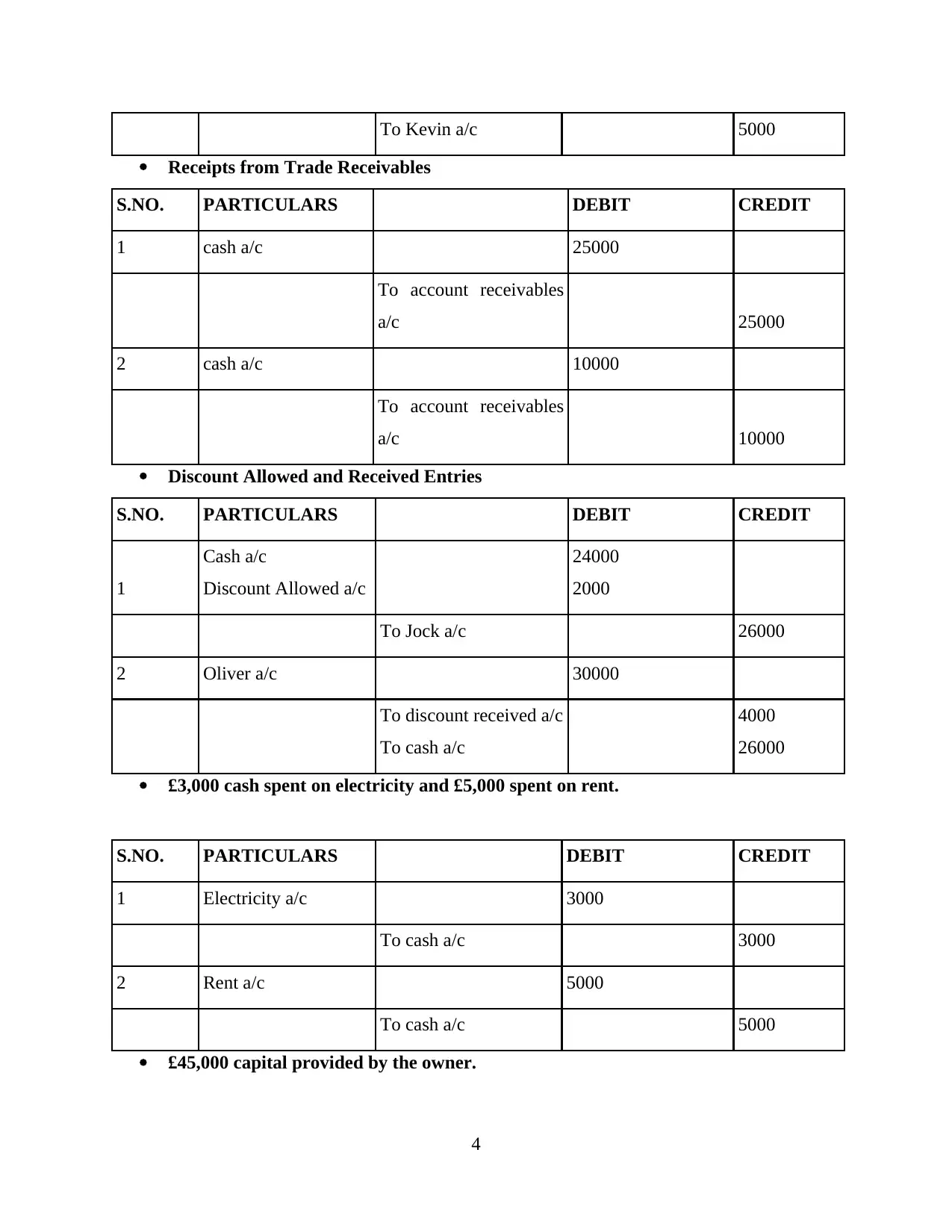

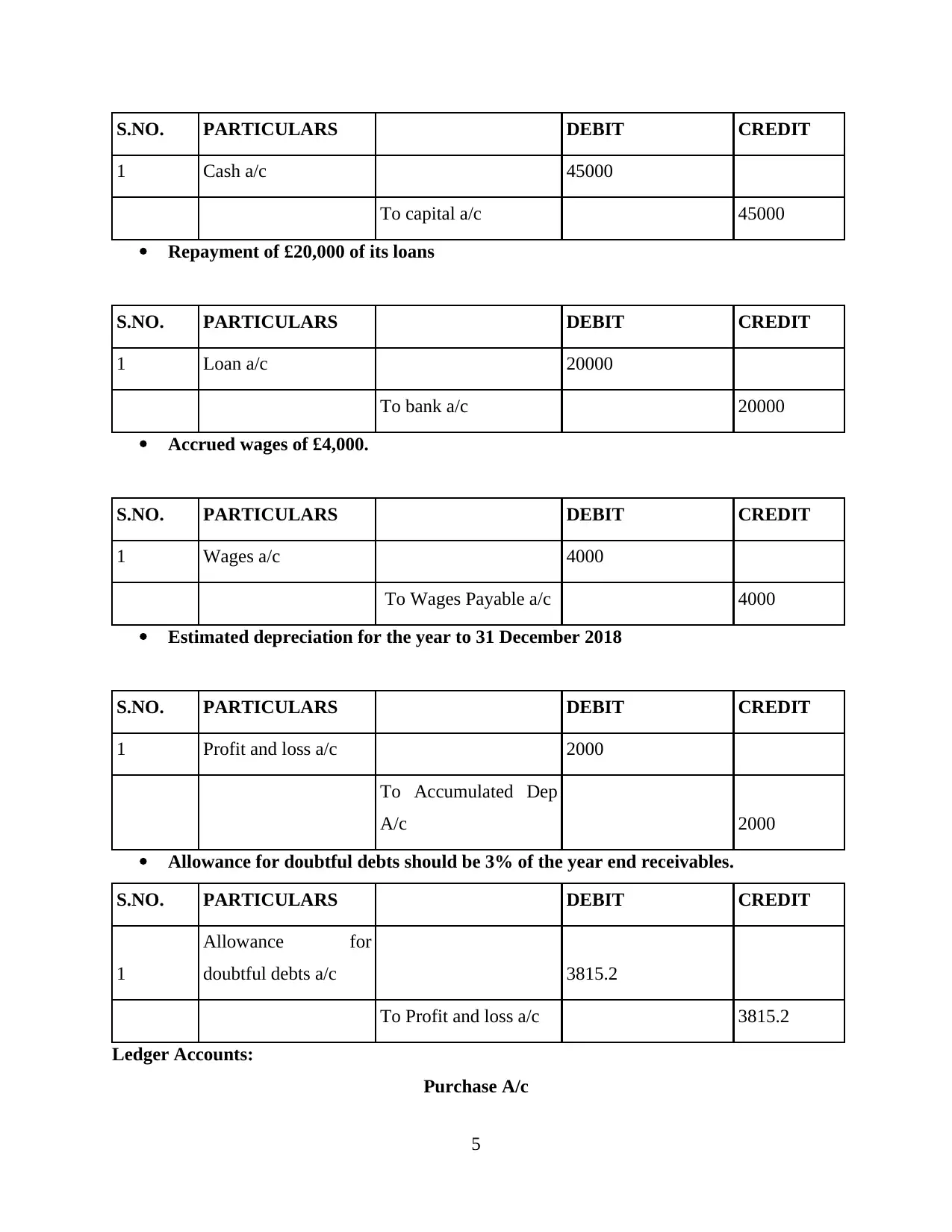

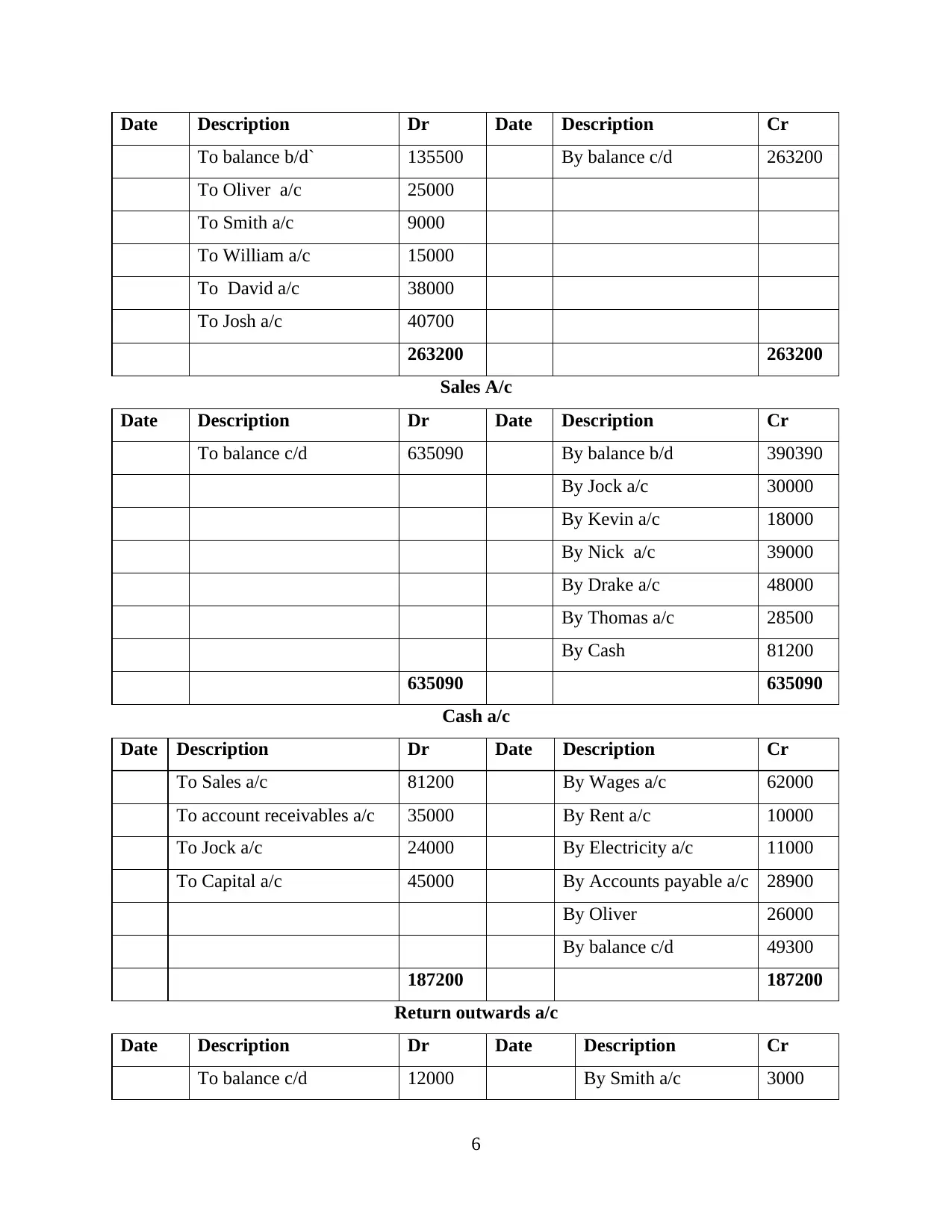

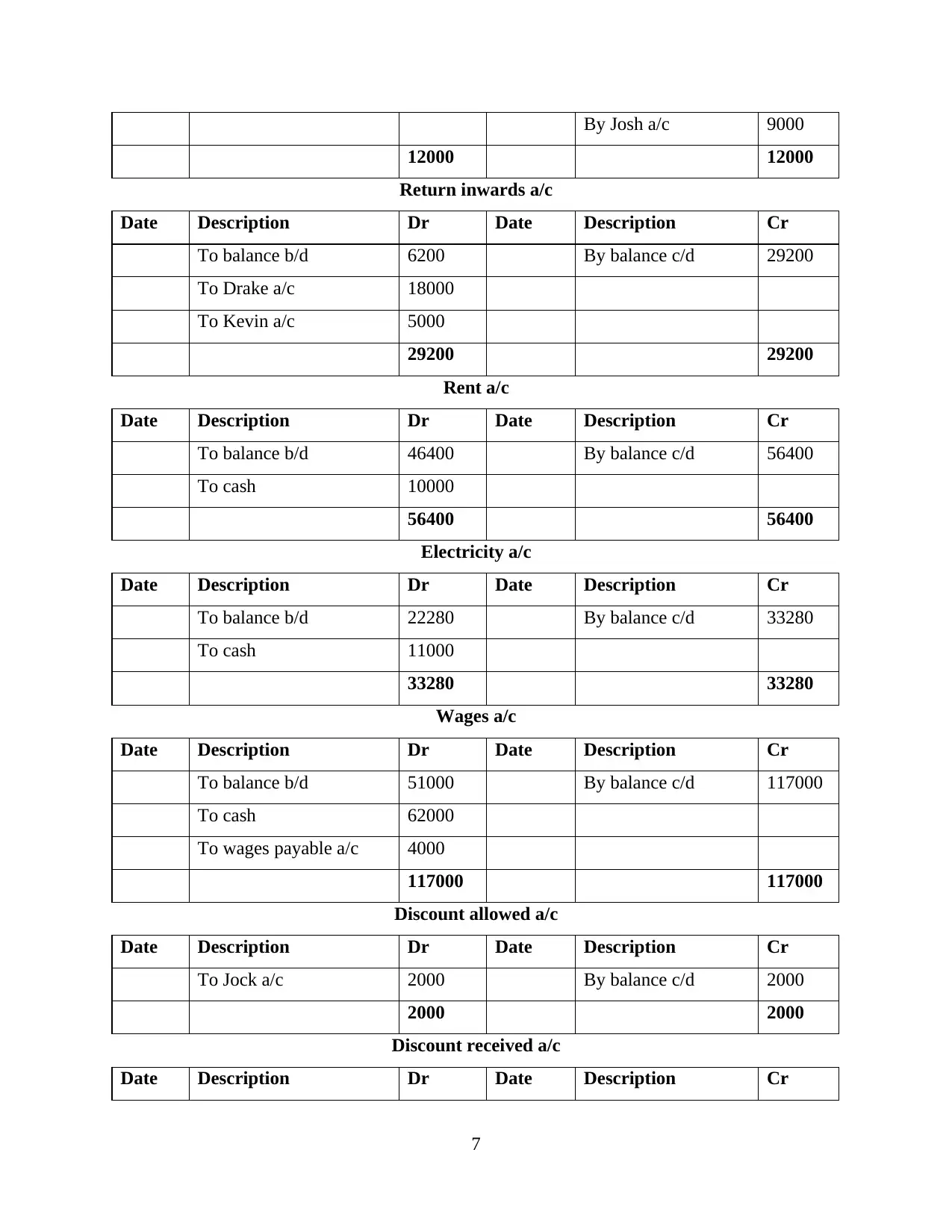

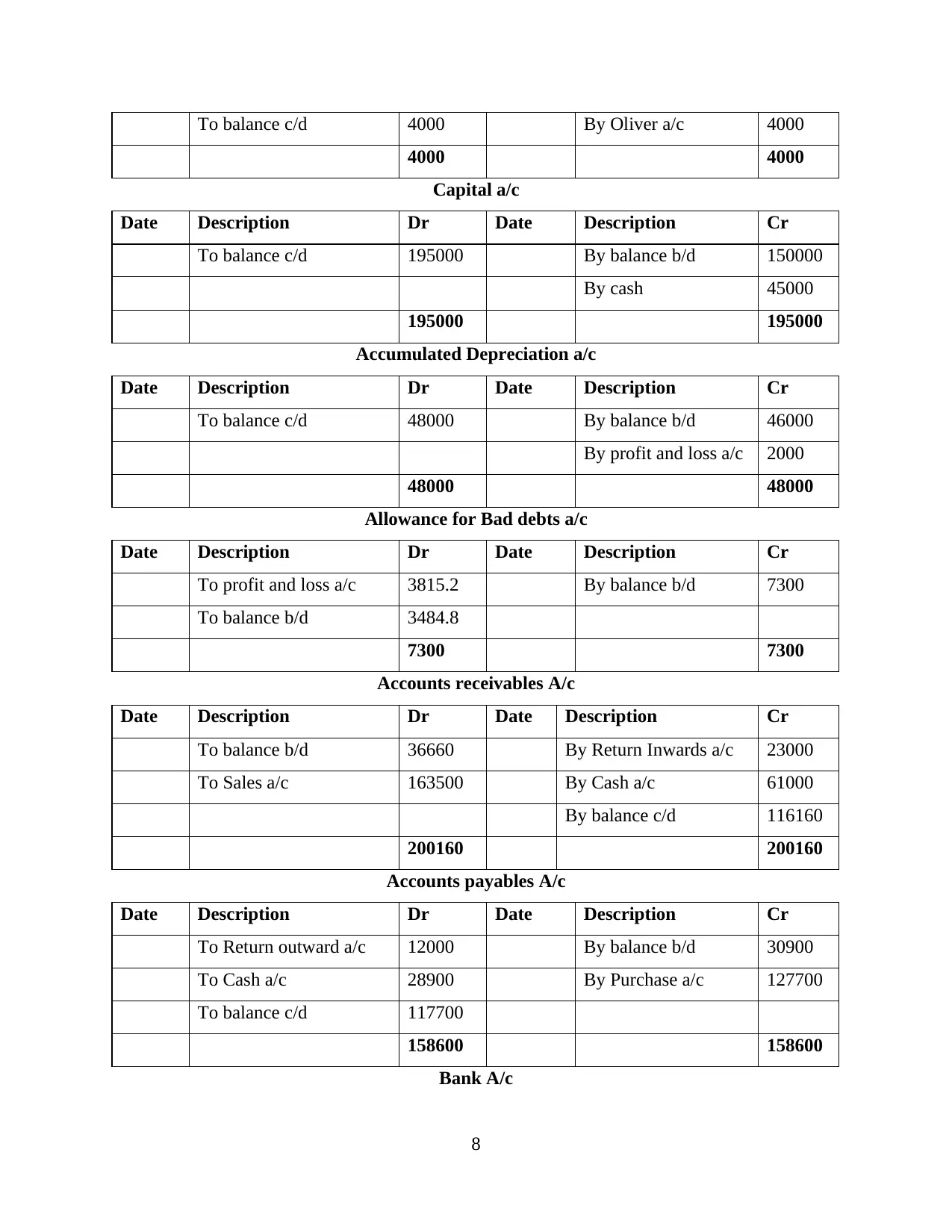

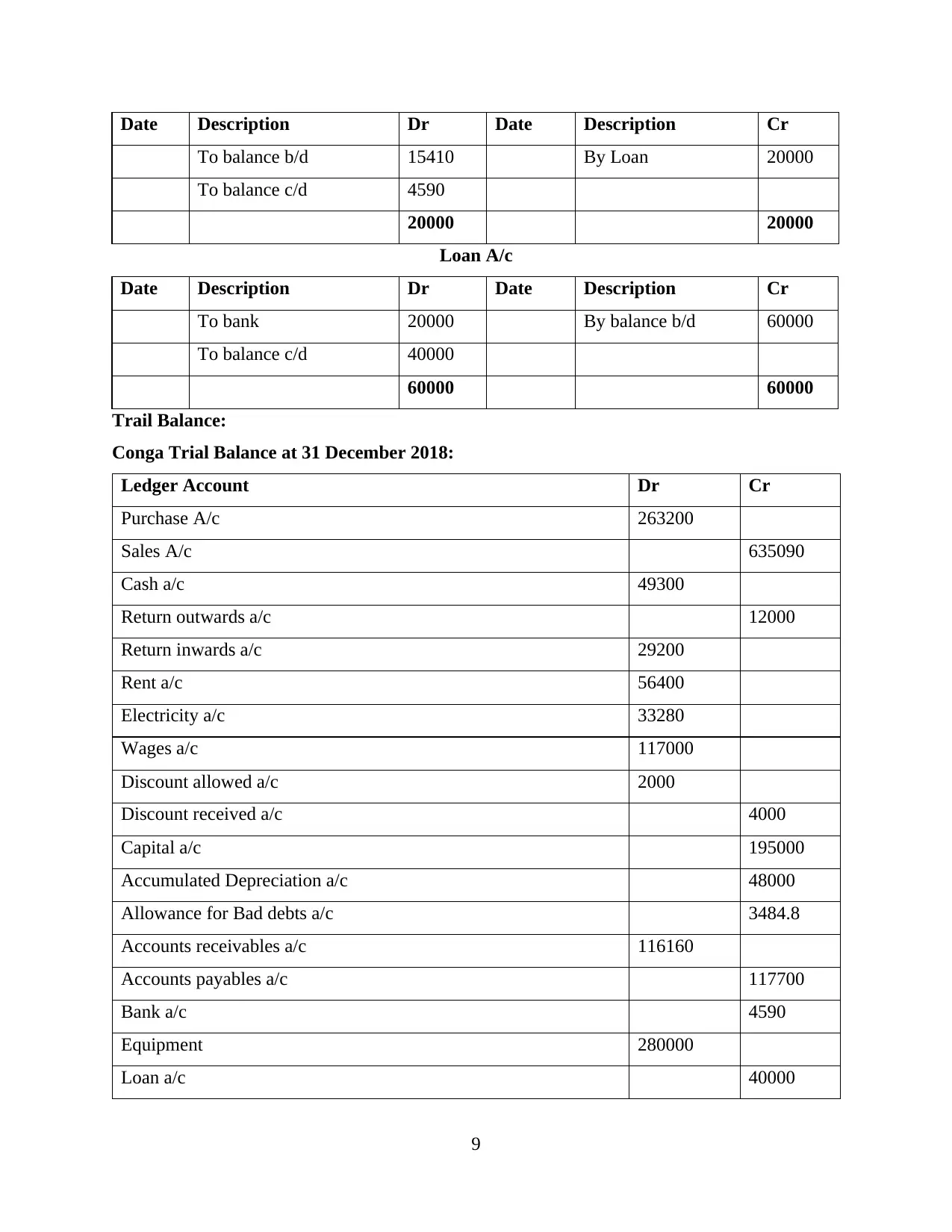

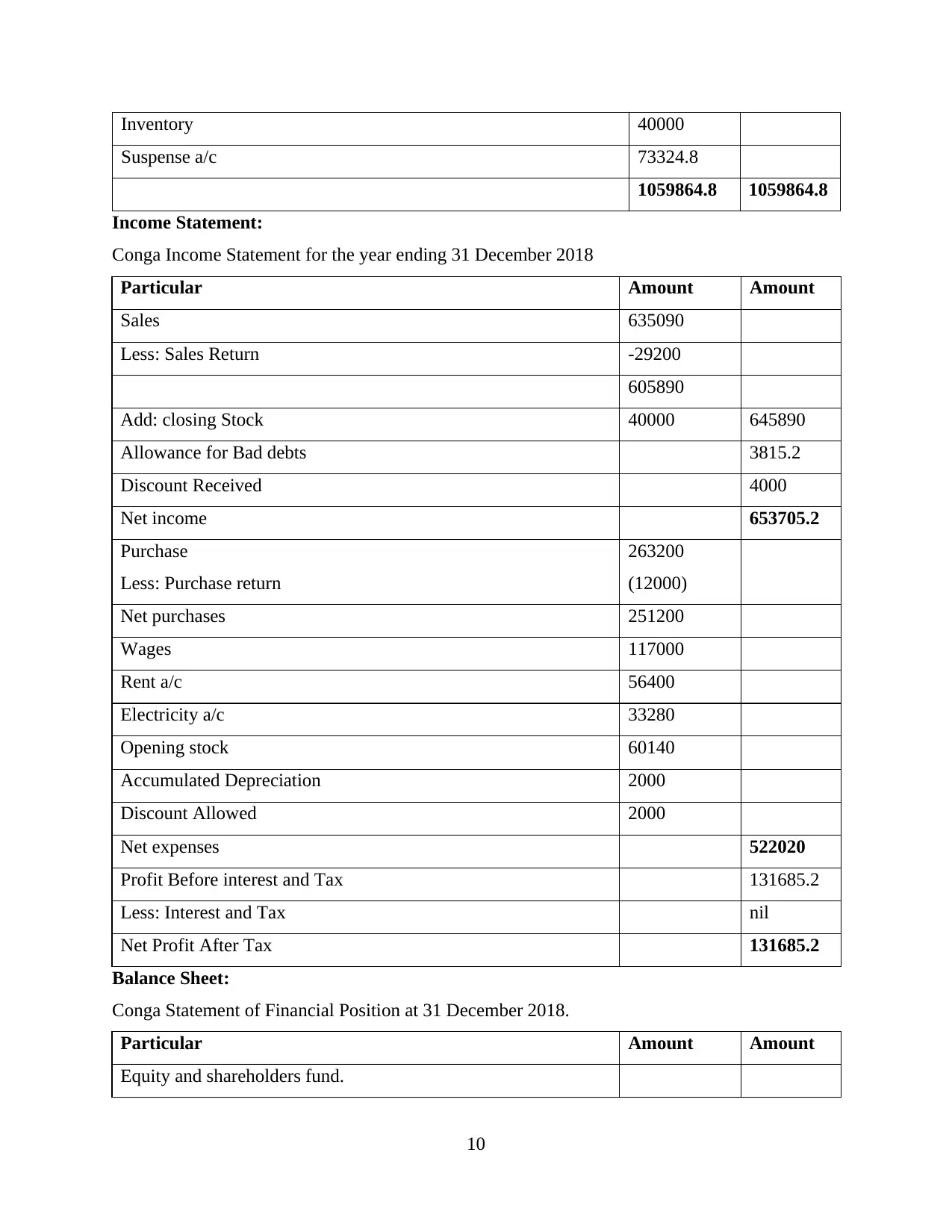

This assignment presents a comprehensive financial accounting report for Conga, a small toy retailer operating as a sole trader. The report meticulously details the process of recording, summarizing, and reporting daily business transactions, encompassing the creation of journals for purchase, sales, and expense entries, along with return inwards and outwards. It includes the preparation of ledger accounts for various financial items such as purchases, sales, cash, returns, rent, electricity, wages, discounts, capital, depreciation, allowance for bad debts, accounts receivables, accounts payables, and bank and loan accounts. The assignment culminates in the creation of a trial balance, income statement, and balance sheet, demonstrating the application of key accounting concepts like prudence and accrual, and providing a snapshot of Conga's financial performance and position for the year ending December 31, 2018.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.