Connect Catering: Management Accounting, Costing, Budgeting

VerifiedAdded on 2022/12/29

|17

|4399

|221

Report

AI Summary

This management accounting report provides an in-depth analysis of Connect Catering Services, a UK-based company, focusing on essential management accounting concepts, various reporting methods, and cost calculation techniques. It includes a discussion on different types of management accounting systems, such as cost accounting, inventory management, job costing, and price optimization. The report further explains the advantages and disadvantages of planning tools used for budgetary control and compares how organizations adapt their management accounting systems to respond to financial problems. The analysis includes income statements prepared using marginal and absorption costing, break-even point calculations, and a reconciliation statement, offering a comprehensive view of the company's financial management strategies. Desklib provides access to this and many other solved assignments for students.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

P1 What is management accounting and state the essential requirements of various types of

management accounting system..................................................................................................4

P2 Explain the different methods used under management accounting reporting......................6

TASK 2.......................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

1 Preparation of income statements:...........................................................................................7

TASK 3.....................................................................................................................................10

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................10

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

P1 What is management accounting and state the essential requirements of various types of

management accounting system..................................................................................................4

P2 Explain the different methods used under management accounting reporting......................6

TASK 2.......................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

1 Preparation of income statements:...........................................................................................7

TASK 3.....................................................................................................................................10

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................10

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management Accounting is the branch of accounting that relates to the implementation of

professional skills, knowledge, tools and techniques that helps composing of statements that

helps management in evaluating its performance and facilitates plans and policies formulation

with the available accounting information. It focuses on optimum utilization of scarce resources

and their safeguarding, operational efficiency and effectiveness, significant and strategic decision

making process that results in high returns and making the stakeholders pleased and proud. The

users for these accounting statements are only the internal management committee of the

organisation. Both financial as well as non financial factors are included in these type of

information (Appelbaum and Nehmer, 2020). These information have a notable impact on

business operations that are being ignored in the other financial statements. It facilitates

management in identifying the areas of key concern that assists management committee in taking

corrective measures for overcoming these issues and enhance operational efficiency.

Management accounting relates to the preparation of accounting information in context with the

the professional knowledge and skills in a way that facilitates organisation's management in

operational planning, directing and controlling and also in formulating policies, in terms of The

Institute of Cost Management Accounting, London (ICMA). Also, as per The American

Accounting Association (AAA), it is the procedure and concept that is required for a successful

process of planning that assists the organisation in choosing the best alternative among various

available after evaluation, then controlling and interpreting its results.

This report related to the scenario of Connect Catering Services. It is one of the best

brand of UK and have its headquarters in Oxfordshire, established in the year 1989 by John

Herring. This report covers the concept of management accounting, its types and various reports

prepared in context with management accounting (Brustbauer, 2016). Cost calculation with

different methods, budgetary tools advantages and disadvantages and the comparison among two

companies in terms of the approach used by them for solving financial problems.

TASK 1

Management Accounting is the branch of accounting that relates to the implementation of

professional skills, knowledge, tools and techniques that helps composing of statements that

helps management in evaluating its performance and facilitates plans and policies formulation

with the available accounting information. It focuses on optimum utilization of scarce resources

and their safeguarding, operational efficiency and effectiveness, significant and strategic decision

making process that results in high returns and making the stakeholders pleased and proud. The

users for these accounting statements are only the internal management committee of the

organisation. Both financial as well as non financial factors are included in these type of

information (Appelbaum and Nehmer, 2020). These information have a notable impact on

business operations that are being ignored in the other financial statements. It facilitates

management in identifying the areas of key concern that assists management committee in taking

corrective measures for overcoming these issues and enhance operational efficiency.

Management accounting relates to the preparation of accounting information in context with the

the professional knowledge and skills in a way that facilitates organisation's management in

operational planning, directing and controlling and also in formulating policies, in terms of The

Institute of Cost Management Accounting, London (ICMA). Also, as per The American

Accounting Association (AAA), it is the procedure and concept that is required for a successful

process of planning that assists the organisation in choosing the best alternative among various

available after evaluation, then controlling and interpreting its results.

This report related to the scenario of Connect Catering Services. It is one of the best

brand of UK and have its headquarters in Oxfordshire, established in the year 1989 by John

Herring. This report covers the concept of management accounting, its types and various reports

prepared in context with management accounting (Brustbauer, 2016). Cost calculation with

different methods, budgetary tools advantages and disadvantages and the comparison among two

companies in terms of the approach used by them for solving financial problems.

TASK 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1 What is management accounting and state the essential requirements of various types of

management accounting system.

Management accounting is the action plan for developing goals and objectives for a

company by measuring, evaluating, clarifying, and conveying the manager the guidance path for

its achievement. It is also sometimes referred as managerial accounting or managerial form of

accounting. It assist the managers in decision making process with the help of available financial

resources and info (Davis and Davis, 2019). It supports the management committee in

performing their operations effectively and efficiently also to control and monitor the functions

of the organization. These are mainly prepared for the use by internal stakeholders and the

external stakeholders are least or are not concerned with these reports. It helps the management

in timely preparation and giving of the financial statements of the organization to the users. Cash

availability, generation of sales revenue, status of accounts payable and receivables and other

similar reports are some type of reports prepared under management accounting system.

Management accounting system has originated from the financial accounting, despite of

this fact, there is a huge difference in both of the accounting system styles. Management

accounting is more beneficial to the internal management committee thus have a wide

acceptance. Few difference between the management accounting and financial accounting are as

follows:

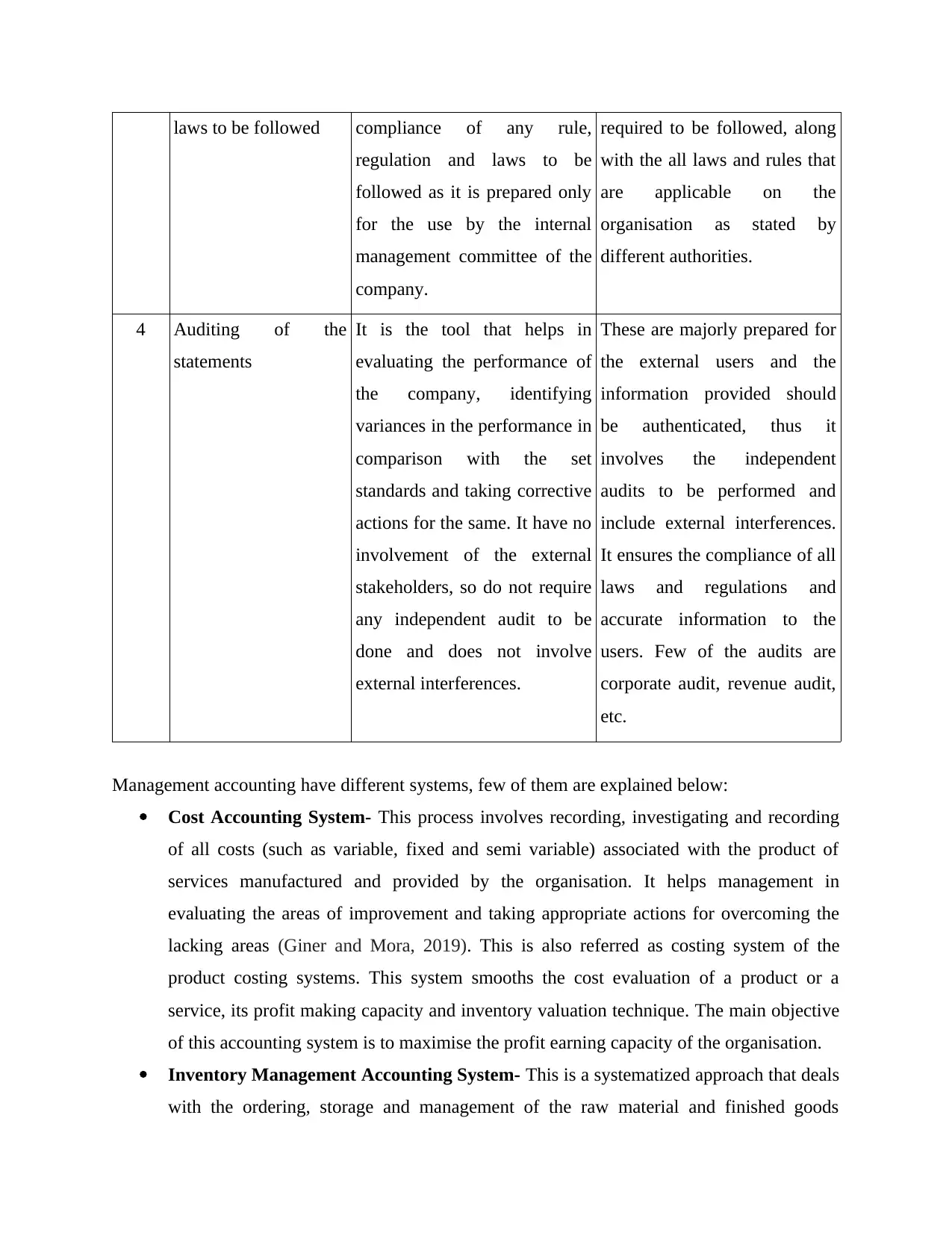

S. No. Basis of Comparison Management Accounting Financial Accounting

1 Content It consists of all type of

information whether financial

and non financial.

It only relates to the

information having a financial

impact associated with it.

2 Motive and Uses The main objective of

preparation of these statements

are for the use of the internal

management as it facilitates

decision making and

performance evaluation (El-

Helaly, 2016).

It is prepared for providing

financial information to the all

interested stakeholders of the

organisation and helps them in

their decision making.

3 Rules, Regulations and Its preparation does not involve All accounting standards are

management accounting system.

Management accounting is the action plan for developing goals and objectives for a

company by measuring, evaluating, clarifying, and conveying the manager the guidance path for

its achievement. It is also sometimes referred as managerial accounting or managerial form of

accounting. It assist the managers in decision making process with the help of available financial

resources and info (Davis and Davis, 2019). It supports the management committee in

performing their operations effectively and efficiently also to control and monitor the functions

of the organization. These are mainly prepared for the use by internal stakeholders and the

external stakeholders are least or are not concerned with these reports. It helps the management

in timely preparation and giving of the financial statements of the organization to the users. Cash

availability, generation of sales revenue, status of accounts payable and receivables and other

similar reports are some type of reports prepared under management accounting system.

Management accounting system has originated from the financial accounting, despite of

this fact, there is a huge difference in both of the accounting system styles. Management

accounting is more beneficial to the internal management committee thus have a wide

acceptance. Few difference between the management accounting and financial accounting are as

follows:

S. No. Basis of Comparison Management Accounting Financial Accounting

1 Content It consists of all type of

information whether financial

and non financial.

It only relates to the

information having a financial

impact associated with it.

2 Motive and Uses The main objective of

preparation of these statements

are for the use of the internal

management as it facilitates

decision making and

performance evaluation (El-

Helaly, 2016).

It is prepared for providing

financial information to the all

interested stakeholders of the

organisation and helps them in

their decision making.

3 Rules, Regulations and Its preparation does not involve All accounting standards are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

laws to be followed compliance of any rule,

regulation and laws to be

followed as it is prepared only

for the use by the internal

management committee of the

company.

required to be followed, along

with the all laws and rules that

are applicable on the

organisation as stated by

different authorities.

4 Auditing of the

statements

It is the tool that helps in

evaluating the performance of

the company, identifying

variances in the performance in

comparison with the set

standards and taking corrective

actions for the same. It have no

involvement of the external

stakeholders, so do not require

any independent audit to be

done and does not involve

external interferences.

These are majorly prepared for

the external users and the

information provided should

be authenticated, thus it

involves the independent

audits to be performed and

include external interferences.

It ensures the compliance of all

laws and regulations and

accurate information to the

users. Few of the audits are

corporate audit, revenue audit,

etc.

Management accounting have different systems, few of them are explained below:

Cost Accounting System- This process involves recording, investigating and recording

of all costs (such as variable, fixed and semi variable) associated with the product of

services manufactured and provided by the organisation. It helps management in

evaluating the areas of improvement and taking appropriate actions for overcoming the

lacking areas (Giner and Mora, 2019). This is also referred as costing system of the

product costing systems. This system smooths the cost evaluation of a product or a

service, its profit making capacity and inventory valuation technique. The main objective

of this accounting system is to maximise the profit earning capacity of the organisation.

Inventory Management Accounting System- This is a systematized approach that deals

with the ordering, storage and management of the raw material and finished goods

regulation and laws to be

followed as it is prepared only

for the use by the internal

management committee of the

company.

required to be followed, along

with the all laws and rules that

are applicable on the

organisation as stated by

different authorities.

4 Auditing of the

statements

It is the tool that helps in

evaluating the performance of

the company, identifying

variances in the performance in

comparison with the set

standards and taking corrective

actions for the same. It have no

involvement of the external

stakeholders, so do not require

any independent audit to be

done and does not involve

external interferences.

These are majorly prepared for

the external users and the

information provided should

be authenticated, thus it

involves the independent

audits to be performed and

include external interferences.

It ensures the compliance of all

laws and regulations and

accurate information to the

users. Few of the audits are

corporate audit, revenue audit,

etc.

Management accounting have different systems, few of them are explained below:

Cost Accounting System- This process involves recording, investigating and recording

of all costs (such as variable, fixed and semi variable) associated with the product of

services manufactured and provided by the organisation. It helps management in

evaluating the areas of improvement and taking appropriate actions for overcoming the

lacking areas (Giner and Mora, 2019). This is also referred as costing system of the

product costing systems. This system smooths the cost evaluation of a product or a

service, its profit making capacity and inventory valuation technique. The main objective

of this accounting system is to maximise the profit earning capacity of the organisation.

Inventory Management Accounting System- This is a systematized approach that deals

with the ordering, storage and management of the raw material and finished goods

inventories and other equipments within the company. It focuses on quality control of the

products manufactured and ensures the availableness of the right stock, in right quantity,

at a right place and on the right time that is purchased at the right cost. It reduces the risk

of shortage of inventory, high inventory storage costs for the organisations having a

complex supply chain management or manufacturing processes. The main aim of this

accounting system is to reduce the cost and over stocking that results in loss minimization

and maintaining liquidity in the organisation.

Job Costing Accounting System- It is a distinctive process that accumulates the

information related to all the cost associated to a particular product or a service,

performed in accordance with the customer's requirement (Henri and Wouters, 2020).

The main purpose behind this system is to evaluate the profit or loss made on each job or

a service. It allows the organisation to quote the price that allows the firm in making

reasonable profits.

Price Optimisation Accounting System- This is a mathematical tool used for

determining the price of a particular product. It assists in predicting changes in quantity

and amount and fix a desired price that a customer is ready, able and willing to pay for

consuming or purchasing the organisation's product. It helps the company in using the

price as a powerful profit maker.

P2 Explain the different methods used under management accounting reporting.

Accounting Reports plays an integral part that provides a complete picture of the

organization's performance in relation to the trends running in the industry. It helps in

ascertaining the company's operations whether they are in direction towards the achievement of

organization's goals and objectives. These reports should be absolute, correct, precised and valid

to rely on, so as to make the decisions and formulate strategies and evaluate performance by the

management.

Budget Report- It is the fundamental report that assists the owners to address and control

the operational cost in the organization. It is prepared on the past experiences and provide

directions to the manager and employees in increasing productivity and providing greater

benefits to employees, cost negotiation with suppliers and vendors (Ipino and Parbonetti,

2017).

products manufactured and ensures the availableness of the right stock, in right quantity,

at a right place and on the right time that is purchased at the right cost. It reduces the risk

of shortage of inventory, high inventory storage costs for the organisations having a

complex supply chain management or manufacturing processes. The main aim of this

accounting system is to reduce the cost and over stocking that results in loss minimization

and maintaining liquidity in the organisation.

Job Costing Accounting System- It is a distinctive process that accumulates the

information related to all the cost associated to a particular product or a service,

performed in accordance with the customer's requirement (Henri and Wouters, 2020).

The main purpose behind this system is to evaluate the profit or loss made on each job or

a service. It allows the organisation to quote the price that allows the firm in making

reasonable profits.

Price Optimisation Accounting System- This is a mathematical tool used for

determining the price of a particular product. It assists in predicting changes in quantity

and amount and fix a desired price that a customer is ready, able and willing to pay for

consuming or purchasing the organisation's product. It helps the company in using the

price as a powerful profit maker.

P2 Explain the different methods used under management accounting reporting.

Accounting Reports plays an integral part that provides a complete picture of the

organization's performance in relation to the trends running in the industry. It helps in

ascertaining the company's operations whether they are in direction towards the achievement of

organization's goals and objectives. These reports should be absolute, correct, precised and valid

to rely on, so as to make the decisions and formulate strategies and evaluate performance by the

management.

Budget Report- It is the fundamental report that assists the owners to address and control

the operational cost in the organization. It is prepared on the past experiences and provide

directions to the manager and employees in increasing productivity and providing greater

benefits to employees, cost negotiation with suppliers and vendors (Ipino and Parbonetti,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job Cost Report- It gives the basic view of total cost incurred on a particular product or

a particular job. Its purpose is to evaluate the profitability relating to a single task or

project. It helps in identifying the most profitable business unit and giving it the most

focus and less focuses to the units earning lower returns.

Inventory and Manufacturing Report- It is the summary report of the inventory held

by the company at the given point of time. The main aim for this report is to enhance the

efficiency in production process and includes items like labor cost, overheads incurred in

the production of a single product.

Order Information Report- It facilitates evaluation of efficiency and effectiveness in

business trends (Krause and Tse, 2016). It comprises of information regarding the

multiple orders obtained by the company. It assist the organization in achieving cost

leadership and integrates different management operations.

Accounts Receivable Aging Report- It is related to the credit balances of the shoppers.

It aligns the organization's policy with the paying capacity of its customers. It is used for

finding the problems associated with the organization's credit policy by the managers. It

ensures the removal of old debts that are potentially bad debts.

Performance Report- This report gives a hostile view of the organization's performance.

It summarize the end results of all the activities or the performance of an individual in

terms of the work done. It is the standard sets for the performance, identifying deviations

and taking correct actions for overcoming the performance gaps (Lev, 2019). It involves

indicators like achievements made, objectives fulfilled, tasks accomplished, etc..

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

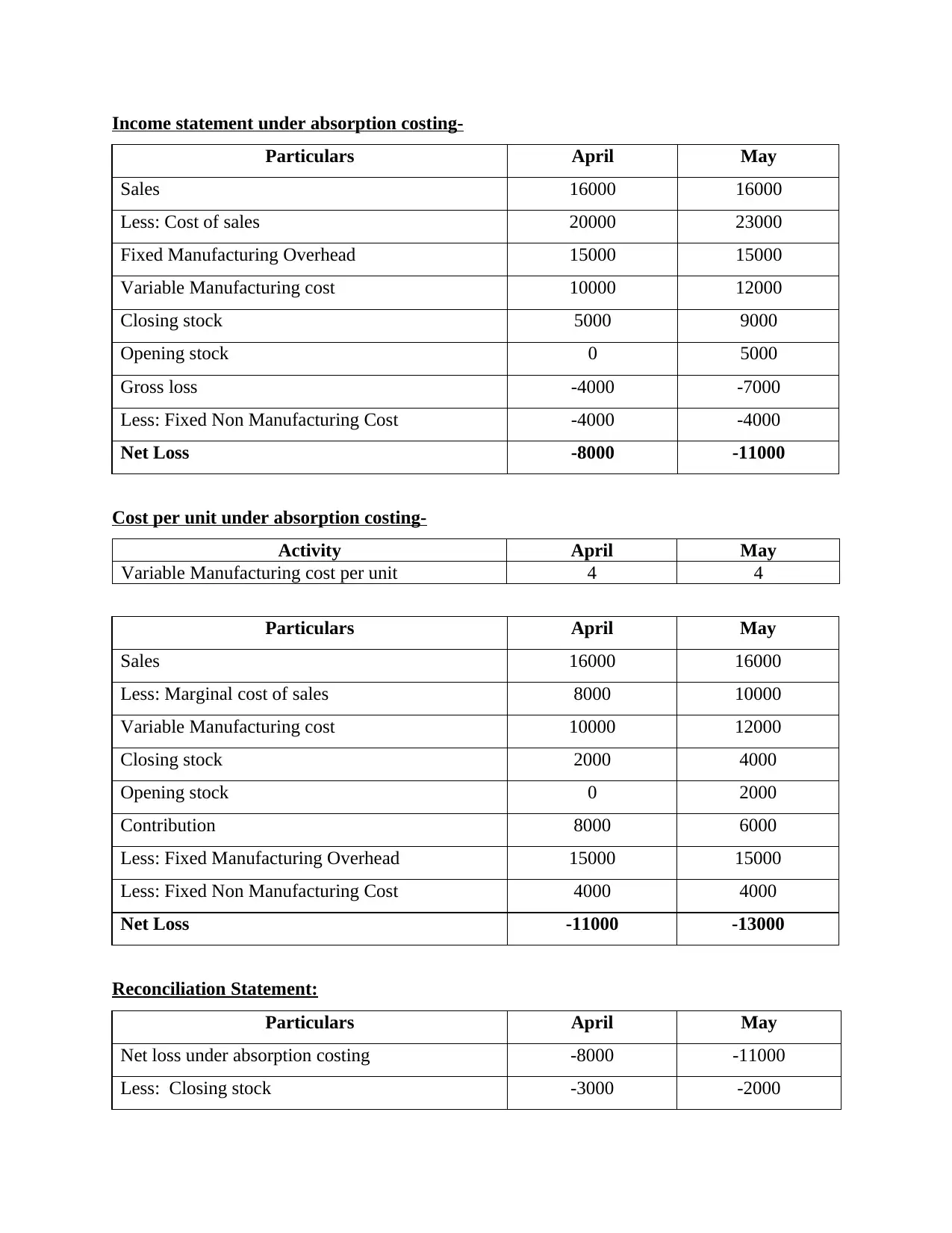

1 Preparation of income statements:

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

Total 10 9

a particular job. Its purpose is to evaluate the profitability relating to a single task or

project. It helps in identifying the most profitable business unit and giving it the most

focus and less focuses to the units earning lower returns.

Inventory and Manufacturing Report- It is the summary report of the inventory held

by the company at the given point of time. The main aim for this report is to enhance the

efficiency in production process and includes items like labor cost, overheads incurred in

the production of a single product.

Order Information Report- It facilitates evaluation of efficiency and effectiveness in

business trends (Krause and Tse, 2016). It comprises of information regarding the

multiple orders obtained by the company. It assist the organization in achieving cost

leadership and integrates different management operations.

Accounts Receivable Aging Report- It is related to the credit balances of the shoppers.

It aligns the organization's policy with the paying capacity of its customers. It is used for

finding the problems associated with the organization's credit policy by the managers. It

ensures the removal of old debts that are potentially bad debts.

Performance Report- This report gives a hostile view of the organization's performance.

It summarize the end results of all the activities or the performance of an individual in

terms of the work done. It is the standard sets for the performance, identifying deviations

and taking correct actions for overcoming the performance gaps (Lev, 2019). It involves

indicators like achievements made, objectives fulfilled, tasks accomplished, etc..

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

1 Preparation of income statements:

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

Total 10 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement under absorption costing-

Particulars April May

Sales 16000 16000

Less: Cost of sales 20000 23000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost 10000 12000

Closing stock 5000 9000

Opening stock 0 5000

Gross loss -4000 -7000

Less: Fixed Non Manufacturing Cost -4000 -4000

Net Loss -8000 -11000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 10000

Variable Manufacturing cost 10000 12000

Closing stock 2000 4000

Opening stock 0 2000

Contribution 8000 6000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non Manufacturing Cost 4000 4000

Net Loss -11000 -13000

Reconciliation Statement:

Particulars April May

Net loss under absorption costing -8000 -11000

Less: Closing stock -3000 -2000

Particulars April May

Sales 16000 16000

Less: Cost of sales 20000 23000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost 10000 12000

Closing stock 5000 9000

Opening stock 0 5000

Gross loss -4000 -7000

Less: Fixed Non Manufacturing Cost -4000 -4000

Net Loss -8000 -11000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 10000

Variable Manufacturing cost 10000 12000

Closing stock 2000 4000

Opening stock 0 2000

Contribution 8000 6000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non Manufacturing Cost 4000 4000

Net Loss -11000 -13000

Reconciliation Statement:

Particulars April May

Net loss under absorption costing -8000 -11000

Less: Closing stock -3000 -2000

Net loss under marginal costing -11000 -13000

2 a.

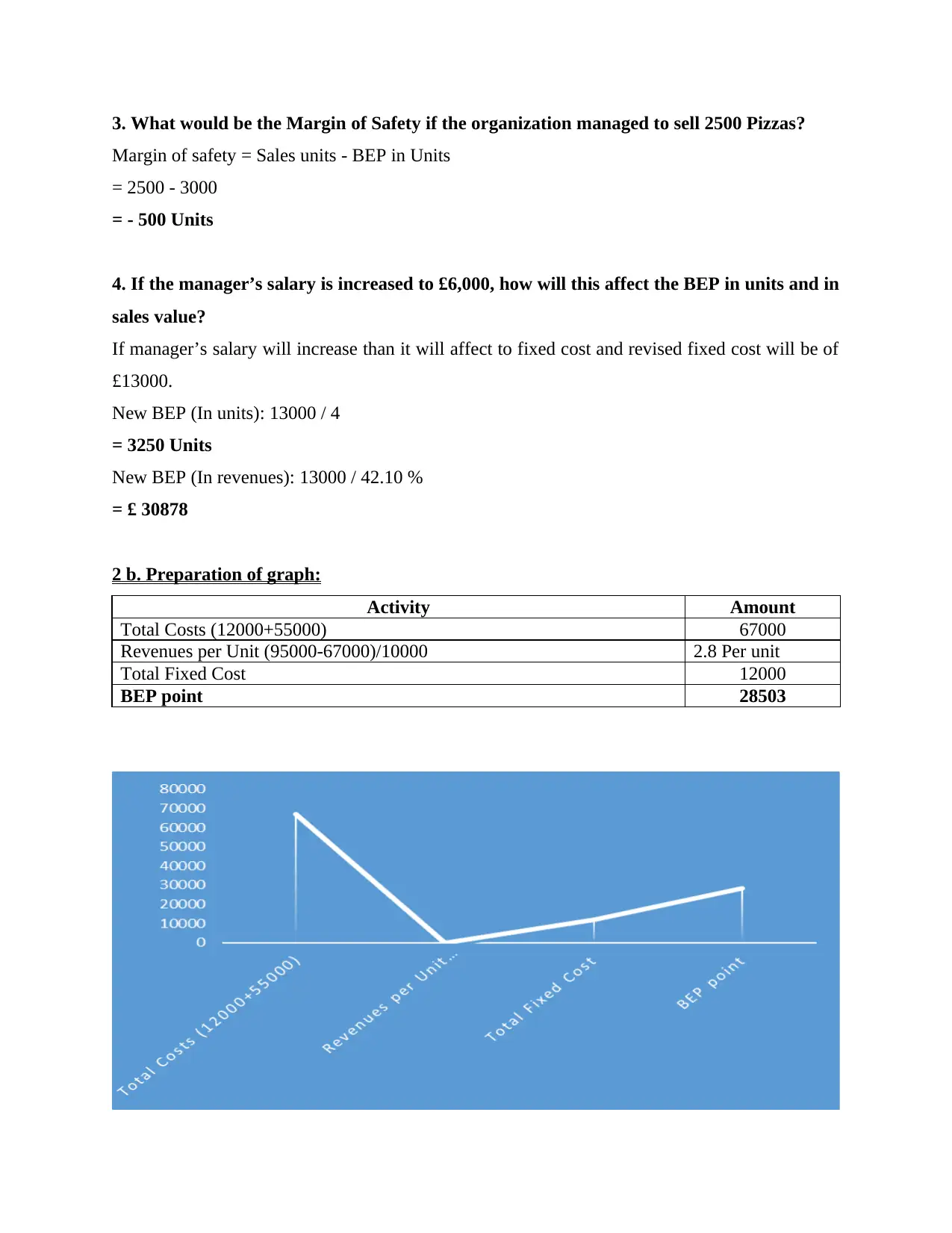

1. Identify which costs are fixed and which costs are variable.

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£ 12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£ 5.50

2. Show the Break-even point using a Break-even graph.

BEP (In units): Fixed cost / contribution per unit

Contribution per unit: Selling Price - Variable cost per unit

= 9.50 - 5.50

= 4.00

BEP: 12000 / 4

= 3000 Units

BEP (In revenues): Fixed cost / PV ratio

PV ratio: Contribution / selling price* 100

= 4/ 9.50*100

= 42.10 %

BEP (In revenues) = 12000 / 42.10 %

= £ 28503

2 a.

1. Identify which costs are fixed and which costs are variable.

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£ 12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£ 5.50

2. Show the Break-even point using a Break-even graph.

BEP (In units): Fixed cost / contribution per unit

Contribution per unit: Selling Price - Variable cost per unit

= 9.50 - 5.50

= 4.00

BEP: 12000 / 4

= 3000 Units

BEP (In revenues): Fixed cost / PV ratio

PV ratio: Contribution / selling price* 100

= 4/ 9.50*100

= 42.10 %

BEP (In revenues) = 12000 / 42.10 %

= £ 28503

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

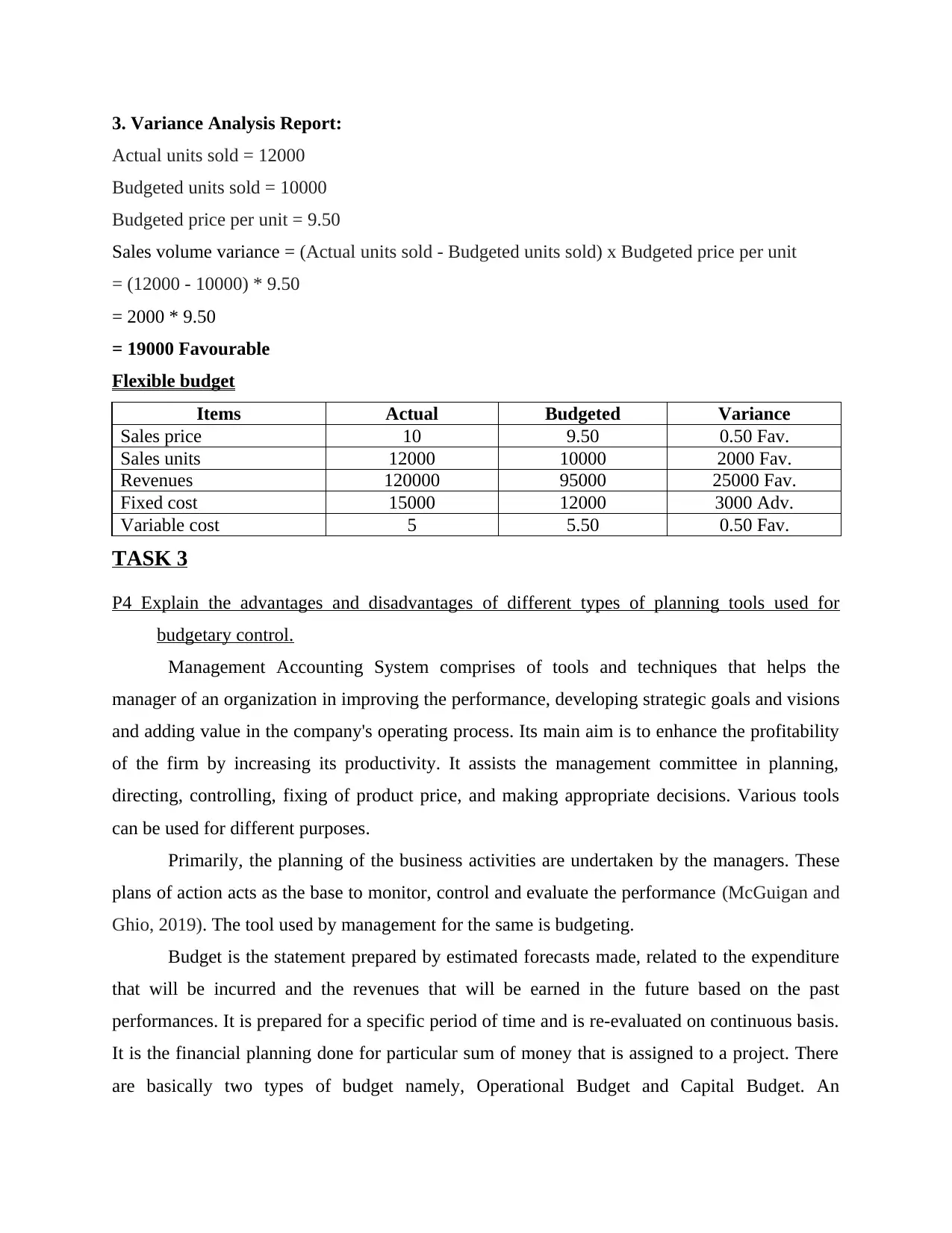

3. What would be the Margin of Safety if the organization managed to sell 2500 Pizzas?

Margin of safety = Sales units - BEP in Units

= 2500 - 3000

= - 500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000 / 4

= 3250 Units

New BEP (In revenues): 13000 / 42.10 %

= £ 30878

2 b. Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

BEP point 28503

Margin of safety = Sales units - BEP in Units

= 2500 - 3000

= - 500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000 / 4

= 3250 Units

New BEP (In revenues): 13000 / 42.10 %

= £ 30878

2 b. Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

BEP point 28503

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Variance Analysis Report:

Actual units sold = 12000

Budgeted units sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000 - 10000) * 9.50

= 2000 * 9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 0.50 Fav.

Sales units 12000 10000 2000 Fav.

Revenues 120000 95000 25000 Fav.

Fixed cost 15000 12000 3000 Adv.

Variable cost 5 5.50 0.50 Fav.

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Management Accounting System comprises of tools and techniques that helps the

manager of an organization in improving the performance, developing strategic goals and visions

and adding value in the company's operating process. Its main aim is to enhance the profitability

of the firm by increasing its productivity. It assists the management committee in planning,

directing, controlling, fixing of product price, and making appropriate decisions. Various tools

can be used for different purposes.

Primarily, the planning of the business activities are undertaken by the managers. These

plans of action acts as the base to monitor, control and evaluate the performance (McGuigan and

Ghio, 2019). The tool used by management for the same is budgeting.

Budget is the statement prepared by estimated forecasts made, related to the expenditure

that will be incurred and the revenues that will be earned in the future based on the past

performances. It is prepared for a specific period of time and is re-evaluated on continuous basis.

It is the financial planning done for particular sum of money that is assigned to a project. There

are basically two types of budget namely, Operational Budget and Capital Budget. An

Actual units sold = 12000

Budgeted units sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000 - 10000) * 9.50

= 2000 * 9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 0.50 Fav.

Sales units 12000 10000 2000 Fav.

Revenues 120000 95000 25000 Fav.

Fixed cost 15000 12000 3000 Adv.

Variable cost 5 5.50 0.50 Fav.

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Management Accounting System comprises of tools and techniques that helps the

manager of an organization in improving the performance, developing strategic goals and visions

and adding value in the company's operating process. Its main aim is to enhance the profitability

of the firm by increasing its productivity. It assists the management committee in planning,

directing, controlling, fixing of product price, and making appropriate decisions. Various tools

can be used for different purposes.

Primarily, the planning of the business activities are undertaken by the managers. These

plans of action acts as the base to monitor, control and evaluate the performance (McGuigan and

Ghio, 2019). The tool used by management for the same is budgeting.

Budget is the statement prepared by estimated forecasts made, related to the expenditure

that will be incurred and the revenues that will be earned in the future based on the past

performances. It is prepared for a specific period of time and is re-evaluated on continuous basis.

It is the financial planning done for particular sum of money that is assigned to a project. There

are basically two types of budget namely, Operational Budget and Capital Budget. An

operational budget predicts the expenses and revenues made in the operational process of the

organization for the coming financial year. Whereas the capital budget includes the income to be

earned or expenditure to be made on the long term capital investments made by the company in

the future. Variety of budgets prepared by Connect Catering services are listed as:

Cash Budget

It is the statement used for estimating the cash flows in the given tenure by the company.

It helps in determination of cash generated from the business operations and their sufficiency for

meeting business expenses. It aim is to provide an insight for the cash requirement and its

allocation and results in optimum utilization of the free available cash and cash equivalent

resources. Its purpose is to estimate the efficiency of the company in managing its regular

operations. It gives a summary of estimated revenues, operating expenses, buy or sale of assets,

settlement of debts and the excess cash available with the organization. Advantages- It prevents the overspending of the cash and provides better prospective of

allocation of the surplus free cash available (Miles, 2019). Also, it also minimizes the

debt component as the payments are made in cash.

Disadvantage- It limits or restricts the spending power of the organization as most of the

cash available is allocated to the processes of the firm, resulting in less free cash

availability. Also it is difficult to track and can be stolen easily.

Sales Budget

It is the basic component required for the preparation of the master budget and includes

expenses made for increasing the sales and the revenue generated over a particular time period.

Its aim is to determine the average forecast earnings on the basis of the historical data and the

management judgment relation to the competitors, demand of the firm's product and the

economical conditions of the environment (Pratt, 2016). It gives the estimation of the quantity of

the products the company would be able to pay and the amount of revenue that would be

generated from such sales. Advantages- It guides the organization for prescribing the targets and motivating the

employees for its achievement by working hard. It also helps in producing the appropriate

quantity of product and neither over production nor under production of goods to be

done.

organization for the coming financial year. Whereas the capital budget includes the income to be

earned or expenditure to be made on the long term capital investments made by the company in

the future. Variety of budgets prepared by Connect Catering services are listed as:

Cash Budget

It is the statement used for estimating the cash flows in the given tenure by the company.

It helps in determination of cash generated from the business operations and their sufficiency for

meeting business expenses. It aim is to provide an insight for the cash requirement and its

allocation and results in optimum utilization of the free available cash and cash equivalent

resources. Its purpose is to estimate the efficiency of the company in managing its regular

operations. It gives a summary of estimated revenues, operating expenses, buy or sale of assets,

settlement of debts and the excess cash available with the organization. Advantages- It prevents the overspending of the cash and provides better prospective of

allocation of the surplus free cash available (Miles, 2019). Also, it also minimizes the

debt component as the payments are made in cash.

Disadvantage- It limits or restricts the spending power of the organization as most of the

cash available is allocated to the processes of the firm, resulting in less free cash

availability. Also it is difficult to track and can be stolen easily.

Sales Budget

It is the basic component required for the preparation of the master budget and includes

expenses made for increasing the sales and the revenue generated over a particular time period.

Its aim is to determine the average forecast earnings on the basis of the historical data and the

management judgment relation to the competitors, demand of the firm's product and the

economical conditions of the environment (Pratt, 2016). It gives the estimation of the quantity of

the products the company would be able to pay and the amount of revenue that would be

generated from such sales. Advantages- It guides the organization for prescribing the targets and motivating the

employees for its achievement by working hard. It also helps in producing the appropriate

quantity of product and neither over production nor under production of goods to be

done.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.