Evaluating Investment Appraisal Techniques in Construction Management

VerifiedAdded on 2023/06/15

|12

|2626

|327

Report

AI Summary

This report provides a comprehensive evaluation of investment appraisal techniques used in construction management, focusing on Net Present Value (NPV), Internal Rate of Return (IRR), Accounting Rate of Return (ARR), and payback period methods. The analysis includes a critical review of these techniques and their application to a major civil construction project in the UK. Furthermore, the report evaluates two heating systems, System A and System B, using the aforementioned techniques, calculating their respective NPV, IRR, and ARR to provide a recommendation based on the financial outcomes. The evaluation considers factors such as discounted cash flows, initial investment, and the expected lifespan of each system, ultimately advising on the most profitable and sustainable option for the client.

CONSTRUCTION

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

Construction management is related with offering the professional service by using

techniques for planning, designing and building of project. The current report has given

emphasis on evaluating the investment appraisal techniques for obtain depth understanding

regarding highlighted techniques. It has paid attention on using techniques such as NPV, IRR,

ARR and payback period methods for calculating outcomes of system A and B so that proper

selection can be done.

Construction management is related with offering the professional service by using

techniques for planning, designing and building of project. The current report has given

emphasis on evaluating the investment appraisal techniques for obtain depth understanding

regarding highlighted techniques. It has paid attention on using techniques such as NPV, IRR,

ARR and payback period methods for calculating outcomes of system A and B so that proper

selection can be done.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK A...........................................................................................................................................1

Evaluating the investment appraisal technique............................................................................1

TASK B...........................................................................................................................................2

Evaluating two systems via calculating.......................................................................................2

Recommendations........................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK A...........................................................................................................................................1

Evaluating the investment appraisal technique............................................................................1

TASK B...........................................................................................................................................2

Evaluating two systems via calculating.......................................................................................2

Recommendations........................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Construction management is concerned with planning, organizing and managing the

projects in order to get profitability & sustainability. In the current era, competition &

complexity has inclined which require firm to pay attention om developing significant

evaluation of options that can allow to have relevant outcomes. The present study will focus on

evaluating capital appraisal techniques and appropriate investment project to have higher

outcome.

TASK A

Evaluating the investment appraisal technique

Civil construction project is related with the art of building bridges, building, canals, etc.

Investment appraisal is one of the significant technique that allows the users to get the

information regarding profitability, period of recovering investment, etc. The civil construction

project that has bene undertaken in UK involves cross rail, leeds flood alleviation scheme, HS2

Northolt tunnels, the stag brewery regeneration, etc. There are basically four types of

techniques which permit to get the ability to evaluate particular project (Soka, 2020). It includes

net present value, internal & accounting rate of return and payback period. Each method of

investment appraisal technique has few benefits & drawbacks which are required to be analysed

to have proper insights. These techniques can be taken into consideration for evaluating cross

rail civil construction project which is as follows:

Net present value is one of the crucial and widely used approach that is associated with

total current value of future stream of payments (Investment appraisal techniques, 2020). If the

derived discounted value of cash flow is positive than project is favourable and vice versa.

There are number of advantages which includes accepting conventional cash flow pattern,

considered to be good measure of profitability and factors risk. It aids in having to accurate

measure profitability by estimating discounted cash flows of cross rail civil construction project

(Kengatharan and Nurullah, 2018). All types of cash in or out flow is accepted by this method to

offer result. Evaluating risk become possible with help of this particular method of capital

appraisal. On the other side, there are few lacking areas which are required to be highlighted for

evaluating significant level of knowledge to obtain fair results. It involves estimation of

opportunity cost, ignoring sunk expenditure, inability to compute required rate of return,

optimistic projections, hindering EPS, etc.

1

Construction management is concerned with planning, organizing and managing the

projects in order to get profitability & sustainability. In the current era, competition &

complexity has inclined which require firm to pay attention om developing significant

evaluation of options that can allow to have relevant outcomes. The present study will focus on

evaluating capital appraisal techniques and appropriate investment project to have higher

outcome.

TASK A

Evaluating the investment appraisal technique

Civil construction project is related with the art of building bridges, building, canals, etc.

Investment appraisal is one of the significant technique that allows the users to get the

information regarding profitability, period of recovering investment, etc. The civil construction

project that has bene undertaken in UK involves cross rail, leeds flood alleviation scheme, HS2

Northolt tunnels, the stag brewery regeneration, etc. There are basically four types of

techniques which permit to get the ability to evaluate particular project (Soka, 2020). It includes

net present value, internal & accounting rate of return and payback period. Each method of

investment appraisal technique has few benefits & drawbacks which are required to be analysed

to have proper insights. These techniques can be taken into consideration for evaluating cross

rail civil construction project which is as follows:

Net present value is one of the crucial and widely used approach that is associated with

total current value of future stream of payments (Investment appraisal techniques, 2020). If the

derived discounted value of cash flow is positive than project is favourable and vice versa.

There are number of advantages which includes accepting conventional cash flow pattern,

considered to be good measure of profitability and factors risk. It aids in having to accurate

measure profitability by estimating discounted cash flows of cross rail civil construction project

(Kengatharan and Nurullah, 2018). All types of cash in or out flow is accepted by this method to

offer result. Evaluating risk become possible with help of this particular method of capital

appraisal. On the other side, there are few lacking areas which are required to be highlighted for

evaluating significant level of knowledge to obtain fair results. It involves estimation of

opportunity cost, ignoring sunk expenditure, inability to compute required rate of return,

optimistic projections, hindering EPS, etc.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

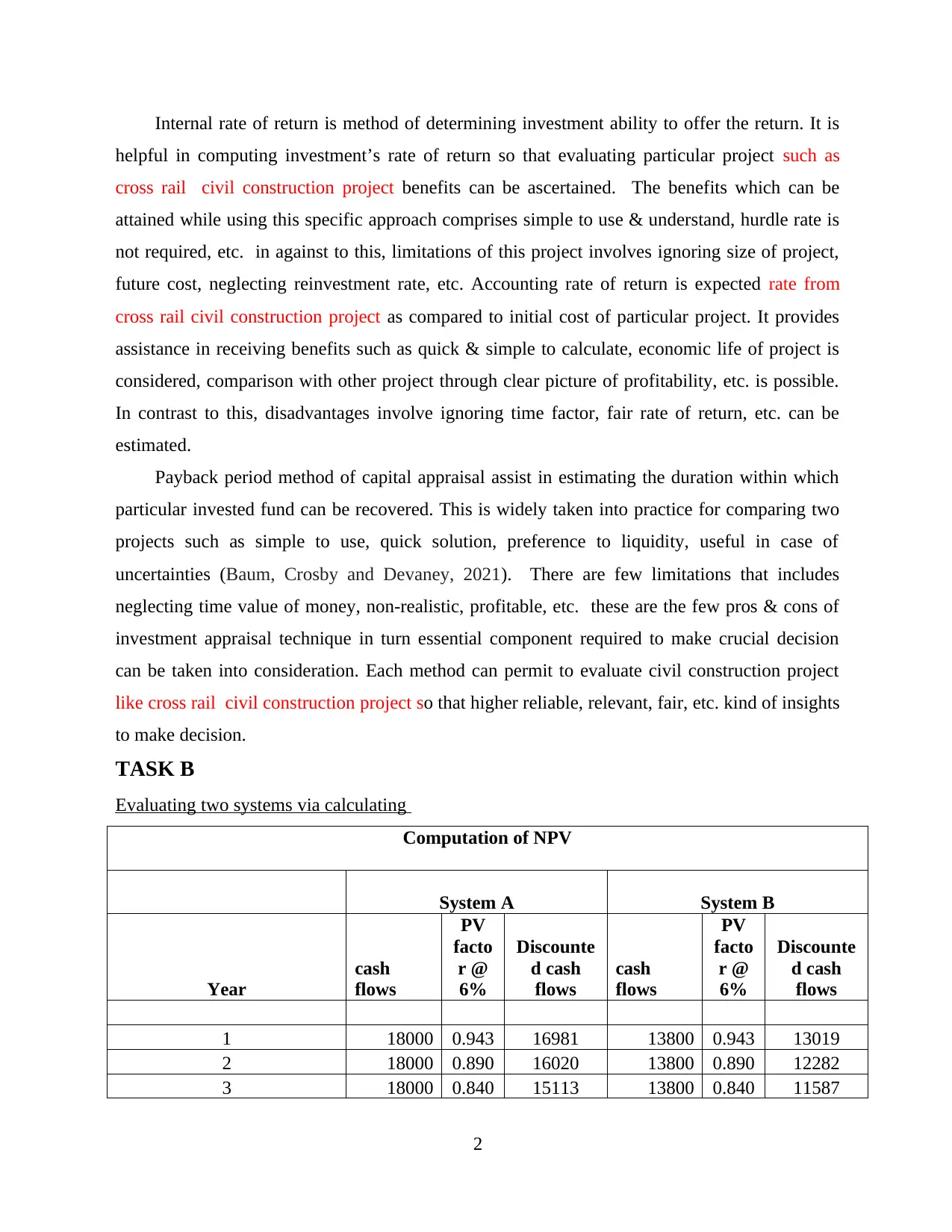

Internal rate of return is method of determining investment ability to offer the return. It is

helpful in computing investment’s rate of return so that evaluating particular project such as

cross rail civil construction project benefits can be ascertained. The benefits which can be

attained while using this specific approach comprises simple to use & understand, hurdle rate is

not required, etc. in against to this, limitations of this project involves ignoring size of project,

future cost, neglecting reinvestment rate, etc. Accounting rate of return is expected rate from

cross rail civil construction project as compared to initial cost of particular project. It provides

assistance in receiving benefits such as quick & simple to calculate, economic life of project is

considered, comparison with other project through clear picture of profitability, etc. is possible.

In contrast to this, disadvantages involve ignoring time factor, fair rate of return, etc. can be

estimated.

Payback period method of capital appraisal assist in estimating the duration within which

particular invested fund can be recovered. This is widely taken into practice for comparing two

projects such as simple to use, quick solution, preference to liquidity, useful in case of

uncertainties (Baum, Crosby and Devaney, 2021). There are few limitations that includes

neglecting time value of money, non-realistic, profitable, etc. these are the few pros & cons of

investment appraisal technique in turn essential component required to make crucial decision

can be taken into consideration. Each method can permit to evaluate civil construction project

like cross rail civil construction project so that higher reliable, relevant, fair, etc. kind of insights

to make decision.

TASK B

Evaluating two systems via calculating

Computation of NPV

System A System B

Year

cash

flows

PV

facto

r @

6%

Discounte

d cash

flows

cash

flows

PV

facto

r @

6%

Discounte

d cash

flows

1 18000 0.943 16981 13800 0.943 13019

2 18000 0.890 16020 13800 0.890 12282

3 18000 0.840 15113 13800 0.840 11587

2

helpful in computing investment’s rate of return so that evaluating particular project such as

cross rail civil construction project benefits can be ascertained. The benefits which can be

attained while using this specific approach comprises simple to use & understand, hurdle rate is

not required, etc. in against to this, limitations of this project involves ignoring size of project,

future cost, neglecting reinvestment rate, etc. Accounting rate of return is expected rate from

cross rail civil construction project as compared to initial cost of particular project. It provides

assistance in receiving benefits such as quick & simple to calculate, economic life of project is

considered, comparison with other project through clear picture of profitability, etc. is possible.

In contrast to this, disadvantages involve ignoring time factor, fair rate of return, etc. can be

estimated.

Payback period method of capital appraisal assist in estimating the duration within which

particular invested fund can be recovered. This is widely taken into practice for comparing two

projects such as simple to use, quick solution, preference to liquidity, useful in case of

uncertainties (Baum, Crosby and Devaney, 2021). There are few limitations that includes

neglecting time value of money, non-realistic, profitable, etc. these are the few pros & cons of

investment appraisal technique in turn essential component required to make crucial decision

can be taken into consideration. Each method can permit to evaluate civil construction project

like cross rail civil construction project so that higher reliable, relevant, fair, etc. kind of insights

to make decision.

TASK B

Evaluating two systems via calculating

Computation of NPV

System A System B

Year

cash

flows

PV

facto

r @

6%

Discounte

d cash

flows

cash

flows

PV

facto

r @

6%

Discounte

d cash

flows

1 18000 0.943 16981 13800 0.943 13019

2 18000 0.890 16020 13800 0.890 12282

3 18000 0.840 15113 13800 0.840 11587

2

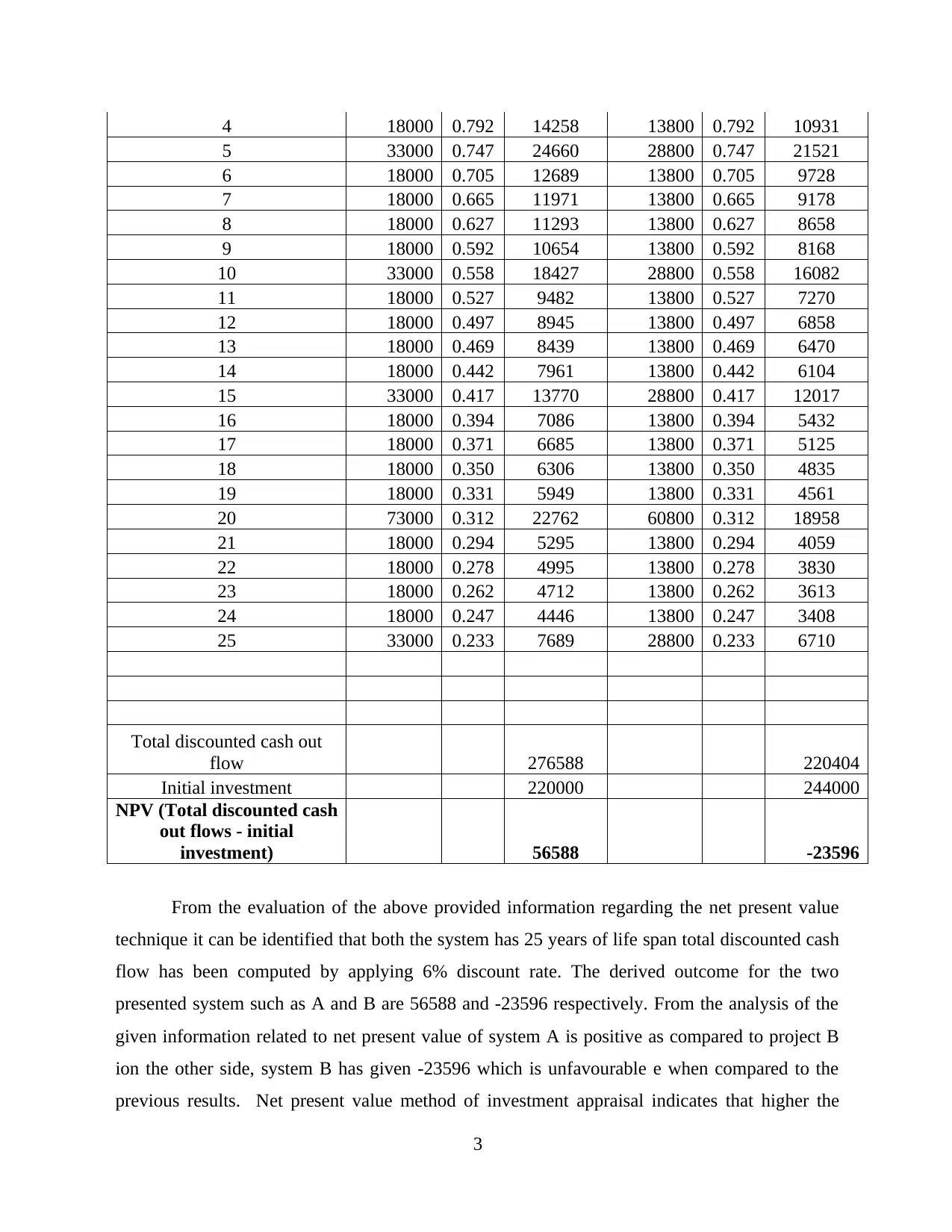

4 18000 0.792 14258 13800 0.792 10931

5 33000 0.747 24660 28800 0.747 21521

6 18000 0.705 12689 13800 0.705 9728

7 18000 0.665 11971 13800 0.665 9178

8 18000 0.627 11293 13800 0.627 8658

9 18000 0.592 10654 13800 0.592 8168

10 33000 0.558 18427 28800 0.558 16082

11 18000 0.527 9482 13800 0.527 7270

12 18000 0.497 8945 13800 0.497 6858

13 18000 0.469 8439 13800 0.469 6470

14 18000 0.442 7961 13800 0.442 6104

15 33000 0.417 13770 28800 0.417 12017

16 18000 0.394 7086 13800 0.394 5432

17 18000 0.371 6685 13800 0.371 5125

18 18000 0.350 6306 13800 0.350 4835

19 18000 0.331 5949 13800 0.331 4561

20 73000 0.312 22762 60800 0.312 18958

21 18000 0.294 5295 13800 0.294 4059

22 18000 0.278 4995 13800 0.278 3830

23 18000 0.262 4712 13800 0.262 3613

24 18000 0.247 4446 13800 0.247 3408

25 33000 0.233 7689 28800 0.233 6710

Total discounted cash out

flow 276588 220404

Initial investment 220000 244000

NPV (Total discounted cash

out flows - initial

investment) 56588 -23596

From the evaluation of the above provided information regarding the net present value

technique it can be identified that both the system has 25 years of life span total discounted cash

flow has been computed by applying 6% discount rate. The derived outcome for the two

presented system such as A and B are 56588 and -23596 respectively. From the analysis of the

given information related to net present value of system A is positive as compared to project B

ion the other side, system B has given -23596 which is unfavourable e when compared to the

previous results. Net present value method of investment appraisal indicates that higher the

3

5 33000 0.747 24660 28800 0.747 21521

6 18000 0.705 12689 13800 0.705 9728

7 18000 0.665 11971 13800 0.665 9178

8 18000 0.627 11293 13800 0.627 8658

9 18000 0.592 10654 13800 0.592 8168

10 33000 0.558 18427 28800 0.558 16082

11 18000 0.527 9482 13800 0.527 7270

12 18000 0.497 8945 13800 0.497 6858

13 18000 0.469 8439 13800 0.469 6470

14 18000 0.442 7961 13800 0.442 6104

15 33000 0.417 13770 28800 0.417 12017

16 18000 0.394 7086 13800 0.394 5432

17 18000 0.371 6685 13800 0.371 5125

18 18000 0.350 6306 13800 0.350 4835

19 18000 0.331 5949 13800 0.331 4561

20 73000 0.312 22762 60800 0.312 18958

21 18000 0.294 5295 13800 0.294 4059

22 18000 0.278 4995 13800 0.278 3830

23 18000 0.262 4712 13800 0.262 3613

24 18000 0.247 4446 13800 0.247 3408

25 33000 0.233 7689 28800 0.233 6710

Total discounted cash out

flow 276588 220404

Initial investment 220000 244000

NPV (Total discounted cash

out flows - initial

investment) 56588 -23596

From the evaluation of the above provided information regarding the net present value

technique it can be identified that both the system has 25 years of life span total discounted cash

flow has been computed by applying 6% discount rate. The derived outcome for the two

presented system such as A and B are 56588 and -23596 respectively. From the analysis of the

given information related to net present value of system A is positive as compared to project B

ion the other side, system B has given -23596 which is unfavourable e when compared to the

previous results. Net present value method of investment appraisal indicates that higher the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

NPG greater will be benefits (Rustagi, 2021). On the basis of given information, it can be

interpreted that discounted cash flow has been derived for the cost incurred by the client. With

respect to this, it can be specified that Project A has higher NPV which is considered to be

expensive as compared to B. from the evaluation it can be recognized that utilizing the project B

is highly beneficial in order to accomplish objective of higher profitability & sustainability.

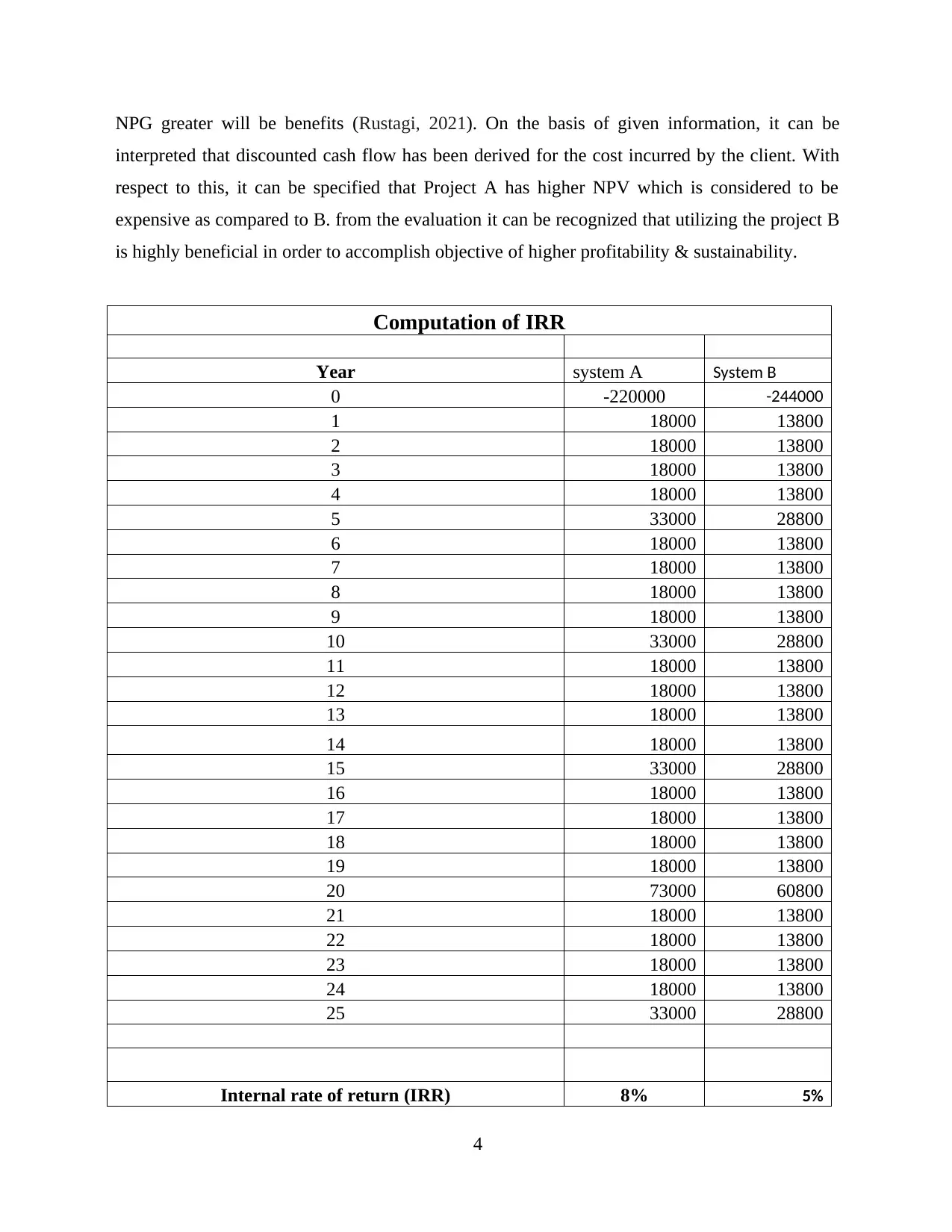

Computation of IRR

Year system A System B

0 -220000 -244000

1 18000 13800

2 18000 13800

3 18000 13800

4 18000 13800

5 33000 28800

6 18000 13800

7 18000 13800

8 18000 13800

9 18000 13800

10 33000 28800

11 18000 13800

12 18000 13800

13 18000 13800

14 18000 13800

15 33000 28800

16 18000 13800

17 18000 13800

18 18000 13800

19 18000 13800

20 73000 60800

21 18000 13800

22 18000 13800

23 18000 13800

24 18000 13800

25 33000 28800

Internal rate of return (IRR) 8% 5%

4

interpreted that discounted cash flow has been derived for the cost incurred by the client. With

respect to this, it can be specified that Project A has higher NPV which is considered to be

expensive as compared to B. from the evaluation it can be recognized that utilizing the project B

is highly beneficial in order to accomplish objective of higher profitability & sustainability.

Computation of IRR

Year system A System B

0 -220000 -244000

1 18000 13800

2 18000 13800

3 18000 13800

4 18000 13800

5 33000 28800

6 18000 13800

7 18000 13800

8 18000 13800

9 18000 13800

10 33000 28800

11 18000 13800

12 18000 13800

13 18000 13800

14 18000 13800

15 33000 28800

16 18000 13800

17 18000 13800

18 18000 13800

19 18000 13800

20 73000 60800

21 18000 13800

22 18000 13800

23 18000 13800

24 18000 13800

25 33000 28800

Internal rate of return (IRR) 8% 5%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On the basis of provided information regarding internal rate of return for the System A

&B, the derived results are 8 and 5% respectively. In addition to this, it can specified that higher

internal rate of return is considered to be profitable. The main reason behind considering this as

one of the beneficial as higher return can allow o meet the objective of higher profitability (Alle

and et.al., 2021). From the assessment of above presented computation it can be articulated that

System A will become able to offer 8% IRR whereas 5% will be obtained from the B obtain. It

can be recognized that A in terms of return Is highly beneficial as compared to B. B will offer

only 5% that r is no an effective outcome respect conducting investment expenditure. It can be

interpreted that System A is beneficial to adopt.

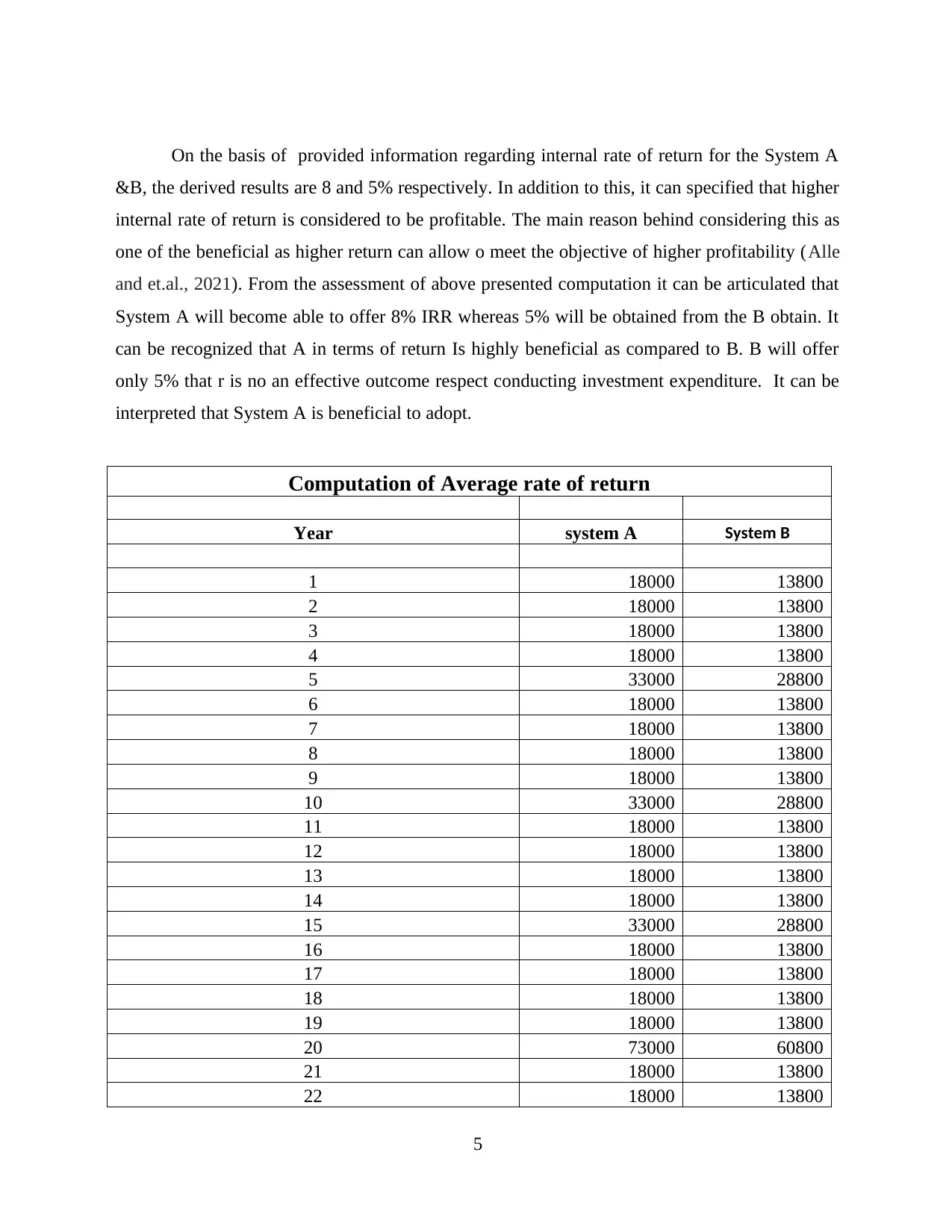

Computation of Average rate of return

Year system A System B

1 18000 13800

2 18000 13800

3 18000 13800

4 18000 13800

5 33000 28800

6 18000 13800

7 18000 13800

8 18000 13800

9 18000 13800

10 33000 28800

11 18000 13800

12 18000 13800

13 18000 13800

14 18000 13800

15 33000 28800

16 18000 13800

17 18000 13800

18 18000 13800

19 18000 13800

20 73000 60800

21 18000 13800

22 18000 13800

5

&B, the derived results are 8 and 5% respectively. In addition to this, it can specified that higher

internal rate of return is considered to be profitable. The main reason behind considering this as

one of the beneficial as higher return can allow o meet the objective of higher profitability (Alle

and et.al., 2021). From the assessment of above presented computation it can be articulated that

System A will become able to offer 8% IRR whereas 5% will be obtained from the B obtain. It

can be recognized that A in terms of return Is highly beneficial as compared to B. B will offer

only 5% that r is no an effective outcome respect conducting investment expenditure. It can be

interpreted that System A is beneficial to adopt.

Computation of Average rate of return

Year system A System B

1 18000 13800

2 18000 13800

3 18000 13800

4 18000 13800

5 33000 28800

6 18000 13800

7 18000 13800

8 18000 13800

9 18000 13800

10 33000 28800

11 18000 13800

12 18000 13800

13 18000 13800

14 18000 13800

15 33000 28800

16 18000 13800

17 18000 13800

18 18000 13800

19 18000 13800

20 73000 60800

21 18000 13800

22 18000 13800

5

23 18000 13800

24 18000 13800

25 33000 28800

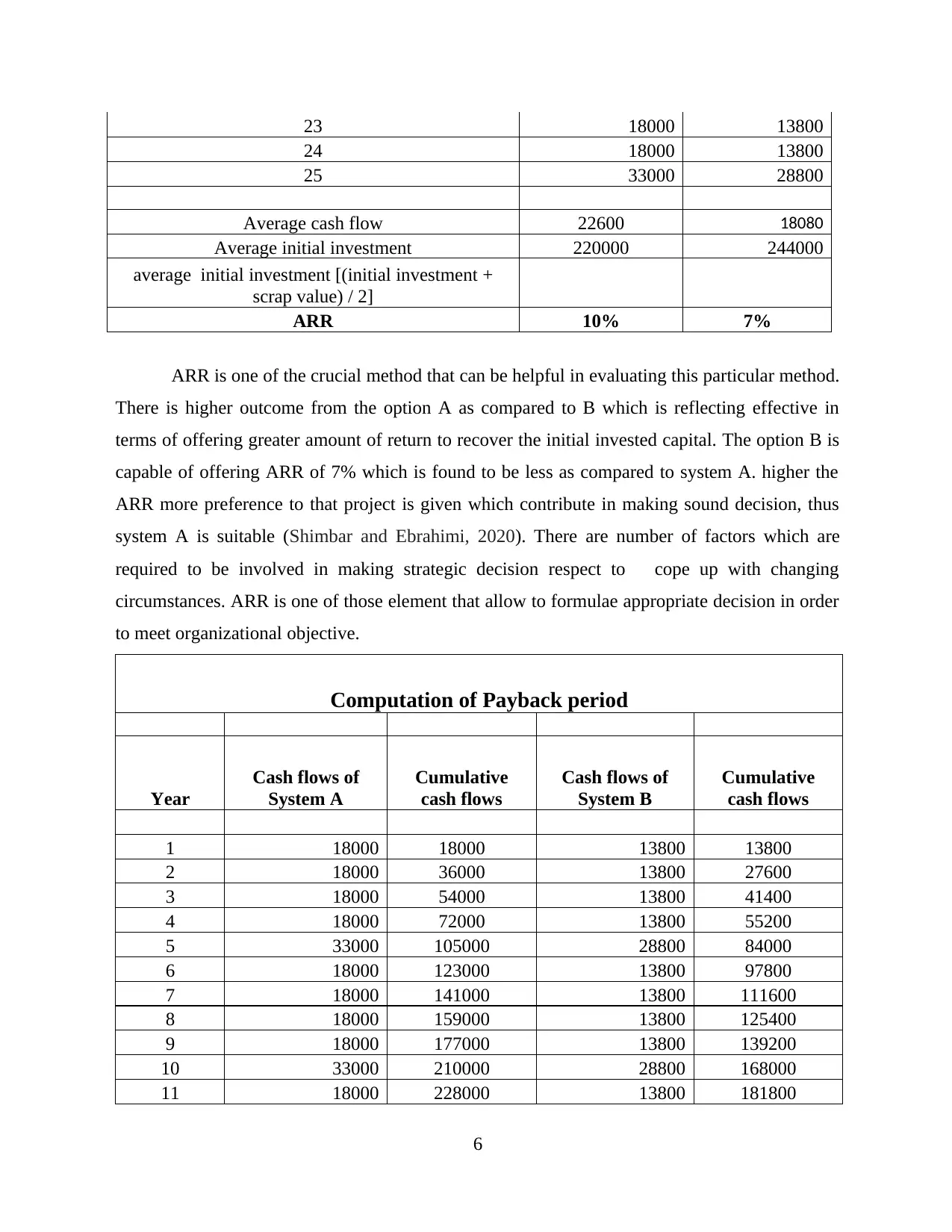

Average cash flow 22600 18080

Average initial investment 220000 244000

average initial investment [(initial investment +

scrap value) / 2]

ARR 10% 7%

ARR is one of the crucial method that can be helpful in evaluating this particular method.

There is higher outcome from the option A as compared to B which is reflecting effective in

terms of offering greater amount of return to recover the initial invested capital. The option B is

capable of offering ARR of 7% which is found to be less as compared to system A. higher the

ARR more preference to that project is given which contribute in making sound decision, thus

system A is suitable (Shimbar and Ebrahimi, 2020). There are number of factors which are

required to be involved in making strategic decision respect to cope up with changing

circumstances. ARR is one of those element that allow to formulae appropriate decision in order

to meet organizational objective.

Computation of Payback period

Year

Cash flows of

System A

Cumulative

cash flows

Cash flows of

System B

Cumulative

cash flows

1 18000 18000 13800 13800

2 18000 36000 13800 27600

3 18000 54000 13800 41400

4 18000 72000 13800 55200

5 33000 105000 28800 84000

6 18000 123000 13800 97800

7 18000 141000 13800 111600

8 18000 159000 13800 125400

9 18000 177000 13800 139200

10 33000 210000 28800 168000

11 18000 228000 13800 181800

6

24 18000 13800

25 33000 28800

Average cash flow 22600 18080

Average initial investment 220000 244000

average initial investment [(initial investment +

scrap value) / 2]

ARR 10% 7%

ARR is one of the crucial method that can be helpful in evaluating this particular method.

There is higher outcome from the option A as compared to B which is reflecting effective in

terms of offering greater amount of return to recover the initial invested capital. The option B is

capable of offering ARR of 7% which is found to be less as compared to system A. higher the

ARR more preference to that project is given which contribute in making sound decision, thus

system A is suitable (Shimbar and Ebrahimi, 2020). There are number of factors which are

required to be involved in making strategic decision respect to cope up with changing

circumstances. ARR is one of those element that allow to formulae appropriate decision in order

to meet organizational objective.

Computation of Payback period

Year

Cash flows of

System A

Cumulative

cash flows

Cash flows of

System B

Cumulative

cash flows

1 18000 18000 13800 13800

2 18000 36000 13800 27600

3 18000 54000 13800 41400

4 18000 72000 13800 55200

5 33000 105000 28800 84000

6 18000 123000 13800 97800

7 18000 141000 13800 111600

8 18000 159000 13800 125400

9 18000 177000 13800 139200

10 33000 210000 28800 168000

11 18000 228000 13800 181800

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

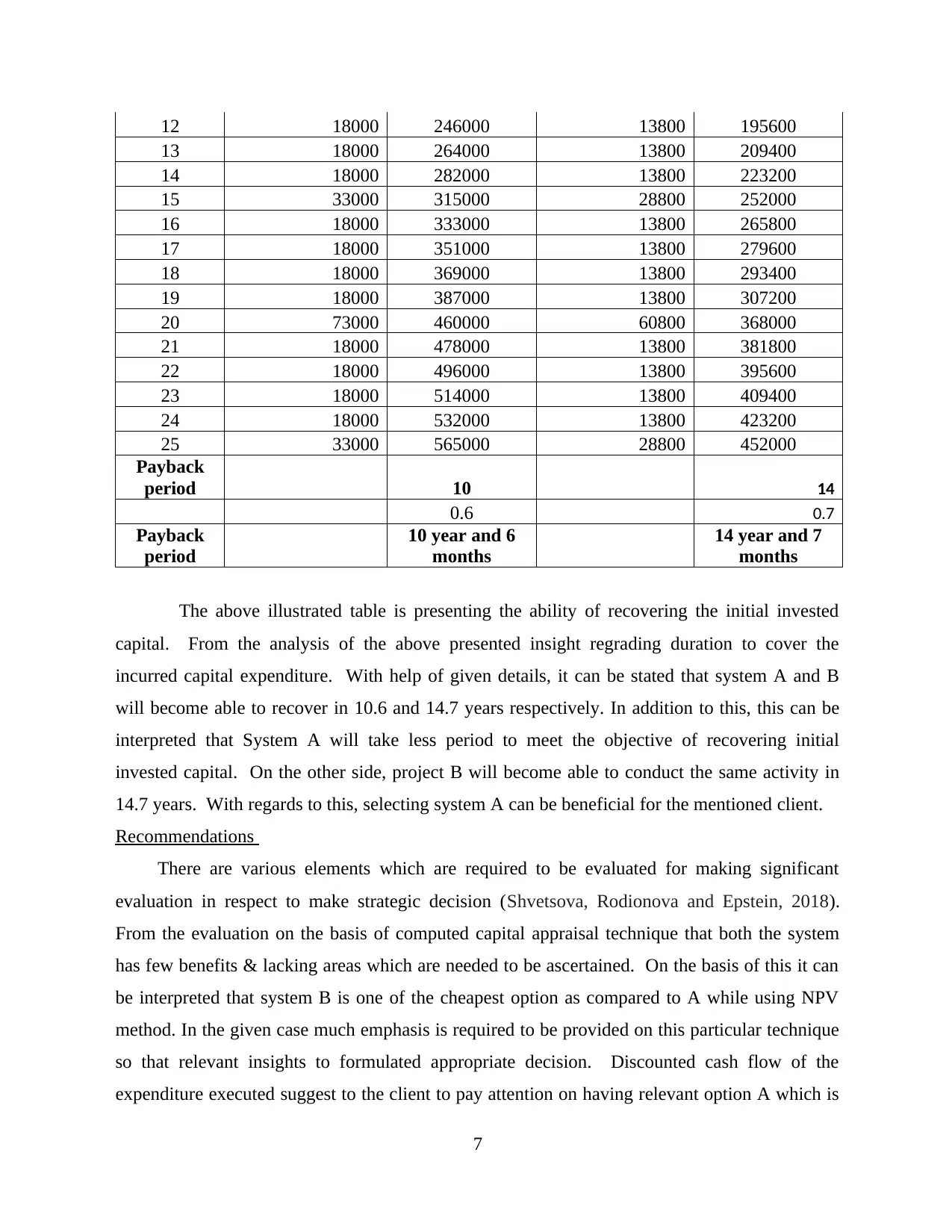

12 18000 246000 13800 195600

13 18000 264000 13800 209400

14 18000 282000 13800 223200

15 33000 315000 28800 252000

16 18000 333000 13800 265800

17 18000 351000 13800 279600

18 18000 369000 13800 293400

19 18000 387000 13800 307200

20 73000 460000 60800 368000

21 18000 478000 13800 381800

22 18000 496000 13800 395600

23 18000 514000 13800 409400

24 18000 532000 13800 423200

25 33000 565000 28800 452000

Payback

period 10 14

0.6 0.7

Payback

period

10 year and 6

months

14 year and 7

months

The above illustrated table is presenting the ability of recovering the initial invested

capital. From the analysis of the above presented insight regrading duration to cover the

incurred capital expenditure. With help of given details, it can be stated that system A and B

will become able to recover in 10.6 and 14.7 years respectively. In addition to this, this can be

interpreted that System A will take less period to meet the objective of recovering initial

invested capital. On the other side, project B will become able to conduct the same activity in

14.7 years. With regards to this, selecting system A can be beneficial for the mentioned client.

Recommendations

There are various elements which are required to be evaluated for making significant

evaluation in respect to make strategic decision (Shvetsova, Rodionova and Epstein, 2018).

From the evaluation on the basis of computed capital appraisal technique that both the system

has few benefits & lacking areas which are needed to be ascertained. On the basis of this it can

be interpreted that system B is one of the cheapest option as compared to A while using NPV

method. In the given case much emphasis is required to be provided on this particular technique

so that relevant insights to formulated appropriate decision. Discounted cash flow of the

expenditure executed suggest to the client to pay attention on having relevant option A which is

7

13 18000 264000 13800 209400

14 18000 282000 13800 223200

15 33000 315000 28800 252000

16 18000 333000 13800 265800

17 18000 351000 13800 279600

18 18000 369000 13800 293400

19 18000 387000 13800 307200

20 73000 460000 60800 368000

21 18000 478000 13800 381800

22 18000 496000 13800 395600

23 18000 514000 13800 409400

24 18000 532000 13800 423200

25 33000 565000 28800 452000

Payback

period 10 14

0.6 0.7

Payback

period

10 year and 6

months

14 year and 7

months

The above illustrated table is presenting the ability of recovering the initial invested

capital. From the analysis of the above presented insight regrading duration to cover the

incurred capital expenditure. With help of given details, it can be stated that system A and B

will become able to recover in 10.6 and 14.7 years respectively. In addition to this, this can be

interpreted that System A will take less period to meet the objective of recovering initial

invested capital. On the other side, project B will become able to conduct the same activity in

14.7 years. With regards to this, selecting system A can be beneficial for the mentioned client.

Recommendations

There are various elements which are required to be evaluated for making significant

evaluation in respect to make strategic decision (Shvetsova, Rodionova and Epstein, 2018).

From the evaluation on the basis of computed capital appraisal technique that both the system

has few benefits & lacking areas which are needed to be ascertained. On the basis of this it can

be interpreted that system B is one of the cheapest option as compared to A while using NPV

method. In the given case much emphasis is required to be provided on this particular technique

so that relevant insights to formulated appropriate decision. Discounted cash flow of the

expenditure executed suggest to the client to pay attention on having relevant option A which is

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered to be cheap when compared to B. With regard to the capital appraisal technique such

as internal & accounting rate of return and payback period the most beneficial project is

considered to A. The main reason behind stating A is more profitable is due to higher return and

less duration to recover capital expenditure. On the basis of requirement of client to have those

systems which is cheap in respect to overcome implemented cost. It can be interpreted that

Project B should be taken into consideration to achieve predetermined goal.

CONCLUSION

From the above report it can be concluded that construction management is one of the

significant practice that aid to manage related project. In addition to this, current report has

evaluated invested appraisal techniques such as payback period, IRR, ARR and net present value

along with advantages & drawbacks. Present study has computed these methods which has

analysed that project B is beneficial for the client.

8

as internal & accounting rate of return and payback period the most beneficial project is

considered to A. The main reason behind stating A is more profitable is due to higher return and

less duration to recover capital expenditure. On the basis of requirement of client to have those

systems which is cheap in respect to overcome implemented cost. It can be interpreted that

Project B should be taken into consideration to achieve predetermined goal.

CONCLUSION

From the above report it can be concluded that construction management is one of the

significant practice that aid to manage related project. In addition to this, current report has

evaluated invested appraisal techniques such as payback period, IRR, ARR and net present value

along with advantages & drawbacks. Present study has computed these methods which has

analysed that project B is beneficial for the client.

8

REFERENCES

Books and journals

Alles, L. and et.al., 2021. An investigation of the usage of capital budgeting techniques by small

and medium enterprises. Quality & Quantity. 55(3). pp.993-1006.

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Kengatharan, L. and Nurullah, M., 2018. Capital investment appraisal practices in the emerging

market economy of Sri Lanka. Asian Journal of Business and Accounting. 11(2).

pp.121-150.

Rustagi, R. P., 2021. Investment Analysis & Portfolio Management. Sultan Chand & Sons.

Shimbar, A. and Ebrahimi, S.B., 2020. Political risk and valuation of renewable energy

investments in developing countries. Renewable Energy. 145. pp.1325-1333.

Shvetsova, O. A., Rodionova, E. A. and Epstein, M. Z., 2018. Evaluation of investment projects

under uncertainty: multi-criteria approach using interval data. Entrepreneurship and

Sustainability Issues. 5(4). pp.914-928.

Soka, I. M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Online

Investment appraisal techniques. 2020. [Online]. Available through: <

https://www.ig.com/uk/glossary-trading-terms/investment-appraisal-definition >.

9

Books and journals

Alles, L. and et.al., 2021. An investigation of the usage of capital budgeting techniques by small

and medium enterprises. Quality & Quantity. 55(3). pp.993-1006.

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Kengatharan, L. and Nurullah, M., 2018. Capital investment appraisal practices in the emerging

market economy of Sri Lanka. Asian Journal of Business and Accounting. 11(2).

pp.121-150.

Rustagi, R. P., 2021. Investment Analysis & Portfolio Management. Sultan Chand & Sons.

Shimbar, A. and Ebrahimi, S.B., 2020. Political risk and valuation of renewable energy

investments in developing countries. Renewable Energy. 145. pp.1325-1333.

Shvetsova, O. A., Rodionova, E. A. and Epstein, M. Z., 2018. Evaluation of investment projects

under uncertainty: multi-criteria approach using interval data. Entrepreneurship and

Sustainability Issues. 5(4). pp.914-928.

Soka, I. M., 2020. Impact of Appraisal Techniques on Investment Returns A Survey of

Institutional Investors (Doctoral dissertation, The Open University of Tanzania).

Online

Investment appraisal techniques. 2020. [Online]. Available through: <

https://www.ig.com/uk/glossary-trading-terms/investment-appraisal-definition >.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.