Evaluating the Contemporary Business Environment: A Report

VerifiedAdded on 2023/01/10

|12

|3899

|93

Report

AI Summary

This report provides a comprehensive analysis of the contemporary business environment, specifically focusing on the UK housing market. It begins by examining the changes in average housing prices over the past decade, presenting statistical data and trends. The report then delves into the economic determinants that influence the housing market, including unemployment rates, mortgage availability, consumer confidence, economic growth, and interest rates. It explores how these factors impact housing prices and market stability. Furthermore, the report investigates the actions taken by the UK government over the years to regulate and influence the housing market, such as the Green Land Belt scheme and state ownership policies. Finally, it assesses the significant influence of the COVID-19 pandemic on the UK housing market, analyzing the impact on demand, prices, and overall market dynamics. The report concludes by summarizing the key findings and implications of the analysis.

CONTEMPORARY

BUSINESS ENVIRONMENT

BUSINESS ENVIRONMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAINBODY...................................................................................................................................3

1 Change in the average prices of housing property changed in decade.....................................3

2. Economic determinants of changes in housing market...........................................................5

3. Action taken by government of over the period of years........................................................7

4. Influence of Covid-19 on Housing Markets of UK.................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAINBODY...................................................................................................................................3

1 Change in the average prices of housing property changed in decade.....................................3

2. Economic determinants of changes in housing market...........................................................5

3. Action taken by government of over the period of years........................................................7

4. Influence of Covid-19 on Housing Markets of UK.................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Busines environment can be defined as the sum of macro and micro environmental

factors that impacts on company’s functions and it’s decision-making process. Macro

environmental factors are also known as external environmental factors that includes political,

socio-cultural, economic, environmental, technological and legal factors that directly impacts on

organization’s decision-making process an it’s business activities. While micro environmental

factors are employees, organization’s infrastructure, management, demand and supply and others

directly impact on organization’s performance and it’s selling revenue. So, these factors are

considered internal factors of the company. To deep understanding of business environment

helps organization to adjust and accept emerging changes effectively. In this report will discuss

over how the average prices of Housing market has changed over the past years in the UK.

MAINBODY

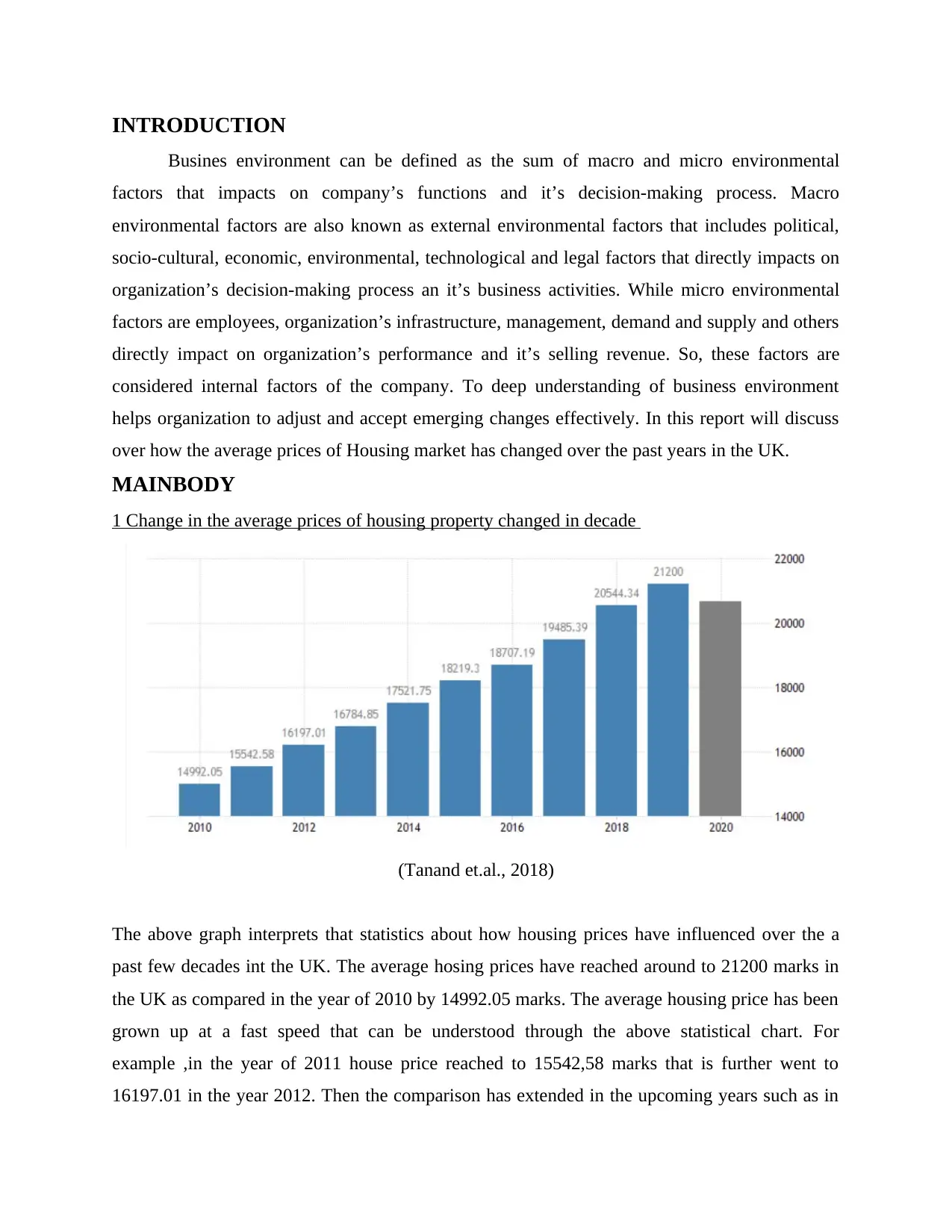

1 Change in the average prices of housing property changed in decade

(Tanand et.al., 2018)

The above graph interprets that statistics about how housing prices have influenced over the a

past few decades int the UK. The average hosing prices have reached around to 21200 marks in

the UK as compared in the year of 2010 by 14992.05 marks. The average housing price has been

grown up at a fast speed that can be understood through the above statistical chart. For

example ,in the year of 2011 house price reached to 15542,58 marks that is further went to

16197.01 in the year 2012. Then the comparison has extended in the upcoming years such as in

Busines environment can be defined as the sum of macro and micro environmental

factors that impacts on company’s functions and it’s decision-making process. Macro

environmental factors are also known as external environmental factors that includes political,

socio-cultural, economic, environmental, technological and legal factors that directly impacts on

organization’s decision-making process an it’s business activities. While micro environmental

factors are employees, organization’s infrastructure, management, demand and supply and others

directly impact on organization’s performance and it’s selling revenue. So, these factors are

considered internal factors of the company. To deep understanding of business environment

helps organization to adjust and accept emerging changes effectively. In this report will discuss

over how the average prices of Housing market has changed over the past years in the UK.

MAINBODY

1 Change in the average prices of housing property changed in decade

(Tanand et.al., 2018)

The above graph interprets that statistics about how housing prices have influenced over the a

past few decades int the UK. The average hosing prices have reached around to 21200 marks in

the UK as compared in the year of 2010 by 14992.05 marks. The average housing price has been

grown up at a fast speed that can be understood through the above statistical chart. For

example ,in the year of 2011 house price reached to 15542,58 marks that is further went to

16197.01 in the year 2012. Then the comparison has extended in the upcoming years such as in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2013 the average price of housing market went to 16784.85 marks that is further extended up to

17521.75 mark in the year of 2014. In the 2015 housing property average price have reached

around 18219.3 mark that is further enhanced to 18707.19 in the year of 2016. 2017 was the

boom year for the housing market because housing price have registered around 19485.39 that

led vast economic benefits for the housing property dealers as well as has improved GDP rate of

UK. But later on, it has further increased to 20544.34 in the years of 2018. In the case of 2019,

the housing prices went to 21200 that has registered as hike price of housing market because it

was quite maximize of all time. But in 2020 the housing prices have declined. The reason behind

is that COVID-19 outbreak all over the world which has led huge loss in all business market

(Davis and et.al., 2018). For example, due to corona pandemic most of the businesses have

unable to transports it’s product to multiple countries and people also avoid to go such places as

per the government instructions. As same case happens with UK countries whereas large number

of businesses runs their business smoothly but due to corona pandemic no business cannot sell

it’s products and services to the people. This situation makes people financially weak and has led

vast change in their demands. Thus, it can be framed that the prices of housing market have

always seen as improving trends excepts 2020.

The reason behind is that demand of house property is too much in people that lead

constant increment in average housing prices. There are other few reasons that have played huge

role in improving prices of houses. For example, inflation is one of the main stimulants that have

increased price of all house properties. Another is disposable income of UK’s people that have

increased due to high availability of job opportunities and raises basic salaries of existing

employees which allows them to invest large capital on the housing properties as it demonstrated

as the safest technique or strategy to invest in smooth running business. So, increment in

disposable income is also one of the specific reasons behind improving demand of housing

properties in the UK’s real estate market. There are large number of people across the global like

to invest in the housing properties to keep hope that it does not contain any type of risk or losses

while in majority of cases investors often would not get large return against investment which

have done by people in the housing property. The wide comparison among the prices is precisely

indicated the fact that price of house property is hiking continuously on a very good rate (De and

Vupru, 2017).

17521.75 mark in the year of 2014. In the 2015 housing property average price have reached

around 18219.3 mark that is further enhanced to 18707.19 in the year of 2016. 2017 was the

boom year for the housing market because housing price have registered around 19485.39 that

led vast economic benefits for the housing property dealers as well as has improved GDP rate of

UK. But later on, it has further increased to 20544.34 in the years of 2018. In the case of 2019,

the housing prices went to 21200 that has registered as hike price of housing market because it

was quite maximize of all time. But in 2020 the housing prices have declined. The reason behind

is that COVID-19 outbreak all over the world which has led huge loss in all business market

(Davis and et.al., 2018). For example, due to corona pandemic most of the businesses have

unable to transports it’s product to multiple countries and people also avoid to go such places as

per the government instructions. As same case happens with UK countries whereas large number

of businesses runs their business smoothly but due to corona pandemic no business cannot sell

it’s products and services to the people. This situation makes people financially weak and has led

vast change in their demands. Thus, it can be framed that the prices of housing market have

always seen as improving trends excepts 2020.

The reason behind is that demand of house property is too much in people that lead

constant increment in average housing prices. There are other few reasons that have played huge

role in improving prices of houses. For example, inflation is one of the main stimulants that have

increased price of all house properties. Another is disposable income of UK’s people that have

increased due to high availability of job opportunities and raises basic salaries of existing

employees which allows them to invest large capital on the housing properties as it demonstrated

as the safest technique or strategy to invest in smooth running business. So, increment in

disposable income is also one of the specific reasons behind improving demand of housing

properties in the UK’s real estate market. There are large number of people across the global like

to invest in the housing properties to keep hope that it does not contain any type of risk or losses

while in majority of cases investors often would not get large return against investment which

have done by people in the housing property. The wide comparison among the prices is precisely

indicated the fact that price of house property is hiking continuously on a very good rate (De and

Vupru, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Economic determinants of changes in housing market

There are a lot of changes which have taken place in the market of housing and socio

economic position of culture, family, society and neighbour are the economic determinants.

Business in market has to understand the economic flow in the country only then they will be

able to price their products and services accordingly. There are a lot of factor which influence

and have to be understood by companies like unemployment rate, credit and supply money,

interest rate, profit ratio people, etc. these factors can get growth in the market and support the

growths as well which would be discussed in the further report so that there is going to be a

better understanding. Customers want to have a satisfied and better lifestyle for themselves

which needs to be provided to them by the help of the government and these companies which

are working in the market (Mcdonnell and Sikander, 2017). But there are a lot of factors which

influence the customer’s needs and demands and those would be discussed as following so that

there is a better functioning.

Unemployment

The housing market is not being able to grow efficiently in the industry is because of this

factor and the organization is dependent on it. For example as of 2009 there were a lot of people

who lost jobs and there were hardly any opportunities for further jobs as well. There were a lot of

people who were left demotivated and they had taken loans which they were not able to pay and

had lost a lot of personal asset. People were not even paid the right wages for the extra efforts

they were asked to do or the hours they spent in the organization. Unemployment in the country

has been a major factor which has made the currency value also fall. There are a lot of factors

which have to be considered but the government is getting in opportunities for the people of the

country and because of this reason the housing market will be able to grow in the country.

Mortgage Availability

As of 2009 to 2014 the banks provided loans to the customers and these loans were large

which the customer’s salaries also could not have been able to pay back. They were five times

their salaries as well. But in 2016 to 2019 the banks started putting interest on this so that they

can get a better interest rate and make a profit from it as well. The customers were being

supported for the lifestyle they wanted to have which was a great factor but the interest levels

increased rapidly. As of 2019 the government took keen interest and reduced the interest rate by

There are a lot of changes which have taken place in the market of housing and socio

economic position of culture, family, society and neighbour are the economic determinants.

Business in market has to understand the economic flow in the country only then they will be

able to price their products and services accordingly. There are a lot of factor which influence

and have to be understood by companies like unemployment rate, credit and supply money,

interest rate, profit ratio people, etc. these factors can get growth in the market and support the

growths as well which would be discussed in the further report so that there is going to be a

better understanding. Customers want to have a satisfied and better lifestyle for themselves

which needs to be provided to them by the help of the government and these companies which

are working in the market (Mcdonnell and Sikander, 2017). But there are a lot of factors which

influence the customer’s needs and demands and those would be discussed as following so that

there is a better functioning.

Unemployment

The housing market is not being able to grow efficiently in the industry is because of this

factor and the organization is dependent on it. For example as of 2009 there were a lot of people

who lost jobs and there were hardly any opportunities for further jobs as well. There were a lot of

people who were left demotivated and they had taken loans which they were not able to pay and

had lost a lot of personal asset. People were not even paid the right wages for the extra efforts

they were asked to do or the hours they spent in the organization. Unemployment in the country

has been a major factor which has made the currency value also fall. There are a lot of factors

which have to be considered but the government is getting in opportunities for the people of the

country and because of this reason the housing market will be able to grow in the country.

Mortgage Availability

As of 2009 to 2014 the banks provided loans to the customers and these loans were large

which the customer’s salaries also could not have been able to pay back. They were five times

their salaries as well. But in 2016 to 2019 the banks started putting interest on this so that they

can get a better interest rate and make a profit from it as well. The customers were being

supported for the lifestyle they wanted to have which was a great factor but the interest levels

increased rapidly. As of 2019 the government took keen interest and reduced the interest rate by

0.5% which was great news for the customers (MEIYANI and Putra, 2019). This is going to

attract a lot of customers in the organization.

Consumer confidence

The customers do not have the confidence in them to be able to take loans from the banks. It

is very important for the customers to be able to pay the loans they have taken from the banks on

time so that they do not lose anything else value able because bank can seize the properties or

anything else (Hogsden, 2018). There are interest rates as well which are present on the loans

and that is a problem for the customers and for that reason the customers will have to be given

positive prices. It is when the customers feel that there is positive pricing for them only then they

will get attracted to housing market in United Kingdom.

Economic growth

The income level of the population was stable till Brexit did not take place and even after

that the population was able to get a better economic stability in the market. The customer’s

needs to have a good economic factor in the family only then they will be able to invest this large

amount in this industry as well (Bianchi, 2017). This is a major factor which the industry is

dependent on and there are so many luxurious houses which are being given away to customers

at a very low price and the company is not being able to make the right profit margins. To have

an improved lifestyle for the customers there are a lot of factors which have been considered by

the government of the country so that they can make the people get the best of services.

Interest rate

There is a direct associated with the interest rate and loans which the people take and were

not being able to pay back the right amount. Without the interest level of the government the

people would not have been able to take the dream house they wanted to because of the interest

rates being so high. There was a sudden rise in the interest rates in as of 2011 and 2012 which

make the customers get demotivated for purchasing the right house for them and because of

which there was an involvement of the government of the country. It was in 2013 that the

government took a lot of interest and reduced the rates which made the sales of the organization

increase.

Brexit is also one of the major factors which have made the sales of housing market fall

because of the following reasons. The currency value and policies which have changed has made

the housing market have a major change (Bansal and et.al., 2018). Due to Brexit a lot of people

attract a lot of customers in the organization.

Consumer confidence

The customers do not have the confidence in them to be able to take loans from the banks. It

is very important for the customers to be able to pay the loans they have taken from the banks on

time so that they do not lose anything else value able because bank can seize the properties or

anything else (Hogsden, 2018). There are interest rates as well which are present on the loans

and that is a problem for the customers and for that reason the customers will have to be given

positive prices. It is when the customers feel that there is positive pricing for them only then they

will get attracted to housing market in United Kingdom.

Economic growth

The income level of the population was stable till Brexit did not take place and even after

that the population was able to get a better economic stability in the market. The customer’s

needs to have a good economic factor in the family only then they will be able to invest this large

amount in this industry as well (Bianchi, 2017). This is a major factor which the industry is

dependent on and there are so many luxurious houses which are being given away to customers

at a very low price and the company is not being able to make the right profit margins. To have

an improved lifestyle for the customers there are a lot of factors which have been considered by

the government of the country so that they can make the people get the best of services.

Interest rate

There is a direct associated with the interest rate and loans which the people take and were

not being able to pay back the right amount. Without the interest level of the government the

people would not have been able to take the dream house they wanted to because of the interest

rates being so high. There was a sudden rise in the interest rates in as of 2011 and 2012 which

make the customers get demotivated for purchasing the right house for them and because of

which there was an involvement of the government of the country. It was in 2013 that the

government took a lot of interest and reduced the rates which made the sales of the organization

increase.

Brexit is also one of the major factors which have made the sales of housing market fall

because of the following reasons. The currency value and policies which have changed has made

the housing market have a major change (Bansal and et.al., 2018). Due to Brexit a lot of people

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

are left unemployed and they are not being given loans for this reason. There is a complete

imbalance in the economic factor and due to Covid-19 the customers have been demotivated to

shift around as well and communicate with others therefore the business is falling. Around

£215,925demand has fallen in the market for housing industry in United Kingdom which will

have to be maintained. The customers have to opt for the best alternative and sacrificed measure

for themselves so that there is a better performance in the future.

3. Action taken by government of over the period of years

The Government has been very active in the field of real estate and housing in UK. There have

been a series of actions that have been adopted by the government of UK and this can be

illustrated in following manner:

Green Land Belt: The UK Government has declared number of lands that are rich in

nature and wildlife under the green land belt scheme where that particular land has been

protected. This is done so that the nature and the wildlife both can be protected and the

benefit that it has towards the environment and sustainability aspect is also enormous

(Meen, Mihailov and Wang, 2016). In these particular areas, the construction of housing

is not allowed and the currently, there is an approximate 17% land that has been

categorised under the green belt land in UK. This helps in regulating the overall area over

which control is implemented regarding the construction of houses or in this case,

construction of any property in these areas that benefit the economy and the country other

wise.

State Ownership: All the property and land in UK is automatically included under the

ownership of the state until and unless there has been any personal registry of any kind by

any individual. This indicates, that initially, only state is the owner of the property and

hence the buying an selling of the land becomes regulated. Further, it also helps in

ensuring that there is no illegal occupying of the land by any individual and helps in

avoidance of any false claims as well that might be made over the land (Rubaszek and

Rubio, 2019). This regulates the overall retail industry and housing industry of UK to an

extreme extent where all the trades and exchanges that is taking place comes under the

review of the state government of UK itself.

Putting maximum and minimum price limits: This is another very effective measure that

has been implemented by the government of U where the overall maximum and

imbalance in the economic factor and due to Covid-19 the customers have been demotivated to

shift around as well and communicate with others therefore the business is falling. Around

£215,925demand has fallen in the market for housing industry in United Kingdom which will

have to be maintained. The customers have to opt for the best alternative and sacrificed measure

for themselves so that there is a better performance in the future.

3. Action taken by government of over the period of years

The Government has been very active in the field of real estate and housing in UK. There have

been a series of actions that have been adopted by the government of UK and this can be

illustrated in following manner:

Green Land Belt: The UK Government has declared number of lands that are rich in

nature and wildlife under the green land belt scheme where that particular land has been

protected. This is done so that the nature and the wildlife both can be protected and the

benefit that it has towards the environment and sustainability aspect is also enormous

(Meen, Mihailov and Wang, 2016). In these particular areas, the construction of housing

is not allowed and the currently, there is an approximate 17% land that has been

categorised under the green belt land in UK. This helps in regulating the overall area over

which control is implemented regarding the construction of houses or in this case,

construction of any property in these areas that benefit the economy and the country other

wise.

State Ownership: All the property and land in UK is automatically included under the

ownership of the state until and unless there has been any personal registry of any kind by

any individual. This indicates, that initially, only state is the owner of the property and

hence the buying an selling of the land becomes regulated. Further, it also helps in

ensuring that there is no illegal occupying of the land by any individual and helps in

avoidance of any false claims as well that might be made over the land (Rubaszek and

Rubio, 2019). This regulates the overall retail industry and housing industry of UK to an

extreme extent where all the trades and exchanges that is taking place comes under the

review of the state government of UK itself.

Putting maximum and minimum price limits: This is another very effective measure that

has been implemented by the government of U where the overall maximum and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

minimum prices have been set up by the government regarding the different categorises

of land in UK (Agnew and Lyons, 2018). Here the prices that have been established by

the government acts as upper or lower limit which cannot be exceeded by any dealer in

the real estate business of UK. These prices are reviewed by the government every year

after taking into consideration different factors like inflation, spending power etc. (Tao,

2019). The government keeps the prices under control and unnecessary hike in the prices

of UK is also avoided. This is necessary so that maximum number of people I UK can

afford the basic necessity of having a roof on their heads.

The analysis of the different factors therefore helps in concluding that there are a variety of

practices that have been adopted by the government of UK towards the increased regulation and

control over the trade practices that are adopted in the housing market of UK.

4. Influence of Covid-19 on Housing Markets of UK

The pandemic of Covid-19 impacted each and every sector of UK but the housing

markets are mainly influenced by this as the house prices and the rents initially fall but still the

houses are unaffordable to people with lower incomes (Nicola and et.al., 2020). During lock-

down, the government of UK advised the buyers to do the virtual meetings rather than in-person.

They must do the real meetings only when they are dealing with the offers and for that also they

must take care of all the safety measures of social distancing such as not touching the walls of

the houses and the property and if social distancing is not possible then they must wear the

masks when in person. Likewise, there are many effects of this pandemic which can be classifies

on the duration of its effects which are as follows:

Short-term

These impacts will be over the next 6-9 months. This will stop the buying and selling of

houses because even after the lock-down is over, the rate of the transaction will fall. This is due

to the financial instability of people causes by the disappearing of their incomes (Ashraf, 2020).

There will be restriction in the new house construction, so the prices will be low. Also, due to

Covid-19, more elderly people died, which freed some existing stock resulting in falling house

prices.

The unfreezing of lock-down was not predictable so if the lock-down lasts for long time, the

recovery rate will be low. Restaurant bookings were stopped, car sales were dropped to zero and

many more active things became inactive. It also made difficult for many businesses to reset and

of land in UK (Agnew and Lyons, 2018). Here the prices that have been established by

the government acts as upper or lower limit which cannot be exceeded by any dealer in

the real estate business of UK. These prices are reviewed by the government every year

after taking into consideration different factors like inflation, spending power etc. (Tao,

2019). The government keeps the prices under control and unnecessary hike in the prices

of UK is also avoided. This is necessary so that maximum number of people I UK can

afford the basic necessity of having a roof on their heads.

The analysis of the different factors therefore helps in concluding that there are a variety of

practices that have been adopted by the government of UK towards the increased regulation and

control over the trade practices that are adopted in the housing market of UK.

4. Influence of Covid-19 on Housing Markets of UK

The pandemic of Covid-19 impacted each and every sector of UK but the housing

markets are mainly influenced by this as the house prices and the rents initially fall but still the

houses are unaffordable to people with lower incomes (Nicola and et.al., 2020). During lock-

down, the government of UK advised the buyers to do the virtual meetings rather than in-person.

They must do the real meetings only when they are dealing with the offers and for that also they

must take care of all the safety measures of social distancing such as not touching the walls of

the houses and the property and if social distancing is not possible then they must wear the

masks when in person. Likewise, there are many effects of this pandemic which can be classifies

on the duration of its effects which are as follows:

Short-term

These impacts will be over the next 6-9 months. This will stop the buying and selling of

houses because even after the lock-down is over, the rate of the transaction will fall. This is due

to the financial instability of people causes by the disappearing of their incomes (Ashraf, 2020).

There will be restriction in the new house construction, so the prices will be low. Also, due to

Covid-19, more elderly people died, which freed some existing stock resulting in falling house

prices.

The unfreezing of lock-down was not predictable so if the lock-down lasts for long time, the

recovery rate will be low. Restaurant bookings were stopped, car sales were dropped to zero and

many more active things became inactive. It also made difficult for many businesses to reset and

survive. The loans are also not sanctioned because the government's decision to give emergency

finance is delaying day by day. The businesses have to be re-invented again resulting in a very

slow recovery to organize employment and production.

Medium-Term

This will lasts up to 2014. It states that if the lock-down lasts longer, then the more

business will find difficulty to sustain themselves and the slower recovery will be. If the lock-

down unfreezes also and the earnings begin but the savings of people will not remain that much

that is enough to buy the houses. The investors have already finished their savings in the

essential supplies of the households. The gains on the existing houses also fell down, resulting in

their inability to buy new larger houses.

The rates of houses today will lasts for 4-5 years but even if the prices of the houses fall down, it

will not result in more buying because the income of people stopped resulting in the depletion of

savings.

Long-Term

This impacts will lasts till 2030. If it is assumed that the pandemic dies and the situation

will recover soon resulting in better economy, then it can be expected that it can boost the

innovation (Cheshire and Hilber, 2020). For example, in communication technology, which can

impact the recovery of airlines negatively. The prices of houses can be increased by the pressure

of the politicians. This will decrease the rate of construction of new houses and the supply will

be less as compared to the demand.

The people start preferring the businesses which are run by sitting in their homes instead

of doing outings and go far. This would increase the demand for the space of offices in their

homes and will make the commuting cost less significant (French, 2020). The people will

migrate to the places where they can get these spaces at lower prices.

It can also impact by providing higher paid jobs which will results in increase in demand of the

houses. The more people will be migrated from the first order cities like London, Manchester etc.

to smaller cities like Cambridge etc. which are well-connected high amenity cities.

So, after going through the impacts of Covid-19 on the housing markets of UK, it becomes

clear that this will have effects which lasts longer on both the housing markets and the housing

policies. The house prices may fall rapidly but simultaneously making unaffordable for the low

income people. The lock-down will force majority of the people in UK to migrate in other

finance is delaying day by day. The businesses have to be re-invented again resulting in a very

slow recovery to organize employment and production.

Medium-Term

This will lasts up to 2014. It states that if the lock-down lasts longer, then the more

business will find difficulty to sustain themselves and the slower recovery will be. If the lock-

down unfreezes also and the earnings begin but the savings of people will not remain that much

that is enough to buy the houses. The investors have already finished their savings in the

essential supplies of the households. The gains on the existing houses also fell down, resulting in

their inability to buy new larger houses.

The rates of houses today will lasts for 4-5 years but even if the prices of the houses fall down, it

will not result in more buying because the income of people stopped resulting in the depletion of

savings.

Long-Term

This impacts will lasts till 2030. If it is assumed that the pandemic dies and the situation

will recover soon resulting in better economy, then it can be expected that it can boost the

innovation (Cheshire and Hilber, 2020). For example, in communication technology, which can

impact the recovery of airlines negatively. The prices of houses can be increased by the pressure

of the politicians. This will decrease the rate of construction of new houses and the supply will

be less as compared to the demand.

The people start preferring the businesses which are run by sitting in their homes instead

of doing outings and go far. This would increase the demand for the space of offices in their

homes and will make the commuting cost less significant (French, 2020). The people will

migrate to the places where they can get these spaces at lower prices.

It can also impact by providing higher paid jobs which will results in increase in demand of the

houses. The more people will be migrated from the first order cities like London, Manchester etc.

to smaller cities like Cambridge etc. which are well-connected high amenity cities.

So, after going through the impacts of Covid-19 on the housing markets of UK, it becomes

clear that this will have effects which lasts longer on both the housing markets and the housing

policies. The house prices may fall rapidly but simultaneously making unaffordable for the low

income people. The lock-down will force majority of the people in UK to migrate in other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

countries. The dealings of the houses must be allowed only when the dealers follow safety

measures of social distancing. Otherwise, they must organize virtual meetings which can be used

to visit the houses virtually.

CONCLUSION

This report has been concluded different aspects related to hiking house prices in the context

of Housing Market in the UK. It further has discussed about economic determinants and how it

has impacted on the housing prices in the UK. It has been summarized about government

initiatives such as tax reduction, subsidiaries and other type of regulation to over control hike

price of houses in the K’s real estate market in this report. The brief study provided

understanding about key impacts on Covid-19 pandemic that has created over the housing

market prices in the UK.

measures of social distancing. Otherwise, they must organize virtual meetings which can be used

to visit the houses virtually.

CONCLUSION

This report has been concluded different aspects related to hiking house prices in the context

of Housing Market in the UK. It further has discussed about economic determinants and how it

has impacted on the housing prices in the UK. It has been summarized about government

initiatives such as tax reduction, subsidiaries and other type of regulation to over control hike

price of houses in the K’s real estate market in this report. The brief study provided

understanding about key impacts on Covid-19 pandemic that has created over the housing

market prices in the UK.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Agnew, K. and Lyons, R. C., 2018. The impact of employment on housing prices: Detailed

evidence from FDI in Ireland. Regional Science and Urban Economics. 70. pp.174-189.

Ashraf, B.N., 2020. Stock markets’ reaction to COVID-19: cases or fatalities?. Research in

International Business and Finance, p.101249.

Bansal, H and et.al., 2018. Social Network Analytics for Contemporary Business Organizations.

IGI Global.

Bianchi, M.T., 2017. Discovering the role of innovation in contemporary business systems: an

assessment technique from the literature analysis. International Journal of Digital Culture

and Electronic Tourism. 2(1). pp.1-15.

Cheshire, P. and Hilber, C.A., 2020. What will crashing the economy do for the UK housing

market?. LSE COVID-19 Blog.

Davis, A and et.al., 2018. A Minimum Income Standard for the UK, 2008-2018: continuity and

change. York: Joseph Rowntree Foundation.

De, U.K. and Vupru, V., 2017. Location and neighbourhood conditions for housing choice and

its rental value. International Journal of Housing Markets and Analysis.

French, N., 2020. Property valuation in the UK: material uncertainty and COVID-19. Journal of

Property Investment & Finance.

Hogsden, J., 2018. The Contemporary Corporate Tax Strategy Environment. In Contemporary

Issues in Accounting (pp. 85-104). Palgrave Macmillan, Cham.

Mcdonnell, L. and Sikander, A., 2017. Skills and competencies for the contemporary human

resource practitioner: a synthesis of the academic, industry and employers'

perspectives. The Journal of Developing Areas. 51(1). pp.83-101.

Meen, G., Mihailov, A. and Wang, Y., 2016. Endogenous UK Housing Cycles and the Risk

Premium: Understanding the Next Housing Crisis (No. em-dp2016-02). Henley Business

School, Reading University

MEIYANI, E. and Putra, A.H.P.K., 2019. The relationship between islamic leadership on

employee engagement distribution in FMCG industry: Anthropology business review. The

Journal of Distribution Science. 17(5). pp.19-28.

Nicola, M. and et.al., 2020. The socio-economic implications of the coronavirus and COVID-19

pandemic: a review. International Journal of Surgery.

Rubaszek, M. and Rubio, M., 2019. Does the rental housing market stabilize the economy? A

micro and macro perspective. Empirical Economics, pp.1-25

Tan, C. T. and et.al., 2018. A Nonlinear ARDL Analysis on the Relation between Housing Price

and Interest Rate: The case of Malaysia. Journal of Islamic, Social, Economics and

Development. 3(14). pp.109-121.

Tao, Q., 2019. Analysis of Commodity Housing Price Based on Partial Least Squares

Regression. Academic Journal of Computing & Information Science. 2(3).

1

Books and journals

Agnew, K. and Lyons, R. C., 2018. The impact of employment on housing prices: Detailed

evidence from FDI in Ireland. Regional Science and Urban Economics. 70. pp.174-189.

Ashraf, B.N., 2020. Stock markets’ reaction to COVID-19: cases or fatalities?. Research in

International Business and Finance, p.101249.

Bansal, H and et.al., 2018. Social Network Analytics for Contemporary Business Organizations.

IGI Global.

Bianchi, M.T., 2017. Discovering the role of innovation in contemporary business systems: an

assessment technique from the literature analysis. International Journal of Digital Culture

and Electronic Tourism. 2(1). pp.1-15.

Cheshire, P. and Hilber, C.A., 2020. What will crashing the economy do for the UK housing

market?. LSE COVID-19 Blog.

Davis, A and et.al., 2018. A Minimum Income Standard for the UK, 2008-2018: continuity and

change. York: Joseph Rowntree Foundation.

De, U.K. and Vupru, V., 2017. Location and neighbourhood conditions for housing choice and

its rental value. International Journal of Housing Markets and Analysis.

French, N., 2020. Property valuation in the UK: material uncertainty and COVID-19. Journal of

Property Investment & Finance.

Hogsden, J., 2018. The Contemporary Corporate Tax Strategy Environment. In Contemporary

Issues in Accounting (pp. 85-104). Palgrave Macmillan, Cham.

Mcdonnell, L. and Sikander, A., 2017. Skills and competencies for the contemporary human

resource practitioner: a synthesis of the academic, industry and employers'

perspectives. The Journal of Developing Areas. 51(1). pp.83-101.

Meen, G., Mihailov, A. and Wang, Y., 2016. Endogenous UK Housing Cycles and the Risk

Premium: Understanding the Next Housing Crisis (No. em-dp2016-02). Henley Business

School, Reading University

MEIYANI, E. and Putra, A.H.P.K., 2019. The relationship between islamic leadership on

employee engagement distribution in FMCG industry: Anthropology business review. The

Journal of Distribution Science. 17(5). pp.19-28.

Nicola, M. and et.al., 2020. The socio-economic implications of the coronavirus and COVID-19

pandemic: a review. International Journal of Surgery.

Rubaszek, M. and Rubio, M., 2019. Does the rental housing market stabilize the economy? A

micro and macro perspective. Empirical Economics, pp.1-25

Tan, C. T. and et.al., 2018. A Nonlinear ARDL Analysis on the Relation between Housing Price

and Interest Rate: The case of Malaysia. Journal of Islamic, Social, Economics and

Development. 3(14). pp.109-121.

Tao, Q., 2019. Analysis of Commodity Housing Price Based on Partial Least Squares

Regression. Academic Journal of Computing & Information Science. 2(3).

1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.