Consolidated Financial Statements Analysis: Good Ltd and Man Ltd

VerifiedAdded on 2019/12/18

|11

|2263

|164

Report

AI Summary

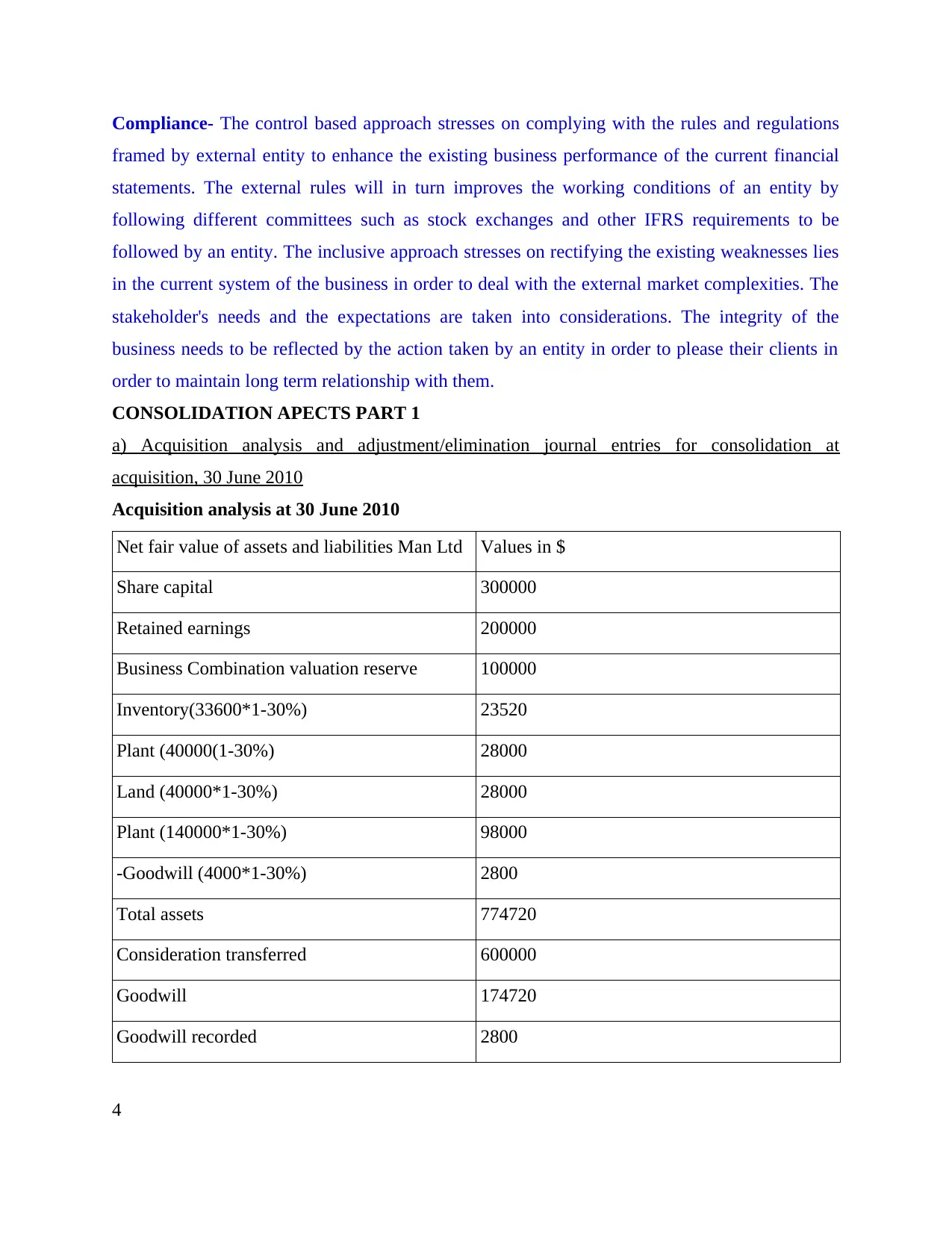

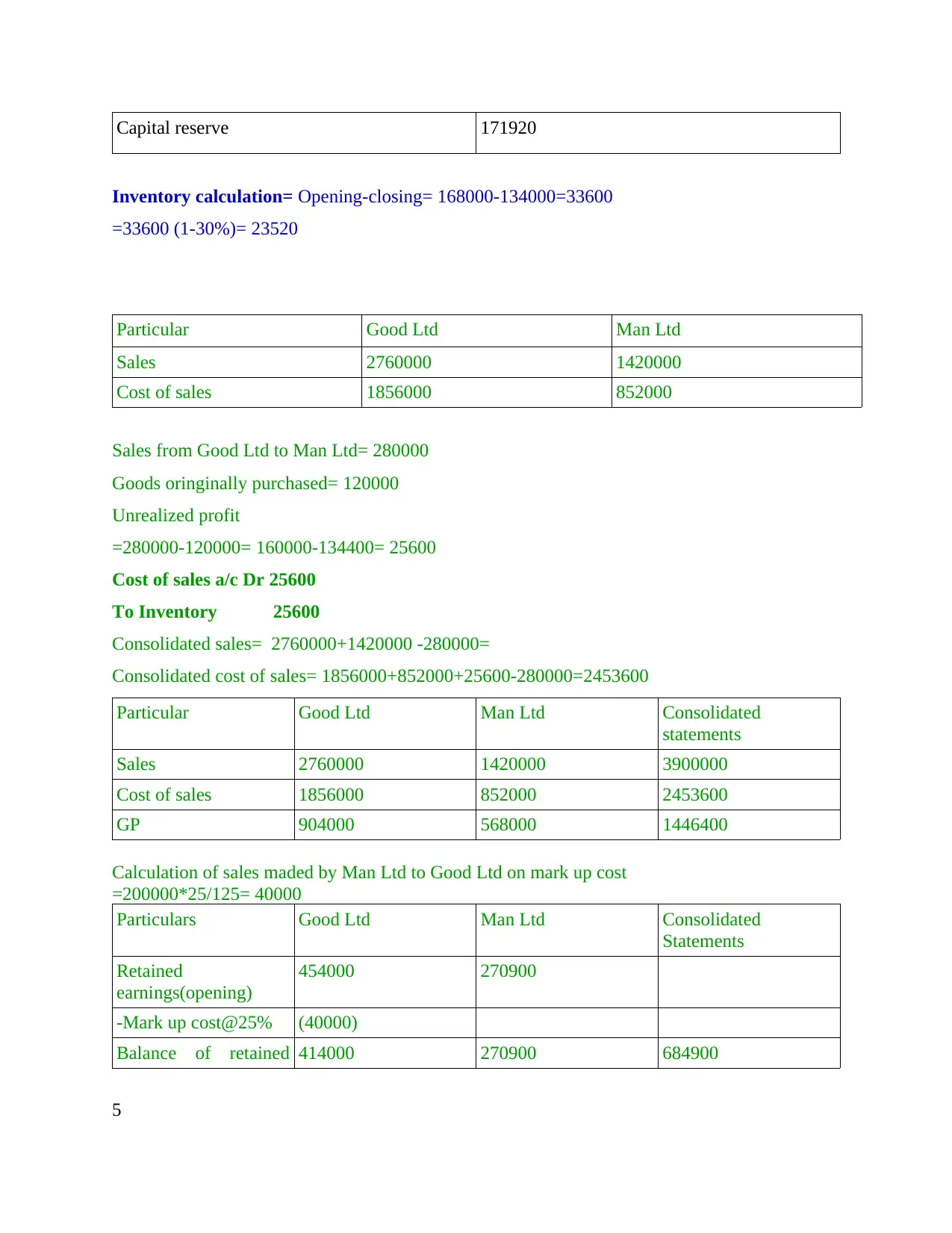

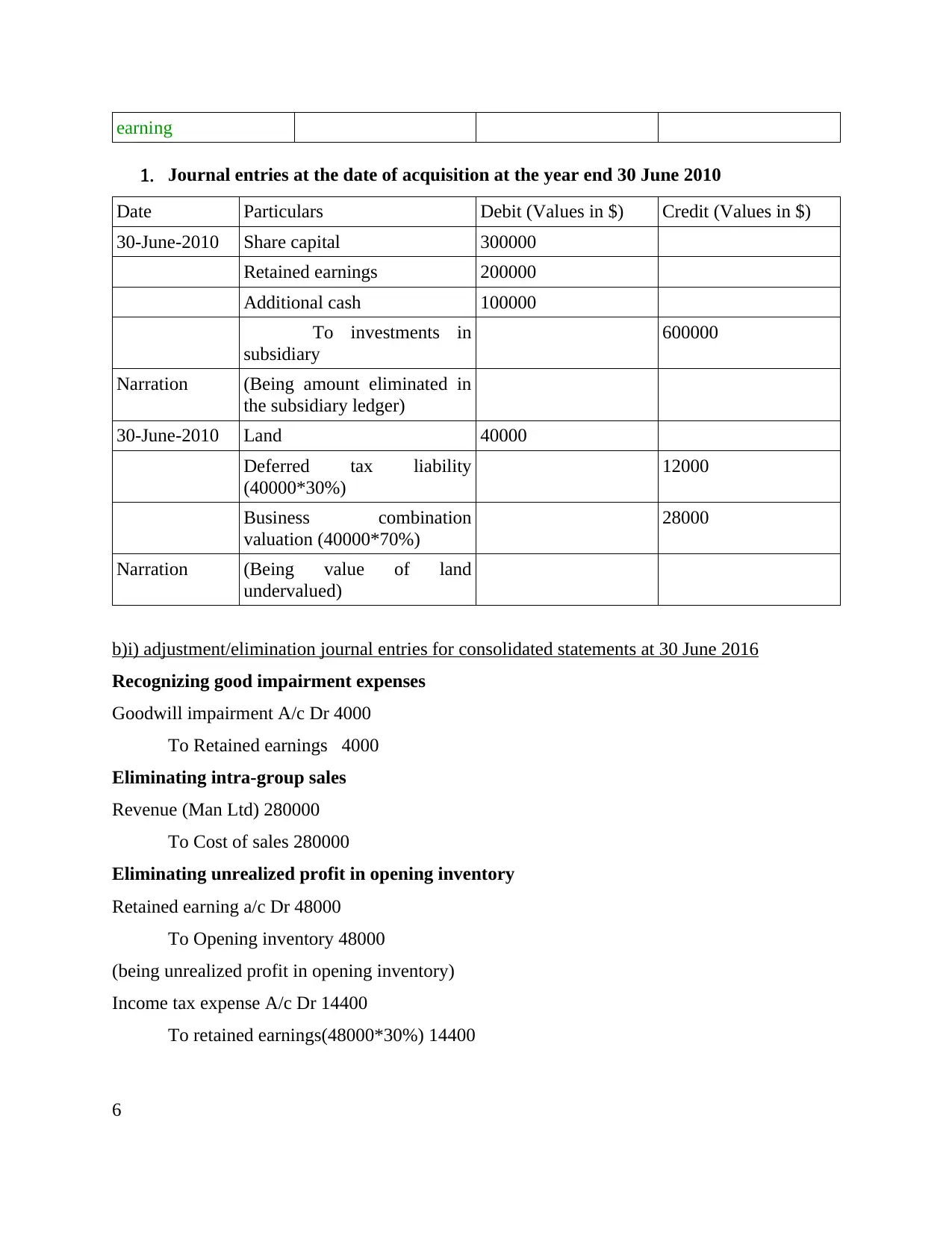

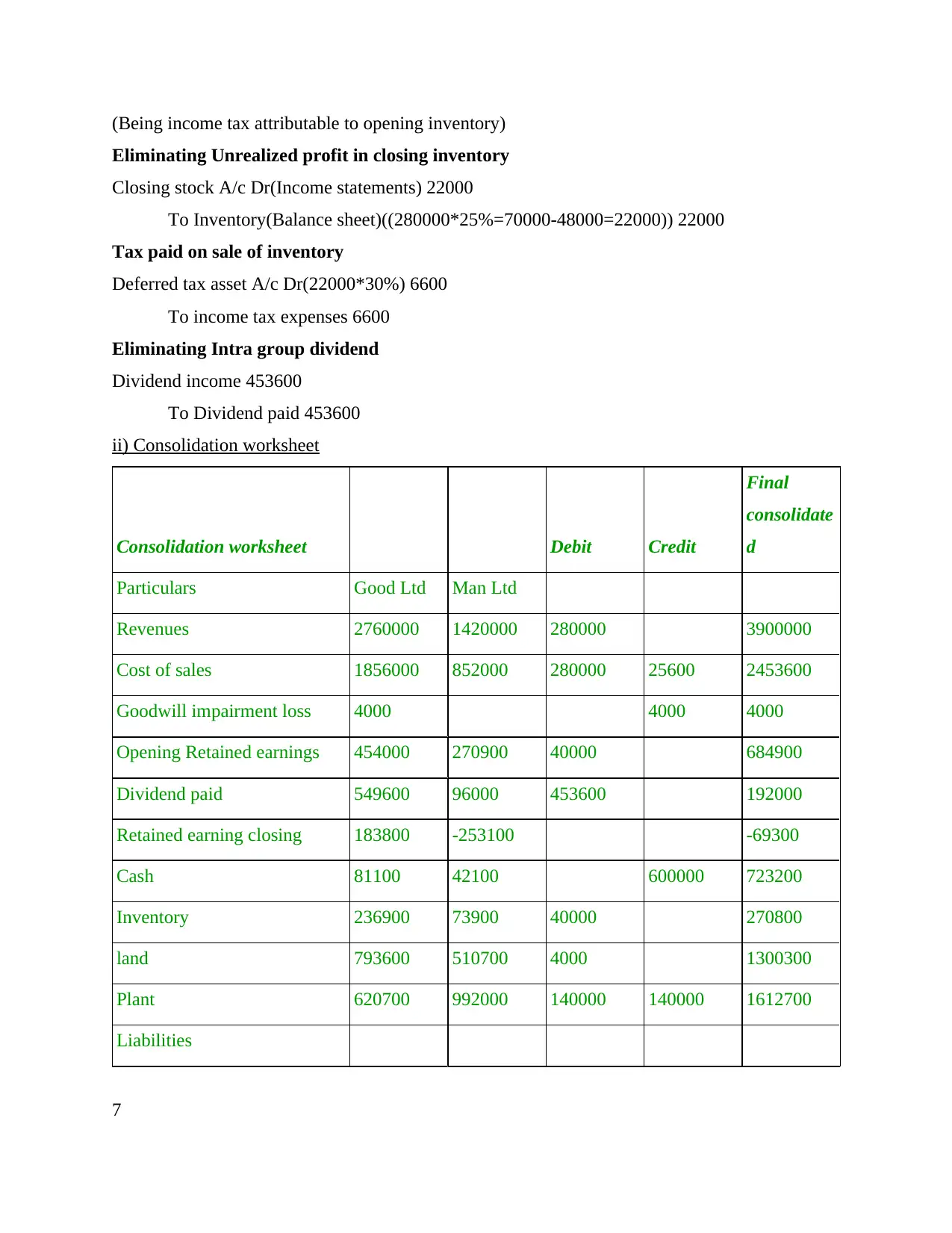

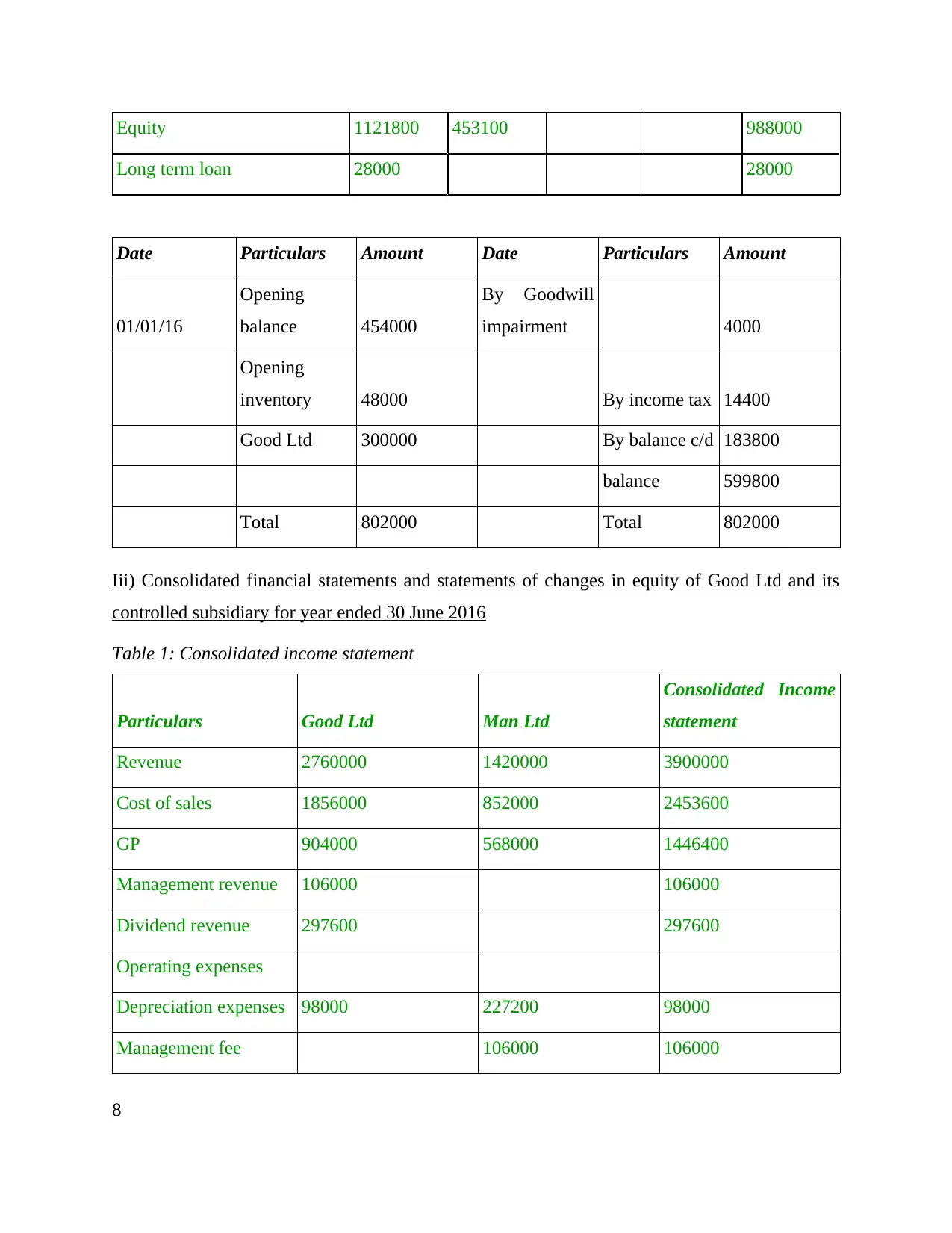

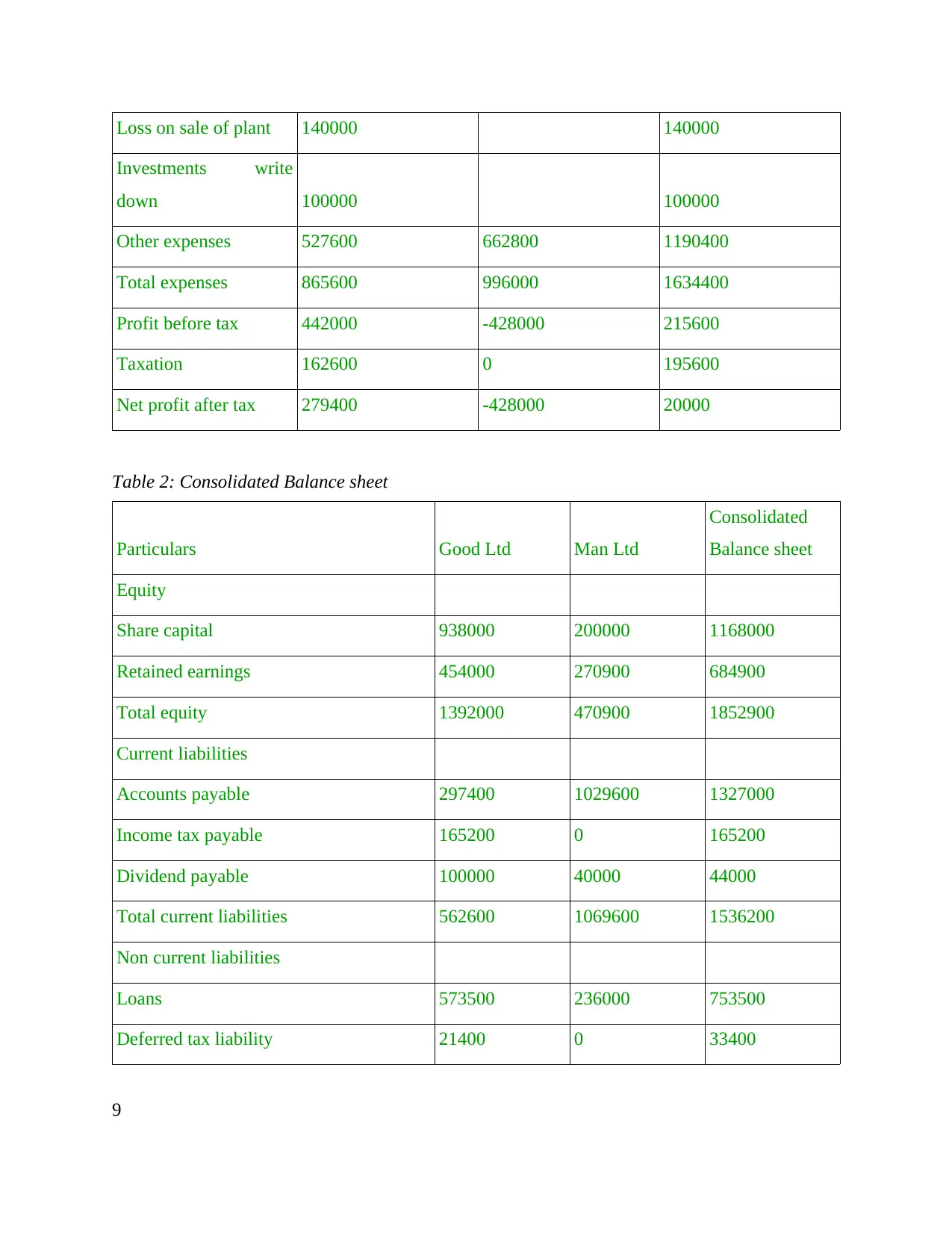

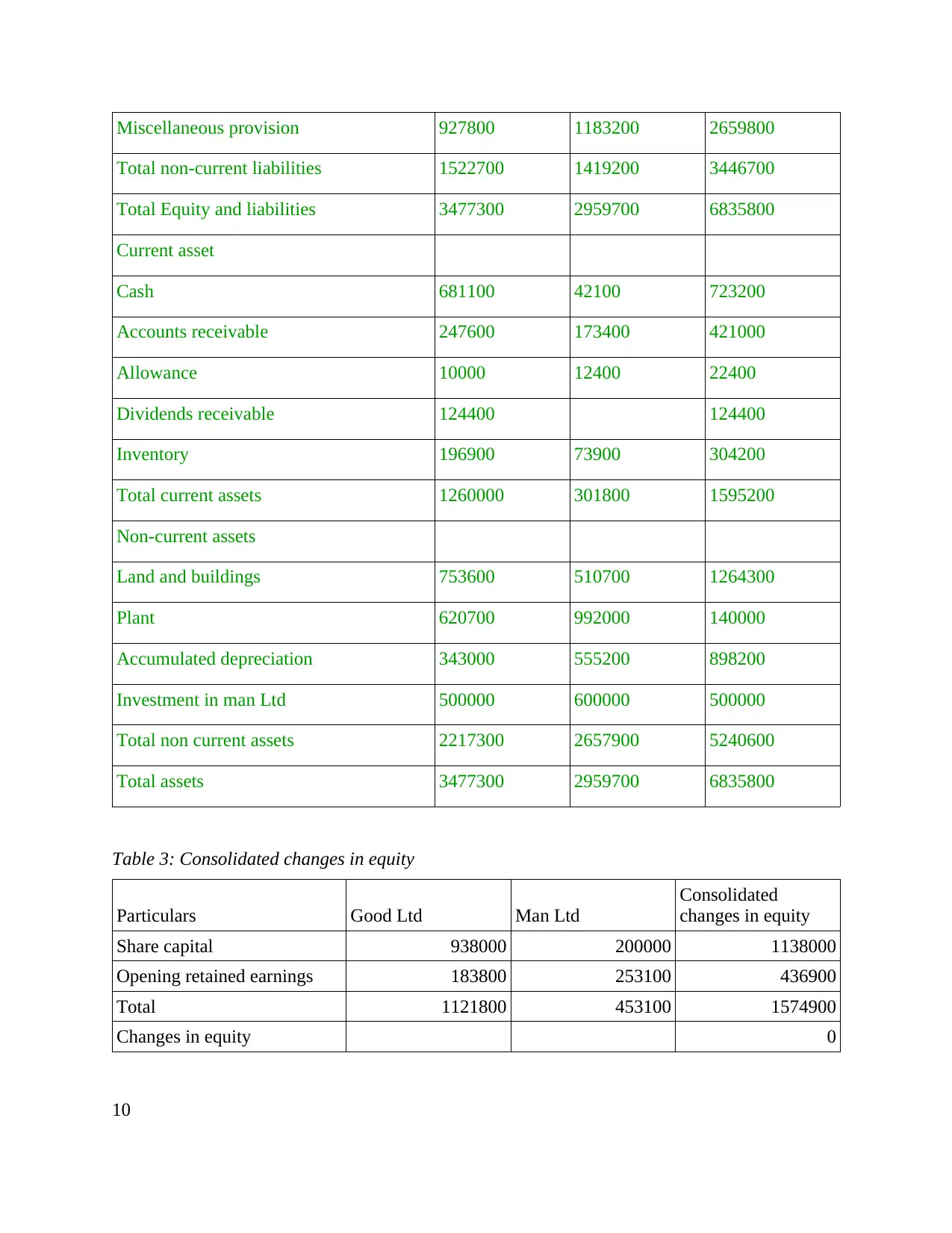

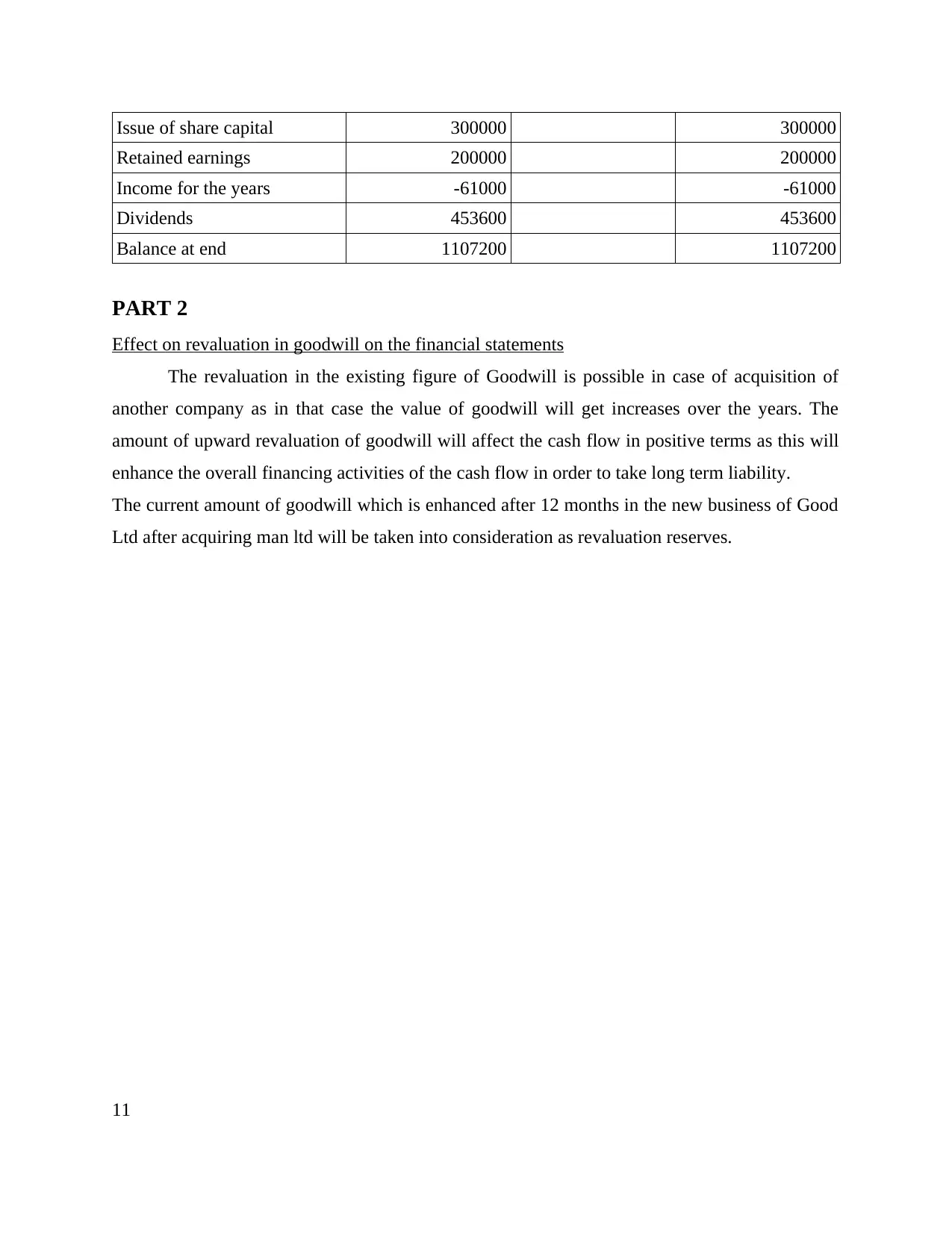

This report provides a comprehensive analysis of consolidated financial statements for Good Ltd and its subsidiary, Man Ltd. It begins with an acquisition analysis and adjustment/elimination journal entries for consolidation at acquisition on June 30, 2010, detailing the net fair value of assets and liabilities, consideration transferred, and goodwill calculations. The report then presents adjustment/elimination journal entries for consolidated statements at June 30, 2016, including entries for goodwill impairment, intra-group sales, unrealized profit in inventory, and intra-group dividends. A consolidation worksheet is provided, along with consolidated financial statements, including income statements, balance sheets, and statements of changes in equity for the year ended June 30, 2016. Part 2 of the report discusses the effect of revaluation on goodwill in the financial statements. The report also includes references to relevant books and journals.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.