Contemporary Accounting Theory Report: Australian Company Analysis

VerifiedAdded on 2021/02/20

|12

|4133

|265

Report

AI Summary

This report delves into contemporary accounting theory, exploring the history and development of conceptual frameworks for financial reporting, particularly within the context of the International Accounting Standards Board (IASB). It examines the concerns of Australian accounting professionals and academics regarding these frameworks, and illustrates their application through the example of Infigen Energy Limited. The report further compares the Global Reporting Initiative (GRI) and the International Integrated Reporting Framework, highlighting their roles in corporate social responsibility. It discusses the rigor of conventional accounting, the theories used to explain sustainability and integrated reports, and the components of an integrated report, using Montauk Holdings Limited as a case study. Finally, the report contrasts Australian companies' approaches to corporate social responsibility and financial performance reporting, providing a comprehensive overview of contemporary accounting practices and challenges.

Contemporary

Accounting Theory

Accounting Theory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

PART 1............................................................................................................................................1

1. Explain the history and development of conceptual framework for financial reporting.........1

2. Explain Australian accounting professions concern regarding conceptual framework...........2

3. Discussed the academic concern regarding conceptual framework........................................3

4. How conceptual framework applied by the Australian company............................................4

PART B............................................................................................................................................5

1. Compare Global Reporting Initiative (GRI) and International Integrated Reporting

Framework for the holistic view of corporate social responsibility............................................5

2. Rigour of conventional accounting..........................................................................................1

3. Explain the required theory which is used to explain the contents of sustainability as well as

integrated reports.........................................................................................................................2

4. Components of integrated report of Montauk Holdings Limited...........................................2

5. Compare the context of Australian company corporate social responsibility in addition to

report it's financial performance..................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................5

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

PART 1............................................................................................................................................1

1. Explain the history and development of conceptual framework for financial reporting.........1

2. Explain Australian accounting professions concern regarding conceptual framework...........2

3. Discussed the academic concern regarding conceptual framework........................................3

4. How conceptual framework applied by the Australian company............................................4

PART B............................................................................................................................................5

1. Compare Global Reporting Initiative (GRI) and International Integrated Reporting

Framework for the holistic view of corporate social responsibility............................................5

2. Rigour of conventional accounting..........................................................................................1

3. Explain the required theory which is used to explain the contents of sustainability as well as

integrated reports.........................................................................................................................2

4. Components of integrated report of Montauk Holdings Limited...........................................2

5. Compare the context of Australian company corporate social responsibility in addition to

report it's financial performance..................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................5

INTRODUCTION

Accounting theory is a logical reasoning which include the different set of principle and

provide overall guidelines in order to build their financial reporting which contain all the

financial informational. Accounting principle include various practices which help the manager

to maintain their transaction for the further analysis (Bedford and Ziegler, 2016). It will help the

manager to build strategy and take effective decision in order to achieve their goals & objectives.

Infigen Energy Limited company selected for the better understanding of this concepts.

Company generate electricity from renewable sources and it was founded in 2003 and provide

renewable energy assets management services. This report include the various topics such as

conceptual framework for financial reporting under the umbrella of International Accounting

Standard Board (IASB). Application of IASB for the financial reporting. In addition, it include

the conventional accounting which explain the sustainability or integrated report. Along with

this, this report include the comparison of Australian company's reporting practices.

MAIN BODY

PART 1

1. Explain the history and development of conceptual framework for financial reporting

Conceptual framework is the theory of accounting which provide the clear guidelines

regarding developing their financial reporting. It is a set of idea, rules, guidelines which help the

organization to maintain their daily transaction in order to develop proper financial report. It will

help the business and their users for building strategy in order to provide effective or efficient

information. Which further helps in increasing productivity or profitability of the company.

International Accounting Standard Board (IASB) is independent body which approve the

International Financial Reporting Standard (IFRS). IASB founded in 2001 after replacing

International Accounting Standard Committee (IASC). IASC establish in 1973 and after this,

various amendments will take place and introduce IASB.

Purpose of the framework is to assist IASB and developing IFRS which is based on

various concepts. It include those activities or policies which is not included in the accounting

standard. Manager of the company follow the judgement which helps in making information

reliable or relevant for the organization. These framework use for the development of financial

reporting where day to day activity are recorded for the further functioning.

1

Accounting theory is a logical reasoning which include the different set of principle and

provide overall guidelines in order to build their financial reporting which contain all the

financial informational. Accounting principle include various practices which help the manager

to maintain their transaction for the further analysis (Bedford and Ziegler, 2016). It will help the

manager to build strategy and take effective decision in order to achieve their goals & objectives.

Infigen Energy Limited company selected for the better understanding of this concepts.

Company generate electricity from renewable sources and it was founded in 2003 and provide

renewable energy assets management services. This report include the various topics such as

conceptual framework for financial reporting under the umbrella of International Accounting

Standard Board (IASB). Application of IASB for the financial reporting. In addition, it include

the conventional accounting which explain the sustainability or integrated report. Along with

this, this report include the comparison of Australian company's reporting practices.

MAIN BODY

PART 1

1. Explain the history and development of conceptual framework for financial reporting

Conceptual framework is the theory of accounting which provide the clear guidelines

regarding developing their financial reporting. It is a set of idea, rules, guidelines which help the

organization to maintain their daily transaction in order to develop proper financial report. It will

help the business and their users for building strategy in order to provide effective or efficient

information. Which further helps in increasing productivity or profitability of the company.

International Accounting Standard Board (IASB) is independent body which approve the

International Financial Reporting Standard (IFRS). IASB founded in 2001 after replacing

International Accounting Standard Committee (IASC). IASC establish in 1973 and after this,

various amendments will take place and introduce IASB.

Purpose of the framework is to assist IASB and developing IFRS which is based on

various concepts. It include those activities or policies which is not included in the accounting

standard. Manager of the company follow the judgement which helps in making information

reliable or relevant for the organization. These framework use for the development of financial

reporting where day to day activity are recorded for the further functioning.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Primary purpose of the financial reporting is to show all the financial information to the

potential investors, lenders and creditors. With the help of these information individual can take

decision regarding their investments and manager of the company to develop strategy for the

further functioning. Financial reporting include the various statements such as profits & loss

accounts, balance sheet and cash flow statements (Budding, Grossi and Tagesson, 2014).

Financial reporting required for the disclosure of financial information for their users

which attract the stakeholders to make their decision regarding investment. With the help of

reporting, internal as well as external users can identify the financial position of the company for

the specific time period weather it is profitable or not. Stakeholders are included, potential

investors, debtor, customers, employees, owner, government, supplier etc.

2. Explain Australian accounting professions concern regarding conceptual framework

In the United State, conceptual framework define as a coherent system of interrelated

objectives. Conceptual framework include the nature of business, functions, limitation and

requirement of financial accounting and reporting. In the Australia, it is consider as a series of

Statement of Accounting Concepts which include the purpose, nature and general purpose of

maintain their records and develop financial reporting.

In 2005, there is a change in the Australian conceptual framework and it will be

developed as International Accounting Standard Broad (IASB). As per accounting professionals,

conceptual framework help the every organization in order to develop their financial report

which include various standards, rules and guidelines. Firstly, organization have to identify the

purpose of developing financial report and then objectives. Information can be qualitative or

quantitative which affect the business in order to increase their sale and profit. Through

attracting consumers and potential investors to achieve their organizational goals & objectives.

As time passes, accounting professionals attract great deal of criticism and it will

generate due to lack of agreement which is greater issue as per the legitimacy perspective. They

also required conceptual framework for the effective analysis. Which help the Australian

company in order to follow all the standards and develop their financial report which is

necessary for the business to know their actual position in terms of market share of profitability

(Carnegie, 2014). Now most of the countries develop their own conceptual framework which is

similar to the IASB. Conceptual framework provide fundamentals of an accounting system

2

potential investors, lenders and creditors. With the help of these information individual can take

decision regarding their investments and manager of the company to develop strategy for the

further functioning. Financial reporting include the various statements such as profits & loss

accounts, balance sheet and cash flow statements (Budding, Grossi and Tagesson, 2014).

Financial reporting required for the disclosure of financial information for their users

which attract the stakeholders to make their decision regarding investment. With the help of

reporting, internal as well as external users can identify the financial position of the company for

the specific time period weather it is profitable or not. Stakeholders are included, potential

investors, debtor, customers, employees, owner, government, supplier etc.

2. Explain Australian accounting professions concern regarding conceptual framework

In the United State, conceptual framework define as a coherent system of interrelated

objectives. Conceptual framework include the nature of business, functions, limitation and

requirement of financial accounting and reporting. In the Australia, it is consider as a series of

Statement of Accounting Concepts which include the purpose, nature and general purpose of

maintain their records and develop financial reporting.

In 2005, there is a change in the Australian conceptual framework and it will be

developed as International Accounting Standard Broad (IASB). As per accounting professionals,

conceptual framework help the every organization in order to develop their financial report

which include various standards, rules and guidelines. Firstly, organization have to identify the

purpose of developing financial report and then objectives. Information can be qualitative or

quantitative which affect the business in order to increase their sale and profit. Through

attracting consumers and potential investors to achieve their organizational goals & objectives.

As time passes, accounting professionals attract great deal of criticism and it will

generate due to lack of agreement which is greater issue as per the legitimacy perspective. They

also required conceptual framework for the effective analysis. Which help the Australian

company in order to follow all the standards and develop their financial report which is

necessary for the business to know their actual position in terms of market share of profitability

(Carnegie, 2014). Now most of the countries develop their own conceptual framework which is

similar to the IASB. Conceptual framework provide fundamentals of an accounting system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which is more suitable for the organization because here manager is accountable for their own

decision.

It provide the clear explanation regarding each action or activity which accountant going

to perform in order to prepare their accounts for the disclosure in the annual reports. Which help

the manager to build effective strategy for the business and take decision for the further

development or achievement of their goals & objectives. Company develop a plan as well as

budget for the company which help the manager to identify the operational problem which is

resolve by following various management accounting system or reporting.

3. Discussed the academic concern regarding conceptual framework

According to Musiolik, Markard and Hekkert 2012, accounting standard is more

consistent and logical which help the organization to record daily transaction as per their

treatment which provide accurate results regarding their financial position in the market.

Conceptual framework provide various importance which increase the international

compatibility of accounting standard, standards setter will be more accountable because they

have to take decision. Accountant professionals compare the standard and constitution which

helps in increasing their accuracy at the time of performing their duty. Development of

accounting standard should be more economical where conceptual framework include all the

issues which reduce the need of additional standard. It will emphasis the role of financial report

rather then restricting concern to the stewardship to make decision useful.

As per Houqe, van Zijl, Dunstan and Karim 2012, conceptual framework provide the

various IFRS which help the organization to follow these standards and develop accurate report

for the external as well as internal users. These financial reports help the individual to take their

decision on the basis of available financial information. It is suggested that, quality of earning is

important to increase because it will protect the investors and provide them strong evidence to

take decision with the available data. In the conceptual framework, it is important to sate the

interest of investors for the financial reporting quality and it is required for the regulation and

maintain the limit of manager and complete their management practices.

Michelon, Pilonato and Ricceri 2015 state that, for the smaller organization it is very

difficult to complete their task in order to achieve their goals & objectives. Small company feel

burden to follow all the relevant accounting standard which is required to implement for the

accurate result in order to achieve their business goals & objectives. Biggest disadvantage of the

3

decision.

It provide the clear explanation regarding each action or activity which accountant going

to perform in order to prepare their accounts for the disclosure in the annual reports. Which help

the manager to build effective strategy for the business and take decision for the further

development or achievement of their goals & objectives. Company develop a plan as well as

budget for the company which help the manager to identify the operational problem which is

resolve by following various management accounting system or reporting.

3. Discussed the academic concern regarding conceptual framework

According to Musiolik, Markard and Hekkert 2012, accounting standard is more

consistent and logical which help the organization to record daily transaction as per their

treatment which provide accurate results regarding their financial position in the market.

Conceptual framework provide various importance which increase the international

compatibility of accounting standard, standards setter will be more accountable because they

have to take decision. Accountant professionals compare the standard and constitution which

helps in increasing their accuracy at the time of performing their duty. Development of

accounting standard should be more economical where conceptual framework include all the

issues which reduce the need of additional standard. It will emphasis the role of financial report

rather then restricting concern to the stewardship to make decision useful.

As per Houqe, van Zijl, Dunstan and Karim 2012, conceptual framework provide the

various IFRS which help the organization to follow these standards and develop accurate report

for the external as well as internal users. These financial reports help the individual to take their

decision on the basis of available financial information. It is suggested that, quality of earning is

important to increase because it will protect the investors and provide them strong evidence to

take decision with the available data. In the conceptual framework, it is important to sate the

interest of investors for the financial reporting quality and it is required for the regulation and

maintain the limit of manager and complete their management practices.

Michelon, Pilonato and Ricceri 2015 state that, for the smaller organization it is very

difficult to complete their task in order to achieve their goals & objectives. Small company feel

burden to follow all the relevant accounting standard which is required to implement for the

accurate result in order to achieve their business goals & objectives. Biggest disadvantage of the

3

conceptual framework is that, it is typical to understand, focus for the economy, include those

transaction which does not involve market transaction or exchange of rights of the assets and

other things. It will show the codification of existing practice which affect the company for the

longer period.

4. How conceptual framework applied by the Australian company

As per the annual report of the Infigen Energy Limited, company build develop financial

report for the disclose of financial information which attract the investors and customers which

further inverse the productivity or profitability (Englund and Gerdin, 2014). These conceptual

framework help the business through various standards, rules and regulation which required to

follow by the company in order achieve their business goals & objectives, there are various

report which is discussed below:

Comprehensive Income: Net profit of the 2018 is 25,673 and 32,264 in the 2017 which

is increased and provide more profit in order to increase their demand.

Financial Position: Balance sheet provide the actual position of the company in terms of

assets and liability of the organization. Total assets of the company in 2018 was

12,58,814. total liability is 687,121 and equity of the company is 571,693.

Change in Equity: This statement is prepared for the change in the equity and it also

include the details of change in the owner's equity in the accounting period. In the annual

report of the company total change in the equity is 2305 in the year of 2018.

Cash Flow: It is the part of financial reporting which help the management to represent

their total inflow or outflow of cash. Total cash inflow from the operating activity is

100,446. net outflow of cash from investing activity is 143,042 and net outflow of cash

from financing activity is 65,510.

Infigen Energy Limited follow the AASB 15 for the revenue from contracts with

customers, this principle based on the revenue recognition which control the goods & services

transfer to the consumers. Another principle which is used by the Infigen Energy Limited is

AASB 16 for leases which create difference between operating and financial leases. These

principle and measurement applied for the revenue recognition and leases which is included in

the balance sheet.

Company use the various standards which is applicable on the different items and it will

help the organization to building their financial report. It will help the stakeholder to analysis

4

transaction which does not involve market transaction or exchange of rights of the assets and

other things. It will show the codification of existing practice which affect the company for the

longer period.

4. How conceptual framework applied by the Australian company

As per the annual report of the Infigen Energy Limited, company build develop financial

report for the disclose of financial information which attract the investors and customers which

further inverse the productivity or profitability (Englund and Gerdin, 2014). These conceptual

framework help the business through various standards, rules and regulation which required to

follow by the company in order achieve their business goals & objectives, there are various

report which is discussed below:

Comprehensive Income: Net profit of the 2018 is 25,673 and 32,264 in the 2017 which

is increased and provide more profit in order to increase their demand.

Financial Position: Balance sheet provide the actual position of the company in terms of

assets and liability of the organization. Total assets of the company in 2018 was

12,58,814. total liability is 687,121 and equity of the company is 571,693.

Change in Equity: This statement is prepared for the change in the equity and it also

include the details of change in the owner's equity in the accounting period. In the annual

report of the company total change in the equity is 2305 in the year of 2018.

Cash Flow: It is the part of financial reporting which help the management to represent

their total inflow or outflow of cash. Total cash inflow from the operating activity is

100,446. net outflow of cash from investing activity is 143,042 and net outflow of cash

from financing activity is 65,510.

Infigen Energy Limited follow the AASB 15 for the revenue from contracts with

customers, this principle based on the revenue recognition which control the goods & services

transfer to the consumers. Another principle which is used by the Infigen Energy Limited is

AASB 16 for leases which create difference between operating and financial leases. These

principle and measurement applied for the revenue recognition and leases which is included in

the balance sheet.

Company use the various standards which is applicable on the different items and it will

help the organization to building their financial report. It will help the stakeholder to analysis

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their decision weather they wanted to invest or not. Use of accounting standards will increase the

reliability, relevancy, efficiency or effectiveness which provide the accurate information

regarding their financial position.

PART B

1. Compare Global Reporting Initiative (GRI) and International Integrated Reporting Framework

for the holistic view of corporate social responsibility

Global reporting initiative (GRI) is an international non Governmental organization and it

will be collaborating with UN environmental programs which is world most widely used

framework for the sustainability report. It include the various principles, indicators which

measure and report the economic, social and other factors performance. Third generation

framework will be introduced in 2006 and it is called GRI G3 guidelines and it is online

available for the general public for free (Hall, 2016). Global reporting initiative used for the

sustainable reporting standard practices which help the organization to maintain, promote or

change the global economy. GRI enable the company to report economic, environmental, social

and government performance.

International Integrated Reporting Framework (IIRF): This framework used to accelerate

the adoption of integrated reporting across the world. Main purpose of the this reporting is to

provide guiding principle and content elements which govern the overall content for the

integrated report. This framework related to the following extensive consultation and test the

business & investors around the world. About 140 business and the investors of 26 countries

participate in the IIRC pilot program and it's main purpose is to establish the guiding principle

and content elements.

Corporate social responsibility reporting: It is the broader concepts where many form will

be depended on the company and industry. Corporate social responsibility (CSR) is the

integrated part of our society and ours company's culture (Hiebl, 2014). As a responsible

corporation, organization have to done something for the society where they done various

activities for the interest of the stakeholders which include many peoples. Organization build

their CSR report which include all the relevant activity that organization done for society for the

sustainable development.

5

reliability, relevancy, efficiency or effectiveness which provide the accurate information

regarding their financial position.

PART B

1. Compare Global Reporting Initiative (GRI) and International Integrated Reporting Framework

for the holistic view of corporate social responsibility

Global reporting initiative (GRI) is an international non Governmental organization and it

will be collaborating with UN environmental programs which is world most widely used

framework for the sustainability report. It include the various principles, indicators which

measure and report the economic, social and other factors performance. Third generation

framework will be introduced in 2006 and it is called GRI G3 guidelines and it is online

available for the general public for free (Hall, 2016). Global reporting initiative used for the

sustainable reporting standard practices which help the organization to maintain, promote or

change the global economy. GRI enable the company to report economic, environmental, social

and government performance.

International Integrated Reporting Framework (IIRF): This framework used to accelerate

the adoption of integrated reporting across the world. Main purpose of the this reporting is to

provide guiding principle and content elements which govern the overall content for the

integrated report. This framework related to the following extensive consultation and test the

business & investors around the world. About 140 business and the investors of 26 countries

participate in the IIRC pilot program and it's main purpose is to establish the guiding principle

and content elements.

Corporate social responsibility reporting: It is the broader concepts where many form will

be depended on the company and industry. Corporate social responsibility (CSR) is the

integrated part of our society and ours company's culture (Hiebl, 2014). As a responsible

corporation, organization have to done something for the society where they done various

activities for the interest of the stakeholders which include many peoples. Organization build

their CSR report which include all the relevant activity that organization done for society for the

sustainable development.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of sustainable reporting guidelines that is Global Reporting Initiative (GRI)

and International Integrated Reporting Framework of the International Integrated Reporting

Council (IIRC) for explaining holistic view of the corporate social responsibility which help the

organization to analyse the corporate financial performance. Because corporate activities that is

CSR will help the business in order to increase their brand image in front of the consumers.

Further it make consumer loyal for that product and increase their productivity or profitability

which help the business to achieve their goals & objectives.

2. Rigour of conventional accounting

Conventional accounting: It is the traditional method which was used earlier by

business entities in order to record accounting information in the books. Under this method

double entry and bookkeeping system were used for the purpose of recording to business

transactions (Malik, 2015). Strengths and limitations of this system are as follows:

Strengths:

Main strength of conventional accounting is that it avoids system errors and corrupt files

as information technology is not used in it. Various people does not have any idea of

operating a computer system and they are also not aware of the ways in which system

errors could be resolved. For them tradition accounting is best way to record information

and keep it safe.

As double entry system is used in conventional accounting so it helps to improve the

errors because this system guides to recognise all the errors which were made by

accountants while recording information is books. It not only direct to remove mistakes

but also help to save time and money which could be spent by them in devastating

business errors if they use computer system(Schaltegger and Burritt, 2017).

Availability of data in conventional accounting is very high so when internet or power

goes out it will not restrict the user to analyse the information because the data is not

stored in a computer system which requires power to access it.

Limitations:

The process of recording information in conventional accounting is time taking as each

and every figure is recorded twice in this system in order to ignore mathematical errors.

Most of the business entities are not able to spend this much time in data recording

process so they use automated accounting systems.

6

and International Integrated Reporting Framework of the International Integrated Reporting

Council (IIRC) for explaining holistic view of the corporate social responsibility which help the

organization to analyse the corporate financial performance. Because corporate activities that is

CSR will help the business in order to increase their brand image in front of the consumers.

Further it make consumer loyal for that product and increase their productivity or profitability

which help the business to achieve their goals & objectives.

2. Rigour of conventional accounting

Conventional accounting: It is the traditional method which was used earlier by

business entities in order to record accounting information in the books. Under this method

double entry and bookkeeping system were used for the purpose of recording to business

transactions (Malik, 2015). Strengths and limitations of this system are as follows:

Strengths:

Main strength of conventional accounting is that it avoids system errors and corrupt files

as information technology is not used in it. Various people does not have any idea of

operating a computer system and they are also not aware of the ways in which system

errors could be resolved. For them tradition accounting is best way to record information

and keep it safe.

As double entry system is used in conventional accounting so it helps to improve the

errors because this system guides to recognise all the errors which were made by

accountants while recording information is books. It not only direct to remove mistakes

but also help to save time and money which could be spent by them in devastating

business errors if they use computer system(Schaltegger and Burritt, 2017).

Availability of data in conventional accounting is very high so when internet or power

goes out it will not restrict the user to analyse the information because the data is not

stored in a computer system which requires power to access it.

Limitations:

The process of recording information in conventional accounting is time taking as each

and every figure is recorded twice in this system in order to ignore mathematical errors.

Most of the business entities are not able to spend this much time in data recording

process so they use automated accounting systems.

6

Conventional accounting is based upon hard copies of information in which data is also

recorded in tangible form. If these are lost by a company then it will become difficult to

analyse actual status and performance of the company.

One of the major limitation of conventional accounting is cost which is very high. If

companies use automated accounting system then the cost of it will be reduced because it

will not require papers and pens to record transactions in the books of accounting (Mikes

and Kaplan, 2014).

3. Explain the required theory which is used to explain the contents of sustainability as well as

integrated reports

Their are various theories which is used for the organization for the sustainability or

integrated of the operations and it will be discussed below:

Institutional theory: This theory include the various components which include the

process which establish the guidelines for the societal behaviour. This theory majorly focus on

structure, adapted over space and time. Institutional theory include the wide range of variables

which influence the decision making process of the company. Manager of the Infigen Energy

company can adopt this theory in order to operate their stakeholders which include government,

employees, customers, supplier etc. For the long term production or survival of the company,

organization make sure that, they follow all the relevant rules, regulation and guidelines in order

to achieve their goals & objectives (Modell, 2015) . Which further helps the organization to

increase their productivity or profitability and it will also affect the performance of employees as

well as whole organization.

Stakeholders theory: This theory include the company's stakeholder which is affected

by the organizational activity and it's operational functions. This theory create a purpose for the

business which create value for the organization and increase the productivity as profitability as

well. Basically it is used for the management where business ethics are more important more

then profit margin of the company because it can affect the company in positive as well as

negative way. With the help of this theory, organization build strategy which help the company

to build strategy which integrates with both resource-based view and a market-based view.

Manager of the Infigen Energy company, build various strategy regarding various laws,

management and human resources. Company face various challenges, so it can resolved through

7

recorded in tangible form. If these are lost by a company then it will become difficult to

analyse actual status and performance of the company.

One of the major limitation of conventional accounting is cost which is very high. If

companies use automated accounting system then the cost of it will be reduced because it

will not require papers and pens to record transactions in the books of accounting (Mikes

and Kaplan, 2014).

3. Explain the required theory which is used to explain the contents of sustainability as well as

integrated reports

Their are various theories which is used for the organization for the sustainability or

integrated of the operations and it will be discussed below:

Institutional theory: This theory include the various components which include the

process which establish the guidelines for the societal behaviour. This theory majorly focus on

structure, adapted over space and time. Institutional theory include the wide range of variables

which influence the decision making process of the company. Manager of the Infigen Energy

company can adopt this theory in order to operate their stakeholders which include government,

employees, customers, supplier etc. For the long term production or survival of the company,

organization make sure that, they follow all the relevant rules, regulation and guidelines in order

to achieve their goals & objectives (Modell, 2015) . Which further helps the organization to

increase their productivity or profitability and it will also affect the performance of employees as

well as whole organization.

Stakeholders theory: This theory include the company's stakeholder which is affected

by the organizational activity and it's operational functions. This theory create a purpose for the

business which create value for the organization and increase the productivity as profitability as

well. Basically it is used for the management where business ethics are more important more

then profit margin of the company because it can affect the company in positive as well as

negative way. With the help of this theory, organization build strategy which help the company

to build strategy which integrates with both resource-based view and a market-based view.

Manager of the Infigen Energy company, build various strategy regarding various laws,

management and human resources. Company face various challenges, so it can resolved through

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CSR activities which increase the interest which further help the organization to develop new

products for the consumers.

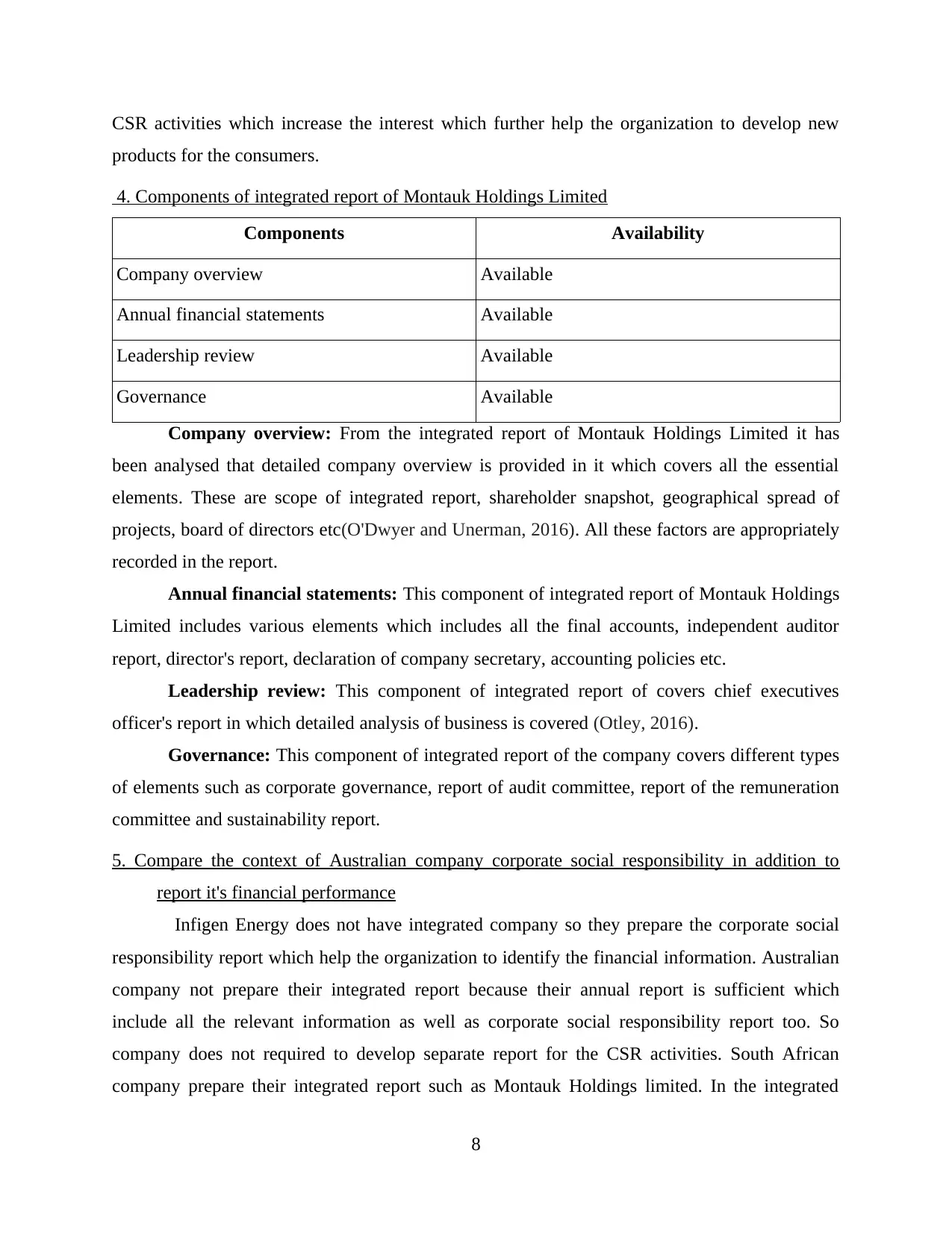

4. Components of integrated report of Montauk Holdings Limited

Components Availability

Company overview Available

Annual financial statements Available

Leadership review Available

Governance Available

Company overview: From the integrated report of Montauk Holdings Limited it has

been analysed that detailed company overview is provided in it which covers all the essential

elements. These are scope of integrated report, shareholder snapshot, geographical spread of

projects, board of directors etc(O'Dwyer and Unerman, 2016). All these factors are appropriately

recorded in the report.

Annual financial statements: This component of integrated report of Montauk Holdings

Limited includes various elements which includes all the final accounts, independent auditor

report, director's report, declaration of company secretary, accounting policies etc.

Leadership review: This component of integrated report of covers chief executives

officer's report in which detailed analysis of business is covered (Otley, 2016).

Governance: This component of integrated report of the company covers different types

of elements such as corporate governance, report of audit committee, report of the remuneration

committee and sustainability report.

5. Compare the context of Australian company corporate social responsibility in addition to

report it's financial performance

Infigen Energy does not have integrated company so they prepare the corporate social

responsibility report which help the organization to identify the financial information. Australian

company not prepare their integrated report because their annual report is sufficient which

include all the relevant information as well as corporate social responsibility report too. So

company does not required to develop separate report for the CSR activities. South African

company prepare their integrated report such as Montauk Holdings limited. In the integrated

8

products for the consumers.

4. Components of integrated report of Montauk Holdings Limited

Components Availability

Company overview Available

Annual financial statements Available

Leadership review Available

Governance Available

Company overview: From the integrated report of Montauk Holdings Limited it has

been analysed that detailed company overview is provided in it which covers all the essential

elements. These are scope of integrated report, shareholder snapshot, geographical spread of

projects, board of directors etc(O'Dwyer and Unerman, 2016). All these factors are appropriately

recorded in the report.

Annual financial statements: This component of integrated report of Montauk Holdings

Limited includes various elements which includes all the final accounts, independent auditor

report, director's report, declaration of company secretary, accounting policies etc.

Leadership review: This component of integrated report of covers chief executives

officer's report in which detailed analysis of business is covered (Otley, 2016).

Governance: This component of integrated report of the company covers different types

of elements such as corporate governance, report of audit committee, report of the remuneration

committee and sustainability report.

5. Compare the context of Australian company corporate social responsibility in addition to

report it's financial performance

Infigen Energy does not have integrated company so they prepare the corporate social

responsibility report which help the organization to identify the financial information. Australian

company not prepare their integrated report because their annual report is sufficient which

include all the relevant information as well as corporate social responsibility report too. So

company does not required to develop separate report for the CSR activities. South African

company prepare their integrated report such as Montauk Holdings limited. In the integrated

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

report of the company they include the company's overview, their financial statement, leadership

review and governance (Parker and Fleischman, 2017) . These information will be missed by the

Montauk Holdings limited so they prepare separately for the better understanding for the

stakeholders. So they can take effective decision in order to achieve their business goals &

objectives. Organization prepare this report which include those which is not recorded in the

annual report of the company.

CONCLUSION

From the above project report it has been concluded that contemporary accounting theory

is the set of different types of assumptions, frameworks and methodologies which are used by

business entities to record financial information in the books. In Australia it is vital for all the

companies to comply with Australian Accounting Standards which are imposed by AASB and

IASB. It is also very important for large as well as small organisations to bring quality in their

final accounts. The qualitative aspects which could be added by them in financial statements are

relevancy, appropriateness, accuracy, transparency etc. Certain accounting standards which are

vital to be followed by companies are AASB 15 and 16 which helps to recognise assets,

liabilities and revenues. Conventional accounting is a traditional method which is used by

companies to ignore mathematical errors and bring accuracy in final reports.

9

review and governance (Parker and Fleischman, 2017) . These information will be missed by the

Montauk Holdings limited so they prepare separately for the better understanding for the

stakeholders. So they can take effective decision in order to achieve their business goals &

objectives. Organization prepare this report which include those which is not recorded in the

annual report of the company.

CONCLUSION

From the above project report it has been concluded that contemporary accounting theory

is the set of different types of assumptions, frameworks and methodologies which are used by

business entities to record financial information in the books. In Australia it is vital for all the

companies to comply with Australian Accounting Standards which are imposed by AASB and

IASB. It is also very important for large as well as small organisations to bring quality in their

final accounts. The qualitative aspects which could be added by them in financial statements are

relevancy, appropriateness, accuracy, transparency etc. Certain accounting standards which are

vital to be followed by companies are AASB 15 and 16 which helps to recognise assets,

liabilities and revenues. Conventional accounting is a traditional method which is used by

companies to ignore mathematical errors and bring accuracy in final reports.

9

REFERENCES

Books and Journals:

Bedford, N. M. and Ziegler, R. E., 2016. The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting

Leaders. 49. p.219.

Budding, T., Grossi, G. and Tagesson, T. eds., 2014. Public sector accounting. Routledge.

D. Carnegie, G., 2014. The present and future of accounting history. Accounting, Auditing &

Accountability Journal. 27(8). pp.1241-1249.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Hall, M., 2016. Realising the richness of psychology theory in contingency-based management

accounting research. Management Accounting Research. 31. pp.63-74.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Houqe, M. N., and et.al., 2012. The effect of IFRS adoption and investor protection on earnings

quality around the world. The International journal of accounting, 47(3), pp.333-355.

Malik, M., 2015. Value-enhancing capabilities of CSR: A brief review of contemporary

literature. Journal of Business Ethics. 127(2). pp.419-438.

Michelon, G., Pilonato, S. and Ricceri, F., 2015. CSR reporting practices and the quality of

disclosure: An empirical analysis. Critical perspectives on accounting, 33, pp.59-78.

Mikes, A. and Kaplan, R. S., 2014, October. Towards a contingency theory of enterprise risk

management. AAA.

Modell, S., 2015. Theoretical triangulation and pluralism in accounting research: a critical realist

critique. Accounting, Auditing & Accountability Journal. 28(7). pp.1138-1150.

Musiolik, J., Markard, J. and Hekkert, M., 2012. Networks and network resources in

technological innovation systems: Towards a conceptual framework for system

building. Technological Forecasting and Social Change, 79(6), pp.1032-1048.

O'Dwyer, B. and Unerman, J., 2016. Fostering rigour in accounting for social

sustainability. Accounting, Organizations and Society. 49. pp.32-40.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parker, L. D. and Fleischman, R. K., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Shehata, N. F., 2014. Theories and determinants of voluntary disclosure. Accounting and

Finance Research (AFR). 3(1).

Smith, M., 2017. Research methods in accounting. Sage.

10

Books and Journals:

Bedford, N. M. and Ziegler, R. E., 2016. The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting

Leaders. 49. p.219.

Budding, T., Grossi, G. and Tagesson, T. eds., 2014. Public sector accounting. Routledge.

D. Carnegie, G., 2014. The present and future of accounting history. Accounting, Auditing &

Accountability Journal. 27(8). pp.1241-1249.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Hall, M., 2016. Realising the richness of psychology theory in contingency-based management

accounting research. Management Accounting Research. 31. pp.63-74.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Houqe, M. N., and et.al., 2012. The effect of IFRS adoption and investor protection on earnings

quality around the world. The International journal of accounting, 47(3), pp.333-355.

Malik, M., 2015. Value-enhancing capabilities of CSR: A brief review of contemporary

literature. Journal of Business Ethics. 127(2). pp.419-438.

Michelon, G., Pilonato, S. and Ricceri, F., 2015. CSR reporting practices and the quality of

disclosure: An empirical analysis. Critical perspectives on accounting, 33, pp.59-78.

Mikes, A. and Kaplan, R. S., 2014, October. Towards a contingency theory of enterprise risk

management. AAA.

Modell, S., 2015. Theoretical triangulation and pluralism in accounting research: a critical realist

critique. Accounting, Auditing & Accountability Journal. 28(7). pp.1138-1150.

Musiolik, J., Markard, J. and Hekkert, M., 2012. Networks and network resources in

technological innovation systems: Towards a conceptual framework for system

building. Technological Forecasting and Social Change, 79(6), pp.1032-1048.

O'Dwyer, B. and Unerman, J., 2016. Fostering rigour in accounting for social

sustainability. Accounting, Organizations and Society. 49. pp.32-40.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parker, L. D. and Fleischman, R. K., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Shehata, N. F., 2014. Theories and determinants of voluntary disclosure. Accounting and

Finance Research (AFR). 3(1).

Smith, M., 2017. Research methods in accounting. Sage.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.