Research Proposal: Contemporary Issues in Accounting and Environment

VerifiedAdded on 2020/02/23

|12

|2718

|272

Report

AI Summary

This research proposal explores the impact of environmental sustainability on contemporary accounting practices. It investigates the effects of increasing carbon radiation on financial and non-financial performance, emphasizing the role of corporate social responsibility (CSR) and stakeholder theory. The report examines the practical and theoretical motivations for environmental protection, reviewing literature on greenhouse gases, carbon emissions, and their impact on financial aspects of companies. The study proposes hypotheses related to the relationship between carbon radiation and financial performance, as well as the role of stakeholders in promoting environmental sustainability. The proposal outlines a conceptual framework that considers various stakeholders, including employees, government, and owners, and their contributions to environmental sustainability and the reduction of carbon emissions. It aims to provide insights into how companies can manage environmental aspects, reduce carbon emissions, and improve their financial positions through sustainable practices. The report highlights the importance of financial analysts in managing funds related to environmental sustainability efforts.

CONTEMPORARY ISSUES IN ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACKNOWLEDGEMENT

I acknowledge that all the policies related with academic misconduct are properly being

understood and followed by me while developing this research proposal. The content developed

for this report by me is original which is not related with other individual’s ideas. However, the

ideas which were expressed by others are properly references in the assignment.

I acknowledge that all the policies related with academic misconduct are properly being

understood and followed by me while developing this research proposal. The content developed

for this report by me is original which is not related with other individual’s ideas. However, the

ideas which were expressed by others are properly references in the assignment.

TABLE OF CONTENTS

ACKNOWLEDGEMENT...............................................................................................................2

INTRODUCTION...........................................................................................................................4

PRACTICAL MOTIVATION.........................................................................................................5

THEORETICAL MOTIVATION...................................................................................................6

LITERATURE REVIEW................................................................................................................7

HYPOTHESIS.................................................................................................................................9

CONCEPTUAL FRAMEWORK OF THE REPORT...................................................................10

REFERENCES..............................................................................................................................11

ACKNOWLEDGEMENT...............................................................................................................2

INTRODUCTION...........................................................................................................................4

PRACTICAL MOTIVATION.........................................................................................................5

THEORETICAL MOTIVATION...................................................................................................6

LITERATURE REVIEW................................................................................................................7

HYPOTHESIS.................................................................................................................................9

CONCEPTUAL FRAMEWORK OF THE REPORT...................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In present time rapid changes in the technology, commercials, social developments and

increasing population is becoming a big question for environment sustainability. The question

which arises is whether the companies growing in the market are paying appropriate amount of

allowance for the harm of environment or are they going green so that they can protect

environment (Hummel and Schlick, 2016). The case study discusses about the way the corporate

firms are increasing which is becoming responsible for the increase in carbon radiation which is

harming the environment due to which atmosphere is getting affected. Increase in the carbon

radiation is causing climate changes across the world. Increase in carbon radiation is affecting

the Ozone layer due to which ultra violet rays are entering directly into the environment and are

having huge impact on the health of the people living in the environment. It is required that the

companies should understand their corporate social responsibilities and develop the mechanism

which could help in the environmental protection aspects (Oates and Moradi-Motlagh, 2016).

Hence, a research proposal is developed which will be based upon stakeholders theory with the

effect of which relevant set of information related with environmental protection aspects could

be taken into consideration. The report will also include information related with theoretical and

practical information related with the aspects of motivation which will help industries in

remaining motivated in protecting the environment and helping in the environmental

sustainability aspects (Jones and Ratnatunga, 2012).

In present time rapid changes in the technology, commercials, social developments and

increasing population is becoming a big question for environment sustainability. The question

which arises is whether the companies growing in the market are paying appropriate amount of

allowance for the harm of environment or are they going green so that they can protect

environment (Hummel and Schlick, 2016). The case study discusses about the way the corporate

firms are increasing which is becoming responsible for the increase in carbon radiation which is

harming the environment due to which atmosphere is getting affected. Increase in the carbon

radiation is causing climate changes across the world. Increase in carbon radiation is affecting

the Ozone layer due to which ultra violet rays are entering directly into the environment and are

having huge impact on the health of the people living in the environment. It is required that the

companies should understand their corporate social responsibilities and develop the mechanism

which could help in the environmental protection aspects (Oates and Moradi-Motlagh, 2016).

Hence, a research proposal is developed which will be based upon stakeholders theory with the

effect of which relevant set of information related with environmental protection aspects could

be taken into consideration. The report will also include information related with theoretical and

practical information related with the aspects of motivation which will help industries in

remaining motivated in protecting the environment and helping in the environmental

sustainability aspects (Jones and Ratnatunga, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PRACTICAL MOTIVATION

Increase in the level of carbon radiation can be noticed day by day which is becoming a serious

issue for the environment at international level due to which climatic changes are occurring and

atmosphere is getting affected (Hummel and Schlick, 2016). With the help of various studies it is

being evaluated that corporate s are the main bodies which are affecting the environment and are

performing a main role in enhancing carbon radiation in the atmosphere. It is required that the

concept of Corporate Social Responsibility should be taken into consideration so as to monitor

the activities of various corporate and understanding the roles and responsibilities they play to

manage all the environmental aspects and protecting the same from getting affected (Dávila,

Epstein and Manzoni, 2016). The report will undertake all the aspects which could help the

companies in understanding there corporate social responsibilities towards to protect the

environment and evaluating the ways with the help of which they can reduce carbon emission.

The research proposal will help in evaluating all the ways with the help of which companies

available in the market could evaluate the ways with the effect of which they can manage to

reduce the carbon emissions (Bagnoli and Watts, 2016). Importance of environmental

sustainability will also be focused upon by the researcher. Several literatures will be reviewed to

evaluate which will help in providing a set direction working on which will help the companies

in protecting the environment and will help them in making an effective set of contribution in the

reduction of carbon radiation and will provide a direction to spread environment sustainability

(Sunderasan, 2013).

Increase in the level of carbon radiation can be noticed day by day which is becoming a serious

issue for the environment at international level due to which climatic changes are occurring and

atmosphere is getting affected (Hummel and Schlick, 2016). With the help of various studies it is

being evaluated that corporate s are the main bodies which are affecting the environment and are

performing a main role in enhancing carbon radiation in the atmosphere. It is required that the

concept of Corporate Social Responsibility should be taken into consideration so as to monitor

the activities of various corporate and understanding the roles and responsibilities they play to

manage all the environmental aspects and protecting the same from getting affected (Dávila,

Epstein and Manzoni, 2016). The report will undertake all the aspects which could help the

companies in understanding there corporate social responsibilities towards to protect the

environment and evaluating the ways with the help of which they can reduce carbon emission.

The research proposal will help in evaluating all the ways with the help of which companies

available in the market could evaluate the ways with the effect of which they can manage to

reduce the carbon emissions (Bagnoli and Watts, 2016). Importance of environmental

sustainability will also be focused upon by the researcher. Several literatures will be reviewed to

evaluate which will help in providing a set direction working on which will help the companies

in protecting the environment and will help them in making an effective set of contribution in the

reduction of carbon radiation and will provide a direction to spread environment sustainability

(Sunderasan, 2013).

THEORETICAL MOTIVATION

Aim of the research is to gather a relevant set of information related with environmental

sustainability in which information related with the ways which could be adopted by the

companies in the environmental sustainability aspects will be focused upon (Oates and Moradi-

Motlagh, 2016). It is being evaluated that carbon radiation and the other gases emitted by the

industries is affecting the ozone layer. This emission of carbon radiation and emission of the

gases is leading to increase pollution due to which various serious diseases are also getting

increased. With the help of the information gained from various previous researches problem

related with the carbon emission and increasing pollution will be resolved (Jong-Seo Choi,

2010). Stakeholder’s theory will be reviewed so as to gather relevant set of information related

with the role they will play in managing environmental sustainability aspects. This will help in

proving the efficiency of the environment and will help in providing a set direction with the

effect of which companies as well as industries available could reduce carbon emission and

could help in managing all the environmental sustainability aspects. The report will also include

information related with the effect of carbon radiation on the non financial performance of the

companies along with the financial performance (Jones and Ratnatunga, 2012).

Aim of the research is to gather a relevant set of information related with environmental

sustainability in which information related with the ways which could be adopted by the

companies in the environmental sustainability aspects will be focused upon (Oates and Moradi-

Motlagh, 2016). It is being evaluated that carbon radiation and the other gases emitted by the

industries is affecting the ozone layer. This emission of carbon radiation and emission of the

gases is leading to increase pollution due to which various serious diseases are also getting

increased. With the help of the information gained from various previous researches problem

related with the carbon emission and increasing pollution will be resolved (Jong-Seo Choi,

2010). Stakeholder’s theory will be reviewed so as to gather relevant set of information related

with the role they will play in managing environmental sustainability aspects. This will help in

proving the efficiency of the environment and will help in providing a set direction with the

effect of which companies as well as industries available could reduce carbon emission and

could help in managing all the environmental sustainability aspects. The report will also include

information related with the effect of carbon radiation on the non financial performance of the

companies along with the financial performance (Jones and Ratnatunga, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LITERATURE REVIEW

Environment sustainability is one of the aspects which are required to be taken into consideration

by the people available in the market. It is required that the business should work towards to

evaluate all the possible solutions which could help in spreading a sustainable environment and

could help in managing things in a proper way. It is required that businesses should adopt the

strategies which could help in the reduction of carbon radiation and emission of various harmful

gasses which are affecting the environment. Greenhouse gases are the gases which traps the heat

in the air (Hummel and Schlick, 2016). There are various set of greenhouse gases which are

affecting the environment and are spreading due to various human activities like fossil fuels and

various other natural processes. There are various type of greenhouse gases which are entering

into the environment by the activities of human and by various other natural processes these

gases are Ozone (O3), Nitrous Oxide (N2O), Methane (CH4), Water Vapour and Carbon

Dioxide (CO2). The financial aspects of the companies are getting affected due to increase in the

carbon radiation (Dávila, Epstein and Manzoni, 2016). Increase in such type of harmful gases is

leading to increasing the financial burden of the companies and also leading to increasing

pollution in the environment. Companies are working towards to develop some or the other

strategies with the help of which carbon emission could get reduced due to which cost of

monitoring he carbon radiation level is increasing. Companies also remain indulged in the

activities with the help of which losses which are occurring could get reduced. Agents plays a

vital role in gathering relevant set of information and evaluating ways with the effect of which

targets of the company could be achieved within the time frame decided by the company

(BEYER and GUTTMAN, 2012). With the help of stakeholders theory it could be evaluated that

stakeholders attached with the company plays a very vital role in managing the work process and

evaluating all the aspects which could help in the protection of the environment. It is necessary

that all the stakeholders should be focused upon by the company and a trial should be made with

the help of which company could provide effective set of contribution in the environmental

sustainability aspects (Bagnoli and Watts, 2016). It is required that companies should develop a

proper list of stakeholders who can help in managing the environment sustainability and could

provide proper set of support in reducing the cost which is occurring in the keeping a track

record on the level of carbon radiation. According to the theories stakeholders plays a very vital

Environment sustainability is one of the aspects which are required to be taken into consideration

by the people available in the market. It is required that the business should work towards to

evaluate all the possible solutions which could help in spreading a sustainable environment and

could help in managing things in a proper way. It is required that businesses should adopt the

strategies which could help in the reduction of carbon radiation and emission of various harmful

gasses which are affecting the environment. Greenhouse gases are the gases which traps the heat

in the air (Hummel and Schlick, 2016). There are various set of greenhouse gases which are

affecting the environment and are spreading due to various human activities like fossil fuels and

various other natural processes. There are various type of greenhouse gases which are entering

into the environment by the activities of human and by various other natural processes these

gases are Ozone (O3), Nitrous Oxide (N2O), Methane (CH4), Water Vapour and Carbon

Dioxide (CO2). The financial aspects of the companies are getting affected due to increase in the

carbon radiation (Dávila, Epstein and Manzoni, 2016). Increase in such type of harmful gases is

leading to increasing the financial burden of the companies and also leading to increasing

pollution in the environment. Companies are working towards to develop some or the other

strategies with the help of which carbon emission could get reduced due to which cost of

monitoring he carbon radiation level is increasing. Companies also remain indulged in the

activities with the help of which losses which are occurring could get reduced. Agents plays a

vital role in gathering relevant set of information and evaluating ways with the effect of which

targets of the company could be achieved within the time frame decided by the company

(BEYER and GUTTMAN, 2012). With the help of stakeholders theory it could be evaluated that

stakeholders attached with the company plays a very vital role in managing the work process and

evaluating all the aspects which could help in the protection of the environment. It is necessary

that all the stakeholders should be focused upon by the company and a trial should be made with

the help of which company could provide effective set of contribution in the environmental

sustainability aspects (Bagnoli and Watts, 2016). It is required that companies should develop a

proper list of stakeholders who can help in managing the environment sustainability and could

provide proper set of support in reducing the cost which is occurring in the keeping a track

record on the level of carbon radiation. According to the theories stakeholders plays a very vital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

role in managing the cost which will indulge in the projection of carbon emission and various

other gases. Employees, government, society, owner and customer are some of the stakeholders

who can make a positive contribution in the environmental sustainability aspect (Wen, 2012).

Employees of the company could take a control over all the activities like reducing the use of

electronic items, saving energy by reducing the wastage of it, plantation of trees in the premises

wherever they could be planted, increasing the men power means working manually rather on

the aspects wherever possible and developing some or the other innovative ideas with the effect

of which carbon emission could be reduced and further work could get managed in a proper way.

Car and Bike pooling is one of the most effective strategies with the effect of which employees

working in the companies could make their effective contribution in environmental sustainability

aspects and reducing pollution (Sunderasan, 2013).

Government helps in developing the policies and protocols related with environmental

sustainability aspect. It develops the policies related with environmental sustainability aspects

which are required to be followed by every single person so as to manage the work in an

appropriate way (Oates and Moradi-Motlagh, 2016). It is required that companies should include

all the environmental related policies in the internal policies and should ensure that every single

employee and member attached with the companies should follow these policies in a proper way.

Government could also make a positive contribution and could help the companies in protecting

the environment and reducing carbon radiation. Providing proper set of funds or equipments at a

minimum cost will help the industries in reducing the cost and will help in maintaining the

financial position in the market (Jong-Seo Choi, 2010).

Owner of the company plays a very vital role in environmental sustainability aspects, there are

many of the things which are required to be focused upon which could provide better solution in

financial management aspects (Jones and Ratnatunga, 2012). Managing finances is a typical task

when it comes to environmental sustainability but by providing right guidance to the employees

and other stakeholders could help companies in keeping a proper track record on the level of

carbon radiation. Indulging in such type of activity will also help in providing a better solution in

managing the company accounts. Processing the things in a right way and choosing appropriate

path will help companies in managing their fund and placing the same in a right order (Hummel

and Schlick, 2016).

other gases. Employees, government, society, owner and customer are some of the stakeholders

who can make a positive contribution in the environmental sustainability aspect (Wen, 2012).

Employees of the company could take a control over all the activities like reducing the use of

electronic items, saving energy by reducing the wastage of it, plantation of trees in the premises

wherever they could be planted, increasing the men power means working manually rather on

the aspects wherever possible and developing some or the other innovative ideas with the effect

of which carbon emission could be reduced and further work could get managed in a proper way.

Car and Bike pooling is one of the most effective strategies with the effect of which employees

working in the companies could make their effective contribution in environmental sustainability

aspects and reducing pollution (Sunderasan, 2013).

Government helps in developing the policies and protocols related with environmental

sustainability aspect. It develops the policies related with environmental sustainability aspects

which are required to be followed by every single person so as to manage the work in an

appropriate way (Oates and Moradi-Motlagh, 2016). It is required that companies should include

all the environmental related policies in the internal policies and should ensure that every single

employee and member attached with the companies should follow these policies in a proper way.

Government could also make a positive contribution and could help the companies in protecting

the environment and reducing carbon radiation. Providing proper set of funds or equipments at a

minimum cost will help the industries in reducing the cost and will help in maintaining the

financial position in the market (Jong-Seo Choi, 2010).

Owner of the company plays a very vital role in environmental sustainability aspects, there are

many of the things which are required to be focused upon which could provide better solution in

financial management aspects (Jones and Ratnatunga, 2012). Managing finances is a typical task

when it comes to environmental sustainability but by providing right guidance to the employees

and other stakeholders could help companies in keeping a proper track record on the level of

carbon radiation. Indulging in such type of activity will also help in providing a better solution in

managing the company accounts. Processing the things in a right way and choosing appropriate

path will help companies in managing their fund and placing the same in a right order (Hummel

and Schlick, 2016).

Financial analysts should try to work on various set of aspects which could help in saving the

cost of firm. Environmental sustainability is the aspect which include huge cost and it is required

that companies should make an effective set of contribution to protect the environment in this

condition it is required that financial analysts should make effective set if contribution in

managing the funds (Hassan, 2015). Developing the strategies with the help of which the cost of

processing the work could get reduced will help in providing a relevant set of support to the

companies in making a more effective contribution in environmental sustainability aspects with

the effect of which company will attain success in achieving the set targets and goals.

Hence, it could be evaluated that stakeholders plays a very vital role in environmental

sustainability aspects in which it is required that company should try to motivate them and

provide appropriate set of guidance with the help of which they can indulge in the environmental

sustainability aspects and could help in resolving the accounting issues of the company in a

proper way (Dawkins and Fraas, 2010).

HYPOTHESIS

Evaluating various aspects by reviewing various literatures disclosure of the impact of carbon

radiation on the performance of company’s financial and non financial aspects could be done. It

is necessary that the company should make appropriate set of decision in managing the regular

investments in environmental sustainability aspects. Such type of activities helps in managing

financial performance (Dawkins and Fraas, 2009). There are certain set of hypothesis which are

being evaluated in relation with the research these are:

H1: The relationship between the impacts of increasing level of carbon radiation on the financial

performance of the company.

H2: Role played by the stakeholders in making strong financial position of the company and

contribution they can make in environmental sustainability aspects (Dávila, Epstein and

Manzoni, 2016).

cost of firm. Environmental sustainability is the aspect which include huge cost and it is required

that companies should make an effective set of contribution to protect the environment in this

condition it is required that financial analysts should make effective set if contribution in

managing the funds (Hassan, 2015). Developing the strategies with the help of which the cost of

processing the work could get reduced will help in providing a relevant set of support to the

companies in making a more effective contribution in environmental sustainability aspects with

the effect of which company will attain success in achieving the set targets and goals.

Hence, it could be evaluated that stakeholders plays a very vital role in environmental

sustainability aspects in which it is required that company should try to motivate them and

provide appropriate set of guidance with the help of which they can indulge in the environmental

sustainability aspects and could help in resolving the accounting issues of the company in a

proper way (Dawkins and Fraas, 2010).

HYPOTHESIS

Evaluating various aspects by reviewing various literatures disclosure of the impact of carbon

radiation on the performance of company’s financial and non financial aspects could be done. It

is necessary that the company should make appropriate set of decision in managing the regular

investments in environmental sustainability aspects. Such type of activities helps in managing

financial performance (Dawkins and Fraas, 2009). There are certain set of hypothesis which are

being evaluated in relation with the research these are:

H1: The relationship between the impacts of increasing level of carbon radiation on the financial

performance of the company.

H2: Role played by the stakeholders in making strong financial position of the company and

contribution they can make in environmental sustainability aspects (Dávila, Epstein and

Manzoni, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

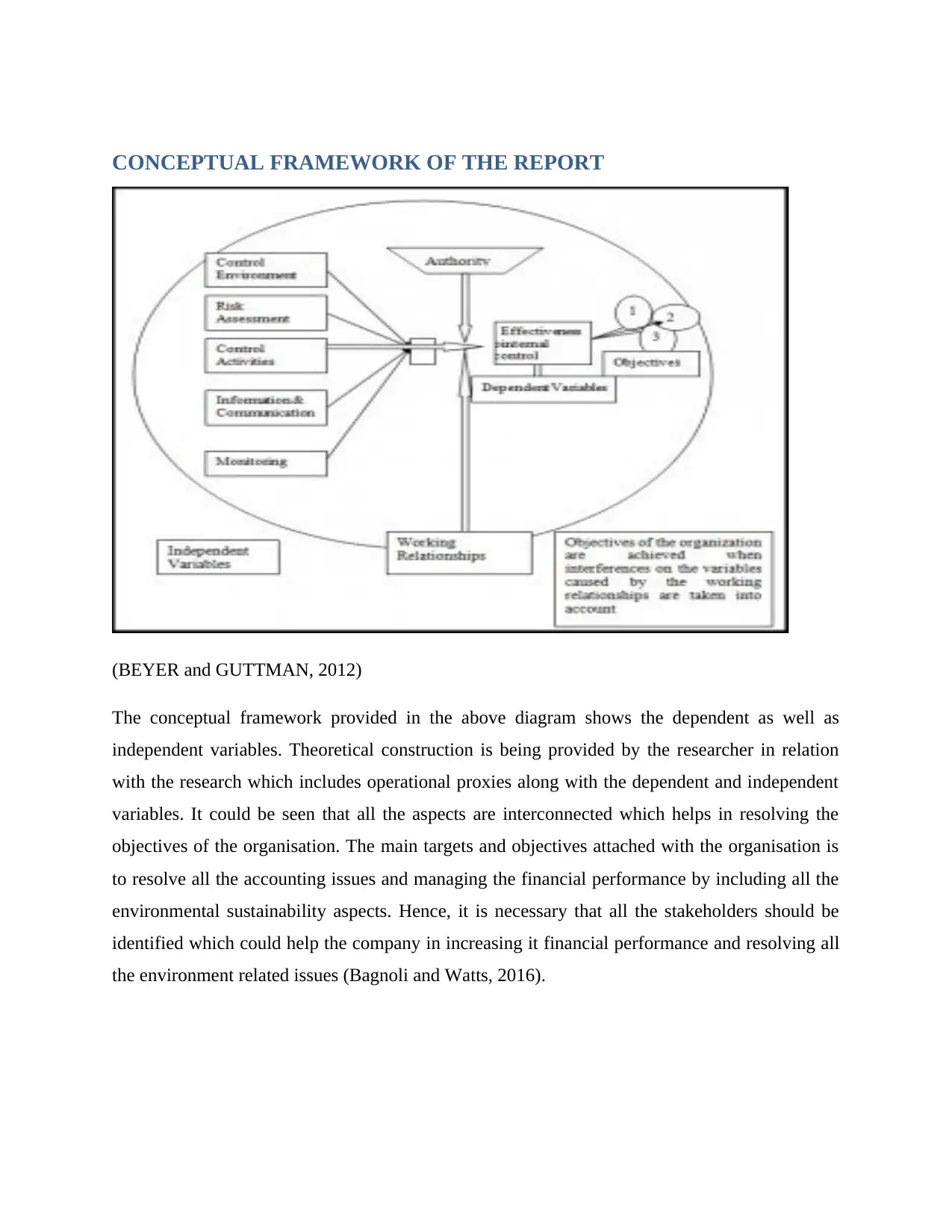

CONCEPTUAL FRAMEWORK OF THE REPORT

(BEYER and GUTTMAN, 2012)

The conceptual framework provided in the above diagram shows the dependent as well as

independent variables. Theoretical construction is being provided by the researcher in relation

with the research which includes operational proxies along with the dependent and independent

variables. It could be seen that all the aspects are interconnected which helps in resolving the

objectives of the organisation. The main targets and objectives attached with the organisation is

to resolve all the accounting issues and managing the financial performance by including all the

environmental sustainability aspects. Hence, it is necessary that all the stakeholders should be

identified which could help the company in increasing it financial performance and resolving all

the environment related issues (Bagnoli and Watts, 2016).

(BEYER and GUTTMAN, 2012)

The conceptual framework provided in the above diagram shows the dependent as well as

independent variables. Theoretical construction is being provided by the researcher in relation

with the research which includes operational proxies along with the dependent and independent

variables. It could be seen that all the aspects are interconnected which helps in resolving the

objectives of the organisation. The main targets and objectives attached with the organisation is

to resolve all the accounting issues and managing the financial performance by including all the

environmental sustainability aspects. Hence, it is necessary that all the stakeholders should be

identified which could help the company in increasing it financial performance and resolving all

the environment related issues (Bagnoli and Watts, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Bagnoli, M. and Watts, S. (2016). Voluntary Assurance of Voluntary CSR Disclosure. Journal of

Economics & Management Strategy, 26(1), pp.205-230.

BEYER, A. and GUTTMAN, I. (2012). Voluntary Disclosure, Manipulation, and Real

Effects. Journal of Accounting Research, 50(5), pp.1141-1177.

Dávila, A., Epstein, M. and Manzoni, J. (2016). Performance measurement and management

control.

Dawkins, C. and Fraas, J. (2009). Beyond Acclamations and Excuses: Environmental

Performance, Voluntary Environmental Disclosure, and the Role of Visibility. Journal of

Business Ethics, 92(4), pp.655-655.

Dawkins, C. and Fraas, J. (2010). Erratum to: Beyond Acclamations and Excuses:

Environmental Performance, Voluntary Environmental Disclosure and the Role of

Visibility. Journal of Business Ethics, 99(3), pp.383-397.

Hassan, A. (2015). Environmental performance and voluntary disclosure on specific

environmental activities: an empirical study of carbon vs. non-carbon intensive industries.

Legitimacy proactive approach. International Journal of Sustainable Economy, 7(4), p.243.

Hummel, K. and Schlick, C. (2016). The relationship between sustainability performance and

sustainability disclosure – Reconciling voluntary disclosure theory and legitimacy

theory. Journal of Accounting and Public Policy, 35(5), pp.455-476.

Jones, S. and Ratnatunga, J. (2012). Contemporary issues in sustainability accounting, assurance

and reporting. Bingley England: Emerald Insight.

Jong-Seo Choi (2010). Content Analysis of Voluntary Environmental Disclosure Made in Stand-

alone Environmental Reports or Company Web-sites: Focusing on the Interrelations between

Disclosure Quality, Environmental Performance and Economic Performance. Journal of

Environmental Policy, 9(3), pp.69-114.

Bagnoli, M. and Watts, S. (2016). Voluntary Assurance of Voluntary CSR Disclosure. Journal of

Economics & Management Strategy, 26(1), pp.205-230.

BEYER, A. and GUTTMAN, I. (2012). Voluntary Disclosure, Manipulation, and Real

Effects. Journal of Accounting Research, 50(5), pp.1141-1177.

Dávila, A., Epstein, M. and Manzoni, J. (2016). Performance measurement and management

control.

Dawkins, C. and Fraas, J. (2009). Beyond Acclamations and Excuses: Environmental

Performance, Voluntary Environmental Disclosure, and the Role of Visibility. Journal of

Business Ethics, 92(4), pp.655-655.

Dawkins, C. and Fraas, J. (2010). Erratum to: Beyond Acclamations and Excuses:

Environmental Performance, Voluntary Environmental Disclosure and the Role of

Visibility. Journal of Business Ethics, 99(3), pp.383-397.

Hassan, A. (2015). Environmental performance and voluntary disclosure on specific

environmental activities: an empirical study of carbon vs. non-carbon intensive industries.

Legitimacy proactive approach. International Journal of Sustainable Economy, 7(4), p.243.

Hummel, K. and Schlick, C. (2016). The relationship between sustainability performance and

sustainability disclosure – Reconciling voluntary disclosure theory and legitimacy

theory. Journal of Accounting and Public Policy, 35(5), pp.455-476.

Jones, S. and Ratnatunga, J. (2012). Contemporary issues in sustainability accounting, assurance

and reporting. Bingley England: Emerald Insight.

Jong-Seo Choi (2010). Content Analysis of Voluntary Environmental Disclosure Made in Stand-

alone Environmental Reports or Company Web-sites: Focusing on the Interrelations between

Disclosure Quality, Environmental Performance and Economic Performance. Journal of

Environmental Policy, 9(3), pp.69-114.

Oates, G. and Moradi-Motlagh, A. (2016). Is voluntary disclosure of environmental performance

associated with actual environmental performance? Evidence from Victorian local governments,

Australia. Australasian Journal of Environmental Management, 23(2), pp.194-205.

Sunderasan, S. (2013). Enabling Environment. India: Springer India.

Wen, X. (2012). Voluntary Disclosure and Investment*. Contemporary Accounting Research,

30(2), pp.677-696.

associated with actual environmental performance? Evidence from Victorian local governments,

Australia. Australasian Journal of Environmental Management, 23(2), pp.194-205.

Sunderasan, S. (2013). Enabling Environment. India: Springer India.

Wen, X. (2012). Voluntary Disclosure and Investment*. Contemporary Accounting Research,

30(2), pp.677-696.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.