ACCT20074: Evaluation of Conceptual Framework and Reporting Practices

VerifiedAdded on 2022/11/11

|22

|5033

|488

Report

AI Summary

This report provides a comprehensive analysis of the conceptual framework (CF) for financial reporting and its application in sustainable reporting. It begins with an examination of the history, development, benefits, and limitations of the CF, followed by an evaluation of its application within Austal Limited. The report then explores the differences between the Global Reporting Initiative (GRI) and integrated reporting, and the theories that underpin sustainability reporting content. The report also provides a discussion of the various components of integrated reports in the context of Sibanye Gold Ltd. The report covers the history and development of the CF, concerns of Australian professionals, potential benefits and limitations, and the application of the CF to evaluate the annual report of Austal Limited. Additionally, the report compares GRI and integrated reporting and their application to a South African company, Sibanye Gold Ltd, and compares reporting practices between Australian and South African companies.

ACCT20074 Contemporary Accounting Theory

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report has examined the usefulness of CF and other voluntary frameworks such as

GRI an integrated reporting for development of sustaible reports. This has been carried out by

analyzing the history, benefits and limitations of CF and also demonstrating its applications

within a selected business entity in Australia, Austal Limited. It is followed by providing a

discussion about the difference between GRI and integrated reporting and theories that have been

applied for developing content of sustainability reporting. The various criteria of integrated

reports have been developed in the context of selected South African company, that is, Sibanye

Gold Ltd (SGL).

2

The report has examined the usefulness of CF and other voluntary frameworks such as

GRI an integrated reporting for development of sustaible reports. This has been carried out by

analyzing the history, benefits and limitations of CF and also demonstrating its applications

within a selected business entity in Australia, Austal Limited. It is followed by providing a

discussion about the difference between GRI and integrated reporting and theories that have been

applied for developing content of sustainability reporting. The various criteria of integrated

reports have been developed in the context of selected South African company, that is, Sibanye

Gold Ltd (SGL).

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Evaluation of conceptual framework and application of it in the chosen company...........6

Section A: History and Development of the CF for Financial Reporting....................................6

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS CF

for Financial Reporting................................................................................................................7

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting..........7

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited........8

D (I): Number of financial statements and their components......................................................8

D (II): Principle of recognition and measurement bases used for assets, revenue and liabilities

....................................................................................................................................................10

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group.......................................................................................10

Part B: Evaluation of integrating reporting/sustainability reporting and application of same in

South Africa Company includes the comparison with one of Australian Company.....................13

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting......................................................13

Section B: Conventional Accounting Strengths and Limitations for Explaining the Contents of

Sustainability and Integrated Reports........................................................................................13

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting..................................................................................................................14

Section D: Use of different components of the integrated reporting to evaluate the reporting

framework of the selected South African Company (Sibanye Gold Limited)...........................15

Section E: Comparison of reporting practices by Australian Company and South African

Company....................................................................................................................................17

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Evaluation of conceptual framework and application of it in the chosen company...........6

Section A: History and Development of the CF for Financial Reporting....................................6

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS CF

for Financial Reporting................................................................................................................7

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting..........7

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited........8

D (I): Number of financial statements and their components......................................................8

D (II): Principle of recognition and measurement bases used for assets, revenue and liabilities

....................................................................................................................................................10

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group.......................................................................................10

Part B: Evaluation of integrating reporting/sustainability reporting and application of same in

South Africa Company includes the comparison with one of Australian Company.....................13

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting......................................................13

Section B: Conventional Accounting Strengths and Limitations for Explaining the Contents of

Sustainability and Integrated Reports........................................................................................13

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting..................................................................................................................14

Section D: Use of different components of the integrated reporting to evaluate the reporting

framework of the selected South African Company (Sibanye Gold Limited)...........................15

Section E: Comparison of reporting practices by Australian Company and South African

Company....................................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

4

References......................................................................................................................................20

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Conceptual framework (CF) can be defined as coherent system of interrelated objectives

and fundamentals that is leading to the development of consistent standards and prescribing the

nature and quality of financial accounting within businesses. On the other hand, sustainable

reporting can be regarded as the practice of providing information about social and

environmental performance of an organization. This report has been prepared in the context of

examining the application of conceptual framework for financial reporting and other voluntary

frameworks such as GRI and integrated reporting framework to develop sustainable reports.

5

Conceptual framework (CF) can be defined as coherent system of interrelated objectives

and fundamentals that is leading to the development of consistent standards and prescribing the

nature and quality of financial accounting within businesses. On the other hand, sustainable

reporting can be regarded as the practice of providing information about social and

environmental performance of an organization. This report has been prepared in the context of

examining the application of conceptual framework for financial reporting and other voluntary

frameworks such as GRI and integrated reporting framework to develop sustainable reports.

5

Part A: Evaluation of conceptual framework and application of it in the chosen company

Section A: History and Development of the CF for Financial Reporting

The conceptual framework is developed for providing assistance to the developers of

financial reports regarding the selection of accounting policies on the basis of theoretical

principles mainly of relevance and faithful presentation. The framework has been developed on

the basis of normative theory which provides guidance regarding the theoretical principles to be

used for carrying out accounting processes.

The framework has initially being developed by the IASB and it has been revised under

the common efforts of both IASB and FASB for the purpose of driving improvement within the

conceptual framework. The conceptual framework has been revised by the IASB and it has

largely been adopted by the countries aiming for complying with international accounting

standards for promoting uniformity in the financial reporting system. The framework is now

largely being applied by business corporations across the world. The CF’s have been developed

in a number (Barth, 2008). There has been the development of Accounting Principles Board

(APB) in the USA for providing the accounting principles to be followed during financial

reporting. The Board is criticized for lack of any real framework for guiding the financial

reporting. There was establishment of a Trueblood Committee in the year 1971 which developed

the Trueblood Report. It has provided about 12 objectives and 7 qualitative criteria to be present

within a financial report (Dean and Clarke, 2003). These objectives and characteristics were not

found to be adequate for providing decision-making information to the users. As such, the APB

is replaced by FASB and released six statements of financial accounting concepts from the year

1978 to 1985. The FASB has joined IASB in the year 2005 for developing a revised CF which

has now being adopted within the US (Macías and Muiño, 2011).

In the UK, Accounting Standards Board (ASB) has adopted the International Accounting

Standards’ Committee (IASC) that is consistent with the US and Australian frameworks. On the

other hand, in Australia there have been only four statement accounting concepts about defining

the reporting entity, objective of general purpose financial reporting, providing qualitative

principles for reporting financial information and stating the definition of recognizing the

financial statement elements. The framework has not provided the statements regarding the

6

Section A: History and Development of the CF for Financial Reporting

The conceptual framework is developed for providing assistance to the developers of

financial reports regarding the selection of accounting policies on the basis of theoretical

principles mainly of relevance and faithful presentation. The framework has been developed on

the basis of normative theory which provides guidance regarding the theoretical principles to be

used for carrying out accounting processes.

The framework has initially being developed by the IASB and it has been revised under

the common efforts of both IASB and FASB for the purpose of driving improvement within the

conceptual framework. The conceptual framework has been revised by the IASB and it has

largely been adopted by the countries aiming for complying with international accounting

standards for promoting uniformity in the financial reporting system. The framework is now

largely being applied by business corporations across the world. The CF’s have been developed

in a number (Barth, 2008). There has been the development of Accounting Principles Board

(APB) in the USA for providing the accounting principles to be followed during financial

reporting. The Board is criticized for lack of any real framework for guiding the financial

reporting. There was establishment of a Trueblood Committee in the year 1971 which developed

the Trueblood Report. It has provided about 12 objectives and 7 qualitative criteria to be present

within a financial report (Dean and Clarke, 2003). These objectives and characteristics were not

found to be adequate for providing decision-making information to the users. As such, the APB

is replaced by FASB and released six statements of financial accounting concepts from the year

1978 to 1985. The FASB has joined IASB in the year 2005 for developing a revised CF which

has now being adopted within the US (Macías and Muiño, 2011).

In the UK, Accounting Standards Board (ASB) has adopted the International Accounting

Standards’ Committee (IASC) that is consistent with the US and Australian frameworks. On the

other hand, in Australia there have been only four statement accounting concepts about defining

the reporting entity, objective of general purpose financial reporting, providing qualitative

principles for reporting financial information and stating the definition of recognizing the

financial statement elements. The framework has not provided the statements regarding the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

measurement concept and therefore is not widely accepted. The Australia adopted the IASBCF

after the decision of Financial Reporting Council in the year 2015 for improving comparability

of its financial reporting system (Chua, Chee and Cheong, 2012). The joint efforts of FASB and

IASB for convergence of accounting standards is leading to the global acceptance of the CF

principles in the financial reporting system of business entities on a global level (Seng, 2014).

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS

CF for Financial Reporting

The Australian accounting professionals such as Certified Public Accountants (CPAs)

and other accounting professional bodies within the country have shred their various concerns

that are associated with the application of CF in financial reporting as provided by the AASB.

The major concern that is present in this context related to considering the financial reporting

thresholds as per the Corporations Act 2001 that have not been given consideration by the AASB

(Lonergan, 2005). In addition to this, there have also been issues shared in regards to cost-benefit

analysis of the framework. There has been inappropriate analysis conducted in regards to

increasing costs required for adopting the new CF of financial reporting as camped to its benefits

achieved. The higher costs would be incurred in providing training to the accounting

professionals and implemented widespread changes in the financial reporting system. This

requires comprehensive and detailed cost-benefits analysis to be conducted before processed

with the acceptance of the AASB proposals (Wong, 2004).

The major challenge that has been identified by the accounting professionals in this

regard is relating to the adoption of IASB framework for small and medium-sized entities. There

is requirement of developing separate framework for controlling the financial reporting of these

corporations. This is because application of the IASB standard would require higher costs for

these entities in comparison to the benefits to be realized. These entities possess limited financial

resources and therefore it would be very difficult for them to comply with all the IASB principles

(AASB adoption of IASB standards by 2005, 2004).

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting

The various accounting researchers have highlighted the following concerns relating to

the CF that has been discussed under its significant benefits and limitations headings as follows:

7

after the decision of Financial Reporting Council in the year 2015 for improving comparability

of its financial reporting system (Chua, Chee and Cheong, 2012). The joint efforts of FASB and

IASB for convergence of accounting standards is leading to the global acceptance of the CF

principles in the financial reporting system of business entities on a global level (Seng, 2014).

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS

CF for Financial Reporting

The Australian accounting professionals such as Certified Public Accountants (CPAs)

and other accounting professional bodies within the country have shred their various concerns

that are associated with the application of CF in financial reporting as provided by the AASB.

The major concern that is present in this context related to considering the financial reporting

thresholds as per the Corporations Act 2001 that have not been given consideration by the AASB

(Lonergan, 2005). In addition to this, there have also been issues shared in regards to cost-benefit

analysis of the framework. There has been inappropriate analysis conducted in regards to

increasing costs required for adopting the new CF of financial reporting as camped to its benefits

achieved. The higher costs would be incurred in providing training to the accounting

professionals and implemented widespread changes in the financial reporting system. This

requires comprehensive and detailed cost-benefits analysis to be conducted before processed

with the acceptance of the AASB proposals (Wong, 2004).

The major challenge that has been identified by the accounting professionals in this

regard is relating to the adoption of IASB framework for small and medium-sized entities. There

is requirement of developing separate framework for controlling the financial reporting of these

corporations. This is because application of the IASB standard would require higher costs for

these entities in comparison to the benefits to be realized. These entities possess limited financial

resources and therefore it would be very difficult for them to comply with all the IASB principles

(AASB adoption of IASB standards by 2005, 2004).

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting

The various accounting researchers have highlighted the following concerns relating to

the CF that has been discussed under its significant benefits and limitations headings as follows:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits

The application of CF into financial reporting has facilitated in removal of all the

inconsistencies present within the accounting principles and lead to the establishment of

more logical and consistent accounting standards

The large number of countries around the world have adopted the CF and therefore its

widespread adoption is leading towards improving the international comparability across

different accounting rules and policies (Silvia, 2016)

It has improved the accountability and transparency in business operations and resulting

in providing the financial information to the users that is more useful in decision-making

It has also caused the need for improving credibility in the accounting standard-setting

procedures as the accounting professionals need to work as per the CF fundamentals

which requires depiction of high relevant and reliable information (Fajard, 2016)

Limitations

The issue of measurement has not yet been resolved under the CF as there has been the

presence of different measurement approaches by business entities across the world for

recognition of assets and liabilities. This can result in causing the issue related with

measurement in accounting (Tschopp and Nastanski, 2014)

There is no usefulness of its integration for smaller business entities

It has only taken into considering the financial performance and relatively ignored the

need for developing a framework for reporting the social and environmental performance

(Pacter, 2013)

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited

D (I): Number of financial statements and their components

This part requires the evaluation of annual report of Austal Group Limited for year 2018

through using the conceptual framework. The purpose is to check whether Ingenia Communities

Group has been successful to apply all the guidelines and information provided in the conceptual

framework (Conceptual Framework, 2018).

8

The application of CF into financial reporting has facilitated in removal of all the

inconsistencies present within the accounting principles and lead to the establishment of

more logical and consistent accounting standards

The large number of countries around the world have adopted the CF and therefore its

widespread adoption is leading towards improving the international comparability across

different accounting rules and policies (Silvia, 2016)

It has improved the accountability and transparency in business operations and resulting

in providing the financial information to the users that is more useful in decision-making

It has also caused the need for improving credibility in the accounting standard-setting

procedures as the accounting professionals need to work as per the CF fundamentals

which requires depiction of high relevant and reliable information (Fajard, 2016)

Limitations

The issue of measurement has not yet been resolved under the CF as there has been the

presence of different measurement approaches by business entities across the world for

recognition of assets and liabilities. This can result in causing the issue related with

measurement in accounting (Tschopp and Nastanski, 2014)

There is no usefulness of its integration for smaller business entities

It has only taken into considering the financial performance and relatively ignored the

need for developing a framework for reporting the social and environmental performance

(Pacter, 2013)

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited

D (I): Number of financial statements and their components

This part requires the evaluation of annual report of Austal Group Limited for year 2018

through using the conceptual framework. The purpose is to check whether Ingenia Communities

Group has been successful to apply all the guidelines and information provided in the conceptual

framework (Conceptual Framework, 2018).

8

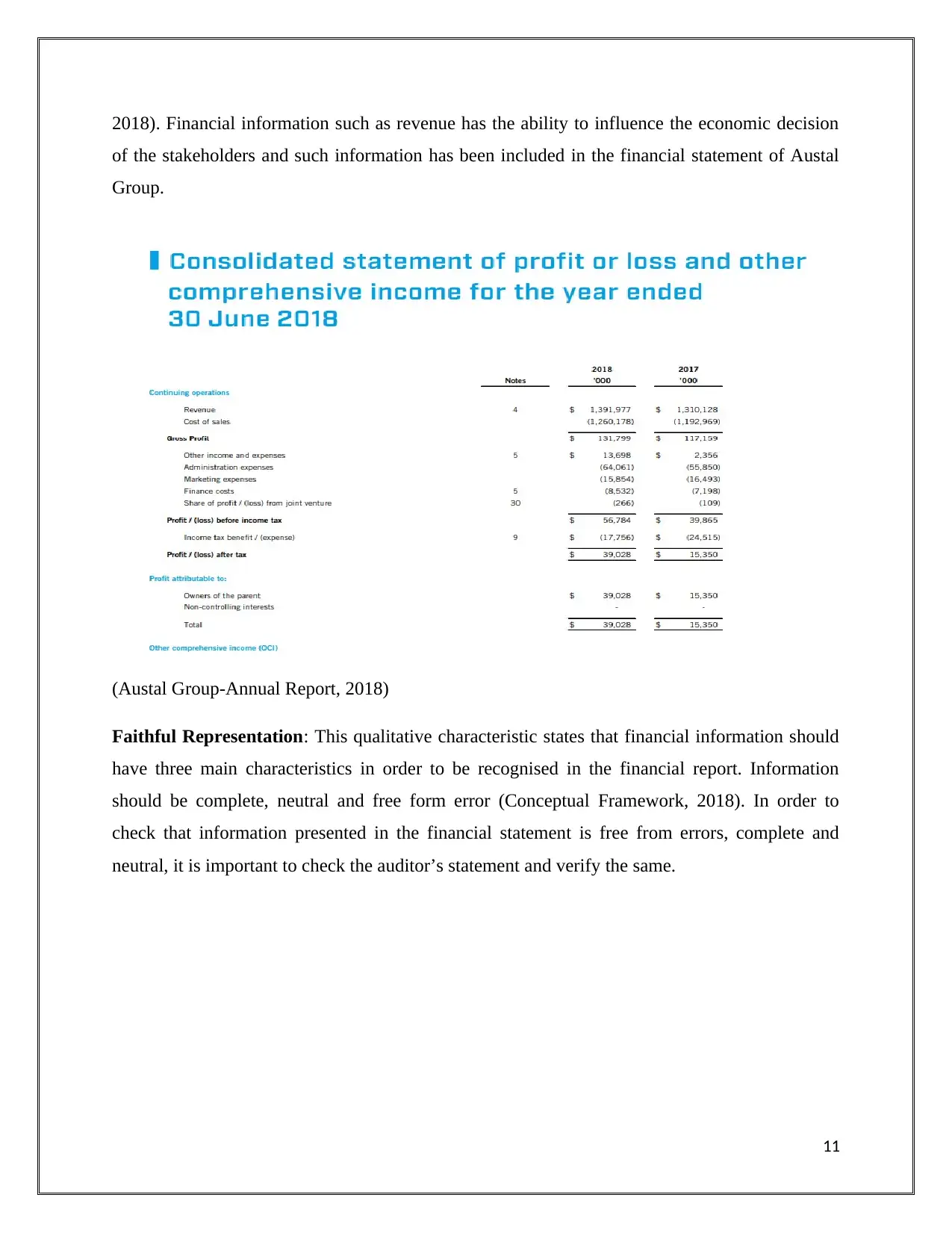

According to the conceptual framework company needs to produce four major categories

of financial statements or reports. Following are the major components of financial statements

that Austal Group Limited has prepared as per the conceptual framework:

Income Statement or statement of financial performance: Income statement is the most

important financial statement prepared to reflect the financial performance of the company

during the specific period. In annual report of Austal Group Limited only consolidated income

statement is provided which shows the financial performance of the holding company as well as

all the subsidiaries. This statement provides information on revenue and expenses (Austal

Group-Annual Report, 2018).

Balance sheet or statement of financial position: Austal Group Limited has provided only

consolidated balance sheet that reflects the financial position of the parent company as well as all

the subsidiaries. The basic elements of the statement of financial positions are assets, liabilities

and equity.

Statement of change in equity: Contribution and distribution made by shareholders are being

disclosed in this statement. This statement is also prepared as consolidated statement.

Statement of cash flow: This statement discloses information on the cash flows various

activities such as operating activity, financing activity and investing activity. It is also presented

as consolidated statement to provide cash flow information for whole group (Austal Group-

Annual Report, 2018).

In addition to above statement, there is need to provide the notes to financial statement to

provide details of measurement, recognition and other information. Notes to accounts is the most

important part of financial statement as it discloses information on methods, assumptions and

judgments that have been used to estimate the amount of all financial elements. In addition to

this it provides information on any change in accounting methods, policies, estimation and

assumptions (Austal Group-Annual Report, 2018).

9

of financial statements or reports. Following are the major components of financial statements

that Austal Group Limited has prepared as per the conceptual framework:

Income Statement or statement of financial performance: Income statement is the most

important financial statement prepared to reflect the financial performance of the company

during the specific period. In annual report of Austal Group Limited only consolidated income

statement is provided which shows the financial performance of the holding company as well as

all the subsidiaries. This statement provides information on revenue and expenses (Austal

Group-Annual Report, 2018).

Balance sheet or statement of financial position: Austal Group Limited has provided only

consolidated balance sheet that reflects the financial position of the parent company as well as all

the subsidiaries. The basic elements of the statement of financial positions are assets, liabilities

and equity.

Statement of change in equity: Contribution and distribution made by shareholders are being

disclosed in this statement. This statement is also prepared as consolidated statement.

Statement of cash flow: This statement discloses information on the cash flows various

activities such as operating activity, financing activity and investing activity. It is also presented

as consolidated statement to provide cash flow information for whole group (Austal Group-

Annual Report, 2018).

In addition to above statement, there is need to provide the notes to financial statement to

provide details of measurement, recognition and other information. Notes to accounts is the most

important part of financial statement as it discloses information on methods, assumptions and

judgments that have been used to estimate the amount of all financial elements. In addition to

this it provides information on any change in accounting methods, policies, estimation and

assumptions (Austal Group-Annual Report, 2018).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D (II): Principle of recognition and measurement bases used for assets, revenue and

liabilities

Revenue: Austal Group recognised most of its revenue through the construction

business. IFRS 15 deals with all types of revenue contracts including construction

contracts. Austal Group recognizes revenue when it is probable that economic benefits

will flow to the company and such revenue can be measured in terms of monetary value.

Revenue is measured at fair value of the consideration received or receivable. Austal

Group makes use of percentage of completion method to recognize the actual revenue

and cost related to such revenue (Conceptual Framework, 2018).

Assets: There are many assets that company present in their balance sheet and there have

different recognition principle and measurement bases of each asset. Cash and cash

equivalents consists of cash and short term deposits with three months of maturity. Trade

receivables are measured as the sales amount less any allowances made for the amount of

uncollectible. Receivables have been recognized on the basis of credit terms given to the

customers and information given in the invoice. Inventory are measured at lower of net

realizable value and cost, and it is recognised at weighted average cost basis. Plant,

property and equipment is being recognised at historical cost basis which means cost less

any accumulated depreciation or impairment. Intangible asset that has been acquired are

initially measured at cost less any impairment losses and amortisation (Austal Group-

Annual Report, 2018).

Liabilities: Trade payable have been measured at amortized cost and they are recognised

when company become obliged to make the payments in future in respect to expenses.

Provisions are recognised when there is obligation to settle the future obligation that has

been arising due to past event. Borrowings are initially recognised at fair value of the

amount received minus any value paid for transaction cost. After that they are measured

at amortized cost through using the effective interest method (Austal Group-Annual

Report, 2018).

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group

Relevance: Relevance means financial information should have predictive and confirmative

value that has capability to influence the economic decision of the users (Conceptual Framework,

10

liabilities

Revenue: Austal Group recognised most of its revenue through the construction

business. IFRS 15 deals with all types of revenue contracts including construction

contracts. Austal Group recognizes revenue when it is probable that economic benefits

will flow to the company and such revenue can be measured in terms of monetary value.

Revenue is measured at fair value of the consideration received or receivable. Austal

Group makes use of percentage of completion method to recognize the actual revenue

and cost related to such revenue (Conceptual Framework, 2018).

Assets: There are many assets that company present in their balance sheet and there have

different recognition principle and measurement bases of each asset. Cash and cash

equivalents consists of cash and short term deposits with three months of maturity. Trade

receivables are measured as the sales amount less any allowances made for the amount of

uncollectible. Receivables have been recognized on the basis of credit terms given to the

customers and information given in the invoice. Inventory are measured at lower of net

realizable value and cost, and it is recognised at weighted average cost basis. Plant,

property and equipment is being recognised at historical cost basis which means cost less

any accumulated depreciation or impairment. Intangible asset that has been acquired are

initially measured at cost less any impairment losses and amortisation (Austal Group-

Annual Report, 2018).

Liabilities: Trade payable have been measured at amortized cost and they are recognised

when company become obliged to make the payments in future in respect to expenses.

Provisions are recognised when there is obligation to settle the future obligation that has

been arising due to past event. Borrowings are initially recognised at fair value of the

amount received minus any value paid for transaction cost. After that they are measured

at amortized cost through using the effective interest method (Austal Group-Annual

Report, 2018).

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group

Relevance: Relevance means financial information should have predictive and confirmative

value that has capability to influence the economic decision of the users (Conceptual Framework,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018). Financial information such as revenue has the ability to influence the economic decision

of the stakeholders and such information has been included in the financial statement of Austal

Group.

(Austal Group-Annual Report, 2018)

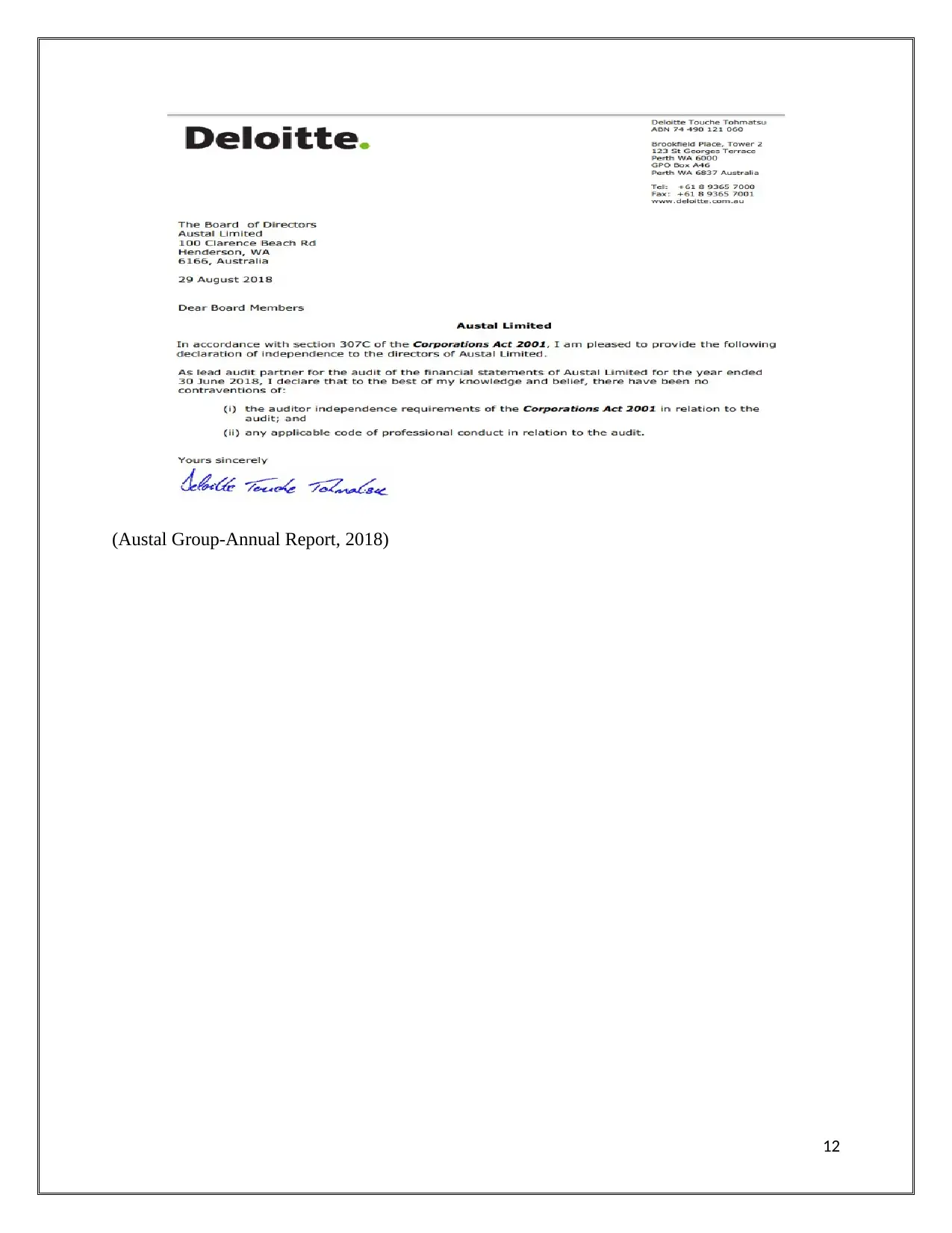

Faithful Representation: This qualitative characteristic states that financial information should

have three main characteristics in order to be recognised in the financial report. Information

should be complete, neutral and free form error (Conceptual Framework, 2018). In order to

check that information presented in the financial statement is free from errors, complete and

neutral, it is important to check the auditor’s statement and verify the same.

11

of the stakeholders and such information has been included in the financial statement of Austal

Group.

(Austal Group-Annual Report, 2018)

Faithful Representation: This qualitative characteristic states that financial information should

have three main characteristics in order to be recognised in the financial report. Information

should be complete, neutral and free form error (Conceptual Framework, 2018). In order to

check that information presented in the financial statement is free from errors, complete and

neutral, it is important to check the auditor’s statement and verify the same.

11

(Austal Group-Annual Report, 2018)

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.