Detailed Solution: Consolidation of Financial Statements Homework

VerifiedAdded on 2019/09/24

|8

|873

|144

Homework Assignment

AI Summary

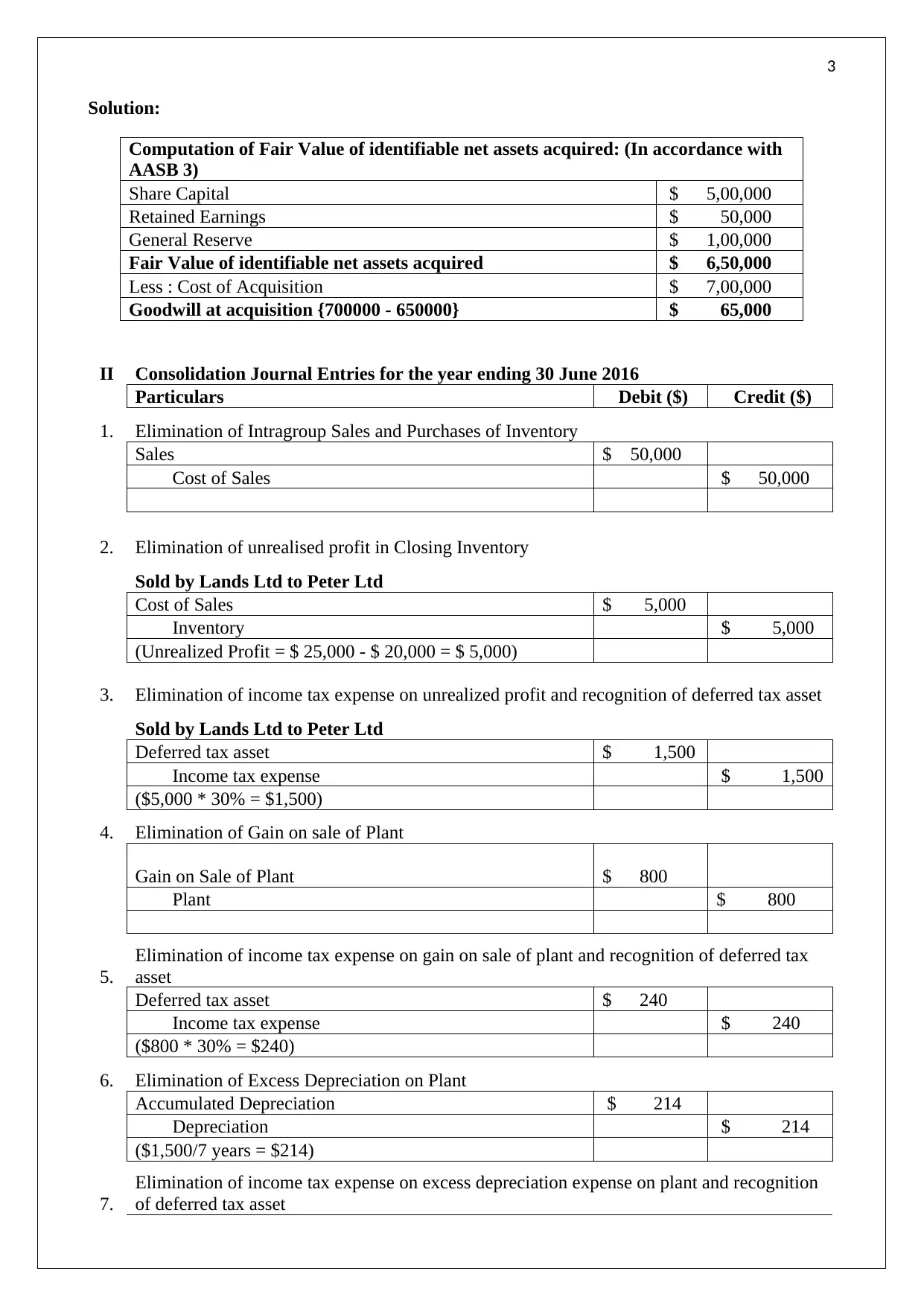

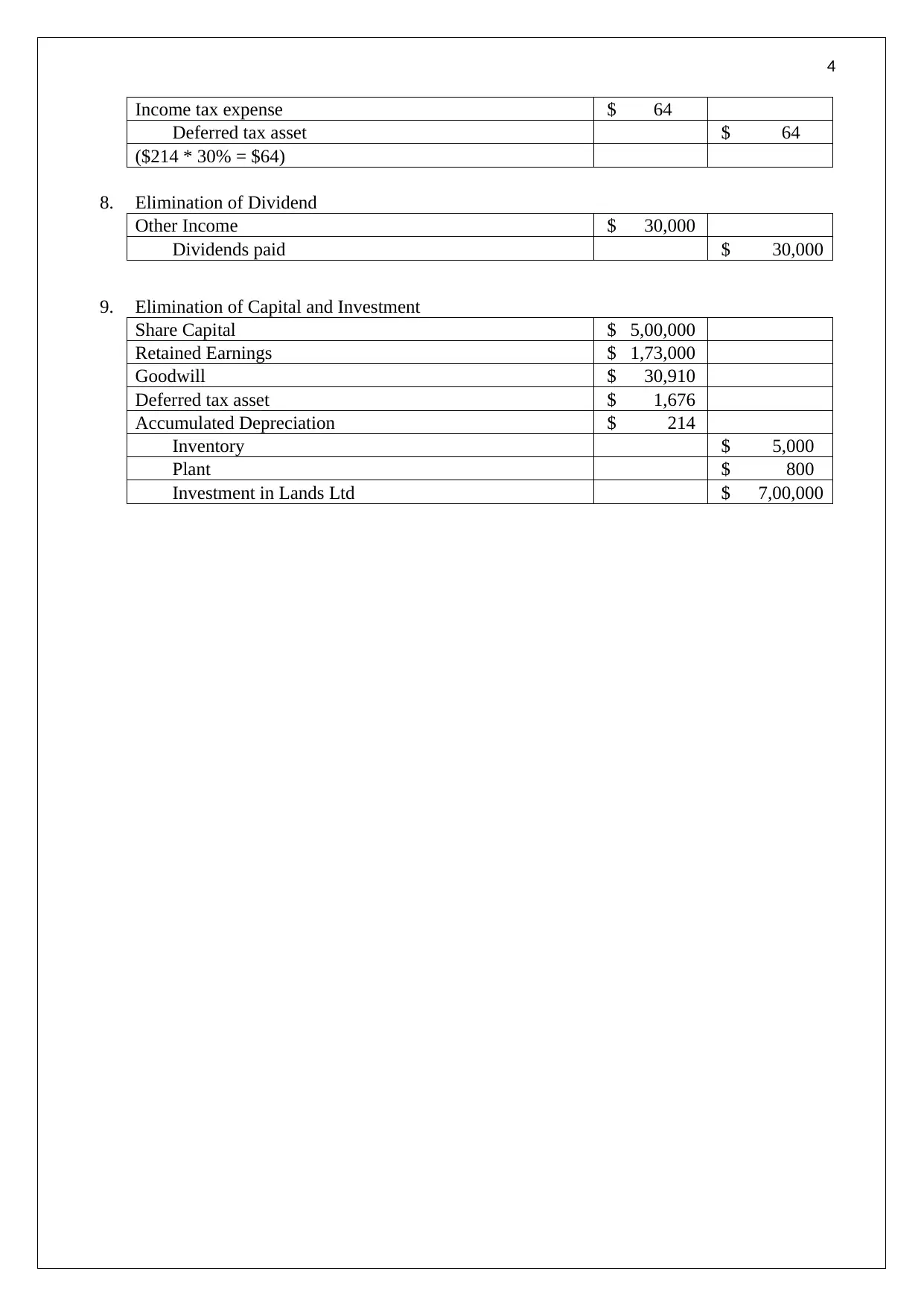

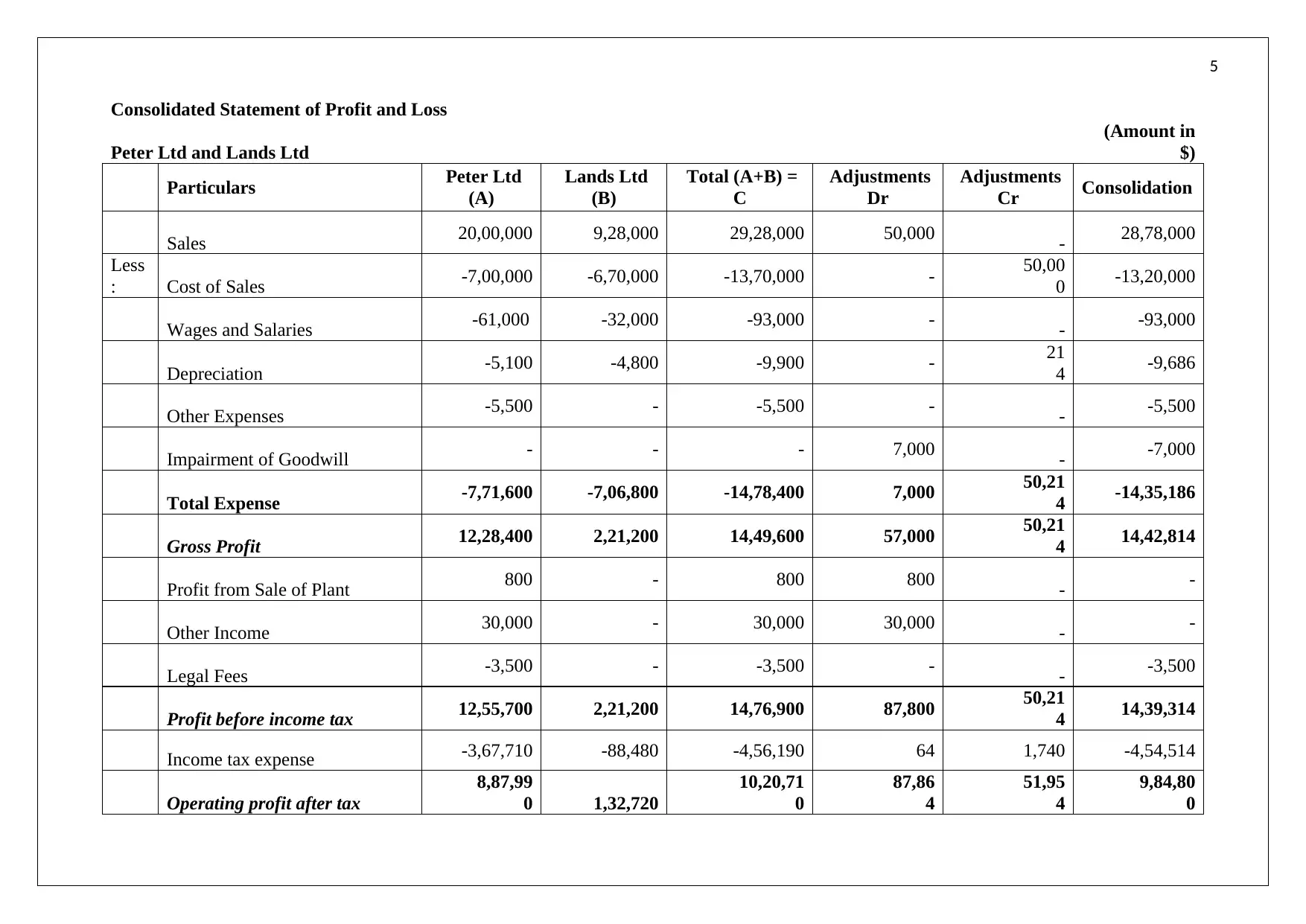

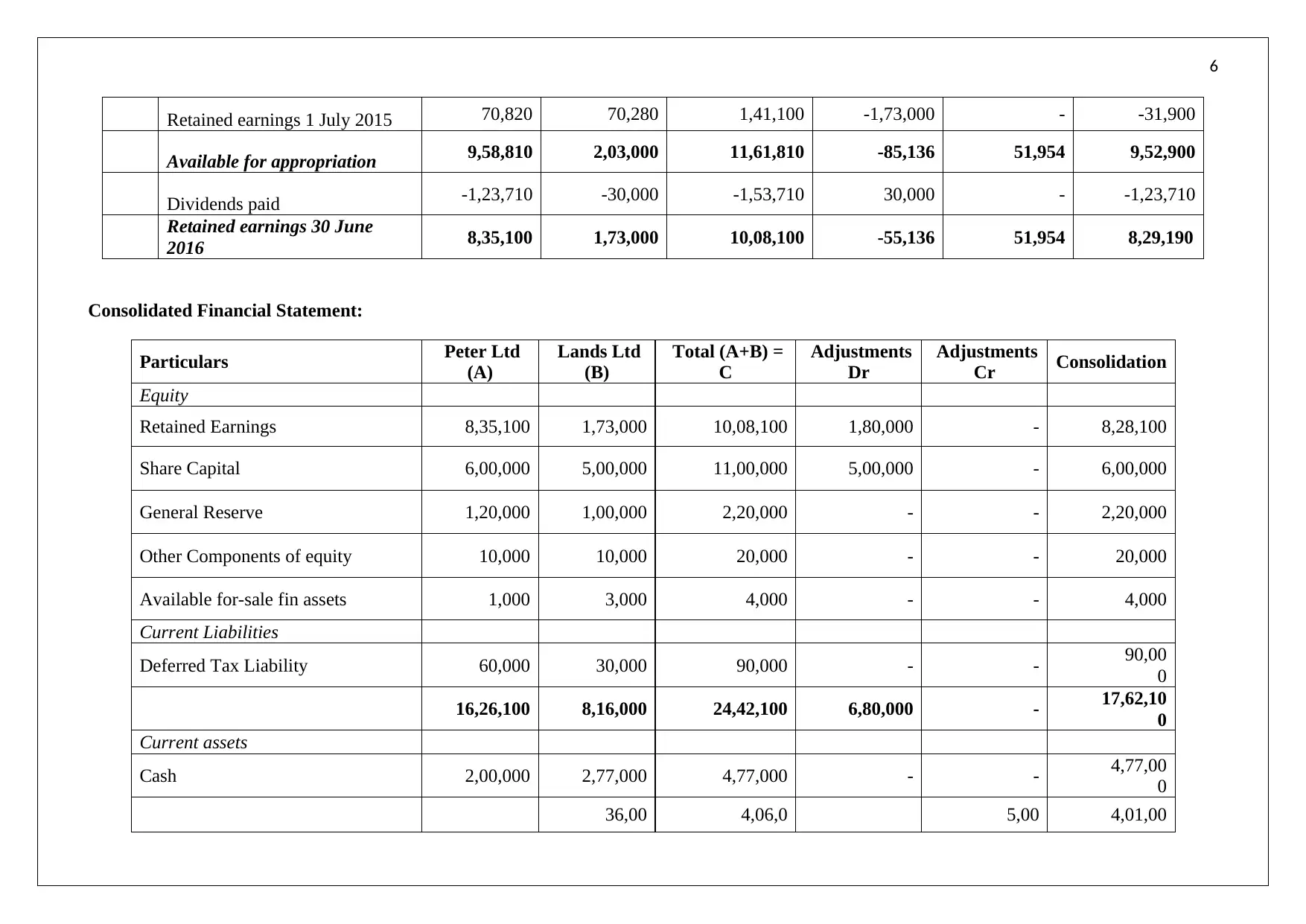

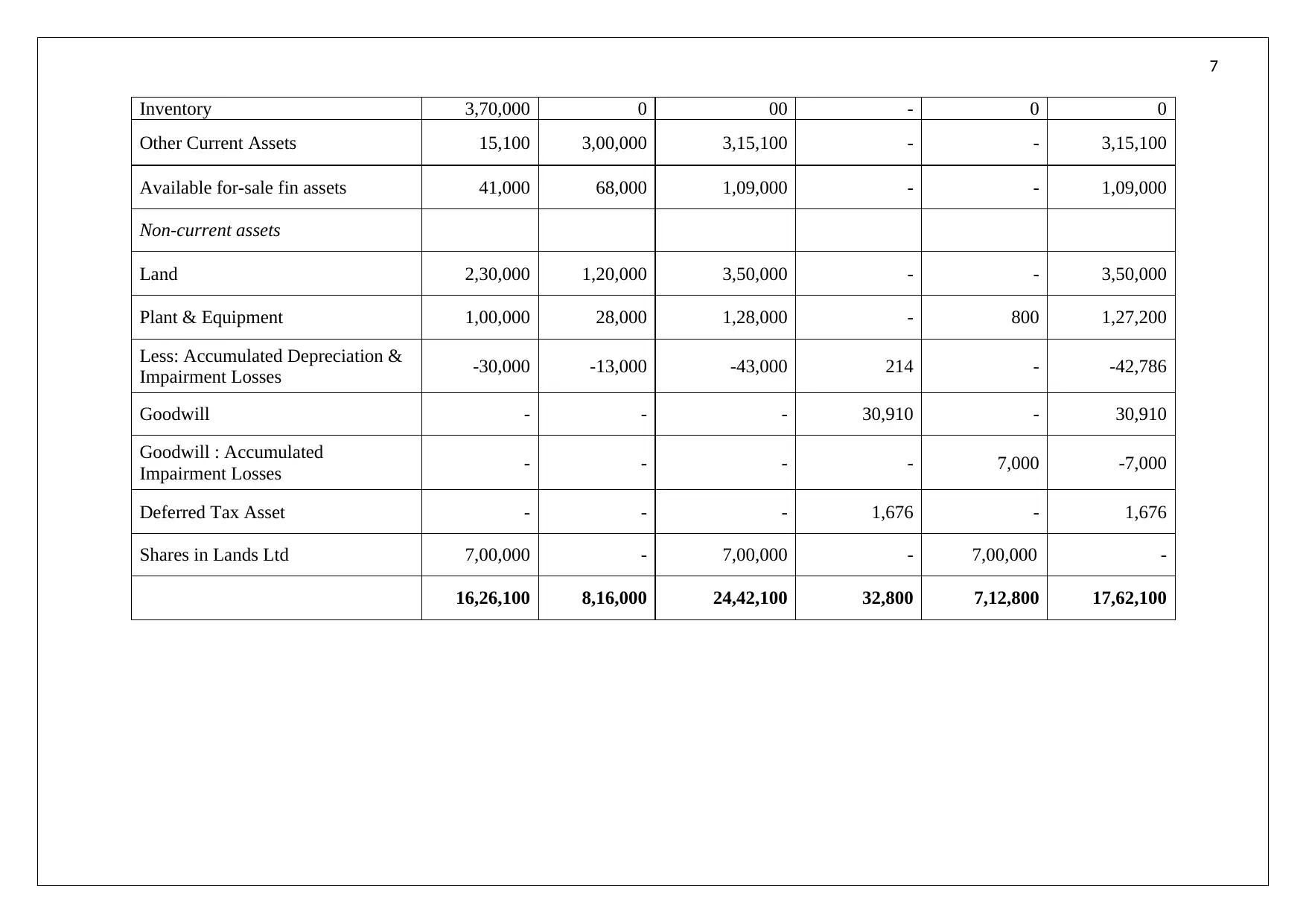

This document presents a comprehensive solution to a financial statement consolidation assignment. It begins with the computation of the fair value of identifiable net assets acquired, adhering to AASB 3 standards, and calculates goodwill. The core of the solution lies in the detailed consolidation journal entries, meticulously addressing the elimination of intragroup sales and purchases, unrealized profits in closing inventory, and income tax expenses. It covers the elimination of gains on the sale of plant, excess depreciation, and dividends. The solution includes a consolidated statement of profit and loss, followed by a consolidated financial statement, providing a clear overview of the combined financial position of the entities. The document also provides references for further study.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.