Accounting Report: Analysis of A1 Investment and Resources Ltd

VerifiedAdded on 2023/04/20

|12

|2486

|70

Report

AI Summary

This report provides a detailed analysis of A1 Investment and Resources Ltd's financial report, focusing on its adherence to the conceptual framework and accounting standards. The report examines the company's compliance with IFRS and AASB regulations, evaluating the relevance and faithful representation of its financial statements. It also assesses the company's performance based on the fundamental and enhancing qualitative characteristics, including comparability, understandability, and timeliness. The analysis covers the users of financial information, the importance of financial statements, and the need for a basic understanding of accounting. The report concludes that A1 Investment and Resources Ltd effectively meets the requirements of the conceptual framework, providing valuable insights for decision-making. The report uses the company's annual report to illustrate the concepts discussed, offering a practical application of accounting principles.

qwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklz

CONTEMPORARY ISSUES IN

ACCOUNTING

uiopasdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmrtyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklz

CONTEMPORARY ISSUES IN

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A1 Investment and Resources Ltd

Abstract

The report is primarily based on the Australian company that is A1 Investment and Resources

Ltd, and a strong critical analysis is undertaken for the company. Such an analysis helps to

know about the effectiveness of the company in tune to the conceptual framework. The main

stress of the report is on the basic elements of the conceptual framework where a strong

understanding is gathered in respect of the company A1 Investment and Resources Ltd. The

report starts with the introduction followed by the major areas of the conceptual framework

and other characteristics.

2

Abstract

The report is primarily based on the Australian company that is A1 Investment and Resources

Ltd, and a strong critical analysis is undertaken for the company. Such an analysis helps to

know about the effectiveness of the company in tune to the conceptual framework. The main

stress of the report is on the basic elements of the conceptual framework where a strong

understanding is gathered in respect of the company A1 Investment and Resources Ltd. The

report starts with the introduction followed by the major areas of the conceptual framework

and other characteristics.

2

A1 Investment and Resources Ltd

Contents

Introduction...........................................................................................................................................3

Requirements of the conceptual framework.........................................................................................3

Fundamental qualitative characteristics................................................................................................5

Enhancing qualitative characteristics....................................................................................................6

The user of financial information..........................................................................................................7

The user needs a basic knowledge of accounting..................................................................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

3

Contents

Introduction...........................................................................................................................................3

Requirements of the conceptual framework.........................................................................................3

Fundamental qualitative characteristics................................................................................................5

Enhancing qualitative characteristics....................................................................................................6

The user of financial information..........................................................................................................7

The user needs a basic knowledge of accounting..................................................................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A1 Investment and Resources Ltd

Introduction

When it comes to the concept of the conceptual framework it needs to be noted that it plays a

predominant part in the presentation, as well as preparation of financial statement for the

users so that they can be assisted in undertaking useful decision. Decision making is enriched

through the concept of CF as it leads to a formidable foundation. Therefore, it is vital that it

provides them with the knowledge to understand the pitfall of financial reporting. Moreover,

to make amend with the need of the conceptual framework, the IASB has provided various

characteristics of qualitative nature such as materiality, reliability, etc. that needs to be

fulfilled by every company. Moreover, the framework even presents a criterion of

recognition that needs to be met so that the reporting of assets, liabilities, expenses can be

projected in a well-defined manner. For the main aim of the report, the annual report of A1

Investment & Resources Ltd has been selected, and the report will consider whether the

company met with the specifications of the CF.

Requirements of the conceptual framework

As per the report of the A1 Investment and Resources Ltd, it can be commented that the

annual report is in tune to the rules and regulations defined by the IFRS. Moreover, it is even

noted that the financial statements adhere to the Article 4 of the IAS Regulation and the

Companies Act 2006 that helps the IASB in the establishment of consistent and strong

accounting. Furthermore, it can be commented that depending on the AASB, the financial

statements of the company projects a real view of the performance that indicates the company

adhered to the conceptual framework objectives (Conceptual Framework, 2016). It even

needs to be noted that directors report is properly linked to the financial statement disclosure

and that plays a vital role in understanding the aim and limitation of the financial reporting.

Therefore, it can be commented that annual report of A1 Investment & Resources Ltd is as

per the obligation of the company and the presentation, as well as preparation, is entire as per

the Corporation Act 2001 of Australia (A1 Investment and Resources, 2016). This is a clear

indication that the company has met with the requirements and that denotes the strong

management of the company.

4

Introduction

When it comes to the concept of the conceptual framework it needs to be noted that it plays a

predominant part in the presentation, as well as preparation of financial statement for the

users so that they can be assisted in undertaking useful decision. Decision making is enriched

through the concept of CF as it leads to a formidable foundation. Therefore, it is vital that it

provides them with the knowledge to understand the pitfall of financial reporting. Moreover,

to make amend with the need of the conceptual framework, the IASB has provided various

characteristics of qualitative nature such as materiality, reliability, etc. that needs to be

fulfilled by every company. Moreover, the framework even presents a criterion of

recognition that needs to be met so that the reporting of assets, liabilities, expenses can be

projected in a well-defined manner. For the main aim of the report, the annual report of A1

Investment & Resources Ltd has been selected, and the report will consider whether the

company met with the specifications of the CF.

Requirements of the conceptual framework

As per the report of the A1 Investment and Resources Ltd, it can be commented that the

annual report is in tune to the rules and regulations defined by the IFRS. Moreover, it is even

noted that the financial statements adhere to the Article 4 of the IAS Regulation and the

Companies Act 2006 that helps the IASB in the establishment of consistent and strong

accounting. Furthermore, it can be commented that depending on the AASB, the financial

statements of the company projects a real view of the performance that indicates the company

adhered to the conceptual framework objectives (Conceptual Framework, 2016). It even

needs to be noted that directors report is properly linked to the financial statement disclosure

and that plays a vital role in understanding the aim and limitation of the financial reporting.

Therefore, it can be commented that annual report of A1 Investment & Resources Ltd is as

per the obligation of the company and the presentation, as well as preparation, is entire as per

the Corporation Act 2001 of Australia (A1 Investment and Resources, 2016). This is a clear

indication that the company has met with the requirements and that denotes the strong

management of the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A1 Investment and Resources Ltd

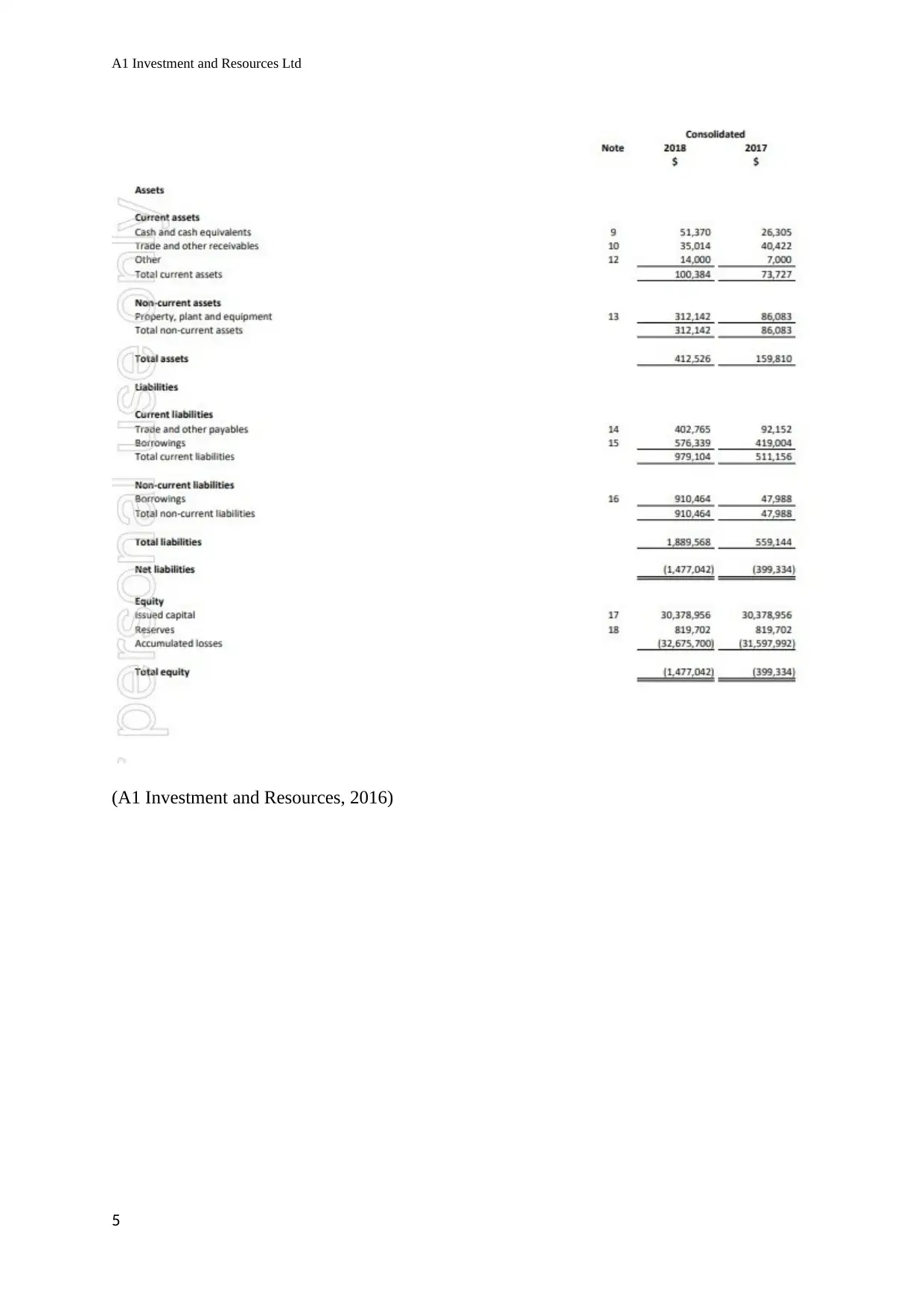

(A1 Investment and Resources, 2016)

5

(A1 Investment and Resources, 2016)

5

A1 Investment and Resources Ltd

Fundamental qualitative characteristics

As per relevance, it can be commented that the company has provided a deep-rooted financial

indication to the users in terms of the company’s performance. For instance, the company has

provided information in tune to the earnings that are underlying in the current year and the

same has been compared with the previous year so that the changes can be done in such a

segment (Seilber, 2015). Hence, with such a comparison, the users can judge whether the

company is able to perform in an effective manner. Another important point that should be

considered is that the company has considered both financial and non-financial features of the

conceptual framework so that it can satisfy the quality of relevance when it comes to

6

Fundamental qualitative characteristics

As per relevance, it can be commented that the company has provided a deep-rooted financial

indication to the users in terms of the company’s performance. For instance, the company has

provided information in tune to the earnings that are underlying in the current year and the

same has been compared with the previous year so that the changes can be done in such a

segment (Seilber, 2015). Hence, with such a comparison, the users can judge whether the

company is able to perform in an effective manner. Another important point that should be

considered is that the company has considered both financial and non-financial features of the

conceptual framework so that it can satisfy the quality of relevance when it comes to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A1 Investment and Resources Ltd

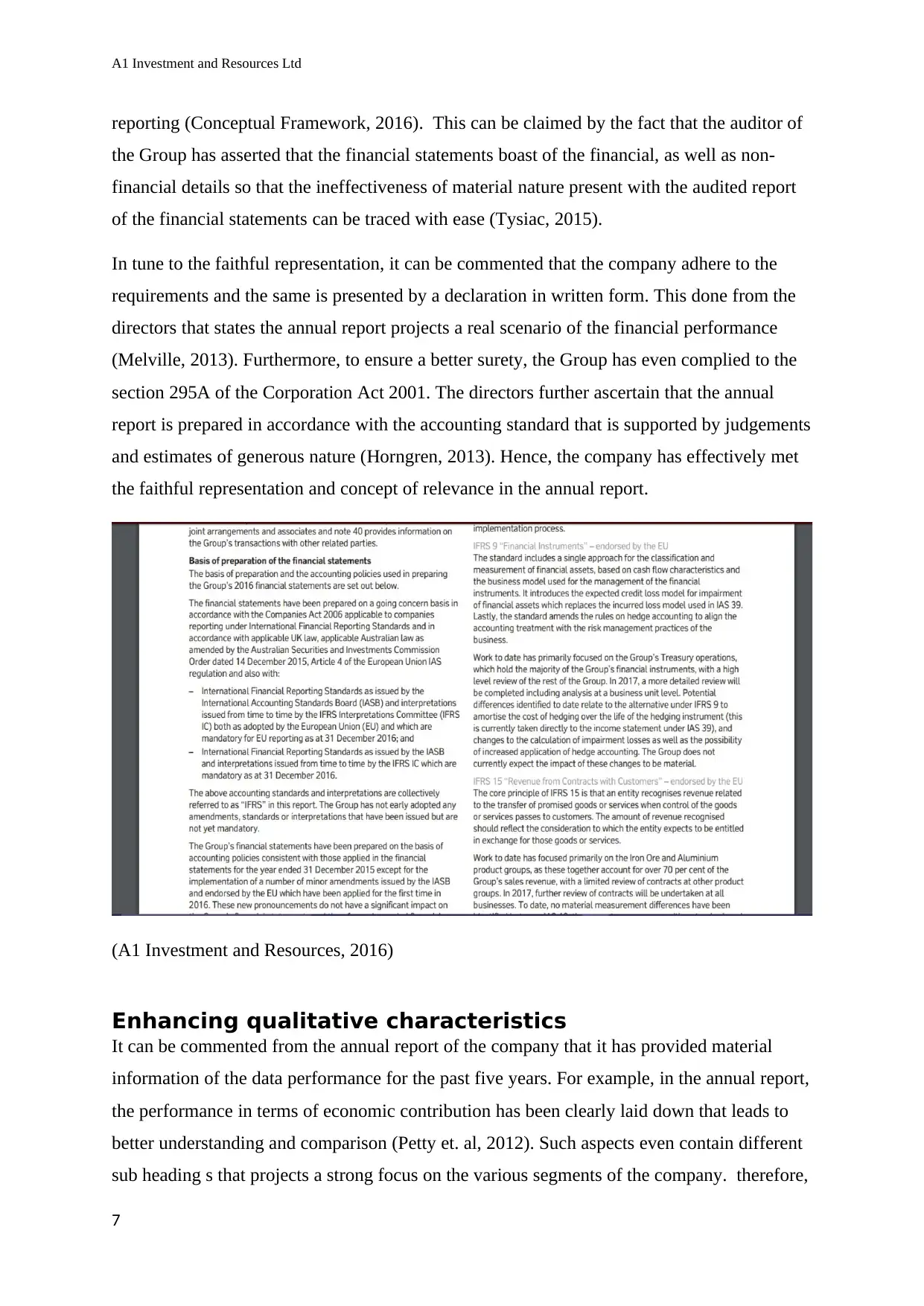

reporting (Conceptual Framework, 2016). This can be claimed by the fact that the auditor of

the Group has asserted that the financial statements boast of the financial, as well as non-

financial details so that the ineffectiveness of material nature present with the audited report

of the financial statements can be traced with ease (Tysiac, 2015).

In tune to the faithful representation, it can be commented that the company adhere to the

requirements and the same is presented by a declaration in written form. This done from the

directors that states the annual report projects a real scenario of the financial performance

(Melville, 2013). Furthermore, to ensure a better surety, the Group has even complied to the

section 295A of the Corporation Act 2001. The directors further ascertain that the annual

report is prepared in accordance with the accounting standard that is supported by judgements

and estimates of generous nature (Horngren, 2013). Hence, the company has effectively met

the faithful representation and concept of relevance in the annual report.

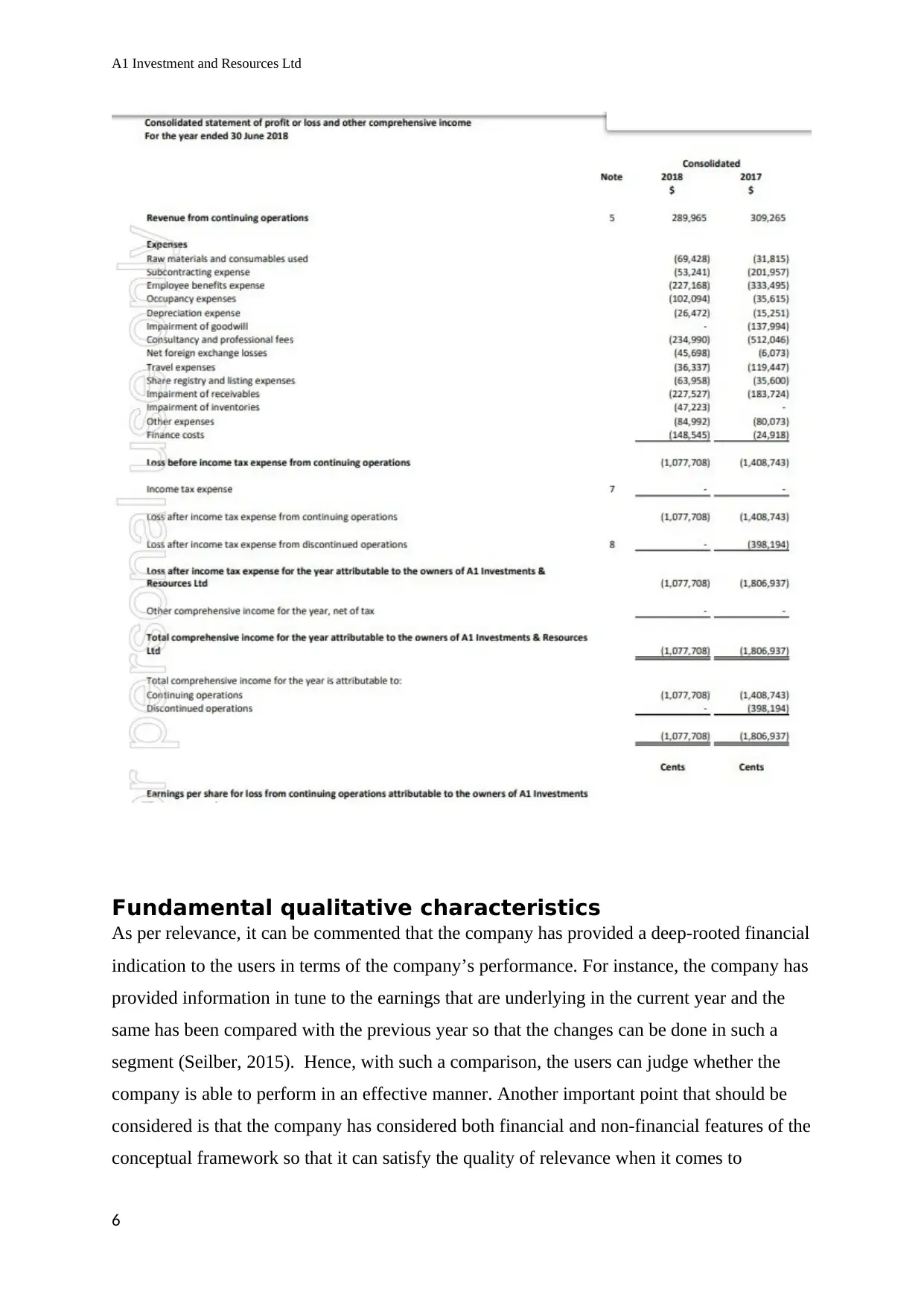

(A1 Investment and Resources, 2016)

Enhancing qualitative characteristics

It can be commented from the annual report of the company that it has provided material

information of the data performance for the past five years. For example, in the annual report,

the performance in terms of economic contribution has been clearly laid down that leads to

better understanding and comparison (Petty et. al, 2012). Such aspects even contain different

sub heading s that projects a strong focus on the various segments of the company. therefore,

7

reporting (Conceptual Framework, 2016). This can be claimed by the fact that the auditor of

the Group has asserted that the financial statements boast of the financial, as well as non-

financial details so that the ineffectiveness of material nature present with the audited report

of the financial statements can be traced with ease (Tysiac, 2015).

In tune to the faithful representation, it can be commented that the company adhere to the

requirements and the same is presented by a declaration in written form. This done from the

directors that states the annual report projects a real scenario of the financial performance

(Melville, 2013). Furthermore, to ensure a better surety, the Group has even complied to the

section 295A of the Corporation Act 2001. The directors further ascertain that the annual

report is prepared in accordance with the accounting standard that is supported by judgements

and estimates of generous nature (Horngren, 2013). Hence, the company has effectively met

the faithful representation and concept of relevance in the annual report.

(A1 Investment and Resources, 2016)

Enhancing qualitative characteristics

It can be commented from the annual report of the company that it has provided material

information of the data performance for the past five years. For example, in the annual report,

the performance in terms of economic contribution has been clearly laid down that leads to

better understanding and comparison (Petty et. al, 2012). Such aspects even contain different

sub heading s that projects a strong focus on the various segments of the company. therefore,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A1 Investment and Resources Ltd

the information can be compared easily from one year to another so that it can be clearly

ascertained whether the company is performing to the best of its abilities. Hence, it is proved

that the company has met with the comparability feature of the CF in its annual report.

Thereafter, the company has an adequate procedure of verification in movements that help in

detection of the material error if the data of the previous year is not correctly provided so that

the comparability feature is not disturbed (Parrino et. al, 2012). Furthermore, if the

information can be compared easily, then it can be verified whether the segments of the

company is performing in an effective manner.

When it comes to the timely information, then it can be commented that the director of A1

investment & Resources Ltd attain the information in a timely manner so that the fulfillment

of duties can be done in an effective manner. This projects that the directors are able to grab

the information in a timely manner so that the responsibilities are smoothly performed. This

even helps them in reporting the information to the financial statement users hence

completing the process of strong decision making (Deegan, 2011). Furthermore, the

company understands the concept of timely information that is in tune with the stakeholders

that ensures all the disclosures has been done in tune to understandability. It can be visualized

through the company’s performance indicators that the reporting has been done in a simple

manner that helps in taking effective decision making. Hence, the information projects the

concept of understandability (Gowthrope, 2011). Overall, the enhancing qualitative

characteristics of the conceptual framework have effectively complied.

The user of financial information

Yes, the users of the financial report are able to use the report in taking a valid decision. The

three financial reports that are used by the financial users are the balance sheet, the income

statement and the Cash Flow statement. The financial report is accurate and is in tune with

the accounting standards thereby helping in taking valid decisions.

The Balance Sheet

The balance sheet projects the financial balances that are the assets, liabilities and the

company’s equity. The strength of the company and the working capital days can be easily

ascertained with the help of it. This means that financial users can easily ascertain the

manner in which the company can handle alterations in revenue while staying in business

(Hamilton, Hyland & Dodd, 2011). Balance sheet even helps in identification of the trend

8

the information can be compared easily from one year to another so that it can be clearly

ascertained whether the company is performing to the best of its abilities. Hence, it is proved

that the company has met with the comparability feature of the CF in its annual report.

Thereafter, the company has an adequate procedure of verification in movements that help in

detection of the material error if the data of the previous year is not correctly provided so that

the comparability feature is not disturbed (Parrino et. al, 2012). Furthermore, if the

information can be compared easily, then it can be verified whether the segments of the

company is performing in an effective manner.

When it comes to the timely information, then it can be commented that the director of A1

investment & Resources Ltd attain the information in a timely manner so that the fulfillment

of duties can be done in an effective manner. This projects that the directors are able to grab

the information in a timely manner so that the responsibilities are smoothly performed. This

even helps them in reporting the information to the financial statement users hence

completing the process of strong decision making (Deegan, 2011). Furthermore, the

company understands the concept of timely information that is in tune with the stakeholders

that ensures all the disclosures has been done in tune to understandability. It can be visualized

through the company’s performance indicators that the reporting has been done in a simple

manner that helps in taking effective decision making. Hence, the information projects the

concept of understandability (Gowthrope, 2011). Overall, the enhancing qualitative

characteristics of the conceptual framework have effectively complied.

The user of financial information

Yes, the users of the financial report are able to use the report in taking a valid decision. The

three financial reports that are used by the financial users are the balance sheet, the income

statement and the Cash Flow statement. The financial report is accurate and is in tune with

the accounting standards thereby helping in taking valid decisions.

The Balance Sheet

The balance sheet projects the financial balances that are the assets, liabilities and the

company’s equity. The strength of the company and the working capital days can be easily

ascertained with the help of it. This means that financial users can easily ascertain the

manner in which the company can handle alterations in revenue while staying in business

(Hamilton, Hyland & Dodd, 2011). Balance sheet even helps in identification of the trend

8

A1 Investment and Resources Ltd

that is prevalent such as the receivable cycle and how the net profit is being utilized and how

often the equipment is replaced.

The Income Statement

The income statement projects the revenue, as well as expenses of the company during a

specified period of time. The main aim of an income statement is to help the users of the

financial statements in knowing about the sales, expenses and the profit and loss.

The Cash Flow Statement

The Cash Flow Statement projects the inflow, as well as outflow of cash during a specified

time span. Such movement of money will help in the accountability of the operation,

investment and financial activities. The users of the income statement can help in getting

strong information of the company’s skills to generate cash so that a healthy business can be

maintained (Hamilton, Hyland & Dodd, 2011). The users can gather up to date reporting in

terms of reduction of costs, the increment in sales, enhance profitability, allocation of human

resources, etc. The financial statements are important because it provides ample information

in terms of decision making and the trend can be interpreted from the financial report.

Therefore, the financial users of the report use it as a guide in terms of the economic decision

making process, and it strives to aid in the concept of forecasting. From the financial

statements, a strong understanding in terms of business practices and market trends can be

gathered with ease and flexibility (Kieso et. al,, 2010).

The user needs a basic knowledge of accounting

The conceptual framework is correct in the regard because that user needs a basic knowledge

of accounting. The financial reports are available and provided in the annual report that can

be easily accessed by the users. The users need a simple knowledge of accounting that can be

used for the interpretation. There are various manner and mechanism that can be used in the

process of interpretation. A simple knowledge in this regard helps in knowing about the

status of the company. The Conceptual framework sets the concepts and notion that helps in

underlying as well as interpreting the financial statements (Gibson, 2010). Hence, going by

the overall discussion, it can be commented that simple knowledge in this regard can help in

ensuring a smooth activity. As the report of the two years are provided in the annual report,

and that can be used for differentiation and getting a knowledge of the actual performance of

the two years. The same can be used to differentiate in terms of percentage type.

9

that is prevalent such as the receivable cycle and how the net profit is being utilized and how

often the equipment is replaced.

The Income Statement

The income statement projects the revenue, as well as expenses of the company during a

specified period of time. The main aim of an income statement is to help the users of the

financial statements in knowing about the sales, expenses and the profit and loss.

The Cash Flow Statement

The Cash Flow Statement projects the inflow, as well as outflow of cash during a specified

time span. Such movement of money will help in the accountability of the operation,

investment and financial activities. The users of the income statement can help in getting

strong information of the company’s skills to generate cash so that a healthy business can be

maintained (Hamilton, Hyland & Dodd, 2011). The users can gather up to date reporting in

terms of reduction of costs, the increment in sales, enhance profitability, allocation of human

resources, etc. The financial statements are important because it provides ample information

in terms of decision making and the trend can be interpreted from the financial report.

Therefore, the financial users of the report use it as a guide in terms of the economic decision

making process, and it strives to aid in the concept of forecasting. From the financial

statements, a strong understanding in terms of business practices and market trends can be

gathered with ease and flexibility (Kieso et. al,, 2010).

The user needs a basic knowledge of accounting

The conceptual framework is correct in the regard because that user needs a basic knowledge

of accounting. The financial reports are available and provided in the annual report that can

be easily accessed by the users. The users need a simple knowledge of accounting that can be

used for the interpretation. There are various manner and mechanism that can be used in the

process of interpretation. A simple knowledge in this regard helps in knowing about the

status of the company. The Conceptual framework sets the concepts and notion that helps in

underlying as well as interpreting the financial statements (Gibson, 2010). Hence, going by

the overall discussion, it can be commented that simple knowledge in this regard can help in

ensuring a smooth activity. As the report of the two years are provided in the annual report,

and that can be used for differentiation and getting a knowledge of the actual performance of

the two years. The same can be used to differentiate in terms of percentage type.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A1 Investment and Resources Ltd

Conclusion

After the assessment of Investment and Resources Ltd, it can be commented that the

company has adhered to the conceptual framework in the annual report. For such an instance,

the company has effectively met with the criteria of recognition in the annual report.

Moreover, the objectives of the conceptual framework have been effectively meeting. For this

instance, the company has adhered to the fundamental and enhancing qualitative

characteristic of corporate reporting that helps the user in taking an effective decision.

10

Conclusion

After the assessment of Investment and Resources Ltd, it can be commented that the

company has adhered to the conceptual framework in the annual report. For such an instance,

the company has effectively met with the criteria of recognition in the annual report.

Moreover, the objectives of the conceptual framework have been effectively meeting. For this

instance, the company has adhered to the fundamental and enhancing qualitative

characteristic of corporate reporting that helps the user in taking an effective decision.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A1 Investment and Resources Ltd

References

A1 Investment and Resources. (2016) A1 Investment and Resources 2016. Available from:

http://www.riotinto.com/documents/RT_2016_Annual_report.pdf [Accessed 21 December

2018]

Conceptual Framework. (2016) Conceptual Framework Pronouncements. Available from:

http://www.aasb.gov.au/Pronouncements/Conceptual-framework.aspx [Accessed 21

December 2018]

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Everingham, G.K, Kleynhans, J.E & Posthumus, L.C. (2007) Principles of Generally

Accepted Accounting Practice. Juta and Company Ltd.

Gibson, C. (2010) Financial Reporting and Analysis: Using Financial Accounting

Information, Cengage Learning.

Gowthrope, C. (2011) Business accounting and finance for non specialists (3rd ed.). South

Western

Hamilton, K., Hyland, B. and Dodd, J. L. (2011) Impairment: IASB-FASB Comparison.

Drake Management Review. [online]. 1(1), p. 55–67. Available from:

https://pdfs.semanticscholar.org/8d8f/5fd070193d6fa52e79d1dee9cc6632159d8a.pdf

[Accessed 21 December 2018]

Horngren, C. (2013) Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Kieso, D., Weygandt, J., Warfield, T; Young, N. and Wiecek, I . (2010) Intermediate

accounting. Toronto: John Wiley & Sons Canada.

Melville, A. (2013) International Financial Reporting – A Practical Guide, Pearson,

Education Limited, UK

Parrino, R., Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance, Hoboken,

NJ: Wiley

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

11

References

A1 Investment and Resources. (2016) A1 Investment and Resources 2016. Available from:

http://www.riotinto.com/documents/RT_2016_Annual_report.pdf [Accessed 21 December

2018]

Conceptual Framework. (2016) Conceptual Framework Pronouncements. Available from:

http://www.aasb.gov.au/Pronouncements/Conceptual-framework.aspx [Accessed 21

December 2018]

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Everingham, G.K, Kleynhans, J.E & Posthumus, L.C. (2007) Principles of Generally

Accepted Accounting Practice. Juta and Company Ltd.

Gibson, C. (2010) Financial Reporting and Analysis: Using Financial Accounting

Information, Cengage Learning.

Gowthrope, C. (2011) Business accounting and finance for non specialists (3rd ed.). South

Western

Hamilton, K., Hyland, B. and Dodd, J. L. (2011) Impairment: IASB-FASB Comparison.

Drake Management Review. [online]. 1(1), p. 55–67. Available from:

https://pdfs.semanticscholar.org/8d8f/5fd070193d6fa52e79d1dee9cc6632159d8a.pdf

[Accessed 21 December 2018]

Horngren, C. (2013) Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Kieso, D., Weygandt, J., Warfield, T; Young, N. and Wiecek, I . (2010) Intermediate

accounting. Toronto: John Wiley & Sons Canada.

Melville, A. (2013) International Financial Reporting – A Practical Guide, Pearson,

Education Limited, UK

Parrino, R., Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance, Hoboken,

NJ: Wiley

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

11

A1 Investment and Resources Ltd

Seilber J. (2015) FASB removes concept of extraordinary, retains guidance on unusual item.

Available from: http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-01-fasb-

extraordinary-unusual-items.pdf [Accessed 21 December 2018]

Tysiac K. (2015) No more extraordinary items: FASB simplifies GAAP. Available from:

http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html [Accessed 21 December 2018]

12

Seilber J. (2015) FASB removes concept of extraordinary, retains guidance on unusual item.

Available from: http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-01-fasb-

extraordinary-unusual-items.pdf [Accessed 21 December 2018]

Tysiac K. (2015) No more extraordinary items: FASB simplifies GAAP. Available from:

http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html [Accessed 21 December 2018]

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.