Contemporary Issues in Accounting: A Report on Ausdrill Ltd

VerifiedAdded on 2023/01/23

|13

|2130

|52

Report

AI Summary

This report provides a comprehensive analysis of contemporary accounting issues within Ausdrill Ltd, an Australian mining company. It examines the company's financial reporting framework, focusing on the objectives of the conceptual framework and its application in preparing financial statements. The report delves into the recognition criteria for assets, liabilities, income, expenses, and equity, alongside an assessment of fundamental and enhancing qualitative characteristics such as relevance, faithful representation, comparability, verifiability, timeliness, and understandability. The analysis is grounded in the Australian Accounting Standards Board (AASB) standards. The report concludes with recommendations for Ausdrill Ltd to enhance the clarity and comprehensiveness of its financial disclosures, addressing areas such as employee benefits, special treatments, and joint ventures. The study aims to provide a detailed understanding of the financial reporting practices and their implications for stakeholders.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The assessment focuses on critically analysing the reporting framework which is used by the

considered company which has its primary operations in Australia. The chosen company for this

assessment is Ausdrill Ltd which has its mining operations in Australia. The report would be

focusing on different components which are included in the financial reports which is prepared

so as to ensure that the same is consistent with the generally accepted framework of reporting.

The reporting and recognising criteria for the business would be given focus in the assessment.

The report would be ending with recommendations for the business.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The assessment focuses on critically analysing the reporting framework which is used by the

considered company which has its primary operations in Australia. The chosen company for this

assessment is Ausdrill Ltd which has its mining operations in Australia. The report would be

focusing on different components which are included in the financial reports which is prepared

so as to ensure that the same is consistent with the generally accepted framework of reporting.

The reporting and recognising criteria for the business would be given focus in the assessment.

The report would be ending with recommendations for the business.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of Conceptual Framework.........................................................................................3

Recognition Criteria.....................................................................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................8

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................11

Introduction

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of Conceptual Framework.........................................................................................3

Recognition Criteria.....................................................................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................8

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................11

Introduction

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

The idea of conceptual framework relates to a guideline which needs to be followed by

every finance expert who are users or are engaged in preparation of the financial statements. The

conceptual framework was introduced so that a level of consistency can be brought about in

accounting practices around the world. The most logical application of the framework is to

prepare the financial statement in a manner which can be easily understood by the users

providing them with accurate information and the same can also be consistent with accounting

practices around the world (Cheng et al. 2014). This framework is supported by accounting

standards, principles, conventions and rules which needs to be followed by entities for

formulating the financial statements (Wang 2014).

The company which is considered for the assessment is Ausdrill Ltd which is considered

to be a important company in the mining sector operating in Australia. In a more specific

analysis, it can be said that the core activities of the company include integrated mining activities

and energy services. The operations of the company is widespread and is currently known to

have operations in 10 countries with more than 4000 employees working for the company

(Ausdrill.com.au. 2019). The company is further looking for more expansion opportunities.

Discussions

Objectives of Conceptual Framework

The objectives of Conceptual framework which can be identified from the perspective of

accounting and also business is listed below in details:

The conceptual framework acts a guide to not only the management of the company

while preparing the financial statements but also for the users of the financial statements

so that they can understand all relevant information which is prepared in the annual

report. The conceptual framework guides companies to provide appropriate disclosures

CONTEMPORARY ISSUES IN ACCOUNTING

The idea of conceptual framework relates to a guideline which needs to be followed by

every finance expert who are users or are engaged in preparation of the financial statements. The

conceptual framework was introduced so that a level of consistency can be brought about in

accounting practices around the world. The most logical application of the framework is to

prepare the financial statement in a manner which can be easily understood by the users

providing them with accurate information and the same can also be consistent with accounting

practices around the world (Cheng et al. 2014). This framework is supported by accounting

standards, principles, conventions and rules which needs to be followed by entities for

formulating the financial statements (Wang 2014).

The company which is considered for the assessment is Ausdrill Ltd which is considered

to be a important company in the mining sector operating in Australia. In a more specific

analysis, it can be said that the core activities of the company include integrated mining activities

and energy services. The operations of the company is widespread and is currently known to

have operations in 10 countries with more than 4000 employees working for the company

(Ausdrill.com.au. 2019). The company is further looking for more expansion opportunities.

Discussions

Objectives of Conceptual Framework

The objectives of Conceptual framework which can be identified from the perspective of

accounting and also business is listed below in details:

The conceptual framework acts a guide to not only the management of the company

while preparing the financial statements but also for the users of the financial statements

so that they can understand all relevant information which is prepared in the annual

report. The conceptual framework guides companies to provide appropriate disclosures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

and ensure a level of simplicity is maintained. The purpose behind maintaining simplicity

and focusing on disclosure is to ensure that even a non-user can easily depict the financial

performance of the business for the period. In the case of Ausdrill Ltd, the company is

listed in ASX which means that the company is likely to follow all rules and regulations

relating to accounting and its disclosures (Henderson et al. 2015). The financial

statements are prepared using a format which is widely used by companies around the

world for reporting.

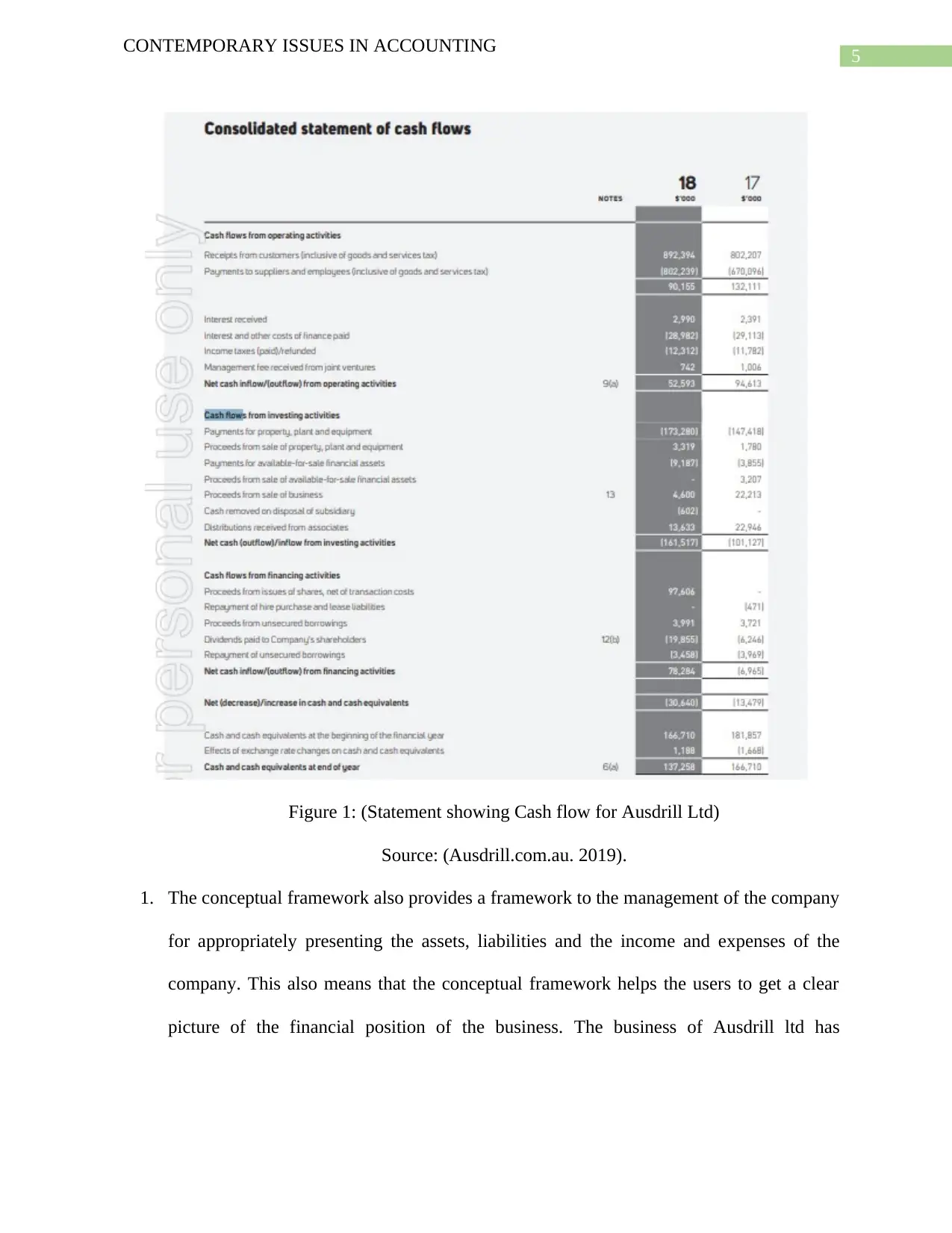

Another objective which can be identified in respect of conceptual framework is to

identify the cash flow situation of the business. The reporting for the cash flows also

requires appropriate identification of the source from where the cash inflows are

generated. Considering the annual report of Ausdrill ltd, the management of the company

has effectively reported the cash inflows for the business as well as the cash outflows

which is related to the business. The annual report of the company shows that the

business has divested a diamond business and also sold certain plant and machinery from

the business which totaled $ 3.3 million. This shows that the cash flow statement which is

prepared by the management is showing all the relevant details regarding the business.

CONTEMPORARY ISSUES IN ACCOUNTING

and ensure a level of simplicity is maintained. The purpose behind maintaining simplicity

and focusing on disclosure is to ensure that even a non-user can easily depict the financial

performance of the business for the period. In the case of Ausdrill Ltd, the company is

listed in ASX which means that the company is likely to follow all rules and regulations

relating to accounting and its disclosures (Henderson et al. 2015). The financial

statements are prepared using a format which is widely used by companies around the

world for reporting.

Another objective which can be identified in respect of conceptual framework is to

identify the cash flow situation of the business. The reporting for the cash flows also

requires appropriate identification of the source from where the cash inflows are

generated. Considering the annual report of Ausdrill ltd, the management of the company

has effectively reported the cash inflows for the business as well as the cash outflows

which is related to the business. The annual report of the company shows that the

business has divested a diamond business and also sold certain plant and machinery from

the business which totaled $ 3.3 million. This shows that the cash flow statement which is

prepared by the management is showing all the relevant details regarding the business.

5

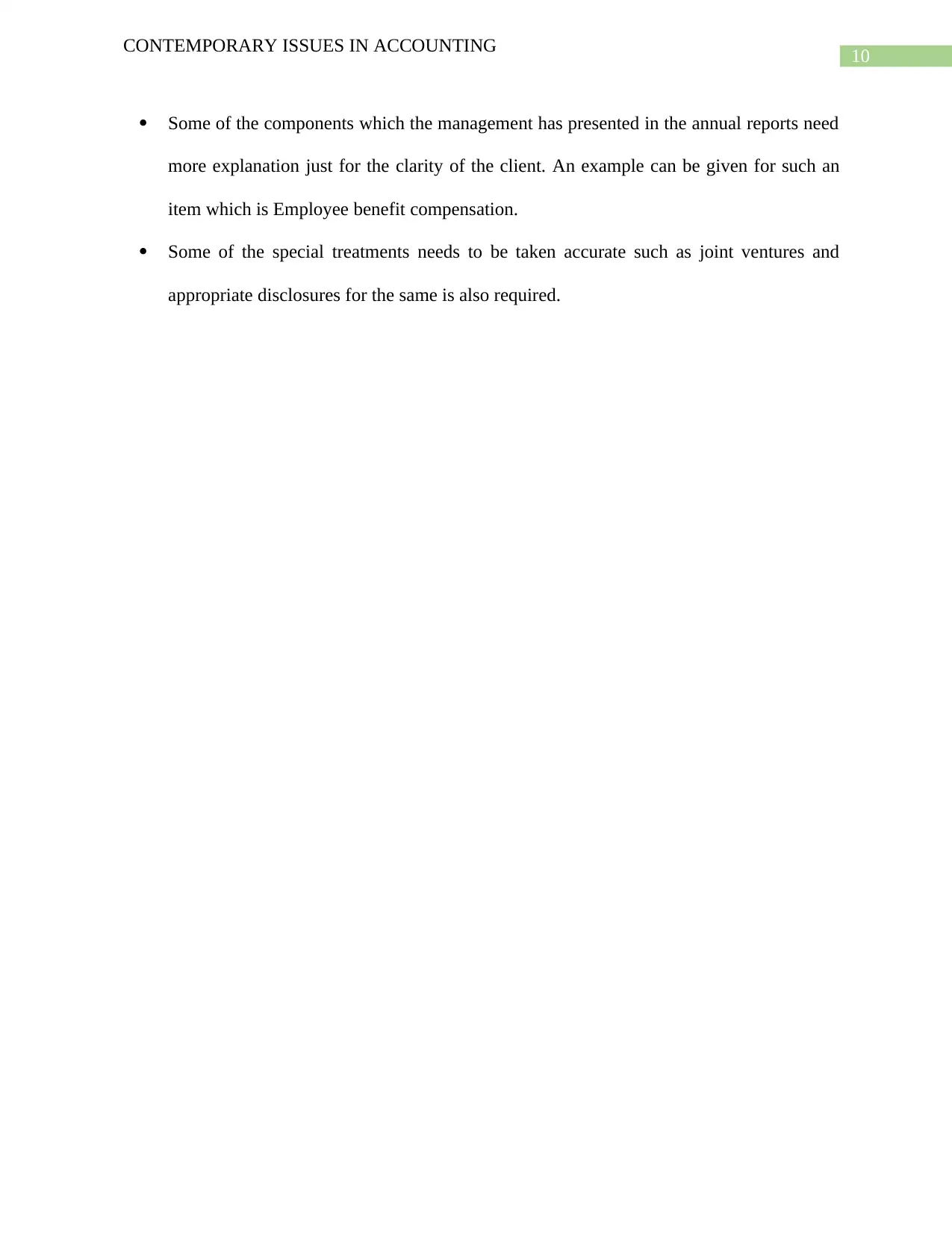

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 1: (Statement showing Cash flow for Ausdrill Ltd)

Source: (Ausdrill.com.au. 2019).

1. The conceptual framework also provides a framework to the management of the company

for appropriately presenting the assets, liabilities and the income and expenses of the

company. This also means that the conceptual framework helps the users to get a clear

picture of the financial position of the business. The business of Ausdrill ltd has

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 1: (Statement showing Cash flow for Ausdrill Ltd)

Source: (Ausdrill.com.au. 2019).

1. The conceptual framework also provides a framework to the management of the company

for appropriately presenting the assets, liabilities and the income and expenses of the

company. This also means that the conceptual framework helps the users to get a clear

picture of the financial position of the business. The business of Ausdrill ltd has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

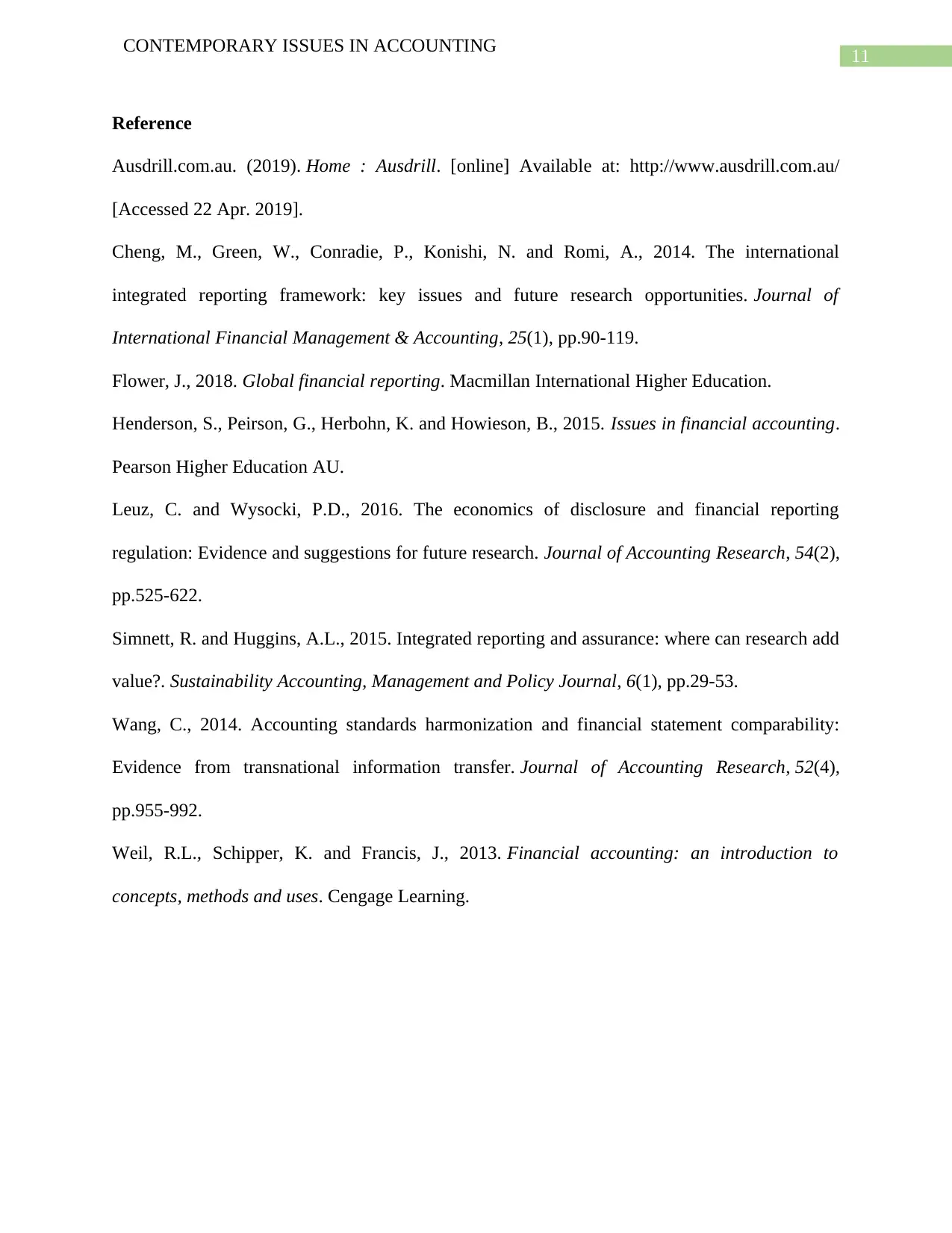

CONTEMPORARY ISSUES IN ACCOUNTING

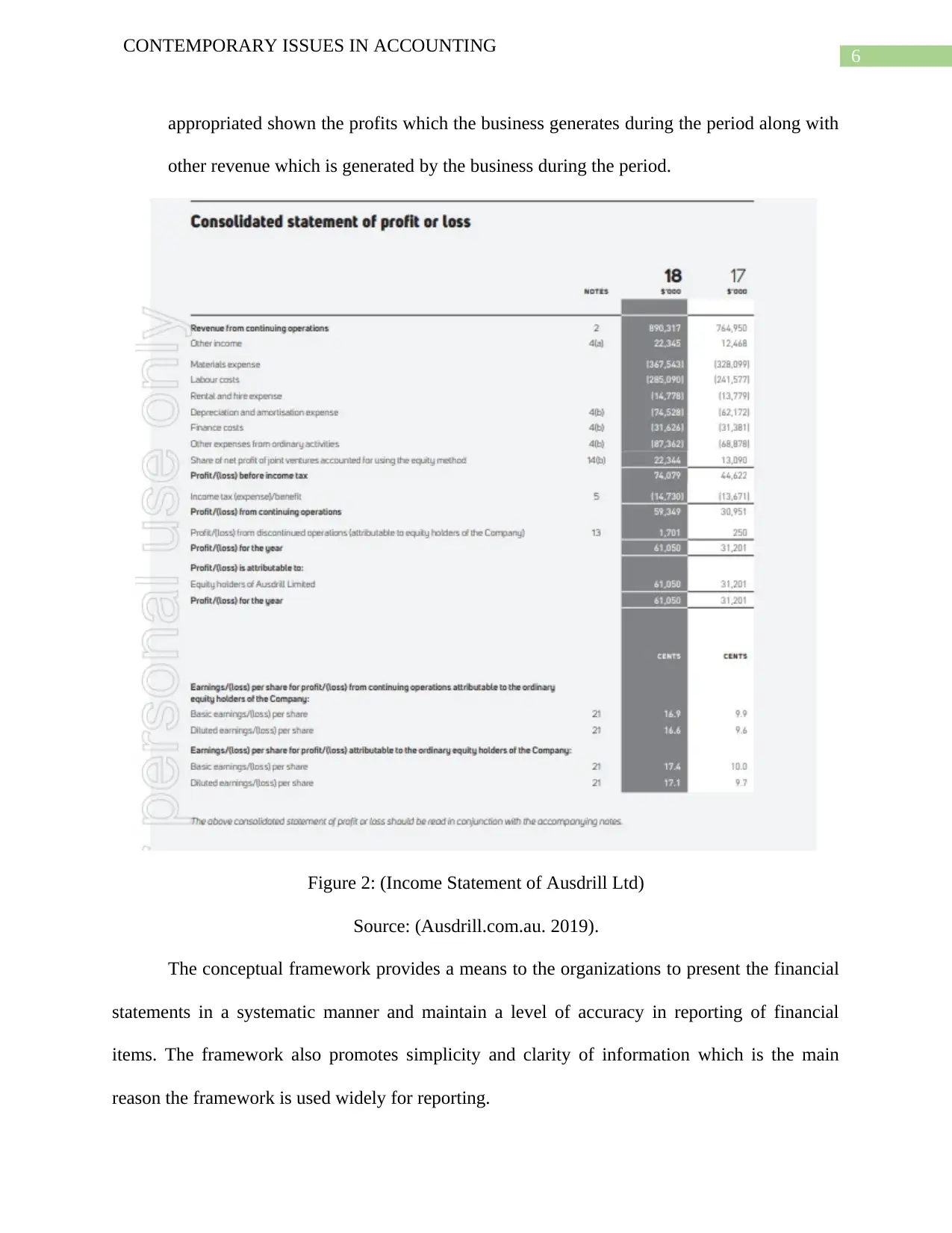

appropriated shown the profits which the business generates during the period along with

other revenue which is generated by the business during the period.

Figure 2: (Income Statement of Ausdrill Ltd)

Source: (Ausdrill.com.au. 2019).

The conceptual framework provides a means to the organizations to present the financial

statements in a systematic manner and maintain a level of accuracy in reporting of financial

items. The framework also promotes simplicity and clarity of information which is the main

reason the framework is used widely for reporting.

CONTEMPORARY ISSUES IN ACCOUNTING

appropriated shown the profits which the business generates during the period along with

other revenue which is generated by the business during the period.

Figure 2: (Income Statement of Ausdrill Ltd)

Source: (Ausdrill.com.au. 2019).

The conceptual framework provides a means to the organizations to present the financial

statements in a systematic manner and maintain a level of accuracy in reporting of financial

items. The framework also promotes simplicity and clarity of information which is the main

reason the framework is used widely for reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

Recognition Criteria

The recognition criteria effectively provide instructions as to how certain items can be

presented in the annual reports. In Australia, the accounting standards are issued by Australian

Accounting Standard Board (AASB) which clarifies regarding all the treatments and disclosures

which needs to be provided (Flower 2018). The different items which are reporting in the

financial statements are discussed below in details:

Assets: The assets form important component of the annual reports and represents the

items which are used by the business for the purpose of generating revenue and profits

for the business. The assets of a business are segregated on the basis of usage which is

either they are short term or long-term assets depending upon the period of use. The

balance sheet of Ausdrill ltd shows current assets which comprises of cash balances, trade

debtors and closing stock value of the business. The non-current assets of the business

consist of assets which are more of fixed nature.

Liabilities: Similarly, to the assets, the liabilities of a business are also segregated in

terms of long term and short-term liability (Weil, Schipper and Francis 2013). The

current liabilities and non-current liabilities of Ausdrill ltd are appropriately presented

and segregated in the annual reports which is shown by the business for the period.

Income: The income of the business is shown in the income statement and the main

source of income for the company is from the mining products which is generated or the

service which is provided.

Expenses: The income statement also consists of expenses of the business and some of

the expenses which is represented in the annual report of 2018 are majorly cash items

with some exceptions as well.

CONTEMPORARY ISSUES IN ACCOUNTING

Recognition Criteria

The recognition criteria effectively provide instructions as to how certain items can be

presented in the annual reports. In Australia, the accounting standards are issued by Australian

Accounting Standard Board (AASB) which clarifies regarding all the treatments and disclosures

which needs to be provided (Flower 2018). The different items which are reporting in the

financial statements are discussed below in details:

Assets: The assets form important component of the annual reports and represents the

items which are used by the business for the purpose of generating revenue and profits

for the business. The assets of a business are segregated on the basis of usage which is

either they are short term or long-term assets depending upon the period of use. The

balance sheet of Ausdrill ltd shows current assets which comprises of cash balances, trade

debtors and closing stock value of the business. The non-current assets of the business

consist of assets which are more of fixed nature.

Liabilities: Similarly, to the assets, the liabilities of a business are also segregated in

terms of long term and short-term liability (Weil, Schipper and Francis 2013). The

current liabilities and non-current liabilities of Ausdrill ltd are appropriately presented

and segregated in the annual reports which is shown by the business for the period.

Income: The income of the business is shown in the income statement and the main

source of income for the company is from the mining products which is generated or the

service which is provided.

Expenses: The income statement also consists of expenses of the business and some of

the expenses which is represented in the annual report of 2018 are majorly cash items

with some exceptions as well.

8

CONTEMPORARY ISSUES IN ACCOUNTING

Equity: Retained earnings form a major part of the equity of the business which is formed

by accumulating profits and the same can be used for the purpose of reinvestment. The

business also utilizes equity capital for meeting the capital fund requirements of the

business and the same is appropriately presented in the annual reports.

Fundamental Qualitative Characteristics

The analysis of the qualitative components from the annual report of Ausdrill ltd are

explained below:

Relevance: The principle of relevance makes its clear that the information which is to be

included in the annual report should be clear and should be relevant to the operations of

the business. In the case of Ausdrill ltd, the management has followed AASB standards

for which disclosures are also provided which makes the information relevant and

accurate. In addition to this, proper disclosures are also provided by the business.

Faithful representation: The information which is presented in the annual report should

be accurate as it is to be noted that banks provides financial assistance after analyzing

such information and shareholders also invests their funds after the analysis (Simnett and

Huggins 2015). The audit report makes it clear that the financial statements are accurate

which means that this condition is also met by the management.

Enhancing Qualitative Characteristics

Comparability: This principle requires the financial information which is presented in the

annual report should be comparable with other periods financial estimates. The

management of Ausdrill ltd has presented previous year results and current years result as

per the format which makes it easier to make comparisons.

CONTEMPORARY ISSUES IN ACCOUNTING

Equity: Retained earnings form a major part of the equity of the business which is formed

by accumulating profits and the same can be used for the purpose of reinvestment. The

business also utilizes equity capital for meeting the capital fund requirements of the

business and the same is appropriately presented in the annual reports.

Fundamental Qualitative Characteristics

The analysis of the qualitative components from the annual report of Ausdrill ltd are

explained below:

Relevance: The principle of relevance makes its clear that the information which is to be

included in the annual report should be clear and should be relevant to the operations of

the business. In the case of Ausdrill ltd, the management has followed AASB standards

for which disclosures are also provided which makes the information relevant and

accurate. In addition to this, proper disclosures are also provided by the business.

Faithful representation: The information which is presented in the annual report should

be accurate as it is to be noted that banks provides financial assistance after analyzing

such information and shareholders also invests their funds after the analysis (Simnett and

Huggins 2015). The audit report makes it clear that the financial statements are accurate

which means that this condition is also met by the management.

Enhancing Qualitative Characteristics

Comparability: This principle requires the financial information which is presented in the

annual report should be comparable with other periods financial estimates. The

management of Ausdrill ltd has presented previous year results and current years result as

per the format which makes it easier to make comparisons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

Verifiability: The information which is presented in the financial statement should be

verifiable by different users. This is done so that accuracy and further check can be

imposed on the financial reports which is prepared by the management. The notes to

accounts serves as an important medium for verifying the dinner,

Timeliness: The principle states that the financial information should be presented by the

company in a suitable time so that the same ate useful for the investors. The financial

reports are presented at the end of year but interims reports can be published on quarterly

basis.

Understandability: The information and the disclosures included in the annual reports

should be interpreted by everyone. This principle emphasizes on use if simple

presentations and not jargons for explain different disclosures (Leuz and Wysocki 2016).

The information which contained needs to be interpreted by the users so that appropriate

decisions can be taken.

Conclusion and Recommendations

The above discussion makes it cleat that the management of Ausdrill ltd effectively

follows the reporting framework and all the information which is presented in the annual reports

are showing true and fair view. The application of the conceptual framework is used mainly for

promoting better understanding of financial information by the users and on the basis of the same

taking important decisions. The financial reports of the business are appropriate presented

complying with all rules and regulations of reporting.

The recommendation which can be suggested to the management of Ausdrill ltd are listed

below in point form:

CONTEMPORARY ISSUES IN ACCOUNTING

Verifiability: The information which is presented in the financial statement should be

verifiable by different users. This is done so that accuracy and further check can be

imposed on the financial reports which is prepared by the management. The notes to

accounts serves as an important medium for verifying the dinner,

Timeliness: The principle states that the financial information should be presented by the

company in a suitable time so that the same ate useful for the investors. The financial

reports are presented at the end of year but interims reports can be published on quarterly

basis.

Understandability: The information and the disclosures included in the annual reports

should be interpreted by everyone. This principle emphasizes on use if simple

presentations and not jargons for explain different disclosures (Leuz and Wysocki 2016).

The information which contained needs to be interpreted by the users so that appropriate

decisions can be taken.

Conclusion and Recommendations

The above discussion makes it cleat that the management of Ausdrill ltd effectively

follows the reporting framework and all the information which is presented in the annual reports

are showing true and fair view. The application of the conceptual framework is used mainly for

promoting better understanding of financial information by the users and on the basis of the same

taking important decisions. The financial reports of the business are appropriate presented

complying with all rules and regulations of reporting.

The recommendation which can be suggested to the management of Ausdrill ltd are listed

below in point form:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

Some of the components which the management has presented in the annual reports need

more explanation just for the clarity of the client. An example can be given for such an

item which is Employee benefit compensation.

Some of the special treatments needs to be taken accurate such as joint ventures and

appropriate disclosures for the same is also required.

CONTEMPORARY ISSUES IN ACCOUNTING

Some of the components which the management has presented in the annual reports need

more explanation just for the clarity of the client. An example can be given for such an

item which is Employee benefit compensation.

Some of the special treatments needs to be taken accurate such as joint ventures and

appropriate disclosures for the same is also required.

11

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Ausdrill.com.au. (2019). Home : Ausdrill. [online] Available at: http://www.ausdrill.com.au/

[Accessed 22 Apr. 2019].

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research add

value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Ausdrill.com.au. (2019). Home : Ausdrill. [online] Available at: http://www.ausdrill.com.au/

[Accessed 22 Apr. 2019].

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can research add

value?. Sustainability Accounting, Management and Policy Journal, 6(1), pp.29-53.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.