Financial Accounting: Consolidated Financial Position of Pee Group

VerifiedAdded on 2023/06/13

|13

|4325

|87

Report

AI Summary

This report provides a detailed analysis of Pee Group's financial accounting practices. It includes the preparation of a consolidated statement of financial position, a discussion of the relevance, reliability, and comparability of financial information, and an evaluation of the company's financial performance using ratio analysis. The report also examines the role of non-financial information in assessing future performance and discusses the fundamental principles of professional ethics for accountants. The analysis covers profitability, credit management, and growth aspects, utilizing data from provided appendices to offer a comprehensive overview of Pee Group's financial health and ethical considerations. Desklib is your go-to platform for similar assignments and study resources.

UG221 Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Preparation of the consolidated statement of financial position for Pee group..................3

b) Discussion about the relevance, reliability and comparability and the usage of these in

making financial information useful......................................................................................5

Question 2........................................................................................................................................6

a) Discussion about the following;.........................................................................................6

Comment on the financial performance of the business using appendix 1...................6

How does non-financial information give a better indication about the future which is

discussed in appendix 2 than appendix 1......................................................................8

b) Discussion related to professional ethics which are important in accounting and give details

about the five fundamental principles of professional ethics for accountants......................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Preparation of the consolidated statement of financial position for Pee group..................3

b) Discussion about the relevance, reliability and comparability and the usage of these in

making financial information useful......................................................................................5

Question 2........................................................................................................................................6

a) Discussion about the following;.........................................................................................6

Comment on the financial performance of the business using appendix 1...................6

How does non-financial information give a better indication about the future which is

discussed in appendix 2 than appendix 1......................................................................8

b) Discussion related to professional ethics which are important in accounting and give details

about the five fundamental principles of professional ethics for accountants......................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial accounting refers to a branch of accounting which includes the working related to

the recording, summarizing and reporting of the transactions which the business deals in. These

transactions are essential for the business to record and report to the diversified stakeholders of

the business (Acosta-González, Fernández-Rodríguez and Ganga, 2019). Financial accounting is

different from managerial accounting. This two accounting are interrelated but serve different

purposes for an organisation. Managerial accounting is concerned with catering for the wants of

business management and financial accounting is concerned with providing information related

to the business to the different stakeholders of the business and assisting them with decision

making. The following report highlights the concept of financial accounting. The principles

which are implemented by the international accounting standards board is also discussed in the

following report. A detailed interpretation of the financial ratio of an organisation.

Question 1

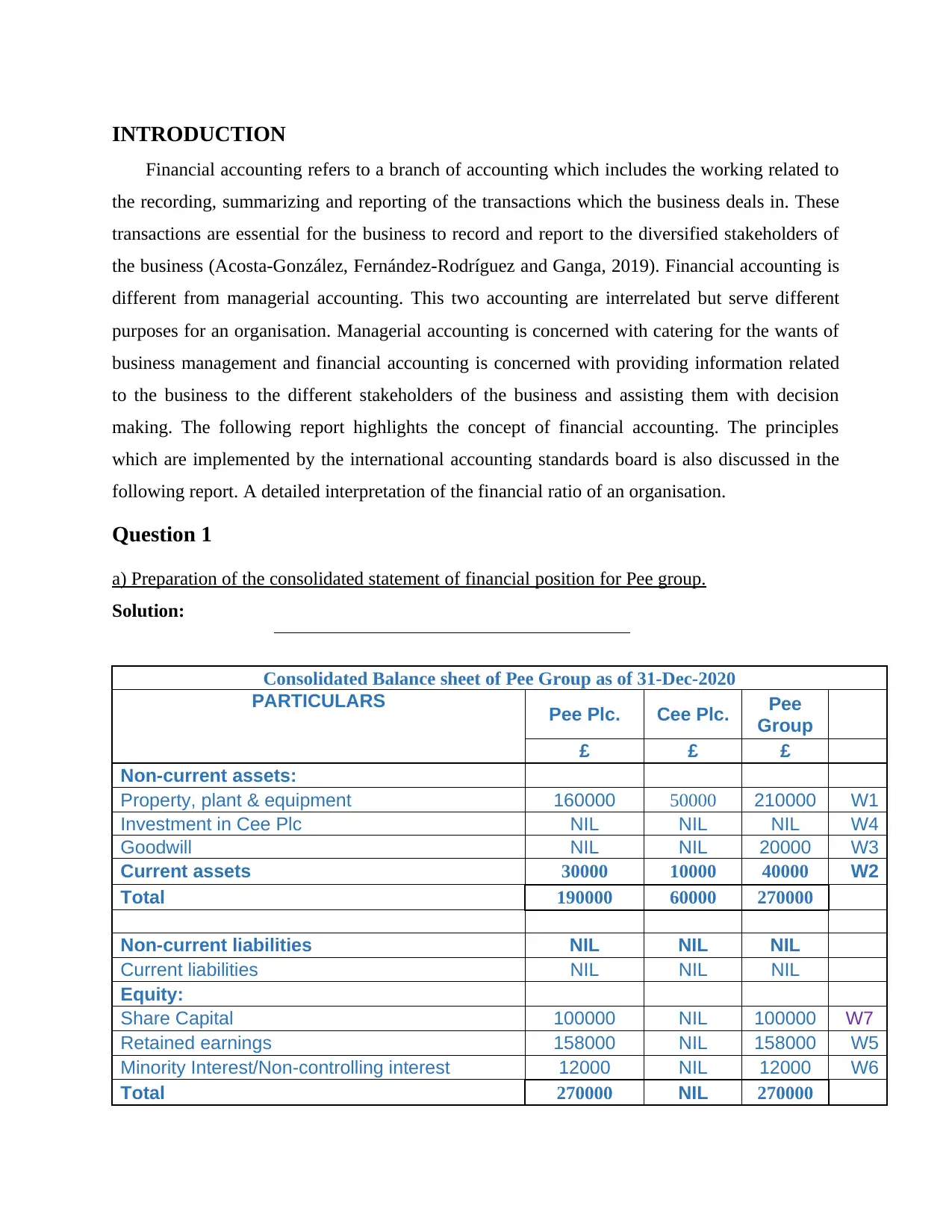

a) Preparation of the consolidated statement of financial position for Pee group.

Solution:

Consolidated Balance sheet of Pee Group as of 31-Dec-2020

PARTICULARS Pee Plc. Cee Plc. Pee

Group

£ £ £

Non-current assets:

Property, plant & equipment 160000 50000 210000 W1

Investment in Cee Plc NIL NIL NIL W4

Goodwill NIL NIL 20000 W3

Current assets 30000 10000 40000 W2

Total 190000 60000 270000

Non-current liabilities NIL NIL NIL

Current liabilities NIL NIL NIL

Equity:

Share Capital 100000 NIL 100000 W7

Retained earnings 158000 NIL 158000 W5

Minority Interest/Non-controlling interest 12000 NIL 12000 W6

Total 270000 NIL 270000

Financial accounting refers to a branch of accounting which includes the working related to

the recording, summarizing and reporting of the transactions which the business deals in. These

transactions are essential for the business to record and report to the diversified stakeholders of

the business (Acosta-González, Fernández-Rodríguez and Ganga, 2019). Financial accounting is

different from managerial accounting. This two accounting are interrelated but serve different

purposes for an organisation. Managerial accounting is concerned with catering for the wants of

business management and financial accounting is concerned with providing information related

to the business to the different stakeholders of the business and assisting them with decision

making. The following report highlights the concept of financial accounting. The principles

which are implemented by the international accounting standards board is also discussed in the

following report. A detailed interpretation of the financial ratio of an organisation.

Question 1

a) Preparation of the consolidated statement of financial position for Pee group.

Solution:

Consolidated Balance sheet of Pee Group as of 31-Dec-2020

PARTICULARS Pee Plc. Cee Plc. Pee

Group

£ £ £

Non-current assets:

Property, plant & equipment 160000 50000 210000 W1

Investment in Cee Plc NIL NIL NIL W4

Goodwill NIL NIL 20000 W3

Current assets 30000 10000 40000 W2

Total 190000 60000 270000

Non-current liabilities NIL NIL NIL

Current liabilities NIL NIL NIL

Equity:

Share Capital 100000 NIL 100000 W7

Retained earnings 158000 NIL 158000 W5

Minority Interest/Non-controlling interest 12000 NIL 12000 W6

Total 270000 NIL 270000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

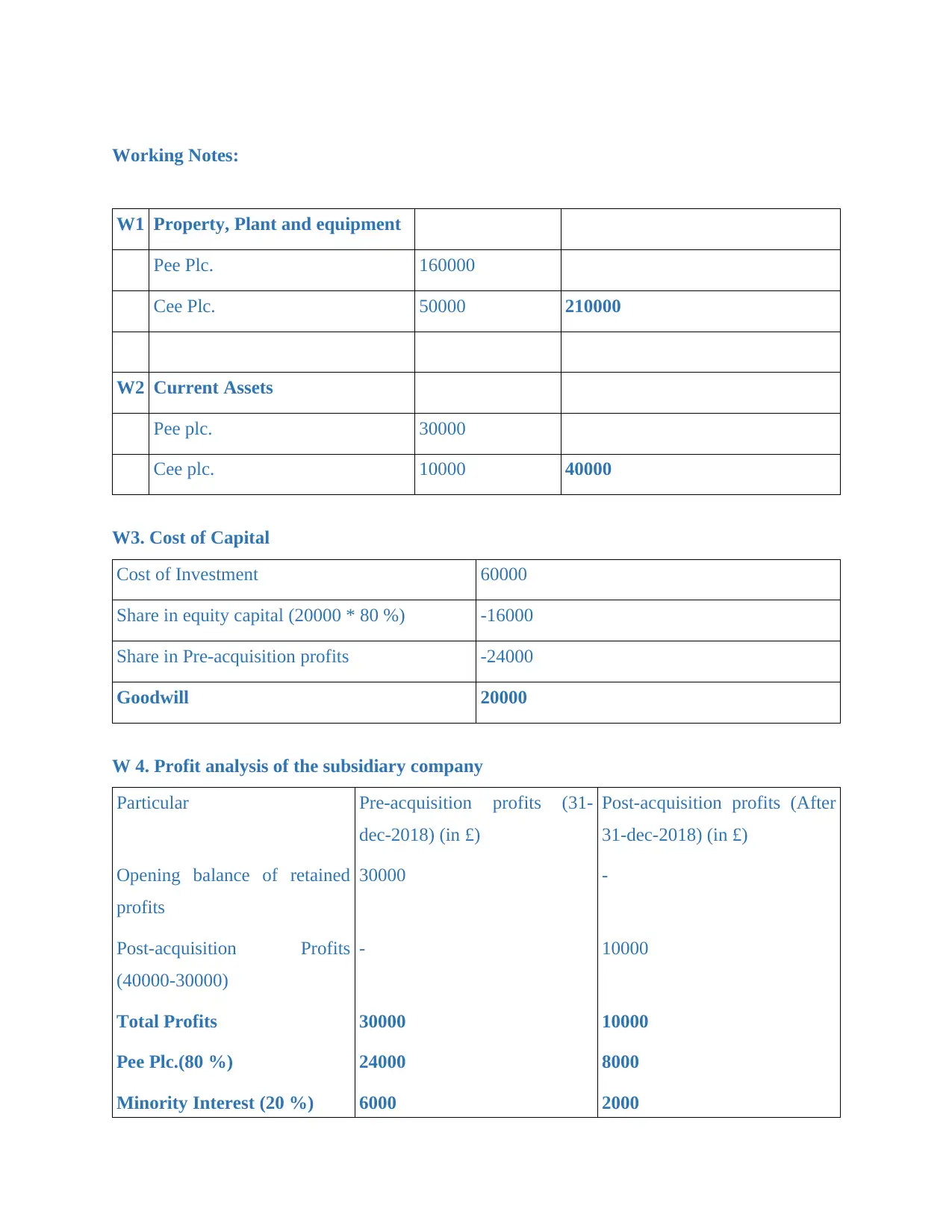

Working Notes:

W1 Property, Plant and equipment

Pee Plc. 160000

Cee Plc. 50000 210000

W2 Current Assets

Pee plc. 30000

Cee plc. 10000 40000

W3. Cost of Capital

Cost of Investment 60000

Share in equity capital (20000 * 80 %) -16000

Share in Pre-acquisition profits -24000

Goodwill 20000

W 4. Profit analysis of the subsidiary company

Particular Pre-acquisition profits (31-

dec-2018) (in £)

Post-acquisition profits (After

31-dec-2018) (in £)

Opening balance of retained

profits

30000 -

Post-acquisition Profits

(40000-30000)

- 10000

Total Profits 30000 10000

Pee Plc.(80 %) 24000 8000

Minority Interest (20 %) 6000 2000

W1 Property, Plant and equipment

Pee Plc. 160000

Cee Plc. 50000 210000

W2 Current Assets

Pee plc. 30000

Cee plc. 10000 40000

W3. Cost of Capital

Cost of Investment 60000

Share in equity capital (20000 * 80 %) -16000

Share in Pre-acquisition profits -24000

Goodwill 20000

W 4. Profit analysis of the subsidiary company

Particular Pre-acquisition profits (31-

dec-2018) (in £)

Post-acquisition profits (After

31-dec-2018) (in £)

Opening balance of retained

profits

30000 -

Post-acquisition Profits

(40000-30000)

- 10000

Total Profits 30000 10000

Pee Plc.(80 %) 24000 8000

Minority Interest (20 %) 6000 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

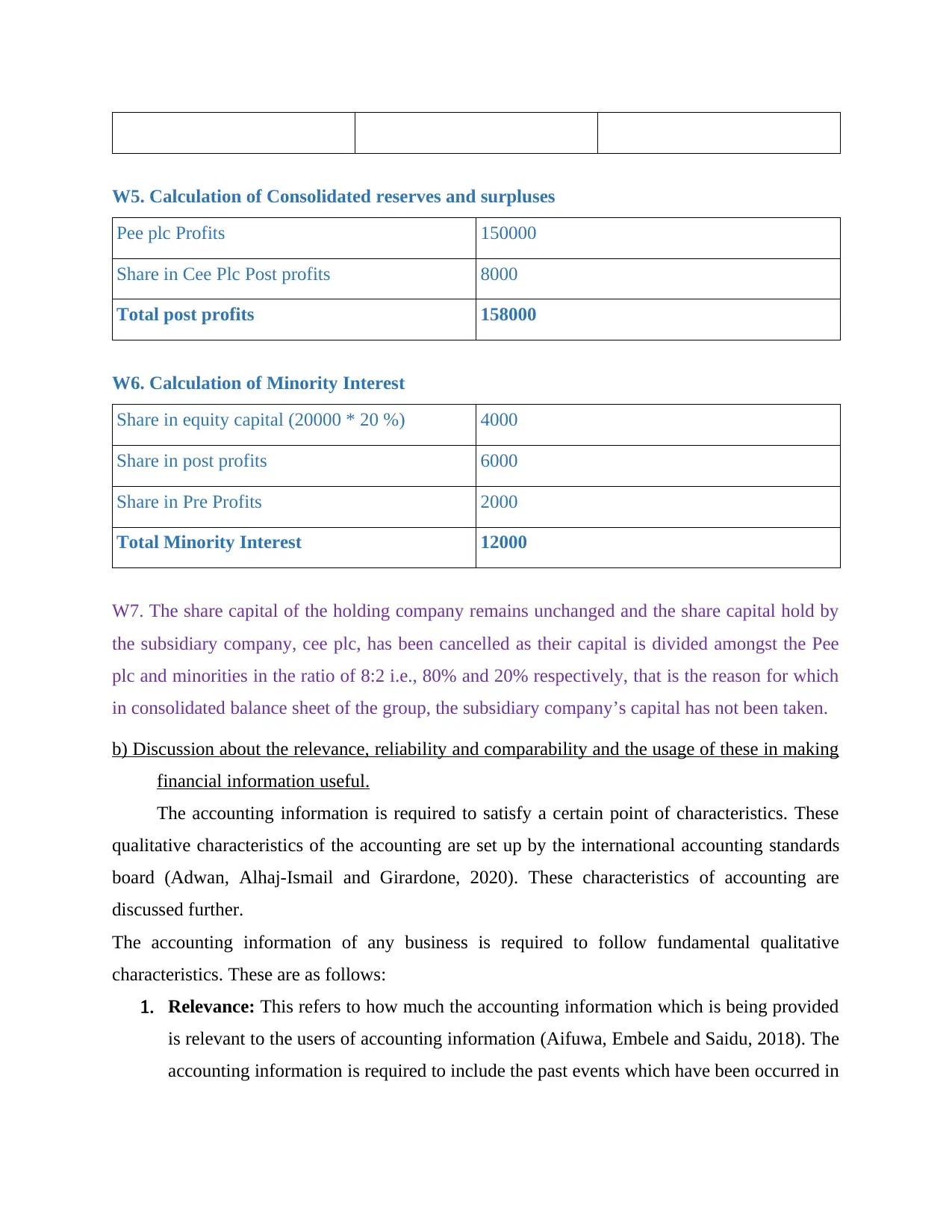

W5. Calculation of Consolidated reserves and surpluses

Pee plc Profits 150000

Share in Cee Plc Post profits 8000

Total post profits 158000

W6. Calculation of Minority Interest

Share in equity capital (20000 * 20 %) 4000

Share in post profits 6000

Share in Pre Profits 2000

Total Minority Interest 12000

W7. The share capital of the holding company remains unchanged and the share capital hold by

the subsidiary company, cee plc, has been cancelled as their capital is divided amongst the Pee

plc and minorities in the ratio of 8:2 i.e., 80% and 20% respectively, that is the reason for which

in consolidated balance sheet of the group, the subsidiary company’s capital has not been taken.

b) Discussion about the relevance, reliability and comparability and the usage of these in making

financial information useful.

The accounting information is required to satisfy a certain point of characteristics. These

qualitative characteristics of the accounting are set up by the international accounting standards

board (Adwan, Alhaj-Ismail and Girardone, 2020). These characteristics of accounting are

discussed further.

The accounting information of any business is required to follow fundamental qualitative

characteristics. These are as follows:

1. Relevance: This refers to how much the accounting information which is being provided

is relevant to the users of accounting information (Aifuwa, Embele and Saidu, 2018). The

accounting information is required to include the past events which have been occurred in

Pee plc Profits 150000

Share in Cee Plc Post profits 8000

Total post profits 158000

W6. Calculation of Minority Interest

Share in equity capital (20000 * 20 %) 4000

Share in post profits 6000

Share in Pre Profits 2000

Total Minority Interest 12000

W7. The share capital of the holding company remains unchanged and the share capital hold by

the subsidiary company, cee plc, has been cancelled as their capital is divided amongst the Pee

plc and minorities in the ratio of 8:2 i.e., 80% and 20% respectively, that is the reason for which

in consolidated balance sheet of the group, the subsidiary company’s capital has not been taken.

b) Discussion about the relevance, reliability and comparability and the usage of these in making

financial information useful.

The accounting information is required to satisfy a certain point of characteristics. These

qualitative characteristics of the accounting are set up by the international accounting standards

board (Adwan, Alhaj-Ismail and Girardone, 2020). These characteristics of accounting are

discussed further.

The accounting information of any business is required to follow fundamental qualitative

characteristics. These are as follows:

1. Relevance: This refers to how much the accounting information which is being provided

is relevant to the users of accounting information (Aifuwa, Embele and Saidu, 2018). The

accounting information is required to include the past events which have been occurred in

the business and also some of the insights which help the users of business information to

be predictive about the possible events which may occur in future.

2. Representational faithfulness: This refers to the reliability of the accounting

information which is required by the users of accounting information. This principle

checks how accurately does the business perform and manage its accounting activities

(Akinwale, 2020). The financial information of the business is required to be complete,

neutral and free from error.

3. Timeliness: This principle refers to the timeliness of the information that is required to

be available to the users of accounting information. The timeliness of the accounting

information is required as the year when the business is operating, the information of the

same year is required to be reported to the different stakeholders as they need to make

decisions for the same.

4. Verifiability: The accounting information is required to be one that can be verified from

the different sources of finance (Awang, Rahman and Ismail, 2019). The verifiability of

the accounting information is important as the users of this information need to check

whether the information provided is correct or not.

Question 2

a) Discussion about the following;

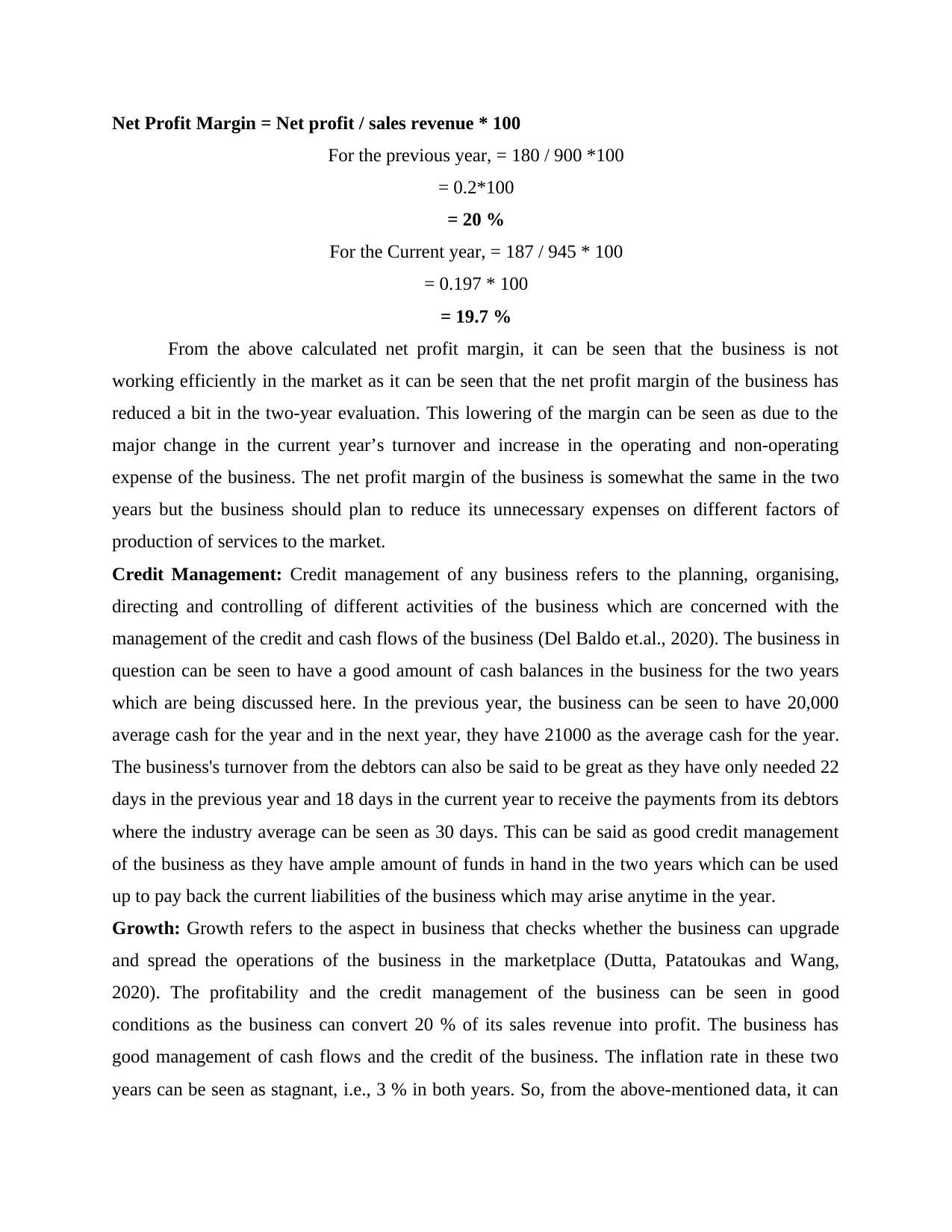

Comment on the financial performance of the business using appendix 1

The financial performance of any business refers to how great a company is working in a

marketplace. The financial performance measure gets essential as the management and other

stakeholders of the business need to ascertain if the business is providing a good rate to return to

its different stakeholders (Baranek, 2018). Following are the required financial ratio analysis

which will help in the discussion about the financial performance of Patrick Financial Services.

Profitability: Profitability refers to the ability of the business to convert its income earned by the

business into profits for the business. The profits of the business are required to be high if the

business is focusing on growth and spreading the business in the vast business marketplace.

Following is the calculation of the net profit margin of the business to check the profitability of

the business;

be predictive about the possible events which may occur in future.

2. Representational faithfulness: This refers to the reliability of the accounting

information which is required by the users of accounting information. This principle

checks how accurately does the business perform and manage its accounting activities

(Akinwale, 2020). The financial information of the business is required to be complete,

neutral and free from error.

3. Timeliness: This principle refers to the timeliness of the information that is required to

be available to the users of accounting information. The timeliness of the accounting

information is required as the year when the business is operating, the information of the

same year is required to be reported to the different stakeholders as they need to make

decisions for the same.

4. Verifiability: The accounting information is required to be one that can be verified from

the different sources of finance (Awang, Rahman and Ismail, 2019). The verifiability of

the accounting information is important as the users of this information need to check

whether the information provided is correct or not.

Question 2

a) Discussion about the following;

Comment on the financial performance of the business using appendix 1

The financial performance of any business refers to how great a company is working in a

marketplace. The financial performance measure gets essential as the management and other

stakeholders of the business need to ascertain if the business is providing a good rate to return to

its different stakeholders (Baranek, 2018). Following are the required financial ratio analysis

which will help in the discussion about the financial performance of Patrick Financial Services.

Profitability: Profitability refers to the ability of the business to convert its income earned by the

business into profits for the business. The profits of the business are required to be high if the

business is focusing on growth and spreading the business in the vast business marketplace.

Following is the calculation of the net profit margin of the business to check the profitability of

the business;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Profit Margin = Net profit / sales revenue * 100

For the previous year, = 180 / 900 *100

= 0.2*100

= 20 %

For the Current year, = 187 / 945 * 100

= 0.197 * 100

= 19.7 %

From the above calculated net profit margin, it can be seen that the business is not

working efficiently in the market as it can be seen that the net profit margin of the business has

reduced a bit in the two-year evaluation. This lowering of the margin can be seen as due to the

major change in the current year’s turnover and increase in the operating and non-operating

expense of the business. The net profit margin of the business is somewhat the same in the two

years but the business should plan to reduce its unnecessary expenses on different factors of

production of services to the market.

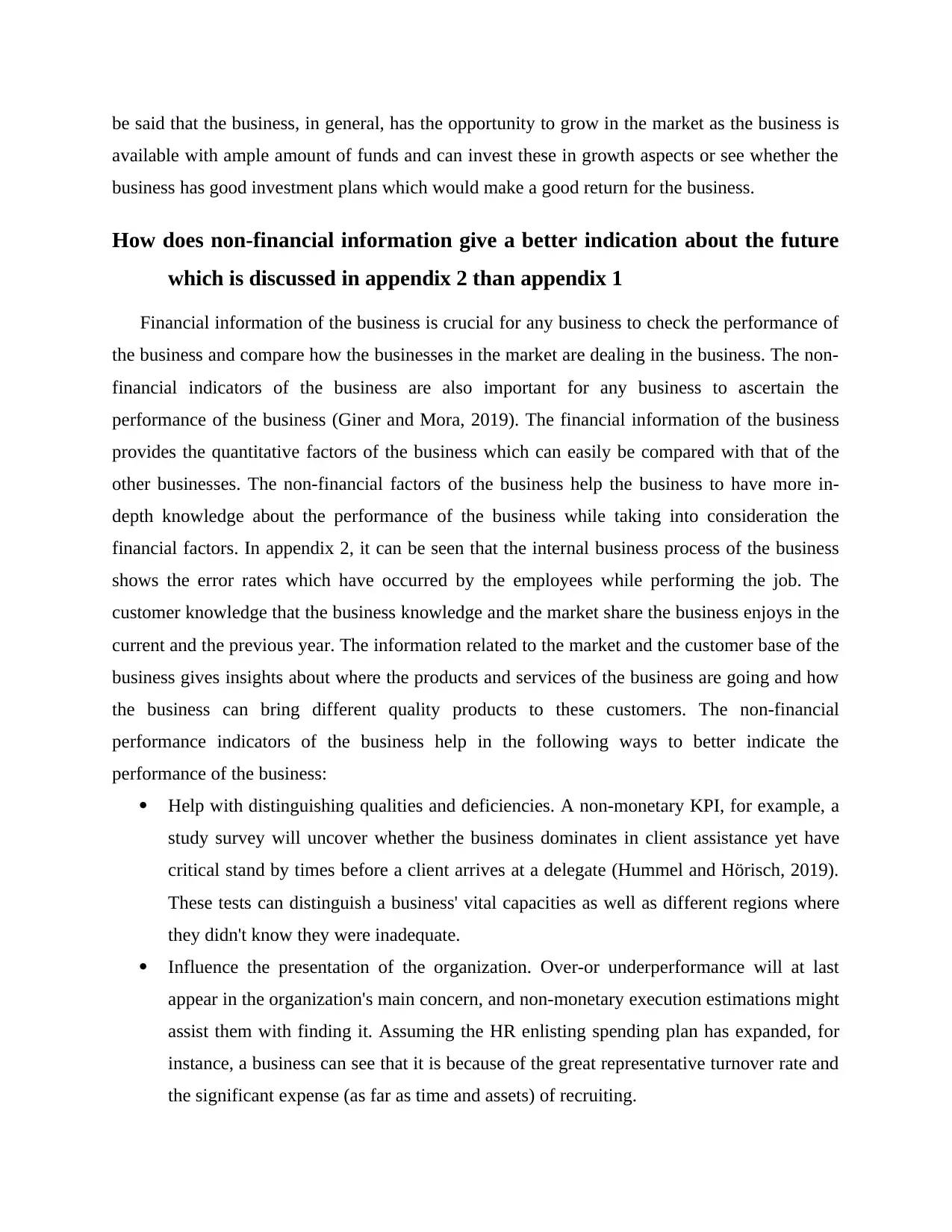

Credit Management: Credit management of any business refers to the planning, organising,

directing and controlling of different activities of the business which are concerned with the

management of the credit and cash flows of the business (Del Baldo et.al., 2020). The business in

question can be seen to have a good amount of cash balances in the business for the two years

which are being discussed here. In the previous year, the business can be seen to have 20,000

average cash for the year and in the next year, they have 21000 as the average cash for the year.

The business's turnover from the debtors can also be said to be great as they have only needed 22

days in the previous year and 18 days in the current year to receive the payments from its debtors

where the industry average can be seen as 30 days. This can be said as good credit management

of the business as they have ample amount of funds in hand in the two years which can be used

up to pay back the current liabilities of the business which may arise anytime in the year.

Growth: Growth refers to the aspect in business that checks whether the business can upgrade

and spread the operations of the business in the marketplace (Dutta, Patatoukas and Wang,

2020). The profitability and the credit management of the business can be seen in good

conditions as the business can convert 20 % of its sales revenue into profit. The business has

good management of cash flows and the credit of the business. The inflation rate in these two

years can be seen as stagnant, i.e., 3 % in both years. So, from the above-mentioned data, it can

For the previous year, = 180 / 900 *100

= 0.2*100

= 20 %

For the Current year, = 187 / 945 * 100

= 0.197 * 100

= 19.7 %

From the above calculated net profit margin, it can be seen that the business is not

working efficiently in the market as it can be seen that the net profit margin of the business has

reduced a bit in the two-year evaluation. This lowering of the margin can be seen as due to the

major change in the current year’s turnover and increase in the operating and non-operating

expense of the business. The net profit margin of the business is somewhat the same in the two

years but the business should plan to reduce its unnecessary expenses on different factors of

production of services to the market.

Credit Management: Credit management of any business refers to the planning, organising,

directing and controlling of different activities of the business which are concerned with the

management of the credit and cash flows of the business (Del Baldo et.al., 2020). The business in

question can be seen to have a good amount of cash balances in the business for the two years

which are being discussed here. In the previous year, the business can be seen to have 20,000

average cash for the year and in the next year, they have 21000 as the average cash for the year.

The business's turnover from the debtors can also be said to be great as they have only needed 22

days in the previous year and 18 days in the current year to receive the payments from its debtors

where the industry average can be seen as 30 days. This can be said as good credit management

of the business as they have ample amount of funds in hand in the two years which can be used

up to pay back the current liabilities of the business which may arise anytime in the year.

Growth: Growth refers to the aspect in business that checks whether the business can upgrade

and spread the operations of the business in the marketplace (Dutta, Patatoukas and Wang,

2020). The profitability and the credit management of the business can be seen in good

conditions as the business can convert 20 % of its sales revenue into profit. The business has

good management of cash flows and the credit of the business. The inflation rate in these two

years can be seen as stagnant, i.e., 3 % in both years. So, from the above-mentioned data, it can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be said that the business, in general, has the opportunity to grow in the market as the business is

available with ample amount of funds and can invest these in growth aspects or see whether the

business has good investment plans which would make a good return for the business.

How does non-financial information give a better indication about the future

which is discussed in appendix 2 than appendix 1

Financial information of the business is crucial for any business to check the performance of

the business and compare how the businesses in the market are dealing in the business. The non-

financial indicators of the business are also important for any business to ascertain the

performance of the business (Giner and Mora, 2019). The financial information of the business

provides the quantitative factors of the business which can easily be compared with that of the

other businesses. The non-financial factors of the business help the business to have more in-

depth knowledge about the performance of the business while taking into consideration the

financial factors. In appendix 2, it can be seen that the internal business process of the business

shows the error rates which have occurred by the employees while performing the job. The

customer knowledge that the business knowledge and the market share the business enjoys in the

current and the previous year. The information related to the market and the customer base of the

business gives insights about where the products and services of the business are going and how

the business can bring different quality products to these customers. The non-financial

performance indicators of the business help in the following ways to better indicate the

performance of the business:

Help with distinguishing qualities and deficiencies. A non-monetary KPI, for example, a

study survey will uncover whether the business dominates in client assistance yet have

critical stand by times before a client arrives at a delegate (Hummel and Hörisch, 2019).

These tests can distinguish a business' vital capacities as well as different regions where

they didn't know they were inadequate.

Influence the presentation of the organization. Over-or underperformance will at last

appear in the organization's main concern, and non-monetary execution estimations might

assist them with finding it. Assuming the HR enlisting spending plan has expanded, for

instance, a business can see that it is because of the great representative turnover rate and

the significant expense (as far as time and assets) of recruiting.

available with ample amount of funds and can invest these in growth aspects or see whether the

business has good investment plans which would make a good return for the business.

How does non-financial information give a better indication about the future

which is discussed in appendix 2 than appendix 1

Financial information of the business is crucial for any business to check the performance of

the business and compare how the businesses in the market are dealing in the business. The non-

financial indicators of the business are also important for any business to ascertain the

performance of the business (Giner and Mora, 2019). The financial information of the business

provides the quantitative factors of the business which can easily be compared with that of the

other businesses. The non-financial factors of the business help the business to have more in-

depth knowledge about the performance of the business while taking into consideration the

financial factors. In appendix 2, it can be seen that the internal business process of the business

shows the error rates which have occurred by the employees while performing the job. The

customer knowledge that the business knowledge and the market share the business enjoys in the

current and the previous year. The information related to the market and the customer base of the

business gives insights about where the products and services of the business are going and how

the business can bring different quality products to these customers. The non-financial

performance indicators of the business help in the following ways to better indicate the

performance of the business:

Help with distinguishing qualities and deficiencies. A non-monetary KPI, for example, a

study survey will uncover whether the business dominates in client assistance yet have

critical stand by times before a client arrives at a delegate (Hummel and Hörisch, 2019).

These tests can distinguish a business' vital capacities as well as different regions where

they didn't know they were inadequate.

Influence the presentation of the organization. Over-or underperformance will at last

appear in the organization's main concern, and non-monetary execution estimations might

assist them with finding it. Assuming the HR enlisting spending plan has expanded, for

instance, a business can see that it is because of the great representative turnover rate and

the significant expense (as far as time and assets) of recruiting.

Further develop representative contribution on the most proficient method to accomplish

vital objectives. Non-monetary KPIs are specific, quantifiable, and stepping stool up to

the association's 10,000 foot view objective when accurately created. Individuals from

the group can see precisely what they need to achieve to meet their goals, as well as why

they need to run a similar report consistently or what their participation rates mean for

usefulness (Lahouel and et.al., 2019). The ordinary tasks and vital bearing are inseparably

connected.

Are more eaasy in making up for superfluous impacts. Each association stands up to

outer dangers that are outside its ability to do anything about and can impact key

measurements like deals and expenses. Downturns, wars, and catastrophic events are

inevitable and wild. In these cases, assuming organizations just checked out monetary

KPIs, apparently the organization's exhibition was irredeemable. Non-monetary

execution estimations, then again, are fundamentally influenced quite a bit by and can

give a more far reaching picture (Pavone and Migliaccio, 2021). They are prevailing in

urgent region of their arrangement if get passing marks for corporate culture and client

bliss in the midst of an exchange war, and that should pay off over the long haul.Using

appendix 2, comment on the performance of the business.

From Appendix 2 following points can be commented on the performance of the business:

From the Internal business processes of the business, it can be seen that the job

completion time of the business has been reduced by 3 weeks on average which is

concerning. The errors done in the jobs by the employees have also increased by 6 % in

the two-year analysis of the business. It can be said that both these factors are somewhat

dependent on each other, as, due to the decrease in the job completion time of the

business, error rates in the job have increased majorly.

From the customer knowledge of the business, it can be seen that the number of

customers per year has reduced. The market share of the business can also be seen as

reducing and now the business only enjoys a 14 % market share. Both these factors can

be said to be affecting this much due to the rise in the fee levels of the business. The

customers are exiting the operations of the business as the market has such firms working

in the same field of the business in question and providing services at a much lesser fee.

vital objectives. Non-monetary KPIs are specific, quantifiable, and stepping stool up to

the association's 10,000 foot view objective when accurately created. Individuals from

the group can see precisely what they need to achieve to meet their goals, as well as why

they need to run a similar report consistently or what their participation rates mean for

usefulness (Lahouel and et.al., 2019). The ordinary tasks and vital bearing are inseparably

connected.

Are more eaasy in making up for superfluous impacts. Each association stands up to

outer dangers that are outside its ability to do anything about and can impact key

measurements like deals and expenses. Downturns, wars, and catastrophic events are

inevitable and wild. In these cases, assuming organizations just checked out monetary

KPIs, apparently the organization's exhibition was irredeemable. Non-monetary

execution estimations, then again, are fundamentally influenced quite a bit by and can

give a more far reaching picture (Pavone and Migliaccio, 2021). They are prevailing in

urgent region of their arrangement if get passing marks for corporate culture and client

bliss in the midst of an exchange war, and that should pay off over the long haul.Using

appendix 2, comment on the performance of the business.

From Appendix 2 following points can be commented on the performance of the business:

From the Internal business processes of the business, it can be seen that the job

completion time of the business has been reduced by 3 weeks on average which is

concerning. The errors done in the jobs by the employees have also increased by 6 % in

the two-year analysis of the business. It can be said that both these factors are somewhat

dependent on each other, as, due to the decrease in the job completion time of the

business, error rates in the job have increased majorly.

From the customer knowledge of the business, it can be seen that the number of

customers per year has reduced. The market share of the business can also be seen as

reducing and now the business only enjoys a 14 % market share. Both these factors can

be said to be affecting this much due to the rise in the fee levels of the business. The

customers are exiting the operations of the business as the market has such firms working

in the same field of the business in question and providing services at a much lesser fee.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The growth rate of the business can be said that it is worsening. The employee retention

rate of the business has reduced from 80 % to 60 % which increases the employee

turnover of the business (Pokharel et.al., 2019). The revenue that the business is earning

from its non-core activities has decreased by 1 % when the industry average has

increased by 5 %. hence, it can clearly be said that the business other businesses in the

industry are working more efficiently and providing better non-core services to the

customers.

From the above-mentioned points, it can be said that the overall performance of the

business is deteriorating and the business need new plans and actions to amend their

image in the industry.

b) Discussion related to professional ethics which are important in accounting and give details

about the five fundamental principles of professional ethics for accountants.

Accounting ethics is a principal standard that bookkeepers should stick to while getting

ready budget summaries for a business. It's an assortment of decides to follow that have been laid

out by government-supported organizations. To stay away from any control of the fiscal

summaries, the bookkeeper ought to stick to bookkeeping morals. Accounting ethics must be

observed by all accountants, and if they do not, they may face financial penalties.

Accounting ethics has a long history that traces all the way back to 1494. The public

authority used to set up a board to take care of the organizations' advantages, however it has

become progressively hard for them to do as such. Accordingly, certain private organizations

were able to perform the responsibility for the organizations, though under the public authority's

oversight. These private groups are obligated to observe the government's norms and standards,

and every new rule must be approved by government authorities before becoming law. By the

year 1905, the accounting system in the United States of America had transformed. The

Association of Government Accountants was created as the government began to take

accounting bodies seriously. After these accountants had learnt and grasped the subject, the

Institute of Internal Auditors was created. The Institute of Internal Auditors was established to

determine whether or not businesses are keeping accurate books of accounts. The government

was eventually given access to the study. As a result of these adjustments, we now have a

competent accounting system in place.

Following are some of the reasons why ethics are there in the accounting field:

rate of the business has reduced from 80 % to 60 % which increases the employee

turnover of the business (Pokharel et.al., 2019). The revenue that the business is earning

from its non-core activities has decreased by 1 % when the industry average has

increased by 5 %. hence, it can clearly be said that the business other businesses in the

industry are working more efficiently and providing better non-core services to the

customers.

From the above-mentioned points, it can be said that the overall performance of the

business is deteriorating and the business need new plans and actions to amend their

image in the industry.

b) Discussion related to professional ethics which are important in accounting and give details

about the five fundamental principles of professional ethics for accountants.

Accounting ethics is a principal standard that bookkeepers should stick to while getting

ready budget summaries for a business. It's an assortment of decides to follow that have been laid

out by government-supported organizations. To stay away from any control of the fiscal

summaries, the bookkeeper ought to stick to bookkeeping morals. Accounting ethics must be

observed by all accountants, and if they do not, they may face financial penalties.

Accounting ethics has a long history that traces all the way back to 1494. The public

authority used to set up a board to take care of the organizations' advantages, however it has

become progressively hard for them to do as such. Accordingly, certain private organizations

were able to perform the responsibility for the organizations, though under the public authority's

oversight. These private groups are obligated to observe the government's norms and standards,

and every new rule must be approved by government authorities before becoming law. By the

year 1905, the accounting system in the United States of America had transformed. The

Association of Government Accountants was created as the government began to take

accounting bodies seriously. After these accountants had learnt and grasped the subject, the

Institute of Internal Auditors was created. The Institute of Internal Auditors was established to

determine whether or not businesses are keeping accurate books of accounts. The government

was eventually given access to the study. As a result of these adjustments, we now have a

competent accounting system in place.

Following are some of the reasons why ethics are there in the accounting field:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It's part of the job description for accountants: Bookkeeping and morals are inseparably

connected in the bookkeeping field (Sakr and Bedeir, 2019). As bookkeepers, we should

make evenhanded, fair decisions that benefit our clients. Assuming that the organization

benefits from the selling of one monetary item over another, the client might be exposed

to bias and falsehood. It is basic, as a feature of the moral code, that the data given isn't

affected by any other individual.

The information must be kept private: Any monetary data uncovered by a bookkeeping

master during a consolidation or obtaining, for instance, would be an infringement of the

trust code. The bookkeepers' activities would similarly be thought of as dishonest. An

organization or association can't do this except if there is a lawful reason to do as such, as

per the Ethics Code.

The employees' honesty: The organization's Ethics code ensures that all representatives

act with respectability and trustworthiness while working with clients and in other expert

commitment. Bookkeepers are additionally denied from distinguishing themselves with

any material that may be underhanded or hurtful to the client or the association, as per the

moral code.

The bookkeeping business is constantly creating, and the occupation of bookkeepers is

adjusting as new innovation, like robotized creditor liabilities, is presented. This implies

that bookkeepers should stay up with the latest to make right decisions on client

circumstance

Bookkeepers should follow all of the managing body's guidelines and guidelines, as per

the set of principles. This will help the firm to hold its impressive skill and assurance that

the fiscal reports precisely mirror the organization's status. Inability to follow the Ethics

code can hurt the organization's standing and maybe lead them to lawful issues.

All organizations are legally necessary to give right monetary data on their expense forms

(Ye and Hu, 2020). To diminish their monetary weight, a few organizations might offer

inaccurate data to the assessment specialists. In the event that they are recognized, they

might come up against indictments of prevarication and robust fines. The Code of Ethics

safeguards you by guaranteeing that you supply honest data while making good on

charges.

The five fundamental principles of professional ethics for accountants are as follows:

connected in the bookkeeping field (Sakr and Bedeir, 2019). As bookkeepers, we should

make evenhanded, fair decisions that benefit our clients. Assuming that the organization

benefits from the selling of one monetary item over another, the client might be exposed

to bias and falsehood. It is basic, as a feature of the moral code, that the data given isn't

affected by any other individual.

The information must be kept private: Any monetary data uncovered by a bookkeeping

master during a consolidation or obtaining, for instance, would be an infringement of the

trust code. The bookkeepers' activities would similarly be thought of as dishonest. An

organization or association can't do this except if there is a lawful reason to do as such, as

per the Ethics Code.

The employees' honesty: The organization's Ethics code ensures that all representatives

act with respectability and trustworthiness while working with clients and in other expert

commitment. Bookkeepers are additionally denied from distinguishing themselves with

any material that may be underhanded or hurtful to the client or the association, as per the

moral code.

The bookkeeping business is constantly creating, and the occupation of bookkeepers is

adjusting as new innovation, like robotized creditor liabilities, is presented. This implies

that bookkeepers should stay up with the latest to make right decisions on client

circumstance

Bookkeepers should follow all of the managing body's guidelines and guidelines, as per

the set of principles. This will help the firm to hold its impressive skill and assurance that

the fiscal reports precisely mirror the organization's status. Inability to follow the Ethics

code can hurt the organization's standing and maybe lead them to lawful issues.

All organizations are legally necessary to give right monetary data on their expense forms

(Ye and Hu, 2020). To diminish their monetary weight, a few organizations might offer

inaccurate data to the assessment specialists. In the event that they are recognized, they

might come up against indictments of prevarication and robust fines. The Code of Ethics

safeguards you by guaranteeing that you supply honest data while making good on

charges.

The five fundamental principles of professional ethics for accountants are as follows:

Integrity: In all proficient and corporate dealings, an expert bookkeeper ought to be

blunt and legitimate.

Objectivity: Inclination, irreconcilable circumstances, or excessive impact of others

ought not be permitted to best proficient or business choices by an expert bookkeeper.

Professional competence and due care: An expert bookkeeper has a constant

commitment to keep their expert information and ability cutting-edge to offer skilled

expert types of assistance to a client or business in view of current practice, regulation,

and methods (Ye, and Hu, 2020,). An expert bookkeeper should perform with

perseverance and stick to all relevant specialized and expert guidelines.

Confidentiality: An expert bookkeeper ought to keep up with the secrecy of data got by

means of expert and business associations and ought not uncover such data to outsiders

without adequate and express approval except if there is a legitimate or expert

commitment to do as such. Private data acquired by means of expert and business

communications ought not be used for the expert bookkeeper's or outsiders gain.

Professional Behaviour: An expert bookkeeper ought to observe every relevant rule and

guidelines and abstain from doing any activities that bring the calling into offensiveness.

CONCLUSION

From the above-mentioned report, it can be concluded that financial accounting is crucial for

businesses. The financial information is required to be relevant, reliable and reported at the right

time to be effective. The discussion related to the performance of the business based on its

financial and non-financial information is crucial for the business to make amends and plan for

the future. Bookkeeping Ethics is an exceptionally valuable and viable strategy for dealing with

bookkeeping in any firm. To promptly handle and apply to account, the bookkeeper needs to

have adequate preparation and be presented to different bookkeeping strategies. The five

fundamental principles of accounting make it important for accountants to follow.

blunt and legitimate.

Objectivity: Inclination, irreconcilable circumstances, or excessive impact of others

ought not be permitted to best proficient or business choices by an expert bookkeeper.

Professional competence and due care: An expert bookkeeper has a constant

commitment to keep their expert information and ability cutting-edge to offer skilled

expert types of assistance to a client or business in view of current practice, regulation,

and methods (Ye, and Hu, 2020,). An expert bookkeeper should perform with

perseverance and stick to all relevant specialized and expert guidelines.

Confidentiality: An expert bookkeeper ought to keep up with the secrecy of data got by

means of expert and business associations and ought not uncover such data to outsiders

without adequate and express approval except if there is a legitimate or expert

commitment to do as such. Private data acquired by means of expert and business

communications ought not be used for the expert bookkeeper's or outsiders gain.

Professional Behaviour: An expert bookkeeper ought to observe every relevant rule and

guidelines and abstain from doing any activities that bring the calling into offensiveness.

CONCLUSION

From the above-mentioned report, it can be concluded that financial accounting is crucial for

businesses. The financial information is required to be relevant, reliable and reported at the right

time to be effective. The discussion related to the performance of the business based on its

financial and non-financial information is crucial for the business to make amends and plan for

the future. Bookkeeping Ethics is an exceptionally valuable and viable strategy for dealing with

bookkeeping in any firm. To promptly handle and apply to account, the bookkeeper needs to

have adequate preparation and be presented to different bookkeeping strategies. The five

fundamental principles of accounting make it important for accountants to follow.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.