Holmes Institute HA2032 Corporate Accounting Assignment Report

VerifiedAdded on 2022/11/11

|15

|3320

|60

Report

AI Summary

This report analyzes corporate and financial accounting, focusing on a takeover scenario involving two ASX-listed companies, JKY Limited and FAB Limited. It examines consolidation accounting, equity accounting, and the application of AASB standards, including AASB 10 and AASB 128, to determine the most appropriate accounting methods for the acquisition. The report delves into intragroup transactions, highlighting the treatment of profits and the importance of reconciliation procedures, and addresses the impact of non-controlling interests (NCI) as per AASB 101. Furthermore, it explores the significance of financial statement disclosures, particularly concerning asset valuation, dividend payments, and return on capital, and emphasizes the role of accounting standards in providing reliable information for investor decision-making, including the impact of taxation and potential market risks. The report concludes by underscoring the importance of financial statement analysis for users and the role of AASB standards in ensuring the fair and true presentation of financial information.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The report has dealt with two companies who are listed in ASX and has gone

through the various aspects of the financial statements of both the companies. The

report has discussed various aspects of the financial reporting which shall benefit

various stakeholders of the companies that have been discussed in this report.

CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The report has dealt with two companies who are listed in ASX and has gone

through the various aspects of the financial statements of both the companies. The

report has discussed various aspects of the financial reporting which shall benefit

various stakeholders of the companies that have been discussed in this report.

3

CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Table of Contents.......................................................................................................2

Introduction...................................................................................................................3

PART A.........................................................................................................................3

Response..................................................................................................................3

Consolidated balance sheet......................................................................................5

PART B.........................................................................................................................6

PART C.........................................................................................................................9

Response..................................................................................................................9

Conclusion..................................................................................................................12

Reference List.............................................................................................................13

CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Table of Contents.......................................................................................................2

Introduction...................................................................................................................3

PART A.........................................................................................................................3

Response..................................................................................................................3

Consolidated balance sheet......................................................................................5

PART B.........................................................................................................................6

PART C.........................................................................................................................9

Response..................................................................................................................9

Conclusion..................................................................................................................12

Reference List.............................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE AND FINANCIAL ACCOUNTING

Introduction

Within the companies, the accounting standards are being regarded as a

significant component. Three parts of the accounting standards are being analyzed

within this paper. The consolidated, as well as the equity accounting, are being

considered within the first part. The AASB 10 and the AASB 128 are being regarded

within this segment. The intragroup transaction of the company JKY limited is being

considered within the second part. A detailed analyzation is being performed over

the accounting standard of AASB 10 and 127. The NCI disclosure is being

considered within the third segment as per the requirement of AASB 101. The whole

section is being summarised within the task.

PART A

Response

The desire of the JKY limited is to acquire FAB limited. This is a company

which is listed in ASX. A suitable profit is present within the treasury of this company.

Choices are there for increasing the profit of the company. The guidelines of the

purchases and joint ventures are being issued by the AASB 128. These are the

guidelines which are required to be followed by the company. Two possible options

are there for attaining the FAB limited which are the method of purchase and the

acquisition where the direct purchase of the company is being implied and the

second option is about the involvement of the acquisition for attaining the company

shares (Watson, 2015). A major amount of profit is being attained by the company

over both the options considering the acquisitions. A special case of the

consolidation as well as equity accounting as per the consequences which are

discussed in the chart:

CORPORATE AND FINANCIAL ACCOUNTING

Introduction

Within the companies, the accounting standards are being regarded as a

significant component. Three parts of the accounting standards are being analyzed

within this paper. The consolidated, as well as the equity accounting, are being

considered within the first part. The AASB 10 and the AASB 128 are being regarded

within this segment. The intragroup transaction of the company JKY limited is being

considered within the second part. A detailed analyzation is being performed over

the accounting standard of AASB 10 and 127. The NCI disclosure is being

considered within the third segment as per the requirement of AASB 101. The whole

section is being summarised within the task.

PART A

Response

The desire of the JKY limited is to acquire FAB limited. This is a company

which is listed in ASX. A suitable profit is present within the treasury of this company.

Choices are there for increasing the profit of the company. The guidelines of the

purchases and joint ventures are being issued by the AASB 128. These are the

guidelines which are required to be followed by the company. Two possible options

are there for attaining the FAB limited which are the method of purchase and the

acquisition where the direct purchase of the company is being implied and the

second option is about the involvement of the acquisition for attaining the company

shares (Watson, 2015). A major amount of profit is being attained by the company

over both the options considering the acquisitions. A special case of the

consolidation as well as equity accounting as per the consequences which are

discussed in the chart:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE AND FINANCIAL ACCOUNTING

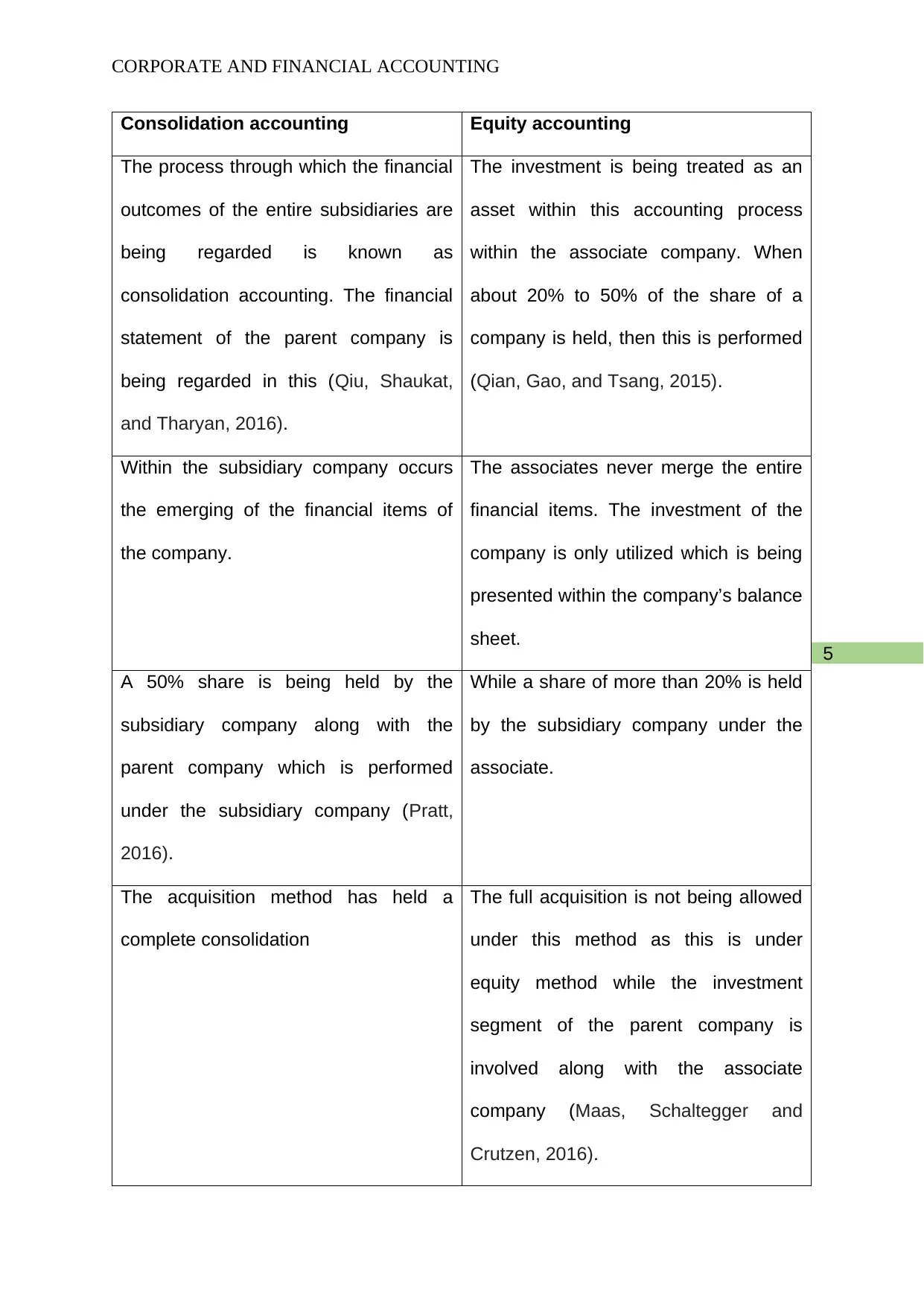

Consolidation accounting Equity accounting

The process through which the financial

outcomes of the entire subsidiaries are

being regarded is known as

consolidation accounting. The financial

statement of the parent company is

being regarded in this (Qiu, Shaukat,

and Tharyan, 2016).

The investment is being treated as an

asset within this accounting process

within the associate company. When

about 20% to 50% of the share of a

company is held, then this is performed

(Qian, Gao, and Tsang, 2015).

Within the subsidiary company occurs

the emerging of the financial items of

the company.

The associates never merge the entire

financial items. The investment of the

company is only utilized which is being

presented within the company’s balance

sheet.

A 50% share is being held by the

subsidiary company along with the

parent company which is performed

under the subsidiary company (Pratt,

2016).

While a share of more than 20% is held

by the subsidiary company under the

associate.

The acquisition method has held a

complete consolidation

The full acquisition is not being allowed

under this method as this is under

equity method while the investment

segment of the parent company is

involved along with the associate

company (Maas, Schaltegger and

Crutzen, 2016).

CORPORATE AND FINANCIAL ACCOUNTING

Consolidation accounting Equity accounting

The process through which the financial

outcomes of the entire subsidiaries are

being regarded is known as

consolidation accounting. The financial

statement of the parent company is

being regarded in this (Qiu, Shaukat,

and Tharyan, 2016).

The investment is being treated as an

asset within this accounting process

within the associate company. When

about 20% to 50% of the share of a

company is held, then this is performed

(Qian, Gao, and Tsang, 2015).

Within the subsidiary company occurs

the emerging of the financial items of

the company.

The associates never merge the entire

financial items. The investment of the

company is only utilized which is being

presented within the company’s balance

sheet.

A 50% share is being held by the

subsidiary company along with the

parent company which is performed

under the subsidiary company (Pratt,

2016).

While a share of more than 20% is held

by the subsidiary company under the

associate.

The acquisition method has held a

complete consolidation

The full acquisition is not being allowed

under this method as this is under

equity method while the investment

segment of the parent company is

involved along with the associate

company (Maas, Schaltegger and

Crutzen, 2016).

6

CORPORATE AND FINANCIAL ACCOUNTING

The company JTY limited should use the consolidation method as the best

method of accounting. This is the method which includes the acquisition or purchase

method. The company is being assisted with it for focusing on the numerous aspects

of financial reporting. The financial statement of the subsidiary is being consolidated

by this. Possible chances are there for increasing the company’s goodwill with profit.

This assists in gaining people’s trust. The company is being assisted with the true

and fair reporting in the long run. The benefits of the acquisition method are taken by

the firm which is the best practice which assists in the proper financial reporting

(Lins, Servaes and Tamayo, 2017). This has happened due to the attachment of the

parent company with the subsidiary company considering the financial statements.

Thus, the company can repose the entire financial transactions. The best practice of

the firms is under this. The benefits of the acquisition and the post-acquisition

process are regarded by the JTY limited the company is being assisted for creating

the best from the selected practice (Kothari, 2019). Thus, there is a successful

purchase acquisition method for business.

The entire disclosure of the financial statement regarding the parent company

is processed under the consolidating accounting along with the subsidiary company.

Consolidated balance sheet

Particulars July ltd FAB ltd

Assets 307000 147000

Liabilities -262000 -125000

Total equities and -307000 -147000

CORPORATE AND FINANCIAL ACCOUNTING

The company JTY limited should use the consolidation method as the best

method of accounting. This is the method which includes the acquisition or purchase

method. The company is being assisted with it for focusing on the numerous aspects

of financial reporting. The financial statement of the subsidiary is being consolidated

by this. Possible chances are there for increasing the company’s goodwill with profit.

This assists in gaining people’s trust. The company is being assisted with the true

and fair reporting in the long run. The benefits of the acquisition method are taken by

the firm which is the best practice which assists in the proper financial reporting

(Lins, Servaes and Tamayo, 2017). This has happened due to the attachment of the

parent company with the subsidiary company considering the financial statements.

Thus, the company can repose the entire financial transactions. The best practice of

the firms is under this. The benefits of the acquisition and the post-acquisition

process are regarded by the JTY limited the company is being assisted for creating

the best from the selected practice (Kothari, 2019). Thus, there is a successful

purchase acquisition method for business.

The entire disclosure of the financial statement regarding the parent company

is processed under the consolidating accounting along with the subsidiary company.

Consolidated balance sheet

Particulars July ltd FAB ltd

Assets 307000 147000

Liabilities -262000 -125000

Total equities and -307000 -147000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

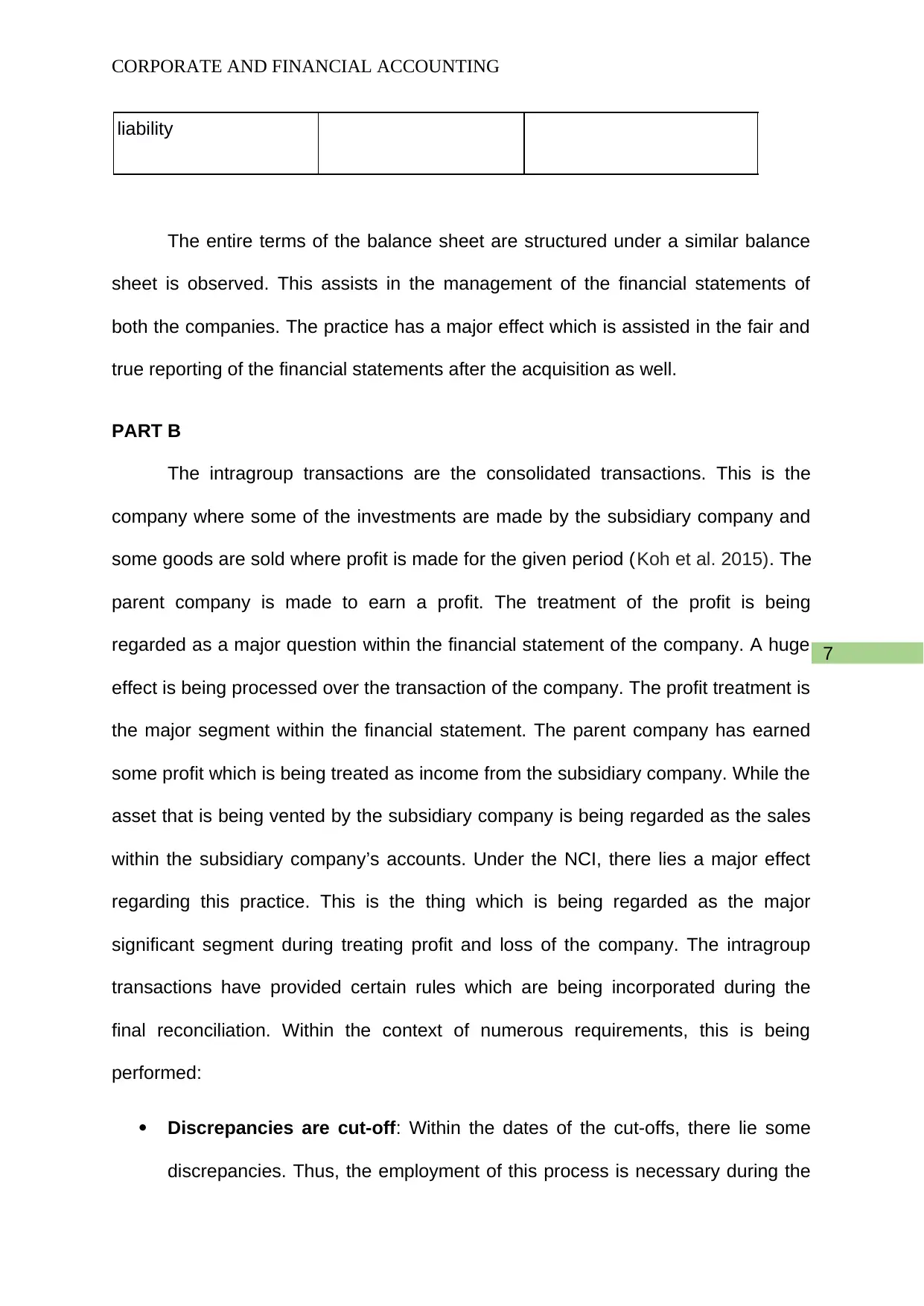

CORPORATE AND FINANCIAL ACCOUNTING

liability

The entire terms of the balance sheet are structured under a similar balance

sheet is observed. This assists in the management of the financial statements of

both the companies. The practice has a major effect which is assisted in the fair and

true reporting of the financial statements after the acquisition as well.

PART B

The intragroup transactions are the consolidated transactions. This is the

company where some of the investments are made by the subsidiary company and

some goods are sold where profit is made for the given period (Koh et al. 2015). The

parent company is made to earn a profit. The treatment of the profit is being

regarded as a major question within the financial statement of the company. A huge

effect is being processed over the transaction of the company. The profit treatment is

the major segment within the financial statement. The parent company has earned

some profit which is being treated as income from the subsidiary company. While the

asset that is being vented by the subsidiary company is being regarded as the sales

within the subsidiary company’s accounts. Under the NCI, there lies a major effect

regarding this practice. This is the thing which is being regarded as the major

significant segment during treating profit and loss of the company. The intragroup

transactions have provided certain rules which are being incorporated during the

final reconciliation. Within the context of numerous requirements, this is being

performed:

Discrepancies are cut-off: Within the dates of the cut-offs, there lie some

discrepancies. Thus, the employment of this process is necessary during the

CORPORATE AND FINANCIAL ACCOUNTING

liability

The entire terms of the balance sheet are structured under a similar balance

sheet is observed. This assists in the management of the financial statements of

both the companies. The practice has a major effect which is assisted in the fair and

true reporting of the financial statements after the acquisition as well.

PART B

The intragroup transactions are the consolidated transactions. This is the

company where some of the investments are made by the subsidiary company and

some goods are sold where profit is made for the given period (Koh et al. 2015). The

parent company is made to earn a profit. The treatment of the profit is being

regarded as a major question within the financial statement of the company. A huge

effect is being processed over the transaction of the company. The profit treatment is

the major segment within the financial statement. The parent company has earned

some profit which is being treated as income from the subsidiary company. While the

asset that is being vented by the subsidiary company is being regarded as the sales

within the subsidiary company’s accounts. Under the NCI, there lies a major effect

regarding this practice. This is the thing which is being regarded as the major

significant segment during treating profit and loss of the company. The intragroup

transactions have provided certain rules which are being incorporated during the

final reconciliation. Within the context of numerous requirements, this is being

performed:

Discrepancies are cut-off: Within the dates of the cut-offs, there lie some

discrepancies. Thus, the employment of this process is necessary during the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE AND FINANCIAL ACCOUNTING

reconciliation process. The companies are being assisted during the

mitigation of the discrepancies within the procedures of accounting regarding

the commonalities (Khan, Serafeim and Yoon, 2016).

The close dates are modified: The close dates have some modifications

within the subsidiary company and the parent company. Thus, the activation

of the reconciliation process is essential. The numerous aspects of the

modifications are being focused by the company considering the accounting

method of both the companies. The big accounting discrepancies are made

responsible regarding the close dates. Like, when the parent company is

closing the account book commendably on each year 31st December. Then

the accounts book of the subsidiary company is closed over the half-yearly

basis. The numerous aspects are being focused through the firefights where

the disclosure date is considered.

Foreign companies’ dominance: The foreign recurrence is responsible for

dominating the transactions that are being processed by the companies within

each other. Thus, the several aspects of the foreign market are being focused

which is significant for the companies. These are both companies which are

being run within similar industries. Thus, it is not being regarded as a major

issue during making some identification of accounting guidelines and

principles that are being demanded the companies (Honggowati et al. 2017).

These are the practice which bears a constant effect and thus, is being

proceeded towards the long run. Thus, to assist the company during the

process of management has become important with the formulation of proper

regulations and rules.

Other reasons for assessment

CORPORATE AND FINANCIAL ACCOUNTING

reconciliation process. The companies are being assisted during the

mitigation of the discrepancies within the procedures of accounting regarding

the commonalities (Khan, Serafeim and Yoon, 2016).

The close dates are modified: The close dates have some modifications

within the subsidiary company and the parent company. Thus, the activation

of the reconciliation process is essential. The numerous aspects of the

modifications are being focused by the company considering the accounting

method of both the companies. The big accounting discrepancies are made

responsible regarding the close dates. Like, when the parent company is

closing the account book commendably on each year 31st December. Then

the accounts book of the subsidiary company is closed over the half-yearly

basis. The numerous aspects are being focused through the firefights where

the disclosure date is considered.

Foreign companies’ dominance: The foreign recurrence is responsible for

dominating the transactions that are being processed by the companies within

each other. Thus, the several aspects of the foreign market are being focused

which is significant for the companies. These are both companies which are

being run within similar industries. Thus, it is not being regarded as a major

issue during making some identification of accounting guidelines and

principles that are being demanded the companies (Honggowati et al. 2017).

These are the practice which bears a constant effect and thus, is being

proceeded towards the long run. Thus, to assist the company during the

process of management has become important with the formulation of proper

regulations and rules.

Other reasons for assessment

9

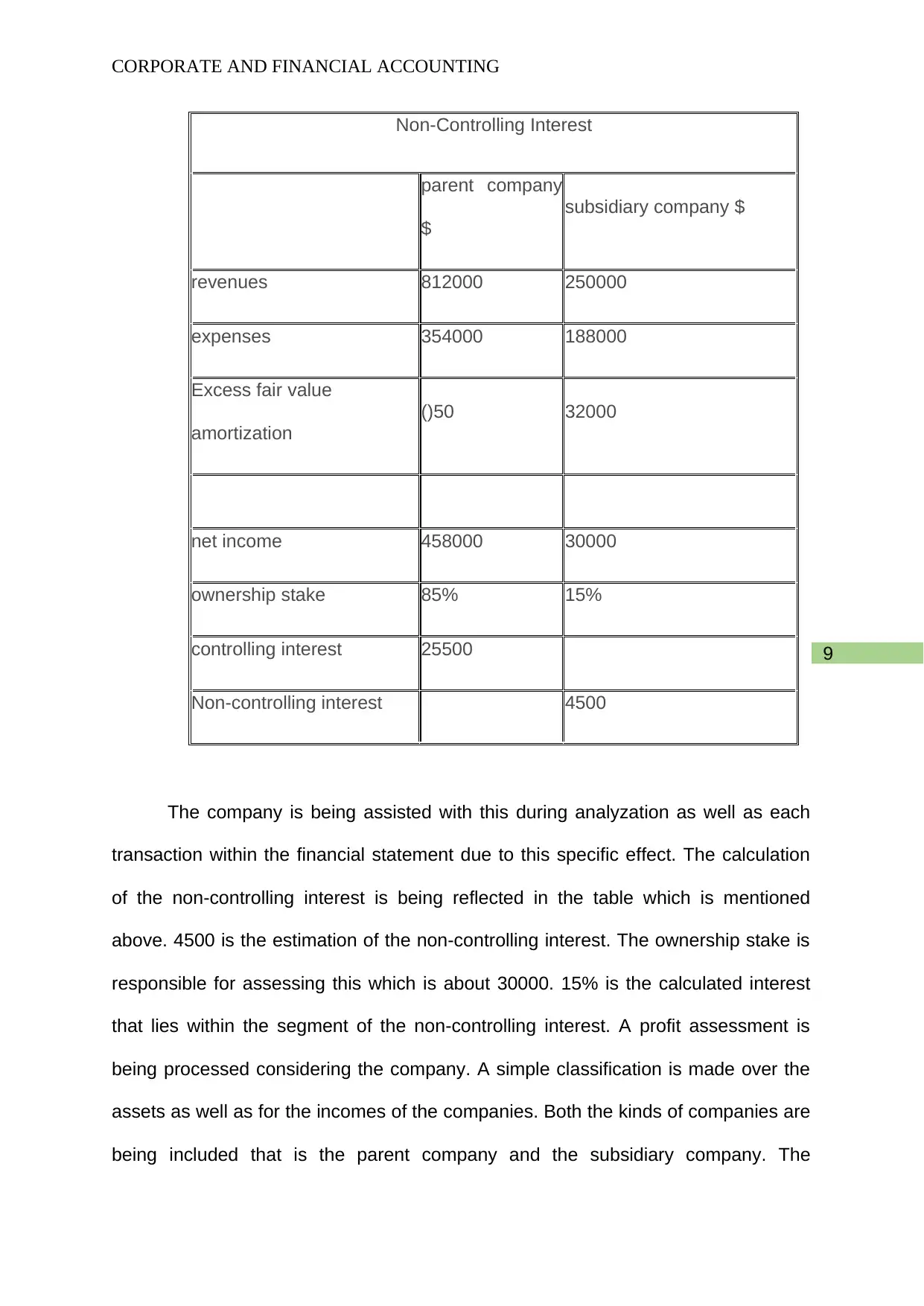

CORPORATE AND FINANCIAL ACCOUNTING

Non-Controlling Interest

parent company

$

subsidiary company $

revenues 812000 250000

expenses 354000 188000

Excess fair value

amortization

()50 32000

net income 458000 30000

ownership stake 85% 15%

controlling interest 25500

Non-controlling interest 4500

The company is being assisted with this during analyzation as well as each

transaction within the financial statement due to this specific effect. The calculation

of the non-controlling interest is being reflected in the table which is mentioned

above. 4500 is the estimation of the non-controlling interest. The ownership stake is

responsible for assessing this which is about 30000. 15% is the calculated interest

that lies within the segment of the non-controlling interest. A profit assessment is

being processed considering the company. A simple classification is made over the

assets as well as for the incomes of the companies. Both the kinds of companies are

being included that is the parent company and the subsidiary company. The

CORPORATE AND FINANCIAL ACCOUNTING

Non-Controlling Interest

parent company

$

subsidiary company $

revenues 812000 250000

expenses 354000 188000

Excess fair value

amortization

()50 32000

net income 458000 30000

ownership stake 85% 15%

controlling interest 25500

Non-controlling interest 4500

The company is being assisted with this during analyzation as well as each

transaction within the financial statement due to this specific effect. The calculation

of the non-controlling interest is being reflected in the table which is mentioned

above. 4500 is the estimation of the non-controlling interest. The ownership stake is

responsible for assessing this which is about 30000. 15% is the calculated interest

that lies within the segment of the non-controlling interest. A profit assessment is

being processed considering the company. A simple classification is made over the

assets as well as for the incomes of the companies. Both the kinds of companies are

being included that is the parent company and the subsidiary company. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE AND FINANCIAL ACCOUNTING

translation has some special effect on the company’s financial statements. The

accurate intercede is being measured that is to be uncontrolled (Duff, 2016).

PART C

Response

The financial statement of the company has provided some information which

is being confined with the proper allocation of the company’s resources. This is

observed that the retained earnings of the company are invested within the

appropriate business plans. Investments are included within these plans that are

resource free. The company has less dependency on the debt fund. Decisions are

being processed by the investors based over the company’s past, the present and

the future events that are being disclosed within the financial statements. The

reflection of the fair and true images over the financial statement which is being

regarded as a basic need. The introduction of the company’s fair value assets is also

being regarded within it within the balance sheet of the company. There are the

resources which are being allocated over the subsidiaries that are available, where

the company is being considered. This is the matter that is being disclosed within the

report of the independent auditor as per his statement (Crowther, 2018). Statutory

compliance has regarded the entire information about the company.

Proper decisions are being taken by the investors that are being based on the

reliability and the relevance of the financial statement. In this context lies the positive

attitude of the investors. The securities or the investors have regarded this, as the

significant decision that is constructed by the company is based over the disclosure.

The security market is being assisted with the information, for instance, the taxation

risk that is being discussed in the financial report of the company for taking suitable

decisions over the terms of investment. A reduction is being noticed in the profit after

CORPORATE AND FINANCIAL ACCOUNTING

translation has some special effect on the company’s financial statements. The

accurate intercede is being measured that is to be uncontrolled (Duff, 2016).

PART C

Response

The financial statement of the company has provided some information which

is being confined with the proper allocation of the company’s resources. This is

observed that the retained earnings of the company are invested within the

appropriate business plans. Investments are included within these plans that are

resource free. The company has less dependency on the debt fund. Decisions are

being processed by the investors based over the company’s past, the present and

the future events that are being disclosed within the financial statements. The

reflection of the fair and true images over the financial statement which is being

regarded as a basic need. The introduction of the company’s fair value assets is also

being regarded within it within the balance sheet of the company. There are the

resources which are being allocated over the subsidiaries that are available, where

the company is being considered. This is the matter that is being disclosed within the

report of the independent auditor as per his statement (Crowther, 2018). Statutory

compliance has regarded the entire information about the company.

Proper decisions are being taken by the investors that are being based on the

reliability and the relevance of the financial statement. In this context lies the positive

attitude of the investors. The securities or the investors have regarded this, as the

significant decision that is constructed by the company is based over the disclosure.

The security market is being assisted with the information, for instance, the taxation

risk that is being discussed in the financial report of the company for taking suitable

decisions over the terms of investment. A reduction is being noticed in the profit after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE AND FINANCIAL ACCOUNTING

the tax as the company is being permitted for paying more tax. A drop in the net

income of the company is also noticed. Thus, investors have also reacted. This has

specified about the termination of the investments within the company until a profit is

made within a company (Caskey and Laux, 2016). In this segment there lies a

chance where the company can lose the market grip. Thus, the users are required to

analyze the financial statements. The accounting standard AASB 10 has suggested

this. The AASB has made this compulsory where IFRS is being issued by this across

the world. The business should adopt the accounting standard for presenting the

financial statement in a suitable way. AASB is being utilized within this accounting

purpose regarding the implementing of the guidelines considering the presentation,

the structure and the financial statement content that the company has prepared.

Some reasons are there which has made discloses important which are:

The true value of the assets is viewed.

The dividend payment is assisted as when the value of an asset is increased,

then the company attracts more investors. Chances are lying for getting more

of the dividends from the company.

The true return rate is shown regarding the employment of capital.

Fair and true value is there within the financial assets of the company.

The company is being assisted with it during taking loans from banks which

specifies about the increased value of the assets for keeping suitable

mortgage along with the ban. Chances are lying where companies can

receive the desired return rate.

After the revaluation of the assets, the true amount of the assets can be

attained.

CORPORATE AND FINANCIAL ACCOUNTING

the tax as the company is being permitted for paying more tax. A drop in the net

income of the company is also noticed. Thus, investors have also reacted. This has

specified about the termination of the investments within the company until a profit is

made within a company (Caskey and Laux, 2016). In this segment there lies a

chance where the company can lose the market grip. Thus, the users are required to

analyze the financial statements. The accounting standard AASB 10 has suggested

this. The AASB has made this compulsory where IFRS is being issued by this across

the world. The business should adopt the accounting standard for presenting the

financial statement in a suitable way. AASB is being utilized within this accounting

purpose regarding the implementing of the guidelines considering the presentation,

the structure and the financial statement content that the company has prepared.

Some reasons are there which has made discloses important which are:

The true value of the assets is viewed.

The dividend payment is assisted as when the value of an asset is increased,

then the company attracts more investors. Chances are lying for getting more

of the dividends from the company.

The true return rate is shown regarding the employment of capital.

Fair and true value is there within the financial assets of the company.

The company is being assisted with it during taking loans from banks which

specifies about the increased value of the assets for keeping suitable

mortgage along with the ban. Chances are lying where companies can

receive the desired return rate.

After the revaluation of the assets, the true amount of the assets can be

attained.

12

CORPORATE AND FINANCIAL ACCOUNTING

The true, as well as the fair image of the asset, is visible after the revaluation

of the asset. The accounting system requires some SAC2 statement regarding the

accounting concept for general purpose. This is being utilized for dealing with the

objectives of the general purpose of financial reporting. This is a significant

disclosure as decision are being taken by the company’s stakeholders and investors

regarding that disclosure. The directors of the company have also used it for the

construction of proper business plans and policies. The company’s resources are

also properly allocated due to this. Certain qualitative characteristics are also

present, where the business could rely on. All these are being regarded as the base

of the financial statement.

The profits are required to be added within the financial statement which is

comprehensive. Within every fund of the owners, the profits are being added by the

company as a major percentage of the subsidiary company is held by this. While the

NCI is not shown when a percentage of less than 50% is being owned by the

shareholder. Ownership right is also not present there, thus, not voting rights are

also there in the aspects of the shareholders. The NCI is not seen to be reporting as

an owner equity fund, when, less than 50% of shares are held by the company. A

consolidated account is there for the companies where the NCI reports about the

financial statements which are essential for the company to stay focused over the

financial statements (Balakrishnan, Watts, and Zuo, 2016).

The reliability of the financial statement is important. The rendering of the

information considering the financial statement is being referred by the quality of the

financial statements that are impacted by any biases or errors. This becomes

possible when faithful information is served regarding the financial statement. The

reader relies on the information (Armstrong et al. 2015). The stakeholders read the

CORPORATE AND FINANCIAL ACCOUNTING

The true, as well as the fair image of the asset, is visible after the revaluation

of the asset. The accounting system requires some SAC2 statement regarding the

accounting concept for general purpose. This is being utilized for dealing with the

objectives of the general purpose of financial reporting. This is a significant

disclosure as decision are being taken by the company’s stakeholders and investors

regarding that disclosure. The directors of the company have also used it for the

construction of proper business plans and policies. The company’s resources are

also properly allocated due to this. Certain qualitative characteristics are also

present, where the business could rely on. All these are being regarded as the base

of the financial statement.

The profits are required to be added within the financial statement which is

comprehensive. Within every fund of the owners, the profits are being added by the

company as a major percentage of the subsidiary company is held by this. While the

NCI is not shown when a percentage of less than 50% is being owned by the

shareholder. Ownership right is also not present there, thus, not voting rights are

also there in the aspects of the shareholders. The NCI is not seen to be reporting as

an owner equity fund, when, less than 50% of shares are held by the company. A

consolidated account is there for the companies where the NCI reports about the

financial statements which are essential for the company to stay focused over the

financial statements (Balakrishnan, Watts, and Zuo, 2016).

The reliability of the financial statement is important. The rendering of the

information considering the financial statement is being referred by the quality of the

financial statements that are impacted by any biases or errors. This becomes

possible when faithful information is served regarding the financial statement. The

reader relies on the information (Armstrong et al. 2015). The stakeholders read the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.