Contemporary Accounting Issue Report: Climate Change and Agency Theory

VerifiedAdded on 2020/03/01

|10

|2074

|147

Report

AI Summary

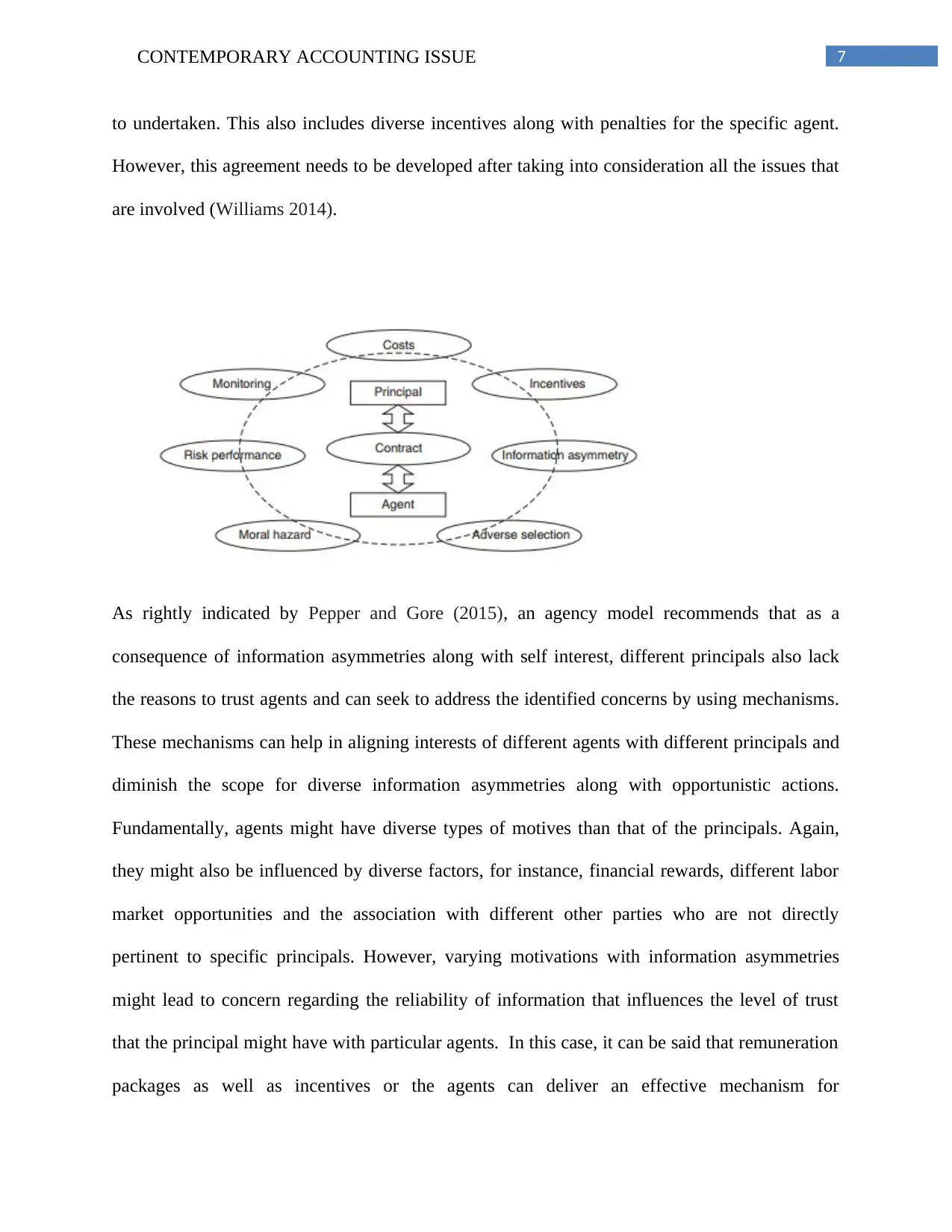

This report delves into the contemporary accounting issue of climate change, examining its implications through the framework of agency theory. It explores how carbon emissions and environmental factors affect financial statements and corporate governance. The study highlights the principal-agent relationship, particularly focusing on the roles of accountants, managers, and auditors in addressing climate-related risks. The report discusses practical and theoretical motivations, reviews relevant literature, and proposes hypotheses regarding target slack and performance-based incentives. It emphasizes the importance of understanding climate change's economic aspects, conducting cost-benefit analyses, and ensuring the reliability of financial information through audits. The analysis includes discussions on moral hazard, information asymmetry, and the role of contracts in mitigating agency problems. The report concludes by outlining the hypotheses for the study, which investigate the relationship between target slack and factors such as the initial setting of targets and the presence of performance-based incentives.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.