Analysis of Contemporary Accounting Issues for Airline Companies

VerifiedAdded on 2020/03/04

|16

|2002

|67

Report

AI Summary

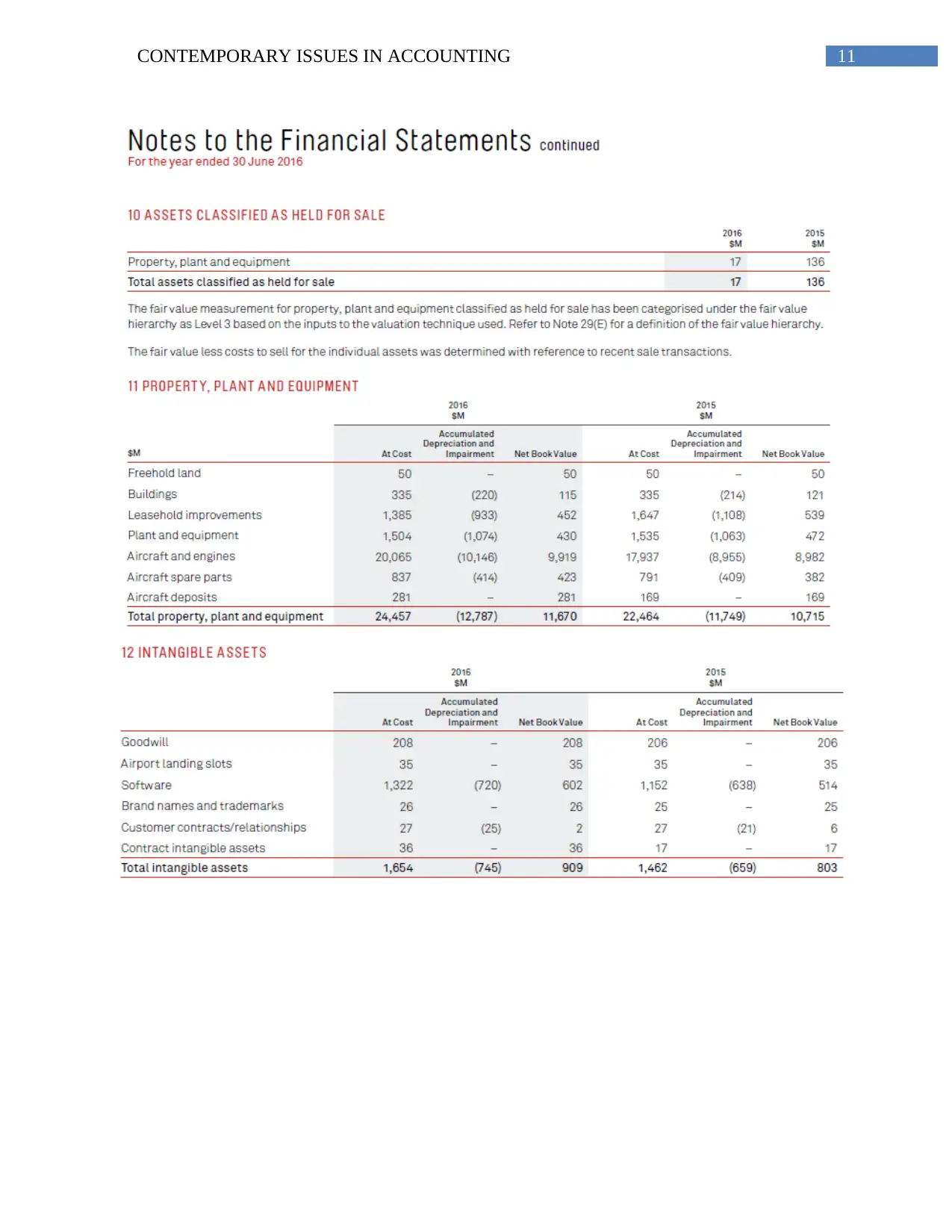

This report provides a comprehensive analysis of the accounting frameworks employed by Qantas Airways and Virgin Australia. It examines their adherence to AASB and Corporations Act 2001, focusing on revenue recognition, asset valuation (tangible and intangible), and depreciation methods. The study highlights the companies' adoption of prudence in financial reporting, including the delayed implementation of new standards like AASB 15 and AASB 16. Furthermore, it explores the rationale behind shareholder investment in these airlines, emphasizing increasing revenue and operating margins. The report concludes by summarizing the key findings and implications of the accounting practices of both companies, offering a comparative perspective on their financial strategies and reporting methodologies.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.