ACCT20074 Contemporary Accounting Theory: MPL vs CPI Analysis

VerifiedAdded on 2023/04/03

|23

|4698

|481

Report

AI Summary

This report provides a comparative analysis of Medibank (MPL) and Capitec Bank Holdings Ltd (CPI) through the lens of contemporary accounting theory, focusing on conceptual frameworks and integrated reporting. It begins with a literature review of the conceptual framework's history and development in the USA, UK, Australia, and globally under the IASB. The report then discusses concerns regarding the application of the IASB/IFRS Conceptual Framework and academics' concerns about its quality. The second part delves into sustainability reporting, comparing the two companies' approaches and adherence to GRI standards and integrated reporting principles. The analysis reveals that both companies, despite their different contexts, are committed to integrated reporting practices, enhancing transparency and stakeholder engagement. Desklib provides this and other solved assignments contributed by students.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Contemporary accounting theory

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MPL VS CPI

Executive Summary

With the due passage of time, sustainability, as well as integrated reporting has assumed a place

of special importance because it reflects the performance of the company in terms of society. The

current report stress upon the performance of two listed companies one based in Australia while

another based in SA to provide a scope of comparison. The report begins with a discussion of the

history and development of conceptual framework followed by various discussion related to

conceptual framework. The advantages and disadvantages of the company is even discussed

together with the major components. The other part of the report engages with the concept of

sustainability reporting and sheds light upon the two companies in consideration. The overall

study gives a glimpse that irrespective of the situation, the companies are adhering to the concept

of integrated reporting.

2

Executive Summary

With the due passage of time, sustainability, as well as integrated reporting has assumed a place

of special importance because it reflects the performance of the company in terms of society. The

current report stress upon the performance of two listed companies one based in Australia while

another based in SA to provide a scope of comparison. The report begins with a discussion of the

history and development of conceptual framework followed by various discussion related to

conceptual framework. The advantages and disadvantages of the company is even discussed

together with the major components. The other part of the report engages with the concept of

sustainability reporting and sheds light upon the two companies in consideration. The overall

study gives a glimpse that irrespective of the situation, the companies are adhering to the concept

of integrated reporting.

2

MPL VS CPI

Contents

Introduction......................................................................................................................................4

Part A Conceptual framework.........................................................................................................5

Part B- integrated reporting...........................................................................................................10

GRI versus IR................................................................................................................................10

Index..............................................................................................................................................12

Preparation of Integrated report.....................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

3

Contents

Introduction......................................................................................................................................4

Part A Conceptual framework.........................................................................................................5

Part B- integrated reporting...........................................................................................................10

GRI versus IR................................................................................................................................10

Index..............................................................................................................................................12

Preparation of Integrated report.....................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

3

MPL VS CPI

Introduction

The reporting practices of the companies have undergone a sea change and corporate external

reporting has become prominent. It is important that the company should have sound financial

reporting system so that the financial system is better placed and helps in the due course of

activities. The report revolves around two companies that is the Medibank and Capitec Bank

Holdings Ltd. The annual report of these two company is selected and studied in an in-depth

manner so as to shed light upon the concept of sustainability and reporting. The major point of

discussion in the reporting is mainly in the form of conceptual framework, GRI standards and

sustainability.

4

Introduction

The reporting practices of the companies have undergone a sea change and corporate external

reporting has become prominent. It is important that the company should have sound financial

reporting system so that the financial system is better placed and helps in the due course of

activities. The report revolves around two companies that is the Medibank and Capitec Bank

Holdings Ltd. The annual report of these two company is selected and studied in an in-depth

manner so as to shed light upon the concept of sustainability and reporting. The major point of

discussion in the reporting is mainly in the form of conceptual framework, GRI standards and

sustainability.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MPL VS CPI

Part A Conceptual framework

a. Literature review of the conceptual framework

The initial introduction of FASB happened in the year 1973 that so that financial accounting

standards can be enhanced and reporting can be more pronounced for the stakeholders such as

auditors, public and other financial statement users. The establishment of the conceptual

framework was done in US, UK and Australia considering the practice of accounting in the year

1961 and 1962. The theory proposed by Grady in the year 1965 persisted on accounting practices

that ultimately led to the emergence of the Accounting principles board. A true blood committee

was established in the year 1972 that contained various components like the outline of the aims

that pertains to the accounting and qualitative features of the financial data. Further, in the year

1974 the replacement of accounting principle was done by FASB that was directed toward the

conceptual framework.

Apart from it, in 1976 the movement of UK towards the identification of users was seen. The

report mainly stressed upon the rights of community and the terms for having a grab on the

financial data. However, at the end it was noticed that the content was not acceptable by the

accounting experts. In 1991, the adoption of IASC framework was done to evaluate the

conceptual framework. This framework was completely in compliance with the framework of

US and Australian framework and known as the IASB framework. The IASB is an independent

private sector body that approves the IFRS (Samaha & Dahaway, 2010). However, the

conceptual framework does not obtain the accounting standard status but drafted in a fashion that

assist the users and helps in proper preparation. It is a mechanism through which assets like

liabilities, income, assets and other expenses are put to recognition (Nobes,2014). The CF gained

prominence when other countries started following the same. It was observed that the

organizations were not using any kind of particular set of standards or rules while preparing the

financial statements before big scams and defaults took place. The crash of the big organizations

made the contents realize the importance of formulating a set of standards in order to present

financial statements of the organization (Page, 2015). It was observed that in the late 1980

International accounting standards board was formalized in order to issue several standards that

5

Part A Conceptual framework

a. Literature review of the conceptual framework

The initial introduction of FASB happened in the year 1973 that so that financial accounting

standards can be enhanced and reporting can be more pronounced for the stakeholders such as

auditors, public and other financial statement users. The establishment of the conceptual

framework was done in US, UK and Australia considering the practice of accounting in the year

1961 and 1962. The theory proposed by Grady in the year 1965 persisted on accounting practices

that ultimately led to the emergence of the Accounting principles board. A true blood committee

was established in the year 1972 that contained various components like the outline of the aims

that pertains to the accounting and qualitative features of the financial data. Further, in the year

1974 the replacement of accounting principle was done by FASB that was directed toward the

conceptual framework.

Apart from it, in 1976 the movement of UK towards the identification of users was seen. The

report mainly stressed upon the rights of community and the terms for having a grab on the

financial data. However, at the end it was noticed that the content was not acceptable by the

accounting experts. In 1991, the adoption of IASC framework was done to evaluate the

conceptual framework. This framework was completely in compliance with the framework of

US and Australian framework and known as the IASB framework. The IASB is an independent

private sector body that approves the IFRS (Samaha & Dahaway, 2010). However, the

conceptual framework does not obtain the accounting standard status but drafted in a fashion that

assist the users and helps in proper preparation. It is a mechanism through which assets like

liabilities, income, assets and other expenses are put to recognition (Nobes,2014). The CF gained

prominence when other countries started following the same. It was observed that the

organizations were not using any kind of particular set of standards or rules while preparing the

financial statements before big scams and defaults took place. The crash of the big organizations

made the contents realize the importance of formulating a set of standards in order to present

financial statements of the organization (Page, 2015). It was observed that in the late 1980

International accounting standards board was formalized in order to issue several standards that

5

MPL VS CPI

can cover accounting theories properly ( O'Mara-Shimek, 2015). The standard was at first made

applicable in the USA and was later being utilized by several different companies in order to

provide stability to their framework(Barth, 2013).

b. Application of the IFRS / IASB conceptual framework of financial reporting.

There are various types of concepts both theoretical and practical in nature that is needed to be

taken into account by an accountant while preparing the financial statements of an organization

(Nobes, 2014). According to the accountants it has been stated that all the things that are

explaining the conceptual framework cannot be applied practically because of which various

type of practical issues can be faced by them during the application of the conceptual framework

that is needed to be followed (O'Mara-Shimek, 2015). There are different functions that are

needed to be fulfilled in order to complete the accounting, reporting and disclosing process

(Leisyte & Westerheijden, 2014).

c. Academic concern

Application of a particular conceptual framework in an organization will not only provide

credibility to the financial statement but also help them to prepare a set of regulations that can be

used by them for presenting the strategies (Zeff, 2012). The worldwide acceptance of these

financial regulations will also help them to compare the financial status of various Nations

because of which the investment process can be made much easy. There are several types of

limitations that are needed to be assessed by the accountant because it will require them to leave

the reasoning and logic path behind (Nobes, 2014). The complex transactions taking place in the

organization are also becoming challenging because of which it needs to adapt to the

technological advancements in the market (Macías & Muino, 2011). Therefore, the use of proper

concepts will not only help the organization to interpret the transactions but also compare them

easily.

There are various pros and cons of the conceptual framework for financial reporting.

The positive side of the conceptual framework is that it confirms the integrity of the

financial reports of an entity (Nobes, 2014).

6

can cover accounting theories properly ( O'Mara-Shimek, 2015). The standard was at first made

applicable in the USA and was later being utilized by several different companies in order to

provide stability to their framework(Barth, 2013).

b. Application of the IFRS / IASB conceptual framework of financial reporting.

There are various types of concepts both theoretical and practical in nature that is needed to be

taken into account by an accountant while preparing the financial statements of an organization

(Nobes, 2014). According to the accountants it has been stated that all the things that are

explaining the conceptual framework cannot be applied practically because of which various

type of practical issues can be faced by them during the application of the conceptual framework

that is needed to be followed (O'Mara-Shimek, 2015). There are different functions that are

needed to be fulfilled in order to complete the accounting, reporting and disclosing process

(Leisyte & Westerheijden, 2014).

c. Academic concern

Application of a particular conceptual framework in an organization will not only provide

credibility to the financial statement but also help them to prepare a set of regulations that can be

used by them for presenting the strategies (Zeff, 2012). The worldwide acceptance of these

financial regulations will also help them to compare the financial status of various Nations

because of which the investment process can be made much easy. There are several types of

limitations that are needed to be assessed by the accountant because it will require them to leave

the reasoning and logic path behind (Nobes, 2014). The complex transactions taking place in the

organization are also becoming challenging because of which it needs to adapt to the

technological advancements in the market (Macías & Muino, 2011). Therefore, the use of proper

concepts will not only help the organization to interpret the transactions but also compare them

easily.

There are various pros and cons of the conceptual framework for financial reporting.

The positive side of the conceptual framework is that it confirms the integrity of the

financial reports of an entity (Nobes, 2014).

6

MPL VS CPI

The conceptual framework also confirms that the financials of an organization are

prepared and projected in complete accordance with the necessary policies and standards.

The conceptual framework is the same across the globe and this is why it is easier for

users from different nations to compare the financials of an organization with the

financials of other organizations (Gigler, Kanodia, Sapra & Venugopalan, 2014).

The negative side of the conceptual framework exists.

The use of a conceptual framework in the preparation and presentation of financial

statements has minimized the job of an accountant. This means the need for an

accountant is now reduced to what it used to be earlier. The role of an accountant is now

limited to just tick marking and they are no longer asked to share reasoning and their

logic pertaining to a particular issue (Nobes, 2014).

Another shortcoming of the conceptual framework is on account of the rapid

advancements in technologies taking place in the current scenario which has paved the

way for complicated transactions (Gigler, Kanodia, Sapra & Venugopalan, 2014). The

reporting and accounting of such complicated transactions have become a challenge for

the accountants. It becomes difficult to compare these complicated transactions as well as

there are huge probabilities for accountants to have numerous interpretations for the same

transaction (Donius, 2010).

d. Application of Conceptual framework by the company

The following statements are prepared by respective companies that have opted for the

conceptual framework while preparing its financial statements.

Medibank

Medibank is an Australian company and is enlisted on the Australian Securities Exchange. The

company has its headquarters in Melbourne. Medibank is in the business of providing private

health insurance for not less than forty years now. The company offers a wide range of insurance

services such as travel insurance, pet insurance, and life insurance. The company operates

through Medibank and ahm brands and presently has a consumer base of not less than 3.7

million (Medibank, 2018).

7

The conceptual framework also confirms that the financials of an organization are

prepared and projected in complete accordance with the necessary policies and standards.

The conceptual framework is the same across the globe and this is why it is easier for

users from different nations to compare the financials of an organization with the

financials of other organizations (Gigler, Kanodia, Sapra & Venugopalan, 2014).

The negative side of the conceptual framework exists.

The use of a conceptual framework in the preparation and presentation of financial

statements has minimized the job of an accountant. This means the need for an

accountant is now reduced to what it used to be earlier. The role of an accountant is now

limited to just tick marking and they are no longer asked to share reasoning and their

logic pertaining to a particular issue (Nobes, 2014).

Another shortcoming of the conceptual framework is on account of the rapid

advancements in technologies taking place in the current scenario which has paved the

way for complicated transactions (Gigler, Kanodia, Sapra & Venugopalan, 2014). The

reporting and accounting of such complicated transactions have become a challenge for

the accountants. It becomes difficult to compare these complicated transactions as well as

there are huge probabilities for accountants to have numerous interpretations for the same

transaction (Donius, 2010).

d. Application of Conceptual framework by the company

The following statements are prepared by respective companies that have opted for the

conceptual framework while preparing its financial statements.

Medibank

Medibank is an Australian company and is enlisted on the Australian Securities Exchange. The

company has its headquarters in Melbourne. Medibank is in the business of providing private

health insurance for not less than forty years now. The company offers a wide range of insurance

services such as travel insurance, pet insurance, and life insurance. The company operates

through Medibank and ahm brands and presently has a consumer base of not less than 3.7

million (Medibank, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MPL VS CPI

The company also extends services in the mental health domain and provides after-hours health

support to not less than 80,000 uniformed Australian Defence Force employees.

i. Statements

Consolidated Statement of Profit or Loss

Consolidated Statement of Profit and Loss signifies the expenses borne and the profits generated

by an organization in a particular financial year. The amount of revenues reflected in the

consolidated statement of profit or loss is attributed to the security holders of an organization as

diluted EPS or basic EPS (Medibank, 2018).

Consolidated Statement of Comprehensive Income

Consolidated Statement of Comprehensive Income signifies the rise or fall in the net profits for

the financial year which could be as a result of profit attributable to non-controlling interests and

alterations in the FV of financial assets that are available for sale. The company also offered a

detailed report and classification of its overall comprehensive income that is assigned to ongoing

as well as discontinued operational activities.

Consolidated Statement of Financial Position

The consolidated statement of financial position of Medibank is prepared on June 30, 2018. The

statement reflects the current financial position of the company with respect to the assets owned

and liabilities owed by the same as on year-end that is June 30, 2018. The company has provided

a further classification of all the assets owned and liabilities owed by the same into current and

non-current items. The remaining balance from the same is represented as equity.

Consolidated Statement of Changes in Equity

The company has prepared and presented its consolidated statement of changes in equity by

means of providing necessary additions or withdrawal of equity with respect to transactions done

by the shareholders such as share placement, shares issued, share-based payments, dividends

paid to shareholders, acquisitions of non-controlling interests and options issued. The remaining

amount after all these additions and reductions is the closing balance of equity.

8

The company also extends services in the mental health domain and provides after-hours health

support to not less than 80,000 uniformed Australian Defence Force employees.

i. Statements

Consolidated Statement of Profit or Loss

Consolidated Statement of Profit and Loss signifies the expenses borne and the profits generated

by an organization in a particular financial year. The amount of revenues reflected in the

consolidated statement of profit or loss is attributed to the security holders of an organization as

diluted EPS or basic EPS (Medibank, 2018).

Consolidated Statement of Comprehensive Income

Consolidated Statement of Comprehensive Income signifies the rise or fall in the net profits for

the financial year which could be as a result of profit attributable to non-controlling interests and

alterations in the FV of financial assets that are available for sale. The company also offered a

detailed report and classification of its overall comprehensive income that is assigned to ongoing

as well as discontinued operational activities.

Consolidated Statement of Financial Position

The consolidated statement of financial position of Medibank is prepared on June 30, 2018. The

statement reflects the current financial position of the company with respect to the assets owned

and liabilities owed by the same as on year-end that is June 30, 2018. The company has provided

a further classification of all the assets owned and liabilities owed by the same into current and

non-current items. The remaining balance from the same is represented as equity.

Consolidated Statement of Changes in Equity

The company has prepared and presented its consolidated statement of changes in equity by

means of providing necessary additions or withdrawal of equity with respect to transactions done

by the shareholders such as share placement, shares issued, share-based payments, dividends

paid to shareholders, acquisitions of non-controlling interests and options issued. The remaining

amount after all these additions and reductions is the closing balance of equity.

8

MPL VS CPI

Consolidated Statement of Cash Flows

The consolidated statement of cash flows comprises of cash flows from both ongoing and

discontinuing operations. The consolidated statement of cash flows represents the amount of

cash entry and exit from the operating, financing and investing activities of an entity.

Capitec Bank Limited

Capitec Bank Limited is a company that operates in South Africa. It was incorporated in the year

1980. The company is presently operating as a subsidiary of Capi. The company has not less than

840 branches and has close to 3000 ATMs currently all over South Africa. The company is

headquartered in Stellenbosch, South Africa. The company offers banking services to South

Africans. The organization offers various facilities such as flexible savings, transaction/savings,

credit facility, personal credit, home loan, credit card, fixed-term savings, payment solutions,

tax-free savings accounts, salary transfer facility, merchant services, Internet banking, workplace

banking, money management and transfers, debit cards, mobile and cash at tills services (Capitec

Bank Holdings Ltd. Company, 2018).

Statements

Consolidated Statement of comprehensive income

The Consolidated statement of comprehensive income represents the interest earned from

lending activities and financial assets. The revenue earned is apportioned to the shareholders as

basic EPS and diluted EPS.

Consolidated statement of financial position

The consolidated statement of financial position highlights the assets owned and liabilities owed

by the entity as on a given date.

Consolidated statement of changes in equity

The Consolidated statement of changes in equity is used to determine the closing balance if

equity as on a given date.

Consolidated statement of cash flows

9

Consolidated Statement of Cash Flows

The consolidated statement of cash flows comprises of cash flows from both ongoing and

discontinuing operations. The consolidated statement of cash flows represents the amount of

cash entry and exit from the operating, financing and investing activities of an entity.

Capitec Bank Limited

Capitec Bank Limited is a company that operates in South Africa. It was incorporated in the year

1980. The company is presently operating as a subsidiary of Capi. The company has not less than

840 branches and has close to 3000 ATMs currently all over South Africa. The company is

headquartered in Stellenbosch, South Africa. The company offers banking services to South

Africans. The organization offers various facilities such as flexible savings, transaction/savings,

credit facility, personal credit, home loan, credit card, fixed-term savings, payment solutions,

tax-free savings accounts, salary transfer facility, merchant services, Internet banking, workplace

banking, money management and transfers, debit cards, mobile and cash at tills services (Capitec

Bank Holdings Ltd. Company, 2018).

Statements

Consolidated Statement of comprehensive income

The Consolidated statement of comprehensive income represents the interest earned from

lending activities and financial assets. The revenue earned is apportioned to the shareholders as

basic EPS and diluted EPS.

Consolidated statement of financial position

The consolidated statement of financial position highlights the assets owned and liabilities owed

by the entity as on a given date.

Consolidated statement of changes in equity

The Consolidated statement of changes in equity is used to determine the closing balance if

equity as on a given date.

Consolidated statement of cash flows

9

MPL VS CPI

The Consolidated statement of cash flows represents the cash inflows and outflows from

operating, investing and financing activities.

ii. Recognition principles and measurement bases

The revenues are segregated into services and other revenue and are recognized and measured on

the basis of IFRS. Historical cost convention method is used in order to measure and display

such assets that are not to be measured at their FV or are available for sales. Various accounting

Standards and IFRS are used so as to measure the liabilities owed by the company. The liabilities

are required to be recognized at their conventional costs and then measured at their FV prior to

their measurement as per applicable Accounting Standards and IFRS.

iii. Qualitative characteristics of information in the company’s financial reports

The financial statements of the company have an essence of comparability of information. The

company has offered the financials of the previous years as well which makes it convenient for

the users to draw necessary comparisons with respect to all the segments and have a better

understanding of the financial growth and performance of the same (Clarke, 2010).

The company has also provided the necessary information pertaining to the adoption of new

policies and any alterations in the previous policies so as to guide the readers to have a better

understanding of the variations in performance.

The company has presented and projected its financials in a manner that the readers of the same

can have an easy understanding of its actual well being. The company has prepared its financials

in accordance with all the standards and necessary guidelines so as to make it easy for the users

to draw necessary comparisons with respect to different parameters between the financials of

different companies.

The presence of verifiability on the company’s part is appreciable as the company has offered

necessary notes with its financials. The notes offer proper explanations of various segments. This

not only makes the financials look verifiable but also enhances the comparability of the same.

10

The Consolidated statement of cash flows represents the cash inflows and outflows from

operating, investing and financing activities.

ii. Recognition principles and measurement bases

The revenues are segregated into services and other revenue and are recognized and measured on

the basis of IFRS. Historical cost convention method is used in order to measure and display

such assets that are not to be measured at their FV or are available for sales. Various accounting

Standards and IFRS are used so as to measure the liabilities owed by the company. The liabilities

are required to be recognized at their conventional costs and then measured at their FV prior to

their measurement as per applicable Accounting Standards and IFRS.

iii. Qualitative characteristics of information in the company’s financial reports

The financial statements of the company have an essence of comparability of information. The

company has offered the financials of the previous years as well which makes it convenient for

the users to draw necessary comparisons with respect to all the segments and have a better

understanding of the financial growth and performance of the same (Clarke, 2010).

The company has also provided the necessary information pertaining to the adoption of new

policies and any alterations in the previous policies so as to guide the readers to have a better

understanding of the variations in performance.

The company has presented and projected its financials in a manner that the readers of the same

can have an easy understanding of its actual well being. The company has prepared its financials

in accordance with all the standards and necessary guidelines so as to make it easy for the users

to draw necessary comparisons with respect to different parameters between the financials of

different companies.

The presence of verifiability on the company’s part is appreciable as the company has offered

necessary notes with its financials. The notes offer proper explanations of various segments. This

not only makes the financials look verifiable but also enhances the comparability of the same.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MPL VS CPI

Part B- integrated reporting

a. GRI versus IR

It is of common knowledge that the financial statements of the organization are vulnerable to

different kind of material misstatements. Application of various International principles and

standards, the risk of such vulnerabilities have been decreased because of which the financial

statements are being made more effective in nature (GRI, 2018). The sustainability reporting of

the integrated reporting guideline projects the major standards that is applicable to the companies

to elevate the factor of competitive advantage. When it comes to International Integrated

Reporting Framework, it enhances the reputation of the corporation and increases the

profitability. The reporting stress upon the establishment of link with the accounting, as well as

non-accounting data and the same can be put to evaluation for tracing the risks.

On the other hand, the implementation of the global reporting initiative helps the organization to

maintain sustainability reporting guidelines in the management structure which further helps it to

display all the socio-economic, environmental and other governance parameters effectively

(Bekiaris, Efthymiou & Koutoupis, 2013). It has been observed that the global reporting

initiative is a non-profit organization that consists of necessary guidelines and can be used by

any organization irrespective of its scale of operations. The fourth generation reports enable the

organization to prepare and present all the important transactions in the financial statements

(Samaha & Dahaway, 2010). Therefore, the sustainability of the report is also maintained

because of which proper implementation of the principles in the financial statements is being

observed. There is various type of accounting format that can be used by the organization while

preparing the fourth generation report (Zeff, 2014).

Proper analysis of the financial condition of the organization is very important because it will not

only help the organization to effectively conduct the tasks but also help it to utilize the capital in

the best possible way. The investors and other stakeholders always try to get hold of authentic

information in the financial statements that can help them to make decisions easily (GRI, 2018).

Therefore, it is important for the financial statements of the organization to depict a true and fair

view of the business so that it all the decisions and investment strategies can be enhanced

properly (Cheng, Green & Ko, 2012). Using proper standards and principles will not only make

11

Part B- integrated reporting

a. GRI versus IR

It is of common knowledge that the financial statements of the organization are vulnerable to

different kind of material misstatements. Application of various International principles and

standards, the risk of such vulnerabilities have been decreased because of which the financial

statements are being made more effective in nature (GRI, 2018). The sustainability reporting of

the integrated reporting guideline projects the major standards that is applicable to the companies

to elevate the factor of competitive advantage. When it comes to International Integrated

Reporting Framework, it enhances the reputation of the corporation and increases the

profitability. The reporting stress upon the establishment of link with the accounting, as well as

non-accounting data and the same can be put to evaluation for tracing the risks.

On the other hand, the implementation of the global reporting initiative helps the organization to

maintain sustainability reporting guidelines in the management structure which further helps it to

display all the socio-economic, environmental and other governance parameters effectively

(Bekiaris, Efthymiou & Koutoupis, 2013). It has been observed that the global reporting

initiative is a non-profit organization that consists of necessary guidelines and can be used by

any organization irrespective of its scale of operations. The fourth generation reports enable the

organization to prepare and present all the important transactions in the financial statements

(Samaha & Dahaway, 2010). Therefore, the sustainability of the report is also maintained

because of which proper implementation of the principles in the financial statements is being

observed. There is various type of accounting format that can be used by the organization while

preparing the fourth generation report (Zeff, 2014).

Proper analysis of the financial condition of the organization is very important because it will not

only help the organization to effectively conduct the tasks but also help it to utilize the capital in

the best possible way. The investors and other stakeholders always try to get hold of authentic

information in the financial statements that can help them to make decisions easily (GRI, 2018).

Therefore, it is important for the financial statements of the organization to depict a true and fair

view of the business so that it all the decisions and investment strategies can be enhanced

properly (Cheng, Green & Ko, 2012). Using proper standards and principles will not only make

11

MPL VS CPI

the financial statements look effective in nature but also will enhance the decision-making

function of the users of the financial statements..

b. Strengths and limitations of conventional accounting based on the conceptual

framework

Advantages

• Implementation of such a reporting system helps an organization to determine the problems

of accounting and provide proper guidance to accounting standards (Bertilsson, 2017).

• The use of conventional accounting system provides a framework that further helps to

practice particular accounting standards (Zeff, 2014).

• Proper application of a conceptual framework candy made because of which the reliability of

the financial statements is enhanced (Bertilsson, 2017).

Disadvantages

• It is not easy to develop the framework.

• The rigidity in the standards makes it difficult for implementation in the framework of the

organization.

• There may be differences observed in the framework and accounting standards.

c. Application of theories

The institutional theory or neo-institutional theory is being used by the organization to explore or

demonstrate the development of the monetary, social, money related and political aspects assets

a huge pressure on the associations. The results provide an integrated highlight is linked with the

era of monetary enhancement, national corporate duty and other framework. The policy makers

refused to project the influence of the political factor that underlines information irregularity in

tune to the years for which the gathering of data has been done provided the examination has o

relevance to the assumptions in the significant changes in the political framework.

12

the financial statements look effective in nature but also will enhance the decision-making

function of the users of the financial statements..

b. Strengths and limitations of conventional accounting based on the conceptual

framework

Advantages

• Implementation of such a reporting system helps an organization to determine the problems

of accounting and provide proper guidance to accounting standards (Bertilsson, 2017).

• The use of conventional accounting system provides a framework that further helps to

practice particular accounting standards (Zeff, 2014).

• Proper application of a conceptual framework candy made because of which the reliability of

the financial statements is enhanced (Bertilsson, 2017).

Disadvantages

• It is not easy to develop the framework.

• The rigidity in the standards makes it difficult for implementation in the framework of the

organization.

• There may be differences observed in the framework and accounting standards.

c. Application of theories

The institutional theory or neo-institutional theory is being used by the organization to explore or

demonstrate the development of the monetary, social, money related and political aspects assets

a huge pressure on the associations. The results provide an integrated highlight is linked with the

era of monetary enhancement, national corporate duty and other framework. The policy makers

refused to project the influence of the political factor that underlines information irregularity in

tune to the years for which the gathering of data has been done provided the examination has o

relevance to the assumptions in the significant changes in the political framework.

12

MPL VS CPI

There are a lot of benefits that can be acquired by an organization if it is having a proper

sustainable reporting system. This kind of reporting system not only helps the organization to

identify different type of sustainable activities that can be carried out by it but also the legality of

the same. It is very important for an organization to conduct the day-to-day operations legally so

that it does not face any kind of difficulty in the future (Schneider, Johnston & Down, 2017). In

order to maintain the sustainability of the financial statements of an organization, it is very

important for the accountants to produce all the transactions in the statements and prepare the

reports in accordance with the legal requirements (Zeff, 2014). Proper financial reports of the

organization will also have invested to confirm the actual profit that is being earned by it. The

environmental and social factors I said to affect the business of the organization (Black, 2010).

Hence, it is important for an organization to always enhance the environment and society by

conducting social activities. The companies are asked to operate in a manner that will be very

helpful for the society and the business at the same time (Bhandari & Adams, 2017). If the

organization is not able to maintain good relations with the society and environment then it may

observe the impact on the workforce and then the internal environment of the organization

because of which the capital structure can be compromised (Wahlen, 2014). All these factors can

collectively disintegrate the organization because of which the lawfulness and legal power of the

entity can harm the governance practices that are being carried out by the organization in order to

have a sustainable reporting system (Tan,2016).

The relationship of the organization and environment is very important because it will not only

help to maintain the integrity of the organizational framework but will also affect the capital

structure and workforce at the same time. The ethnicity of the relationship of the organization

and environment must be evaluated by the corporate structure so that it can be of best interest to

the organization (Wahlen, 2014). The company should carry out all the operations and activities

in the best interest of society and environment so that proper ethnicity can be maintained while

conducting the activities.

d. Index or Checklist

The integrated report of an organization consists of various components that help it to evaluate

the position of the business in the market. It also enables the organization to determine the

structure of government under which it is functioning. Proper utilization of integrated reporting

13

There are a lot of benefits that can be acquired by an organization if it is having a proper

sustainable reporting system. This kind of reporting system not only helps the organization to

identify different type of sustainable activities that can be carried out by it but also the legality of

the same. It is very important for an organization to conduct the day-to-day operations legally so

that it does not face any kind of difficulty in the future (Schneider, Johnston & Down, 2017). In

order to maintain the sustainability of the financial statements of an organization, it is very

important for the accountants to produce all the transactions in the statements and prepare the

reports in accordance with the legal requirements (Zeff, 2014). Proper financial reports of the

organization will also have invested to confirm the actual profit that is being earned by it. The

environmental and social factors I said to affect the business of the organization (Black, 2010).

Hence, it is important for an organization to always enhance the environment and society by

conducting social activities. The companies are asked to operate in a manner that will be very

helpful for the society and the business at the same time (Bhandari & Adams, 2017). If the

organization is not able to maintain good relations with the society and environment then it may

observe the impact on the workforce and then the internal environment of the organization

because of which the capital structure can be compromised (Wahlen, 2014). All these factors can

collectively disintegrate the organization because of which the lawfulness and legal power of the

entity can harm the governance practices that are being carried out by the organization in order to

have a sustainable reporting system (Tan,2016).

The relationship of the organization and environment is very important because it will not only

help to maintain the integrity of the organizational framework but will also affect the capital

structure and workforce at the same time. The ethnicity of the relationship of the organization

and environment must be evaluated by the corporate structure so that it can be of best interest to

the organization (Wahlen, 2014). The company should carry out all the operations and activities

in the best interest of society and environment so that proper ethnicity can be maintained while

conducting the activities.

d. Index or Checklist

The integrated report of an organization consists of various components that help it to evaluate

the position of the business in the market. It also enables the organization to determine the

structure of government under which it is functioning. Proper utilization of integrated reporting

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MPL VS CPI

system will help the organization to conduct business easily in both short and long-term

(Bhattacharya & Sen, 2010). It is important for the management structure of the organization to

evaluate the business model.

Environment

The IR must comprise of all the compliances that are done in respect to the environment. The

framework depends on the company’s functioning and the geographical condition.

● Socio-Political

The report should comprise of the structure of federal governance that helps the firm to create

the anticipated value in the market.

Risks

It is necessary for an organization to determine all the risks and opportunities that are in its way

so that proper flow of operations can be determined.

Resource management

Management of course and expenses are very important for the organization to allocate and

appropriately use the resources in accordance with the budget.

● Health & Safety (H&S)

14

system will help the organization to conduct business easily in both short and long-term

(Bhattacharya & Sen, 2010). It is important for the management structure of the organization to

evaluate the business model.

Environment

The IR must comprise of all the compliances that are done in respect to the environment. The

framework depends on the company’s functioning and the geographical condition.

● Socio-Political

The report should comprise of the structure of federal governance that helps the firm to create

the anticipated value in the market.

Risks

It is necessary for an organization to determine all the risks and opportunities that are in its way

so that proper flow of operations can be determined.

Resource management

Management of course and expenses are very important for the organization to allocate and

appropriately use the resources in accordance with the budget.

● Health & Safety (H&S)

14

MPL VS CPI

An IR must comprise of the regulations that deals with the H&S that helps the company to keep

a tab on the strategies that concerns the avoidance of the strategic challenges on HS

● People

This is one of the major factors that is vital for the attainment of strategic goals to financial

outcomes and period. Having the correct people is having an asset because it trends to create

competitive advantage.

● Strategy and resource allocation

The explanation of the strategy that has been undertaken to attain the goals of the

organization. Further, it must state whether the entity ensure sustainability and differentiate

from others in the sector.

15

An IR must comprise of the regulations that deals with the H&S that helps the company to keep

a tab on the strategies that concerns the avoidance of the strategic challenges on HS

● People

This is one of the major factors that is vital for the attainment of strategic goals to financial

outcomes and period. Having the correct people is having an asset because it trends to create

competitive advantage.

● Strategy and resource allocation

The explanation of the strategy that has been undertaken to attain the goals of the

organization. Further, it must state whether the entity ensure sustainability and differentiate

from others in the sector.

15

MPL VS CPI

● Performance

The performance should be clearly established and provide a clear view of the performance of

the organization.

● Capitec has disclosed the seven principles in the annual report that projects an

understanding that all the activities has been undertaken and compliances are properly

done. The company has briefed regarding the operating environment, leadership review,

risk management, employees, remuneration report, and social responsibility

16

● Performance

The performance should be clearly established and provide a clear view of the performance of

the organization.

● Capitec has disclosed the seven principles in the annual report that projects an

understanding that all the activities has been undertaken and compliances are properly

done. The company has briefed regarding the operating environment, leadership review,

risk management, employees, remuneration report, and social responsibility

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MPL VS CPI

e. Comparison of Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African Company

As per the preparation of index of major components in the integrated report, it can be observed

that Capitec has prepared and adhered to all the components. All the key components has been

clearly reflected in the Integrated report 2018. The company has introduced new integrated

system that is used to manage strategy, operations, as well as risk. Similarly Capitec works

towards the attainment of goals by providing a strong emphasis on the society. It strives to

provide better quality education and different facilities to the employees (Capitec Bank Holdings

Ltd. Company, 2018).

17

e. Comparison of Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African Company

As per the preparation of index of major components in the integrated report, it can be observed

that Capitec has prepared and adhered to all the components. All the key components has been

clearly reflected in the Integrated report 2018. The company has introduced new integrated

system that is used to manage strategy, operations, as well as risk. Similarly Capitec works

towards the attainment of goals by providing a strong emphasis on the society. It strives to

provide better quality education and different facilities to the employees (Capitec Bank Holdings

Ltd. Company, 2018).

17

MPL VS CPI

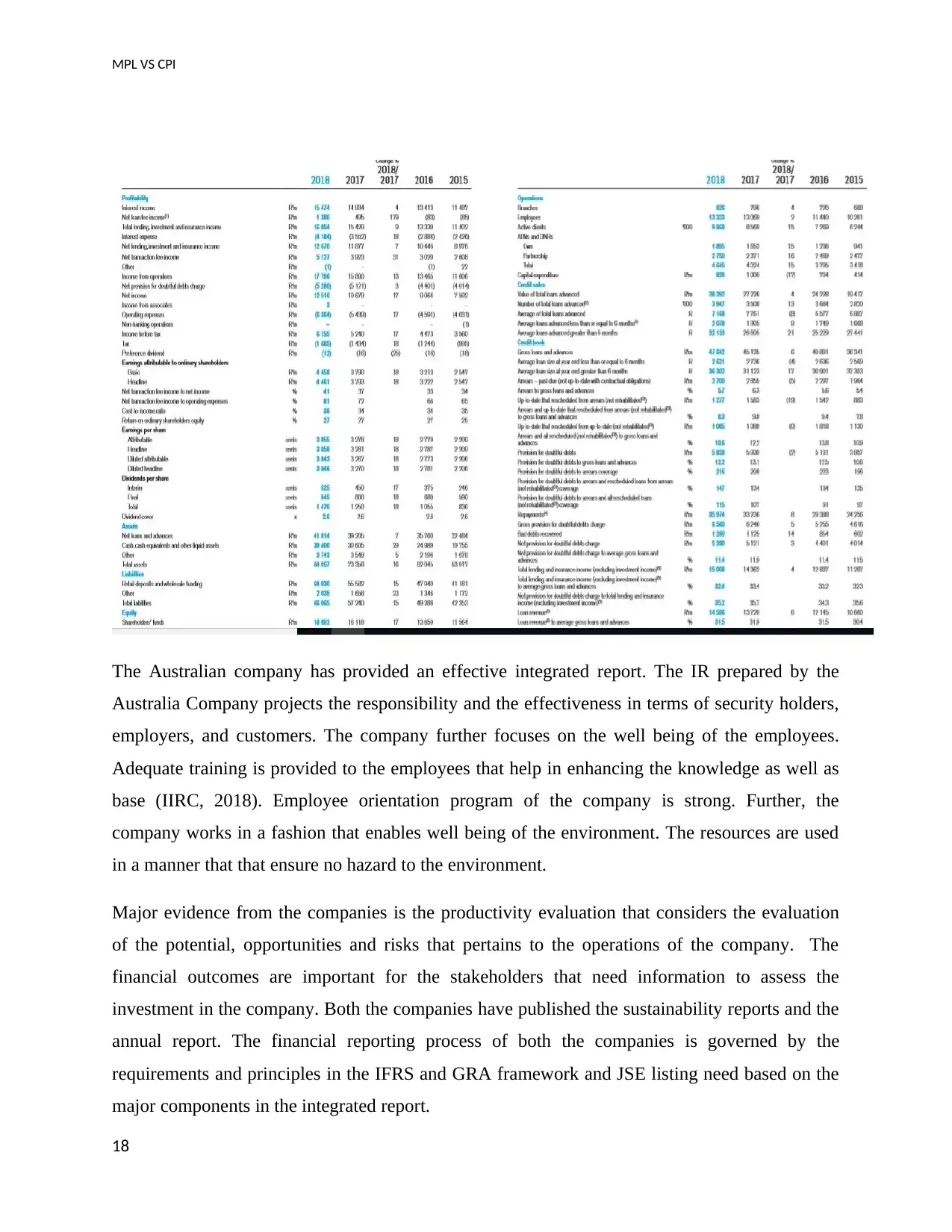

The Australian company has provided an effective integrated report. The IR prepared by the

Australia Company projects the responsibility and the effectiveness in terms of security holders,

employers, and customers. The company further focuses on the well being of the employees.

Adequate training is provided to the employees that help in enhancing the knowledge as well as

base (IIRC, 2018). Employee orientation program of the company is strong. Further, the

company works in a fashion that enables well being of the environment. The resources are used

in a manner that that ensure no hazard to the environment.

Major evidence from the companies is the productivity evaluation that considers the evaluation

of the potential, opportunities and risks that pertains to the operations of the company. The

financial outcomes are important for the stakeholders that need information to assess the

investment in the company. Both the companies have published the sustainability reports and the

annual report. The financial reporting process of both the companies is governed by the

requirements and principles in the IFRS and GRA framework and JSE listing need based on the

major components in the integrated report.

18

The Australian company has provided an effective integrated report. The IR prepared by the

Australia Company projects the responsibility and the effectiveness in terms of security holders,

employers, and customers. The company further focuses on the well being of the employees.

Adequate training is provided to the employees that help in enhancing the knowledge as well as

base (IIRC, 2018). Employee orientation program of the company is strong. Further, the

company works in a fashion that enables well being of the environment. The resources are used

in a manner that that ensure no hazard to the environment.

Major evidence from the companies is the productivity evaluation that considers the evaluation

of the potential, opportunities and risks that pertains to the operations of the company. The

financial outcomes are important for the stakeholders that need information to assess the

investment in the company. Both the companies have published the sustainability reports and the

annual report. The financial reporting process of both the companies is governed by the

requirements and principles in the IFRS and GRA framework and JSE listing need based on the

major components in the integrated report.

18

MPL VS CPI

Conclusion

Going by the study, it can be commented that both the companies has complied with the

principles of sustainability reporting. Moreover, as per the annual report, it has been noted that

the conceptual framework is effectively followed. The principle CF has provided immense

benefit to the company in terms of credibility and exposure. The financial reporting has been

effective with the presence of CF. The integrated and sustainability reporting has been a driving

force and is a major component it comes to the reporting form. Moreover, it stress upon the role

played by the society for the benefit of the society as a whole.

19

Conclusion

Going by the study, it can be commented that both the companies has complied with the

principles of sustainability reporting. Moreover, as per the annual report, it has been noted that

the conceptual framework is effectively followed. The principle CF has provided immense

benefit to the company in terms of credibility and exposure. The financial reporting has been

effective with the presence of CF. The integrated and sustainability reporting has been a driving

force and is a major component it comes to the reporting form. Moreover, it stress upon the role

played by the society for the benefit of the society as a whole.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MPL VS CPI

References

Barth, M. E. (2013). Global Comparability in Financial Reporting: What, Why, How, and

When?. China Journal of Accounting Studies 1(1), 2–12. Doi:

10.1080/21697221.2013.781765).

Bekiaris, M., Efthymiou, T., & Koutoupis, A. G. (2013). Economic crisis impact on corporate

governance & internal audit: The case of Greece. Corporate Ownership & Control,

11(1), 55-64. Retrieved from https://doi.org/10.22495/cocv11i1art5

Bertilsson, J. (2017). The slippery relationship between brand ethic and profit. Retrieved

from http://www.ephemerajournal.org/contribution/slippery-relationship-between-

brand-ethic-and-profit

Bhandari, S.B. and Adams, M.T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), p.11.

Bhattacharya, Du S & Sen S, CB. (2010) Maximizing business returns to corporate social

responsibility (CSR): The role of CSR communication. Management Review, 12(8),

19-26. Retrieved from:

https://www.academia.edu/31227763/Maximizing_Business_Returns_to_Corporate_S

ocial_Responsibility_CSR_The_Role_of_CSR_Communication

Black, W. K. (2010). Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles

and Crises. Working paper, University of Missouri-Kansas City.

Capitec Bank Holdings Ltd. Company (2018). Capitec Bank Holdings Ltd. Company 2018

annual report & accounts. Retrieved from:

https://resources.capitecbank.co.za/capitec_bank_integrated_annual_report_2018.pdf

20

References

Barth, M. E. (2013). Global Comparability in Financial Reporting: What, Why, How, and

When?. China Journal of Accounting Studies 1(1), 2–12. Doi:

10.1080/21697221.2013.781765).

Bekiaris, M., Efthymiou, T., & Koutoupis, A. G. (2013). Economic crisis impact on corporate

governance & internal audit: The case of Greece. Corporate Ownership & Control,

11(1), 55-64. Retrieved from https://doi.org/10.22495/cocv11i1art5

Bertilsson, J. (2017). The slippery relationship between brand ethic and profit. Retrieved

from http://www.ephemerajournal.org/contribution/slippery-relationship-between-

brand-ethic-and-profit

Bhandari, S.B. and Adams, M.T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), p.11.

Bhattacharya, Du S & Sen S, CB. (2010) Maximizing business returns to corporate social

responsibility (CSR): The role of CSR communication. Management Review, 12(8),

19-26. Retrieved from:

https://www.academia.edu/31227763/Maximizing_Business_Returns_to_Corporate_S

ocial_Responsibility_CSR_The_Role_of_CSR_Communication

Black, W. K. (2010). Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles

and Crises. Working paper, University of Missouri-Kansas City.

Capitec Bank Holdings Ltd. Company (2018). Capitec Bank Holdings Ltd. Company 2018

annual report & accounts. Retrieved from:

https://resources.capitecbank.co.za/capitec_bank_integrated_annual_report_2018.pdf

20

MPL VS CPI

Cheng, M., Green, W. & Ko, J. (2012). The impact of sustainability assurance and company

strategy on investors’ decisions. Melbourne.

Clarke, T. (2010) International Corporate Governance. London and New York, Routledge,

Donius, B. (2010) Profit Maximization - Ethics = The ‘Goldman Standard . Retrieved

from http://www.huffingtonpost.com/bill-donius/profit-maximization---

eth_b_553605.html

Gerber, M. C., Gerber, A. J., and Van der Merwe, A. J. (2014). An Analysis of Fundamental

Concepts in the Conceptual Framework Using Ontology Technologies. South African

Journal of Economic & Management Sciences 17(4), 396–411. Retrieved from

http://www.sajems.org/index.php/sajems/article/view/525/434

Gigler, F., Kanodia, C., Sapra, H. and Venugopalan, R. (2014). How Frequent Financial

Reporting Can Cause Managerial Short‐Termism: An Analysis of the Costs and

Benefits of Increasing Reporting Frequency. Journal of Accounting Research, 52(2),

357-387. Retrieved from: https://doi.org/10.1111/1475-679X.12043

GRI. (2018) Global reporting index. Retrieved from

https://www.globalreporting.org/Pages/default.aspx

IASB.(2013) A Review of the Conceptual Framework for Financial Reporting. DP/2013/1

No. DP/2013/1, Discussion Paper. London: United Kingdom. Retrieved from

http://www.ifrs.org/Current-Projects/IASB-Projects/Conceptual-Framework/

Discussion- Paper-July-2013/Documents/Discussion-Paper-Conceptual-Framework-

July-2013.pdf).

IIRC. (2018) Integrated reporting. Retrieved from https://integratedreporting.org/iirc-website-

terms-of-use/

Leisyte, I & Westerheijden, D.F. (2014). Stakeholders and Quality Assurance in Education.

Oxford university Press.

Macías, M., and Muino, F. (2011) Examining dual accounting systems in Europe. The

International Journal of Accounting 46(1), 51–78. Doi: 10.1016/j.intacc.2010.12.001).

21

Cheng, M., Green, W. & Ko, J. (2012). The impact of sustainability assurance and company

strategy on investors’ decisions. Melbourne.

Clarke, T. (2010) International Corporate Governance. London and New York, Routledge,

Donius, B. (2010) Profit Maximization - Ethics = The ‘Goldman Standard . Retrieved

from http://www.huffingtonpost.com/bill-donius/profit-maximization---

eth_b_553605.html

Gerber, M. C., Gerber, A. J., and Van der Merwe, A. J. (2014). An Analysis of Fundamental

Concepts in the Conceptual Framework Using Ontology Technologies. South African

Journal of Economic & Management Sciences 17(4), 396–411. Retrieved from

http://www.sajems.org/index.php/sajems/article/view/525/434

Gigler, F., Kanodia, C., Sapra, H. and Venugopalan, R. (2014). How Frequent Financial

Reporting Can Cause Managerial Short‐Termism: An Analysis of the Costs and

Benefits of Increasing Reporting Frequency. Journal of Accounting Research, 52(2),

357-387. Retrieved from: https://doi.org/10.1111/1475-679X.12043

GRI. (2018) Global reporting index. Retrieved from

https://www.globalreporting.org/Pages/default.aspx

IASB.(2013) A Review of the Conceptual Framework for Financial Reporting. DP/2013/1

No. DP/2013/1, Discussion Paper. London: United Kingdom. Retrieved from

http://www.ifrs.org/Current-Projects/IASB-Projects/Conceptual-Framework/

Discussion- Paper-July-2013/Documents/Discussion-Paper-Conceptual-Framework-

July-2013.pdf).

IIRC. (2018) Integrated reporting. Retrieved from https://integratedreporting.org/iirc-website-

terms-of-use/

Leisyte, I & Westerheijden, D.F. (2014). Stakeholders and Quality Assurance in Education.

Oxford university Press.

Macías, M., and Muino, F. (2011) Examining dual accounting systems in Europe. The

International Journal of Accounting 46(1), 51–78. Doi: 10.1016/j.intacc.2010.12.001).

21

MPL VS CPI

Masquefa, B., and Teller, P. (2010). Towards a theoretical framework for the diffusion of

accounting and control system in 2010 Fourth International Conference on Research

Challenges in Information Science (RCIS), IEEE. pp. 599–606.Doi:

10.1109/RCIS.2010.5507293)

Medibank. (2018). Medibank Company 2018. Retrieved from:

https://www.medibank.com.au/about/investor-centre/

Nobes, C. (2014). International Classification of Financial Reporting (3rd ed.). New York:

Retrieved from https://books.google.com/books?

hl=en&lr=&id=yow9BAAAQBAJ&pgis=1

O'Mara-Shimek,M. (2015). A communicative efficiency and effectiveness model for

using metaphor and metonymy in financial news reporting On the Horizon,

23(3), .216-230, Retrieved from https://doi.org/10.1108/OTH-06-2015-0030

Page, M. (2015). The search for a conceptual framework: Quest for a holy grail, or

hunting a snark?. Accounting, Auditing & Accountability Journal, 18(4), 565-576.

Retrieved from https://doi.org/10.1108/09513570510609360

Samaha, K. & Dahaway, K. (2010). Factors influencing corporate disclosure transparency, in

the active share trading firms: An Explanatory study. Research in Emerging

Economies, 10, 87-118. DOI: 10.1108/S1479-3563(2010)0000010009

Schneider, G., Johnston, P. & Down, K. (2017). What is Risk Intelligence? Risk Management

Today. 27(3), 43-47. Retrieved from:

https://risk2solution.com/wp-content/uploads/2018/12/Risk-Culture-Getting-it-right.-

White-Paper.pdf

Tan, B.S. (2016). Interim financial reporting: how frequent should it be?. International

Journal of Economics and Accounting, 7(2),116-126. Retrieved from

https://doi.org/10.1504/IJEA.2016.078304

Wahlen, J. (2014). Financial Reporting, Financial Statement Analysis and Valuation/James.

Cengage Learning.

22

Masquefa, B., and Teller, P. (2010). Towards a theoretical framework for the diffusion of

accounting and control system in 2010 Fourth International Conference on Research

Challenges in Information Science (RCIS), IEEE. pp. 599–606.Doi:

10.1109/RCIS.2010.5507293)

Medibank. (2018). Medibank Company 2018. Retrieved from:

https://www.medibank.com.au/about/investor-centre/

Nobes, C. (2014). International Classification of Financial Reporting (3rd ed.). New York:

Retrieved from https://books.google.com/books?

hl=en&lr=&id=yow9BAAAQBAJ&pgis=1

O'Mara-Shimek,M. (2015). A communicative efficiency and effectiveness model for

using metaphor and metonymy in financial news reporting On the Horizon,

23(3), .216-230, Retrieved from https://doi.org/10.1108/OTH-06-2015-0030

Page, M. (2015). The search for a conceptual framework: Quest for a holy grail, or

hunting a snark?. Accounting, Auditing & Accountability Journal, 18(4), 565-576.

Retrieved from https://doi.org/10.1108/09513570510609360

Samaha, K. & Dahaway, K. (2010). Factors influencing corporate disclosure transparency, in

the active share trading firms: An Explanatory study. Research in Emerging

Economies, 10, 87-118. DOI: 10.1108/S1479-3563(2010)0000010009

Schneider, G., Johnston, P. & Down, K. (2017). What is Risk Intelligence? Risk Management

Today. 27(3), 43-47. Retrieved from:

https://risk2solution.com/wp-content/uploads/2018/12/Risk-Culture-Getting-it-right.-

White-Paper.pdf

Tan, B.S. (2016). Interim financial reporting: how frequent should it be?. International

Journal of Economics and Accounting, 7(2),116-126. Retrieved from

https://doi.org/10.1504/IJEA.2016.078304

Wahlen, J. (2014). Financial Reporting, Financial Statement Analysis and Valuation/James.

Cengage Learning.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MPL VS CPI

Zeff, S. A. (2012). Development of Accounting Standards in Handbook of Key Global

Financial Markets, Institutions, and Infrastructure. Academic Press. Retrieved from

http://0- proquestcombo.safaribooksonline.com.innopac.up.ac.za/book/finance/

9780123978738/ii-

key-market-institutions-and-infrastructure-in-global-finance/chp030_html).

23

Zeff, S. A. (2012). Development of Accounting Standards in Handbook of Key Global

Financial Markets, Institutions, and Infrastructure. Academic Press. Retrieved from

http://0- proquestcombo.safaribooksonline.com.innopac.up.ac.za/book/finance/

9780123978738/ii-

key-market-institutions-and-infrastructure-in-global-finance/chp030_html).

23

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.