ACCM4300 Assessment 3: Analysis of Consolidated Financial Statements

VerifiedAdded on 2022/08/26

|10

|506

|18

Report

AI Summary

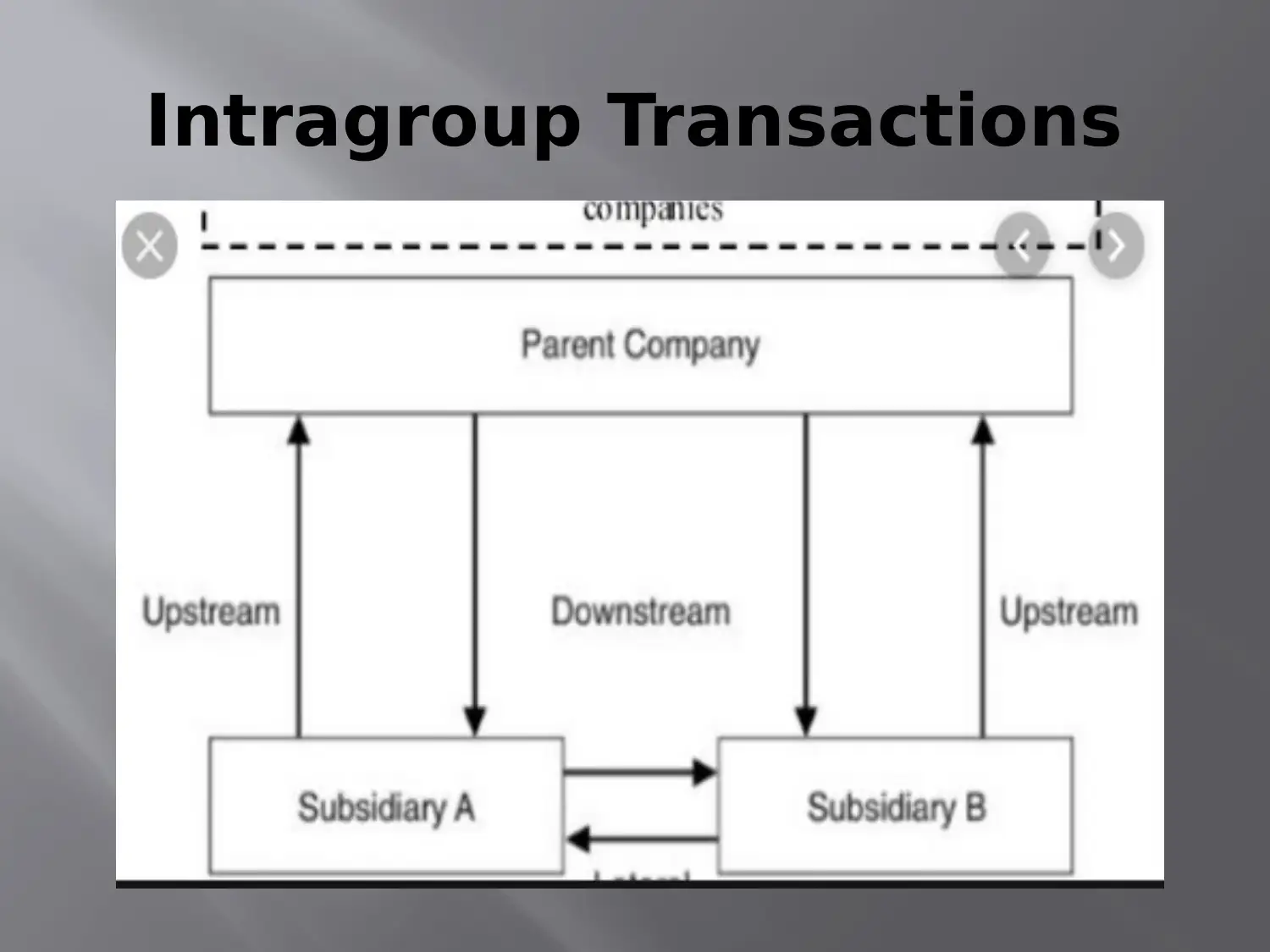

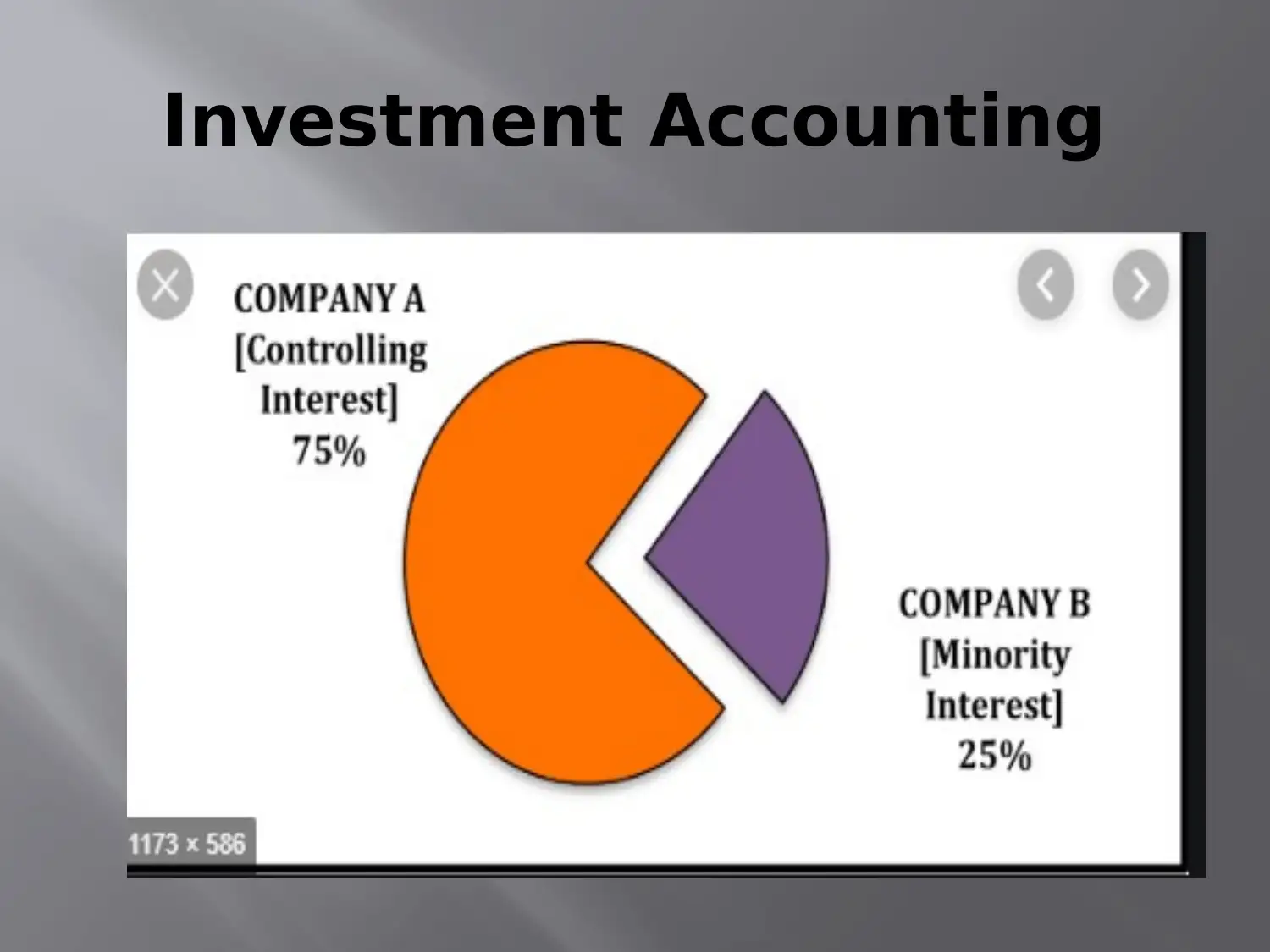

This report addresses accounting issues related to the consolidated financial statements of Tom Ltd, as highlighted in an email from the CEO. It focuses on two primary areas: intragroup transactions and investment accounting. The report recommends eliminating all intragroup balances, including transactions, income, and expenses, to prevent double-posting, aligning with AASB 127. Regarding investment accounting, the report advises accounting for investments at cost or in accordance with AASB 139, emphasizing the importance of proper disclosures and the presentation of minority interests in the consolidated balance sheet. The report stresses that the percentage of holdings directly impacts minority interest disclosures, and any misrepresentation in investments would affect the financial position of the business. The report provides a clear and concise overview of the accounting treatments required for consolidated items and offers recommendations for appropriate reporting and disclosures.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.