Financial Accounting Report: UG221 Financial Accounting Assignment

VerifiedAdded on 2022/11/30

|12

|3642

|435

Report

AI Summary

This financial accounting report presents a comprehensive analysis of the Pee Group's financial performance, focusing on the preparation of a consolidated statement of financial position as of December 31, 2020, following the acquisition of Cee Ltd. The report addresses key aspects of financial reporting, including the qualitative characteristics of relevance, reliability, and comparability. It further evaluates the financial performance of Patrick Financial Services, examining growth, profitability, and credit management using data from provided appendices. The report also delves into non-financial information, employing a balance scorecard to assess future success and growth prospects. Additionally, it explores the importance of professional ethics in accounting, outlining fundamental principles. The analysis encompasses the application of accounting standards, the interpretation of financial data, and the implications for decision-making, providing insights into the financial health and strategic considerations for the businesses involved.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION- 1.................................................................................................................................1

a) Consolidated statement of financial position for the Pee Group as at 31st December, 2020..1

b) Relevance, reliability and comparability impacting the financial information and making it

more useful...................................................................................................................................2

QUESTION- 2.................................................................................................................................4

a) I) Financial performance of Patrick Financial Services...........................................................4

II) Non-financial information giving the indication of future success........................................5

b) Importance of professional ethics in accounting.....................................................................7

Fundamental principles of professional ethics for accountants...................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION- 1.................................................................................................................................1

a) Consolidated statement of financial position for the Pee Group as at 31st December, 2020..1

b) Relevance, reliability and comparability impacting the financial information and making it

more useful...................................................................................................................................2

QUESTION- 2.................................................................................................................................4

a) I) Financial performance of Patrick Financial Services...........................................................4

II) Non-financial information giving the indication of future success........................................5

b) Importance of professional ethics in accounting.....................................................................7

Fundamental principles of professional ethics for accountants...................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial accounting is the process of recording, summarizing and interpreting the

financial position of the business through the preparation of the financial statements of the

company. Such financial statements are used by the internal and external users to analyse the

performance of the business and based on the insights take the meaningful decisions associated

with the company. Apart from the financial perspective the non-financial perspective of the

business is also important to seek the useful data pertaining to the results generated by the

company. The customer oriented approach, long term growth and development plans and

innovations that help the business survive in the market are some critical aspects of the business

that shows wider picture related to the entity. The current project shall be showing the

preparation of the consolidated financial statements of the business with the acquired subsidiary.

Further it shall be showing the detailed explanation related to the balance scorecard and on the

basis of that the comments can be made on the performance of the business in the financial and

non-financial terms.

MAIN BODY

QUESTION- 1

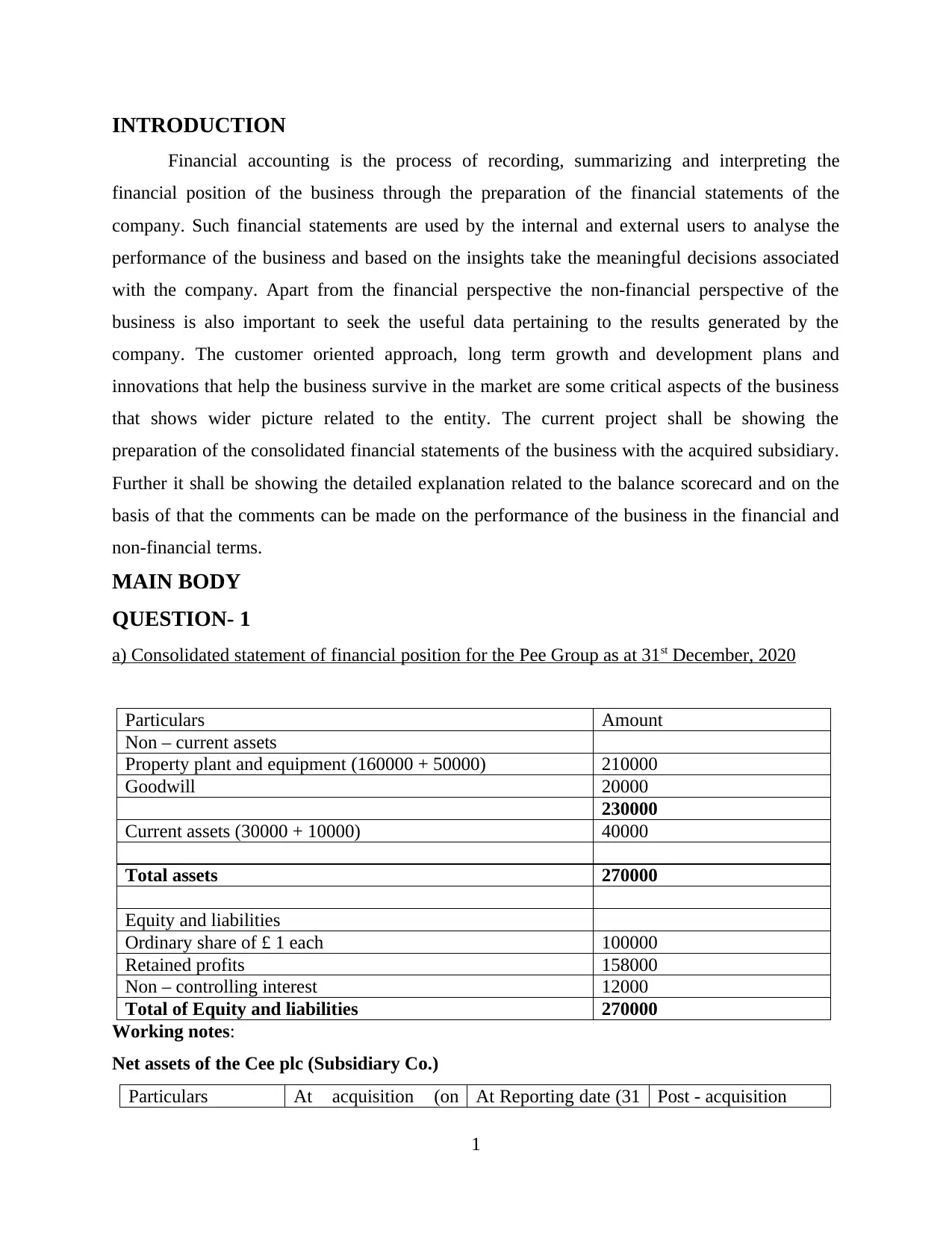

a) Consolidated statement of financial position for the Pee Group as at 31st December, 2020

Particulars Amount

Non – current assets

Property plant and equipment (160000 + 50000) 210000

Goodwill 20000

230000

Current assets (30000 + 10000) 40000

Total assets 270000

Equity and liabilities

Ordinary share of £ 1 each 100000

Retained profits 158000

Non – controlling interest 12000

Total of Equity and liabilities 270000

Working notes:

Net assets of the Cee plc (Subsidiary Co.)

Particulars At acquisition (on At Reporting date (31 Post - acquisition

1

Financial accounting is the process of recording, summarizing and interpreting the

financial position of the business through the preparation of the financial statements of the

company. Such financial statements are used by the internal and external users to analyse the

performance of the business and based on the insights take the meaningful decisions associated

with the company. Apart from the financial perspective the non-financial perspective of the

business is also important to seek the useful data pertaining to the results generated by the

company. The customer oriented approach, long term growth and development plans and

innovations that help the business survive in the market are some critical aspects of the business

that shows wider picture related to the entity. The current project shall be showing the

preparation of the consolidated financial statements of the business with the acquired subsidiary.

Further it shall be showing the detailed explanation related to the balance scorecard and on the

basis of that the comments can be made on the performance of the business in the financial and

non-financial terms.

MAIN BODY

QUESTION- 1

a) Consolidated statement of financial position for the Pee Group as at 31st December, 2020

Particulars Amount

Non – current assets

Property plant and equipment (160000 + 50000) 210000

Goodwill 20000

230000

Current assets (30000 + 10000) 40000

Total assets 270000

Equity and liabilities

Ordinary share of £ 1 each 100000

Retained profits 158000

Non – controlling interest 12000

Total of Equity and liabilities 270000

Working notes:

Net assets of the Cee plc (Subsidiary Co.)

Particulars At acquisition (on At Reporting date (31 Post - acquisition

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

December 2018) December 2020)

Equity shares 20000 20000

Retained earnings 30000 40000 10000

Fair value of the

net assets

50000 60000 10000

Value of Non – controlling interest at acquisition

= Fair value of net assets at acquisition * % of NCI = 50000 * 20% = 10000

Goodwill = Fair value paid by parent on acquisition of controlling interest + fair value of NCI at

acquisition – Fair value of net assets on the date of acquisition

Goodwill arises on consolidation = 60000 + 10000 – 50000 = 20000

Group retained earnings to be shown in consolidated statement of financial position

Pee Ltd. (parent)’s retained earnings as on 31 December 2020 + % share of post - acquisition

profit of Cee Ltd. (Subsidiary)

= 150000 + 80% of 10000 = 158000.

So, there are certain terms that has been used for the purpose of preparing the above

consolidated statement of financial position for the group, where the Pee Plc has obtained 80%

share in the Cee Ltd., therefore Pee ltd. becomes the parent of Cee Ltd. and accordingly Cee ltd.

becomes Subsidiary of Pee Ltd (Inuwa and Baraya, 2017).

NCI calculation for the date of reporting that is, 31 December 2020

= Opening NCI on 31 December 2018 + NCI % share of profit arises on post – acquisition

= 10000 + 20% of 10000 = 12000.

The consolidated financial statements as prepared by the company is a group statement

that includes the data pertaining to the subsidiary of the company. All the income and expenses,

assets and liabilities of the business are ascertained in the combined manner and accordingly the

value of goodwill and non-controlling interest of the company is ascertained by the company.

b) Relevance, reliability and comparability impacting the financial information and making it

more useful

The financial statements of the company are prepared in accordance with the

International Accounting Standards Board (IASB) and the Conceptual Framework that is

prescribed by them. There are some qualitative characteristics as prescribed by this framework

that shall be leading to the proper preparation of these financial statements and the representation

2

Equity shares 20000 20000

Retained earnings 30000 40000 10000

Fair value of the

net assets

50000 60000 10000

Value of Non – controlling interest at acquisition

= Fair value of net assets at acquisition * % of NCI = 50000 * 20% = 10000

Goodwill = Fair value paid by parent on acquisition of controlling interest + fair value of NCI at

acquisition – Fair value of net assets on the date of acquisition

Goodwill arises on consolidation = 60000 + 10000 – 50000 = 20000

Group retained earnings to be shown in consolidated statement of financial position

Pee Ltd. (parent)’s retained earnings as on 31 December 2020 + % share of post - acquisition

profit of Cee Ltd. (Subsidiary)

= 150000 + 80% of 10000 = 158000.

So, there are certain terms that has been used for the purpose of preparing the above

consolidated statement of financial position for the group, where the Pee Plc has obtained 80%

share in the Cee Ltd., therefore Pee ltd. becomes the parent of Cee Ltd. and accordingly Cee ltd.

becomes Subsidiary of Pee Ltd (Inuwa and Baraya, 2017).

NCI calculation for the date of reporting that is, 31 December 2020

= Opening NCI on 31 December 2018 + NCI % share of profit arises on post – acquisition

= 10000 + 20% of 10000 = 12000.

The consolidated financial statements as prepared by the company is a group statement

that includes the data pertaining to the subsidiary of the company. All the income and expenses,

assets and liabilities of the business are ascertained in the combined manner and accordingly the

value of goodwill and non-controlling interest of the company is ascertained by the company.

b) Relevance, reliability and comparability impacting the financial information and making it

more useful

The financial statements of the company are prepared in accordance with the

International Accounting Standards Board (IASB) and the Conceptual Framework that is

prescribed by them. There are some qualitative characteristics as prescribed by this framework

that shall be leading to the proper preparation of these financial statements and the representation

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the financial information. This financial information then becomes more useful for the users in

the process of decision-making and assists them in planning their future in accordance with the

growth prospects visible in respect of the business. These major characteristics are described

below:- Relevance- Relevance is the most essential characteristic of the information that is

provided in the financial statements of the business as it states that such data must be

meaningful and material in respect of the users such that it can influence the econmic

decisions in respect of the company (Herrador-Alcaide, Hernández-Solís and Galván,

2019). The information that is involved must be relevant in a manner that it creates value

for the people who are referring it and are capable to base their decisions over this useful

details. The qualitative aspect of relevance also signifies that the data must have

predictive capacity which is that it must be presented in a manner that the users can

identify the opportunities related to some income and assets as possessed by the

organization. On the contrary they can also define the adversities that may arise in the

future due to the liabilities and the current expenditures made by the company.

Materiality is another significant aspect that is covered under the qualitative characteristic

of relevance that needs to be ensured while preparing the financial statements of the

business as it is considered that this shall be making the information more useful for the

internal and external users. This is in the manner that the decision-making process can be

based upon it through ascertaining the current and the future financial position of the

company. So it can be relevance makes the data more sound and efficient developing the

potential customers and investors for the company. Reliability- Reliability is another major requirement pertaining to the information that is

being included in the preparation of the financial statements. The reliability of

information states the data must be such that can be trusted by the ones who refer to it

and uses it while they are during conclusions regarding the performance of the company

in the particular financial year (The IASB’s Conceptual Framework for Financial

Reporting, 2021). This can be well ensured if the professional accountant uses all the

fundamental principles of accounting like the integrity, honesty, due diligence,

professional knowledge, confidentiality and the ethical code of conduct. This shall be

ascertaining that the data is free from any kind of material misstatements, omissions and

3

the process of decision-making and assists them in planning their future in accordance with the

growth prospects visible in respect of the business. These major characteristics are described

below:- Relevance- Relevance is the most essential characteristic of the information that is

provided in the financial statements of the business as it states that such data must be

meaningful and material in respect of the users such that it can influence the econmic

decisions in respect of the company (Herrador-Alcaide, Hernández-Solís and Galván,

2019). The information that is involved must be relevant in a manner that it creates value

for the people who are referring it and are capable to base their decisions over this useful

details. The qualitative aspect of relevance also signifies that the data must have

predictive capacity which is that it must be presented in a manner that the users can

identify the opportunities related to some income and assets as possessed by the

organization. On the contrary they can also define the adversities that may arise in the

future due to the liabilities and the current expenditures made by the company.

Materiality is another significant aspect that is covered under the qualitative characteristic

of relevance that needs to be ensured while preparing the financial statements of the

business as it is considered that this shall be making the information more useful for the

internal and external users. This is in the manner that the decision-making process can be

based upon it through ascertaining the current and the future financial position of the

company. So it can be relevance makes the data more sound and efficient developing the

potential customers and investors for the company. Reliability- Reliability is another major requirement pertaining to the information that is

being included in the preparation of the financial statements. The reliability of

information states the data must be such that can be trusted by the ones who refer to it

and uses it while they are during conclusions regarding the performance of the company

in the particular financial year (The IASB’s Conceptual Framework for Financial

Reporting, 2021). This can be well ensured if the professional accountant uses all the

fundamental principles of accounting like the integrity, honesty, due diligence,

professional knowledge, confidentiality and the ethical code of conduct. This shall be

ascertaining that the data is free from any kind of material misstatements, omissions and

3

is not influenced undue pressures or the fraudulent practices that are undertaken in the

business. If the details presented by the officials of the company are reliable in nature in

that case it shall be contributing to boosting the loyalty, confidence and trustworthiness of

the various stakeholders towards the business and this will be retaining them longer with

the business.

Comparability- The comparability of the data is also an essential characteristic that needs

to be maintained to facilitate comparison by the users of the financial statement. This

comparison is made to check the trend that is followed by the businesses in respect of

previous year's data, it can also be inter departmental comparison or the comparison

among the competitors in the industry (Kimmel, Weygandt and Kieso, 2018). All these

kind of comparisons are useful in analysing the financial health and status of the

company. In the interdepartmental comparison the management gets to know the profit

making and the loss making ventures in the business. And accordingly they invest in the

growing businesses and shut down the ones which are loss making for the company. The

comparative statement studying the trend of the business helps the business in future

strategic formulation. Further the statement that is prepared in reference to competitors

shall be analysing the competition in the market and plan for taking the competitive

advantage in the industry.

With the comparative statement, also the consistency statement is to be prepared by the company

that shall be indicating that the company is following the accounting policies and standards with

consistency. This shall further assist in the comparison of the statements of the companies who

are following the similar standards and policies in the company.

QUESTION- 2

a) I) Financial performance of Patrick Financial Services

As per the information stated in appendix 1, representing the financial performance of

Patrick Financial Services who is providing the consultancy services in respect of accountancy

and taxation, the growth, profitability and the credit management of the company can be

analysed. The two years data of the company is provided with respect to that the commenting on

the financial position and growth that the company has attained over the period. The evaluation

of the company information is as follows:-

4

business. If the details presented by the officials of the company are reliable in nature in

that case it shall be contributing to boosting the loyalty, confidence and trustworthiness of

the various stakeholders towards the business and this will be retaining them longer with

the business.

Comparability- The comparability of the data is also an essential characteristic that needs

to be maintained to facilitate comparison by the users of the financial statement. This

comparison is made to check the trend that is followed by the businesses in respect of

previous year's data, it can also be inter departmental comparison or the comparison

among the competitors in the industry (Kimmel, Weygandt and Kieso, 2018). All these

kind of comparisons are useful in analysing the financial health and status of the

company. In the interdepartmental comparison the management gets to know the profit

making and the loss making ventures in the business. And accordingly they invest in the

growing businesses and shut down the ones which are loss making for the company. The

comparative statement studying the trend of the business helps the business in future

strategic formulation. Further the statement that is prepared in reference to competitors

shall be analysing the competition in the market and plan for taking the competitive

advantage in the industry.

With the comparative statement, also the consistency statement is to be prepared by the company

that shall be indicating that the company is following the accounting policies and standards with

consistency. This shall further assist in the comparison of the statements of the companies who

are following the similar standards and policies in the company.

QUESTION- 2

a) I) Financial performance of Patrick Financial Services

As per the information stated in appendix 1, representing the financial performance of

Patrick Financial Services who is providing the consultancy services in respect of accountancy

and taxation, the growth, profitability and the credit management of the company can be

analysed. The two years data of the company is provided with respect to that the commenting on

the financial position and growth that the company has attained over the period. The evaluation

of the company information is as follows:-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Growth- It can be analysed that the company has been successful in generating growth

and prosperity for the business to some extent (McCallig, Robb and Rohde, 2019). This is

because it can evidently be noticed that the turnover of the company has increased as

compared to the previous year by 5% which is from 900 to 945. The majority of such

growth is in accordance with the inflation rate that is there in the economy. But the

inflation is by 3% and company revenue has boosted by 5%, this means there is growth in

the business. Profitability- On the contrary with reference to the profitability of the business it can be

commented that the company's net profit margin has dropped down as in the previous

year the margin was about 20% which has decreased in the current year to 19.8%. This

can be due to the operational inefficiency increasing the costs of the business.

Credit management- The credit management policy of the company is better than the

industry average as the efficient recovery agents of the company collect the amount due

from the receivables within a period of 18 days in the current year which has improved

by 4 days as compared to the last year. This improves the efficiency in the operating

cycle due the sufficient availability of the liquidity. This can also be seen through the

increased cash balances of the business.

II) Non-financial information giving the indication of future success

The appendix 2 representing the non financial information pertaining to Patrick Financial

Services gives better indication in respect of the future success and growth prospects of the

company (Weygandt, Kimmel and Kieso, 2018). The balance scorecard as prepared gives deeper

insight regarding the business operations, customer perspectives, innovation and the learning and

growth approaches followed by the business. From the internal business processes it can be

assessed that the average job completion time has significantly reduced from 10 weeks to 7

weeks in the current year. But simultaneously it can also be seen that the decreased time has

increased the error ratio from 10 % to 16 % which signifies that the faster operations have not

increased the operational efficiency of the business. The error ratio shows the mistakes

undertaken in the jobs provided to clients which has dropped down the level of customer

satisfaction reducing the market share and the number of customers for the company. The change

in customer perspectives can also be due to the increased fees charge for the accounting and

taxation consultancy by the company from 600 to 775 per job. The information from the balance

5

and prosperity for the business to some extent (McCallig, Robb and Rohde, 2019). This is

because it can evidently be noticed that the turnover of the company has increased as

compared to the previous year by 5% which is from 900 to 945. The majority of such

growth is in accordance with the inflation rate that is there in the economy. But the

inflation is by 3% and company revenue has boosted by 5%, this means there is growth in

the business. Profitability- On the contrary with reference to the profitability of the business it can be

commented that the company's net profit margin has dropped down as in the previous

year the margin was about 20% which has decreased in the current year to 19.8%. This

can be due to the operational inefficiency increasing the costs of the business.

Credit management- The credit management policy of the company is better than the

industry average as the efficient recovery agents of the company collect the amount due

from the receivables within a period of 18 days in the current year which has improved

by 4 days as compared to the last year. This improves the efficiency in the operating

cycle due the sufficient availability of the liquidity. This can also be seen through the

increased cash balances of the business.

II) Non-financial information giving the indication of future success

The appendix 2 representing the non financial information pertaining to Patrick Financial

Services gives better indication in respect of the future success and growth prospects of the

company (Weygandt, Kimmel and Kieso, 2018). The balance scorecard as prepared gives deeper

insight regarding the business operations, customer perspectives, innovation and the learning and

growth approaches followed by the business. From the internal business processes it can be

assessed that the average job completion time has significantly reduced from 10 weeks to 7

weeks in the current year. But simultaneously it can also be seen that the decreased time has

increased the error ratio from 10 % to 16 % which signifies that the faster operations have not

increased the operational efficiency of the business. The error ratio shows the mistakes

undertaken in the jobs provided to clients which has dropped down the level of customer

satisfaction reducing the market share and the number of customers for the company. The change

in customer perspectives can also be due to the increased fees charge for the accounting and

taxation consultancy by the company from 600 to 775 per job. The information from the balance

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

scorecard also determine that the employee retention rate has dropped down from 80 % to 60 %

showing the dissatisfaction among the workforce of the company. Further the revenue generated

from the non core activities like consultancy in respect of pension and businesses has also taken

downward turn.

Overall these non financial information as gathered and arranged in the format of balance

scorecard are also critical in determining whether the business shall remain a successful venture

in the future or not. The information pertaining to the current year is showing that the company is

facing a tough time in managing its employees as well as its customers. This is the reason that it

is not able to capitalize on the growth opportunities in the market. The lack of operational

efficiency has significantly impacted its growth as the error ratio has caused dissatisfaction

among their customers and employees.

The overall performance is deteriorated for the company in the current year due to the

uncertainties in the business processes. This has to be improved through employing highly

qualified employees having better knowledge to provide consultancy services. Also, techniques

need to be discovered so that the customer loyalty and trust can be regained by the business. This

shall improvise the market share that is currently shared in the company. One more way of

improving the organizational performance is through concentrating on the non-core activities

like the pension and the business consultancy services as undertaken by the company. These

activities of the business are having the high profitability margin and thereby shall be efficient

improving its net profit margin (Schroeder, Clark and Cathey, 2019). Sometimes these activities

can also help the business in generating the competitive advantage so that the market share of the

company can be boosted significantly.

This kind of deeper insights about the company can be gained through the non-financial

information as the financial information has limited scope in defining the current position of the

business. The turnover of the company is showing an increasing trend whereas the net profit ratio

shows slightest inefficiency that is possessed by the company. On the contrary with the non-

financial information it could be known that there are high level of operational inefficiencies in

the company which has led to slow growth despite of inflation. Also the company has high

degree of employee as well as customer dissatisfaction that has been contributing to further drop

down in the performance of the company.

6

showing the dissatisfaction among the workforce of the company. Further the revenue generated

from the non core activities like consultancy in respect of pension and businesses has also taken

downward turn.

Overall these non financial information as gathered and arranged in the format of balance

scorecard are also critical in determining whether the business shall remain a successful venture

in the future or not. The information pertaining to the current year is showing that the company is

facing a tough time in managing its employees as well as its customers. This is the reason that it

is not able to capitalize on the growth opportunities in the market. The lack of operational

efficiency has significantly impacted its growth as the error ratio has caused dissatisfaction

among their customers and employees.

The overall performance is deteriorated for the company in the current year due to the

uncertainties in the business processes. This has to be improved through employing highly

qualified employees having better knowledge to provide consultancy services. Also, techniques

need to be discovered so that the customer loyalty and trust can be regained by the business. This

shall improvise the market share that is currently shared in the company. One more way of

improving the organizational performance is through concentrating on the non-core activities

like the pension and the business consultancy services as undertaken by the company. These

activities of the business are having the high profitability margin and thereby shall be efficient

improving its net profit margin (Schroeder, Clark and Cathey, 2019). Sometimes these activities

can also help the business in generating the competitive advantage so that the market share of the

company can be boosted significantly.

This kind of deeper insights about the company can be gained through the non-financial

information as the financial information has limited scope in defining the current position of the

business. The turnover of the company is showing an increasing trend whereas the net profit ratio

shows slightest inefficiency that is possessed by the company. On the contrary with the non-

financial information it could be known that there are high level of operational inefficiencies in

the company which has led to slow growth despite of inflation. Also the company has high

degree of employee as well as customer dissatisfaction that has been contributing to further drop

down in the performance of the company.

6

b) Importance of professional ethics in accounting

The professional ethics are very important in the accounting arena and it monitors that the

certified public accountants are fulfilling their duties with due integrity and objectivity. This is of

major importance as they are preparing the financial statements that are reflecting the

performance and position of the business and so the process needs to be undertaken with due

care and responsibility. Some major importances of maintaining the ethical code of conduct

while conducting accounting are:-

If the accountant is following all the fundamental principles it shall mean that the

compliance as to the legal and regulatory requirements are fulfilled. The reporting

framework has been complied with, all the accounting standards and policies are duly

followed in order to ensure the true and fair view is represented by the financial

statements.

It is significant to follow the professional ethics while conducting the accounting work as

it shall be ensuring the maintenance of the public trust and loyalty on the business affairs

of the company (Warren, Jonick and Schneider, 2020). Since various users of accounting

information base their future decisions over the demonstration as provided by the books

of accounts so it needs to be regulated.

Another major importance is that if the accountants are performing their functions with

integrity and honesty then any kind of fraudulent practices by the employees and

management of the company shall be discouraged, it will avoid any misrepresentations

and mistakes in the organization.

Lastly it can be assessed that accounting managers of the company are dealing with the

sensitive information of the company which needs to be protected from the other

competitors in the industry. For this reason it can be assessed that confidentiality must be

maintained by the accounting managers.

Fundamental principles of professional ethics for accountants

There are five fundamental principles that are necessary for the accountants to follow in

order to ensure the ethical code of conduct in the organization. The fundamental principles of

professional ethics are described below:- Integrity- This principle indicates that an accountant must be straightforward and honest

in their approach and managing all the professional and business relationships.

7

The professional ethics are very important in the accounting arena and it monitors that the

certified public accountants are fulfilling their duties with due integrity and objectivity. This is of

major importance as they are preparing the financial statements that are reflecting the

performance and position of the business and so the process needs to be undertaken with due

care and responsibility. Some major importances of maintaining the ethical code of conduct

while conducting accounting are:-

If the accountant is following all the fundamental principles it shall mean that the

compliance as to the legal and regulatory requirements are fulfilled. The reporting

framework has been complied with, all the accounting standards and policies are duly

followed in order to ensure the true and fair view is represented by the financial

statements.

It is significant to follow the professional ethics while conducting the accounting work as

it shall be ensuring the maintenance of the public trust and loyalty on the business affairs

of the company (Warren, Jonick and Schneider, 2020). Since various users of accounting

information base their future decisions over the demonstration as provided by the books

of accounts so it needs to be regulated.

Another major importance is that if the accountants are performing their functions with

integrity and honesty then any kind of fraudulent practices by the employees and

management of the company shall be discouraged, it will avoid any misrepresentations

and mistakes in the organization.

Lastly it can be assessed that accounting managers of the company are dealing with the

sensitive information of the company which needs to be protected from the other

competitors in the industry. For this reason it can be assessed that confidentiality must be

maintained by the accounting managers.

Fundamental principles of professional ethics for accountants

There are five fundamental principles that are necessary for the accountants to follow in

order to ensure the ethical code of conduct in the organization. The fundamental principles of

professional ethics are described below:- Integrity- This principle indicates that an accountant must be straightforward and honest

in their approach and managing all the professional and business relationships.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Objectivity- This fundamental principle states that an accountant must not be bias, undue

influenced or must not have conflict of interests that can override or influence the

professional or business judgement pertaining to the accounting results of the company. Professional competence and due care- This fundamental principle suggests that an

accountant who is providing the professional service to the client has to be updated by all

the amendments, legislations and knowledgeable skills to provide highly competent

services to the clients. A professional must act due diligently while accounting and the

applicable standards and techniques such that the representations are true to the current

position of the company. Confidentiality- It assesses that the professional accountant who is providing services

must maintain confidentiality of the sensitive data that is handled by them and should not

disclose it to the third party unless they are authorized to do so or are legally permitted to

disclose the facts associated with the company (Garbowski and et.al., 2019). The

accountant shall only access the information for which they are permitted and will also

not let third party know any of the details related to the professional and business

relationships shared by the accountant.

Professional behaviour- It explains that the actions and behaviour of the accountant must

be governing the compliance of the laws and regulations as suggested by legislations and

should avoid any of the activities that are discrediting the profession and its code of

conduct.

CONCLUSION

It can be summarized from the above project that both the financial and the non-financial

information of the company are of significant use while determining the status and position of

the business. Based on this analysis the users of the accounting information are able to draw

conclusions and take the decisions in respect of the organization. The financial information can

be drawn from the financial statements of the company and the ratio analysis statement that is

comparing the past and current position of the company. Apart from that for the other non-

financial information regarding the entity can be evaluated from the balance scorecard which is

determining the customer perspectives, innovation and the learning and growth of the

organization. Apart from that it analyses that the professional accountants are to strictly follow

the ethical code of conduct in the business through the compliance with the several fundamental

8

influenced or must not have conflict of interests that can override or influence the

professional or business judgement pertaining to the accounting results of the company. Professional competence and due care- This fundamental principle suggests that an

accountant who is providing the professional service to the client has to be updated by all

the amendments, legislations and knowledgeable skills to provide highly competent

services to the clients. A professional must act due diligently while accounting and the

applicable standards and techniques such that the representations are true to the current

position of the company. Confidentiality- It assesses that the professional accountant who is providing services

must maintain confidentiality of the sensitive data that is handled by them and should not

disclose it to the third party unless they are authorized to do so or are legally permitted to

disclose the facts associated with the company (Garbowski and et.al., 2019). The

accountant shall only access the information for which they are permitted and will also

not let third party know any of the details related to the professional and business

relationships shared by the accountant.

Professional behaviour- It explains that the actions and behaviour of the accountant must

be governing the compliance of the laws and regulations as suggested by legislations and

should avoid any of the activities that are discrediting the profession and its code of

conduct.

CONCLUSION

It can be summarized from the above project that both the financial and the non-financial

information of the company are of significant use while determining the status and position of

the business. Based on this analysis the users of the accounting information are able to draw

conclusions and take the decisions in respect of the organization. The financial information can

be drawn from the financial statements of the company and the ratio analysis statement that is

comparing the past and current position of the company. Apart from that for the other non-

financial information regarding the entity can be evaluated from the balance scorecard which is

determining the customer perspectives, innovation and the learning and growth of the

organization. Apart from that it analyses that the professional accountants are to strictly follow

the ethical code of conduct in the business through the compliance with the several fundamental

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

principles. This is necessary to generate the public trust, provide fair view and to prevent the

company from fraudulent activities.

9

company from fraudulent activities.

9

REFERENCES

Books and Journals

Garbowski, M. and et.al., 2019. Financial accounting of E-business enterprises. Academy of

Accounting and Financial Studies Journal. 23. pp.1-5.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2018. Financial Accounting with International

Financial Reporting Standards. John Wiley & Sons.

McCallig, J., Robb, A. and Rohde, F., 2019. Establishing the representational faithfulness of

financial accounting information using multiparty security, network analysis and a

blockchain. International Journal of Accounting Information Systems. 33. pp.47-58.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: Tools for business

decision making. John Wiley & Sons.

Herrador-Alcaide, T. C., Hernández-Solís, M. and Galván, R. S., 2019. Feelings of satisfaction in

mature students of financial accounting in a virtual learning environment: an experience

of measurement in higher education. International Journal of Educational Technology

in Higher Education. 16(1). pp.1-19.

Inuwa, U. and Baraya, A. U., 2017. Effects of cooperative and guided discovery approach on

financial accounting achievement among secondary school students. ATBU Journal of

Science, Technology and Education. 5(2). pp.60-70.

Online

The IASB’s Conceptual Framework for Financial Reporting. 2021. [Online] Available through:

<https://www.acowtancy.com/textbook/acca-fa/b1-the-qualitative-characteristics-of-

financial-information/qualitative-characteristics-1/notes>

10

Books and Journals

Garbowski, M. and et.al., 2019. Financial accounting of E-business enterprises. Academy of

Accounting and Financial Studies Journal. 23. pp.1-5.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2018. Financial Accounting with International

Financial Reporting Standards. John Wiley & Sons.

McCallig, J., Robb, A. and Rohde, F., 2019. Establishing the representational faithfulness of

financial accounting information using multiparty security, network analysis and a

blockchain. International Journal of Accounting Information Systems. 33. pp.47-58.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: Tools for business

decision making. John Wiley & Sons.

Herrador-Alcaide, T. C., Hernández-Solís, M. and Galván, R. S., 2019. Feelings of satisfaction in

mature students of financial accounting in a virtual learning environment: an experience

of measurement in higher education. International Journal of Educational Technology

in Higher Education. 16(1). pp.1-19.

Inuwa, U. and Baraya, A. U., 2017. Effects of cooperative and guided discovery approach on

financial accounting achievement among secondary school students. ATBU Journal of

Science, Technology and Education. 5(2). pp.60-70.

Online

The IASB’s Conceptual Framework for Financial Reporting. 2021. [Online] Available through:

<https://www.acowtancy.com/textbook/acca-fa/b1-the-qualitative-characteristics-of-

financial-information/qualitative-characteristics-1/notes>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.