Connectta Limited's Costing System: A Management Accounting Report

VerifiedAdded on 2022/11/17

|14

|3023

|164

Report

AI Summary

This report provides a comprehensive evaluation of the costing system and business operations of Connectta Limited, focusing on its job costing system. The analysis includes calculations for work-in-process inventory, finished goods inventory costs, and the determination of over-applied or under-applied overhead. The report explores two alternative accounting treatments for handling these overhead balances. Furthermore, it examines the deficiencies of the job costing system and highlights how an activity-based costing system could improve overhead cost allocation. The report emphasizes the benefits of activity-based costing in overcoming the limitations of traditional costing methods and making informed management decisions for future economic growth. The findings suggest that implementing activity-based costing would enable Connectta Limited to better allocate overhead costs and improve overall financial management.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Executive Summary:

This report is prepared with the aim of evaluating the costing system and business operations

conducted by Connectta Limited. The organisation is observed to follow job costing system

so that the business costs could be disclosed appropriately. It has been analysed that there are

two alternative treatments of under-applied or over-applied manufacturing overhead. The first

method would be to charge the same to the cost of sales account or it could be charged to

finished goods inventory, work in process inventory and cost of sales in the cost proportion

carried by the relevant accounts. Finally, it has been found that job costing system has certain

loopholes and by implementing activity-based costing system within the organisation,

Connectta Limited could conduct better overhead cost allocation.

Executive Summary:

This report is prepared with the aim of evaluating the costing system and business operations

conducted by Connectta Limited. The organisation is observed to follow job costing system

so that the business costs could be disclosed appropriately. It has been analysed that there are

two alternative treatments of under-applied or over-applied manufacturing overhead. The first

method would be to charge the same to the cost of sales account or it could be charged to

finished goods inventory, work in process inventory and cost of sales in the cost proportion

carried by the relevant accounts. Finally, it has been found that job costing system has certain

loopholes and by implementing activity-based costing system within the organisation,

Connectta Limited could conduct better overhead cost allocation.

2MANAGEMENT ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

1. Appropriateness of job costing system:.................................................................................3

2. Balance in work in process inventory account of Connectta Limited as at 31 December:....4

3. Costs of the chairs in finished goods inventory of Connectta Limited as at 31 December:. .5

4. Over-applied or under-applied overhead of Connectta Limited for the year:........................6

5. Two alternative accounting treatments for over-applied or under-applied overhead balances

when using job costing system:..................................................................................................7

6. Ways through which activity-based costing could overcome the deficiencies inherent in the

existing costing system:.............................................................................................................8

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

1. Appropriateness of job costing system:.................................................................................3

2. Balance in work in process inventory account of Connectta Limited as at 31 December:....4

3. Costs of the chairs in finished goods inventory of Connectta Limited as at 31 December:. .5

4. Over-applied or under-applied overhead of Connectta Limited for the year:........................6

5. Two alternative accounting treatments for over-applied or under-applied overhead balances

when using job costing system:..................................................................................................7

6. Ways through which activity-based costing could overcome the deficiencies inherent in the

existing costing system:.............................................................................................................8

Conclusion:..............................................................................................................................11

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Introduction:

This report is prepared with the aim of evaluating the costing system and business

operations conducted by Connectta Limited. The organisation is observed to follow job

costing system so that the business costs could be disclosed appropriately. The paper would

deal with analysing the costing methods available to the business and the ways through which

it is possible to make improvements. Various costs have been computed for Connectta

Limited. Along with this, the paper would be representing alternative treatments related to

overhead costs and their effect on the overall costs. The evaluation would be carried out for

over-applied and under-applied overhead costs and the way the treatment is to be made from

the viewpoint of cost accounting. The paper would ascertain the role of the activity-based

costing system and the way through which it assists the management of the organisation in

undertaking decisions for future economic growth. Finally, the report would shed light on the

merits of activity-based costing system and the ways through it overcomes the loopholes

inherent in the conventional costing system.

1. Appropriateness of job costing system:

This section has emphasised on various aspects associated with the reporting

framework of cost accounting and the framework followed on the part of Connectta Limited.

In the current market scenario, an organisation is needed to ascertain the suitable business

costs for projecting profits to be earned as well as projecting the product prices provided to

the customers (Bobryshev et al. 2015). Job costing could be defined as the system, which an

organisation uses in order to fulfil the orders made by the customers. From the business

perspective, job costing method is applied by the management of the organisation in order to

control the raw material usage. The organisations take into consideration the orders of the

customers in order to meet their overall demand. By taking into account the core activities of

Introduction:

This report is prepared with the aim of evaluating the costing system and business

operations conducted by Connectta Limited. The organisation is observed to follow job

costing system so that the business costs could be disclosed appropriately. The paper would

deal with analysing the costing methods available to the business and the ways through which

it is possible to make improvements. Various costs have been computed for Connectta

Limited. Along with this, the paper would be representing alternative treatments related to

overhead costs and their effect on the overall costs. The evaluation would be carried out for

over-applied and under-applied overhead costs and the way the treatment is to be made from

the viewpoint of cost accounting. The paper would ascertain the role of the activity-based

costing system and the way through which it assists the management of the organisation in

undertaking decisions for future economic growth. Finally, the report would shed light on the

merits of activity-based costing system and the ways through it overcomes the loopholes

inherent in the conventional costing system.

1. Appropriateness of job costing system:

This section has emphasised on various aspects associated with the reporting

framework of cost accounting and the framework followed on the part of Connectta Limited.

In the current market scenario, an organisation is needed to ascertain the suitable business

costs for projecting profits to be earned as well as projecting the product prices provided to

the customers (Bobryshev et al. 2015). Job costing could be defined as the system, which an

organisation uses in order to fulfil the orders made by the customers. From the business

perspective, job costing method is applied by the management of the organisation in order to

control the raw material usage. The organisations take into consideration the orders of the

customers in order to meet their overall demand. By taking into account the core activities of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

the organisation, there are different options available to the management about the suitable

costing method, which has to be applied based on the business operations. The job costing

method is used mainly for projecting the overall cost of the manufacturing firms and

organisations relying more on the orders of the customers in order to meet the production

needs along with generation of sales revenue from operations (Bromwich and Scapens 2016).

This technique is deemed to be suitable for those organisations operating in the

manufacturing sector and they disclose the costs in the costing reports that are developed by

following the principles of the job costing system. Different organisations are observed to be

utilising the job costing technique in order to present their business costs effectively like

manufacturing firms, hospitals and other businesses (Chenhall and Moers 2015). Thus, job

costing system is a technique of ascertaining cost for a single unit of cost, which is for a

particular job. There are certain circumstances under which job costing system is deemed to

be value for a business organisation and they are elucidated briefly as follows:

Job costing method could be used at the time an organisation is offering any special

product based on the particular need of the customer.

Another scenario where the job costing technique could be utilised is when an

organisation manufactures a variety of products that are not alike or similar (Dekker

2016).

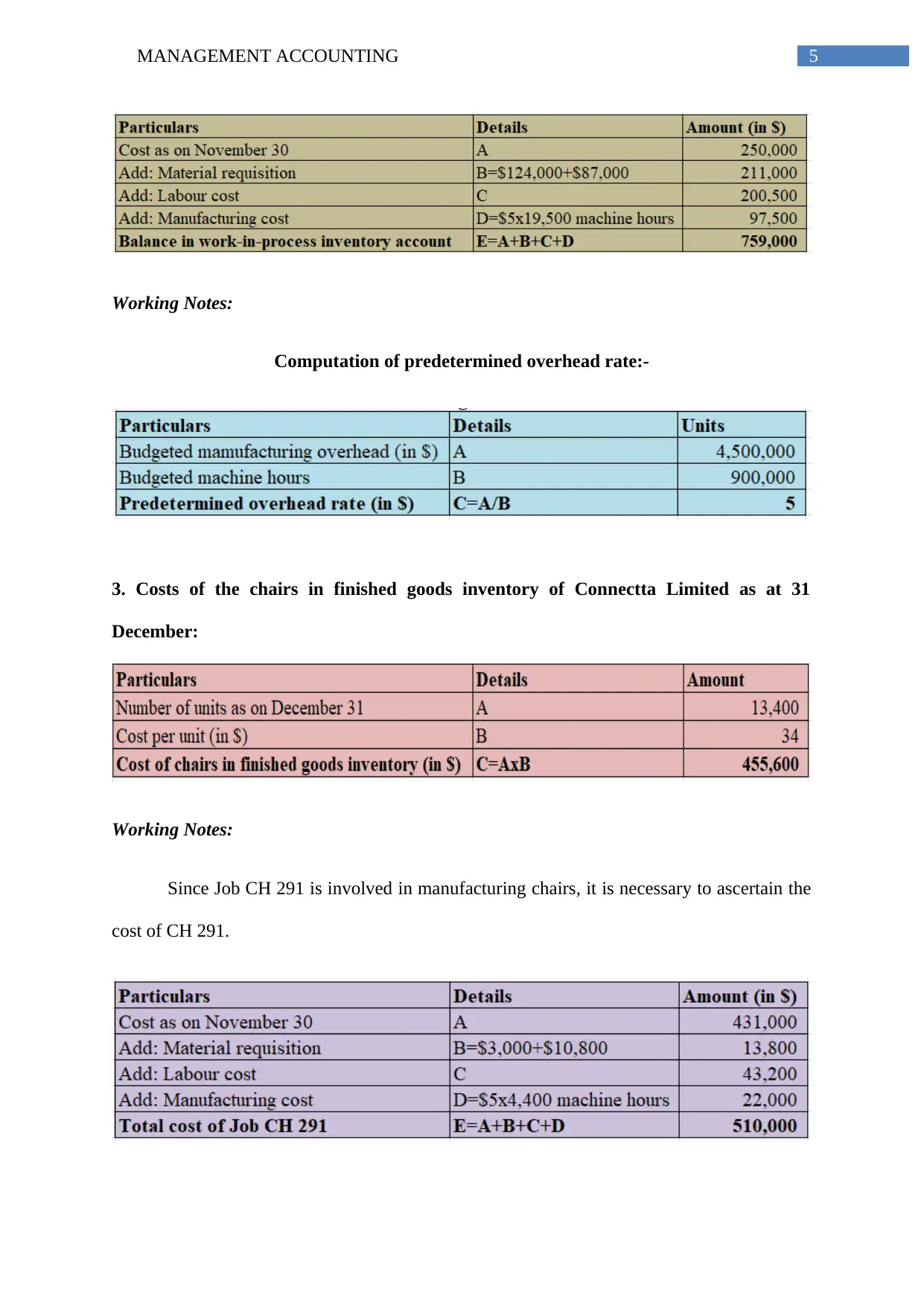

2. Balance in work in process inventory account of Connectta Limited as at 31

December:

The only job remaining in work in process inventory is Job PS 812 Printer Stands.

the organisation, there are different options available to the management about the suitable

costing method, which has to be applied based on the business operations. The job costing

method is used mainly for projecting the overall cost of the manufacturing firms and

organisations relying more on the orders of the customers in order to meet the production

needs along with generation of sales revenue from operations (Bromwich and Scapens 2016).

This technique is deemed to be suitable for those organisations operating in the

manufacturing sector and they disclose the costs in the costing reports that are developed by

following the principles of the job costing system. Different organisations are observed to be

utilising the job costing technique in order to present their business costs effectively like

manufacturing firms, hospitals and other businesses (Chenhall and Moers 2015). Thus, job

costing system is a technique of ascertaining cost for a single unit of cost, which is for a

particular job. There are certain circumstances under which job costing system is deemed to

be value for a business organisation and they are elucidated briefly as follows:

Job costing method could be used at the time an organisation is offering any special

product based on the particular need of the customer.

Another scenario where the job costing technique could be utilised is when an

organisation manufactures a variety of products that are not alike or similar (Dekker

2016).

2. Balance in work in process inventory account of Connectta Limited as at 31

December:

The only job remaining in work in process inventory is Job PS 812 Printer Stands.

5MANAGEMENT ACCOUNTING

Working Notes:

Computation of predetermined overhead rate:-

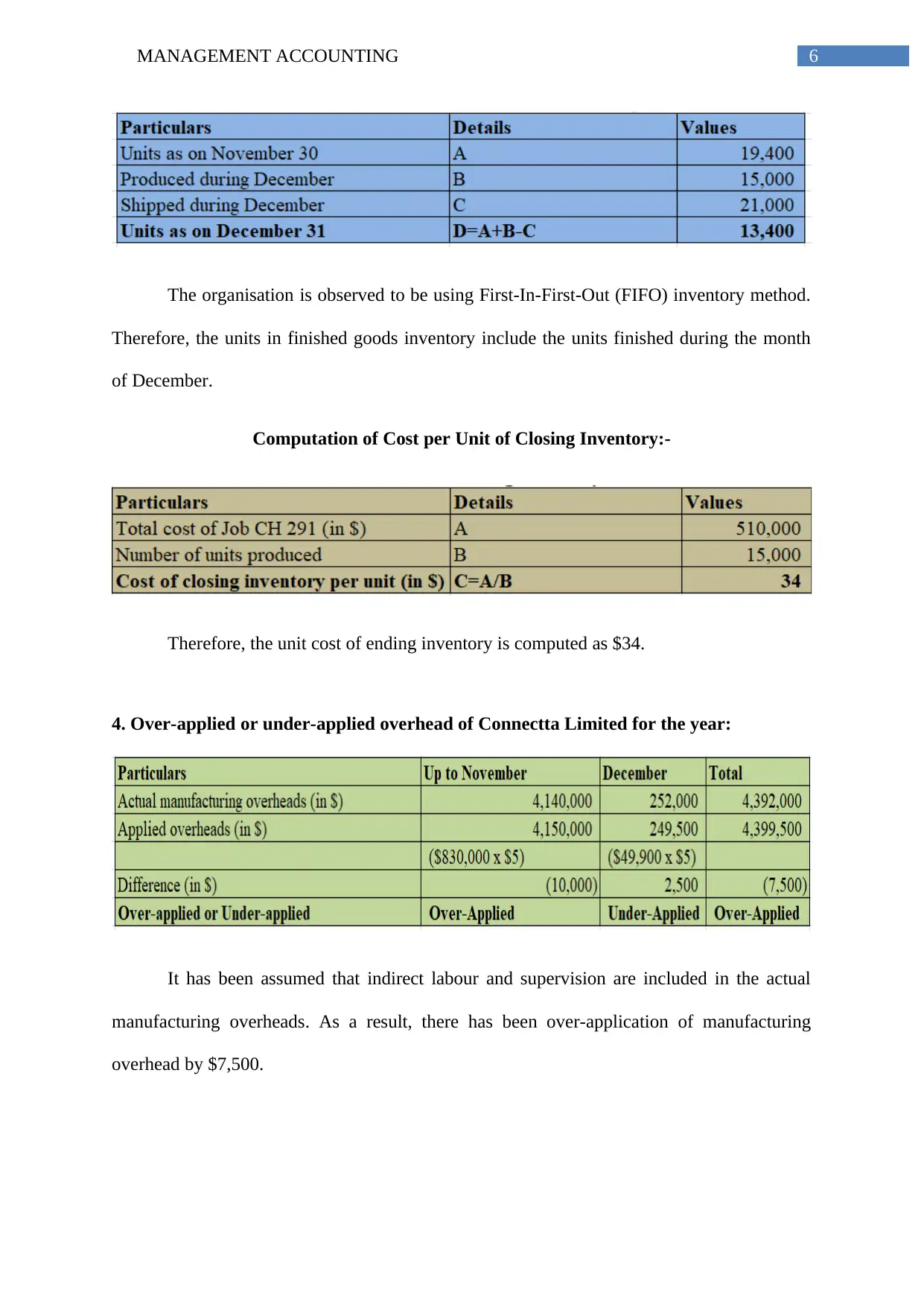

3. Costs of the chairs in finished goods inventory of Connectta Limited as at 31

December:

Working Notes:

Since Job CH 291 is involved in manufacturing chairs, it is necessary to ascertain the

cost of CH 291.

Working Notes:

Computation of predetermined overhead rate:-

3. Costs of the chairs in finished goods inventory of Connectta Limited as at 31

December:

Working Notes:

Since Job CH 291 is involved in manufacturing chairs, it is necessary to ascertain the

cost of CH 291.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

The organisation is observed to be using First-In-First-Out (FIFO) inventory method.

Therefore, the units in finished goods inventory include the units finished during the month

of December.

Computation of Cost per Unit of Closing Inventory:-

Therefore, the unit cost of ending inventory is computed as $34.

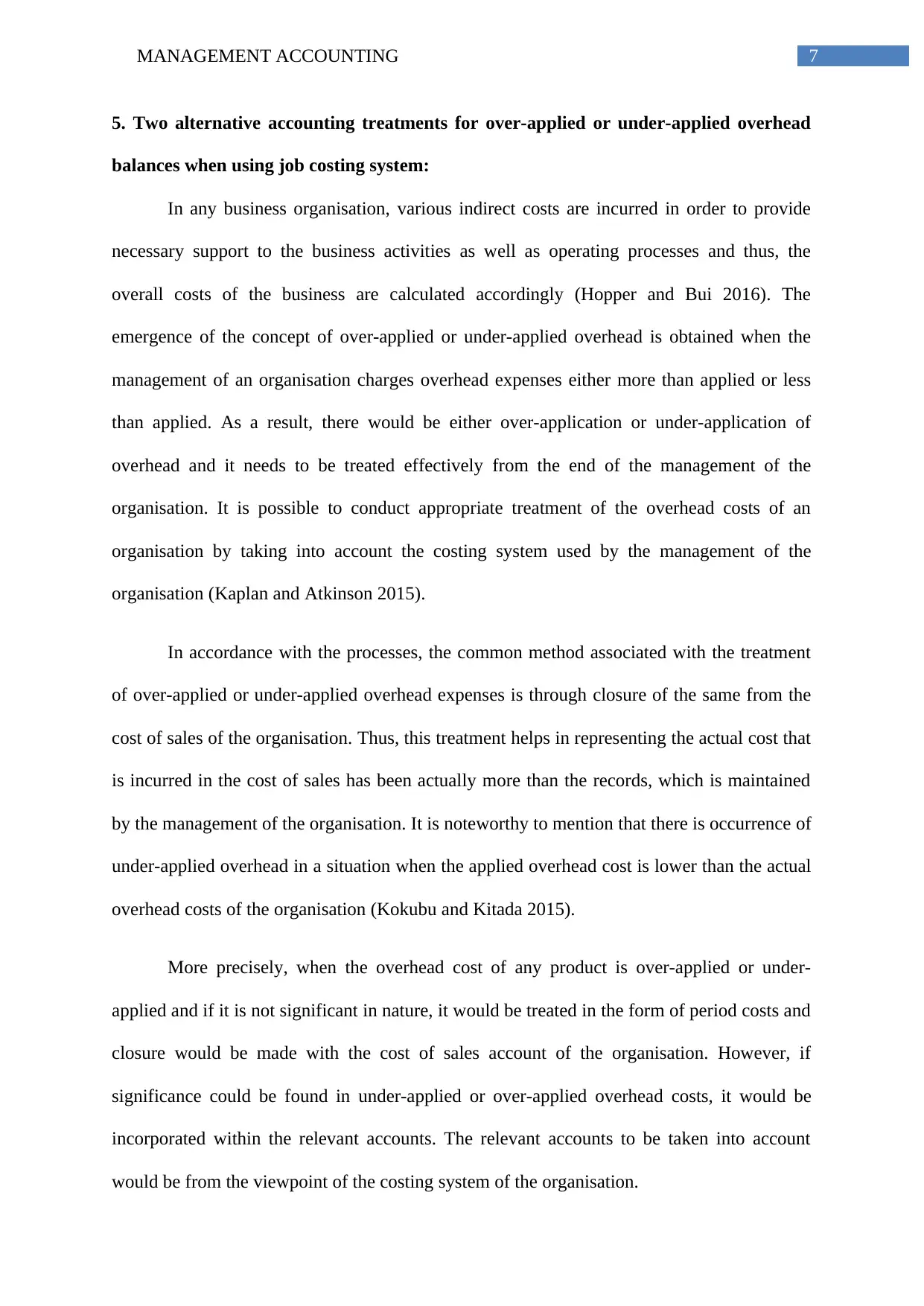

4. Over-applied or under-applied overhead of Connectta Limited for the year:

It has been assumed that indirect labour and supervision are included in the actual

manufacturing overheads. As a result, there has been over-application of manufacturing

overhead by $7,500.

The organisation is observed to be using First-In-First-Out (FIFO) inventory method.

Therefore, the units in finished goods inventory include the units finished during the month

of December.

Computation of Cost per Unit of Closing Inventory:-

Therefore, the unit cost of ending inventory is computed as $34.

4. Over-applied or under-applied overhead of Connectta Limited for the year:

It has been assumed that indirect labour and supervision are included in the actual

manufacturing overheads. As a result, there has been over-application of manufacturing

overhead by $7,500.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

5. Two alternative accounting treatments for over-applied or under-applied overhead

balances when using job costing system:

In any business organisation, various indirect costs are incurred in order to provide

necessary support to the business activities as well as operating processes and thus, the

overall costs of the business are calculated accordingly (Hopper and Bui 2016). The

emergence of the concept of over-applied or under-applied overhead is obtained when the

management of an organisation charges overhead expenses either more than applied or less

than applied. As a result, there would be either over-application or under-application of

overhead and it needs to be treated effectively from the end of the management of the

organisation. It is possible to conduct appropriate treatment of the overhead costs of an

organisation by taking into account the costing system used by the management of the

organisation (Kaplan and Atkinson 2015).

In accordance with the processes, the common method associated with the treatment

of over-applied or under-applied overhead expenses is through closure of the same from the

cost of sales of the organisation. Thus, this treatment helps in representing the actual cost that

is incurred in the cost of sales has been actually more than the records, which is maintained

by the management of the organisation. It is noteworthy to mention that there is occurrence of

under-applied overhead in a situation when the applied overhead cost is lower than the actual

overhead costs of the organisation (Kokubu and Kitada 2015).

More precisely, when the overhead cost of any product is over-applied or under-

applied and if it is not significant in nature, it would be treated in the form of period costs and

closure would be made with the cost of sales account of the organisation. However, if

significance could be found in under-applied or over-applied overhead costs, it would be

incorporated within the relevant accounts. The relevant accounts to be taken into account

would be from the viewpoint of the costing system of the organisation.

5. Two alternative accounting treatments for over-applied or under-applied overhead

balances when using job costing system:

In any business organisation, various indirect costs are incurred in order to provide

necessary support to the business activities as well as operating processes and thus, the

overall costs of the business are calculated accordingly (Hopper and Bui 2016). The

emergence of the concept of over-applied or under-applied overhead is obtained when the

management of an organisation charges overhead expenses either more than applied or less

than applied. As a result, there would be either over-application or under-application of

overhead and it needs to be treated effectively from the end of the management of the

organisation. It is possible to conduct appropriate treatment of the overhead costs of an

organisation by taking into account the costing system used by the management of the

organisation (Kaplan and Atkinson 2015).

In accordance with the processes, the common method associated with the treatment

of over-applied or under-applied overhead expenses is through closure of the same from the

cost of sales of the organisation. Thus, this treatment helps in representing the actual cost that

is incurred in the cost of sales has been actually more than the records, which is maintained

by the management of the organisation. It is noteworthy to mention that there is occurrence of

under-applied overhead in a situation when the applied overhead cost is lower than the actual

overhead costs of the organisation (Kokubu and Kitada 2015).

More precisely, when the overhead cost of any product is over-applied or under-

applied and if it is not significant in nature, it would be treated in the form of period costs and

closure would be made with the cost of sales account of the organisation. However, if

significance could be found in under-applied or over-applied overhead costs, it would be

incorporated within the relevant accounts. The relevant accounts to be taken into account

would be from the viewpoint of the costing system of the organisation.

8MANAGEMENT ACCOUNTING

In summary, it could be stated that disposal of over-applied or under-applied

manufacturing overhead could be made in two ways. The first method would be to charge the

same to the cost of sales account or it could be charged to finished goods inventory, work in

process inventory and cost of sales in the cost proportion carried by the relevant accounts

(Lavia López and Hiebl 2014). However, the ultimate treatment would be the same in case of

both the alternatives.

6. Ways through which activity-based costing could overcome the deficiencies inherent

in the existing costing system:

Activity-based costing system is an accounting method that an organisation uses for

effective identification of costs associated with business operations and the same is allocated

to the overhead costs in an appropriate manner. This system aids in recognising the

relationship among the products, costs and overhead activities manufactured by the

organisation (Messner 2016). This method is deemed to be the most popular costing

technique when it comes to cost identification, as the same could be associated with the

necessary business activities. The overhead expenses of the organisation allocate the indirect

costs suitably when compared with the traditional costing methods like job costing.

This system is used primarily by the manufacturing organisations owing to the fact

that the reliability of the cost data is enhanced and thus, an effective presentation of the

business costs could be made. As a result, the management of the organisation could

undertake sound decisions about its cost elements (Van Der Stede 2015). There are certain

ways through which activity-based costing system could overcome the deficiencies inherent

in the job costing system of Connectta Limited and they are summarised briefly as follows:

Cost allocation:

In summary, it could be stated that disposal of over-applied or under-applied

manufacturing overhead could be made in two ways. The first method would be to charge the

same to the cost of sales account or it could be charged to finished goods inventory, work in

process inventory and cost of sales in the cost proportion carried by the relevant accounts

(Lavia López and Hiebl 2014). However, the ultimate treatment would be the same in case of

both the alternatives.

6. Ways through which activity-based costing could overcome the deficiencies inherent

in the existing costing system:

Activity-based costing system is an accounting method that an organisation uses for

effective identification of costs associated with business operations and the same is allocated

to the overhead costs in an appropriate manner. This system aids in recognising the

relationship among the products, costs and overhead activities manufactured by the

organisation (Messner 2016). This method is deemed to be the most popular costing

technique when it comes to cost identification, as the same could be associated with the

necessary business activities. The overhead expenses of the organisation allocate the indirect

costs suitably when compared with the traditional costing methods like job costing.

This system is used primarily by the manufacturing organisations owing to the fact

that the reliability of the cost data is enhanced and thus, an effective presentation of the

business costs could be made. As a result, the management of the organisation could

undertake sound decisions about its cost elements (Van Der Stede 2015). There are certain

ways through which activity-based costing system could overcome the deficiencies inherent

in the job costing system of Connectta Limited and they are summarised briefly as follows:

Cost allocation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Both job costing system and activity-based costing system perform costing of a cost

object; however, there is difference in methodology. For instance, it is assumed that a job of

Connectta Limited consumes a particular amount of materials and labour, which could be

gauged exactly. Therefore, the costing of these two items could be made in a similar fashion

as in the case of job costing system like by multiplying the material consumed by the

component by the unit price of the materials along with multiplying the overall labour hours

that the component has used by the labour rate per hour (Nielsen, Mitchell and Nørreklit

2015). Moreover, there would be addition of the overhead portion of the organisation, which

has been consumed by the component.

In traditional costing system, it is made through loading a proportion of the overall

overhead expense of the firm to the component. However, in the activity-based costing

system, there is need to ascertain the actual overhead activities conducted on the component.

The overhead activities are gauged in terms of their cost drivers. On all overhead activities,

there is overall collection of the total overhead cost at the organisational level. In addition,

the cost per unit of each activity is computed by dividing the overall cost pool of overhead of

that activity by the total cost driver units utilised at the organisational level (Otley 2016).

After this, the cost driver units have to be multiplied that the component has actually used by

the rate of the cost driver with the help of which it is possible to find out the real cost of

overhead activity carried out on the component. This leads to better allocation of overhead

cost in activity-based costing system compared to the job costing system.

Two-stage allocation:

In job costing, there is allocation of overhead costs of service departments to the

production departments and as a result, the number of cost pools is limited in this system.

However, activity-based costing system develop distinct cost pools for the service activities

Both job costing system and activity-based costing system perform costing of a cost

object; however, there is difference in methodology. For instance, it is assumed that a job of

Connectta Limited consumes a particular amount of materials and labour, which could be

gauged exactly. Therefore, the costing of these two items could be made in a similar fashion

as in the case of job costing system like by multiplying the material consumed by the

component by the unit price of the materials along with multiplying the overall labour hours

that the component has used by the labour rate per hour (Nielsen, Mitchell and Nørreklit

2015). Moreover, there would be addition of the overhead portion of the organisation, which

has been consumed by the component.

In traditional costing system, it is made through loading a proportion of the overall

overhead expense of the firm to the component. However, in the activity-based costing

system, there is need to ascertain the actual overhead activities conducted on the component.

The overhead activities are gauged in terms of their cost drivers. On all overhead activities,

there is overall collection of the total overhead cost at the organisational level. In addition,

the cost per unit of each activity is computed by dividing the overall cost pool of overhead of

that activity by the total cost driver units utilised at the organisational level (Otley 2016).

After this, the cost driver units have to be multiplied that the component has actually used by

the rate of the cost driver with the help of which it is possible to find out the real cost of

overhead activity carried out on the component. This leads to better allocation of overhead

cost in activity-based costing system compared to the job costing system.

Two-stage allocation:

In job costing, there is allocation of overhead costs of service departments to the

production departments and as a result, the number of cost pools is limited in this system.

However, activity-based costing system develop distinct cost pools for the service activities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

and overhead expenses of service activities are allocated directly to the particular products

through the application of the cost driver rates (Quattrone 2016). Therefore, activity-based

costing system eradicates the need of allocating or reapportioning overheads related to the

service departments.

Use of historical costs:

There is difference in historical orientation between job costing system and activity-

based costing system. It is usual for an organisation to utilise the actual historical cost in

order to develop the standards of manufacturing cost (Senftlechner and Hiebl 2015). These

costs generally take into account duplication, rework, inefficiency, redundancy and waste.

The acceptance of historical costs and representing such costs on standards do not support

continual enhancement. In a competitive scenario, in which pro-activeness could be seen

among the competitors in waste elimination and activity enhancements, it is possible for an

organisation to go out of its standards so that its standards could be met effectively (Shields

2015).

Despite the fact that the computation of activity-based costs are made with the help of

historical resource costs, difference in orientation could be observed with the job costing

system. As mentioned by Tappura et al. (2015), activity-based costing system is more

concerned regarding the competitive positions in future and it utilises historical cost only in

the form of a baseline for enhancement in business activities and operations.

Therefore, by considering all the above-discussed aspects, it would be possible for

Connectta Limited to overcome the loopholes in its existing job costing system through the

implementation of the modern activity-based costing within the organisation.

and overhead expenses of service activities are allocated directly to the particular products

through the application of the cost driver rates (Quattrone 2016). Therefore, activity-based

costing system eradicates the need of allocating or reapportioning overheads related to the

service departments.

Use of historical costs:

There is difference in historical orientation between job costing system and activity-

based costing system. It is usual for an organisation to utilise the actual historical cost in

order to develop the standards of manufacturing cost (Senftlechner and Hiebl 2015). These

costs generally take into account duplication, rework, inefficiency, redundancy and waste.

The acceptance of historical costs and representing such costs on standards do not support

continual enhancement. In a competitive scenario, in which pro-activeness could be seen

among the competitors in waste elimination and activity enhancements, it is possible for an

organisation to go out of its standards so that its standards could be met effectively (Shields

2015).

Despite the fact that the computation of activity-based costs are made with the help of

historical resource costs, difference in orientation could be observed with the job costing

system. As mentioned by Tappura et al. (2015), activity-based costing system is more

concerned regarding the competitive positions in future and it utilises historical cost only in

the form of a baseline for enhancement in business activities and operations.

Therefore, by considering all the above-discussed aspects, it would be possible for

Connectta Limited to overcome the loopholes in its existing job costing system through the

implementation of the modern activity-based costing within the organisation.

11MANAGEMENT ACCOUNTING

Conclusion:

Based on the above analysis, it is apparent that job costing method could be used at

the time an organisation is offering any special product based on the particular need of the

customer. Different cost calculations of the job costing system in relation to Connectta

Limited have been made. In addition, it has been analysed that there are two alternative

treatments of under-applied or over-applied manufacturing overhead. The first method would

be to charge the same to the cost of sales account or it could be charged to finished goods

inventory, work in process inventory and cost of sales in the cost proportion carried by the

relevant accounts. Finally, it has been found that job costing system has certain loopholes and

by implementing activity-based costing system within the organisation, Connectta Limited

could conduct better overhead cost allocation.

Conclusion:

Based on the above analysis, it is apparent that job costing method could be used at

the time an organisation is offering any special product based on the particular need of the

customer. Different cost calculations of the job costing system in relation to Connectta

Limited have been made. In addition, it has been analysed that there are two alternative

treatments of under-applied or over-applied manufacturing overhead. The first method would

be to charge the same to the cost of sales account or it could be charged to finished goods

inventory, work in process inventory and cost of sales in the cost proportion carried by the

relevant accounts. Finally, it has been found that job costing system has certain loopholes and

by implementing activity-based costing system within the organisation, Connectta Limited

could conduct better overhead cost allocation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.