Comprehensive Insurance and Risk Management Assignment

VerifiedAdded on 2022/08/14

|14

|3465

|14

Homework Assignment

AI Summary

This assignment comprehensively explores various aspects of insurance and risk management. Section A defines different types of risk, including pure, speculative, diversifiable, and non-diversifiable risks, and discusses Australian consumer protection acts related to financial advice. It also examines the underwriting process, emphasizing the significance of evaluating family health history, personal health history, and drug use. Section B involves a case study, calculating life cover based on a client's financial situation, considering mortgage, loans, and future expenses, and recommending suitable premium options like stepped, level, and hybrid premiums. The assignment further addresses personal insurance advice, including term life, TPD, and trauma insurance, and explores the process of providing and implementing financial advice, considering legislation and underwriting. Additionally, it delves into the taxation of insurance premiums and benefits for individuals and employers, covering term life, income protection, and trauma policies. The assignment concludes with a discussion of trauma insurance, its benefits, policy structures, and coverage for life-threatening conditions.

Running head: INSURANCE

Insurance

Name of the Student

Name of the University

Author Note

Insurance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INSURANCE

Table of Contents

Section A.........................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Section B......................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................7

Question 3....................................................................................................................................8

Answer to Question 4.................................................................................................................10

References..................................................................................................................................12

Table of Contents

Section A.........................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Section B......................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................7

Question 3....................................................................................................................................8

Answer to Question 4.................................................................................................................10

References..................................................................................................................................12

2INSURANCE

Section A

Question 1

a) A pure risk arises when there is only the possibility of a loss or no loss incurred by an

individual. A speculative risk is one in which there is a possibility of either profit or loss

to be incurred by an individual.

b) A diversifiable risk is unique to a portfolio and can be avoided by changing the portfolio.

Non-diversifiable risk is inherent to all assets and liabilities and cannot be avoided.

c) Loss of income due to sickness is a pure risk. Investing in shares is a speculative risk.

Change in customer preferences is a diversifiable risk. Inflation is a non-diversifiable

risk.

Question 2

The various acts which are in place in Australia to protect the consumers with regards to

the financial advice received by them are the Insurance Act 1973, Insurance Contracts Act 1984,

and the Life Insurance Act 1995. The Insurance Act 1973 improves consumer protection by

restricting the general insurance business only to entities which are able to meet the suitability

requirements. These requirements include policies designed to ensure solvency, capital adequacy

and effective risk management. In case of an unsatisfactory management or an unsatisfactory

financial position of the company, the continuance of the same may be threatened. Even if the

company winds up from business, the interests of consumers are well protected. Another relevant

act is the Insurance Contracts Act 1984. This states that the insurer must inform the policy owner

about the renewal of the policy. Otherwise the policy automatically gets renewed under the

original guidelines. In case of any change in health in a life insurance policy, the same is not

required to be disclosed. The Life Insurance Act 1995 was passed to act as a successor to the

Section A

Question 1

a) A pure risk arises when there is only the possibility of a loss or no loss incurred by an

individual. A speculative risk is one in which there is a possibility of either profit or loss

to be incurred by an individual.

b) A diversifiable risk is unique to a portfolio and can be avoided by changing the portfolio.

Non-diversifiable risk is inherent to all assets and liabilities and cannot be avoided.

c) Loss of income due to sickness is a pure risk. Investing in shares is a speculative risk.

Change in customer preferences is a diversifiable risk. Inflation is a non-diversifiable

risk.

Question 2

The various acts which are in place in Australia to protect the consumers with regards to

the financial advice received by them are the Insurance Act 1973, Insurance Contracts Act 1984,

and the Life Insurance Act 1995. The Insurance Act 1973 improves consumer protection by

restricting the general insurance business only to entities which are able to meet the suitability

requirements. These requirements include policies designed to ensure solvency, capital adequacy

and effective risk management. In case of an unsatisfactory management or an unsatisfactory

financial position of the company, the continuance of the same may be threatened. Even if the

company winds up from business, the interests of consumers are well protected. Another relevant

act is the Insurance Contracts Act 1984. This states that the insurer must inform the policy owner

about the renewal of the policy. Otherwise the policy automatically gets renewed under the

original guidelines. In case of any change in health in a life insurance policy, the same is not

required to be disclosed. The Life Insurance Act 1995 was passed to act as a successor to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INSURANCE

Insurance Act 1945. This act acts as a means of consumer protection by ensuring the capital

adequacy and solvency of a company. The insurance companies are supervised by ASIC and

APRA. Any transfers and amalgamations between companies are supervised by the court.

Question 3

a) The main reason behind evaluating the family health history, personal health history and

dug use of a client is their relevance to the process of underwriting. These issues tend to

impact the health of a client along with the company’s potential to pay them. In order to

have a better idea of the risk they are undertaking and to determine the amount of

premium, these factors become relevant in underwriting a policy. Hence, people who

have a long history of health issues are given a policy with high premium. In case of a

healthier client, the premiums tend to be lower due to the low risk involved.

b) In case of a loss making underwriter, constantly increasing the premiums will have a

negative impact on policy retention. In these cases, policy owners tend to take their

insurance policies away from the company. To retain the customers, the company will

have to reduce their premium pool. This ultimately increases the risk concentration of the

entity. Risk concentration leads to higher claims costs, increase in earnings volatility and

reduces the profitability of entities. Hence, the continuously increasing premiums tend to

adversely impact the policy retention and ultimately impact the risk concentration of the

policy.

Section B

Question 1

a)

i.

Insurance Act 1945. This act acts as a means of consumer protection by ensuring the capital

adequacy and solvency of a company. The insurance companies are supervised by ASIC and

APRA. Any transfers and amalgamations between companies are supervised by the court.

Question 3

a) The main reason behind evaluating the family health history, personal health history and

dug use of a client is their relevance to the process of underwriting. These issues tend to

impact the health of a client along with the company’s potential to pay them. In order to

have a better idea of the risk they are undertaking and to determine the amount of

premium, these factors become relevant in underwriting a policy. Hence, people who

have a long history of health issues are given a policy with high premium. In case of a

healthier client, the premiums tend to be lower due to the low risk involved.

b) In case of a loss making underwriter, constantly increasing the premiums will have a

negative impact on policy retention. In these cases, policy owners tend to take their

insurance policies away from the company. To retain the customers, the company will

have to reduce their premium pool. This ultimately increases the risk concentration of the

entity. Risk concentration leads to higher claims costs, increase in earnings volatility and

reduces the profitability of entities. Hence, the continuously increasing premiums tend to

adversely impact the policy retention and ultimately impact the risk concentration of the

policy.

Section B

Question 1

a)

i.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INSURANCE

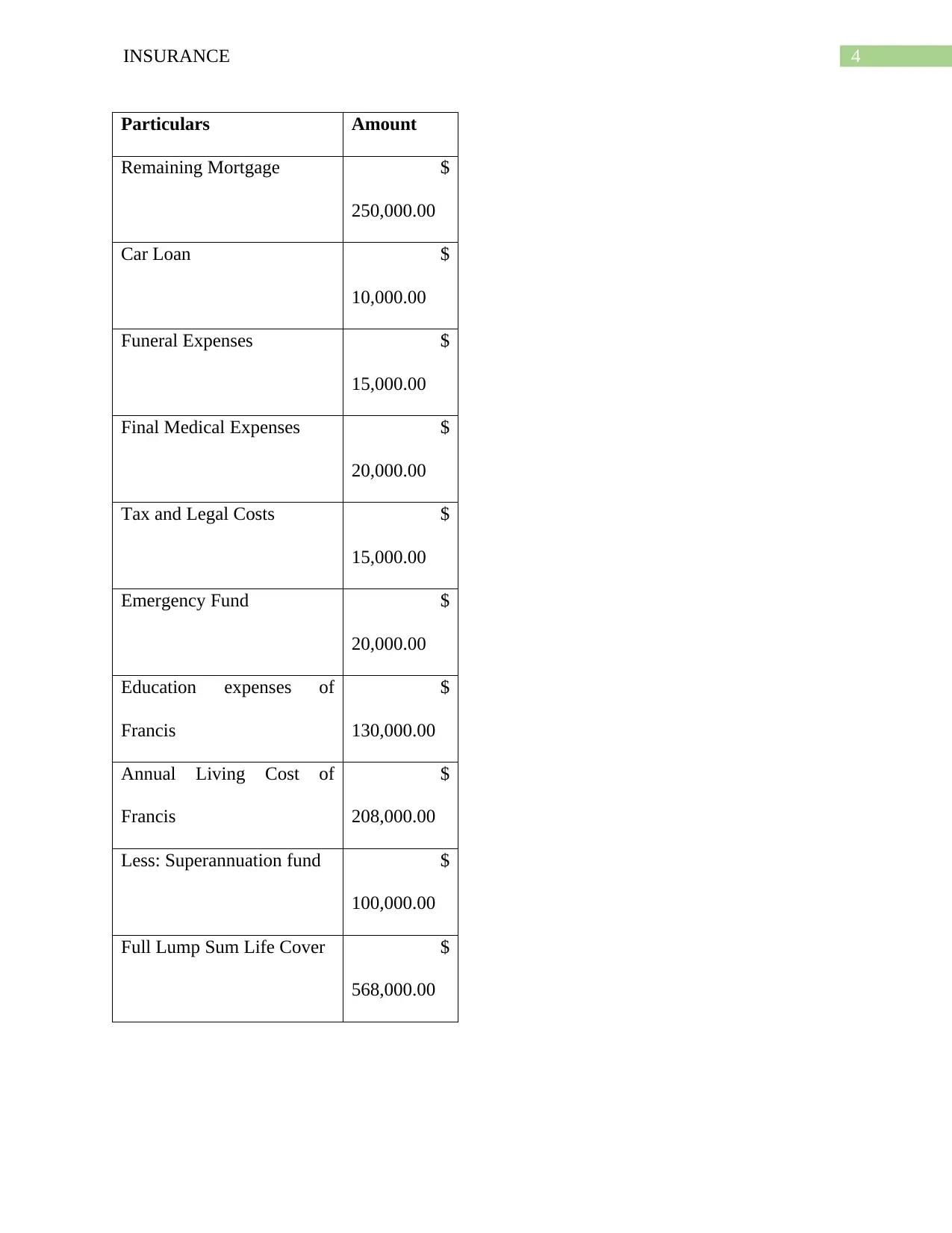

Particulars Amount

Remaining Mortgage $

250,000.00

Car Loan $

10,000.00

Funeral Expenses $

15,000.00

Final Medical Expenses $

20,000.00

Tax and Legal Costs $

15,000.00

Emergency Fund $

20,000.00

Education expenses of

Francis

$

130,000.00

Annual Living Cost of

Francis

$

208,000.00

Less: Superannuation fund $

100,000.00

Full Lump Sum Life Cover $

568,000.00

Particulars Amount

Remaining Mortgage $

250,000.00

Car Loan $

10,000.00

Funeral Expenses $

15,000.00

Final Medical Expenses $

20,000.00

Tax and Legal Costs $

15,000.00

Emergency Fund $

20,000.00

Education expenses of

Francis

$

130,000.00

Annual Living Cost of

Francis

$

208,000.00

Less: Superannuation fund $

100,000.00

Full Lump Sum Life Cover $

568,000.00

5INSURANCE

In the above case, the calculations have been done on the basis of the requirements of

Courtney. Hence, the balance in the cash management account has not been taken into

consideration. It is assumed that the superannuation will be used in the payment of her remaining

debts. As she intends to retain her house in the long run, the value of the house is not included in

calculating the amount of life cover. Both the tuition fees and the living costs of Frances have

been taken for an estimated period of 8 years, which is the time required for him to complete his

education. As the superannuation fund can be used in the payment of debts, it has been deducted

from the annual costs incurred by her. This gives a total of $568000 which would be an

appropriate life cover. Future values have not been taken into consideration.

II. The premium options that are available for Courtney are the stepped premiums, level

premiums and hybrid premiums. In Stepped premiums, the premium tends to increase

as the policy holder gets older. They cater better to the needs of clients who are closer

to retirement or expiry. Level premiums do not change with the age of the policy

holder but tend to be more costly at the beginning of the policy (Adler 2015). The

main advantage of this premium is that the costs are pre-determined and there is no

drastic change in costs with time. One of the disadvantages of the level premium is

that it may take a long time to become cheaper than a stepped premium option.

Another policy is the hybrid premium which is a combination of both. This is useful

for clients who want to hold the cover for an extended period of time but cannot

afford the cost of level premium in the initial years. The most suitable policy for

Courtney would be the level premium as the premium costs will be lower with age

and she can reap the benefits in the long run.

In the above case, the calculations have been done on the basis of the requirements of

Courtney. Hence, the balance in the cash management account has not been taken into

consideration. It is assumed that the superannuation will be used in the payment of her remaining

debts. As she intends to retain her house in the long run, the value of the house is not included in

calculating the amount of life cover. Both the tuition fees and the living costs of Frances have

been taken for an estimated period of 8 years, which is the time required for him to complete his

education. As the superannuation fund can be used in the payment of debts, it has been deducted

from the annual costs incurred by her. This gives a total of $568000 which would be an

appropriate life cover. Future values have not been taken into consideration.

II. The premium options that are available for Courtney are the stepped premiums, level

premiums and hybrid premiums. In Stepped premiums, the premium tends to increase

as the policy holder gets older. They cater better to the needs of clients who are closer

to retirement or expiry. Level premiums do not change with the age of the policy

holder but tend to be more costly at the beginning of the policy (Adler 2015). The

main advantage of this premium is that the costs are pre-determined and there is no

drastic change in costs with time. One of the disadvantages of the level premium is

that it may take a long time to become cheaper than a stepped premium option.

Another policy is the hybrid premium which is a combination of both. This is useful

for clients who want to hold the cover for an extended period of time but cannot

afford the cost of level premium in the initial years. The most suitable policy for

Courtney would be the level premium as the premium costs will be lower with age

and she can reap the benefits in the long run.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INSURANCE

III. The other personal insurance advice that would be provided to Courtney would

include undertaking more policies to ensure more safety with regards to her son’s

future. The main advantage provided by the personal insurance policies is that they

provide the required funds to meet the income and capital needs of Courtney when a

trigger event occurs. This would involve the inclusion of all of term life insurance,

TPD and trauma insurance under one policy. It would also involve the inclusion of

another person to be covered under the life insurance policy. The main advantage of

the term life insurance policy is that it would provide a lump sum death benefit in the

event of death. All the debt payments can be covered with this amount. Income

protection insurance, in a manner similar to that of TPD insurance, covers the

inability to earn income. The cover would be decided by the insurer but would be

useful for situations when she is unable to work due to some unforeseen

circumstances. Another advice which should be considered by her is the linking of the

insurance policy to her superannuation fund. This is a good platform for obtaining tax

deductibility for insurance while also acting as an alternative funding mechanism for

the policies undertaken by her. However, not all policies are allowed to be included in

this situation.

b) The process that would be followed in relation to providing and implementing the

advice would be as follows:

The first step would involve the interacting with the client thoroughly and identify

their needs and requirements for both the short term and the long term;

After which the focus would be shifted towards building a rapport with the client.

This will involve providing them with confidence that the firm will act by keeping

III. The other personal insurance advice that would be provided to Courtney would

include undertaking more policies to ensure more safety with regards to her son’s

future. The main advantage provided by the personal insurance policies is that they

provide the required funds to meet the income and capital needs of Courtney when a

trigger event occurs. This would involve the inclusion of all of term life insurance,

TPD and trauma insurance under one policy. It would also involve the inclusion of

another person to be covered under the life insurance policy. The main advantage of

the term life insurance policy is that it would provide a lump sum death benefit in the

event of death. All the debt payments can be covered with this amount. Income

protection insurance, in a manner similar to that of TPD insurance, covers the

inability to earn income. The cover would be decided by the insurer but would be

useful for situations when she is unable to work due to some unforeseen

circumstances. Another advice which should be considered by her is the linking of the

insurance policy to her superannuation fund. This is a good platform for obtaining tax

deductibility for insurance while also acting as an alternative funding mechanism for

the policies undertaken by her. However, not all policies are allowed to be included in

this situation.

b) The process that would be followed in relation to providing and implementing the

advice would be as follows:

The first step would involve the interacting with the client thoroughly and identify

their needs and requirements for both the short term and the long term;

After which the focus would be shifted towards building a rapport with the client.

This will involve providing them with confidence that the firm will act by keeping

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INSURANCE

the best intentions of the client and provide assurance about keeping their best

interests in mind;

The client’s needs would be identified on the basis of the above interaction. Some

of them would be explained to them to obtain their confirmation. Courtney is need

of a life insurance policy which covers her life premium while also meeting with

her mortgage and other payment obligations. Similarly, she would also be told

that her cash management account would not be included in the payment of

insurance related expenses or their calculation;

Similarly, complying with the legislation will also be taken into consideration.

These include the appropriate usage of the terms ‘independent’, ‘impartial’ and

‘unbiased’. No fraudulent inducements like providing misinformation or making

false promises will be undertaken as a part of the business. Similarly, no material

facts would be concealed or conflicting remuneration would be taken to complete

a deal;

The underwriting process would be done on the basis of the requirements of

Courtney and her personal family history. In this case, a majority of her expenses

and requirements would be taken into consideration. Similarly, a thorough

background check of her personal health and the family health will be conducted.

The risk involved in her job and retaining the house will all be considered during

the underwriting process; and

Other advice would be provided to her about the insurances like TPD and Salary

Continuance Insurance option would be explained to her. The benefits of linking

the best intentions of the client and provide assurance about keeping their best

interests in mind;

The client’s needs would be identified on the basis of the above interaction. Some

of them would be explained to them to obtain their confirmation. Courtney is need

of a life insurance policy which covers her life premium while also meeting with

her mortgage and other payment obligations. Similarly, she would also be told

that her cash management account would not be included in the payment of

insurance related expenses or their calculation;

Similarly, complying with the legislation will also be taken into consideration.

These include the appropriate usage of the terms ‘independent’, ‘impartial’ and

‘unbiased’. No fraudulent inducements like providing misinformation or making

false promises will be undertaken as a part of the business. Similarly, no material

facts would be concealed or conflicting remuneration would be taken to complete

a deal;

The underwriting process would be done on the basis of the requirements of

Courtney and her personal family history. In this case, a majority of her expenses

and requirements would be taken into consideration. Similarly, a thorough

background check of her personal health and the family health will be conducted.

The risk involved in her job and retaining the house will all be considered during

the underwriting process; and

Other advice would be provided to her about the insurances like TPD and Salary

Continuance Insurance option would be explained to her. The benefits of linking

8INSURANCE

the insurance option to the superannuation fund would also be thoroughly

explained.

Question 2

a) I) The premiums of a term life insurance policy owned and purchased by the insured is

not allowed as a deduction for taxation purposes for an individual while it is allowed as a

deduction in the hands of the employer. The FBT on premium is not allowed as a

deduction in the hands of the individual while it is allowed as a deduction in the hands of

the employer.

II) The premium on the income protection fund owned by an insured with their employer

paying the premium is allowed as a tax deduction for both the individual and the

employer. However, FBT on premium is not allowed as a deduction and income tax is

levied on the proceeds.

III) The premium on the trauma policy owned and paid for by the insured is not allowed

as a deduction in the hands of the individual while it is allowed as a deduction in the

hands of the employer. However, the proceeds from the life insurance product are not

allowed as a deduction for both the individual and the employer.

b) For Life insurance products, the premium paid by an individual is not allowed as a

deduction. The TPD and Trauma insurance premium paid for by an individual is not

allowed as a deduction.

Question 3

I. The trauma insurance provides a benefit when the person whose life is insured suffers

from a life-threatening condition like cancer, stroke, heart attack or an organ transplant as

defined in the conditions of the policy. The other names for this insurance include

the insurance option to the superannuation fund would also be thoroughly

explained.

Question 2

a) I) The premiums of a term life insurance policy owned and purchased by the insured is

not allowed as a deduction for taxation purposes for an individual while it is allowed as a

deduction in the hands of the employer. The FBT on premium is not allowed as a

deduction in the hands of the individual while it is allowed as a deduction in the hands of

the employer.

II) The premium on the income protection fund owned by an insured with their employer

paying the premium is allowed as a tax deduction for both the individual and the

employer. However, FBT on premium is not allowed as a deduction and income tax is

levied on the proceeds.

III) The premium on the trauma policy owned and paid for by the insured is not allowed

as a deduction in the hands of the individual while it is allowed as a deduction in the

hands of the employer. However, the proceeds from the life insurance product are not

allowed as a deduction for both the individual and the employer.

b) For Life insurance products, the premium paid by an individual is not allowed as a

deduction. The TPD and Trauma insurance premium paid for by an individual is not

allowed as a deduction.

Question 3

I. The trauma insurance provides a benefit when the person whose life is insured suffers

from a life-threatening condition like cancer, stroke, heart attack or an organ transplant as

defined in the conditions of the policy. The other names for this insurance include

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INSURANCE

Critical Illness, Major Illness Insurance or Living Insurance (Lowe and Reid 2017). The

claim can be made by an individual if the insured suffers from an illness or an accident

which is defined under the term ‘trauma’ in the insurance policy. Paralysis, heart bypass

surgery and major head trauma are also covered under the definition of trauma. However,

no benefit would be paid for deliberate, self-inflicted acts or infection. For events like

heart attack, stroke and cancer, the cover will be excluded for the first 90 days.

II. Since its introduction in the late 1980s in Australia, trauma insurance has begun to grow

in terms of sales and popularity. The various policy structures available for a trauma

insurance are as follows:

It is available as an additional with a whole-of-life or an endowment policy. Any

payment for the trauma insurance was considered as an advancement of the total

benefit and the policy ended after the payment of the trauma benefit.

For a term life insurance policy, it was available as an additional rider benefit. In

this situation, the trauma benefit is considered as an advancement of benefit

payment. However, the policy ended only if the trauma benefit amount was the

same as the term benefit amount. Otherwise, the policy continued with an insured

benefit equal to the remaining death cover. Some policies also allow the

segregation of the trauma benefit from that of the death benefit in case of a term

life insurance policy. The option to buyback is also available. Here, the level of

the death benefit reduced by the trauma benefit is reinstated. This is done through

a right of the insured to reinstate the death benefit sum insured by making a

certain amount of predetermined payments after a predetermined period.

Critical Illness, Major Illness Insurance or Living Insurance (Lowe and Reid 2017). The

claim can be made by an individual if the insured suffers from an illness or an accident

which is defined under the term ‘trauma’ in the insurance policy. Paralysis, heart bypass

surgery and major head trauma are also covered under the definition of trauma. However,

no benefit would be paid for deliberate, self-inflicted acts or infection. For events like

heart attack, stroke and cancer, the cover will be excluded for the first 90 days.

II. Since its introduction in the late 1980s in Australia, trauma insurance has begun to grow

in terms of sales and popularity. The various policy structures available for a trauma

insurance are as follows:

It is available as an additional with a whole-of-life or an endowment policy. Any

payment for the trauma insurance was considered as an advancement of the total

benefit and the policy ended after the payment of the trauma benefit.

For a term life insurance policy, it was available as an additional rider benefit. In

this situation, the trauma benefit is considered as an advancement of benefit

payment. However, the policy ended only if the trauma benefit amount was the

same as the term benefit amount. Otherwise, the policy continued with an insured

benefit equal to the remaining death cover. Some policies also allow the

segregation of the trauma benefit from that of the death benefit in case of a term

life insurance policy. The option to buyback is also available. Here, the level of

the death benefit reduced by the trauma benefit is reinstated. This is done through

a right of the insured to reinstate the death benefit sum insured by making a

certain amount of predetermined payments after a predetermined period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INSURANCE

A separate policy for a standalone trauma insurance was introduced around 1995.

Here, the policy ends after the payment of the trauma benefit.

III. The trauma insurance pays a lump sum benefit if the life insured suffers from an illness

or accident whose definition is covered under the definition of an event in the policy.

Trauma insurance policies cover various events which are reviewed regularly by the

insurers and enhancements are made to the conditions covered by them. Some of the

events for which payment is made include heart attack, stroke, cancer, heart bypass

surgery, paralysis and major head trauma. For these events, full payments are made on

the basis of timing of the event. However, these events should occur naturally and not a

result of the deliberate act or doing of the person insured. In case of less serious events

like carcinoma in situ and partial blindness, the payments made tend to be partial in

nature. However, there are additional benefits which are of note. In case of diagnosis of

certain chronic and progressive events like multiple sclerosis and cardiomyopathy,

advance payments are made by the insurance provider. Similarly, an indexation facility

which increases the benefit amount every year in line with CPI is generally included to

ensure that the payments made keep up with the inflation in the market.

Answer to Question 4

a) Personal Sickness & Accident (PS&A) insurance products are issued by the general

insurers whereas life insurance companies tend to offer the trauma and critical illness

policies. Life insurance products can be taken up on an agreed basis. This means that the

policy will remain at the same level which it was at the time of taking out the policy.

However, PS&A insurance payments change on the basis of the change in income of the

insurer. Similarly, life insurance policies generally tend to pay out a policy only when

A separate policy for a standalone trauma insurance was introduced around 1995.

Here, the policy ends after the payment of the trauma benefit.

III. The trauma insurance pays a lump sum benefit if the life insured suffers from an illness

or accident whose definition is covered under the definition of an event in the policy.

Trauma insurance policies cover various events which are reviewed regularly by the

insurers and enhancements are made to the conditions covered by them. Some of the

events for which payment is made include heart attack, stroke, cancer, heart bypass

surgery, paralysis and major head trauma. For these events, full payments are made on

the basis of timing of the event. However, these events should occur naturally and not a

result of the deliberate act or doing of the person insured. In case of less serious events

like carcinoma in situ and partial blindness, the payments made tend to be partial in

nature. However, there are additional benefits which are of note. In case of diagnosis of

certain chronic and progressive events like multiple sclerosis and cardiomyopathy,

advance payments are made by the insurance provider. Similarly, an indexation facility

which increases the benefit amount every year in line with CPI is generally included to

ensure that the payments made keep up with the inflation in the market.

Answer to Question 4

a) Personal Sickness & Accident (PS&A) insurance products are issued by the general

insurers whereas life insurance companies tend to offer the trauma and critical illness

policies. Life insurance products can be taken up on an agreed basis. This means that the

policy will remain at the same level which it was at the time of taking out the policy.

However, PS&A insurance payments change on the basis of the change in income of the

insurer. Similarly, life insurance policies generally tend to pay out a policy only when

11INSURANCE

there is the death of an individual whereas PS&A policies pay lump sums only for deaths

resulting from an accident. In case of Trauma cover, a lump sum benefit is paid to the

insured if there is a diagnosis of a terminal illness like cancer, stroke or heart condition.

The aspect of a person being able to return to work remains irrelevant in case of a

Trauma Insurance. However, for a PS&A cover, the benefits are paid on a weekly or

monthly basis only when there is a loss of the income of the individual due to the illness.

PS&A products may choose to provide a cover of up to 100%. Income protection

products, however, have a cap of 75% of the income earned by the individual. The time

period with regards to PS&A products is also shorter. It is usually for a period of 1 or 2

years and not for the lifetime of an individual. Another key difference is that the insurer

can cancel the PS&A products whereas the life insurance products can only be cancelled

by the insured in most cases. In case of a change in occupation to a more risky

occupation, the insurer may choose to not renew the insurance policy of an individual.

However, a life insurance policy is continued to be paid as long as the premiums are paid

by the policy holder. Life insurance policies have a better suitability in the long run

whereas PS&A policies are advisable for the short and medium term (Driver et al. 2018).

As PS&A is a more simplified form of insurance, it does not require any medical

underwriting. Applicants whose claims were rejected in the past tend to have their claims

accepted in the PS&A products. The risk of the claim being rejected and the process

undertaken to complete the process of underwriting in a life insurance product like Total

and Permanent Disability (TPD) insurance is much higher. In case of PS&A products,

there are a wide number of exclusions including illnesses like HIV, AIDS and other

mental illnesses. Even though life insurance policies also have exclusions, they are not so

there is the death of an individual whereas PS&A policies pay lump sums only for deaths

resulting from an accident. In case of Trauma cover, a lump sum benefit is paid to the

insured if there is a diagnosis of a terminal illness like cancer, stroke or heart condition.

The aspect of a person being able to return to work remains irrelevant in case of a

Trauma Insurance. However, for a PS&A cover, the benefits are paid on a weekly or

monthly basis only when there is a loss of the income of the individual due to the illness.

PS&A products may choose to provide a cover of up to 100%. Income protection

products, however, have a cap of 75% of the income earned by the individual. The time

period with regards to PS&A products is also shorter. It is usually for a period of 1 or 2

years and not for the lifetime of an individual. Another key difference is that the insurer

can cancel the PS&A products whereas the life insurance products can only be cancelled

by the insured in most cases. In case of a change in occupation to a more risky

occupation, the insurer may choose to not renew the insurance policy of an individual.

However, a life insurance policy is continued to be paid as long as the premiums are paid

by the policy holder. Life insurance policies have a better suitability in the long run

whereas PS&A policies are advisable for the short and medium term (Driver et al. 2018).

As PS&A is a more simplified form of insurance, it does not require any medical

underwriting. Applicants whose claims were rejected in the past tend to have their claims

accepted in the PS&A products. The risk of the claim being rejected and the process

undertaken to complete the process of underwriting in a life insurance product like Total

and Permanent Disability (TPD) insurance is much higher. In case of PS&A products,

there are a wide number of exclusions including illnesses like HIV, AIDS and other

mental illnesses. Even though life insurance policies also have exclusions, they are not so

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.