Exam 2 Solutions: Exploring Contemporary Issues in Accounting

VerifiedAdded on 2023/06/14

|9

|2219

|190

Quiz and Exam

AI Summary

This document presents solutions to an exam focused on contemporary issues in accounting. It covers topics such as earning management techniques (cookie jar reserves, big bath accounting, revenue recognition), cultural differences impacting accounting practices, the differences between rule-based and principle-based approaches to corporate governance, and how bonus plans can mitigate agency problems. It also discusses positive accounting theory, corporate social and environmental reporting, international accounting harmonization and convergence, and the distinction between capital market research and behavioral accounting research. Further, the solutions address the triple bottom line concept (profit, people, planet), the differences between positive and normative accounting theories, and the conceptual framework versus accounting standards, referencing relevant academic sources and online materials. This resource is designed to aid students in understanding and mastering these complex accounting concepts.

Exam 2 Contemporary Issues

in Accounting

in Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MAIN BODY...................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................4

Question 4...................................................................................................................................4

Question 5...................................................................................................................................5

Question 6...................................................................................................................................5

Question 7...................................................................................................................................6

Question 8...................................................................................................................................6

Question 9...................................................................................................................................6

Question 10.................................................................................................................................7

REFERENCES................................................................................................................................9

MAIN BODY...................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................4

Question 4...................................................................................................................................4

Question 5...................................................................................................................................5

Question 6...................................................................................................................................5

Question 7...................................................................................................................................6

Question 8...................................................................................................................................6

Question 9...................................................................................................................................6

Question 10.................................................................................................................................7

REFERENCES................................................................................................................................9

MAIN BODY

Question 1

The earning management is being defined as the use of different accounting techniques in

order to make the financial statement which provides an overly positive phase of the business.

there are different levels of earning management and this involves Level 1, Level 2 and new

market. Along with this there is also different types of methods and approaches which can be

used in order to implement the earning management in proper and effective manner. These

methods and approaches involves the following-

The first method is Cookie Jar reserve and in this comes under technique of aggressive

accounting. Under this technique the reserve is being created and when company face bad

situation at that time it is used.

Another technique is the big bath which is used when company faces loss due to bad

period because of external forces. In accordance to this technique, company makes the

situation worse by writing off all the bad debts, overvaluation of asset depreciation and

others.

Another technique of earning management is expense and revenue recognition which is

also known as income smoothing and this is part of fraudulent accounting. For example,

company can record its expenses before it actually occurs or even may show more sales

even it has not occurred in actual.

Question 2

There are different types of cultural aspect which differentiate among the different

countries. This is particularly because of the reason that every country has their own specific

cultures to be followed. Hence, this varies from country to country as their policy and accounting

structure are also different and because of this there is a difference within the accounting as well.

There are different variables which differentiates that cultural aspect across the countries like

level of education, personality, perception, attitude of the person, experience and others. Hence,

this affects the working of the accounting policies as well of the companies in different countries.

This is particularly because of the reason that many a times accounting process of different

countries are different. For example, the revenue recognition of one company is different in a

Question 1

The earning management is being defined as the use of different accounting techniques in

order to make the financial statement which provides an overly positive phase of the business.

there are different levels of earning management and this involves Level 1, Level 2 and new

market. Along with this there is also different types of methods and approaches which can be

used in order to implement the earning management in proper and effective manner. These

methods and approaches involves the following-

The first method is Cookie Jar reserve and in this comes under technique of aggressive

accounting. Under this technique the reserve is being created and when company face bad

situation at that time it is used.

Another technique is the big bath which is used when company faces loss due to bad

period because of external forces. In accordance to this technique, company makes the

situation worse by writing off all the bad debts, overvaluation of asset depreciation and

others.

Another technique of earning management is expense and revenue recognition which is

also known as income smoothing and this is part of fraudulent accounting. For example,

company can record its expenses before it actually occurs or even may show more sales

even it has not occurred in actual.

Question 2

There are different types of cultural aspect which differentiate among the different

countries. This is particularly because of the reason that every country has their own specific

cultures to be followed. Hence, this varies from country to country as their policy and accounting

structure are also different and because of this there is a difference within the accounting as well.

There are different variables which differentiates that cultural aspect across the countries like

level of education, personality, perception, attitude of the person, experience and others. Hence,

this affects the working of the accounting policies as well of the companies in different countries.

This is particularly because of the reason that many a times accounting process of different

countries are different. For example, the revenue recognition of one company is different in a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

country. On the other hand, this might be different in some other country and this can also affect

the working and the accounting of the company.

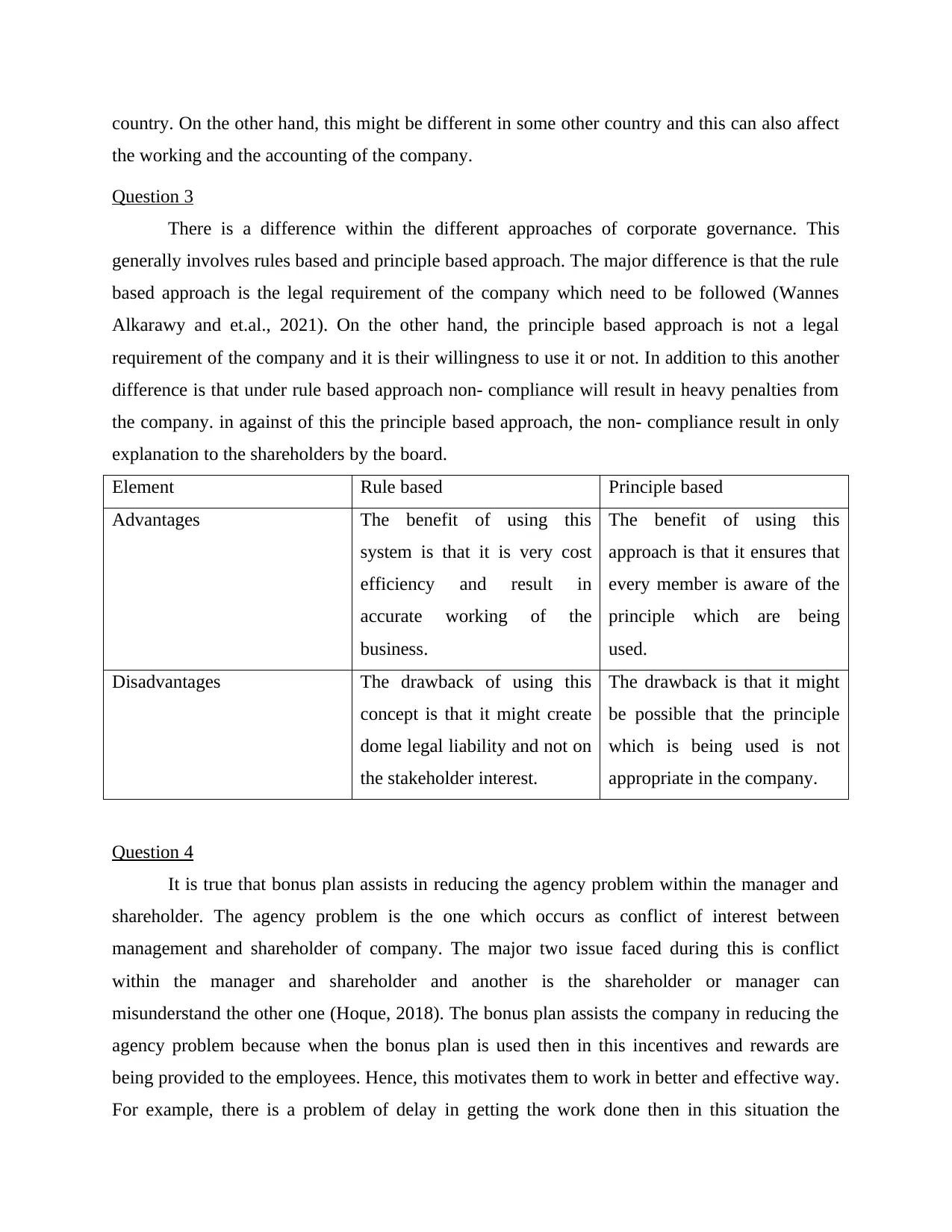

Question 3

There is a difference within the different approaches of corporate governance. This

generally involves rules based and principle based approach. The major difference is that the rule

based approach is the legal requirement of the company which need to be followed (Wannes

Alkarawy and et.al., 2021). On the other hand, the principle based approach is not a legal

requirement of the company and it is their willingness to use it or not. In addition to this another

difference is that under rule based approach non- compliance will result in heavy penalties from

the company. in against of this the principle based approach, the non- compliance result in only

explanation to the shareholders by the board.

Element Rule based Principle based

Advantages The benefit of using this

system is that it is very cost

efficiency and result in

accurate working of the

business.

The benefit of using this

approach is that it ensures that

every member is aware of the

principle which are being

used.

Disadvantages The drawback of using this

concept is that it might create

dome legal liability and not on

the stakeholder interest.

The drawback is that it might

be possible that the principle

which is being used is not

appropriate in the company.

Question 4

It is true that bonus plan assists in reducing the agency problem within the manager and

shareholder. The agency problem is the one which occurs as conflict of interest between

management and shareholder of company. The major two issue faced during this is conflict

within the manager and shareholder and another is the shareholder or manager can

misunderstand the other one (Hoque, 2018). The bonus plan assists the company in reducing the

agency problem because when the bonus plan is used then in this incentives and rewards are

being provided to the employees. Hence, this motivates them to work in better and effective way.

For example, there is a problem of delay in getting the work done then in this situation the

the working and the accounting of the company.

Question 3

There is a difference within the different approaches of corporate governance. This

generally involves rules based and principle based approach. The major difference is that the rule

based approach is the legal requirement of the company which need to be followed (Wannes

Alkarawy and et.al., 2021). On the other hand, the principle based approach is not a legal

requirement of the company and it is their willingness to use it or not. In addition to this another

difference is that under rule based approach non- compliance will result in heavy penalties from

the company. in against of this the principle based approach, the non- compliance result in only

explanation to the shareholders by the board.

Element Rule based Principle based

Advantages The benefit of using this

system is that it is very cost

efficiency and result in

accurate working of the

business.

The benefit of using this

approach is that it ensures that

every member is aware of the

principle which are being

used.

Disadvantages The drawback of using this

concept is that it might create

dome legal liability and not on

the stakeholder interest.

The drawback is that it might

be possible that the principle

which is being used is not

appropriate in the company.

Question 4

It is true that bonus plan assists in reducing the agency problem within the manager and

shareholder. The agency problem is the one which occurs as conflict of interest between

management and shareholder of company. The major two issue faced during this is conflict

within the manager and shareholder and another is the shareholder or manager can

misunderstand the other one (Hoque, 2018). The bonus plan assists the company in reducing the

agency problem because when the bonus plan is used then in this incentives and rewards are

being provided to the employees. Hence, this motivates them to work in better and effective way.

For example, there is a problem of delay in getting the work done then in this situation the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company or shareholder can give bonus or other incentive to the employees so that objective is

achieved and agency problem is being eradicated from the company. Another example is that

when there is some conflict in the thinking of shareholder and manager then here company must

find a mediate way to solve the problem in better and effective manner so that agency problem is

eradicated.

Question 5

The positive accounting theory is the one which highlights the importance of the

minimization of information asymmetry between the owners and managers. It can be said as the

presentation from the managers with mindful operations of both good and bad news which is

about the entity. The organizational impacts which affects the future of the shareholders are

explained in this theory (Srivastava and Baag, 2020). The corporate social and environmental

reporting is also known as the financial or the non-financial disclosure of the effects on the social

and environmental effects of the business. This is important for the organization for the

management of the business as it known as the voluntary activity. It helps in the being able to

explain and also predict the accounting practices which are related to social and environmental

reporting which is associated with the individual behaviour towards the selection of the

accounting methods for the maximization of their utility.

Question 6

In the international accounting harmonization is the analysation of the differences

between the national accounting rules and international accounting methods which are

considered to be effective in the management of the different adaptation which are required in

the accounting standards. This helps the accounts to achieve higher significance and positive

coefficients for the comparison of the firms which considers local accounting standards.

Convergence in the international accounting standards is referred to the goals of the

accounting towards the establishment of the single set of high level of accounting standards

which can be used internationally with relation to the efforts of the standards. This is used by the

standards setters towards the achievement of the discussed goals (Kotsupatriy and et.al., 2020).

The adaptation in the international accounting can also be said as the adaptation which

the business does towards the standards, countries and culture that affects the performance of the

emerging capital markets. In this several factors play a fundamental role towards the accounting

achieved and agency problem is being eradicated from the company. Another example is that

when there is some conflict in the thinking of shareholder and manager then here company must

find a mediate way to solve the problem in better and effective manner so that agency problem is

eradicated.

Question 5

The positive accounting theory is the one which highlights the importance of the

minimization of information asymmetry between the owners and managers. It can be said as the

presentation from the managers with mindful operations of both good and bad news which is

about the entity. The organizational impacts which affects the future of the shareholders are

explained in this theory (Srivastava and Baag, 2020). The corporate social and environmental

reporting is also known as the financial or the non-financial disclosure of the effects on the social

and environmental effects of the business. This is important for the organization for the

management of the business as it known as the voluntary activity. It helps in the being able to

explain and also predict the accounting practices which are related to social and environmental

reporting which is associated with the individual behaviour towards the selection of the

accounting methods for the maximization of their utility.

Question 6

In the international accounting harmonization is the analysation of the differences

between the national accounting rules and international accounting methods which are

considered to be effective in the management of the different adaptation which are required in

the accounting standards. This helps the accounts to achieve higher significance and positive

coefficients for the comparison of the firms which considers local accounting standards.

Convergence in the international accounting standards is referred to the goals of the

accounting towards the establishment of the single set of high level of accounting standards

which can be used internationally with relation to the efforts of the standards. This is used by the

standards setters towards the achievement of the discussed goals (Kotsupatriy and et.al., 2020).

The adaptation in the international accounting can also be said as the adaptation which

the business does towards the standards, countries and culture that affects the performance of the

emerging capital markets. In this several factors play a fundamental role towards the accounting

systems. This is also helpful for the business in the largely facilitating the acceptance of the

application of the new standards.

Question 7

The capital market research is that one which includes the research relating to

performance of company, valuation of securities and other accounting information. This research

particularly involves the research within the capital market and the relation between accounting

measures and capital market value. On the other hand, the behavioural accounting research is the

one which involves researching for behaviour beside the accounting knowledge (HASHIM and

et.al., 2021). This type of research assist in finding out how the person takes the decision and

communicate with others.

The major difference between both the type of research is that capital market research

particularly includes macro level research. on the other hand, behavioural market research

involves research at micro level only. The former includes analysis of aggregate of security

market whereas latter involves analysis of individual firm and manager.

Question 8

The triple bottom line is being referred to as the concept which every company need to

follow and use in order to get successful. The TBL involves the social and environmental

concerns which need to be considered at time of earning profit. The TBL theory involves the

three major element that is profit, people and planet. For the business to be successful it is

necessary that each of the three element is being used and followed by the company. this model

generally covers the social, financial and environmental aspect of working and as a result of this

there is overall development of the company and result in increasing profitability of the business.

this TBL is used in order to create a sustainable future which completely focuses on the

sustainability of the business. along with this the TBL is also beneficial because it will enhance

the brand image of the company and as a result of this company will be having a competitive

advantage.

Question 9

Positive accounting pay attention on attempting to describe accounting as it actually

conducted. Under positive accounting practices accountant concentrate on collecting and

analysing real data such as revenue and expenses of previous period (Positive and Normative

application of the new standards.

Question 7

The capital market research is that one which includes the research relating to

performance of company, valuation of securities and other accounting information. This research

particularly involves the research within the capital market and the relation between accounting

measures and capital market value. On the other hand, the behavioural accounting research is the

one which involves researching for behaviour beside the accounting knowledge (HASHIM and

et.al., 2021). This type of research assist in finding out how the person takes the decision and

communicate with others.

The major difference between both the type of research is that capital market research

particularly includes macro level research. on the other hand, behavioural market research

involves research at micro level only. The former includes analysis of aggregate of security

market whereas latter involves analysis of individual firm and manager.

Question 8

The triple bottom line is being referred to as the concept which every company need to

follow and use in order to get successful. The TBL involves the social and environmental

concerns which need to be considered at time of earning profit. The TBL theory involves the

three major element that is profit, people and planet. For the business to be successful it is

necessary that each of the three element is being used and followed by the company. this model

generally covers the social, financial and environmental aspect of working and as a result of this

there is overall development of the company and result in increasing profitability of the business.

this TBL is used in order to create a sustainable future which completely focuses on the

sustainability of the business. along with this the TBL is also beneficial because it will enhance

the brand image of the company and as a result of this company will be having a competitive

advantage.

Question 9

Positive accounting pay attention on attempting to describe accounting as it actually

conducted. Under positive accounting practices accountant concentrate on collecting and

analysing real data such as revenue and expenses of previous period (Positive and Normative

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting – What’s the Difference? 2022). This type of theory largely focuses on striving the

accounting for objectivity and having subjective parameters for having making assumptions. It

pays attention on analysing the economic statistics hand data in turn relevant information to

manage accounting practice can become possible. There are several companies which highlights

the positive accounting theory into its processes. On the other side, normative accounting theory

is related with focusing on the accounting as it should be done. It aims to describe accounting

that should be done via using subjective morality derived. This is basically based on the

observation that involves figuring out what principals should be applied to each situation by

offering number of choices. Accounting practice is as form of valuing he judgement that can

introduce morality into accounting. It helps investors or company to obtain the information

regarding the future course of action by involving future events rather than data. On the basis of

this it can be interpreted that these both are different.

Question 10

Conceptual framework is related with specific definitions for discussion of accounting

problems. It is the financial accounting theory that is related with body of sets standards to test

problems that are practical. This allows to get the information as plays role in issues that

concern financial reporting (Difference Between Conceptual Frameworks and Accounting

Standards, 2022). This assist the financial auditors and preparations for improving the

implementation of the IFRS regulations which is feature of the logical system that considered to

be versatile. On the other side, accounting standard is related h with defining specific financial

statements' credibility & reliability. It consists collection of public standards for identifying,

measuring, presenting h and disclosing facts contained in an n organization's financial statement.

These are rules that are stringent and not compatible with different financial accounting

perspective. There are fur main qualitative characteristics continue to be timeliness

understandability, verifiability and comparability. This is considered to be elements h of

financial statements that are recognition n and measurement of elements so that accurate

understanding can be obtained.

accounting for objectivity and having subjective parameters for having making assumptions. It

pays attention on analysing the economic statistics hand data in turn relevant information to

manage accounting practice can become possible. There are several companies which highlights

the positive accounting theory into its processes. On the other side, normative accounting theory

is related with focusing on the accounting as it should be done. It aims to describe accounting

that should be done via using subjective morality derived. This is basically based on the

observation that involves figuring out what principals should be applied to each situation by

offering number of choices. Accounting practice is as form of valuing he judgement that can

introduce morality into accounting. It helps investors or company to obtain the information

regarding the future course of action by involving future events rather than data. On the basis of

this it can be interpreted that these both are different.

Question 10

Conceptual framework is related with specific definitions for discussion of accounting

problems. It is the financial accounting theory that is related with body of sets standards to test

problems that are practical. This allows to get the information as plays role in issues that

concern financial reporting (Difference Between Conceptual Frameworks and Accounting

Standards, 2022). This assist the financial auditors and preparations for improving the

implementation of the IFRS regulations which is feature of the logical system that considered to

be versatile. On the other side, accounting standard is related h with defining specific financial

statements' credibility & reliability. It consists collection of public standards for identifying,

measuring, presenting h and disclosing facts contained in an n organization's financial statement.

These are rules that are stringent and not compatible with different financial accounting

perspective. There are fur main qualitative characteristics continue to be timeliness

understandability, verifiability and comparability. This is considered to be elements h of

financial statements that are recognition n and measurement of elements so that accurate

understanding can be obtained.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Srivastava, J. and Baag, P. K., 2020. Positive accounting theory and agency costs: A critical

perspective.AIMS International. 2. pp.101-113.

Kotsupatriy, M., and et.al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management. 11(5).

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Wannes Alkarawy, H.G., and et.al., 2021. Approach to the assessment of the financial and

accounting risks with digital economy conditions for projects (representation). Journal

of Contemporary Issues in Business & Government, 27(5).

HASHIM, F.H.M., and et.al., 2021. Forensic Accounting Skills and the Effective Identification

in Money Laundering Activities–Transaction Monitoring Perspective. Journal of

Contemporary Issues in Business and Government| Vol, 27(2), p.60.

Online

Positive and Normative Accounting – What’s the Difference? 2022. [Online]. Available

through: <http://www.aspiringaccountants.co.uk/positive-normative-accounting/>

Difference Between Conceptual Frameworks and Accounting Standards. 2022. [Online].

Available through: <https://askanydifference.com/difference-between-conceptual-

frameworks-and-accounting-standards/#:~:text=Main%20Differences%20Between

%20Conceptual%20Frameworks,financial%20statements'%20credibility%20and

%20reliability.>

Books and Journals

Srivastava, J. and Baag, P. K., 2020. Positive accounting theory and agency costs: A critical

perspective.AIMS International. 2. pp.101-113.

Kotsupatriy, M., and et.al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management. 11(5).

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Wannes Alkarawy, H.G., and et.al., 2021. Approach to the assessment of the financial and

accounting risks with digital economy conditions for projects (representation). Journal

of Contemporary Issues in Business & Government, 27(5).

HASHIM, F.H.M., and et.al., 2021. Forensic Accounting Skills and the Effective Identification

in Money Laundering Activities–Transaction Monitoring Perspective. Journal of

Contemporary Issues in Business and Government| Vol, 27(2), p.60.

Online

Positive and Normative Accounting – What’s the Difference? 2022. [Online]. Available

through: <http://www.aspiringaccountants.co.uk/positive-normative-accounting/>

Difference Between Conceptual Frameworks and Accounting Standards. 2022. [Online].

Available through: <https://askanydifference.com/difference-between-conceptual-

frameworks-and-accounting-standards/#:~:text=Main%20Differences%20Between

%20Conceptual%20Frameworks,financial%20statements'%20credibility%20and

%20reliability.>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.