Financial Accounting: Consolidation Worksheet Solutions and Analysis

VerifiedAdded on 2020/05/03

|6

|846

|212

Homework Assignment

AI Summary

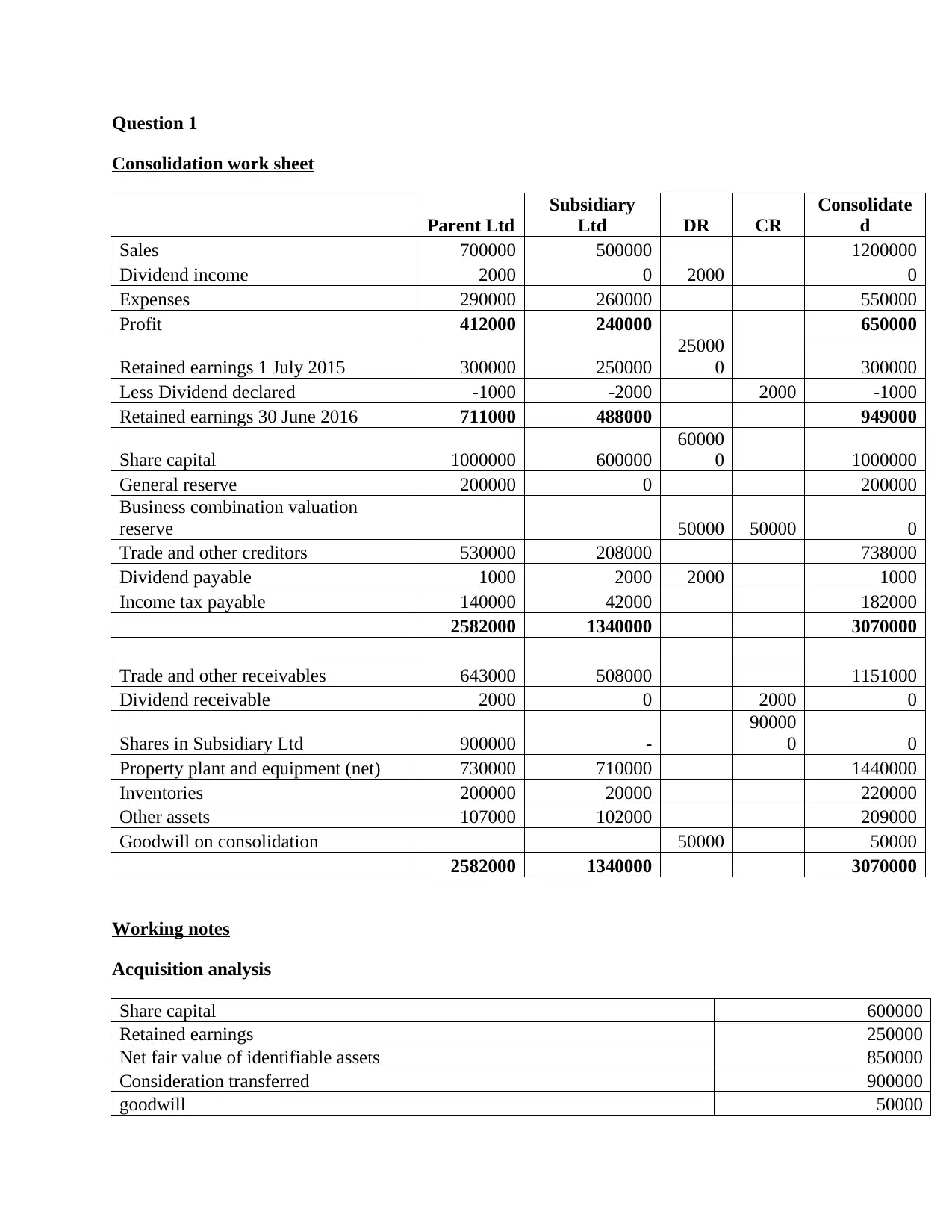

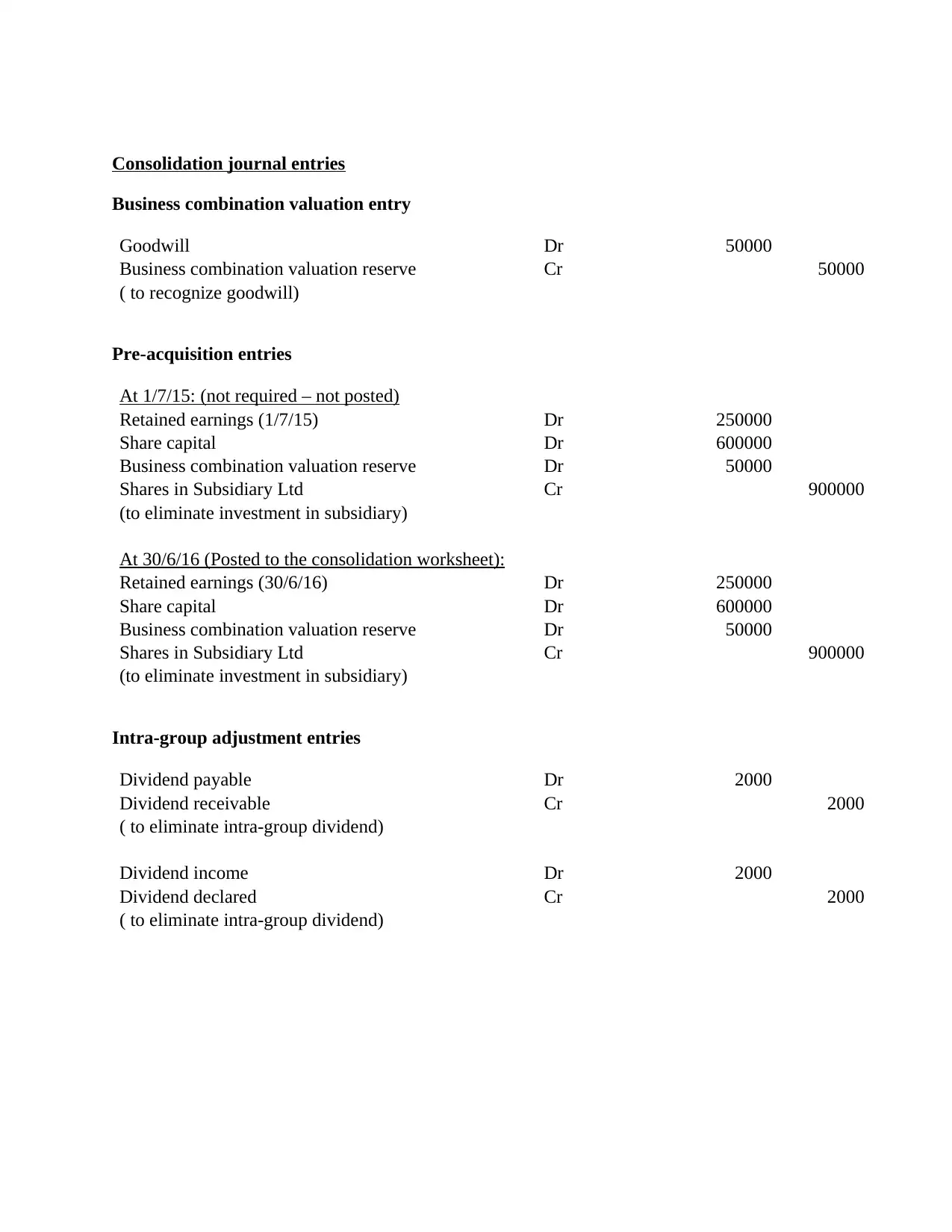

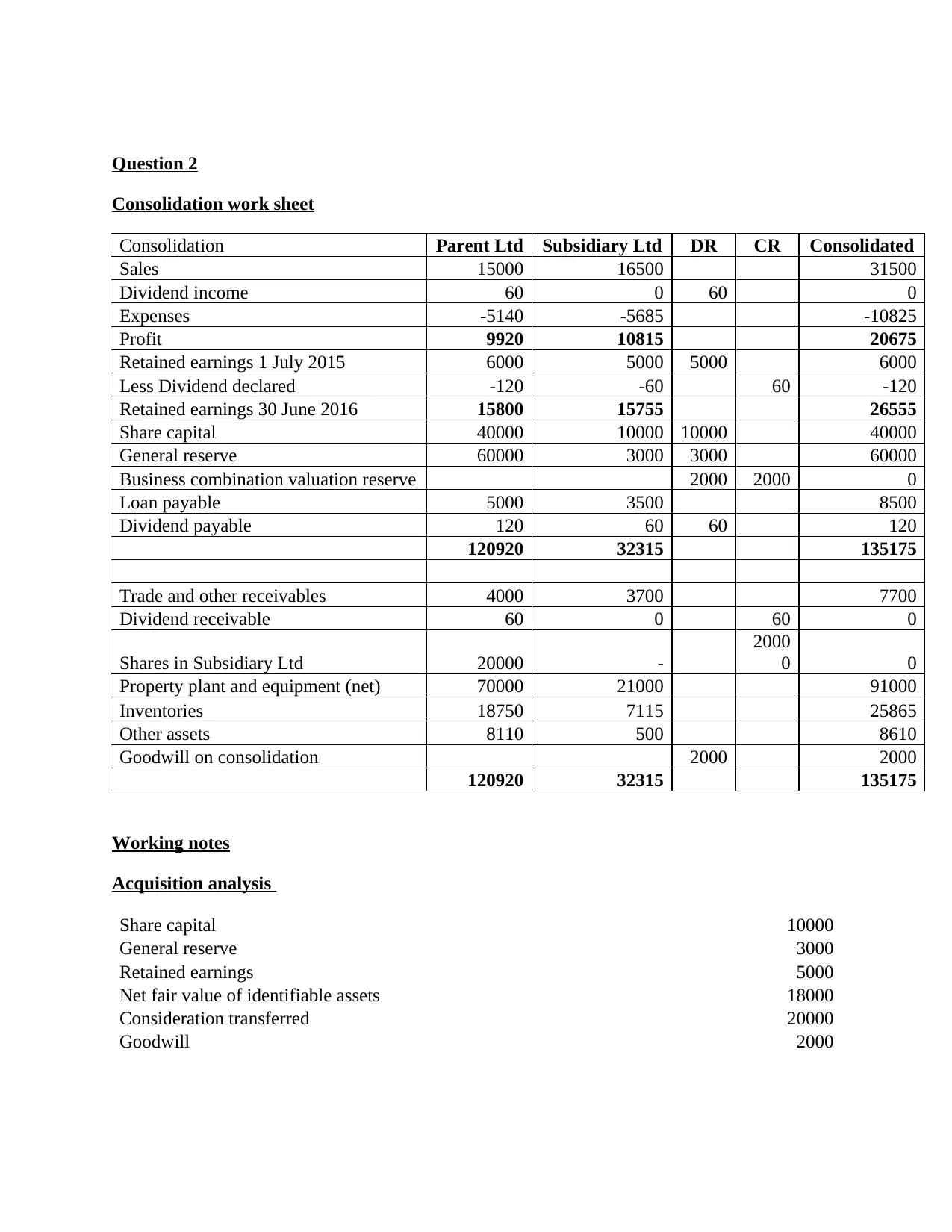

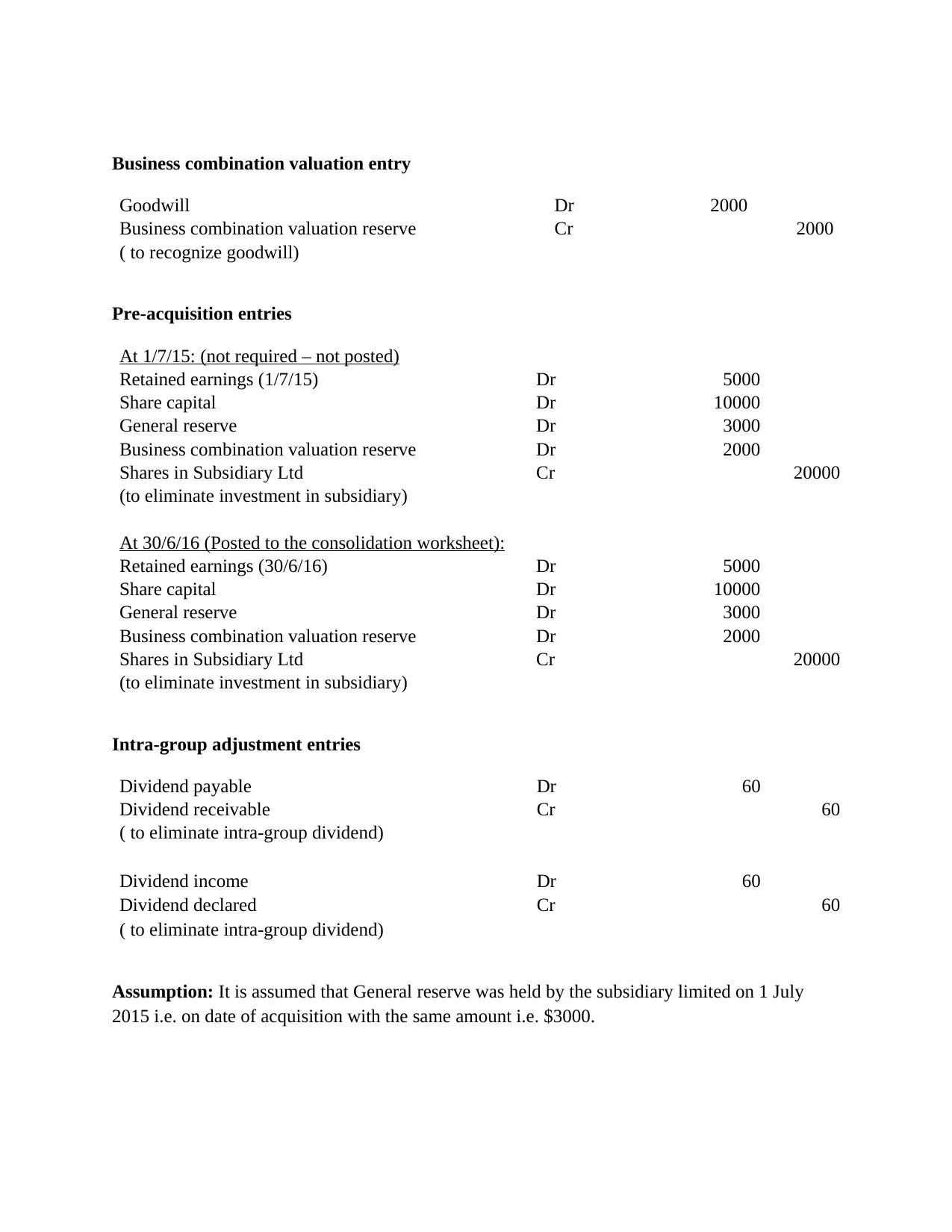

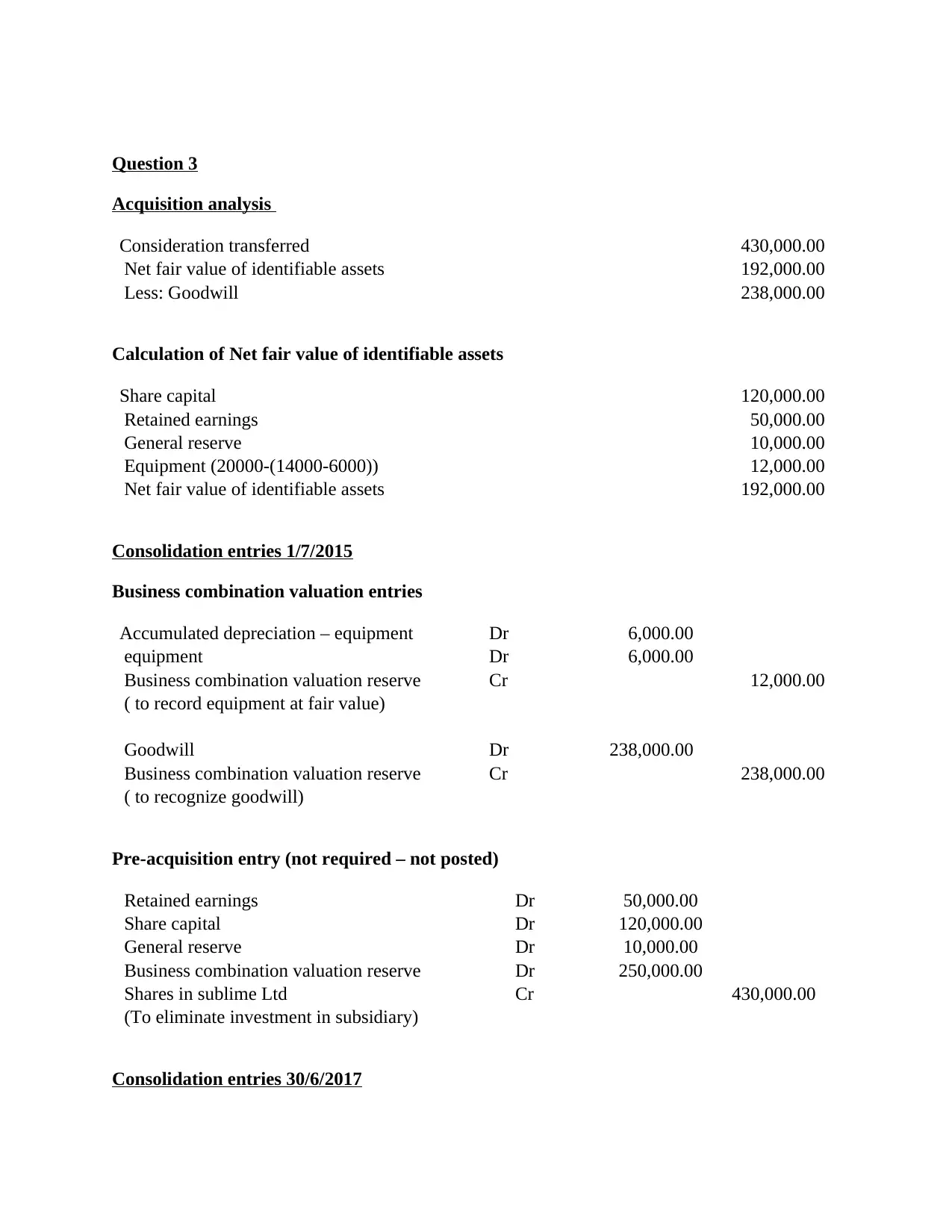

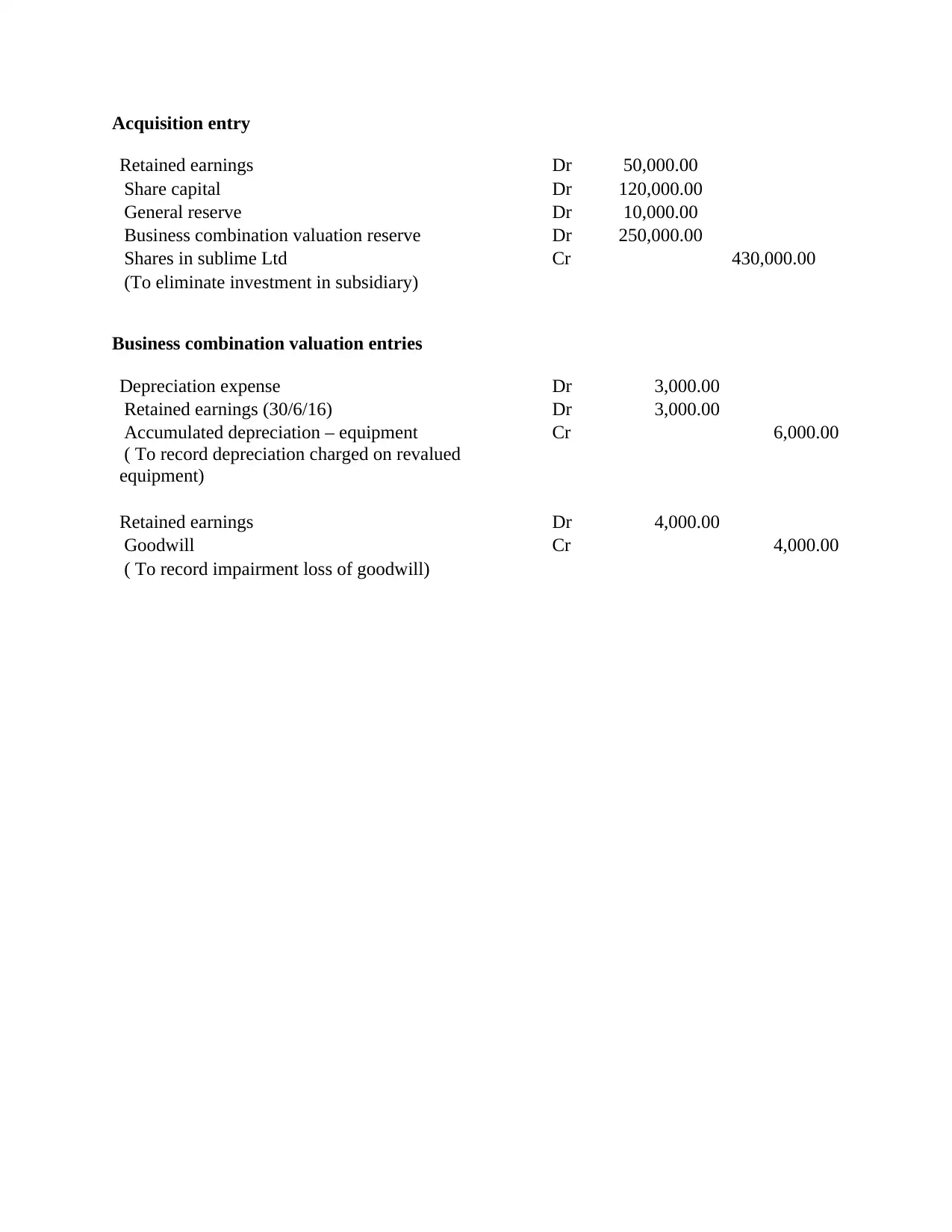

This document presents comprehensive solutions to consolidation worksheet problems in financial accounting. It includes detailed consolidation worksheets for multiple scenarios involving parent and subsidiary companies, incorporating journal entries to account for business combinations, including goodwill calculations and the recognition of fair value adjustments. The assignment covers pre-acquisition entries, intra-group adjustments, and the preparation of consolidated financial statements. Additionally, it provides acquisition analyses, outlining the consideration transferred, net fair value of identifiable assets, and the resulting goodwill. The solutions demonstrate the elimination of intercompany transactions, dividend adjustments, and the allocation of depreciation expenses. The assignment is designed to illustrate the process of consolidating financial statements, ensuring a clear understanding of the accounting treatment for various consolidation adjustments.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.