An Analysis of Contemporary Accounting Issues: Charter Hall Group

VerifiedAdded on 2020/04/15

|16

|2265

|258

Report

AI Summary

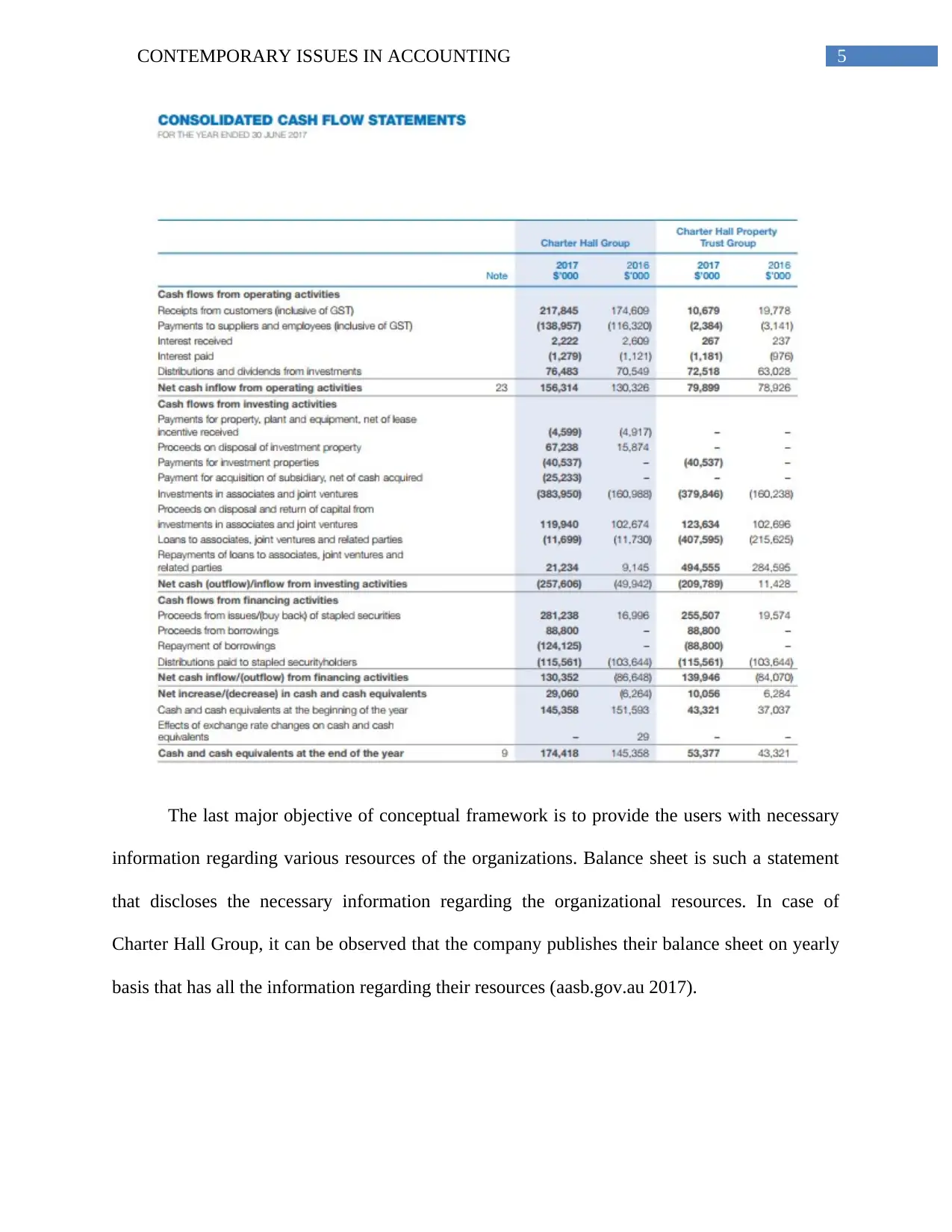

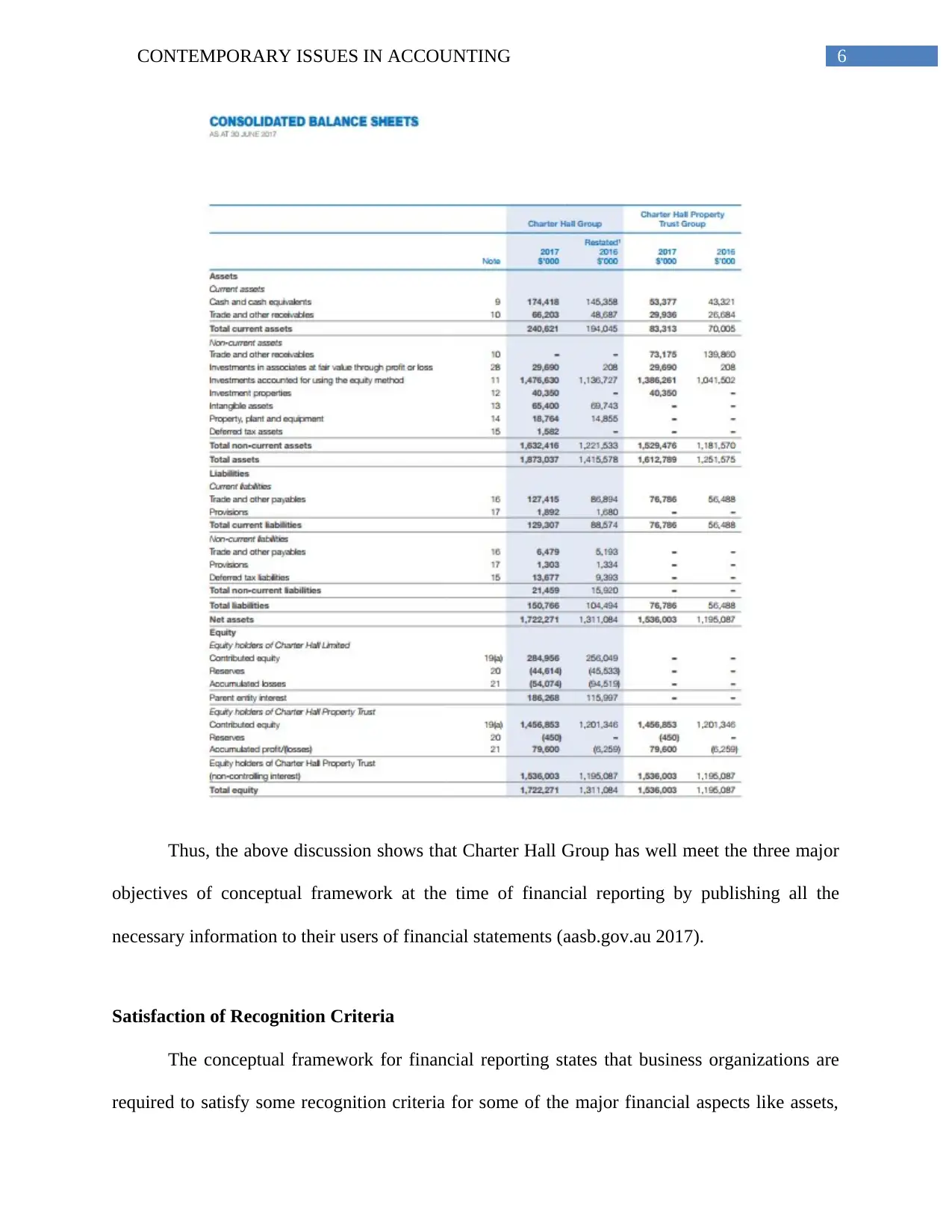

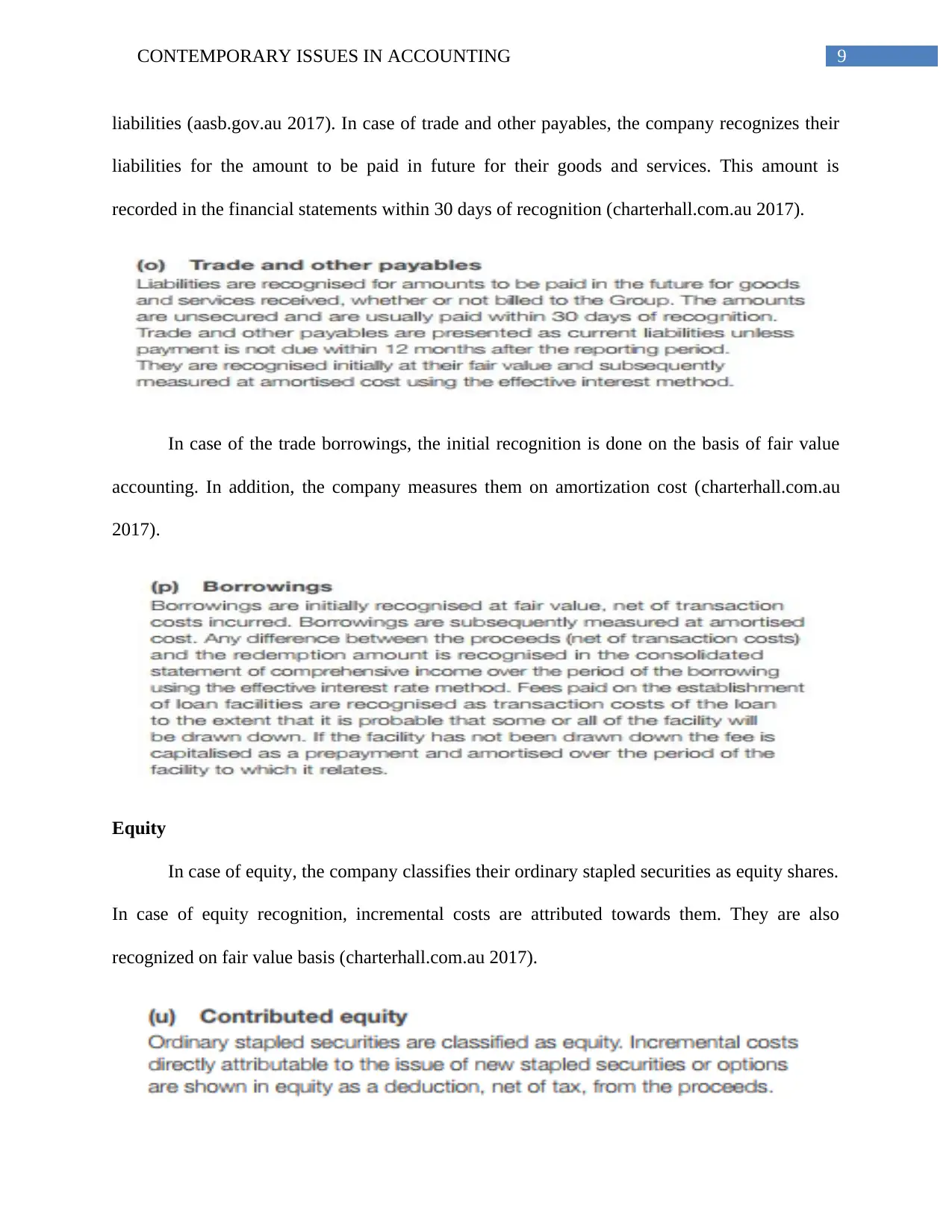

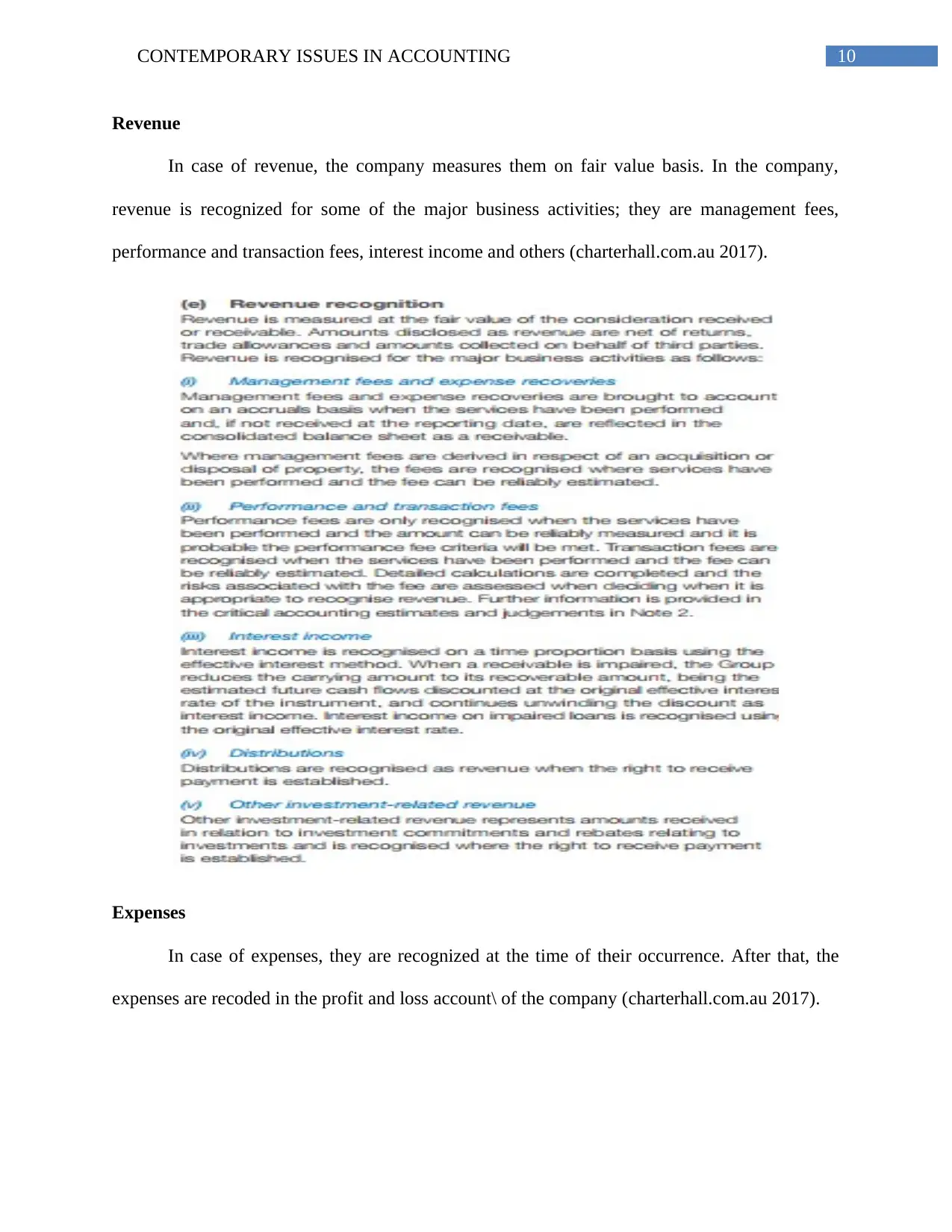

This report provides a detailed analysis of Charter Hall Group's financial reporting practices, focusing on its compliance with the Conceptual Framework for Financial Reporting. The study examines how Charter Hall Group meets the objectives of the framework, including providing useful information for decision-making and reporting on future cash flows and organizational resources. The report also assesses the company's adherence to recognition criteria for assets, liabilities, equity, revenue, and expenses, as well as its satisfaction of the fundamental qualitative characteristics of relevance, faithful representation, comparability, verifiability, timeliness, and understandability. The analysis draws on Charter Hall Group's annual reports and relevant accounting standards (AASB, IFRS, IASB, and Corporation Act 2001) to evaluate the quality and transparency of its financial reporting.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.