Comparative Analysis: Job Costing and ABC in Manufacturing Context

VerifiedAdded on 2023/03/23

|14

|3127

|77

Case Study

AI Summary

This case study provides a comprehensive analysis of job costing and activity-based costing (ABC) methods, primarily focusing on a manufacturing company's production processes. It begins by introducing the importance of accurate pricing in manufacturing and highlights the limitations of traditional costing methods. The paper then delves into the specifics of job costing, including its application in scenarios where products or services are customized. It discusses the allocation of manufacturing overhead and potential difficulties in this process. The case study provides detailed calculations for work-in-progress inventory, finished goods inventory, and cost of production. It also addresses the treatment of over-applied or under-applied overheads, presenting two alternative accounting treatments. Finally, the paper explores how activity-based costing can overcome the deficiencies of traditional job costing by dividing production into diverse activities and allocating expenses based on the cost of those activities. The analysis emphasizes the importance of accurate cost allocation for effective pricing strategies.

Management of Accounting Problem

0| P a g e

0| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The primary aim of the paper is to develop the view regarding the concept of job costing as well

as the activity-based costing from both the theoretical along with the practical aspect. The case

study shows that the management is included with the vital formation of the production process

which has been used for the calculation of the cost as well as the quantity within the paper for the

end of 31st December. The paper eventually evaluates the aspects of ABC costing than job

costing. The method, as well as the advantage of job costing, is effectively discussed within the

paper.

1| P a g e

The primary aim of the paper is to develop the view regarding the concept of job costing as well

as the activity-based costing from both the theoretical along with the practical aspect. The case

study shows that the management is included with the vital formation of the production process

which has been used for the calculation of the cost as well as the quantity within the paper for the

end of 31st December. The paper eventually evaluates the aspects of ABC costing than job

costing. The method, as well as the advantage of job costing, is effectively discussed within the

paper.

1| P a g e

Table of Contents

Introduction.................................................................................................................................................3

Job costing method......................................................................................................................................3

Balance within the work in the progress inventory account.........................................................................4

Cost of the chairs within the finished goods inventory................................................................................5

Over-applied or the under-applied overheads..............................................................................................7

Two alternative accounting treatments........................................................................................................8

The ways of overcoming the deficiencies by activity-based costing............................................................8

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

2| P a g e

Introduction.................................................................................................................................................3

Job costing method......................................................................................................................................3

Balance within the work in the progress inventory account.........................................................................4

Cost of the chairs within the finished goods inventory................................................................................5

Over-applied or the under-applied overheads..............................................................................................7

Two alternative accounting treatments........................................................................................................8

The ways of overcoming the deficiencies by activity-based costing............................................................8

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

2| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The manufacturing organisation in recent years has developed their understanding and their

value in the field of management accounting. For this type of firm, it is highly essential that they

ensure the two pricing process attached to the particular product and the services are accurate

and even relevant. The wrong pricing will have a negative impact on the business. It is the fact

that assigning the price to the product or the service within the organisation can be effectively

done with the help of job costing method. This needs to be utilised only under some serious or

certain circumstances within the firm. The method of job costing deal with the cost of production

within the organisation. The primary objective of the paper is to evaluate the job costing method

as well as provide the calculation for the overall cost of production along with the finished

goods.

Job costing method

The job costing method is highly essential for the calculation of the associated cost with the

material labour as well as the indirect expense within the particular job that has been executed by

the company. In the world, numerous companies provide manufacturing goods as well as the

service to the customers according to the demand of the customers. For example; the software

that could be customized is provided by the IT firm that is eventually based on the specific needs

along with the requirement of the firm rather than by providing the similar service to their each

of the consumers within the market (Mu, Jiang, and Leng, 2017). In this scenario, it can be seen

that the traditional costing method is not appropriate as within the traditional method the entire

cost has been calculated together as well as distributed among the manufacturing of the products

in an equal way. This costing method is not appropriate for the scenario as the product along

with the services can be customized, and even the customers are taking the diverse service from

the company (Oseifuah, 2014). There is a high probability that the firm management can even

charge the lower selling price as it is effective compared to the value from the one customers as

well as the charge can be more from another customer because of the application of traditional

costing method within the business process.

It can be critically viewed that the job costing method is effectively utilised within the business

that eventually divide their production procedure that also based on the diverse job activities. It

3| P a g e

The manufacturing organisation in recent years has developed their understanding and their

value in the field of management accounting. For this type of firm, it is highly essential that they

ensure the two pricing process attached to the particular product and the services are accurate

and even relevant. The wrong pricing will have a negative impact on the business. It is the fact

that assigning the price to the product or the service within the organisation can be effectively

done with the help of job costing method. This needs to be utilised only under some serious or

certain circumstances within the firm. The method of job costing deal with the cost of production

within the organisation. The primary objective of the paper is to evaluate the job costing method

as well as provide the calculation for the overall cost of production along with the finished

goods.

Job costing method

The job costing method is highly essential for the calculation of the associated cost with the

material labour as well as the indirect expense within the particular job that has been executed by

the company. In the world, numerous companies provide manufacturing goods as well as the

service to the customers according to the demand of the customers. For example; the software

that could be customized is provided by the IT firm that is eventually based on the specific needs

along with the requirement of the firm rather than by providing the similar service to their each

of the consumers within the market (Mu, Jiang, and Leng, 2017). In this scenario, it can be seen

that the traditional costing method is not appropriate as within the traditional method the entire

cost has been calculated together as well as distributed among the manufacturing of the products

in an equal way. This costing method is not appropriate for the scenario as the product along

with the services can be customized, and even the customers are taking the diverse service from

the company (Oseifuah, 2014). There is a high probability that the firm management can even

charge the lower selling price as it is effective compared to the value from the one customers as

well as the charge can be more from another customer because of the application of traditional

costing method within the business process.

It can be critically viewed that the job costing method is effectively utilised within the business

that eventually divide their production procedure that also based on the diverse job activities. It

3| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will allow the business to increase the accuracy of the pricing strategy that has been developed

by the firm (Pleis, 2016). From the scenario, it is clear that Connectta has effectively divided

their products along with the service in the two diver job. The company has effectively

categorized their production procedure as per the chair manufacturing then the computer caddy

manufacturing as well as the desk and the printer stand. The use of job costing within the

business process is highly essential for developing the value of the business activity.

The cost that is associated with the purchased part then the material as well as the labour that can

be segmented easily based on labour as well as material that has been used for the production in

a particular job (Akhavan, Ward, and Bozic, 2016). The primary difficulty of this scenario is that

the allocation of the manufacturing overhead. The manufacturing overhead is effectively

incurred within the firm in term of the production in every sector of the product as well as

service. It is highly essential that the appropriate allocation method for the manufacturing

overhead regarding the pricing strategy (Sears, and Angilletta Jr, 2015). If the production

procedure also has suitable machine power to maintain its activity in term of the business

process. Then also in the production process, the machine intensive along with the

manufacturing overhead needs to be divided that also on the basis of the machine power

(Namazi, 2016). On the other hand, it can also be seen that the production procedure within the

labour intensive than the labour hours is effectively utilised within each of the jobs.

4| P a g e

by the firm (Pleis, 2016). From the scenario, it is clear that Connectta has effectively divided

their products along with the service in the two diver job. The company has effectively

categorized their production procedure as per the chair manufacturing then the computer caddy

manufacturing as well as the desk and the printer stand. The use of job costing within the

business process is highly essential for developing the value of the business activity.

The cost that is associated with the purchased part then the material as well as the labour that can

be segmented easily based on labour as well as material that has been used for the production in

a particular job (Akhavan, Ward, and Bozic, 2016). The primary difficulty of this scenario is that

the allocation of the manufacturing overhead. The manufacturing overhead is effectively

incurred within the firm in term of the production in every sector of the product as well as

service. It is highly essential that the appropriate allocation method for the manufacturing

overhead regarding the pricing strategy (Sears, and Angilletta Jr, 2015). If the production

procedure also has suitable machine power to maintain its activity in term of the business

process. Then also in the production process, the machine intensive along with the

manufacturing overhead needs to be divided that also on the basis of the machine power

(Namazi, 2016). On the other hand, it can also be seen that the production procedure within the

labour intensive than the labour hours is effectively utilised within each of the jobs.

4| P a g e

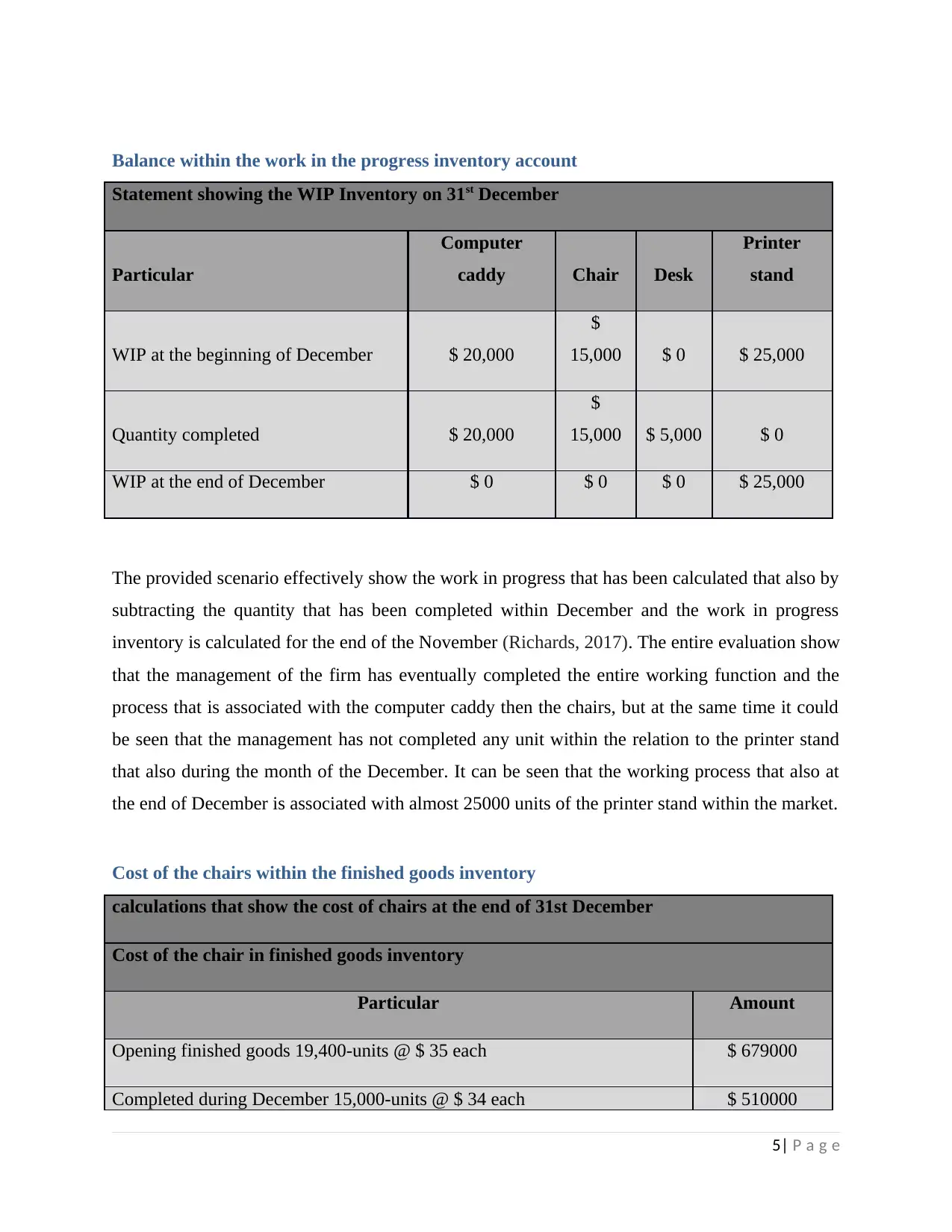

Balance within the work in the progress inventory account

Statement showing the WIP Inventory on 31st December

Particular

Computer

caddy Chair Desk

Printer

stand

WIP at the beginning of December $ 20,000

$

15,000 $ 0 $ 25,000

Quantity completed $ 20,000

$

15,000 $ 5,000 $ 0

WIP at the end of December $ 0 $ 0 $ 0 $ 25,000

The provided scenario effectively show the work in progress that has been calculated that also by

subtracting the quantity that has been completed within December and the work in progress

inventory is calculated for the end of the November (Richards, 2017). The entire evaluation show

that the management of the firm has eventually completed the entire working function and the

process that is associated with the computer caddy then the chairs, but at the same time it could

be seen that the management has not completed any unit within the relation to the printer stand

that also during the month of the December. It can be seen that the working process that also at

the end of December is associated with almost 25000 units of the printer stand within the market.

Cost of the chairs within the finished goods inventory

calculations that show the cost of chairs at the end of 31st December

Cost of the chair in finished goods inventory

Particular Amount

Opening finished goods 19,400-units @ $ 35 each $ 679000

Completed during December 15,000-units @ $ 34 each $ 510000

5| P a g e

Statement showing the WIP Inventory on 31st December

Particular

Computer

caddy Chair Desk

Printer

stand

WIP at the beginning of December $ 20,000

$

15,000 $ 0 $ 25,000

Quantity completed $ 20,000

$

15,000 $ 5,000 $ 0

WIP at the end of December $ 0 $ 0 $ 0 $ 25,000

The provided scenario effectively show the work in progress that has been calculated that also by

subtracting the quantity that has been completed within December and the work in progress

inventory is calculated for the end of the November (Richards, 2017). The entire evaluation show

that the management of the firm has eventually completed the entire working function and the

process that is associated with the computer caddy then the chairs, but at the same time it could

be seen that the management has not completed any unit within the relation to the printer stand

that also during the month of the December. It can be seen that the working process that also at

the end of December is associated with almost 25000 units of the printer stand within the market.

Cost of the chairs within the finished goods inventory

calculations that show the cost of chairs at the end of 31st December

Cost of the chair in finished goods inventory

Particular Amount

Opening finished goods 19,400-units @ $ 35 each $ 679000

Completed during December 15,000-units @ $ 34 each $ 510000

5| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

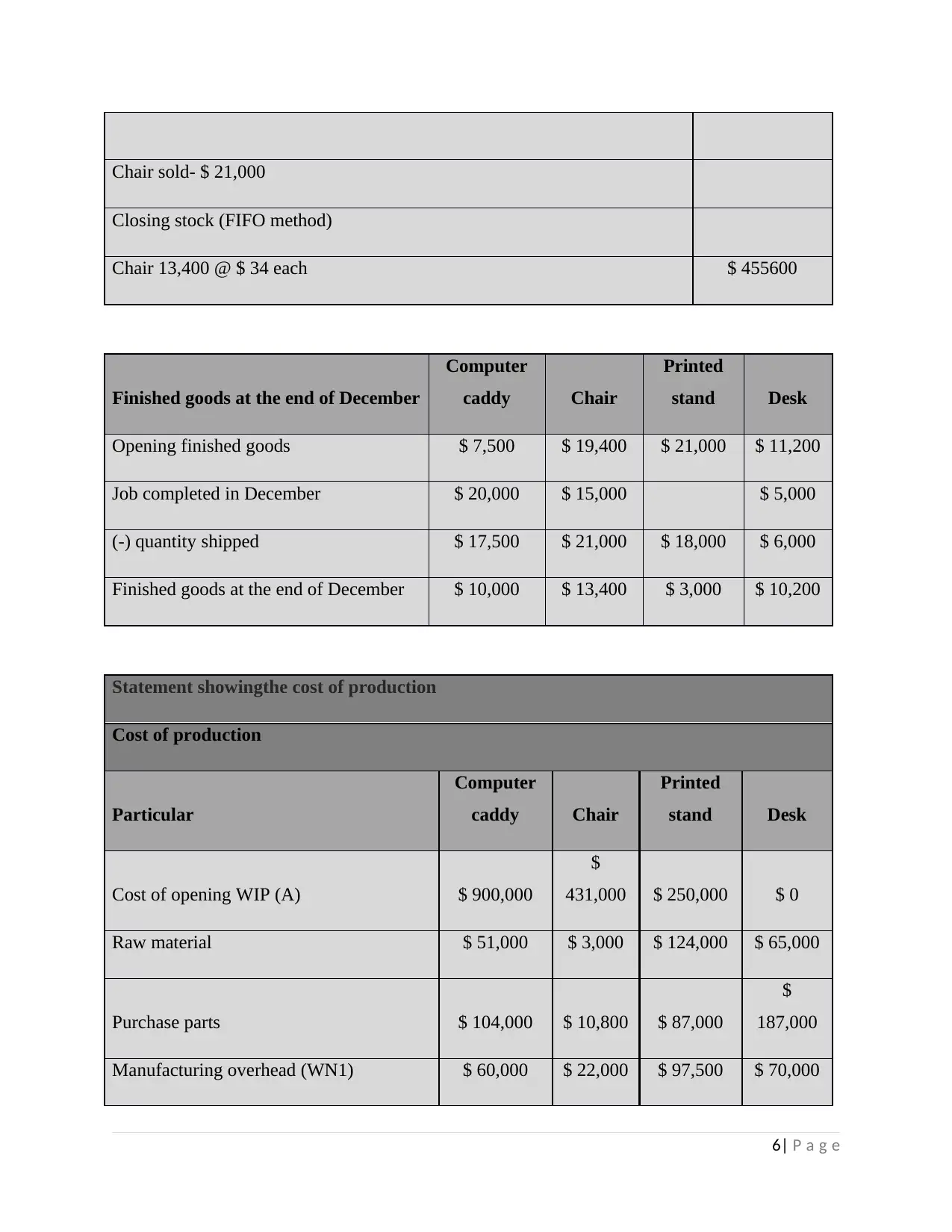

Chair sold- $ 21,000

Closing stock (FIFO method)

Chair 13,400 @ $ 34 each $ 455600

Finished goods at the end of December

Computer

caddy Chair

Printed

stand Desk

Opening finished goods $ 7,500 $ 19,400 $ 21,000 $ 11,200

Job completed in December $ 20,000 $ 15,000 $ 5,000

(-) quantity shipped $ 17,500 $ 21,000 $ 18,000 $ 6,000

Finished goods at the end of December $ 10,000 $ 13,400 $ 3,000 $ 10,200

Statement showingthe cost of production

Cost of production

Particular

Computer

caddy Chair

Printed

stand Desk

Cost of opening WIP (A) $ 900,000

$

431,000 $ 250,000 $ 0

Raw material $ 51,000 $ 3,000 $ 124,000 $ 65,000

Purchase parts $ 104,000 $ 10,800 $ 87,000

$

187,000

Manufacturing overhead (WN1) $ 60,000 $ 22,000 $ 97,500 $ 70,000

6| P a g e

Closing stock (FIFO method)

Chair 13,400 @ $ 34 each $ 455600

Finished goods at the end of December

Computer

caddy Chair

Printed

stand Desk

Opening finished goods $ 7,500 $ 19,400 $ 21,000 $ 11,200

Job completed in December $ 20,000 $ 15,000 $ 5,000

(-) quantity shipped $ 17,500 $ 21,000 $ 18,000 $ 6,000

Finished goods at the end of December $ 10,000 $ 13,400 $ 3,000 $ 10,200

Statement showingthe cost of production

Cost of production

Particular

Computer

caddy Chair

Printed

stand Desk

Cost of opening WIP (A) $ 900,000

$

431,000 $ 250,000 $ 0

Raw material $ 51,000 $ 3,000 $ 124,000 $ 65,000

Purchase parts $ 104,000 $ 10,800 $ 87,000

$

187,000

Manufacturing overhead (WN1) $ 60,000 $ 22,000 $ 97,500 $ 70,000

6| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

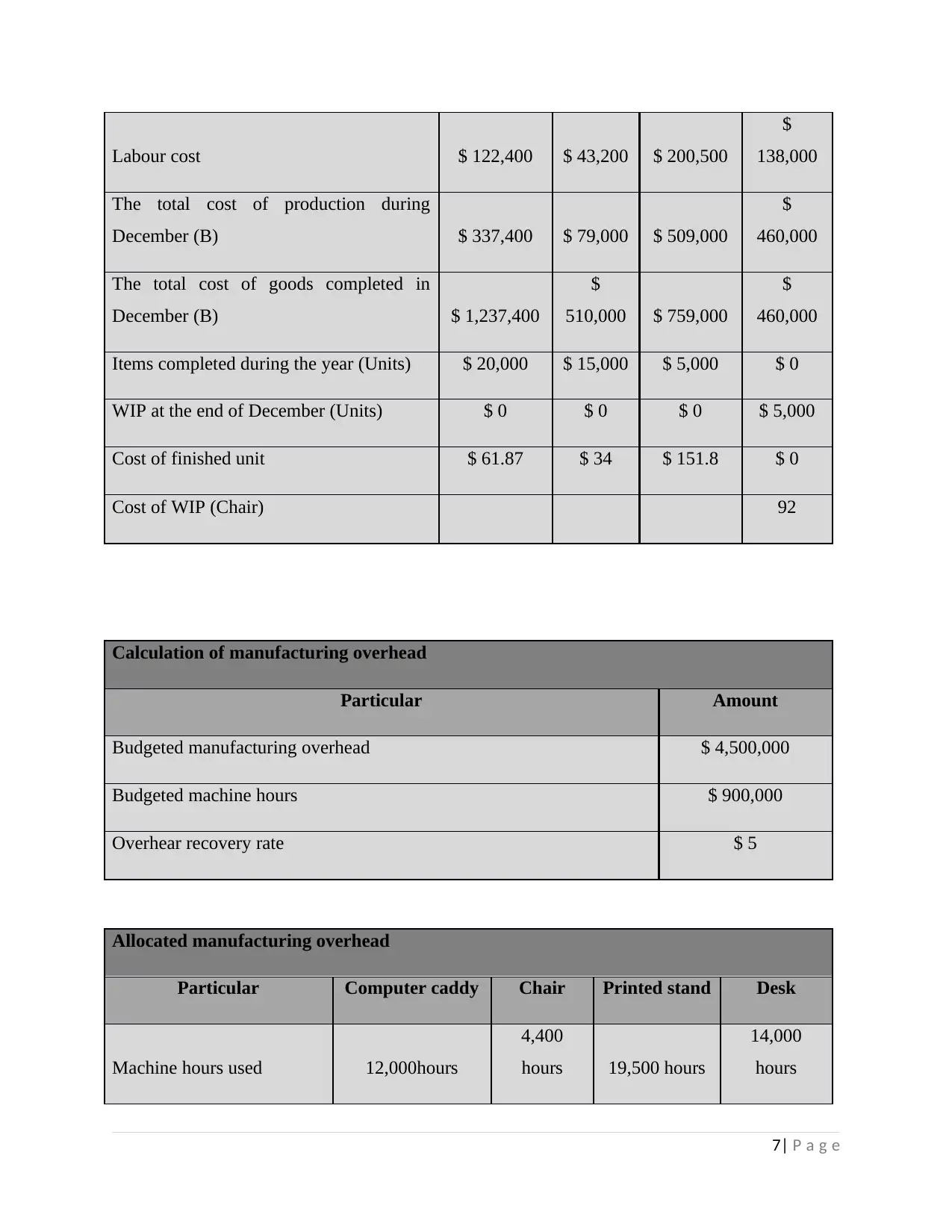

Labour cost $ 122,400 $ 43,200 $ 200,500

$

138,000

The total cost of production during

December (B) $ 337,400 $ 79,000 $ 509,000

$

460,000

The total cost of goods completed in

December (B) $ 1,237,400

$

510,000 $ 759,000

$

460,000

Items completed during the year (Units) $ 20,000 $ 15,000 $ 5,000 $ 0

WIP at the end of December (Units) $ 0 $ 0 $ 0 $ 5,000

Cost of finished unit $ 61.87 $ 34 $ 151.8 $ 0

Cost of WIP (Chair) 92

Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing overhead $ 4,500,000

Budgeted machine hours $ 900,000

Overhear recovery rate $ 5

Allocated manufacturing overhead

Particular Computer caddy Chair Printed stand Desk

Machine hours used 12,000hours

4,400

hours 19,500 hours

14,000

hours

7| P a g e

$

138,000

The total cost of production during

December (B) $ 337,400 $ 79,000 $ 509,000

$

460,000

The total cost of goods completed in

December (B) $ 1,237,400

$

510,000 $ 759,000

$

460,000

Items completed during the year (Units) $ 20,000 $ 15,000 $ 5,000 $ 0

WIP at the end of December (Units) $ 0 $ 0 $ 0 $ 5,000

Cost of finished unit $ 61.87 $ 34 $ 151.8 $ 0

Cost of WIP (Chair) 92

Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing overhead $ 4,500,000

Budgeted machine hours $ 900,000

Overhear recovery rate $ 5

Allocated manufacturing overhead

Particular Computer caddy Chair Printed stand Desk

Machine hours used 12,000hours

4,400

hours 19,500 hours

14,000

hours

7| P a g e

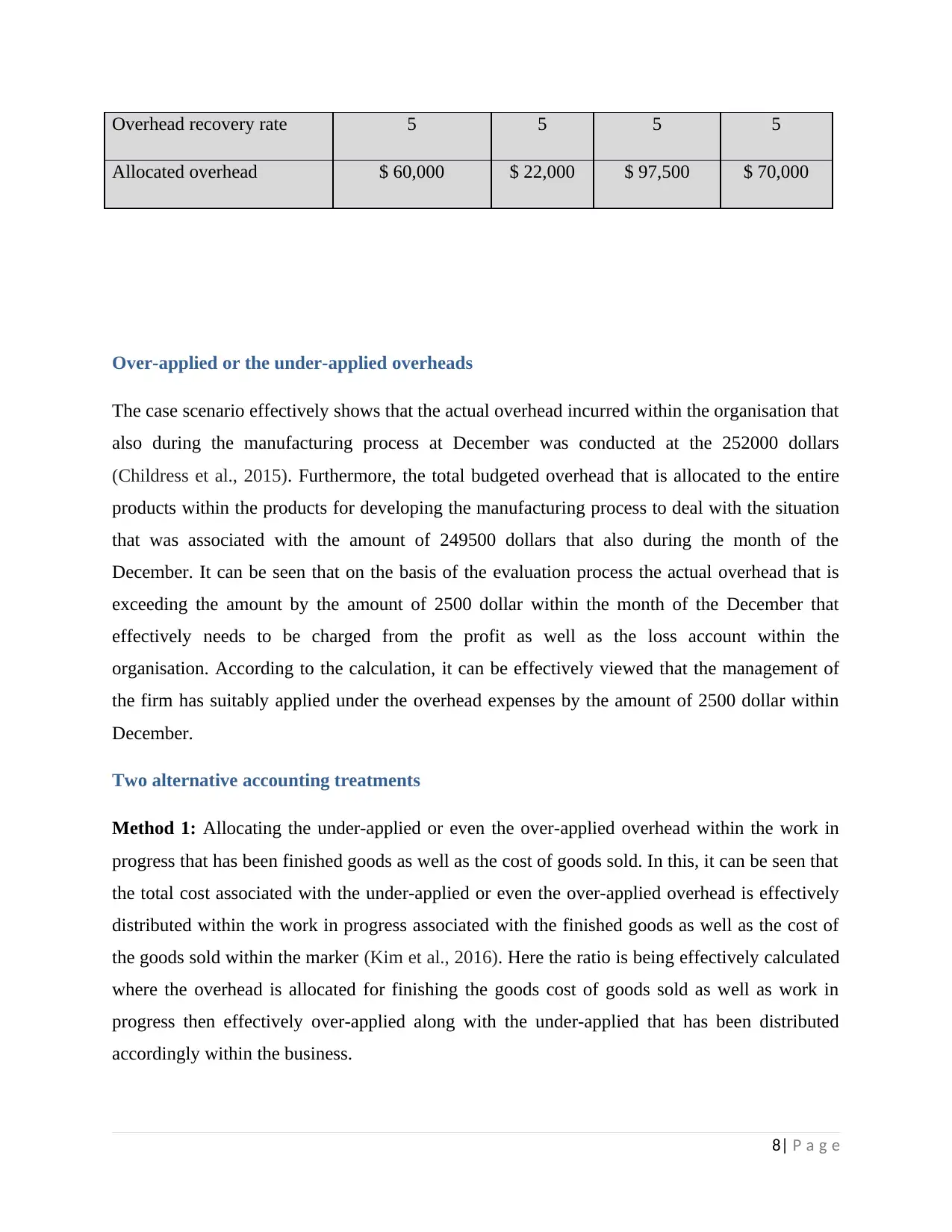

Overhead recovery rate 5 5 5 5

Allocated overhead $ 60,000 $ 22,000 $ 97,500 $ 70,000

Over-applied or the under-applied overheads

The case scenario effectively shows that the actual overhead incurred within the organisation that

also during the manufacturing process at December was conducted at the 252000 dollars

(Childress et al., 2015). Furthermore, the total budgeted overhead that is allocated to the entire

products within the products for developing the manufacturing process to deal with the situation

that was associated with the amount of 249500 dollars that also during the month of the

December. It can be seen that on the basis of the evaluation process the actual overhead that is

exceeding the amount by the amount of 2500 dollar within the month of the December that

effectively needs to be charged from the profit as well as the loss account within the

organisation. According to the calculation, it can be effectively viewed that the management of

the firm has suitably applied under the overhead expenses by the amount of 2500 dollar within

December.

Two alternative accounting treatments

Method 1: Allocating the under-applied or even the over-applied overhead within the work in

progress that has been finished goods as well as the cost of goods sold. In this, it can be seen that

the total cost associated with the under-applied or even the over-applied overhead is effectively

distributed within the work in progress associated with the finished goods as well as the cost of

the goods sold within the marker (Kim et al., 2016). Here the ratio is being effectively calculated

where the overhead is allocated for finishing the goods cost of goods sold as well as work in

progress then effectively over-applied along with the under-applied that has been distributed

accordingly within the business.

8| P a g e

Allocated overhead $ 60,000 $ 22,000 $ 97,500 $ 70,000

Over-applied or the under-applied overheads

The case scenario effectively shows that the actual overhead incurred within the organisation that

also during the manufacturing process at December was conducted at the 252000 dollars

(Childress et al., 2015). Furthermore, the total budgeted overhead that is allocated to the entire

products within the products for developing the manufacturing process to deal with the situation

that was associated with the amount of 249500 dollars that also during the month of the

December. It can be seen that on the basis of the evaluation process the actual overhead that is

exceeding the amount by the amount of 2500 dollar within the month of the December that

effectively needs to be charged from the profit as well as the loss account within the

organisation. According to the calculation, it can be effectively viewed that the management of

the firm has suitably applied under the overhead expenses by the amount of 2500 dollar within

December.

Two alternative accounting treatments

Method 1: Allocating the under-applied or even the over-applied overhead within the work in

progress that has been finished goods as well as the cost of goods sold. In this, it can be seen that

the total cost associated with the under-applied or even the over-applied overhead is effectively

distributed within the work in progress associated with the finished goods as well as the cost of

the goods sold within the marker (Kim et al., 2016). Here the ratio is being effectively calculated

where the overhead is allocated for finishing the goods cost of goods sold as well as work in

progress then effectively over-applied along with the under-applied that has been distributed

accordingly within the business.

8| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Method 2: Profit and loss account within the company is also considered to be one of the most

common and suitable methods that are associated with changing the under-applied as well as the

over-applied overhead within the business. In this method, both the under and the over applied is

effectively included within the cost of the good sold that has been recorded within the

organisation (Yang, Lee, and Chen, 2016). According to the case study, it is clearly provided that

the under-applied overhead is associated entirely with the cost of the goods sold is eventually

increased, but in the case of over-applied, the overhead is decreased. It can be seen that this is

one of the most commonly utilised processes within the business for maintaining the activity and

the management process within the field.

The ways of overcoming the deficiencies by activity-based costing

The activity-based costing is effectively helpful for evaluating the actual cost regarding the

production within the scenario. The advantages of the activity-based costing which effectively

support for the improvements of the accuracy as well as the relevancy within the allocation of the

expense are as follows;

In this, all, the production procedure is effectively divided within the diverse activities in

the costing process (Weygandt et al., 2018). Allocation of the expense that also on the

product as well as the service manufactured within the firm is effectively on the basis of

the cost that is associated with various activities that performed within the production of

the particular products.

The present method effectively shows that the management of the firm is using the

machinery that also for the allocation of the overhead expenses. It can be seen that in this

type of allocation, the numerous can be inaccurate with the use of the machines that also

in term of the products. It can also be seen that this allocation did not provide an accurate

allocation of overhead expenses (Wagner, 2015).

The cost drivers are effectively prepared with the firm regarding the process of allocation

that is also for the particular expenses within the different products as well as service

which will enhance the accuracy of the allocation cost (Maas, Schaltegger, and Crutzen,

2016).

The traditional costing method the effective cost of the firm are distributed as per the

number of the units produced by the firm and also due to the percentage of the labour

9| P a g e

common and suitable methods that are associated with changing the under-applied as well as the

over-applied overhead within the business. In this method, both the under and the over applied is

effectively included within the cost of the good sold that has been recorded within the

organisation (Yang, Lee, and Chen, 2016). According to the case study, it is clearly provided that

the under-applied overhead is associated entirely with the cost of the goods sold is eventually

increased, but in the case of over-applied, the overhead is decreased. It can be seen that this is

one of the most commonly utilised processes within the business for maintaining the activity and

the management process within the field.

The ways of overcoming the deficiencies by activity-based costing

The activity-based costing is effectively helpful for evaluating the actual cost regarding the

production within the scenario. The advantages of the activity-based costing which effectively

support for the improvements of the accuracy as well as the relevancy within the allocation of the

expense are as follows;

In this, all, the production procedure is effectively divided within the diverse activities in

the costing process (Weygandt et al., 2018). Allocation of the expense that also on the

product as well as the service manufactured within the firm is effectively on the basis of

the cost that is associated with various activities that performed within the production of

the particular products.

The present method effectively shows that the management of the firm is using the

machinery that also for the allocation of the overhead expenses. It can be seen that in this

type of allocation, the numerous can be inaccurate with the use of the machines that also

in term of the products. It can also be seen that this allocation did not provide an accurate

allocation of overhead expenses (Wagner, 2015).

The cost drivers are effectively prepared with the firm regarding the process of allocation

that is also for the particular expenses within the different products as well as service

which will enhance the accuracy of the allocation cost (Maas, Schaltegger, and Crutzen,

2016).

The traditional costing method the effective cost of the firm are distributed as per the

number of the units produced by the firm and also due to the percentage of the labour

9| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hour which has been effectively utilised for the production of the particular products. The

accurate method of the allocation process is effectively utilised within the process of

activity-based costing (Schaltegger, and Zvezdov, 2015).

Total cost pools that have been decided within the case in the traditional costing method

is primarily limited to the area of one or two (Bierer et al., 2015). Whereas, within the

case of the activity-based costing, it can be seen that the cost of pools is effectively

representatives regarding the different activities that have been undertaken by the

company for the production procedure.

The complexity within the allocation process of the expenses that also through the

activity-based costing that can be effectively high and even the activity-based costing

with the have the definitely for improving the various pricing strategies to the business

(Gurcanli, Bilir, and Sevim, 2015).

10| P a g e

accurate method of the allocation process is effectively utilised within the process of

activity-based costing (Schaltegger, and Zvezdov, 2015).

Total cost pools that have been decided within the case in the traditional costing method

is primarily limited to the area of one or two (Bierer et al., 2015). Whereas, within the

case of the activity-based costing, it can be seen that the cost of pools is effectively

representatives regarding the different activities that have been undertaken by the

company for the production procedure.

The complexity within the allocation process of the expenses that also through the

activity-based costing that can be effectively high and even the activity-based costing

with the have the definitely for improving the various pricing strategies to the business

(Gurcanli, Bilir, and Sevim, 2015).

10| P a g e

Conclusion

The paper eventually concludes the fact that the importance of selecting a suitable and

appropriate method regarding the costing purpose is considered crucial for the organisation. The

paper also concludes that effective methodology is utilised for the process of allocation by the

organisation. The paper also conclude that the requirement for improving the level of accuracy

for estimating the budgeted of overhead expense of the business termed as the total budget of the

expense. The paper also conclude that the cost of the effective value of business within the

market to deal with the situation in the entire process of the firm.

11| P a g e

The paper eventually concludes the fact that the importance of selecting a suitable and

appropriate method regarding the costing purpose is considered crucial for the organisation. The

paper also concludes that effective methodology is utilised for the process of allocation by the

organisation. The paper also conclude that the requirement for improving the level of accuracy

for estimating the budgeted of overhead expense of the business termed as the total budget of the

expense. The paper also conclude that the cost of the effective value of business within the

market to deal with the situation in the entire process of the firm.

11| P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.