Consolidated Financial Statements Preparation and Analysis

VerifiedAdded on 2020/05/04

|8

|830

|59

AI Summary

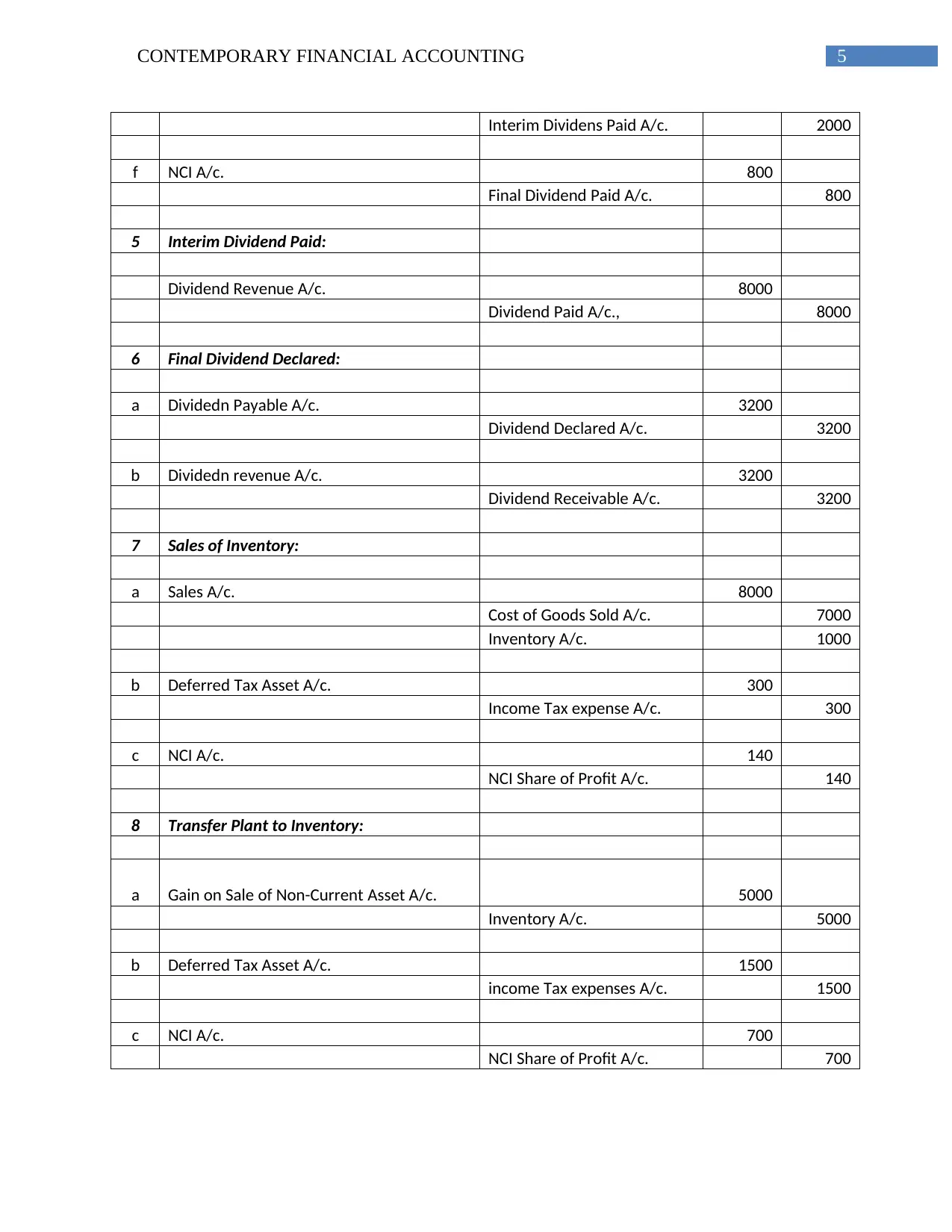

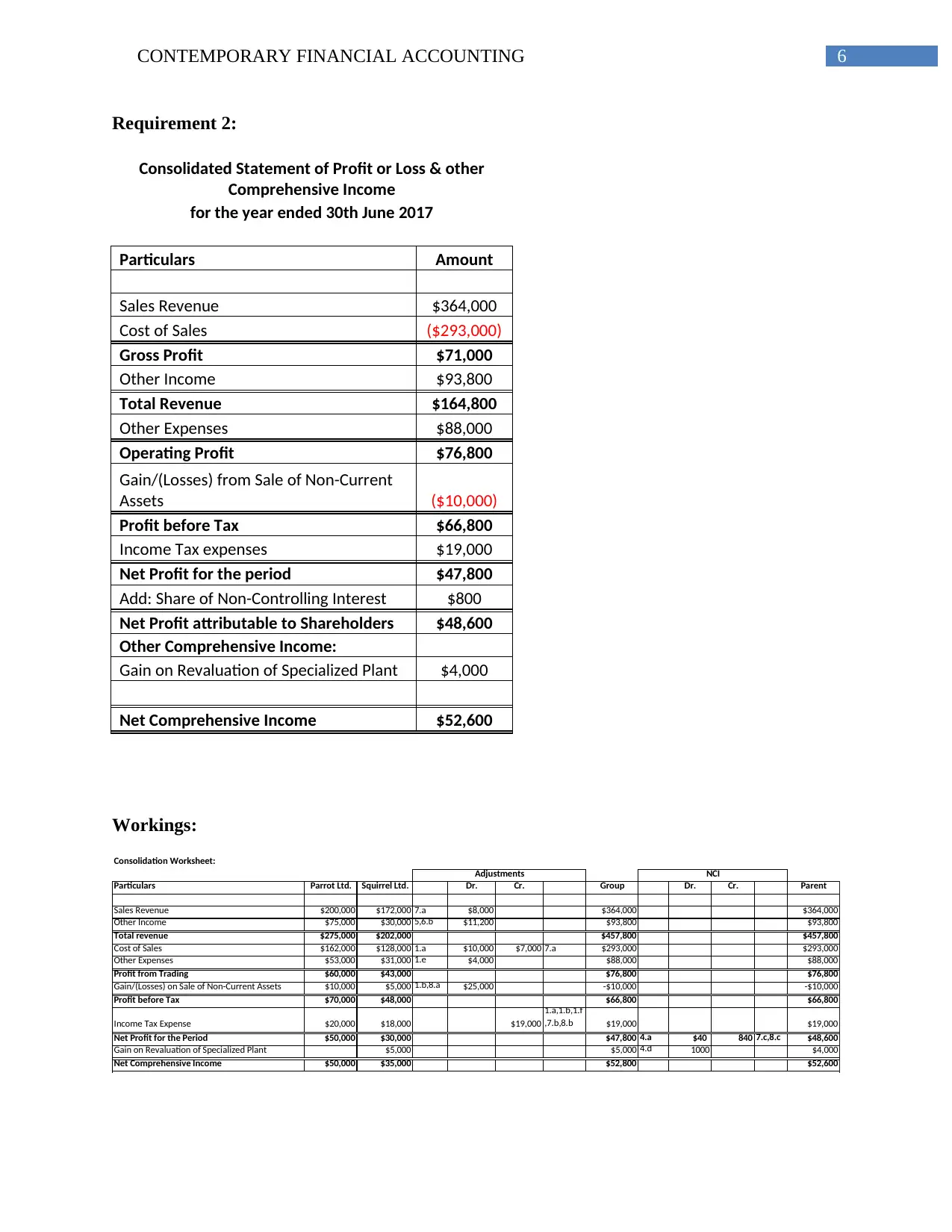

The task is to create a consolidated statement of profit or loss for a corporate group for the financial year ending on 30th June 2017. This involves aggregating financial data from multiple entities within the group while eliminating intercompany transactions. The assignment also includes accounting for non-controlling interests and understanding their impact on overall profitability. Key components such as sales revenue, cost of sales, other income, operating profit, taxes, and net profit attributable to shareholders must be accurately calculated and presented. Additionally, any comprehensive income items like gains from asset revaluation need inclusion in the final statement. This exercise provides insight into complex financial consolidation processes essential for accurate financial reporting and analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.