Analyzing the Connection: Logistics Strategy & Financial Performance

VerifiedAdded on 2019/09/30

|9

|1360

|629

Report

AI Summary

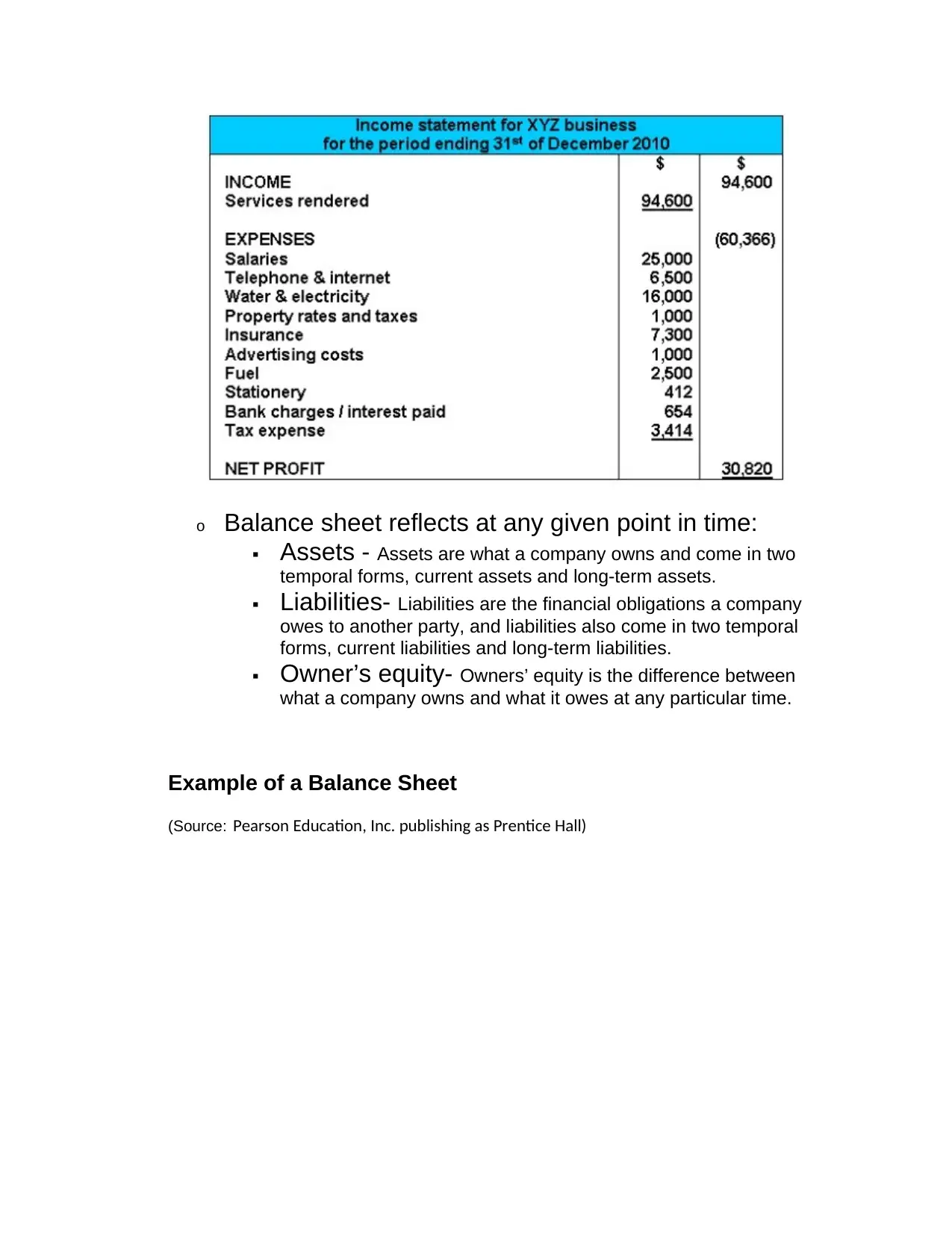

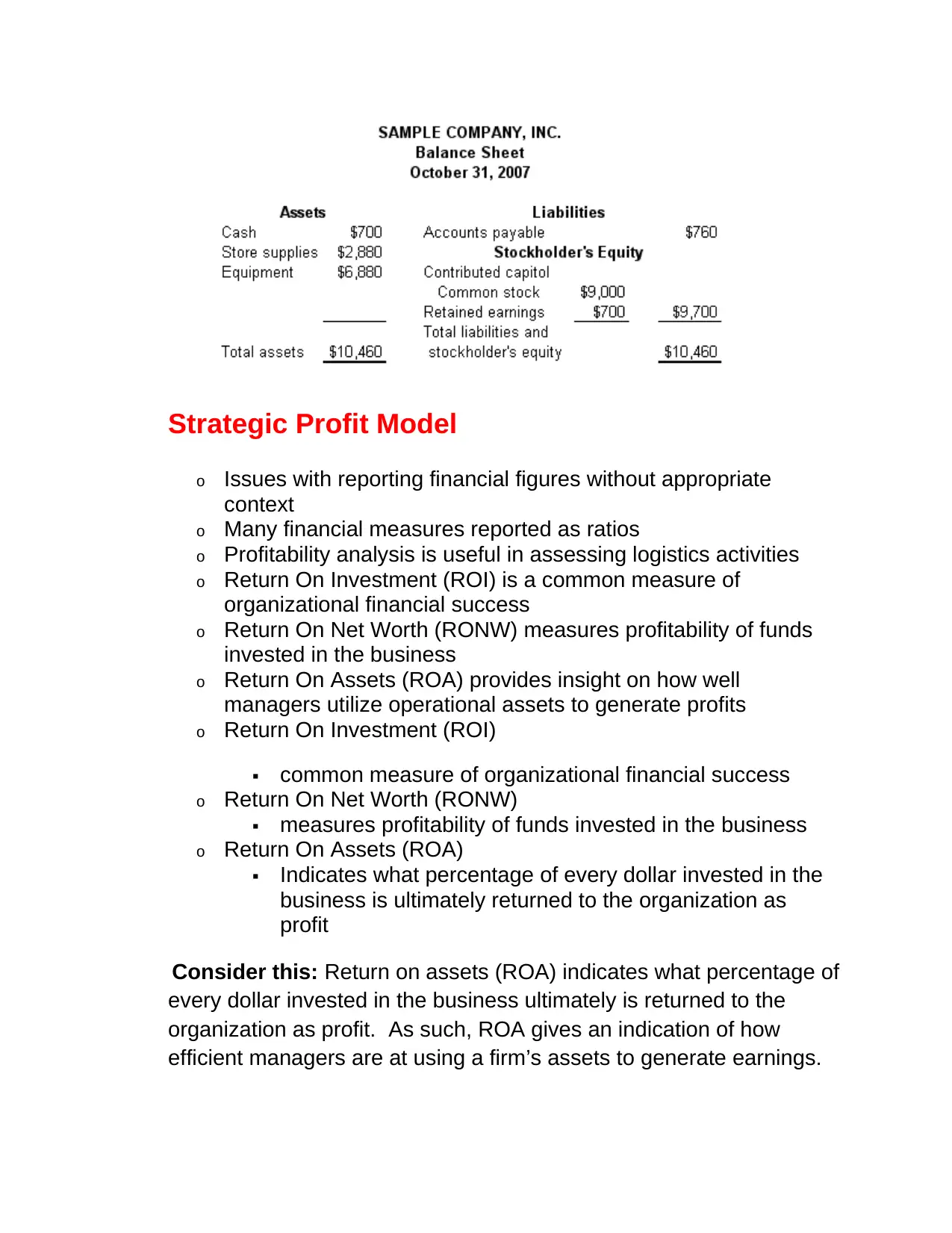

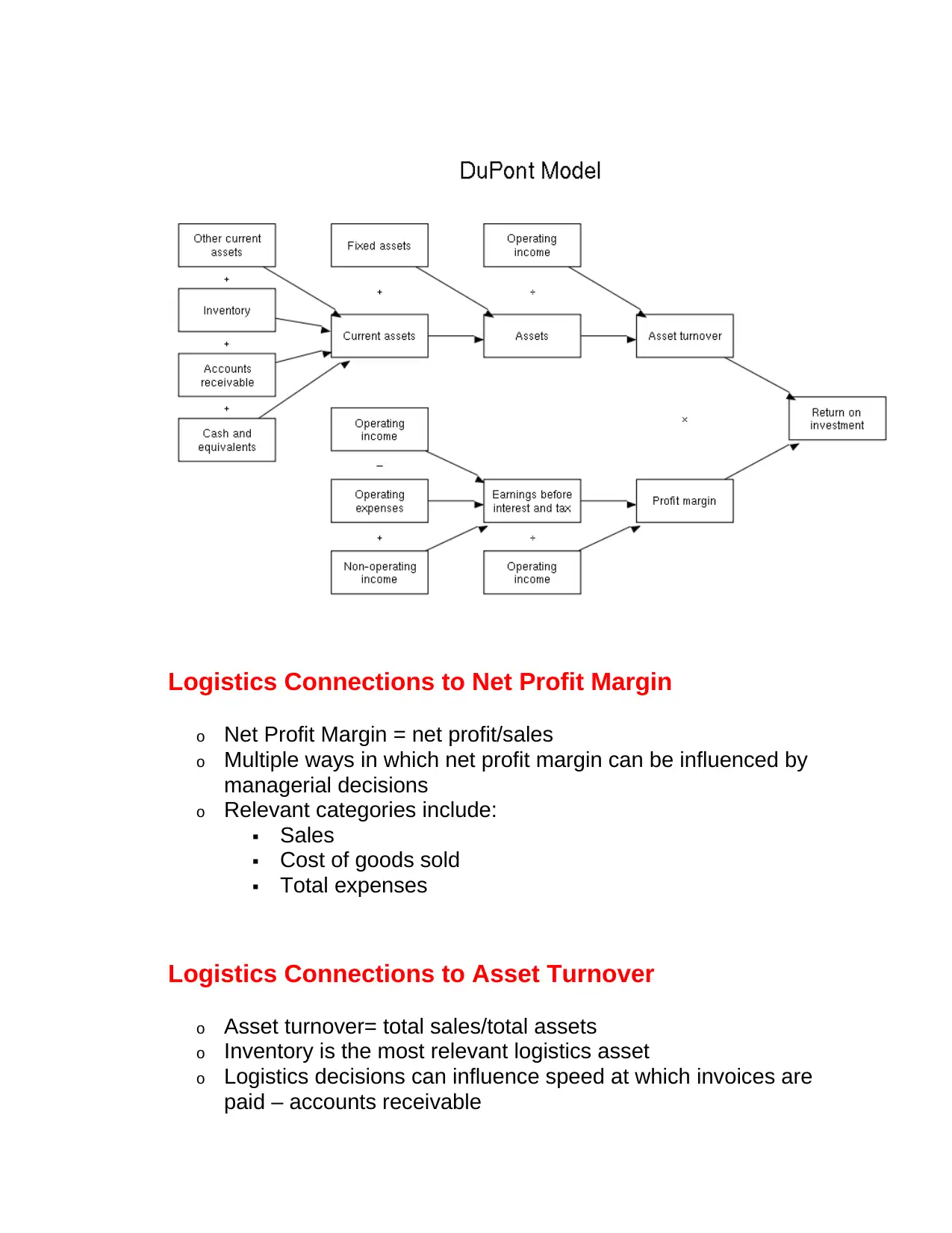

This report examines the critical link between logistics strategies and financial performance. It begins by defining the corporate, business, and functional levels of strategy, emphasizing how logistics, as a functional area, translates higher-level goals into actionable plans. The report then introduces key financial terminology, including income statements, balance sheets, and financial ratios like ROI, RONW, and ROA, highlighting their importance in assessing logistics activities. The Strategic Profit Model (SPM) is presented as a framework for analyzing the impact of logistics changes on profitability, alongside the Balanced Scorecard (BSC), which offers a more holistic approach to performance measurement. Furthermore, the report details various logistics measures across transportation, warehousing, and inventory, emphasizing the need to connect logistics capabilities to firm performance and communicate their value in financial terms. The report concludes by stressing the importance of aligning logistics strategies with overall corporate strategy and working collaboratively with other functional areas like marketing and manufacturing to achieve financial success.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.