Assessment of Contemporary Financial Reporting for Pro Medicus Limited

VerifiedAdded on 2023/01/18

|13

|2200

|29

Report

AI Summary

This report critically examines the financial reporting practices of Pro Medicus Limited, focusing on its adherence to the conceptual framework for financial reporting. The analysis evaluates whether the company has met the measurement requirements of the framework, complied with both fundamental and enhancing qualitative characteristics, and provided information useful for various users, including investors and creditors. The report assesses whether users possess sufficient knowledge of accounting to understand the reports and whether Pro Medicus meets the requirements for general-purpose financial reporting. It uses data extracted from the company's annual report to support its conclusions and offers recommendations based on its findings, providing a comprehensive overview of the company's financial reporting quality and its alignment with accounting standards.

Running head: REPORT 0

CONTEMPORARY ISSUES IN ACCOUNTING

APRIL 16, 2019

STUDENT DETAILS:

CONTEMPORARY ISSUES IN ACCOUNTING

APRIL 16, 2019

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Introduction................................................................................................................................2

Background of company............................................................................................................2

Measurement requirements of the conceptual framework.........................................................3

Complied with fundamental qualitative characteristics.............................................................5

Complied with enhancing qualitative characteristics.................................................................6

Use of the financial reports for the users...................................................................................7

Requirements by the users.........................................................................................................8

Requirements for general purpose financial reporting...............................................................9

Conclusion and recommendations...........................................................................................10

References................................................................................................................................11

Contents

Introduction................................................................................................................................2

Background of company............................................................................................................2

Measurement requirements of the conceptual framework.........................................................3

Complied with fundamental qualitative characteristics.............................................................5

Complied with enhancing qualitative characteristics.................................................................6

Use of the financial reports for the users...................................................................................7

Requirements by the users.........................................................................................................8

Requirements for general purpose financial reporting...............................................................9

Conclusion and recommendations...........................................................................................10

References................................................................................................................................11

REPORT 2

Introduction

In present world, accounting is implemented in numerous areas such as own finance and

finance related to business. In these two aspects, some issues are biased and immoral

deviating from ideal and impartial features of accounting procedure. Theses contemporary

issues normally apparent in social aspects, national aspect, and accounting principle having

political nature (Lewandowski, 2016). The contemporary issues introduce the latest problems

facing by the finance and accounting professional. In the following parts, the newest issues,

which influence on the contemporary approaches in the practice and accounting, are

discussed and critically examined. This report states the measurement requirements of

conceptual framework, adoption of the enhancing qualitative characteristics, adoption of the

fundamental qualitative characteristics, use of financial reporting by the users and

requirements of general purpose financial statements (GPFSs).

Background of company

Pro Medicus Limited manufactures the assimilated software application for healthcare sector.

The major works of the corporation are to provide services to the clinics and hospitals and

make supply of the products related to healthcare. It also provides the services to Australian

organisations related to the health and diagnostic centres in North America, Europe and

Australia. The product and service of company involve the Visage 7.0 and Radiology

Information System. The Radiology Information Systems of company offer the software

related to medical for the practice management; teaching, application and service of experts;

after trade supports and service products; Promedicus.net protected mail, and digital

radiology incorporation goods. In the addition of this, the Visage 7.0 provides the software

related to medical; PACS or digital images software; teaching, application and expert service,

Introduction

In present world, accounting is implemented in numerous areas such as own finance and

finance related to business. In these two aspects, some issues are biased and immoral

deviating from ideal and impartial features of accounting procedure. Theses contemporary

issues normally apparent in social aspects, national aspect, and accounting principle having

political nature (Lewandowski, 2016). The contemporary issues introduce the latest problems

facing by the finance and accounting professional. In the following parts, the newest issues,

which influence on the contemporary approaches in the practice and accounting, are

discussed and critically examined. This report states the measurement requirements of

conceptual framework, adoption of the enhancing qualitative characteristics, adoption of the

fundamental qualitative characteristics, use of financial reporting by the users and

requirements of general purpose financial statements (GPFSs).

Background of company

Pro Medicus Limited manufactures the assimilated software application for healthcare sector.

The major works of the corporation are to provide services to the clinics and hospitals and

make supply of the products related to healthcare. It also provides the services to Australian

organisations related to the health and diagnostic centres in North America, Europe and

Australia. The product and service of company involve the Visage 7.0 and Radiology

Information System. The Radiology Information Systems of company offer the software

related to medical for the practice management; teaching, application and service of experts;

after trade supports and service products; Promedicus.net protected mail, and digital

radiology incorporation goods. In the addition of this, the Visage 7.0 provides the software

related to medical; PACS or digital images software; teaching, application and expert service,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

and support goods. PPME IP Australia Pty Ltd, Romed (USA) Pty Ltd, and Visage Imaging

Inc. are the subsidiaries of Pro Medicus Limited.

Measurement requirements of the conceptual framework

The clear system of interconnected purposes and basics that is predictable and anticipated to

lead to reliable standards and that recommends a scope, functions and restrictions of financial

statements and financial accounting. The conceptual framework renders the recommendation

or the instruction so they may be regarded as accounting’s normative theories. This attempts

to render the accounting’s structured ‘theory. The Conceptual Framework is useful in

providing the general purpose financial statements (GPFS) and not specific purpose financial

statement. In AISB framework, there are five components of financial reporting, such as

liabilities, assets, expenses, income and equity. The company follows significant accounting

policies to form the basis for valuation of assets, liabilities, income, expenses and equity. It

can be observed from the annual report of company-

and support goods. PPME IP Australia Pty Ltd, Romed (USA) Pty Ltd, and Visage Imaging

Inc. are the subsidiaries of Pro Medicus Limited.

Measurement requirements of the conceptual framework

The clear system of interconnected purposes and basics that is predictable and anticipated to

lead to reliable standards and that recommends a scope, functions and restrictions of financial

statements and financial accounting. The conceptual framework renders the recommendation

or the instruction so they may be regarded as accounting’s normative theories. This attempts

to render the accounting’s structured ‘theory. The Conceptual Framework is useful in

providing the general purpose financial statements (GPFS) and not specific purpose financial

statement. In AISB framework, there are five components of financial reporting, such as

liabilities, assets, expenses, income and equity. The company follows significant accounting

policies to form the basis for valuation of assets, liabilities, income, expenses and equity. It

can be observed from the annual report of company-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

REPORT 5

Complied with fundamental qualitative characteristics

To make sure the financial data is helpful for the financial decisions making, it is

significantly required to consider the characteristics or merits that are required to possess by

financial information. The IASB Conceptual Framework identifies the fundamental

qualitative characteristics. The fundamental qualitative characteristics of financial reporting

data are typed as relevance and faithful representation. These are discussed as follows-

1. Relevance- According to this fundamental qualitative characteristics of financial

reporting information, it is required that data should be proper to the needs of a user

that is the case when the information influences the financial decision of users.

Something is proper in case where this affects the decision on the allocation of rare

means if this is able of creating the differences in the judgement. This may involving

reporting particularly related information, or data whose misstatements or errors may

influence the financial decision of users (Kelley and Knowles, 2016).

2. The faithful representation- the faithful representation means to the concept that

financial statement be produced that exactly state the conditions of business.

considering the annual report of Pro Medicus Limited, this is observed that financial

statements of the corporation render the relevant and faithful representation. The

entity faithfully represents the transactions and other event, states the underlying

matter of events, and prudently states the estimates and worries by the appropriate

disclosures (Kršeková and Pakšiová, 2015). For an example, the company has

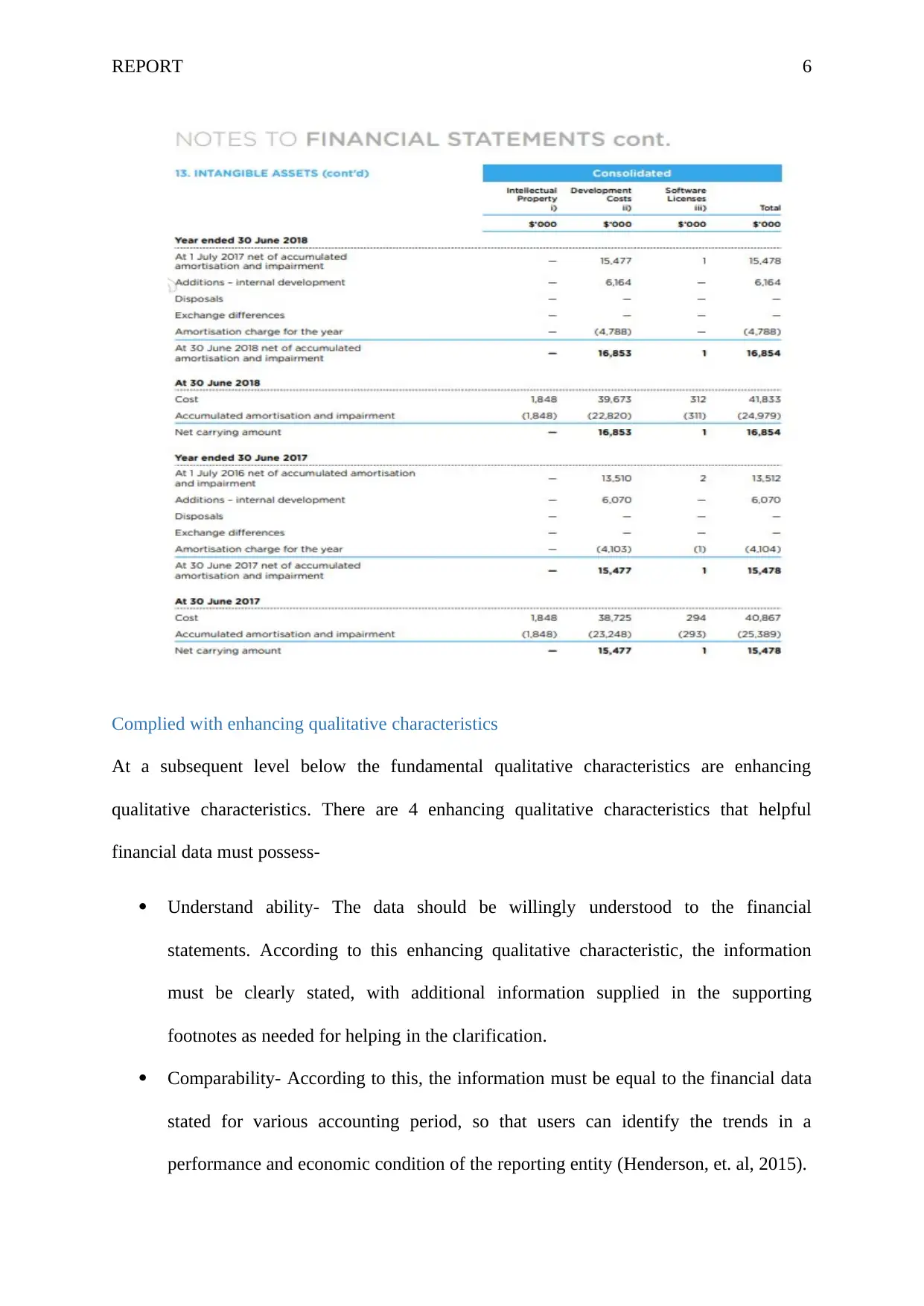

complied with characteristic ‘faithful representation’ in respect of intangible assets-

Complied with fundamental qualitative characteristics

To make sure the financial data is helpful for the financial decisions making, it is

significantly required to consider the characteristics or merits that are required to possess by

financial information. The IASB Conceptual Framework identifies the fundamental

qualitative characteristics. The fundamental qualitative characteristics of financial reporting

data are typed as relevance and faithful representation. These are discussed as follows-

1. Relevance- According to this fundamental qualitative characteristics of financial

reporting information, it is required that data should be proper to the needs of a user

that is the case when the information influences the financial decision of users.

Something is proper in case where this affects the decision on the allocation of rare

means if this is able of creating the differences in the judgement. This may involving

reporting particularly related information, or data whose misstatements or errors may

influence the financial decision of users (Kelley and Knowles, 2016).

2. The faithful representation- the faithful representation means to the concept that

financial statement be produced that exactly state the conditions of business.

considering the annual report of Pro Medicus Limited, this is observed that financial

statements of the corporation render the relevant and faithful representation. The

entity faithfully represents the transactions and other event, states the underlying

matter of events, and prudently states the estimates and worries by the appropriate

disclosures (Kršeková and Pakšiová, 2015). For an example, the company has

complied with characteristic ‘faithful representation’ in respect of intangible assets-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

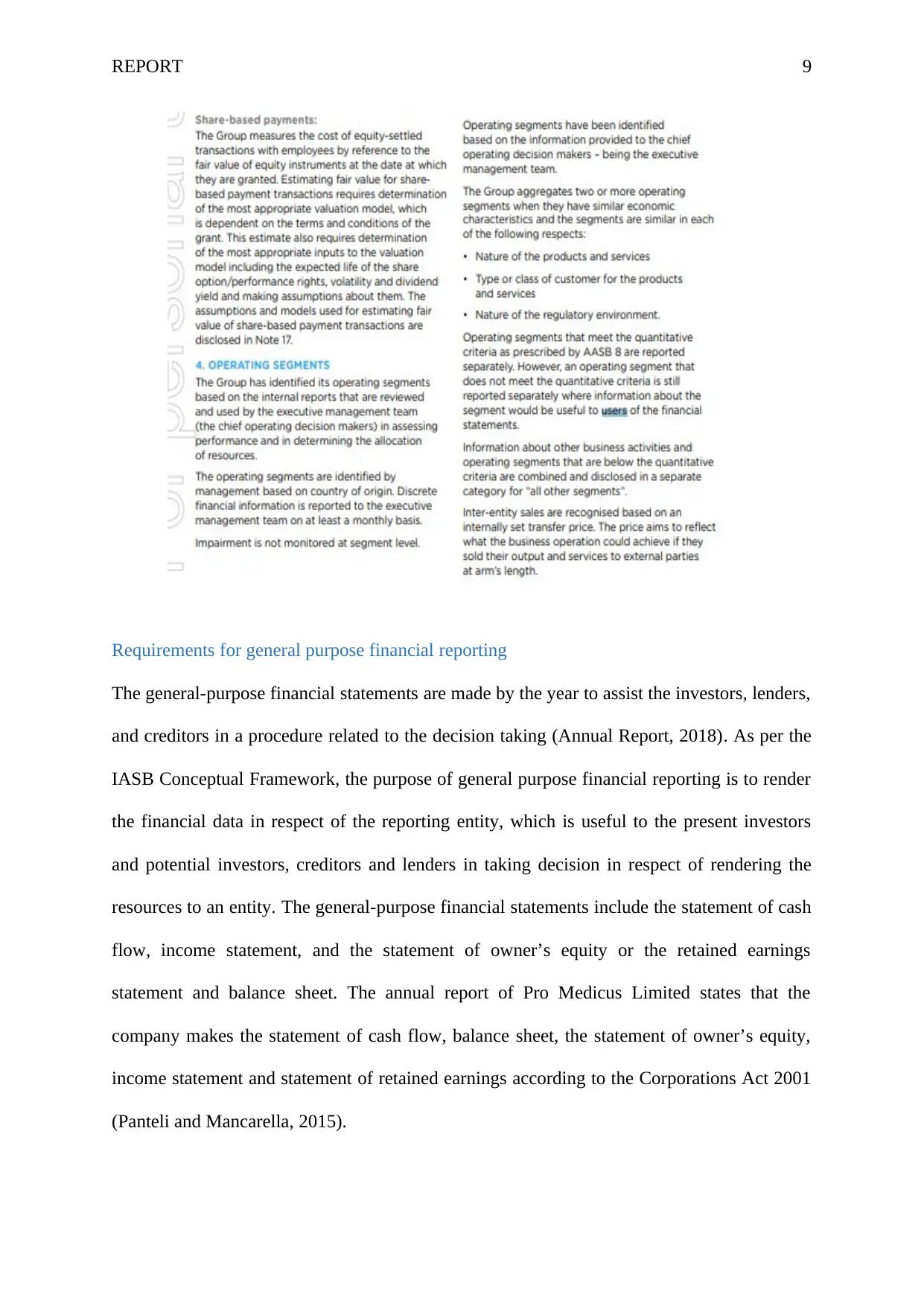

Complied with enhancing qualitative characteristics

At a subsequent level below the fundamental qualitative characteristics are enhancing

qualitative characteristics. There are 4 enhancing qualitative characteristics that helpful

financial data must possess-

Understand ability- The data should be willingly understood to the financial

statements. According to this enhancing qualitative characteristic, the information

must be clearly stated, with additional information supplied in the supporting

footnotes as needed for helping in the clarification.

Comparability- According to this, the information must be equal to the financial data

stated for various accounting period, so that users can identify the trends in a

performance and economic condition of the reporting entity (Henderson, et. al, 2015).

Complied with enhancing qualitative characteristics

At a subsequent level below the fundamental qualitative characteristics are enhancing

qualitative characteristics. There are 4 enhancing qualitative characteristics that helpful

financial data must possess-

Understand ability- The data should be willingly understood to the financial

statements. According to this enhancing qualitative characteristic, the information

must be clearly stated, with additional information supplied in the supporting

footnotes as needed for helping in the clarification.

Comparability- According to this, the information must be equal to the financial data

stated for various accounting period, so that users can identify the trends in a

performance and economic condition of the reporting entity (Henderson, et. al, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

Timeliness- The timeliness of accounting data refers to the requirements of

information to utilise quickly proper for them to make actions. The information

become obsolete and unreasonable in a matter while this is not reported timely.

Verifiability- the Company’s accounting is verifiable while it is reproducible, so that,

given the same data and expectation, the independent accountant can make same

result the company did. The verifiability is useful in helping that the information

faithfully states the economic portents it purports to state. In other words, it is

observed that the various experts and viewers may get consents that the particular

representation is a faithful representation.

Therefore, it is stated by annual report of Pro Medicus Limited that the company

represents the financial data in a way that the people with relevant knowledge of

finance and businesses, and willingness to study information, should be able to

understand this. Thus, the company has complied with enhancing qualitative

characteristics (Gummer and Mandinach, 2015).

Use of the financial reports for the users

The financial reporting is helpful for the users of financial statements like the investors,

creditors, lenders and potential investors (Christensen, et. al, 2016). The users may utilise the

financial statements to take decisions. The annual report of company states that the depositors

and shareholders of an entity require the financial data to take relevant decision related to the

investment and economic decisions. Furthermore, the lenders of funding for the instance

financial institutions and banks are interested to have the knowledge of capacity of entity to

make the payment of liabilities on the maturity. Furthermore, the creditors require the

financial data to know the capacity to pay obligations by a corporation on maturity. In this

way, various investors, creditors and lenders may not need reporting entity to render data to

them in a direct manner and should depended on the general purpose financial reports for

Timeliness- The timeliness of accounting data refers to the requirements of

information to utilise quickly proper for them to make actions. The information

become obsolete and unreasonable in a matter while this is not reported timely.

Verifiability- the Company’s accounting is verifiable while it is reproducible, so that,

given the same data and expectation, the independent accountant can make same

result the company did. The verifiability is useful in helping that the information

faithfully states the economic portents it purports to state. In other words, it is

observed that the various experts and viewers may get consents that the particular

representation is a faithful representation.

Therefore, it is stated by annual report of Pro Medicus Limited that the company

represents the financial data in a way that the people with relevant knowledge of

finance and businesses, and willingness to study information, should be able to

understand this. Thus, the company has complied with enhancing qualitative

characteristics (Gummer and Mandinach, 2015).

Use of the financial reports for the users

The financial reporting is helpful for the users of financial statements like the investors,

creditors, lenders and potential investors (Christensen, et. al, 2016). The users may utilise the

financial statements to take decisions. The annual report of company states that the depositors

and shareholders of an entity require the financial data to take relevant decision related to the

investment and economic decisions. Furthermore, the lenders of funding for the instance

financial institutions and banks are interested to have the knowledge of capacity of entity to

make the payment of liabilities on the maturity. Furthermore, the creditors require the

financial data to know the capacity to pay obligations by a corporation on maturity. In this

way, various investors, creditors and lenders may not need reporting entity to render data to

them in a direct manner and should depended on the general purpose financial reports for

REPORT 8

financial data they require. Accordingly, they are key users to whom general-purpose

financial reports are directed (Sampaio and González, 2017).

Requirements by the users

It is said by conceptual framework that users require only the basic knowledge of

accounting. However, they are required more than this. It is normally accepted that the user is

anticipated to get certain skills in the financial accounting. Besides this, the financial reports

are made for the user who has proper understanding of the business and financial functions

and who assesses the data properly and thoroughly. At time, even knowledgeable, well-

versed and hardworking user can require to look for the help of the consultant to get the

knowledge of data in respect of the difficult financial phenomena. The user of entity is

required to have knowledge of the International Accounting Standards, accounting standards

of Australia and the international financial reporting statement from the company’s financial

statements. Therefore, the users may deal the accounting transaction according to the

Australian accounting standards (Geisker and Tallis, 2018).

financial data they require. Accordingly, they are key users to whom general-purpose

financial reports are directed (Sampaio and González, 2017).

Requirements by the users

It is said by conceptual framework that users require only the basic knowledge of

accounting. However, they are required more than this. It is normally accepted that the user is

anticipated to get certain skills in the financial accounting. Besides this, the financial reports

are made for the user who has proper understanding of the business and financial functions

and who assesses the data properly and thoroughly. At time, even knowledgeable, well-

versed and hardworking user can require to look for the help of the consultant to get the

knowledge of data in respect of the difficult financial phenomena. The user of entity is

required to have knowledge of the International Accounting Standards, accounting standards

of Australia and the international financial reporting statement from the company’s financial

statements. Therefore, the users may deal the accounting transaction according to the

Australian accounting standards (Geisker and Tallis, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

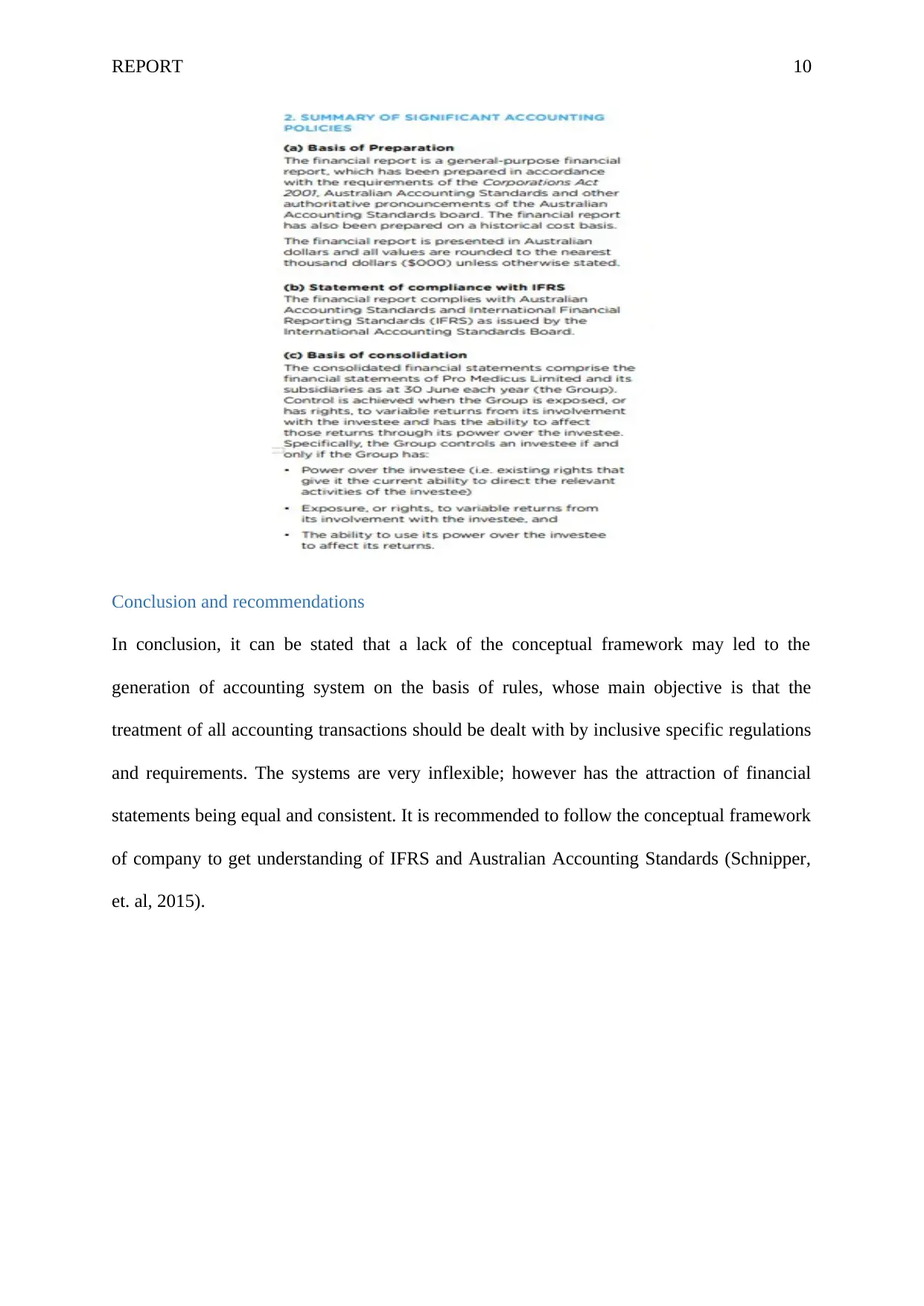

Requirements for general purpose financial reporting

The general-purpose financial statements are made by the year to assist the investors, lenders,

and creditors in a procedure related to the decision taking (Annual Report, 2018). As per the

IASB Conceptual Framework, the purpose of general purpose financial reporting is to render

the financial data in respect of the reporting entity, which is useful to the present investors

and potential investors, creditors and lenders in taking decision in respect of rendering the

resources to an entity. The general-purpose financial statements include the statement of cash

flow, income statement, and the statement of owner’s equity or the retained earnings

statement and balance sheet. The annual report of Pro Medicus Limited states that the

company makes the statement of cash flow, balance sheet, the statement of owner’s equity,

income statement and statement of retained earnings according to the Corporations Act 2001

(Panteli and Mancarella, 2015).

Requirements for general purpose financial reporting

The general-purpose financial statements are made by the year to assist the investors, lenders,

and creditors in a procedure related to the decision taking (Annual Report, 2018). As per the

IASB Conceptual Framework, the purpose of general purpose financial reporting is to render

the financial data in respect of the reporting entity, which is useful to the present investors

and potential investors, creditors and lenders in taking decision in respect of rendering the

resources to an entity. The general-purpose financial statements include the statement of cash

flow, income statement, and the statement of owner’s equity or the retained earnings

statement and balance sheet. The annual report of Pro Medicus Limited states that the

company makes the statement of cash flow, balance sheet, the statement of owner’s equity,

income statement and statement of retained earnings according to the Corporations Act 2001

(Panteli and Mancarella, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

Conclusion and recommendations

In conclusion, it can be stated that a lack of the conceptual framework may led to the

generation of accounting system on the basis of rules, whose main objective is that the

treatment of all accounting transactions should be dealt with by inclusive specific regulations

and requirements. The systems are very inflexible; however has the attraction of financial

statements being equal and consistent. It is recommended to follow the conceptual framework

of company to get understanding of IFRS and Australian Accounting Standards (Schnipper,

et. al, 2015).

Conclusion and recommendations

In conclusion, it can be stated that a lack of the conceptual framework may led to the

generation of accounting system on the basis of rules, whose main objective is that the

treatment of all accounting transactions should be dealt with by inclusive specific regulations

and requirements. The systems are very inflexible; however has the attraction of financial

statements being equal and consistent. It is recommended to follow the conceptual framework

of company to get understanding of IFRS and Australian Accounting Standards (Schnipper,

et. al, 2015).

REPORT 11

References

Annual Report (2018) Pro Medicus .[Online] Available at: < http://www.promed.com.au/wp-

content/uploads/2019/03/PME-Annual-Report-2018.pdf> [Accessed 16/04/2019]

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R. (2016) Accounting

information in financial contracting: The incomplete contract theory perspective. Journal of

accounting research, 54(2), pp.397-435.

Geisker, J. and Tallis, J. (2018) Litigation funding in Australia: A year of review and

change?. LSJ: Law Society of NSW Journal, (46), p.81.

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B. (2015) Issues in financial

accounting. Pearson Higher Education AU.

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance

and risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-

66.

References

Annual Report (2018) Pro Medicus .[Online] Available at: < http://www.promed.com.au/wp-

content/uploads/2019/03/PME-Annual-Report-2018.pdf> [Accessed 16/04/2019]

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R. (2016) Accounting

information in financial contracting: The incomplete contract theory perspective. Journal of

accounting research, 54(2), pp.397-435.

Geisker, J. and Tallis, J. (2018) Litigation funding in Australia: A year of review and

change?. LSJ: Law Society of NSW Journal, (46), p.81.

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B. (2015) Issues in financial

accounting. Pearson Higher Education AU.

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance

and risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-

66.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.