Contemporary Issues in Accounting: Environmental Accounting Focus

VerifiedAdded on 2022/12/30

|17

|3309

|31

Report

AI Summary

This research proposal delves into contemporary issues in accounting, specifically highlighting the unaccountability of environmental factors within traditional financial accounting practices. The paper emphasizes the significance of environmental accounting, presenting a general introduction, practical and theoretical motivations, and a comprehensive literature review. It explores the deficiencies of traditional accounting systems in addressing environmental concerns, emphasizing the importance of incorporating environmental factors for managers, accountants, and regulators. The theoretical motivation centers on environmental management systems, while practical motivation highlights the impact of environmental disasters and the need for sustainability. The literature review examines existing research on corporate social and environmental reporting, challenges faced by traditional accounting, and the impact of environmental management accounting in Europe. The proposal concludes with a hypothesis suggesting a negative impact of unaccounted environmental factors on financial health, along with a description of the proposed research methodology, which will utilize both primary and secondary data to investigate the issue further.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s note

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The paper discusses about a research proposal that is purely based on the contemporary issues

that are faced in financial accounting by the accountants. The broad area of issues has been

narrowed down and a particular issue has been focussed on. The issue that is firmly

emphasised in the paper is the issue of accounting that is related to the unaccountability of the

environmental factors and the importance of environmental accounting over traditional

accounting. The mandatory sections provided in the paper in relation to this issue are general

introduction of the topic, relevance of the topic to the paper and importance of the issue.

Other highlighted sections comprise of theoretical and practical motivation of the issue.

Theoretical motivation states the theory or the accounting framework on which the current

issue is based. Practical motivation talks about the practical implication of the issue. The

literature review section describes some of the important papers related to environmental

accounting and the challenges faced by traditional accounting due unaccountability of

environmental factors. At the end part, a suitable hypothesis is provided that clearly justifies

the paper and the method applied for research is also stated briefly.

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The paper discusses about a research proposal that is purely based on the contemporary issues

that are faced in financial accounting by the accountants. The broad area of issues has been

narrowed down and a particular issue has been focussed on. The issue that is firmly

emphasised in the paper is the issue of accounting that is related to the unaccountability of the

environmental factors and the importance of environmental accounting over traditional

accounting. The mandatory sections provided in the paper in relation to this issue are general

introduction of the topic, relevance of the topic to the paper and importance of the issue.

Other highlighted sections comprise of theoretical and practical motivation of the issue.

Theoretical motivation states the theory or the accounting framework on which the current

issue is based. Practical motivation talks about the practical implication of the issue. The

literature review section describes some of the important papers related to environmental

accounting and the challenges faced by traditional accounting due unaccountability of

environmental factors. At the end part, a suitable hypothesis is provided that clearly justifies

the paper and the method applied for research is also stated briefly.

2

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Practical Motivation...................................................................................................................3

Theoretical Motivation...............................................................................................................4

Literature Review.......................................................................................................................4

Hypothesis..................................................................................................................................7

Research Method........................................................................................................................7

Appendix..................................................................................................................................11

Table – Annotated Bibliography for Selected Articles............................................................11

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Practical Motivation...................................................................................................................3

Theoretical Motivation...............................................................................................................4

Literature Review.......................................................................................................................4

Hypothesis..................................................................................................................................7

Research Method........................................................................................................................7

Appendix..................................................................................................................................11

Table – Annotated Bibliography for Selected Articles............................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Contemporary issues in Accounting is a very important study as it is related to the

upper level, advanced financial accounting subjects. There could be a range of accounting

concepts and policies which are required for addressing the contemporary accounting issues.

The issues could be of many types such as approaches to measurement, accounting of the fair

value, conceptual framework related to financial reporting, corporate governance and

management of the earnings. It is important to provide a research on the contemporary issues

of accounting because these issues hamper the accounting principles and standards, auditing

standards, quality control maintenance and different strategies of regulation. The objective of

this research is to provide a significant relationship between the fundamental environment

and the accounting functions based on accounting research quality. The objective can be

fulfilled through the theory of environmental accounting and also through a review of the five

aspects related to this category, that is, sustainability, disclosure of information, management

of cost and behavioural science.

Practical Motivation

The paper is focussed on the study of the issues that are related to environmental

accounting and explores the root of the issue as well. The development of the issues related to

environmental accounting was first initiated in connection with sustainability and

environmental disasters. There have been many deficiencies of the traditional accounting

system due to non-accountability of the relevance of the environment (Rankin et al.

2012). This issue is very important to practice by the managers, accountants, regulators and

other authorities because they are always reluctant in taking into account the environmental

factors in traditional accounting and therefore lack of these factors would disregard the social

cost (Rankin et al. 2012). These issues are important to highlight as these would lead to

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Contemporary issues in Accounting is a very important study as it is related to the

upper level, advanced financial accounting subjects. There could be a range of accounting

concepts and policies which are required for addressing the contemporary accounting issues.

The issues could be of many types such as approaches to measurement, accounting of the fair

value, conceptual framework related to financial reporting, corporate governance and

management of the earnings. It is important to provide a research on the contemporary issues

of accounting because these issues hamper the accounting principles and standards, auditing

standards, quality control maintenance and different strategies of regulation. The objective of

this research is to provide a significant relationship between the fundamental environment

and the accounting functions based on accounting research quality. The objective can be

fulfilled through the theory of environmental accounting and also through a review of the five

aspects related to this category, that is, sustainability, disclosure of information, management

of cost and behavioural science.

Practical Motivation

The paper is focussed on the study of the issues that are related to environmental

accounting and explores the root of the issue as well. The development of the issues related to

environmental accounting was first initiated in connection with sustainability and

environmental disasters. There have been many deficiencies of the traditional accounting

system due to non-accountability of the relevance of the environment (Rankin et al.

2012). This issue is very important to practice by the managers, accountants, regulators and

other authorities because they are always reluctant in taking into account the environmental

factors in traditional accounting and therefore lack of these factors would disregard the social

cost (Rankin et al. 2012). These issues are important to highlight as these would lead to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

exploitation of natural resources. This issue is necessary to address because it is important for

analysing and disclosing the problems of a defined economic system.

Theoretical Motivation

The environmental accounting relates to the framework or theory of environmental

management system (Welford 2016). According to environmental management system, there

are processes and practices that are undertaken for the enhancement of operational efficiency

of the corporation through the impact of environment (Laugen et al. 2014). Due to positive

environmental effect, the firm’s operation would improve and it would in turn lead to the

improvement of the performance of the firm in the market. In recent days, accountants try to

quantify the environmental impact of business activities in order to assess the sustainability

of environment and also the surrounding community (Henderson et al. 2015). In addition to

this, addressing issues related to environment would help in the formulation of a strategic

planning which would incorporate the sustainability of the environment. Sometimes due to

not being socially and environmentally responsible, the firms might be forced to shut down

their operations. Therefore, in recent days, firms are working hard for achieving a greater

level of social and environmental development in their course of operations (Bebbington,

Unerman and O’dwyer 2014).

Literature Review

The first paper published in relation to the environmental accounting brings into light

the phenomenon of corporate social and environmental reporting. The different factors that

have aided to the activity of corporate social and environmental reporting are the roles of the

information that have appeared in the dialogue of the organisation with the society (Fernando

and Lawrence 2014). According to views of different authors, the two approaches or

corporate social and environmental reporting is based on a form of accountability and the

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

exploitation of natural resources. This issue is necessary to address because it is important for

analysing and disclosing the problems of a defined economic system.

Theoretical Motivation

The environmental accounting relates to the framework or theory of environmental

management system (Welford 2016). According to environmental management system, there

are processes and practices that are undertaken for the enhancement of operational efficiency

of the corporation through the impact of environment (Laugen et al. 2014). Due to positive

environmental effect, the firm’s operation would improve and it would in turn lead to the

improvement of the performance of the firm in the market. In recent days, accountants try to

quantify the environmental impact of business activities in order to assess the sustainability

of environment and also the surrounding community (Henderson et al. 2015). In addition to

this, addressing issues related to environment would help in the formulation of a strategic

planning which would incorporate the sustainability of the environment. Sometimes due to

not being socially and environmentally responsible, the firms might be forced to shut down

their operations. Therefore, in recent days, firms are working hard for achieving a greater

level of social and environmental development in their course of operations (Bebbington,

Unerman and O’dwyer 2014).

Literature Review

The first paper published in relation to the environmental accounting brings into light

the phenomenon of corporate social and environmental reporting. The different factors that

have aided to the activity of corporate social and environmental reporting are the roles of the

information that have appeared in the dialogue of the organisation with the society (Fernando

and Lawrence 2014). According to views of different authors, the two approaches or

corporate social and environmental reporting is based on a form of accountability and the

5

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

theory of stakeholders. It is mainly concerned with the self-reporting activity performed by

the organisations. It is depicted in the paper that this reporting process is generally concerned

with the natural environment, employees, customers and communities. All these elements

together leads to the formation of organisation-society interaction. Empirical researches have

revealed that the corporate, social and environmental reporting sometimes might not be

effective as it is not governed strictly by the regulations and it also does not seem to have any

relation with profitability (Fernando and Lawrence 2014). Despite of these challenges of the

authors in their empirical investigation, there exists different theories that reflect the decision-

usefulness studies, economic theory studies and social and political theory studies. These

theories govern the information that are reflected in the reporting of the financial report by

the companies.

The second paper chosen for this research focusses on the challenges that are faced by

the traditional accounting due to introduction of a new concept of accounting known as

environmental accounting. It has been widely stated that the economic activity performed in

the natural environment influences environmental accounting at a greater extent and also

helps to reach a level of sustainability in the organisation (Bhimani and Willcocks 2014).

This in turn increases the corporate social responsibilities of the organisation. This broadly

means that the base of environmental protection and accounting is situated in the concept of

social accounting (Bhimani and Willcocks 2014).

According to the authors of this paper, the relationship between environment and

information for accounting in the economic sphere can be considered as a separate area for

the development of accounts. Initially social accounting was considered to be a factor

responsible for the capitalisation of the value of the stakeholders. Recent days have put on

more focus on the environmental side making it stronger in value for the firms (Bhimani and

Willcocks 2014). Considering the performance of the recent business firms, the

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

theory of stakeholders. It is mainly concerned with the self-reporting activity performed by

the organisations. It is depicted in the paper that this reporting process is generally concerned

with the natural environment, employees, customers and communities. All these elements

together leads to the formation of organisation-society interaction. Empirical researches have

revealed that the corporate, social and environmental reporting sometimes might not be

effective as it is not governed strictly by the regulations and it also does not seem to have any

relation with profitability (Fernando and Lawrence 2014). Despite of these challenges of the

authors in their empirical investigation, there exists different theories that reflect the decision-

usefulness studies, economic theory studies and social and political theory studies. These

theories govern the information that are reflected in the reporting of the financial report by

the companies.

The second paper chosen for this research focusses on the challenges that are faced by

the traditional accounting due to introduction of a new concept of accounting known as

environmental accounting. It has been widely stated that the economic activity performed in

the natural environment influences environmental accounting at a greater extent and also

helps to reach a level of sustainability in the organisation (Bhimani and Willcocks 2014).

This in turn increases the corporate social responsibilities of the organisation. This broadly

means that the base of environmental protection and accounting is situated in the concept of

social accounting (Bhimani and Willcocks 2014).

According to the authors of this paper, the relationship between environment and

information for accounting in the economic sphere can be considered as a separate area for

the development of accounts. Initially social accounting was considered to be a factor

responsible for the capitalisation of the value of the stakeholders. Recent days have put on

more focus on the environmental side making it stronger in value for the firms (Bhimani and

Willcocks 2014). Considering the performance of the recent business firms, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

environmental costs and revenues have come into picture while measuring and managing the

accounts of the company. The major environmental disasters have played a major role in

encouraging people about the environmental impact of the human activity.

The third paper that has been selected to conduct this research is based on a case-

study about the impact of environmental management accounting in Europe. The current

practices that are carried out in Europe are highlighted followed by the future potential of the

business. The paper analyses a trans-European project for investigating the future links

between environmental management and management accounting functions of the company

(Christ and Burritt 2013). This include four basic approaches of reporting such as external

financial reporting, social accountability reporting, energy and materials accounting, and

environmental management accounting (Christ and Burritt 2013).

The different approaches to environmental accounting relates to the balance between

financial and non-financial data, well-established distinction of accounting between the

primary target audiences. Few of the researchers of this paper deny that organisation’s

financial performance could be best measured by the non-financial indicators. Some of the

non-accountants challenge this view. In their perspective, the environmental accounting is

very well related to the performance measurement of the firms (Christ and Burritt 2013). The

external financial reporting assesses the financial effects of the company with respect to

environmental factors. These segments could be based on returns and risks. Without the use

of environmental factors, the investors, lenders or other financial stakeholders would not be

well informed about the financial condition and position of the company.

Another paper related to this study emphasises on sustainability development.

According to the paper, many studies have revealed that financial accounting could not

completely rely on the sustainability development due to regulations of financial accounting

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

environmental costs and revenues have come into picture while measuring and managing the

accounts of the company. The major environmental disasters have played a major role in

encouraging people about the environmental impact of the human activity.

The third paper that has been selected to conduct this research is based on a case-

study about the impact of environmental management accounting in Europe. The current

practices that are carried out in Europe are highlighted followed by the future potential of the

business. The paper analyses a trans-European project for investigating the future links

between environmental management and management accounting functions of the company

(Christ and Burritt 2013). This include four basic approaches of reporting such as external

financial reporting, social accountability reporting, energy and materials accounting, and

environmental management accounting (Christ and Burritt 2013).

The different approaches to environmental accounting relates to the balance between

financial and non-financial data, well-established distinction of accounting between the

primary target audiences. Few of the researchers of this paper deny that organisation’s

financial performance could be best measured by the non-financial indicators. Some of the

non-accountants challenge this view. In their perspective, the environmental accounting is

very well related to the performance measurement of the firms (Christ and Burritt 2013). The

external financial reporting assesses the financial effects of the company with respect to

environmental factors. These segments could be based on returns and risks. Without the use

of environmental factors, the investors, lenders or other financial stakeholders would not be

well informed about the financial condition and position of the company.

Another paper related to this study emphasises on sustainability development.

According to the paper, many studies have revealed that financial accounting could not

completely rely on the sustainability development due to regulations of financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

which had certain specific accounting norms (Bennett and James 2017). Due to these

limitations in the accounting norms, the capturing and presentation of environmental costs

have been not incompletely and inaccurately. The insufficient communication between the

accountants and the environmental experts has aided to this issue. This has deliberately led to

misallocation and incorrect calculation of the environmental costs (Loughran and McDonald

2016). In order to mitigate these limitations, there has been emergence of a newly formed

concept that is known as Environmental management accounting. This concept takes into

account both the monetary as well as physical aspects of environmental accounting. Though

in recent days it is found that the implementation of this concept also has certain

uncertainties.

All the papers to be used for the research narrowly comes down to the view that

environmental factors are very important for the purpose of financial accounting as well as

reporting. However, there has been limitation in the implementation of the concept of

environmental accounting due to its non-quantifiable nature. Inspite of these issues, the

concept has raised its importance in the firms and has been able to establish its importance

successfully in the accounting procedures of the firms.

Hypothesis

Null Hypothesis : The unaccountability of the environmental factors for the purpose

of financial accounting as well as reporting has a direct negative impact on the financial

health of the firm and creates misleading information in the financial report to be shown to

the stakeholders of the company.

Research Method

The research to be conducted for this study would be performed with the help of

primary as well as secondary data. The primary research is based on the primary data that

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

which had certain specific accounting norms (Bennett and James 2017). Due to these

limitations in the accounting norms, the capturing and presentation of environmental costs

have been not incompletely and inaccurately. The insufficient communication between the

accountants and the environmental experts has aided to this issue. This has deliberately led to

misallocation and incorrect calculation of the environmental costs (Loughran and McDonald

2016). In order to mitigate these limitations, there has been emergence of a newly formed

concept that is known as Environmental management accounting. This concept takes into

account both the monetary as well as physical aspects of environmental accounting. Though

in recent days it is found that the implementation of this concept also has certain

uncertainties.

All the papers to be used for the research narrowly comes down to the view that

environmental factors are very important for the purpose of financial accounting as well as

reporting. However, there has been limitation in the implementation of the concept of

environmental accounting due to its non-quantifiable nature. Inspite of these issues, the

concept has raised its importance in the firms and has been able to establish its importance

successfully in the accounting procedures of the firms.

Hypothesis

Null Hypothesis : The unaccountability of the environmental factors for the purpose

of financial accounting as well as reporting has a direct negative impact on the financial

health of the firm and creates misleading information in the financial report to be shown to

the stakeholders of the company.

Research Method

The research to be conducted for this study would be performed with the help of

primary as well as secondary data. The primary research is based on the primary data that

8

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

will be collected directly from the internal people such as employees belonging to the

different organisations that have come up to introduce environmental accounting in the

organisation (Johnston 2017). The secondary research will be done with the help of

secondary data that will be collected from the different journals and articles published by the

authentic sources related to the companies and also by different featuring the positive and

negative effects of environmental accounting.

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

will be collected directly from the internal people such as employees belonging to the

different organisations that have come up to introduce environmental accounting in the

organisation (Johnston 2017). The secondary research will be done with the help of

secondary data that will be collected from the different journals and articles published by the

authentic sources related to the companies and also by different featuring the positive and

negative effects of environmental accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

References

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and

accountability (pp. 21-32). Routledge.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bhimani, A. and Willcocks, L., 2014. Digitisation,‘Big Data’and the transformation of

accounting information. Accounting and Business Research, 44(4), pp.469-490.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting: the significance

of contingent variables for adoption. Journal of Cleaner Production, 41, pp.163-173.

Fernando, S. and Lawrence, S., 2014. A theoretical framework for CSR practices: integrating

legitimacy theory, stakeholder theory and institutional theory. Journal of Theoretical

Accounting Research, 10(1), pp.149-178.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Johnston, M.P., 2017. Secondary data analysis: A method of which the time has

come. Qualitative and quantitative methods in libraries, 3(3), pp.619-626.

Laugen, A.T., Engelhard, G.H., Whitlock, R., Arlinghaus, R., Dankel, D.J., Dunlop, E.S.,

Eikeset, A.M., Enberg, K., Jørgensen, C., Matsumura, S. and Nusslé, S., 2014. Evolutionary

impact assessment: accounting for evolutionary consequences of fishing in an ecosystem

approach to fisheries management. Fish and Fisheries, 15(1), pp.65-96.

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

References

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and

accountability (pp. 21-32). Routledge.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bhimani, A. and Willcocks, L., 2014. Digitisation,‘Big Data’and the transformation of

accounting information. Accounting and Business Research, 44(4), pp.469-490.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting: the significance

of contingent variables for adoption. Journal of Cleaner Production, 41, pp.163-173.

Fernando, S. and Lawrence, S., 2014. A theoretical framework for CSR practices: integrating

legitimacy theory, stakeholder theory and institutional theory. Journal of Theoretical

Accounting Research, 10(1), pp.149-178.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Johnston, M.P., 2017. Secondary data analysis: A method of which the time has

come. Qualitative and quantitative methods in libraries, 3(3), pp.619-626.

Laugen, A.T., Engelhard, G.H., Whitlock, R., Arlinghaus, R., Dankel, D.J., Dunlop, E.S.,

Eikeset, A.M., Enberg, K., Jørgensen, C., Matsumura, S. and Nusslé, S., 2014. Evolutionary

impact assessment: accounting for evolutionary consequences of fishing in an ecosystem

approach to fisheries management. Fish and Fisheries, 15(1), pp.65-96.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Rankin, M., Stanton, P., McGowan, S., Ferlauto, K. and Tilling, M., 2012. Contemporary

issues in accounting.

Welford, R., 2016. Corporate environmental management 1: systems and strategies.

Routledge.

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Rankin, M., Stanton, P., McGowan, S., Ferlauto, K. and Tilling, M., 2012. Contemporary

issues in accounting.

Welford, R., 2016. Corporate environmental management 1: systems and strategies.

Routledge.

11

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

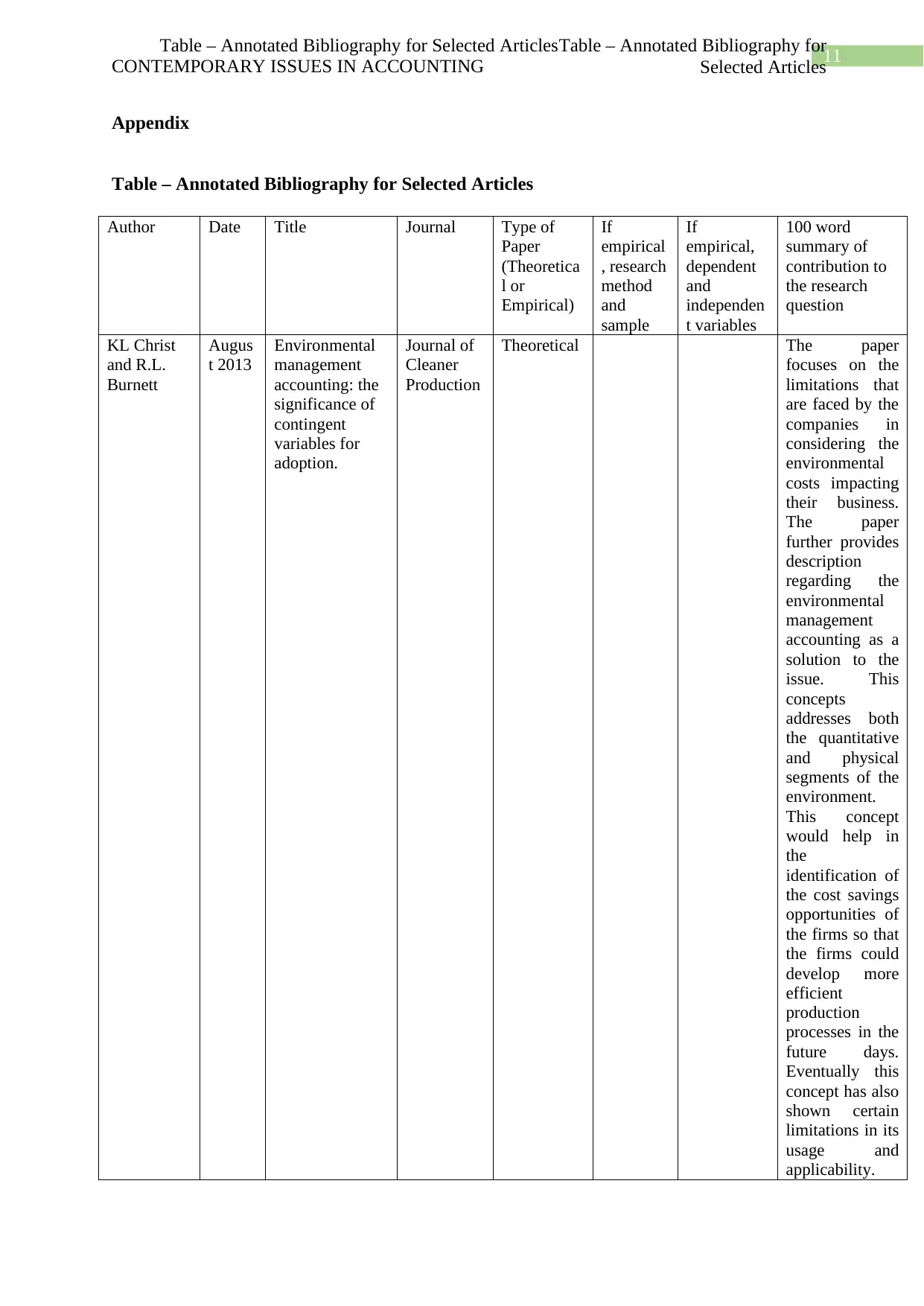

Appendix

Table – Annotated Bibliography for Selected Articles

Author Date Title Journal Type of

Paper

(Theoretica

l or

Empirical)

If

empirical

, research

method

and

sample

If

empirical,

dependent

and

independen

t variables

100 word

summary of

contribution to

the research

question

KL Christ

and R.L.

Burnett

Augus

t 2013

Environmental

management

accounting: the

significance of

contingent

variables for

adoption.

Journal of

Cleaner

Production

Theoretical The paper

focuses on the

limitations that

are faced by the

companies in

considering the

environmental

costs impacting

their business.

The paper

further provides

description

regarding the

environmental

management

accounting as a

solution to the

issue. This

concepts

addresses both

the quantitative

and physical

segments of the

environment.

This concept

would help in

the

identification of

the cost savings

opportunities of

the firms so that

the firms could

develop more

efficient

production

processes in the

future days.

Eventually this

concept has also

shown certain

limitations in its

usage and

applicability.

Table – Annotated Bibliography for Selected ArticlesTable – Annotated Bibliography for

Selected ArticlesCONTEMPORARY ISSUES IN ACCOUNTING

Appendix

Table – Annotated Bibliography for Selected Articles

Author Date Title Journal Type of

Paper

(Theoretica

l or

Empirical)

If

empirical

, research

method

and

sample

If

empirical,

dependent

and

independen

t variables

100 word

summary of

contribution to

the research

question

KL Christ

and R.L.

Burnett

Augus

t 2013

Environmental

management

accounting: the

significance of

contingent

variables for

adoption.

Journal of

Cleaner

Production

Theoretical The paper

focuses on the

limitations that

are faced by the

companies in

considering the

environmental

costs impacting

their business.

The paper

further provides

description

regarding the

environmental

management

accounting as a

solution to the

issue. This

concepts

addresses both

the quantitative

and physical

segments of the

environment.

This concept

would help in

the

identification of

the cost savings

opportunities of

the firms so that

the firms could

develop more

efficient

production

processes in the

future days.

Eventually this

concept has also

shown certain

limitations in its

usage and

applicability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.