Contemporary Accounting Theory: Conceptual Framework and Reporting

VerifiedAdded on 2022/11/11

|16

|4095

|106

Report

AI Summary

This report provides a comprehensive analysis of contemporary accounting theory, focusing on the conceptual framework and integrated/sustainability reporting. Part A delves into the development and concerns surrounding the IASB's conceptual framework, including issues raised by the AASB and academics, alongside an examination of Oil Search Limited's application of the framework. Part B explores the comparison between sustainability and integrated reporting, the suitability of conventional accounting, and the application of relevant theories to support their adoption. The report provides a comparative analysis of sustainability and integrated reporting, the suitability of conventional accounting to support the contents of sustainability and integrated reporting, and the application of theories to support the adoption of sustainability and integrated reporting in accounting. It also includes a detailed look at the components of an integrated report and the application of Vivo Energy Plc, concluding with an assessment of Oil Search Limited's integrated reporting practices. The report is based on the assignment brief ACCT20074 Contemporary Accounting Theory Term 1 Assessment 3: Practical report (Major assignment). It adheres to the guidelines of the report format with a word limit of 3,000 – 3,500 words and includes the executive summary, introduction, responses to the requirements in 2 parts & conclusion but excluding the list of references and appendixes.

Running head: CONTEMPORARY ACCOUNTING THEORY

Contemporary accounting theory

Name

Institution

Contemporary accounting theory

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 2

Abstract

Executive Summary

Business entities are guided by conceptual frameworks when preparing their financial

reports and statements. Likewise, the changing trends in financial reporting have seen the

stakeholders changing their focus on the items to be included in financial reports. Companies are

now focussing on creating value by forming a positive relationship with their stakeholders. The

increasing need to include non-financial performance in the financial statements have led to the

creation of sustainability reporting as well as integrated reporting. This report exams the two

important components of accounting, that is, the conceptual framework and integrated and

sustainability reporting. Key elements of the two pillars of accounting have been exhausted. The

findings show that although the Australian Accounting Standards Board (AASB) fully support

the IASB's conceptual framework, several issues need to be addressed as listed in the paper.

Likewise, the application of integrated and sustainability reporting at the expense of conventional

financial reporting is slowly gaining momentum as proposed by GRI and IIRC, respectively.

There is evident enough from the annual reports of Oil Search and Vivo Energy companies that

show the application of the conceptual framework, sustainability reporting an integrated

reporting.

Abstract

Executive Summary

Business entities are guided by conceptual frameworks when preparing their financial

reports and statements. Likewise, the changing trends in financial reporting have seen the

stakeholders changing their focus on the items to be included in financial reports. Companies are

now focussing on creating value by forming a positive relationship with their stakeholders. The

increasing need to include non-financial performance in the financial statements have led to the

creation of sustainability reporting as well as integrated reporting. This report exams the two

important components of accounting, that is, the conceptual framework and integrated and

sustainability reporting. Key elements of the two pillars of accounting have been exhausted. The

findings show that although the Australian Accounting Standards Board (AASB) fully support

the IASB's conceptual framework, several issues need to be addressed as listed in the paper.

Likewise, the application of integrated and sustainability reporting at the expense of conventional

financial reporting is slowly gaining momentum as proposed by GRI and IIRC, respectively.

There is evident enough from the annual reports of Oil Search and Vivo Energy companies that

show the application of the conceptual framework, sustainability reporting an integrated

reporting.

CONTEMPORARY ACCOUNTING THEORY 3

Introduction

The report discusses the application of both the Conceptual framework and sustainability/

integrated reporting. The report is divided into two parts. Part A addresses the concept of

financial reporting that was developed and endorsed by the International Accounting Standards

Board (IASB). PART A is further divided into four sections. Section A discusses the

development of the conceptual framework by IASB. Section B discusses the concerns raised by

the Australian Accounting Standards Board (AASB). Section C reviews the concerns raised by

academicians regarding the application of the conceptual framework. And Section D analysis the

application of the concept by the Oil Search Limited 10 Toea to prepare its financial statements.

Part B is divided into five sections to address the importance and adoption of integrated or

sustainability reporting in accounting. Section A is a comparative analysis of sustainability

reporting and integrated reporting. Section B discusses the suitability of conventional accounting

to support the contents of sustainability and integrated reporting. Section C discusses how

theories can be used to support the adoption of sustainability and integrated reporting in

accounting. Section D presents a tabular analysis on the components of an integrated report as

well as the application of Vivo Energy Plc in South Africa. Section E discuss whether or not the

Oil Search Limited 10 Toea Company prepares an integrated report.

PART A: Conceptual framework

a) Development of IASB’s Conceptual Framework for Financial Reporting

IASB has released three versions of the conceptual framework for financial reporting. The

three versions were released in 1989, 2010 and 2018. The three versions were developed based

Introduction

The report discusses the application of both the Conceptual framework and sustainability/

integrated reporting. The report is divided into two parts. Part A addresses the concept of

financial reporting that was developed and endorsed by the International Accounting Standards

Board (IASB). PART A is further divided into four sections. Section A discusses the

development of the conceptual framework by IASB. Section B discusses the concerns raised by

the Australian Accounting Standards Board (AASB). Section C reviews the concerns raised by

academicians regarding the application of the conceptual framework. And Section D analysis the

application of the concept by the Oil Search Limited 10 Toea to prepare its financial statements.

Part B is divided into five sections to address the importance and adoption of integrated or

sustainability reporting in accounting. Section A is a comparative analysis of sustainability

reporting and integrated reporting. Section B discusses the suitability of conventional accounting

to support the contents of sustainability and integrated reporting. Section C discusses how

theories can be used to support the adoption of sustainability and integrated reporting in

accounting. Section D presents a tabular analysis on the components of an integrated report as

well as the application of Vivo Energy Plc in South Africa. Section E discuss whether or not the

Oil Search Limited 10 Toea Company prepares an integrated report.

PART A: Conceptual framework

a) Development of IASB’s Conceptual Framework for Financial Reporting

IASB has released three versions of the conceptual framework for financial reporting. The

three versions were released in 1989, 2010 and 2018. The three versions were developed based

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 4

on the concerns and issues raised by the users about the previous versions. The conceptual

framework remained unchanged since its introduction in 1989. Both the FASB and IASB began

the process of reviewing and revising the concept of financial reporting began in 2004. However,

numerous consultations and disagreement between the two bodies slowed down the work. FASB

and IASB could only finalise Phase A of the project. IASB was forced to abandon their

collaboration with FASB and which show the completion of Phases B to H by September 2010

(IASB, The Conceptual Framework for Financial Reporting, 2010).

However, users of the 2010 conceptual framework cited several drawbacks. For instance,

the 2010 version lacked clear definition and distinction between different financial elements

which are included in the financial statements. Majority of participants raised several conceptual

issues during the 2011 agenda consultation. For instance, participants cited the 2010 concept of

financial reporting hindered the preparation of financial statements and reports. Therefore, in

September 2012, IASB embarked on addressing the conceptual issues that had been raised.

Instead of revision the concept, the board decided to address the topics that had been excluded in

the previous versions. As a result, two topics (disclosure and presentation were added. A finalised

project was published in 2013. The board embarked on collecting views of different users. The

final copy of the conceptual framework was released in May 2018. The 2018 version of the

conceptual framework comprises of eight topics (IASB, Conceptual Framework for Financial

Reporting 2018 , 2018).

b) Concerns raised by Australian accounting professions regarding the application of the

conceptual framework

AASB has raised key concerns about the application of the conceptual framework in

Australia. The two issues revolve around the reporting entity and special purpose financial

on the concerns and issues raised by the users about the previous versions. The conceptual

framework remained unchanged since its introduction in 1989. Both the FASB and IASB began

the process of reviewing and revising the concept of financial reporting began in 2004. However,

numerous consultations and disagreement between the two bodies slowed down the work. FASB

and IASB could only finalise Phase A of the project. IASB was forced to abandon their

collaboration with FASB and which show the completion of Phases B to H by September 2010

(IASB, The Conceptual Framework for Financial Reporting, 2010).

However, users of the 2010 conceptual framework cited several drawbacks. For instance,

the 2010 version lacked clear definition and distinction between different financial elements

which are included in the financial statements. Majority of participants raised several conceptual

issues during the 2011 agenda consultation. For instance, participants cited the 2010 concept of

financial reporting hindered the preparation of financial statements and reports. Therefore, in

September 2012, IASB embarked on addressing the conceptual issues that had been raised.

Instead of revision the concept, the board decided to address the topics that had been excluded in

the previous versions. As a result, two topics (disclosure and presentation were added. A finalised

project was published in 2013. The board embarked on collecting views of different users. The

final copy of the conceptual framework was released in May 2018. The 2018 version of the

conceptual framework comprises of eight topics (IASB, Conceptual Framework for Financial

Reporting 2018 , 2018).

b) Concerns raised by Australian accounting professions regarding the application of the

conceptual framework

AASB has raised key concerns about the application of the conceptual framework in

Australia. The two issues revolve around the reporting entity and special purpose financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 5

statements. AASB identified an inconsistency definition of reporting entity between the

Australian Statement of Accounting Concepts (SAC 1) and the Conceptual Framework for

Financial Reporting (RCF). The issues have led to a heated debate on the more appropriate

definition to follow in Australia. According to the RCF, all entities are required to prepare

general purpose financial statements (GPFS). While SAC 1 only requires legal entities to prepare

GPFS. AASB is concerned that the inconsistency in the definition may lead to non-compliance

with IFRS, wrong application of the Australian Accounting Standards (AASs) and

misinterpretation (KPMG, 2018).

The board also has issues about how the conceptual framework addresses the special

purpose financial statements (SPFS). AASB has been concerned about the failure of SPFS to

facilitate transparency, consistency, and comparability of financial statements. Before the release

of the 2018 version, AASB maintained that revising the conceptual framework was the only way

of sufficiently addressing the SPFS issue (KPMG, 2018).

c) Academic’s concerns regarding the application of the conceptual framework

Academicians have raised three areas of concerns with the conceptual framework. First,

academicians have linked the process of developing the conceptual framework with the creation

of a constitution. Both suffer from political interference. IASB listens to the concerns and views

of different stakeholders from different jurisdictions (Macías & Muiño, 2011). Each participant in

the process seeks to support their position leading to self-interest. Therefore, there is a likelihood

that the conceptual framework would fail to meet its objectivity when self-interests overrides

social interests (general purpose of financial reporting) (Kober, Lee, & Ng, 2012).

statements. AASB identified an inconsistency definition of reporting entity between the

Australian Statement of Accounting Concepts (SAC 1) and the Conceptual Framework for

Financial Reporting (RCF). The issues have led to a heated debate on the more appropriate

definition to follow in Australia. According to the RCF, all entities are required to prepare

general purpose financial statements (GPFS). While SAC 1 only requires legal entities to prepare

GPFS. AASB is concerned that the inconsistency in the definition may lead to non-compliance

with IFRS, wrong application of the Australian Accounting Standards (AASs) and

misinterpretation (KPMG, 2018).

The board also has issues about how the conceptual framework addresses the special

purpose financial statements (SPFS). AASB has been concerned about the failure of SPFS to

facilitate transparency, consistency, and comparability of financial statements. Before the release

of the 2018 version, AASB maintained that revising the conceptual framework was the only way

of sufficiently addressing the SPFS issue (KPMG, 2018).

c) Academic’s concerns regarding the application of the conceptual framework

Academicians have raised three areas of concerns with the conceptual framework. First,

academicians have linked the process of developing the conceptual framework with the creation

of a constitution. Both suffer from political interference. IASB listens to the concerns and views

of different stakeholders from different jurisdictions (Macías & Muiño, 2011). Each participant in

the process seeks to support their position leading to self-interest. Therefore, there is a likelihood

that the conceptual framework would fail to meet its objectivity when self-interests overrides

social interests (general purpose of financial reporting) (Kober, Lee, & Ng, 2012).

CONTEMPORARY ACCOUNTING THEORY 6

Second, discussions involving controversial issues have been associated with heated

debates. IASB through IFRS would be forced to abandon such debates for the future to avoid

confrontation between members. As a result, IASB might fail to address weight accounting

concerns leading to the loss of trust and relevancy of the framework (Christensen, 2010). Third,

organisations have turned their attention towards creating value by investing in the community

and environment. However, the conceptual framework does not provide a guideline of how

organisations should account for non-financial performances (Lin, 2015).

d) Oil Search Limited 10 Toea’s (ASX: OSH) application of the IASB’s concept of financial

reporting

i) OSH’s Financial statements/reports and their components as per the Conceptual

Framework

Chapter Three of the conceptual framework defines a financial statement as a financial report that

offers information about an entity’s financial elements such as assets, equity, liabilities, expenses,

and income. Common financial statements are the Income statement, Cash flow statement, and

the balance sheet (Oil Search, 2018 Annual Report, 2019).

OSH’s financial year ends on 31 December every year. The company prepared four financial

statements for the year ended 31 December 2018.

a) Comprehensive Income Statements: The statement comprises of three financial elements,

that is, revenue ($1,535,761,000), expenses ($11,945,559,000) and Net Income

(341,202,000).

b) Balance Sheet: The statement comprises of three financial elements, that is, Assets

($10,673,891,000), Liabilities ($5,508,273,000), and Equity (5,165,618,000).

Second, discussions involving controversial issues have been associated with heated

debates. IASB through IFRS would be forced to abandon such debates for the future to avoid

confrontation between members. As a result, IASB might fail to address weight accounting

concerns leading to the loss of trust and relevancy of the framework (Christensen, 2010). Third,

organisations have turned their attention towards creating value by investing in the community

and environment. However, the conceptual framework does not provide a guideline of how

organisations should account for non-financial performances (Lin, 2015).

d) Oil Search Limited 10 Toea’s (ASX: OSH) application of the IASB’s concept of financial

reporting

i) OSH’s Financial statements/reports and their components as per the Conceptual

Framework

Chapter Three of the conceptual framework defines a financial statement as a financial report that

offers information about an entity’s financial elements such as assets, equity, liabilities, expenses,

and income. Common financial statements are the Income statement, Cash flow statement, and

the balance sheet (Oil Search, 2018 Annual Report, 2019).

OSH’s financial year ends on 31 December every year. The company prepared four financial

statements for the year ended 31 December 2018.

a) Comprehensive Income Statements: The statement comprises of three financial elements,

that is, revenue ($1,535,761,000), expenses ($11,945,559,000) and Net Income

(341,202,000).

b) Balance Sheet: The statement comprises of three financial elements, that is, Assets

($10,673,891,000), Liabilities ($5,508,273,000), and Equity (5,165,618,000).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY 7

c) Cash flow statements: The statement comprises of three elements, that is, operating

activities ($854,632,000), investing activities ($810,997,000), financing activities ($-

458,324) and cash and cash equivalents ($600,557) (Oil Search, 2018 Annual Report,

2019).

d) Changes in Equity statements: The statement comprises of net amount from items such as

share capital, foreign reserves, treasury share reserve, employee equity compensation

reserve, and retained earnings. The change in equity totaled to $339,197,000.

ii) Recognition principles and measurement bases applied by OSH for revenue, assets, and

liabilities.

Recognition and measurement of financial elements are discussed in Chapter 5 and 6 of the

conceptual framework, respectively. Recognition refers to the process of including financial

elements in the financial statements. Likewise, measurement is defined as the process of

assigning monetary values to the financial elements. Recognition and measurement of financial

elements are done by considering several factors which should be both relevant and show faithful

representation (IASB, 2018).

OSH recognizes and measures all its financial assets and liabilities at fair value. The

company considers factors such as transactions costs, amortised cost, and depreciation (where

applicable) to measure assets and liabilities. The fair value of financial assets and liabilities refer

to their carrying amounts. Likewise, OSH recognises its income at realisable amount and

expenses at the historical cost (Oil Search, 2018 Annual Report, 2019).

iii) Qualitative characteristics of information exhibit in OSH’s financial reports.

c) Cash flow statements: The statement comprises of three elements, that is, operating

activities ($854,632,000), investing activities ($810,997,000), financing activities ($-

458,324) and cash and cash equivalents ($600,557) (Oil Search, 2018 Annual Report,

2019).

d) Changes in Equity statements: The statement comprises of net amount from items such as

share capital, foreign reserves, treasury share reserve, employee equity compensation

reserve, and retained earnings. The change in equity totaled to $339,197,000.

ii) Recognition principles and measurement bases applied by OSH for revenue, assets, and

liabilities.

Recognition and measurement of financial elements are discussed in Chapter 5 and 6 of the

conceptual framework, respectively. Recognition refers to the process of including financial

elements in the financial statements. Likewise, measurement is defined as the process of

assigning monetary values to the financial elements. Recognition and measurement of financial

elements are done by considering several factors which should be both relevant and show faithful

representation (IASB, 2018).

OSH recognizes and measures all its financial assets and liabilities at fair value. The

company considers factors such as transactions costs, amortised cost, and depreciation (where

applicable) to measure assets and liabilities. The fair value of financial assets and liabilities refer

to their carrying amounts. Likewise, OSH recognises its income at realisable amount and

expenses at the historical cost (Oil Search, 2018 Annual Report, 2019).

iii) Qualitative characteristics of information exhibit in OSH’s financial reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

Chapter two of the conceptual framework addresses the qualitative characteristics which a

financial report should have to be considered useful. The characteristic is faithful representation

and relevance. The two characteristics are further enhanced by factors such as comparability,

verifiability, timeliness, and understandability (IASB, 2018).

The financial report has been declared to have met the two qualitative characteristics by the

directors and the Deloitte Auditing firm. According to RJ Lee, the chairman of the board of

directors, the company had complied with the IAS and IFRS. Second, financial notes were

provided as required by the ASEC. Third, the financial report provided a true and fair financial

position of OSH’s financial position as at 31 December 2018. Auditors from Deloitte experienced

their satisfaction with the company’s financial report at the end of the audit (Oil Search, 2018

Annual Report, 2019).

PART B: Integrated/sustainability reporting

a) Comparative analysis between sustainability reporting and integrated reporting.

Both sustainability and integrated financial reporting goes beyond providing financial

information, particularly to the shareholders and investors. Unlike traditional reporting, both

sustainability and integrated reporting take the non-financial performance of an entity into

account. However, sustainability reporting is different from integrated reporting. Sustainability

reporting push for the inclusion of how companies intend to manage social and environmental

issues arising from their activities. GRI stated that companies cause a severe impact on the

community and the environment. Therefore, they should publicly disclose the risks that their

activities impose on the two factors as well as the strategies put in place to rectify arising issues

(Cohen, 2017).

Chapter two of the conceptual framework addresses the qualitative characteristics which a

financial report should have to be considered useful. The characteristic is faithful representation

and relevance. The two characteristics are further enhanced by factors such as comparability,

verifiability, timeliness, and understandability (IASB, 2018).

The financial report has been declared to have met the two qualitative characteristics by the

directors and the Deloitte Auditing firm. According to RJ Lee, the chairman of the board of

directors, the company had complied with the IAS and IFRS. Second, financial notes were

provided as required by the ASEC. Third, the financial report provided a true and fair financial

position of OSH’s financial position as at 31 December 2018. Auditors from Deloitte experienced

their satisfaction with the company’s financial report at the end of the audit (Oil Search, 2018

Annual Report, 2019).

PART B: Integrated/sustainability reporting

a) Comparative analysis between sustainability reporting and integrated reporting.

Both sustainability and integrated financial reporting goes beyond providing financial

information, particularly to the shareholders and investors. Unlike traditional reporting, both

sustainability and integrated reporting take the non-financial performance of an entity into

account. However, sustainability reporting is different from integrated reporting. Sustainability

reporting push for the inclusion of how companies intend to manage social and environmental

issues arising from their activities. GRI stated that companies cause a severe impact on the

community and the environment. Therefore, they should publicly disclose the risks that their

activities impose on the two factors as well as the strategies put in place to rectify arising issues

(Cohen, 2017).

CONTEMPORARY ACCOUNTING THEORY 9

On the other hand, integrated reporting goes beyond the inclusion of environmental and

social issues in the financial reports. Integrated reporting covers how companies create long term

value by turning both traditional and sustainability risks into opportunities. In other words,

integrated reporting hold that companies should convert social and environmental thinking into

business values (paiaconsulting, 2019).

Sustainability reporting which support separate publication of financial and sustainable

reports. Integrated reporting supports the integration of the two reports into one. Therefore,

integrated reporting in broader of the two because it brings together the information in the two

reports into one. An integrated report would include i) Financial and Operating analysis, ii)

Financial statements, iii) Corporate Governance report, and iv) Sustainability reporting

(paiaconsulting, 2019).

b) The suitability of conventional accounting to support the contents of sustainability and

integrated reporting.

Conventional accounting, also known as traditional accounting, has been criticised by many

users amid the current accounting trends. Conventional accounting deals only with financial

aspects of performance and ignores the social and environmental impacts of the entity’s

operations (Cohen, 2017).

Financial statements show the economic situation of a company. They are also the primary

sources of information to different stakeholders. Companies rely on the community and

environment to create value. However, conventional accounting does not exhibit how entity

operations influence social and environmental factors. Moreover, traditional accounting does not

show how companies are committed to addressing issues facing their employees, shareholders,

On the other hand, integrated reporting goes beyond the inclusion of environmental and

social issues in the financial reports. Integrated reporting covers how companies create long term

value by turning both traditional and sustainability risks into opportunities. In other words,

integrated reporting hold that companies should convert social and environmental thinking into

business values (paiaconsulting, 2019).

Sustainability reporting which support separate publication of financial and sustainable

reports. Integrated reporting supports the integration of the two reports into one. Therefore,

integrated reporting in broader of the two because it brings together the information in the two

reports into one. An integrated report would include i) Financial and Operating analysis, ii)

Financial statements, iii) Corporate Governance report, and iv) Sustainability reporting

(paiaconsulting, 2019).

b) The suitability of conventional accounting to support the contents of sustainability and

integrated reporting.

Conventional accounting, also known as traditional accounting, has been criticised by many

users amid the current accounting trends. Conventional accounting deals only with financial

aspects of performance and ignores the social and environmental impacts of the entity’s

operations (Cohen, 2017).

Financial statements show the economic situation of a company. They are also the primary

sources of information to different stakeholders. Companies rely on the community and

environment to create value. However, conventional accounting does not exhibit how entity

operations influence social and environmental factors. Moreover, traditional accounting does not

show how companies are committed to addressing issues facing their employees, shareholders,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING THEORY

10

society, and customers. Traditional reports do not include reports about their sustainability

investment and performance (Macve, 2015).

c) Application of theories to support the adoption of sustainability and integrated reporting in

accounting.

Both the stakeholders and legitimacy theories can be used to support the adoption of

sustainability and integrated accounting reporting.

Edward Freeman developed the stakeholder theory. Freeman defined a stakeholder as a

person or group that influence or is influenced by organisational activities. The theory states the

stronger the relationship between an entity and its stakeholders, the easier it as to fulfill its goals,

and the opposite is true. For a stronger relationship, companies should voluntarily invest a

significant amount of resources back to the community. In other words, companies should not

only focus on benefiting from society and the environment without giving back. Stakeholder

theory push for a stronger relationship between organisations and their stakeholders as proposed

by sustainability and integrated reporting (Deegan, 2013).

Legitimacy theory also establishes a relationship between a company and the society. The

theory states that the survival of any organisation depends on its respect to social values and

norms. The legitimate theory stipulates a company must be to act legitimately before its external

stakeholders. Therefore, companies can earn a legal status by voluntary providing information

about social and environmental disclosures in the annual reports. The theory recognises the

importance of social and environmental disclosures for the survival of any organization.

Remember that external stakeholders have the power to influence the legitimacy status of a

company (Deegan, 2013).

10

society, and customers. Traditional reports do not include reports about their sustainability

investment and performance (Macve, 2015).

c) Application of theories to support the adoption of sustainability and integrated reporting in

accounting.

Both the stakeholders and legitimacy theories can be used to support the adoption of

sustainability and integrated accounting reporting.

Edward Freeman developed the stakeholder theory. Freeman defined a stakeholder as a

person or group that influence or is influenced by organisational activities. The theory states the

stronger the relationship between an entity and its stakeholders, the easier it as to fulfill its goals,

and the opposite is true. For a stronger relationship, companies should voluntarily invest a

significant amount of resources back to the community. In other words, companies should not

only focus on benefiting from society and the environment without giving back. Stakeholder

theory push for a stronger relationship between organisations and their stakeholders as proposed

by sustainability and integrated reporting (Deegan, 2013).

Legitimacy theory also establishes a relationship between a company and the society. The

theory states that the survival of any organisation depends on its respect to social values and

norms. The legitimate theory stipulates a company must be to act legitimately before its external

stakeholders. Therefore, companies can earn a legal status by voluntary providing information

about social and environmental disclosures in the annual reports. The theory recognises the

importance of social and environmental disclosures for the survival of any organization.

Remember that external stakeholders have the power to influence the legitimacy status of a

company (Deegan, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY

11

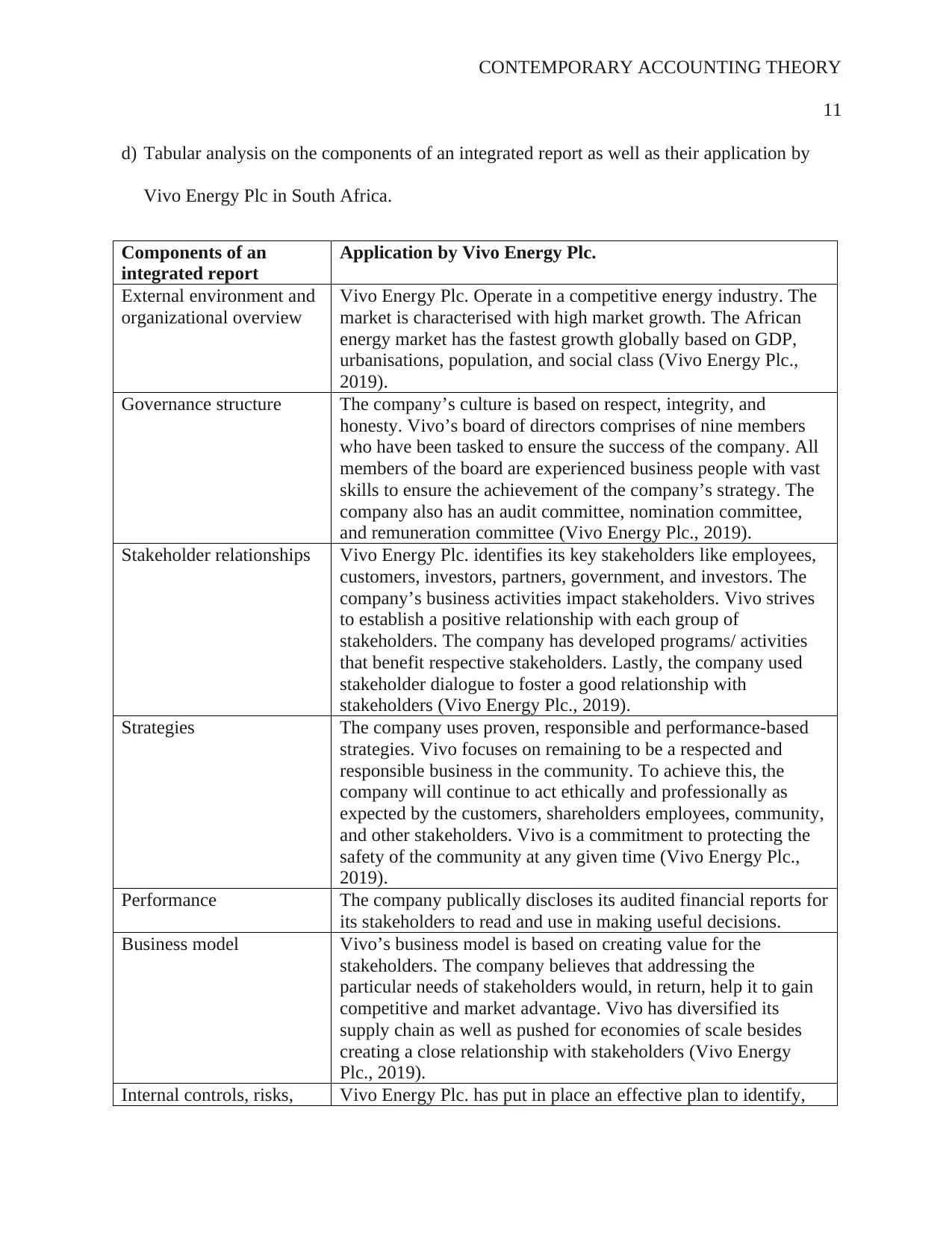

d) Tabular analysis on the components of an integrated report as well as their application by

Vivo Energy Plc in South Africa.

Components of an

integrated report

Application by Vivo Energy Plc.

External environment and

organizational overview

Vivo Energy Plc. Operate in a competitive energy industry. The

market is characterised with high market growth. The African

energy market has the fastest growth globally based on GDP,

urbanisations, population, and social class (Vivo Energy Plc.,

2019).

Governance structure The company’s culture is based on respect, integrity, and

honesty. Vivo’s board of directors comprises of nine members

who have been tasked to ensure the success of the company. All

members of the board are experienced business people with vast

skills to ensure the achievement of the company’s strategy. The

company also has an audit committee, nomination committee,

and remuneration committee (Vivo Energy Plc., 2019).

Stakeholder relationships Vivo Energy Plc. identifies its key stakeholders like employees,

customers, investors, partners, government, and investors. The

company’s business activities impact stakeholders. Vivo strives

to establish a positive relationship with each group of

stakeholders. The company has developed programs/ activities

that benefit respective stakeholders. Lastly, the company used

stakeholder dialogue to foster a good relationship with

stakeholders (Vivo Energy Plc., 2019).

Strategies The company uses proven, responsible and performance-based

strategies. Vivo focuses on remaining to be a respected and

responsible business in the community. To achieve this, the

company will continue to act ethically and professionally as

expected by the customers, shareholders employees, community,

and other stakeholders. Vivo is a commitment to protecting the

safety of the community at any given time (Vivo Energy Plc.,

2019).

Performance The company publically discloses its audited financial reports for

its stakeholders to read and use in making useful decisions.

Business model Vivo’s business model is based on creating value for the

stakeholders. The company believes that addressing the

particular needs of stakeholders would, in return, help it to gain

competitive and market advantage. Vivo has diversified its

supply chain as well as pushed for economies of scale besides

creating a close relationship with stakeholders (Vivo Energy

Plc., 2019).

Internal controls, risks, Vivo Energy Plc. has put in place an effective plan to identify,

11

d) Tabular analysis on the components of an integrated report as well as their application by

Vivo Energy Plc in South Africa.

Components of an

integrated report

Application by Vivo Energy Plc.

External environment and

organizational overview

Vivo Energy Plc. Operate in a competitive energy industry. The

market is characterised with high market growth. The African

energy market has the fastest growth globally based on GDP,

urbanisations, population, and social class (Vivo Energy Plc.,

2019).

Governance structure The company’s culture is based on respect, integrity, and

honesty. Vivo’s board of directors comprises of nine members

who have been tasked to ensure the success of the company. All

members of the board are experienced business people with vast

skills to ensure the achievement of the company’s strategy. The

company also has an audit committee, nomination committee,

and remuneration committee (Vivo Energy Plc., 2019).

Stakeholder relationships Vivo Energy Plc. identifies its key stakeholders like employees,

customers, investors, partners, government, and investors. The

company’s business activities impact stakeholders. Vivo strives

to establish a positive relationship with each group of

stakeholders. The company has developed programs/ activities

that benefit respective stakeholders. Lastly, the company used

stakeholder dialogue to foster a good relationship with

stakeholders (Vivo Energy Plc., 2019).

Strategies The company uses proven, responsible and performance-based

strategies. Vivo focuses on remaining to be a respected and

responsible business in the community. To achieve this, the

company will continue to act ethically and professionally as

expected by the customers, shareholders employees, community,

and other stakeholders. Vivo is a commitment to protecting the

safety of the community at any given time (Vivo Energy Plc.,

2019).

Performance The company publically discloses its audited financial reports for

its stakeholders to read and use in making useful decisions.

Business model Vivo’s business model is based on creating value for the

stakeholders. The company believes that addressing the

particular needs of stakeholders would, in return, help it to gain

competitive and market advantage. Vivo has diversified its

supply chain as well as pushed for economies of scale besides

creating a close relationship with stakeholders (Vivo Energy

Plc., 2019).

Internal controls, risks, Vivo Energy Plc. has put in place an effective plan to identify,

CONTEMPORARY ACCOUNTING THEORY

12

and opportunities assess, classify, and mitigate risks and risk exposure factors.

Some of the risk factors that hinder the effective operations of

the company are deteriorating relationship and reputation of

partners, oil price fluctuations, health and safety of employees,

currency exchange risks, credit management and non-compliance

risks, fraud, criminal activities, and bribery. Vivo has put in

place a countermeasure to address each of the risk factors.

Lastly, Vivo has invested heavily in maintaining/ improving the

quality of its assets and products (Vivo Energy Plc., 2019).

e) Sustainability/ integrated/ corporate social reports by the Oil Search Limited 10 Toea

Company.

Just like Vivo Energy Plc., Oil Search Limited 10 Toea Company also releases its social

responsibility report. First, OSH has a social responsibility strategy focus on identifying the

social and environmental issues caused by its activities and then create acceptable and sustainable

solutions. Supporting sustainable development remains a critical part of the company. Second,

stakeholder engagement is also a component of OSH’s sustainability report. The company

acknowledges that mutual respect with its key stakeholders is important in creating value. OSH

has given much priority to stakeholder dialogue. OSH’s leading stakeholders are shareholders,

suppliers, communities, government, employees, customers, and Non-government organisations.

The company engages each of these stakeholders based on mutual priorities (Oil Search, 2019).

Third, the company acknowledges that it operates in communities with different ethical

standards and cultural practices. Some communities are associated with a high level of corruption

and bribery risks. Therefore, OSH’s operations are guided by the principles of transparency and

integrity. Moreover, contractors and employees must adhere to the company’s code of conduct,

social responsibility policy, and corruption preventions policy (Oil Search Company, 2019).

Fourth, OSH has ensured that its activities have a minimal negative impact on the environment

12

and opportunities assess, classify, and mitigate risks and risk exposure factors.

Some of the risk factors that hinder the effective operations of

the company are deteriorating relationship and reputation of

partners, oil price fluctuations, health and safety of employees,

currency exchange risks, credit management and non-compliance

risks, fraud, criminal activities, and bribery. Vivo has put in

place a countermeasure to address each of the risk factors.

Lastly, Vivo has invested heavily in maintaining/ improving the

quality of its assets and products (Vivo Energy Plc., 2019).

e) Sustainability/ integrated/ corporate social reports by the Oil Search Limited 10 Toea

Company.

Just like Vivo Energy Plc., Oil Search Limited 10 Toea Company also releases its social

responsibility report. First, OSH has a social responsibility strategy focus on identifying the

social and environmental issues caused by its activities and then create acceptable and sustainable

solutions. Supporting sustainable development remains a critical part of the company. Second,

stakeholder engagement is also a component of OSH’s sustainability report. The company

acknowledges that mutual respect with its key stakeholders is important in creating value. OSH

has given much priority to stakeholder dialogue. OSH’s leading stakeholders are shareholders,

suppliers, communities, government, employees, customers, and Non-government organisations.

The company engages each of these stakeholders based on mutual priorities (Oil Search, 2019).

Third, the company acknowledges that it operates in communities with different ethical

standards and cultural practices. Some communities are associated with a high level of corruption

and bribery risks. Therefore, OSH’s operations are guided by the principles of transparency and

integrity. Moreover, contractors and employees must adhere to the company’s code of conduct,

social responsibility policy, and corruption preventions policy (Oil Search Company, 2019).

Fourth, OSH has ensured that its activities have a minimal negative impact on the environment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.