ACCT20074 Contemporary Accounting Theory: Part A and B Report

VerifiedAdded on 2023/03/29

|20

|4030

|391

Report

AI Summary

This report provides a comprehensive analysis of contemporary accounting theory, specifically focusing on the conceptual framework for financial reporting. Part A delves into the history and development of the framework, examining its evolution in the USA, UK, Australia, and globally under the IASB. It also addresses the Australian accounting profession's concerns and academic critiques regarding the framework's quality, including its potential benefits and limitations. The report then analyzes how an Australian company, Iron Mountain Incorp, applies the conceptual framework in its financial statements, including the recognition principles and qualitative characteristics of the data presented. Part B links the International Integrated Reporting System with Sustainability Reporting Guidelines, assessing the strengths and weaknesses of accounting based on the conceptual framework. It also compares the framework's application in Iron Mountain Incorp with a South African company, Globe Trade Centre, based on integrated reporting practices. The report utilizes financial statements and academic research to support its analysis, providing a detailed overview of the conceptual framework's practical application and theoretical implications.

Running head: CONTEMPORARY ACCOUNTING THEORY 1

Contemporary Accounting Theory Part (A&B)

Students Name

Institution Affiliation

Date

Contemporary Accounting Theory Part (A&B)

Students Name

Institution Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 2

1. Executive Summary

The ideology behind the establishment of a conceptual framework (CF), in the sector of

accounting is built on the mandate to recognize key issues while studying financial statements.

This framework is made to enable the company to achieve and assess its financial health. Thus,

this paper critically asses the conceptual framework applied in an ASX listed company: Iron

Mountain Incorp and how the company relates this idea in the selecting of financial events,

concerns, and statements. In part B, the paper will link the International Integrated Reporting

System over the Sustainability Reporting Guidelines, which entails and explain the specific

strengths and limitations of accounting based on CF. The paper will compare the assessment of

the framework against a South African Country Globe Trade Centre on an index, Iron Mountain

Incorp against the company’s integrated reportage.

1. Executive Summary

The ideology behind the establishment of a conceptual framework (CF), in the sector of

accounting is built on the mandate to recognize key issues while studying financial statements.

This framework is made to enable the company to achieve and assess its financial health. Thus,

this paper critically asses the conceptual framework applied in an ASX listed company: Iron

Mountain Incorp and how the company relates this idea in the selecting of financial events,

concerns, and statements. In part B, the paper will link the International Integrated Reporting

System over the Sustainability Reporting Guidelines, which entails and explain the specific

strengths and limitations of accounting based on CF. The paper will compare the assessment of

the framework against a South African Country Globe Trade Centre on an index, Iron Mountain

Incorp against the company’s integrated reportage.

CONTEMPORARY ACCOUNTING THEORY 3

2. Introduction

The certification of the concept is expected to outlay critical financial guidelines that basically

control and underlie the steps to preparing and proposing a company’s financial statement and

economic assessment. In that regard, this financial information is applied by several key

investors in the company to effectively formulate the CF, appropriate for assessing the finances

of a company. Therefore, this paper assesses the concept evaluation of two companies: Iron

Mountain Incorp and the Globe Trade Centre, which are Australian and South African

companies respectively. It is also important to evaluate the IASB in expressing revised and

standardized accounting protocols, which is relevant for financial statement relevant by

companies when supplying financial procedures or handling problems evident in the compliance

activities to particular accounting standards. In that regard, this paper examines the conceptual

framework purposed for financial reporting and its relevance application in an Australian

company i.e. Iron Mountain Incorp. The following paper of this paper will assess the

sustainability and integrated writing framework applicable in South African Company i.e. Globe

Trade Centre.

Part A

a) Review of the history and development of the Conceptual Framework for Financial

Reporting

The Conceptual Framework (CF) improvement in the UK, US and other nations in the world

began in 1976, following its overview by the FASB in the US. The conceptual framework was

generated as a basic structure that crucially outlays accounting procedures, which cordially

sustains accounting reporting concerns. From 1978 to 2010, the governing entity had delivered

eight accounting statements concerning the relevant financial reports applied by various

2. Introduction

The certification of the concept is expected to outlay critical financial guidelines that basically

control and underlie the steps to preparing and proposing a company’s financial statement and

economic assessment. In that regard, this financial information is applied by several key

investors in the company to effectively formulate the CF, appropriate for assessing the finances

of a company. Therefore, this paper assesses the concept evaluation of two companies: Iron

Mountain Incorp and the Globe Trade Centre, which are Australian and South African

companies respectively. It is also important to evaluate the IASB in expressing revised and

standardized accounting protocols, which is relevant for financial statement relevant by

companies when supplying financial procedures or handling problems evident in the compliance

activities to particular accounting standards. In that regard, this paper examines the conceptual

framework purposed for financial reporting and its relevance application in an Australian

company i.e. Iron Mountain Incorp. The following paper of this paper will assess the

sustainability and integrated writing framework applicable in South African Company i.e. Globe

Trade Centre.

Part A

a) Review of the history and development of the Conceptual Framework for Financial

Reporting

The Conceptual Framework (CF) improvement in the UK, US and other nations in the world

began in 1976, following its overview by the FASB in the US. The conceptual framework was

generated as a basic structure that crucially outlays accounting procedures, which cordially

sustains accounting reporting concerns. From 1978 to 2010, the governing entity had delivered

eight accounting statements concerning the relevant financial reports applied by various

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 4

businesses, including one SFAC No. 4, which indicated the conceptual framework that applies to

non-business enterprises (Prosic, 2015). Moreover, SFACs No. 1, 2 and 3 have already been

changed, which leave only 5 as valid SFAC Nos. The reporting is SFAC No. 4, which symbolize

the conceptual framework considered by the International Accounting Standards Committee

(IASC). This accounting body was recognized in 1973, which characterized a predecessor unit of

the accounting standards body globally.

By 1st April 2010, the accounting unit (IASB) expected the role of IASC obliged to set out the

Conceptual framework, despite the existing standards being mention as the International

Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In 1975, the entity offered its

initial reporting of the IAS, which signified the accounting policy disclosure (Crombie, 2012).

The IASC offered its 28th IAS by April 1989, which represented the financial statements for

investment in the relevant associates. Therefore, the conceptual framework advanced for the

performance and preparation of accounting frameworks had been approved by April 1989 by the

IASC. This writing was therefore published in 1989 and applied by the IASB in 2001, despite its

relevance in expressing and unindustrialized the IAS framework.

For the purpose of late issuance of the standard, the essential purpose of the CF is to assist the

financial entity to formulate International Accounting Standards in the future; and permit the

review of the current Standards paragraphs (IASB, 2010b and B1713) suggesting this framework

(Ehoff, 2010). The accounting body dedicated itself into an agreement with the United States’

FASB, which was referred as the 2nd Norwalk Agreement by 2002; and instructing that two

accounting units would principally consider eliminating its present differences and join on the

basis of the quality conceptual framework (Ehoff, 2010). Succeeding the joint conference in

2004, the accounting bodies (FASB and IASB) decided to include particular key components and

businesses, including one SFAC No. 4, which indicated the conceptual framework that applies to

non-business enterprises (Prosic, 2015). Moreover, SFACs No. 1, 2 and 3 have already been

changed, which leave only 5 as valid SFAC Nos. The reporting is SFAC No. 4, which symbolize

the conceptual framework considered by the International Accounting Standards Committee

(IASC). This accounting body was recognized in 1973, which characterized a predecessor unit of

the accounting standards body globally.

By 1st April 2010, the accounting unit (IASB) expected the role of IASC obliged to set out the

Conceptual framework, despite the existing standards being mention as the International

Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In 1975, the entity offered its

initial reporting of the IAS, which signified the accounting policy disclosure (Crombie, 2012).

The IASC offered its 28th IAS by April 1989, which represented the financial statements for

investment in the relevant associates. Therefore, the conceptual framework advanced for the

performance and preparation of accounting frameworks had been approved by April 1989 by the

IASC. This writing was therefore published in 1989 and applied by the IASB in 2001, despite its

relevance in expressing and unindustrialized the IAS framework.

For the purpose of late issuance of the standard, the essential purpose of the CF is to assist the

financial entity to formulate International Accounting Standards in the future; and permit the

review of the current Standards paragraphs (IASB, 2010b and B1713) suggesting this framework

(Ehoff, 2010). The accounting body dedicated itself into an agreement with the United States’

FASB, which was referred as the 2nd Norwalk Agreement by 2002; and instructing that two

accounting units would principally consider eliminating its present differences and join on the

basis of the quality conceptual framework (Ehoff, 2010). Succeeding the joint conference in

2004, the accounting bodies (FASB and IASB) decided to include particular key components and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 5

concerns as an interlinked task to express a single Conceptual Framework. This initiative as

overseen and recognized based on the original FASB’s conceptual framework and the IASB’s

framework. All the two boards used the established framework as a basis of their accounting

standards for the CF.

b) Explanation of the Australian accounting profession's concerns regarding the

Conceptual Framework

The Quasi-legislation indicates that the requirement for the Constitution-centered CF in Australia

makes it nearly difficult to ensure that documented accounting frameworks are reliable and have

been formulated logically. Despite the fact that it is apparently convenient to assess the

fundamentals of accounting in the term ‘objectives’ of the significant accounting statements, the

occupations claim that the looseness of the standards in Australia has offered more possible

accounting problems. In that case, the Australian Accounting Profession is more worried about

the assessment of the CF tasks instead of its aims in the evaluation of the unit's financial

statements. This further suggests that the professions presently reject the reference and

intellectual lines of CF on the basis on accounting ’objectives’ in the evaluation of financial

statements. The main purpose for this is that the presence of the urged to create the underpinning

accounting frameworks falters short-term accounting aims.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential profits and restrictions to consider as an academic alarm. Therefore, here

are the profits evident following the overview of the framework in the accounting industry. Since

many countries have recognized CF, which is similar globally, there is a need for nations to

concerns as an interlinked task to express a single Conceptual Framework. This initiative as

overseen and recognized based on the original FASB’s conceptual framework and the IASB’s

framework. All the two boards used the established framework as a basis of their accounting

standards for the CF.

b) Explanation of the Australian accounting profession's concerns regarding the

Conceptual Framework

The Quasi-legislation indicates that the requirement for the Constitution-centered CF in Australia

makes it nearly difficult to ensure that documented accounting frameworks are reliable and have

been formulated logically. Despite the fact that it is apparently convenient to assess the

fundamentals of accounting in the term ‘objectives’ of the significant accounting statements, the

occupations claim that the looseness of the standards in Australia has offered more possible

accounting problems. In that case, the Australian Accounting Profession is more worried about

the assessment of the CF tasks instead of its aims in the evaluation of the unit's financial

statements. This further suggests that the professions presently reject the reference and

intellectual lines of CF on the basis on accounting ’objectives’ in the evaluation of financial

statements. The main purpose for this is that the presence of the urged to create the underpinning

accounting frameworks falters short-term accounting aims.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential profits and restrictions to consider as an academic alarm. Therefore, here

are the profits evident following the overview of the framework in the accounting industry. Since

many countries have recognized CF, which is similar globally, there is a need for nations to

CONTEMPORARY ACCOUNTING THEORY 6

embrace considerable global compatibility on the basis of several accounting standards (Prosic,

2015). In that case, academic’s concern on excellence features on the standard’s comparability

and uniformity over the global financial reporting (whereby professions argue that it is relevant

for the assessment of foreign asset capitals and flows.

Academics are concerned with accounting logic and uniformity, which implies that

accounting standards recognized following the request of CF should be logical and

reliable.

CF provides the global fundamentals of accounting systems. Therefore, the standard-

setters are anticipated to be accountable for all their financial choices (Romolini, Fissi &

Gori, 2017). In case these choices are recovered from key concerns evaluated in the CF,

the accounting professions expect the standards to be clear thereby necessitating more

clarification prior to the application.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the

best guidance for entities to reports on particular accounting standards and evaluation of

any financial concern (Crombie, 2012).

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

Conceptual frameworks are outrageous to formulate.

The enhancement of the CF is affected by governmental actions. With this, some

accountants present the concern that CFS is more inclined to political procedures.

embrace considerable global compatibility on the basis of several accounting standards (Prosic,

2015). In that case, academic’s concern on excellence features on the standard’s comparability

and uniformity over the global financial reporting (whereby professions argue that it is relevant

for the assessment of foreign asset capitals and flows.

Academics are concerned with accounting logic and uniformity, which implies that

accounting standards recognized following the request of CF should be logical and

reliable.

CF provides the global fundamentals of accounting systems. Therefore, the standard-

setters are anticipated to be accountable for all their financial choices (Romolini, Fissi &

Gori, 2017). In case these choices are recovered from key concerns evaluated in the CF,

the accounting professions expect the standards to be clear thereby necessitating more

clarification prior to the application.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the

best guidance for entities to reports on particular accounting standards and evaluation of

any financial concern (Crombie, 2012).

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

Conceptual frameworks are outrageous to formulate.

The enhancement of the CF is affected by governmental actions. With this, some

accountants present the concern that CFS is more inclined to political procedures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 7

Linked to the limitation outlined above, whenever the CF considers involving accounting

concerns, there is always an issue of financial estimation of given assets as argued by

(Molyneux & Wilson, 2017).

The CFs considers more on financial-related matters. In that case, this framework will consider

disregarding several execution segments such as ecological and social revealing components.

Moreover, through the assessment of financial execution, CFs critically transits the consideration

of financial analysts based on corporate execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) Statements that have been organized as per the Conceptual Framework and their key

components

Linked to the limitation outlined above, whenever the CF considers involving accounting

concerns, there is always an issue of financial estimation of given assets as argued by

(Molyneux & Wilson, 2017).

The CFs considers more on financial-related matters. In that case, this framework will consider

disregarding several execution segments such as ecological and social revealing components.

Moreover, through the assessment of financial execution, CFs critically transits the consideration

of financial analysts based on corporate execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) Statements that have been organized as per the Conceptual Framework and their key

components

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

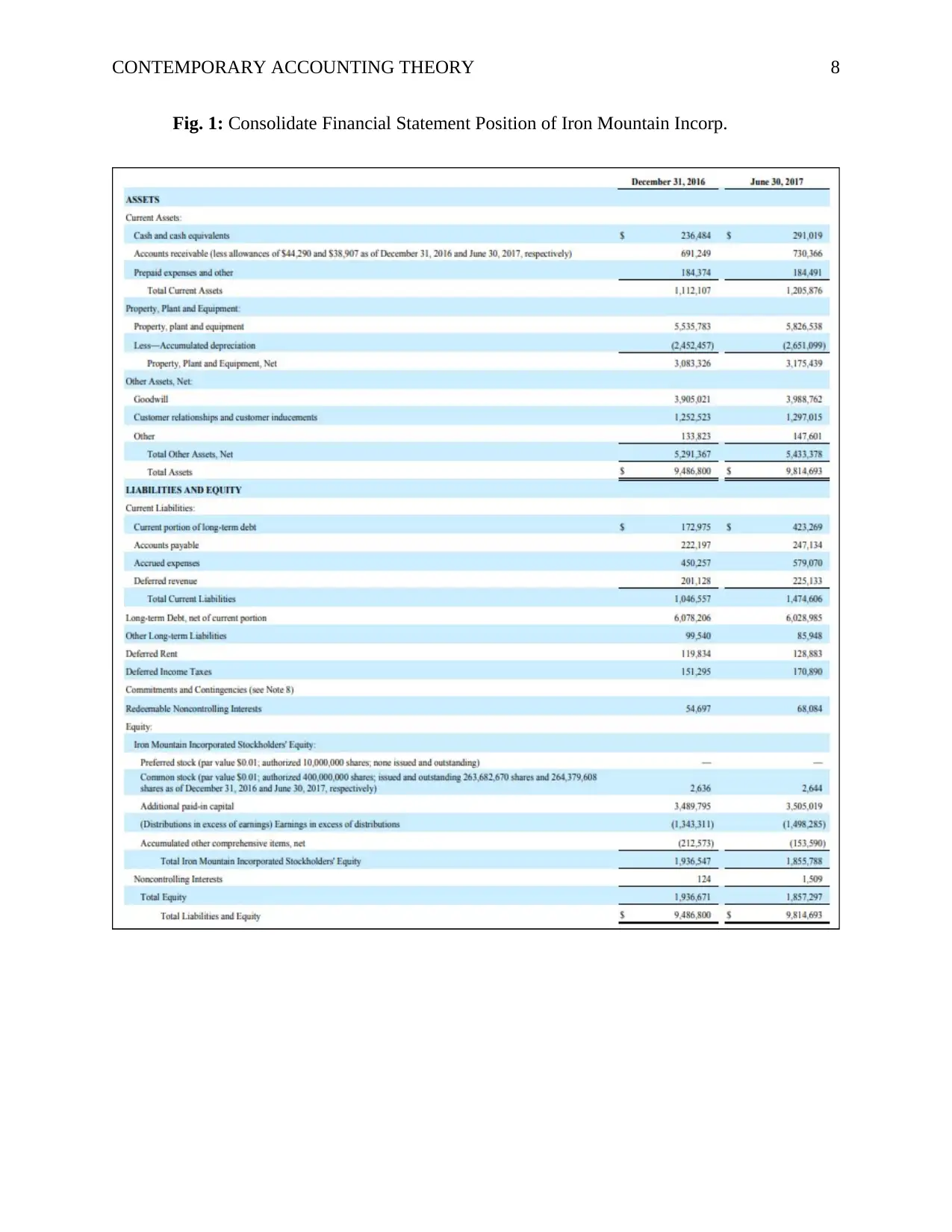

Fig. 1: Consolidate Financial Statement Position of Iron Mountain Incorp.

Fig. 1: Consolidate Financial Statement Position of Iron Mountain Incorp.

CONTEMPORARY ACCOUNTING THEORY 9

According to Fig. 1 above, the company has organized its financial information considering the

company’s consolidated financial statements components, which include the assets, liabilities

and revenue.

The company has created 20 reports having key components evident in all. The components

comprise:

The reasons for accounting reporting: FASB's first Notice of financial and Accounting

Ideas (SFAC 1) (1978) distinguished the wide purposes of accounting evaluation. The

first broad goal expressed in SFAC 1 is to give information that is supportive to present

and potential investors and different customers in making the stable venture, credit, and

comparable choices. From this beginning point in SFAC 1, the Iron Mountain In carp

communicated other gradually explicit targets. The Fundamental of Useful Financial

Data: The second element in the conceptual framework is the subjective attribute that

financial information ought to have in the event that it is to be valuable in basic

governance. In SFAC 2, the FASB said that information is helpful on the off chance that

it is (I) essential, (ii) reliable, and (iii) tantamount (Carnevale & Mazzuca, 2012). Data is

relevant on the off chance that it can have any kind of effect in a choice. The information

has this quality when it enables customers to expect the future or evaluate the past and is

acquired so as to influence their choices.

Financial Statement Elements: Another important improvement in constructing up a

conceptual framework is to choose the components of budget reports. This includes

distinguishing the classes of Iron Mountain Incorp information that ought to be included

in monetary reports. FASB's exchange of fiscal summary components integrates

According to Fig. 1 above, the company has organized its financial information considering the

company’s consolidated financial statements components, which include the assets, liabilities

and revenue.

The company has created 20 reports having key components evident in all. The components

comprise:

The reasons for accounting reporting: FASB's first Notice of financial and Accounting

Ideas (SFAC 1) (1978) distinguished the wide purposes of accounting evaluation. The

first broad goal expressed in SFAC 1 is to give information that is supportive to present

and potential investors and different customers in making the stable venture, credit, and

comparable choices. From this beginning point in SFAC 1, the Iron Mountain In carp

communicated other gradually explicit targets. The Fundamental of Useful Financial

Data: The second element in the conceptual framework is the subjective attribute that

financial information ought to have in the event that it is to be valuable in basic

governance. In SFAC 2, the FASB said that information is helpful on the off chance that

it is (I) essential, (ii) reliable, and (iii) tantamount (Carnevale & Mazzuca, 2012). Data is

relevant on the off chance that it can have any kind of effect in a choice. The information

has this quality when it enables customers to expect the future or evaluate the past and is

acquired so as to influence their choices.

Financial Statement Elements: Another important improvement in constructing up a

conceptual framework is to choose the components of budget reports. This includes

distinguishing the classes of Iron Mountain Incorp information that ought to be included

in monetary reports. FASB's exchange of fiscal summary components integrates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 10

meanings of important components, for example, resources, liabilities, value, incomes,

costs, additions, and misfortunes (Crombie, 2012).

Financial Quantity and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for selecting (1) when

things ought to be perceived in the budget abstracts, and (2) how to measure numbers to

financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

The recognition principle and measurement for assets, liabilities and revenue is based on a

criterion that focusses on recognizing if the benefits of sale or sure are likely (Hodge, Rajgopal

& Shevlin, 2009). For assets, businesses should ensure that financial data can be measured

quantitatively. For instance, the management could evaluate the manner in which individuals

place value on a subjective matter like dedicative employee and customer loyalty. For liabilities,

businesses should be able to satisfy the appropriate definition of liability, which focusses on

resources outflow symbolizing the company’s financial benefits, including the revenues, from

the company, which are probable. The second recognition principles for liabilities include the

valuation of obligations, which can be evaluated reliably. According to Timbate & Park (2018),

it is coherent to recognize liabilities when it is crucial for the company, especially if it required

doing so. The recognition of revenue should be based on an evaluation of obligation that accord

to the definition of financial sustainability.

(iii) Qualitative characteristics of data displayed in various company's several fiscal reports

Qualitative characteristics of data shown by the company’s fiscal reports include:

meanings of important components, for example, resources, liabilities, value, incomes,

costs, additions, and misfortunes (Crombie, 2012).

Financial Quantity and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for selecting (1) when

things ought to be perceived in the budget abstracts, and (2) how to measure numbers to

financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

The recognition principle and measurement for assets, liabilities and revenue is based on a

criterion that focusses on recognizing if the benefits of sale or sure are likely (Hodge, Rajgopal

& Shevlin, 2009). For assets, businesses should ensure that financial data can be measured

quantitatively. For instance, the management could evaluate the manner in which individuals

place value on a subjective matter like dedicative employee and customer loyalty. For liabilities,

businesses should be able to satisfy the appropriate definition of liability, which focusses on

resources outflow symbolizing the company’s financial benefits, including the revenues, from

the company, which are probable. The second recognition principles for liabilities include the

valuation of obligations, which can be evaluated reliably. According to Timbate & Park (2018),

it is coherent to recognize liabilities when it is crucial for the company, especially if it required

doing so. The recognition of revenue should be based on an evaluation of obligation that accord

to the definition of financial sustainability.

(iii) Qualitative characteristics of data displayed in various company's several fiscal reports

Qualitative characteristics of data shown by the company’s fiscal reports include:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 11

Operationalization of the subjective attributes: To build an estimation apparatus, Recent writing

is used which characterizes finance related describing poor quality as far as the upgrading

subjective attributes are most important and decide the substance of finance connected specifying

information (Alfiero, Cane, Doronzo & Esposito, 2018).

Importance: ‘Significance’ feature of the company refers to its capability to comprehend

various concerns raised by clients as suppliers of capital in the company. Since the previous

literature, the significance of operationalized applying various accounting components denotes

corroborative and prescient framework. As discussed earlier in this paper, accountants will

critically assess the value of economic gains instead of the accounting reporting and its value.

This feature is controlled due to the fact that it ignores non-financial data and future financial-

connected data that are available by investors (Mostyn, 2012). In order to improve the quality,

extensive and prescient analysis of the Iron Mountain Incorp financial statement is needed.

Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Sustainability and international integrated reporting frameworks are applicable in the enterprise

world today (Pérez-López, Moreno-Romero, & Barkemeyer, 2013). The role of businesses in

society today is gradually improving, as compared its initial responsibility of assessing its

productivity or recording its finances. The Sustainability Reporting Guideline presents the

significant standards applicable to the help businesses to enhance competitive benefit

(Ceulemans, Lozano & Alonso-Almeida, 2015). In addition, the component of environmental

sustainability in the instruction is critically suggested for firms to apply the world today.

Operationalization of the subjective attributes: To build an estimation apparatus, Recent writing

is used which characterizes finance related describing poor quality as far as the upgrading

subjective attributes are most important and decide the substance of finance connected specifying

information (Alfiero, Cane, Doronzo & Esposito, 2018).

Importance: ‘Significance’ feature of the company refers to its capability to comprehend

various concerns raised by clients as suppliers of capital in the company. Since the previous

literature, the significance of operationalized applying various accounting components denotes

corroborative and prescient framework. As discussed earlier in this paper, accountants will

critically assess the value of economic gains instead of the accounting reporting and its value.

This feature is controlled due to the fact that it ignores non-financial data and future financial-

connected data that are available by investors (Mostyn, 2012). In order to improve the quality,

extensive and prescient analysis of the Iron Mountain Incorp financial statement is needed.

Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Sustainability and international integrated reporting frameworks are applicable in the enterprise

world today (Pérez-López, Moreno-Romero, & Barkemeyer, 2013). The role of businesses in

society today is gradually improving, as compared its initial responsibility of assessing its

productivity or recording its finances. The Sustainability Reporting Guideline presents the

significant standards applicable to the help businesses to enhance competitive benefit

(Ceulemans, Lozano & Alonso-Almeida, 2015). In addition, the component of environmental

sustainability in the instruction is critically suggested for firms to apply the world today.

CONTEMPORARY ACCOUNTING THEORY 12

However, this form of reporting focusses more on a particular segment of the entity’s status but

unable to show the specific and significant climatic transitions and environmental factors

(Crombie, 2012). Apart from that sustainability reports do not effectively indicate financial

information relevant for evaluating the opportunities and risks of an entity.

International Integrated Reporting Framework progresses the corporation’s reputation; thus, the

productivity of the company can be assessed based on global customs and laws (Messner, 2010).

The reporting necessitates stakeholders to make the relationship with both the accounting and

non-accounting information analysts to be able to successfully assess possible dangers. Various

companies have actively begun to get readily integrated reports in different arrangements and

each report has been designed as per the requirements of business possessions. Moreover,

integrated announcing standards and rules have been dispersed by the Worldwide Integrated

Detailing Board, so as to provide a way to report assessors (Soyka, 2013). With the enlarging

relevant and spread of integrated detailing, banters about the benefits and issues experienced in

the readiness expanded. In this research, the followings are clarified: the terms of monetary

announcing, sustainability analysis, and accounting detailing; the growth of these terms; benefits

of integrated revealing and issues that might be experienced while readiness; and the connection

between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strengths

The conservative accounting, centered on the CF gives a firm foundation for formulating future

financial statement standards, which improve the sustainability status of exact companies

However, this form of reporting focusses more on a particular segment of the entity’s status but

unable to show the specific and significant climatic transitions and environmental factors

(Crombie, 2012). Apart from that sustainability reports do not effectively indicate financial

information relevant for evaluating the opportunities and risks of an entity.

International Integrated Reporting Framework progresses the corporation’s reputation; thus, the

productivity of the company can be assessed based on global customs and laws (Messner, 2010).

The reporting necessitates stakeholders to make the relationship with both the accounting and

non-accounting information analysts to be able to successfully assess possible dangers. Various

companies have actively begun to get readily integrated reports in different arrangements and

each report has been designed as per the requirements of business possessions. Moreover,

integrated announcing standards and rules have been dispersed by the Worldwide Integrated

Detailing Board, so as to provide a way to report assessors (Soyka, 2013). With the enlarging

relevant and spread of integrated detailing, banters about the benefits and issues experienced in

the readiness expanded. In this research, the followings are clarified: the terms of monetary

announcing, sustainability analysis, and accounting detailing; the growth of these terms; benefits

of integrated revealing and issues that might be experienced while readiness; and the connection

between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated reports

Strengths

The conservative accounting, centered on the CF gives a firm foundation for formulating future

financial statement standards, which improve the sustainability status of exact companies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.