BHP Billiton and the AASB: Analysis of Accounting Standards

VerifiedAdded on 2023/06/13

|18

|2955

|81

Report

AI Summary

This report provides a detailed analysis of BHP Billiton, an Australian ASX Top 100 listed firm, and its adherence to the Conceptual Framework issued by the Australian Accounting Standards Board (AASB). It critically examines both the fundamental and enhancing characteristics of the company's financial statements, focusing on aspects such as asset valuation, liability management, equity reporting, inventory assessment, accounts receivable handling, and the treatment of plant, property, and equipment (PPE). The report further analyzes the relevance and faithful representation of financial information, exploring qualitative features like comparability and verifiability. It also evaluates the company's accounting practices for leases and depreciation, providing a comprehensive overview of BHP Billiton's financial reporting in accordance with AASB guidelines. Desklib provides solved assignments and past papers for students.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

University Name

Student Name

Authors’ Note

Contemporary Issues in Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The current study explicates in detail about diverse systems of accounting that can help in

enhancing the systems of monitoring, analysing, controlling and at the same time directing

functionalities of business. This study also assists in presenting analytical findings on

accounting dimensions that can essentially focus on the requirements of analysing

compliance to set rules as well as regulations of Conceptual Framework issued by the

Australian Accounting Standards Board. In itself, this study is a comprehensive account

directed to an Australian ASX Top 100 listed firm BHP Billiton illustrating effectiveness of

the corporation to meet the requirements of the conceptual framework of accounting issued

by Australian Accounting Standards Board (also simply referred to as AASB). In addition to

this, the study at hand also presents critical analysis of both fundamental as well as enhancing

characteristics of pecuniary statement of the firm.

BHP, previously referred to as BHP Billiton, is essentially an Anglo-

Australian transnational that operates in the areas of mining, metals, natural gal, iron ore as

well as petroleum among many others. The company serves in the metals and mining

industry worldwide.

Critical review of objectives of conceptual framework issued by AASB

As suggested by Scott (2015), the main objective of general purpose financial reporting

(GPFR) is present in detail important financial information as regards reporting business

entity under deliberation. Essentially, pecuniary information is of great importance to various

users of financial information. As such, the primary audience or in other words users of this

financial information include financiers, both creditors as well as debtors along with many

other stakeholders of the firm. These users require financial information for arriving at

Introduction

The current study explicates in detail about diverse systems of accounting that can help in

enhancing the systems of monitoring, analysing, controlling and at the same time directing

functionalities of business. This study also assists in presenting analytical findings on

accounting dimensions that can essentially focus on the requirements of analysing

compliance to set rules as well as regulations of Conceptual Framework issued by the

Australian Accounting Standards Board. In itself, this study is a comprehensive account

directed to an Australian ASX Top 100 listed firm BHP Billiton illustrating effectiveness of

the corporation to meet the requirements of the conceptual framework of accounting issued

by Australian Accounting Standards Board (also simply referred to as AASB). In addition to

this, the study at hand also presents critical analysis of both fundamental as well as enhancing

characteristics of pecuniary statement of the firm.

BHP, previously referred to as BHP Billiton, is essentially an Anglo-

Australian transnational that operates in the areas of mining, metals, natural gal, iron ore as

well as petroleum among many others. The company serves in the metals and mining

industry worldwide.

Critical review of objectives of conceptual framework issued by AASB

As suggested by Scott (2015), the main objective of general purpose financial reporting

(GPFR) is present in detail important financial information as regards reporting business

entity under deliberation. Essentially, pecuniary information is of great importance to various

users of financial information. As such, the primary audience or in other words users of this

financial information include financiers, both creditors as well as debtors along with many

other stakeholders of the firm. These users require financial information for arriving at

3CONTEMPORARY ISSUES IN ACCOUNTING

specific economic decisions that in turn might affect their own interests (DesJardins and

McCall 2014). Primarily, these interests include judgment regarding purchasing, selling,

retaining equity, acquiring funds, settling borrowed money and many others.

Figure: Conceptual Framework (AASB)

(Source: Jessen et al. 2014).

Target user of General Purpose Financial Reports (GPFR)

The primary users or else audiences of general purpose financial report are subsisting and

probable investors, lenders along with creditors in framing decisions regarding pecuniary

resources of the firm (Schaltegger and Burritt 2017).

Essentially, conceptual Framework shows the intention along with standards of general

purpose financial report- (GPFR). Fundamentally, conceptual framework can be considered

to be an effective instrument that can aid board of the company in enhancing financial

standards based on particular principles, concepts as well as premises. Furthermore, it can

also be hereby stated in this that persons accountable for preparation of GPFR can help in

designing effective and all together reliable stratagems of accounting. Conversely, financial

standards can aid in enhancing entire processes of implementation of distinct accounting

scheme (Jessen et al. 2014).

specific economic decisions that in turn might affect their own interests (DesJardins and

McCall 2014). Primarily, these interests include judgment regarding purchasing, selling,

retaining equity, acquiring funds, settling borrowed money and many others.

Figure: Conceptual Framework (AASB)

(Source: Jessen et al. 2014).

Target user of General Purpose Financial Reports (GPFR)

The primary users or else audiences of general purpose financial report are subsisting and

probable investors, lenders along with creditors in framing decisions regarding pecuniary

resources of the firm (Schaltegger and Burritt 2017).

Essentially, conceptual Framework shows the intention along with standards of general

purpose financial report- (GPFR). Fundamentally, conceptual framework can be considered

to be an effective instrument that can aid board of the company in enhancing financial

standards based on particular principles, concepts as well as premises. Furthermore, it can

also be hereby stated in this that persons accountable for preparation of GPFR can help in

designing effective and all together reliable stratagems of accounting. Conversely, financial

standards can aid in enhancing entire processes of implementation of distinct accounting

scheme (Jessen et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CONTEMPORARY ISSUES IN ACCOUNTING

In essence, analysis of financial declarations of the corporation reflects conformation with the

directives of “Conceptual Framework of Australian Accounting Standards Board”. In actual

fact, this assists in acquiring complete understanding as regards purposes of financial

assertions. Additionally, this also helps in understanding qualitative exclusivity that can

consequently help in instituting effectiveness of financial pronouncements (Bridgett et al.

2015). Nevertheless, there are different constituents of financial pronouncements that can aid

diverse users to make use of the amassed information to develop economic decisions as to

buy/sell, handling equity, various instruments of debt, resolution and agreements of loans

otherwise credit. Thus, it is the way by which financial pronouncements are said to satisfy

and meet all the obligations as well as objectives of definite regulations. As correctly

mentioned by Libby (2017), numerous financial items are stated in the pecuniary statements

of firms namely, revenue, assets/liabilities and financial pronouncements namely assets

and liabilities (taking in both current and non-current). Thus, users of financial information of

firms can find out about capacity and financial assets of the corporation. In addition to this,

the users can evaluate predictions of the firm in the upcoming period from assertions on

potential cash flow. Also, this too assists in the processes of analysing efficacy of

administration of the corporation in undertaking their responsibilities.

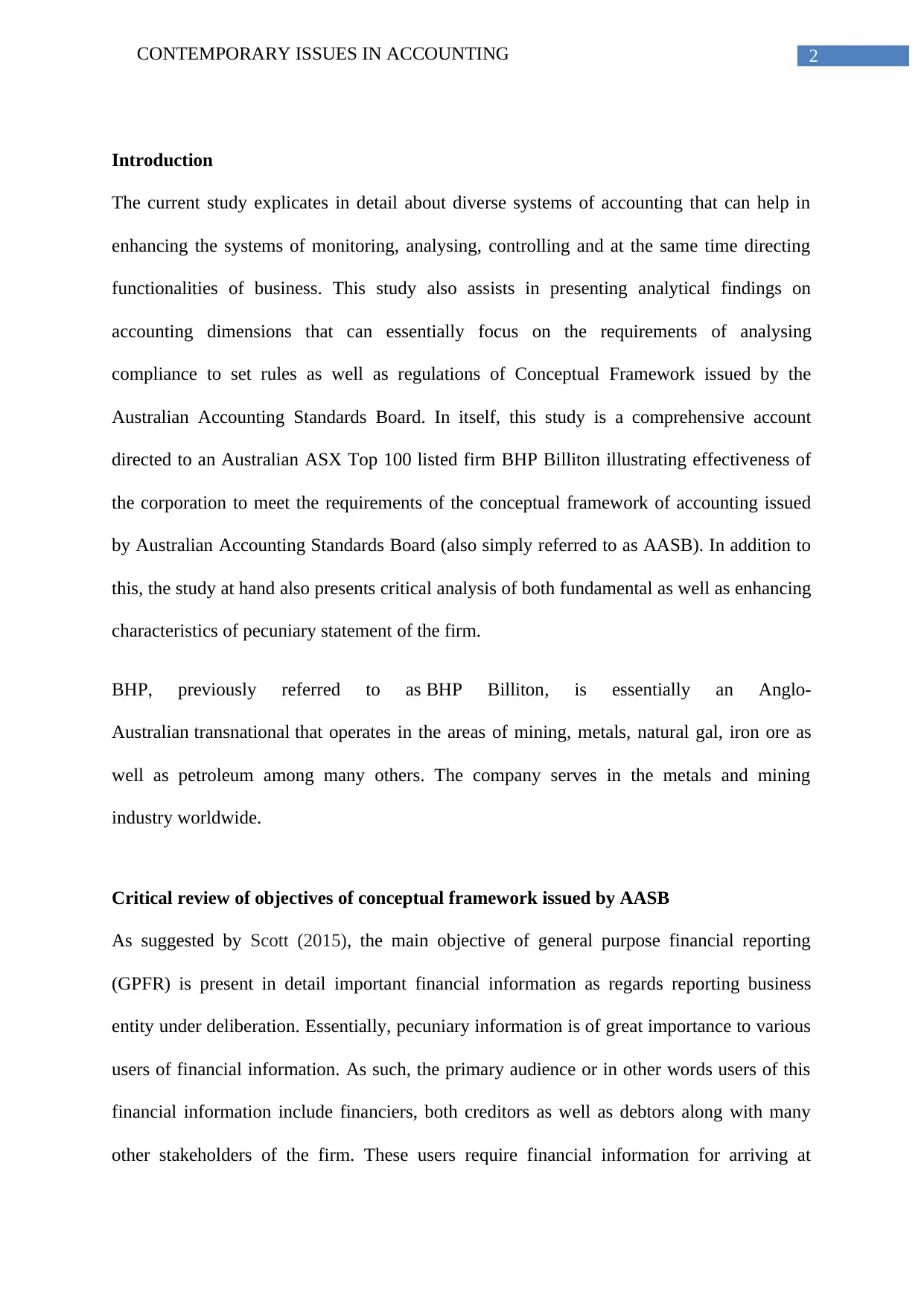

Asset: As per the financial declarations recorded during the period 2016, the total assets of

the business concern are registered to be USD 118953 million. In addition to this, the assets

of the firm BHP Billiton are necessarily expressed as Australian Dollars that are also the

operational currency of the specific corporation. Nevertheless, the procedure of evaluation of

assets mentioned in the financial pronouncements replicate the fact that assets of the firm can

be classified as “held for sale”. This can be essentially enumerated at comparatively low

value of the recognized cost weighed against fair value after deduction of the costs that is

borne by the company for sales (Zhang and Andrew 2014).

In essence, analysis of financial declarations of the corporation reflects conformation with the

directives of “Conceptual Framework of Australian Accounting Standards Board”. In actual

fact, this assists in acquiring complete understanding as regards purposes of financial

assertions. Additionally, this also helps in understanding qualitative exclusivity that can

consequently help in instituting effectiveness of financial pronouncements (Bridgett et al.

2015). Nevertheless, there are different constituents of financial pronouncements that can aid

diverse users to make use of the amassed information to develop economic decisions as to

buy/sell, handling equity, various instruments of debt, resolution and agreements of loans

otherwise credit. Thus, it is the way by which financial pronouncements are said to satisfy

and meet all the obligations as well as objectives of definite regulations. As correctly

mentioned by Libby (2017), numerous financial items are stated in the pecuniary statements

of firms namely, revenue, assets/liabilities and financial pronouncements namely assets

and liabilities (taking in both current and non-current). Thus, users of financial information of

firms can find out about capacity and financial assets of the corporation. In addition to this,

the users can evaluate predictions of the firm in the upcoming period from assertions on

potential cash flow. Also, this too assists in the processes of analysing efficacy of

administration of the corporation in undertaking their responsibilities.

Asset: As per the financial declarations recorded during the period 2016, the total assets of

the business concern are registered to be USD 118953 million. In addition to this, the assets

of the firm BHP Billiton are necessarily expressed as Australian Dollars that are also the

operational currency of the specific corporation. Nevertheless, the procedure of evaluation of

assets mentioned in the financial pronouncements replicate the fact that assets of the firm can

be classified as “held for sale”. This can be essentially enumerated at comparatively low

value of the recognized cost weighed against fair value after deduction of the costs that is

borne by the company for sales (Zhang and Andrew 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CONTEMPORARY ISSUES IN ACCOUNTING

Table: Assets of BHP Billiton

(Source: BHP Billiton | A leading global resources company 2018)

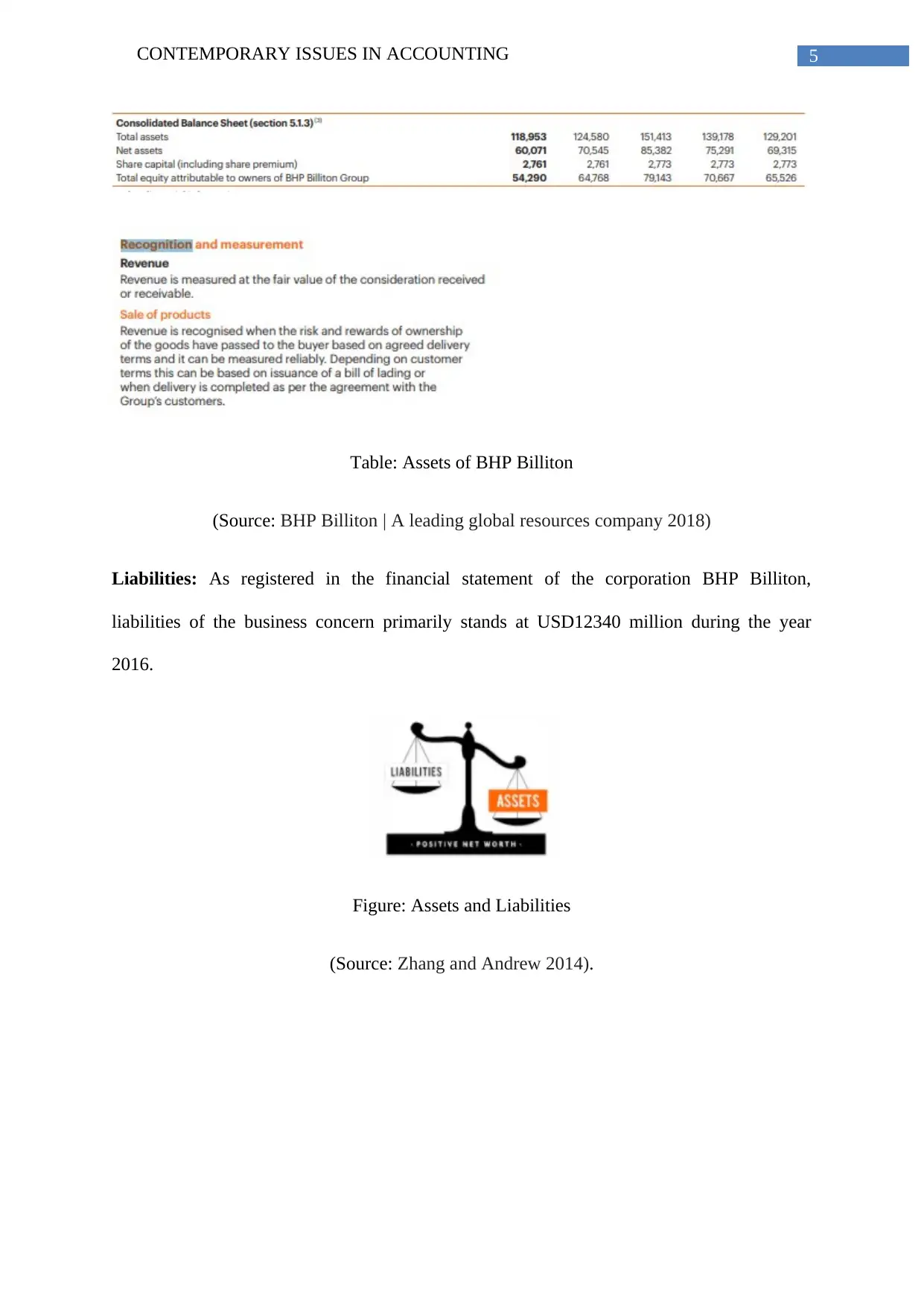

Liabilities: As registered in the financial statement of the corporation BHP Billiton,

liabilities of the business concern primarily stands at USD12340 million during the year

2016.

Figure: Assets and Liabilities

(Source: Zhang and Andrew 2014).

Table: Assets of BHP Billiton

(Source: BHP Billiton | A leading global resources company 2018)

Liabilities: As registered in the financial statement of the corporation BHP Billiton,

liabilities of the business concern primarily stands at USD12340 million during the year

2016.

Figure: Assets and Liabilities

(Source: Zhang and Andrew 2014).

6CONTEMPORARY ISSUES IN ACCOUNTING

Table: Assets and Liabilities

(Source: BHP Billiton | A leading global resources company 2018)

Equity: Thorough study of the balance sheet of the corporation BHP Billiton reveals that

shareholders’ equity. The equity is registered to be USD 60071 million in the financial

statement during the period 2016. As stated in the financial pronouncement of the

corporation, derivatives expressed at particularly the fair value by way of profit/loss

enumerated at fair value (Craig et al. 2017). So, the corporation utilizes diverse models on

particularly accounting of derivatives that requires measurement at fair value.

Table: Assets and Liabilities

(Source: BHP Billiton | A leading global resources company 2018)

Equity: Thorough study of the balance sheet of the corporation BHP Billiton reveals that

shareholders’ equity. The equity is registered to be USD 60071 million in the financial

statement during the period 2016. As stated in the financial pronouncement of the

corporation, derivatives expressed at particularly the fair value by way of profit/loss

enumerated at fair value (Craig et al. 2017). So, the corporation utilizes diverse models on

particularly accounting of derivatives that requires measurement at fair value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CONTEMPORARY ISSUES IN ACCOUNTING

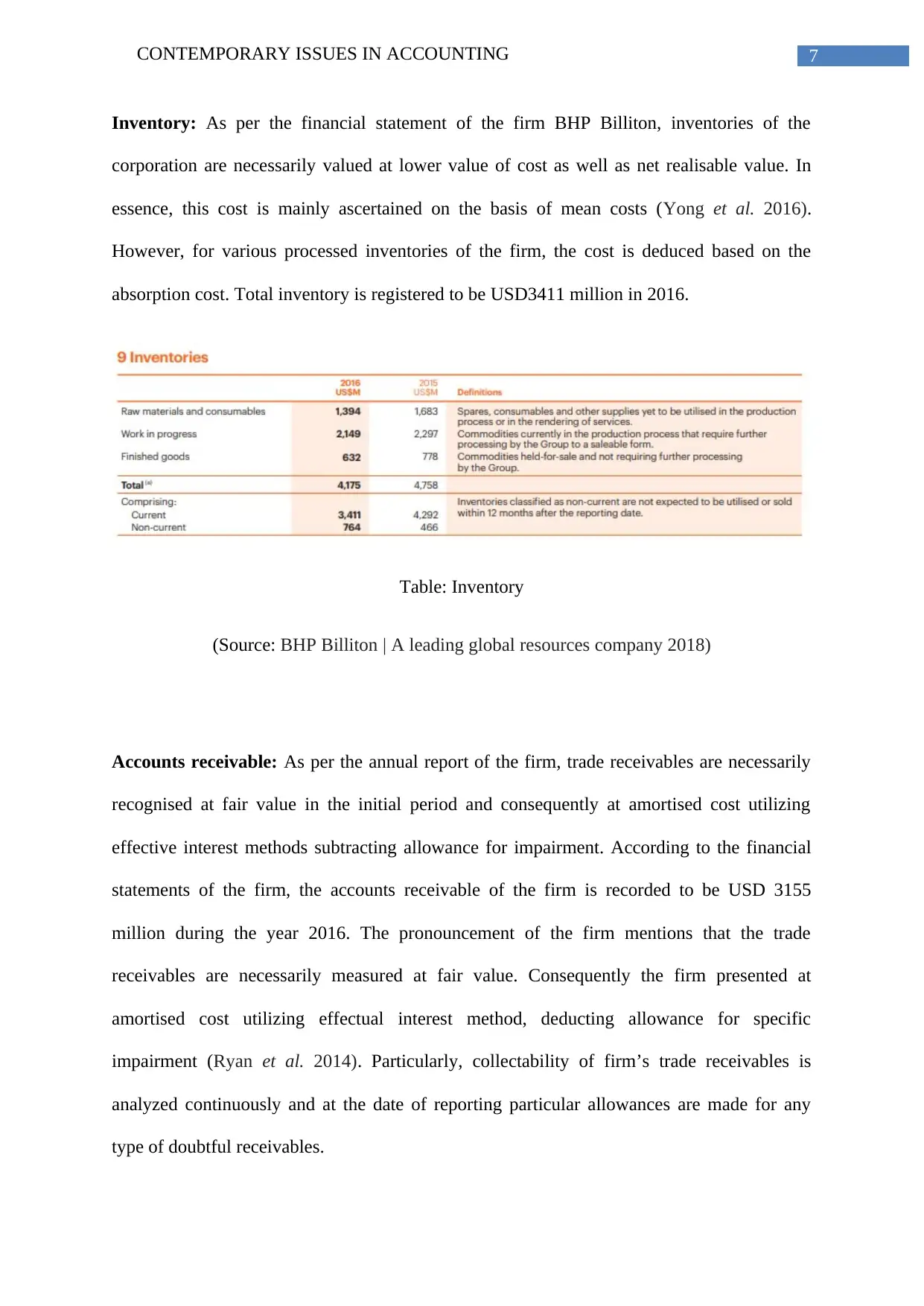

Inventory: As per the financial statement of the firm BHP Billiton, inventories of the

corporation are necessarily valued at lower value of cost as well as net realisable value. In

essence, this cost is mainly ascertained on the basis of mean costs (Yong et al. 2016).

However, for various processed inventories of the firm, the cost is deduced based on the

absorption cost. Total inventory is registered to be USD3411 million in 2016.

Table: Inventory

(Source: BHP Billiton | A leading global resources company 2018)

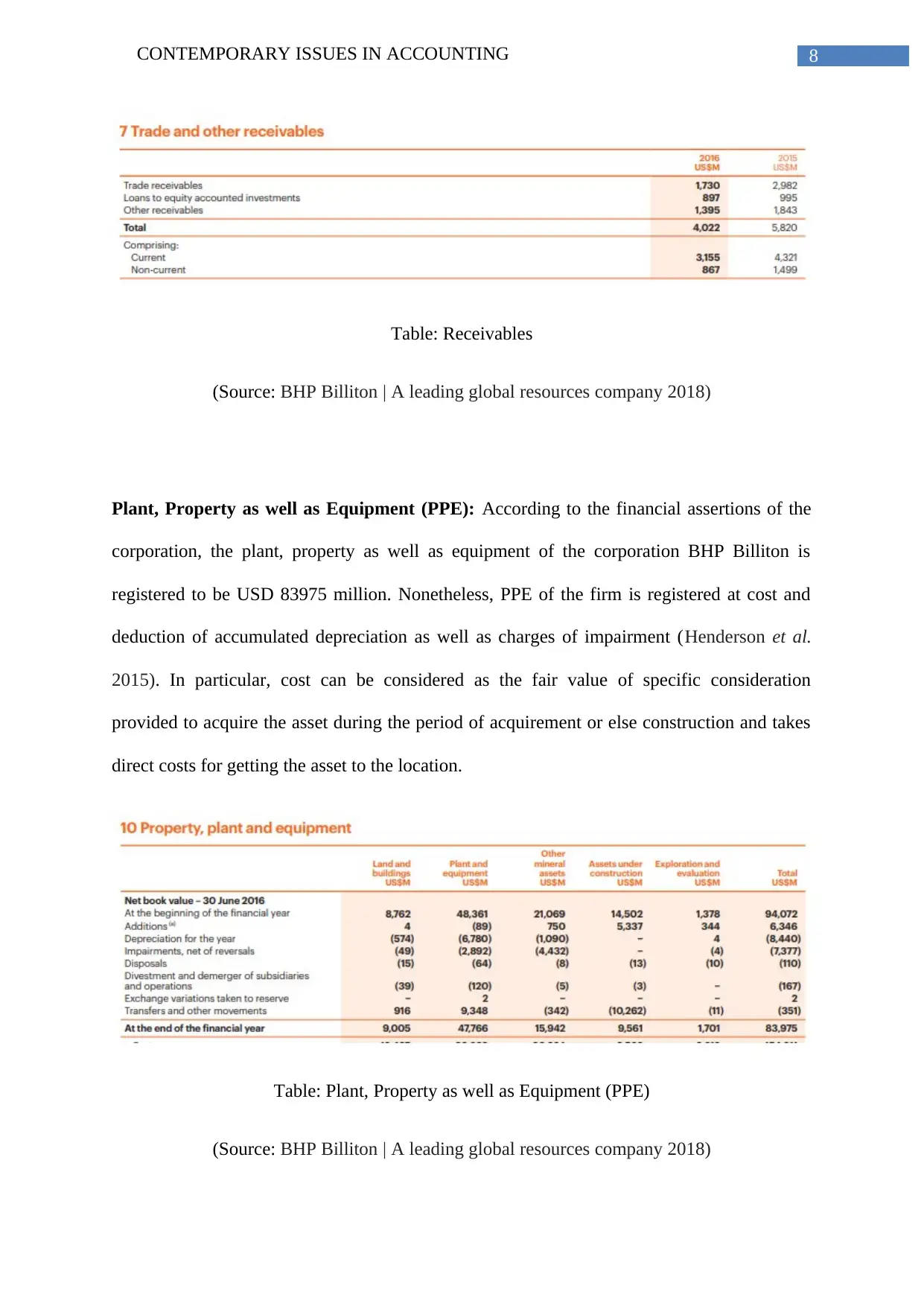

Accounts receivable: As per the annual report of the firm, trade receivables are necessarily

recognised at fair value in the initial period and consequently at amortised cost utilizing

effective interest methods subtracting allowance for impairment. According to the financial

statements of the firm, the accounts receivable of the firm is recorded to be USD 3155

million during the year 2016. The pronouncement of the firm mentions that the trade

receivables are necessarily measured at fair value. Consequently the firm presented at

amortised cost utilizing effectual interest method, deducting allowance for specific

impairment (Ryan et al. 2014). Particularly, collectability of firm’s trade receivables is

analyzed continuously and at the date of reporting particular allowances are made for any

type of doubtful receivables.

Inventory: As per the financial statement of the firm BHP Billiton, inventories of the

corporation are necessarily valued at lower value of cost as well as net realisable value. In

essence, this cost is mainly ascertained on the basis of mean costs (Yong et al. 2016).

However, for various processed inventories of the firm, the cost is deduced based on the

absorption cost. Total inventory is registered to be USD3411 million in 2016.

Table: Inventory

(Source: BHP Billiton | A leading global resources company 2018)

Accounts receivable: As per the annual report of the firm, trade receivables are necessarily

recognised at fair value in the initial period and consequently at amortised cost utilizing

effective interest methods subtracting allowance for impairment. According to the financial

statements of the firm, the accounts receivable of the firm is recorded to be USD 3155

million during the year 2016. The pronouncement of the firm mentions that the trade

receivables are necessarily measured at fair value. Consequently the firm presented at

amortised cost utilizing effectual interest method, deducting allowance for specific

impairment (Ryan et al. 2014). Particularly, collectability of firm’s trade receivables is

analyzed continuously and at the date of reporting particular allowances are made for any

type of doubtful receivables.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CONTEMPORARY ISSUES IN ACCOUNTING

Table: Receivables

(Source: BHP Billiton | A leading global resources company 2018)

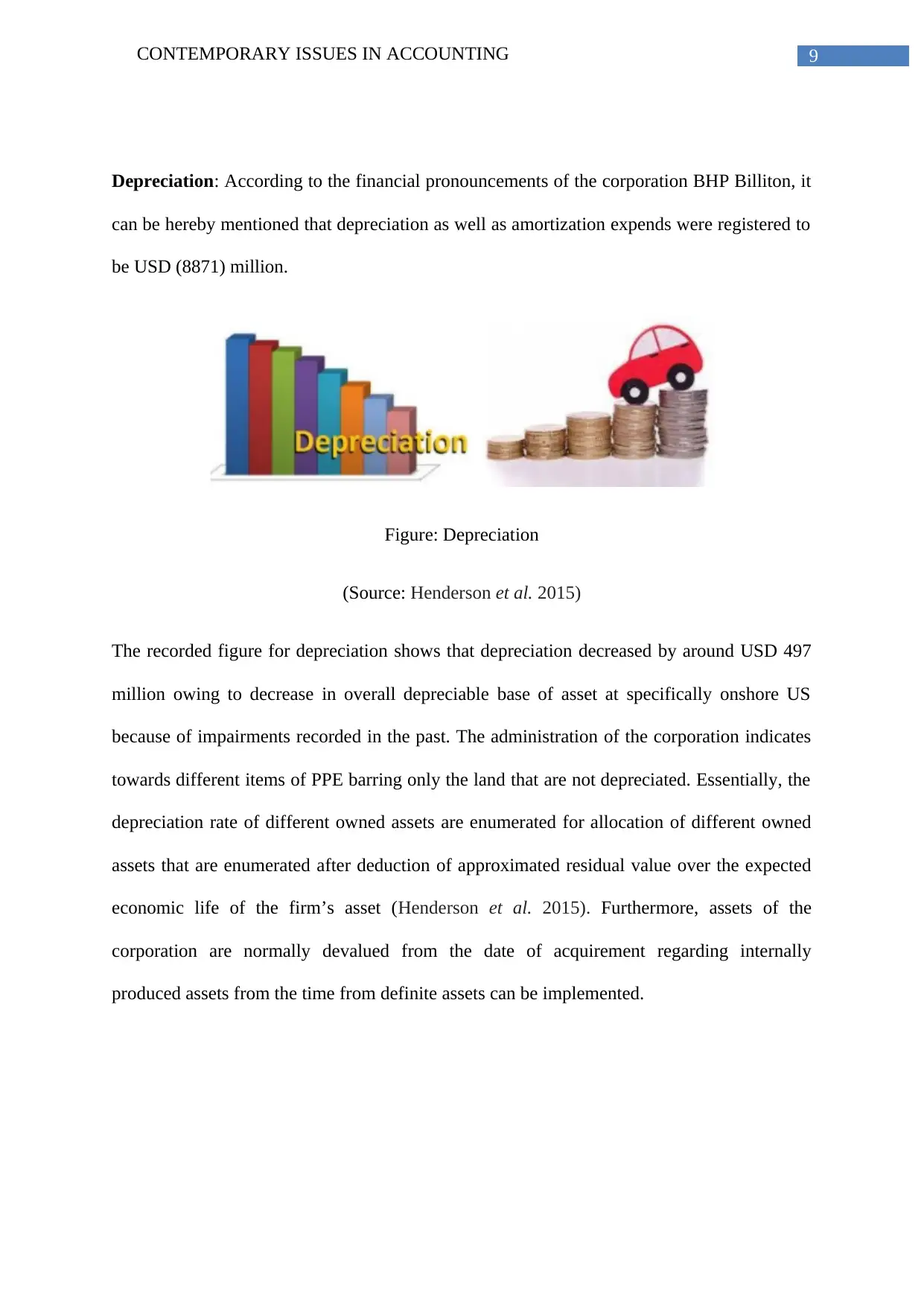

Plant, Property as well as Equipment (PPE): According to the financial assertions of the

corporation, the plant, property as well as equipment of the corporation BHP Billiton is

registered to be USD 83975 million. Nonetheless, PPE of the firm is registered at cost and

deduction of accumulated depreciation as well as charges of impairment (Henderson et al.

2015). In particular, cost can be considered as the fair value of specific consideration

provided to acquire the asset during the period of acquirement or else construction and takes

direct costs for getting the asset to the location.

Table: Plant, Property as well as Equipment (PPE)

(Source: BHP Billiton | A leading global resources company 2018)

Table: Receivables

(Source: BHP Billiton | A leading global resources company 2018)

Plant, Property as well as Equipment (PPE): According to the financial assertions of the

corporation, the plant, property as well as equipment of the corporation BHP Billiton is

registered to be USD 83975 million. Nonetheless, PPE of the firm is registered at cost and

deduction of accumulated depreciation as well as charges of impairment (Henderson et al.

2015). In particular, cost can be considered as the fair value of specific consideration

provided to acquire the asset during the period of acquirement or else construction and takes

direct costs for getting the asset to the location.

Table: Plant, Property as well as Equipment (PPE)

(Source: BHP Billiton | A leading global resources company 2018)

9CONTEMPORARY ISSUES IN ACCOUNTING

Depreciation: According to the financial pronouncements of the corporation BHP Billiton, it

can be hereby mentioned that depreciation as well as amortization expends were registered to

be USD (8871) million.

Figure: Depreciation

(Source: Henderson et al. 2015)

The recorded figure for depreciation shows that depreciation decreased by around USD 497

million owing to decrease in overall depreciable base of asset at specifically onshore US

because of impairments recorded in the past. The administration of the corporation indicates

towards different items of PPE barring only the land that are not depreciated. Essentially, the

depreciation rate of different owned assets are enumerated for allocation of different owned

assets that are enumerated after deduction of approximated residual value over the expected

economic life of the firm’s asset (Henderson et al. 2015). Furthermore, assets of the

corporation are normally devalued from the date of acquirement regarding internally

produced assets from the time from definite assets can be implemented.

Depreciation: According to the financial pronouncements of the corporation BHP Billiton, it

can be hereby mentioned that depreciation as well as amortization expends were registered to

be USD (8871) million.

Figure: Depreciation

(Source: Henderson et al. 2015)

The recorded figure for depreciation shows that depreciation decreased by around USD 497

million owing to decrease in overall depreciable base of asset at specifically onshore US

because of impairments recorded in the past. The administration of the corporation indicates

towards different items of PPE barring only the land that are not depreciated. Essentially, the

depreciation rate of different owned assets are enumerated for allocation of different owned

assets that are enumerated after deduction of approximated residual value over the expected

economic life of the firm’s asset (Henderson et al. 2015). Furthermore, assets of the

corporation are normally devalued from the date of acquirement regarding internally

produced assets from the time from definite assets can be implemented.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CONTEMPORARY ISSUES IN ACCOUNTING

Table: Depreciation

(Source: BHP Billiton | A leading global resources company 2018)

Treatment of leases: Assets of the firm that are held under lease lead to receiving

considerably all the risks as well as rewards of ownership. These are capitalized as plant,

property as well as equipment at the lower of the value. The operating lease rentals are

recorded to be USD (528 million). There are equipment leases and assets are held under

lease. This lead to group accepting all the risk considerably and rewards of various

ownerships can be capitalized as particularly plant, property as well as equipment (Scott

2015). Operating lease as mentioned in the report are not capitalised and payments for rent

are included in the income statement

Analysis of financial assertions as regards relevance as well as faithful representation

Schaltegger and Burritt (2017) suggests that characteristics of effective financial information

comprises of relevance together with faithful representation of specific information as regards

finances of business segments. Jessen et al. (2014) suggests that relevance point out towards

Table: Depreciation

(Source: BHP Billiton | A leading global resources company 2018)

Treatment of leases: Assets of the firm that are held under lease lead to receiving

considerably all the risks as well as rewards of ownership. These are capitalized as plant,

property as well as equipment at the lower of the value. The operating lease rentals are

recorded to be USD (528 million). There are equipment leases and assets are held under

lease. This lead to group accepting all the risk considerably and rewards of various

ownerships can be capitalized as particularly plant, property as well as equipment (Scott

2015). Operating lease as mentioned in the report are not capitalised and payments for rent

are included in the income statement

Analysis of financial assertions as regards relevance as well as faithful representation

Schaltegger and Burritt (2017) suggests that characteristics of effective financial information

comprises of relevance together with faithful representation of specific information as regards

finances of business segments. Jessen et al. (2014) suggests that relevance point out towards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CONTEMPORARY ISSUES IN ACCOUNTING

financial information that aids in comprehending variations in diverse economic decisions.

Evaluation of financial information in the annual report of the corporation BHP Billiton aids

in comprehending variations in different financial decisions. Furthermore, faithful

representation of different economic occurrences is presented in numerical terms or else

narrative.

Review of fundamental qualitative enhancing features of financial assertion

As rightly indicated by Libby (2017), fundamental qualitative characteristics of monetary

information delivered in financial assertions take account of relevance together with faithful

representation of specific monetary information.

Relevance

As rightly indicated by Zhang and Andrew (2014), relevance of information in financial

statements can help in delivering economic decisions of a variety of users in case if that has

definite predictive value. Financial declaration presenting important information can assist in

evaluating variations in economic judgment. Furthermore, it necessarily takes in predictive

value aside from confirmatory value.

Faithful Representation

As correctly mentioned by Libby (2017), faithful representation helps in replicating economic

situations presented as a body of literature otherwise numerals. In order to be of use, financial

information in actual fact has the obligation to be both relevant and faithful representation.

Exhaustive analysis of financial declarations of financial assertions of the corporation BHP

Billiton states about a certain confidence level of consumers, diverse economic dimensions of

Australia, particular dimensions of growth, important information on partners of business

together with influence of worldwide business forces.

financial information that aids in comprehending variations in diverse economic decisions.

Evaluation of financial information in the annual report of the corporation BHP Billiton aids

in comprehending variations in different financial decisions. Furthermore, faithful

representation of different economic occurrences is presented in numerical terms or else

narrative.

Review of fundamental qualitative enhancing features of financial assertion

As rightly indicated by Libby (2017), fundamental qualitative characteristics of monetary

information delivered in financial assertions take account of relevance together with faithful

representation of specific monetary information.

Relevance

As rightly indicated by Zhang and Andrew (2014), relevance of information in financial

statements can help in delivering economic decisions of a variety of users in case if that has

definite predictive value. Financial declaration presenting important information can assist in

evaluating variations in economic judgment. Furthermore, it necessarily takes in predictive

value aside from confirmatory value.

Faithful Representation

As correctly mentioned by Libby (2017), faithful representation helps in replicating economic

situations presented as a body of literature otherwise numerals. In order to be of use, financial

information in actual fact has the obligation to be both relevant and faithful representation.

Exhaustive analysis of financial declarations of financial assertions of the corporation BHP

Billiton states about a certain confidence level of consumers, diverse economic dimensions of

Australia, particular dimensions of growth, important information on partners of business

together with influence of worldwide business forces.

12CONTEMPORARY ISSUES IN ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.