Contemporary Issues in Accounting: McMillan Shakespeare Analysis

VerifiedAdded on 2023/01/18

|19

|2542

|35

Report

AI Summary

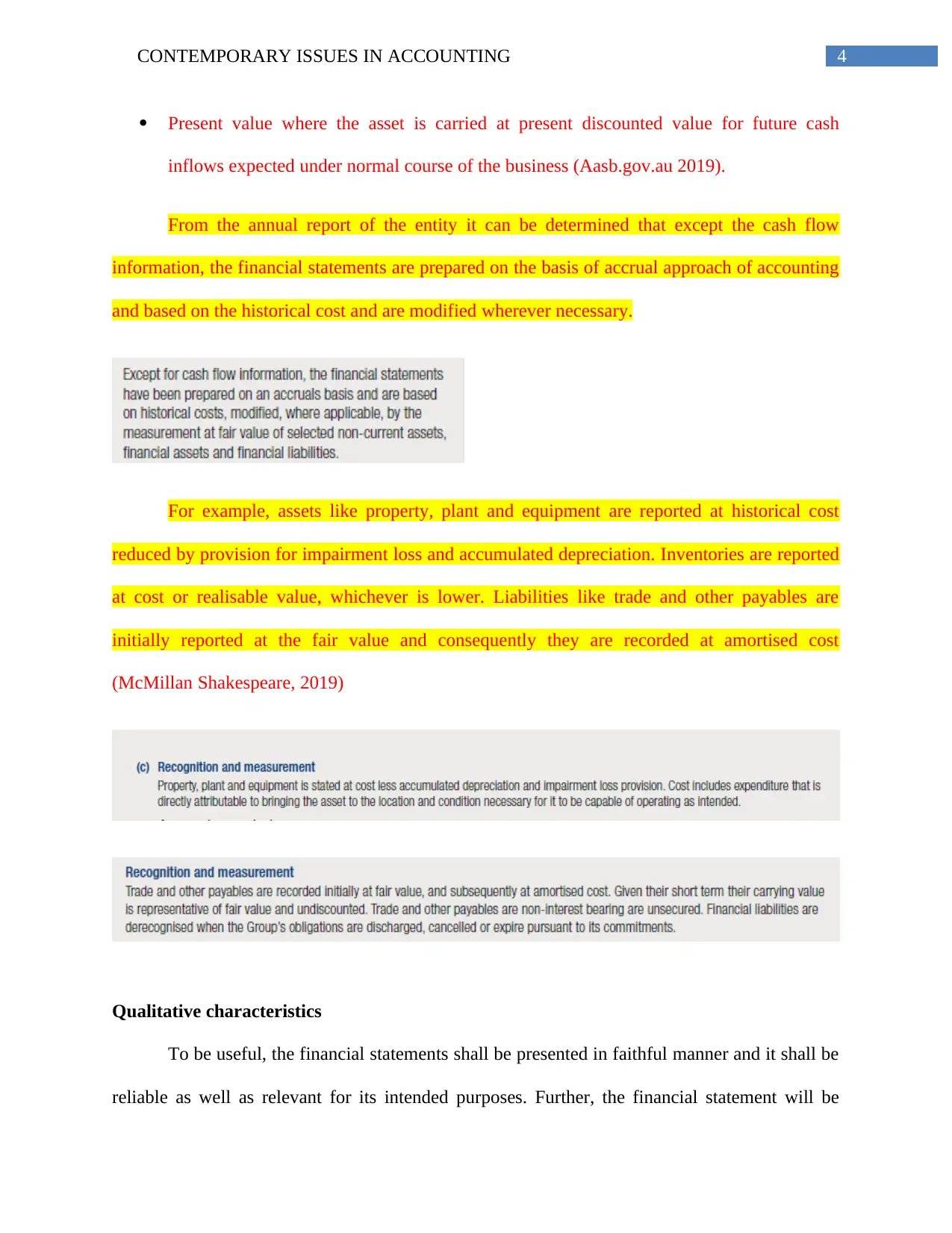

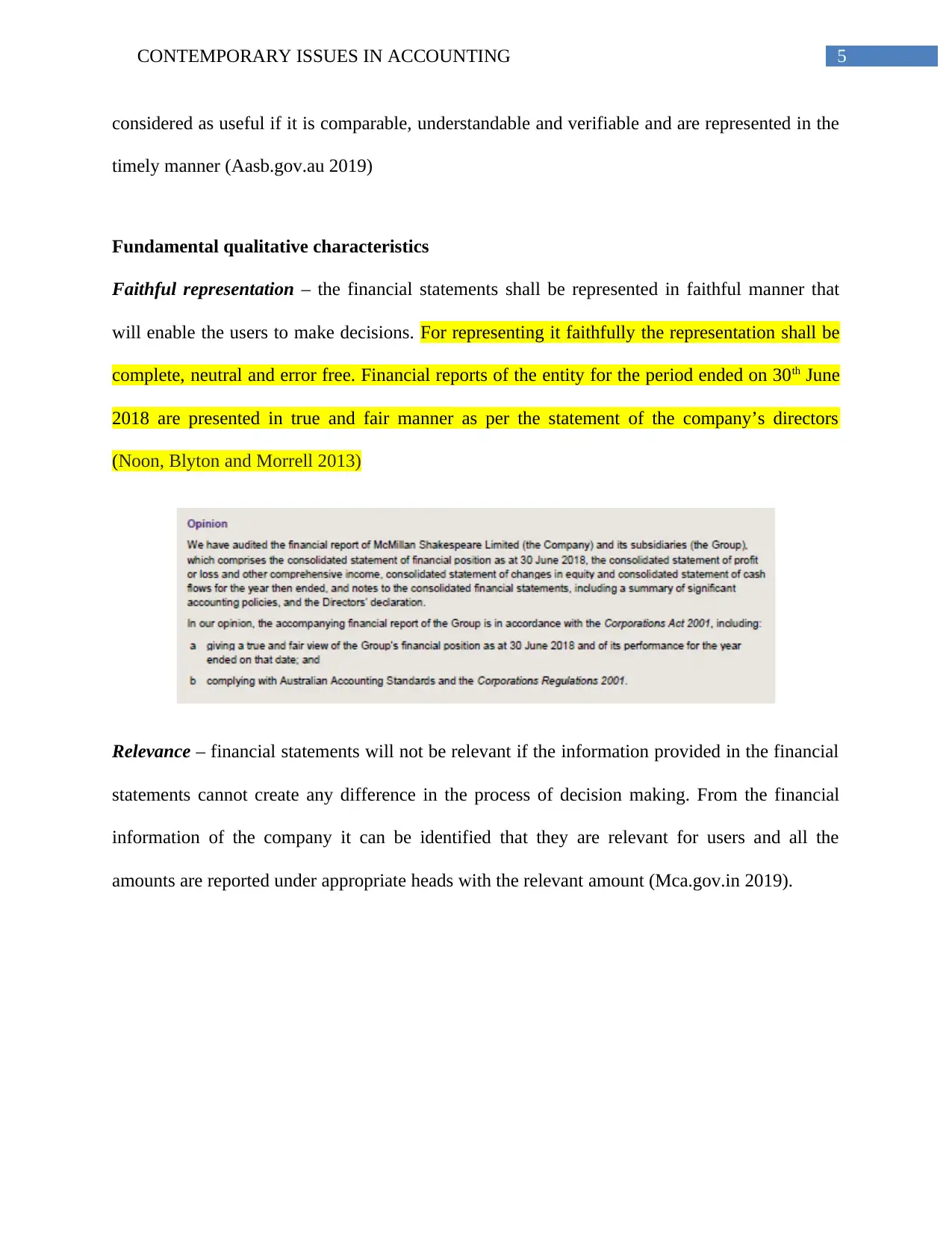

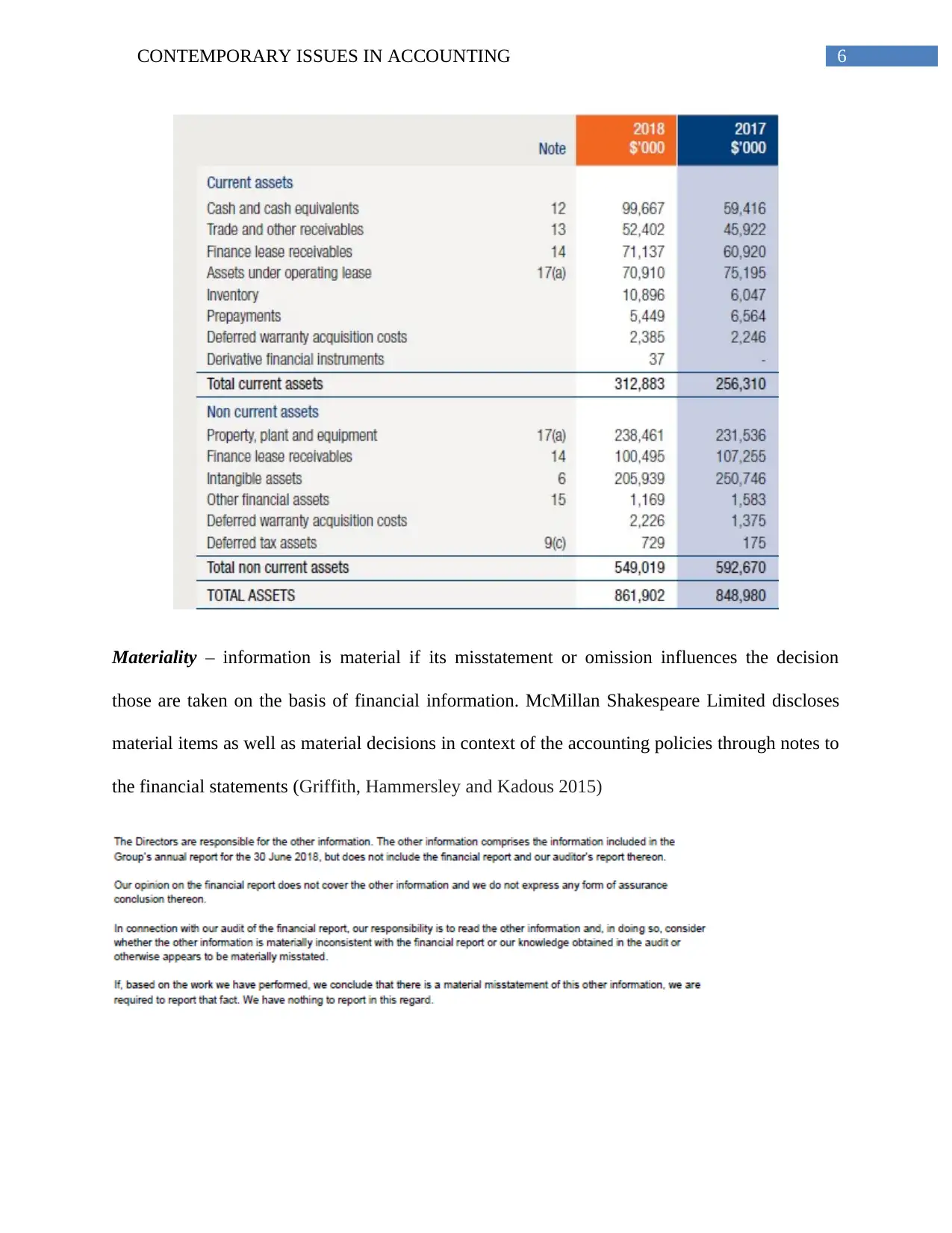

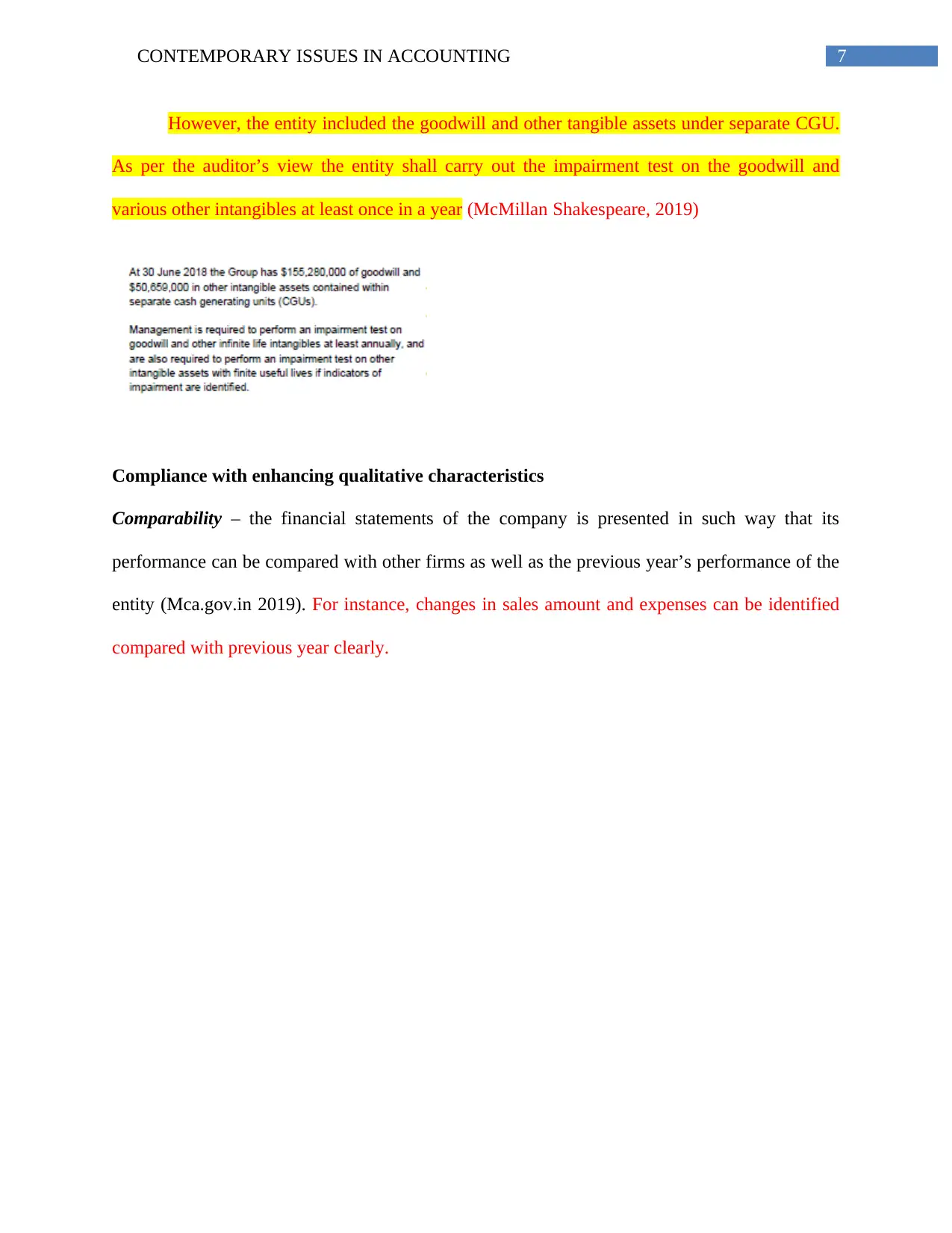

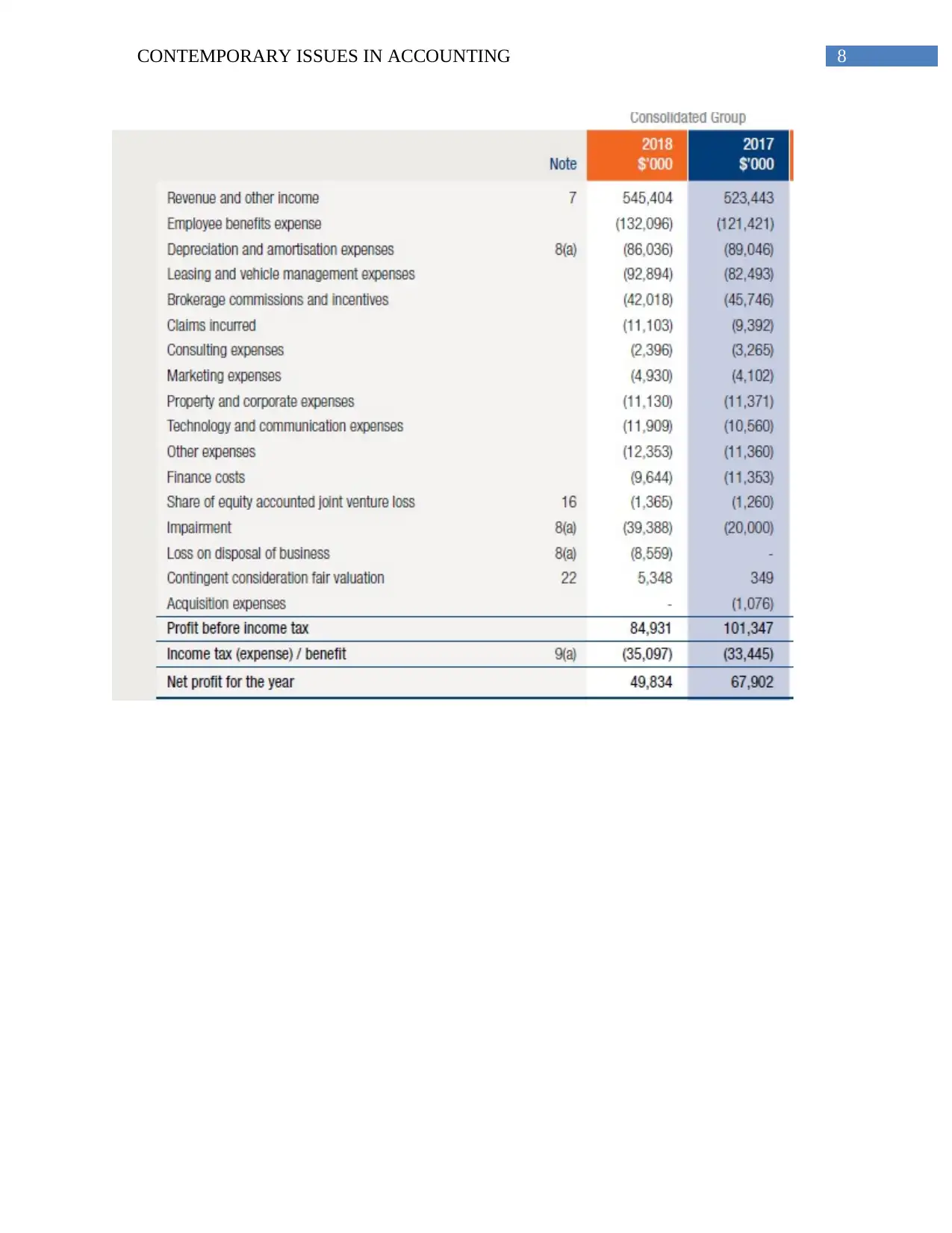

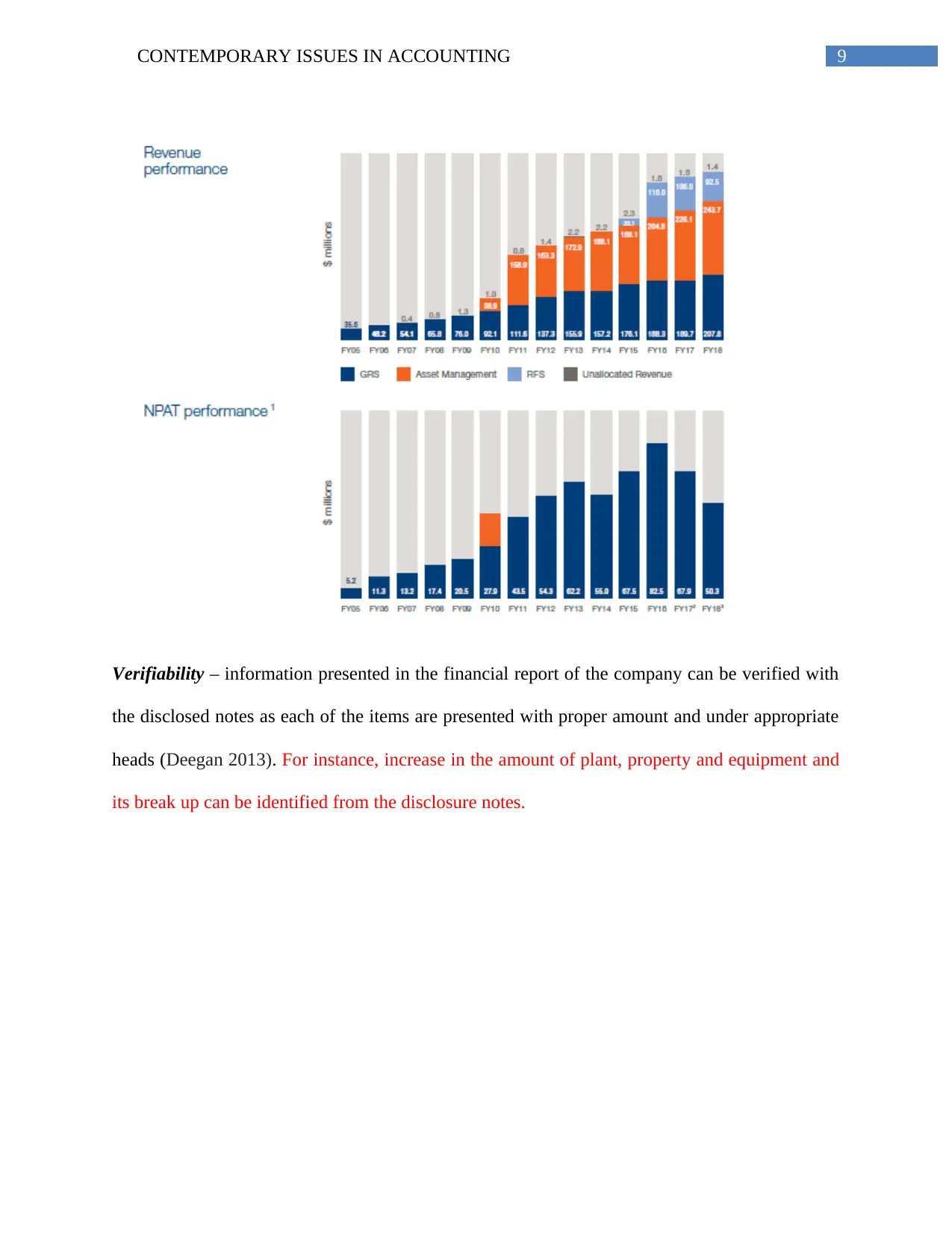

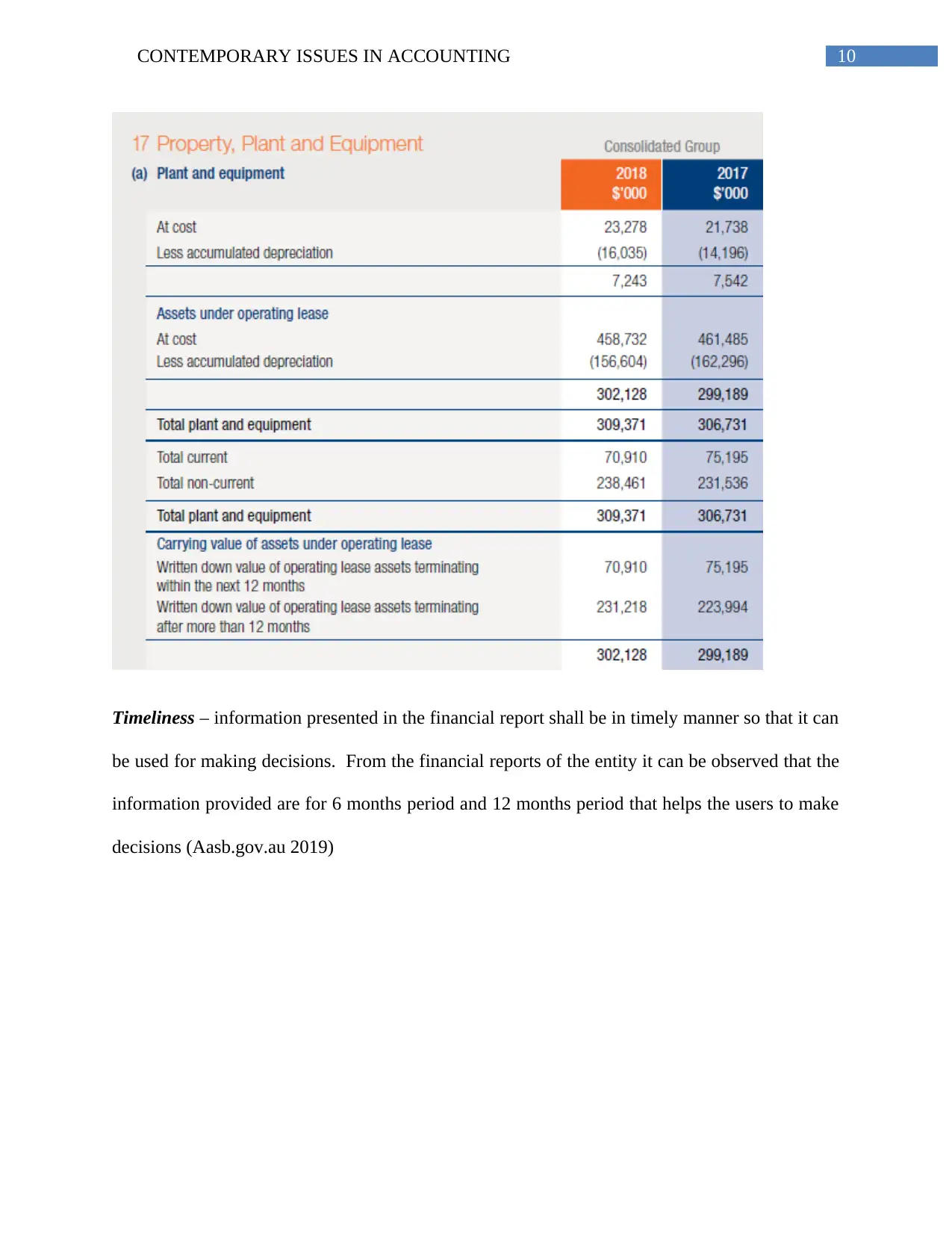

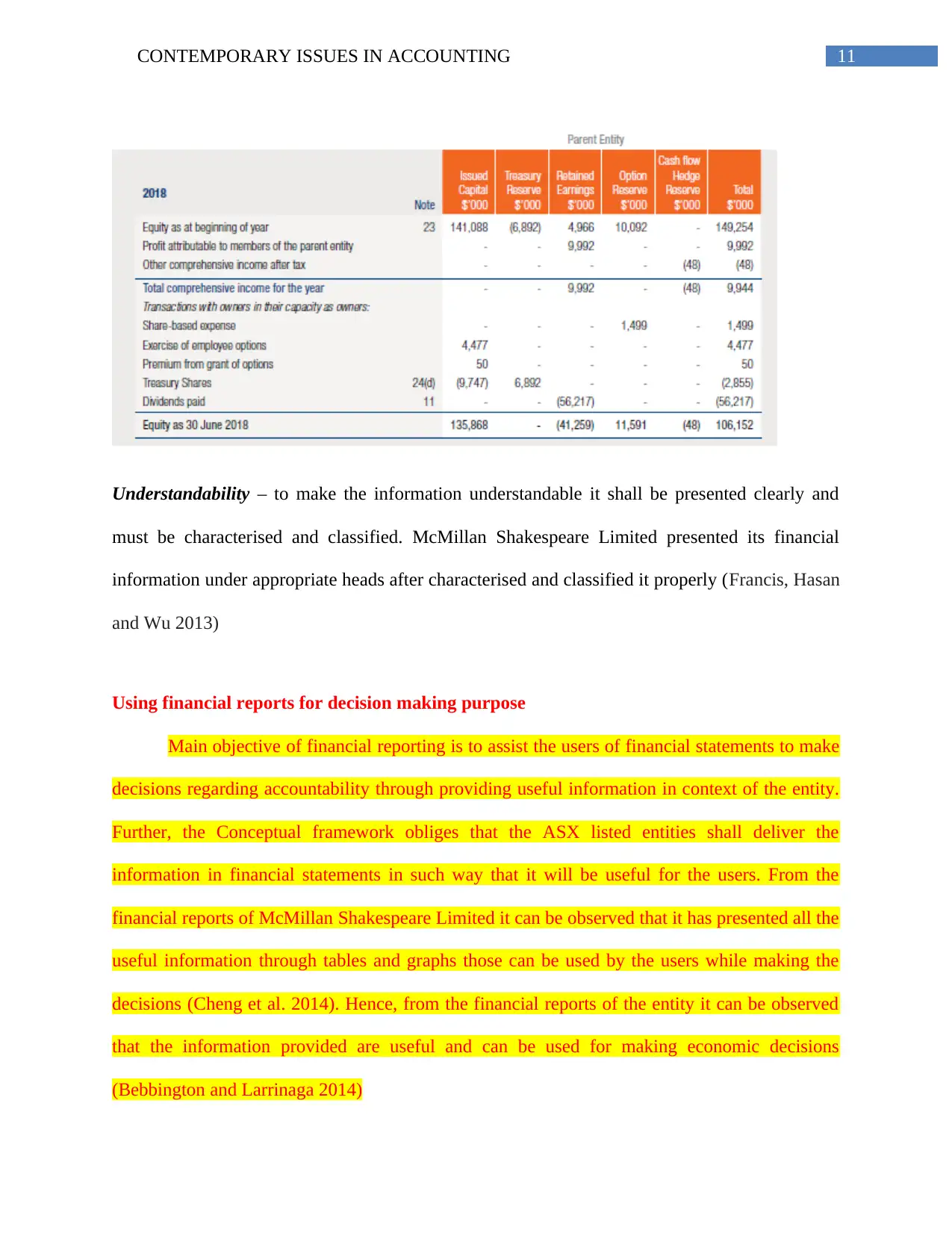

This report analyzes the financial statements of McMillan Shakespeare Limited to determine compliance with the conceptual framework. It examines the presentation of financial statements, focusing on recognition criteria and qualitative characteristics. The report identifies that the financial report is a general purpose financial report prepared according to AAS, Corporation Act 2001, and AASB interpretations. It concludes that McMillan Shakespeare Limited complies with all the objectives of the conceptual framework in the context of GPFR. The analysis covers the elements of financial statements like assets, liabilities, equity, expenses, and revenues, their recognition and measurement as per the conceptual framework. The report also emphasizes the company's adherence to the qualitative characteristics of the framework, including faithfulness, relevance, comparability, understandability, and timeliness, and their importance in decision-making. The report highlights that the company discloses material items and decisions in its financial statements, ensuring that the information provided is useful for making economic decisions.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.