Analysis of Accounting Framework for Astron Corporation's Financials

VerifiedAdded on 2023/05/28

|22

|2407

|97

Report

AI Summary

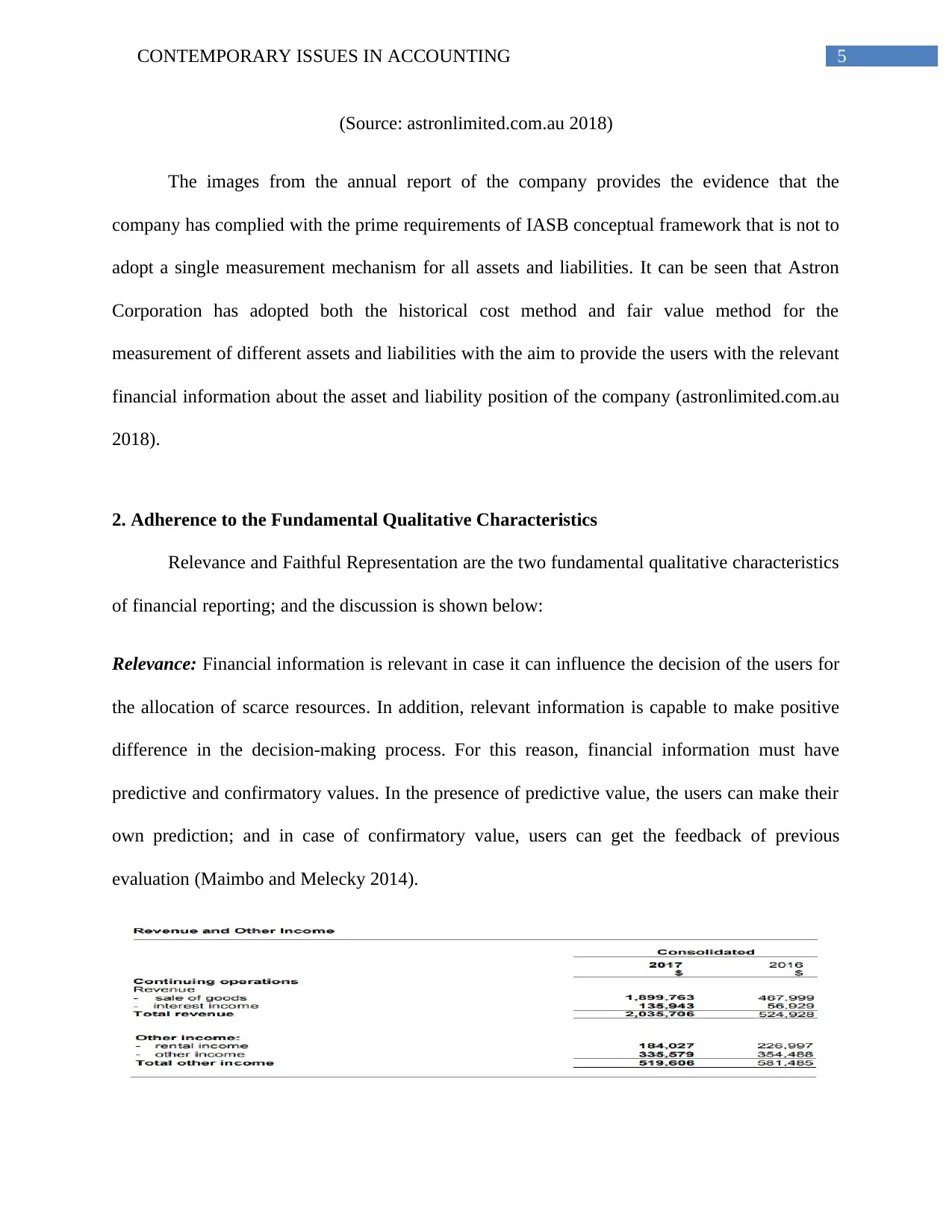

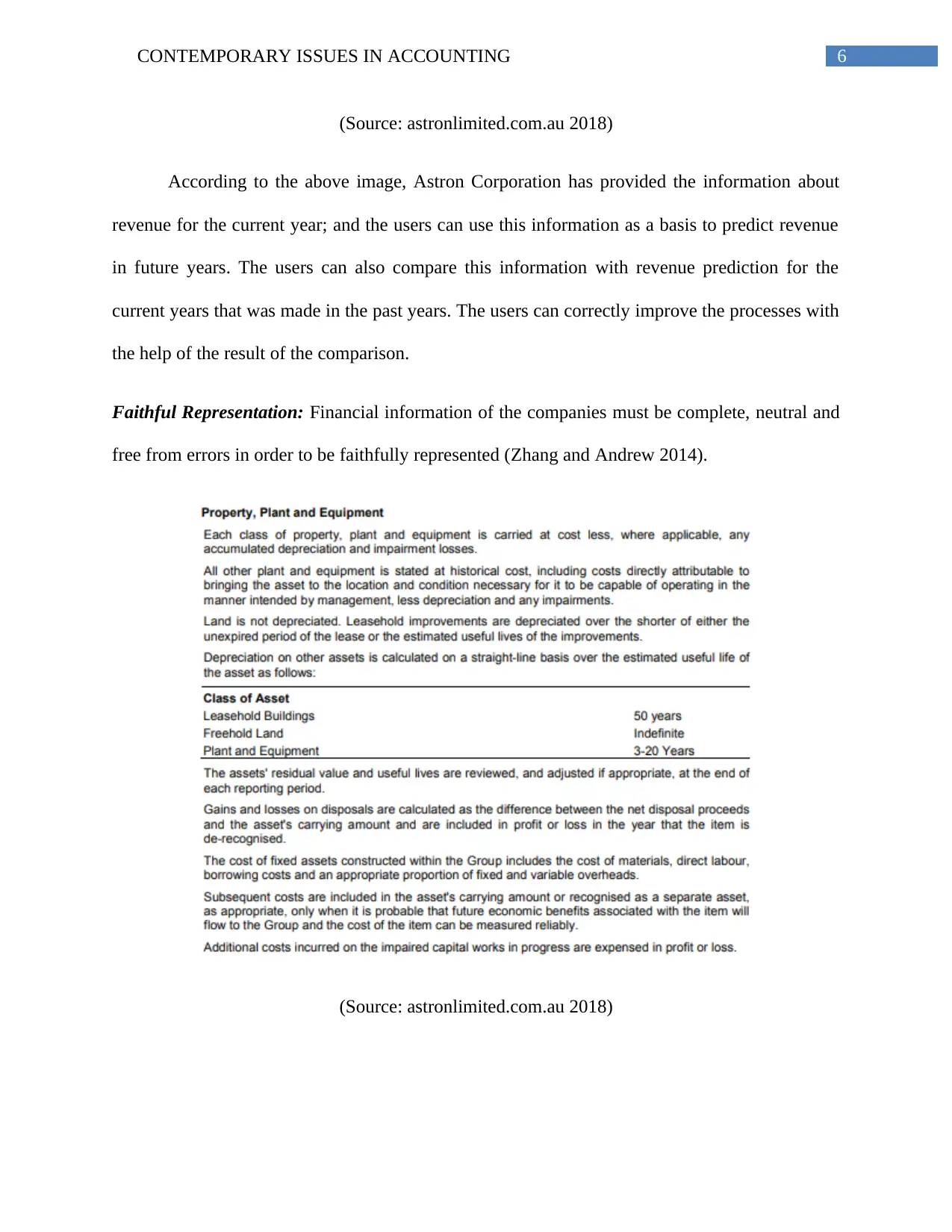

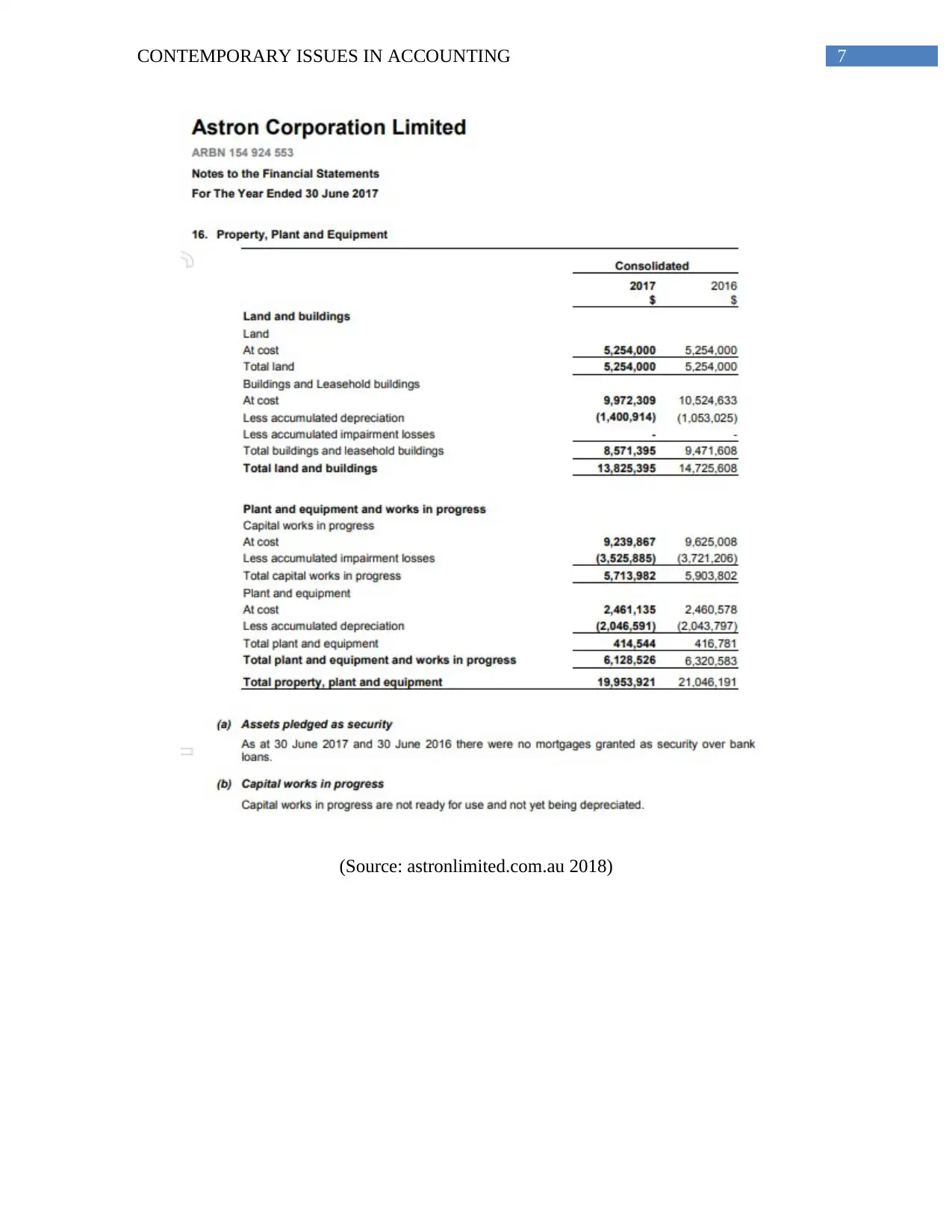

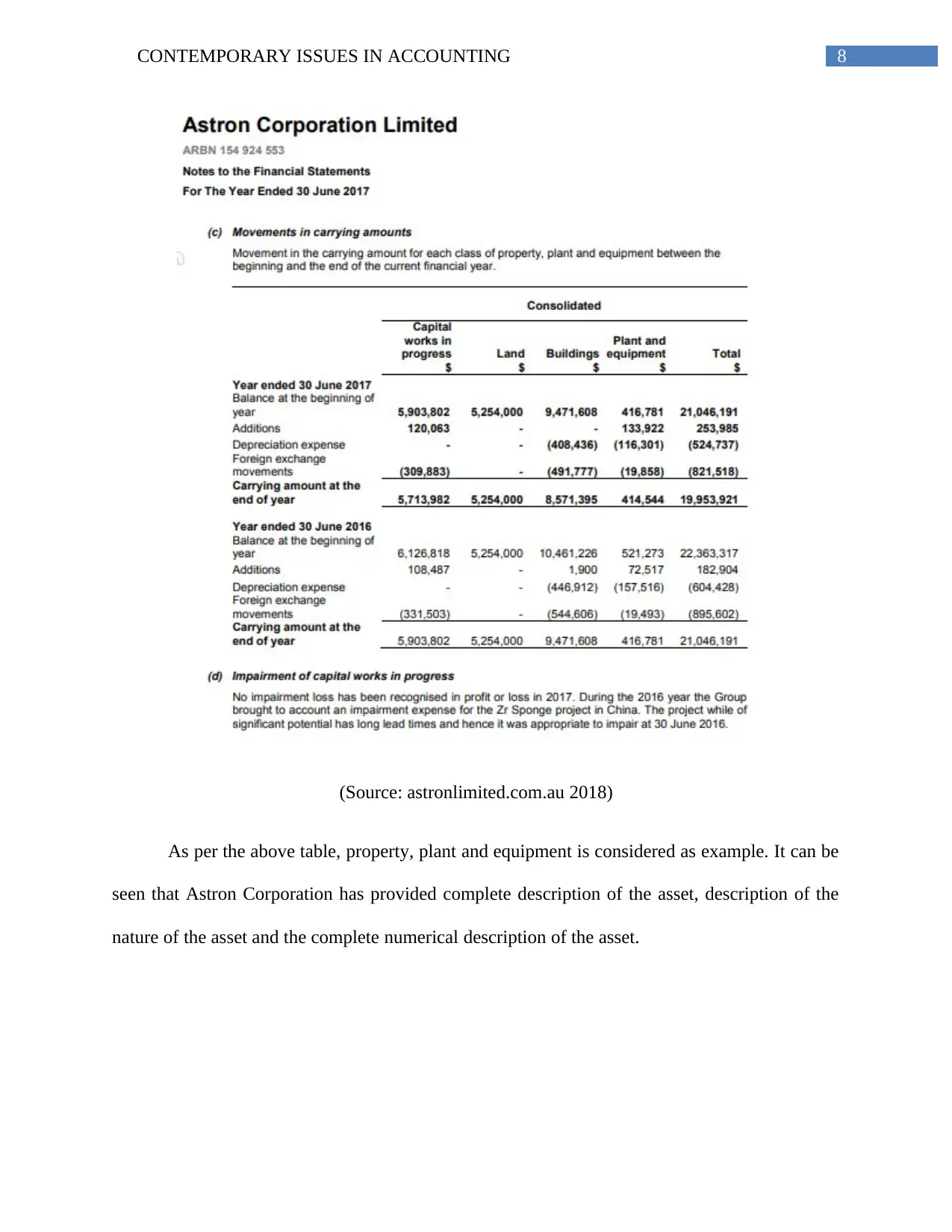

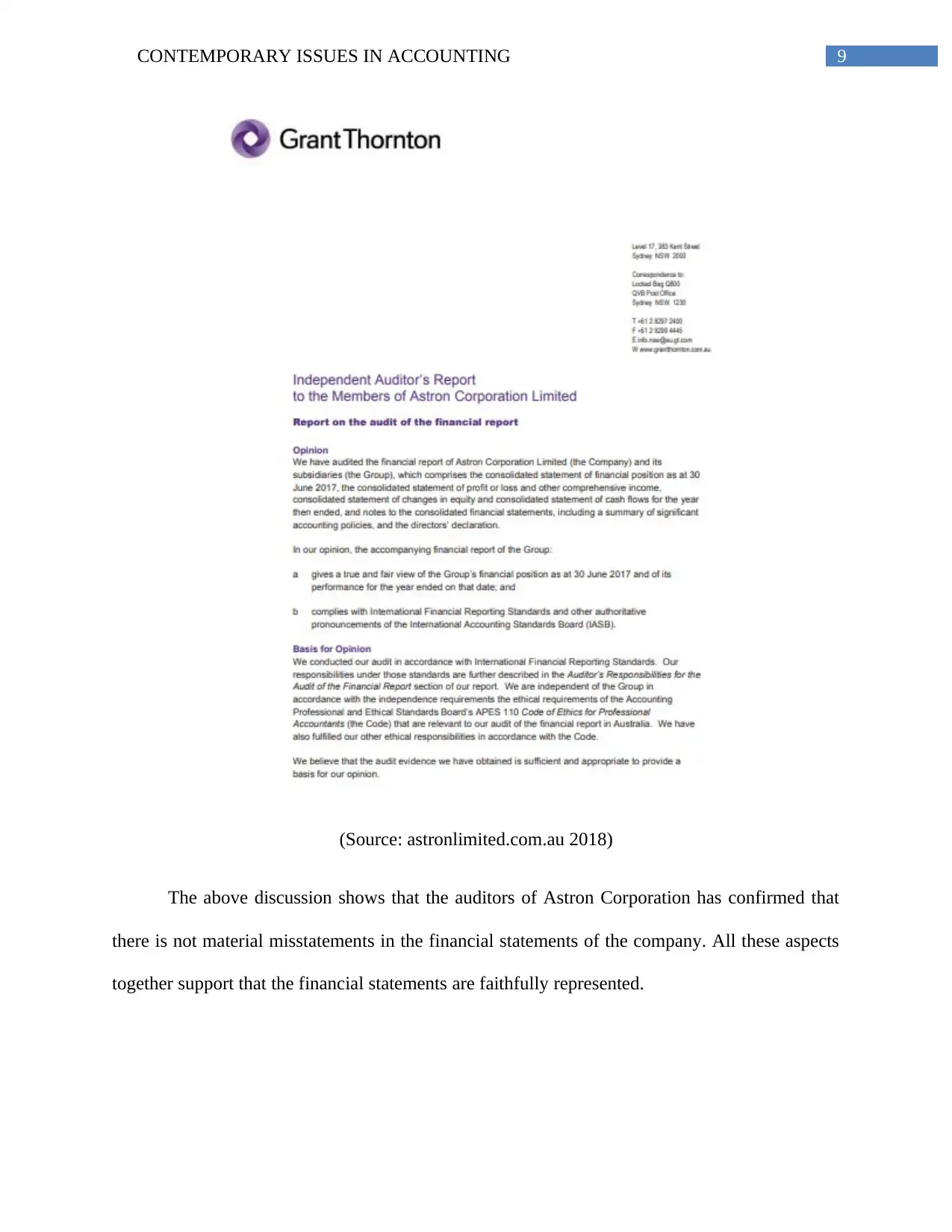

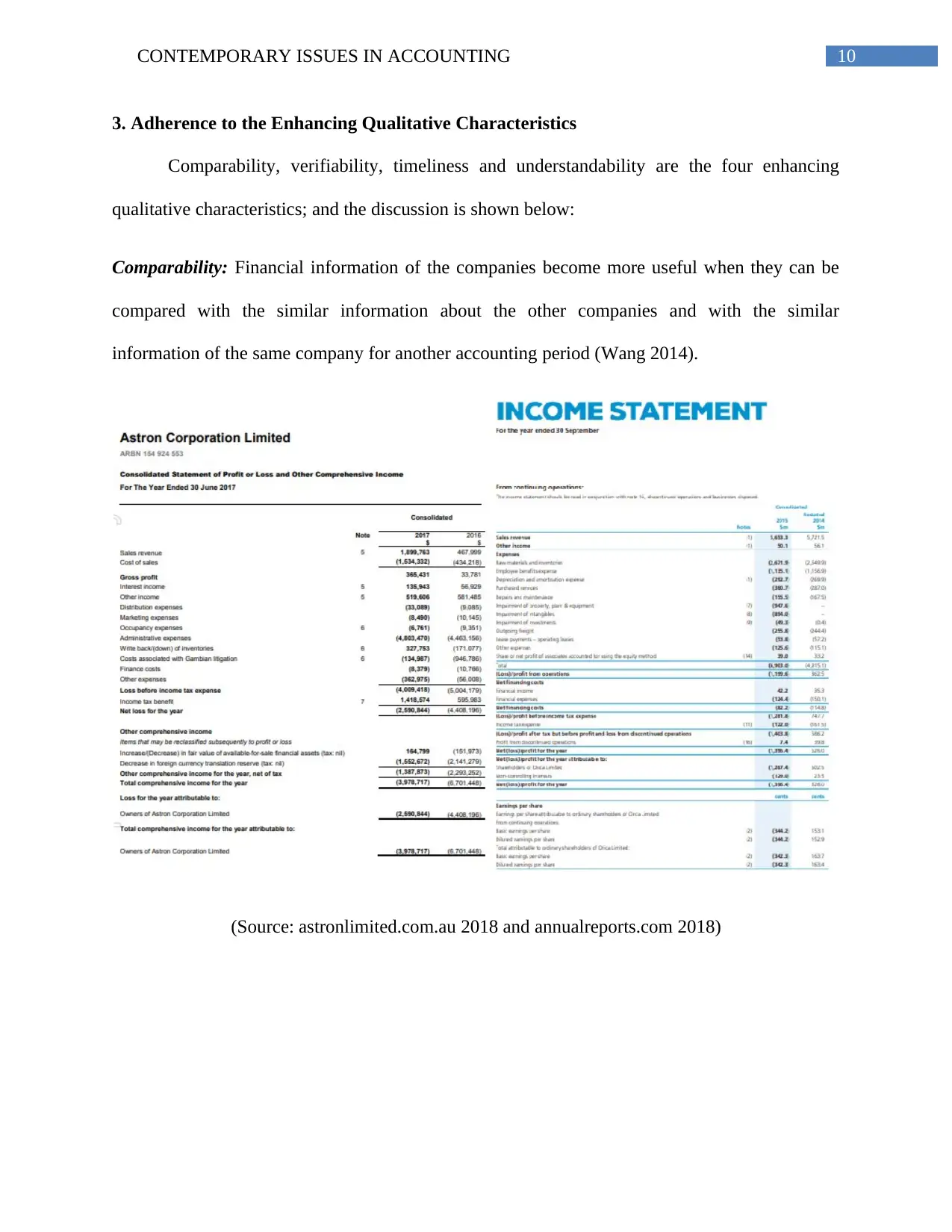

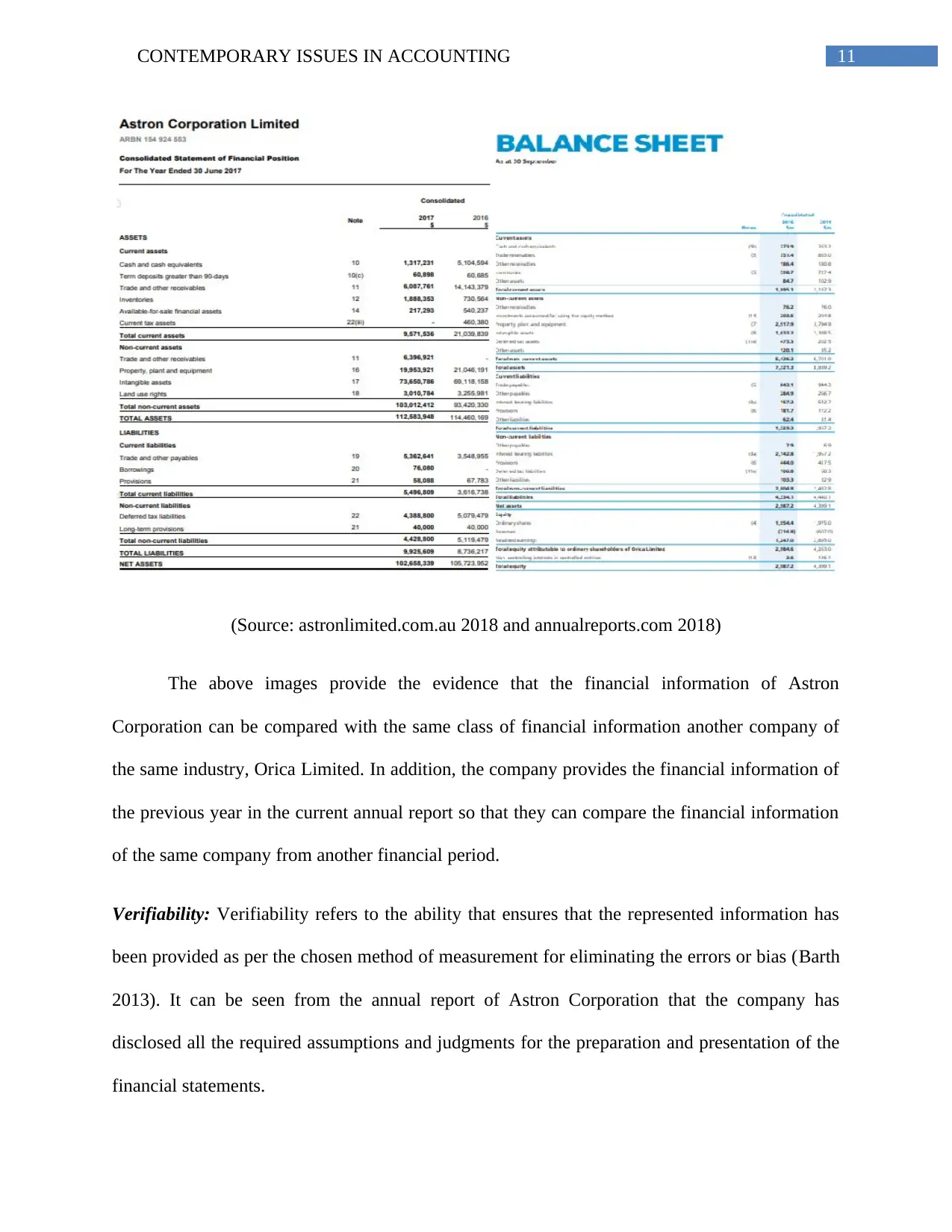

This report provides a comprehensive analysis of Astron Corporation's adherence to the accounting conceptual framework. It examines the company's compliance with measurement requirements, including the use of historical cost and fair value methods, and evaluates its adherence to fundamental and enhancing qualitative characteristics like relevance, faithful representation, comparability, and understandability. The report assesses whether users of financial reports can effectively utilize the information for decision-making, considering the required basic knowledge and the requirements of general-purpose financial reporting. By analyzing Astron Corporation's financial statements, the report highlights how the company complies with the IASB conceptual framework, ultimately assessing the quality and usefulness of its financial reporting practices. The report concludes by summarizing the key findings regarding Astron Corporation's financial reporting.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.